In response to recent calls for increased scholarly attention to time in sustainability accounting, the paper explores how time, understood as temporal viewpoints, is mobilised in accounts of biodiversity in order to uncover the roles of time in framing biodiversity performance. We introduce a ‘time-aware stance' to advance research on emancipatory extinction accounting and address temporal complexities in sustainability reporting.

A qualitative case study of World Wide Fund for Nature (WWF) Sweden's annual reports (2021–2023) and social media posts (2023) was conducted. WWF-SE's longstanding work with biodiversity makes for an instrumental case to highlight the roles of time. The analysis is organised around the idea of accounting as a process of framing, combined with Chakhovich's concept of time rationalities.

Five roles of time are identified: time as trend, urgency, expectation, snapshot and journey, each reflecting a viewpoint from either the past or the present. We also propose a sixth role: time as imagination, building on a viewpoint from the future. The opportunities and shortcomings of each role are discussed, highlighting the value of a time-aware stance in the framing of biodiversity performance.

The study offers practical guidance and theoretical insights on how to mobilise time in emancipatory extinction accounting. The time-aware stance can act as a lens to help organisations reconcile urgency with perseverance to guide actionable and cohesive sustainability accounts.

1. Introduction

Biodiversity is increasingly recognised as a key concern for policymakers and firms alike, as seen in the 2030 Agenda for Sustainable Development and the Kunming–Montreal Global Biodiversity Framework, as well as in its inclusion in reporting frameworks such as the Global Reporting Initiative (GRI), the European Sustainability Reporting Standards (ESRS), and Taskforce for Nature-related Financial Disclosures (TNFD). Biodiversity is “the variability among living organisms including terrestrial, marine and other aquatic ecosystems and the ecological complexes of which they are a part” (WWF, 2024, p. 19) or, more succinctly, “the heartbeat of our living planet” (ibid.). The World Economic Forum (2020) estimates that more than half of the world's GDP is highly or moderately dependent on nature and nature's services, such as medical substances, pollination and purification of soil, water and air. Due to climate change, many species and habitats are now facing irreversible biodiversity loss (Freeman and Groom, 2013; Schaltegger et al., 2023), which makes biodiversity one of the principal challenges for human and planetary health (Jones and Solomon, 2013). As such, biodiversity can be viewed as the ticking clock, necessitating a time-aware stance to grapple with both the urgency of biodiversity loss and the need to manage biodiversity activities and outcomes consistently over the long term.

Time has always been inherent to the understanding of sustainability in the organisational context (Bansal and DesJardine, 2014; Slawinski and Bansal, 2012), primarily seen in distinctions between the shorter and the longer term. A prevalent idea in the Brundtland definition of sustainability, as well as the more recent Kunming–Montreal Global Biodiversity Framework, is the importance of balancing present and future needs in pursuit of intergenerational equity. In an organisational context, this is typically understood as the need to incorporate long-term thinking and accountability to mitigate the risk of prioritising short-term, firm-centric or financial gains (Dyllick and Muff, 2016; Freeman and Groom, 2013; Hahn et al., 2015). More recently, scholars have challenged long-termism as the de facto temporal perspective of organisations' sustainability concerns, instead putting the spotlight on the short-term urgency of these matters (Tregidga and Laine, 2022). However, beyond studies exploring the role of time in discounting the current value of biodiversity assets (e.g. Drupp et al., 2024; Freeman and Groom, 2013), prior work on biodiversity accounting takes a rather tangential approach to time, despite recent studies arguing that time should be more visible in accounts of sustainability (Tregidga and Laine, 2022). Research on corporate biodiversity reporting has shown that organisations tend to describe biodiversity solely as a long-term project (Boiral, 2016; Roberts et al., 2023) that may incur costs and liabilities in the future (Rimmel and Jonäll, 2013), or that they struggle to combine short-term and long-term values in day-to-day accounting practice (Weir, 2019). This echoes the sustainability accounting literature showing that companies often describe their sustainability work as an ongoing journey of incremental improvements (Chakhovich and Virtanen, 2023; Milne et al., 2006). In line with Tregidga and Laine (2022), it seems evident that sustainability accounting could benefit from engaging more deeply with the temporal dimensions of biodiversity to increase the understanding of what is at stake across multiple time horizons. Also, as recent studies on performance management (Chakhovich, 2013, 2019) suggest, it is important to consider not only the length of the time horizon but also the viewpoint of the account-giver. A temporal viewpoint refers to an account-giver's orientation (from the past, present or future) towards events and affects how performance is assessed.

Biodiversity is an excellent case for developing the limited theorising of time in sustainability accounting, for several reasons. First, biodiversity necessarily operates on an infinite timescale due to the irreversible nature of biodiversity loss. Efforts to protect biodiversity are therefore often complex matters oriented towards long-term goals (Sobkowiak et al., 2020; WWF, 2024), which appear rather ill-suited to the quarterly and annual reporting practices that characterise conventional accounting (Chambers, 1989; Johnson and Kaplan, 1987). At the same time, extinction is a real and ongoing threat to many species (Jones and Solomon, 2013; WWF, 2024). Biodiversity thus embodies the critical sustainability challenge of managing the paradox of multiple time horizons (Slawinski and Bansal, 2012; Tregidga and Laine, 2022; Weir, 2019). Second, current research largely revolves around describing the limited or superficial state of corporate biodiversity reporting (Adler et al., 2018; Carvalho et al., 2023; Hassan et al., 2022; Lamont et al., 2023; Maroun and Ecim, 2024) and, to a lesser extent, the challenge of NGOs' and public sector organisations' biodiversity accounting (Cuckston, 2022; Sobkowiak et al., 2020; Weir, 2019). This stream of literature has not yet comprehensively explored the underlying complexities that affect biodiversity accounting, including temporal viewpoints. Rather than critiquing current shortcomings, which may or may not lead to improved sustainability (Bigoni and Mohammed, 2023), we take an emancipatory perspective and propose a time-aware stance to highlight the role of time as a horizon that actively shapes the framing (Callon and Muniesa, 2005; Cuckston, 2022) of biodiversity performance. In doing so, we contribute to the emancipatory approach to biodiversity accounting, a stream of literature that has emerged in recent years with the intention to offer guidance on how to improve biodiversity reporting and “encourage changes in mindsets” (Maroun and Atkins, 2018, p. 107).

Against this backdrop, the aim of the paper is to explore how time, understood as temporal viewpoints, is mobilised in accounts of biodiversity in order to uncover the roles of time in framing biodiversity performance. This allows us to discuss opportunities of a time-aware stance for the emancipatory approach to biodiversity accounting.

Because firms tend to report sparingly on biodiversity, as outlined above, we opted to focus on The World Wide Fund for Nature (WWF), an organisation dedicated to biodiversity, as a case of a “rich [site] for research into how accounting plays a role in achieving biodiversity conservation” (Cuckston, 2018, p. 221). In our use of a success case, we also follow Maroun and Atkins (2018), who use examples of emancipatory biodiversity reporting to guide practice. WWF are at the forefront of biodiversity conservation and an advocate for biodiversity globally, as evidenced by their frequent mention as a biodiversity partner of firms (Adler et al., 2017). The literature on biodiversity accounting relies heavily on studies of the corporate context and would benefit from also considering the role of actors outside the for-profit domain (Atkins and Maroun, 2018; Sobkowiak et al., 2020). We thus extend prior work on biodiversity accounting by investigating how time is mobilised in WWF Sweden's annual reports and other official communication channels. Our analysis is informed by the idea of accounting as a process of framing (Callon and Muniesa, 2005), which we combine with the concept of time rationalities (Chakhovich, 2013, 2019), to shed light on how an organisation's temporal viewpoint shapes accounts of biodiversity performance. Our analysis of WWF Sweden revealed five roles of time in framing biodiversity performance: time as trend, urgency, expectation, snapshot and journey, all of which reflect a viewpoint from either the past or the present. The lack of viewpoints from the future led us to suggest one additional role absent from the empirical material: time as imagination. Each role offers opportunities and risks for emancipatory approaches to biodiversity accounting. By discussing these in relation to prior literature, we demonstrate the value of a time-aware stance as a way to reflexively engage with temporal viewpoints when considering biodiversity performance.

The rest of the paper is organised as follows. Section 2 introduces prior work on biodiversity reporting and accounting, including the ideas and objectives of the emancipatory stream of accounting literature, to which we address the results of the paper. Section 3 outlines the analytical lens used to interpret the empirics. Section 4 outlines the research methodology, while Section 5 introduces the empirical findings regarding WWF-SE's mobilisation of time in their accounts of biodiversity performance. Section 6 is the discussion, where we develop a framework of the roles of time in biodiversity accounting. Section 7 concludes the paper.

2. Accounting for biodiversity

Biodiversity has received limited attention in the literature on sustainability accounting, with the number of studies increasing only in recent years (Blanco-Zaitegi et al., 2022; Maione et al., 2024; Roberts et al., 2021). Instead, topics such as climate change and greenhouse gas emissions have received significantly more attention, both from practitioners and the research community (Carvalho et al., 2023; He et al., 2022; Velte et al., 2020). While there is a body of literature exploring how to make biodiversity calculable by discussing natural capital balance sheets, offsetting and externality accounting (e.g. Bebbington and Rubin, 2022; Freeman and Groom, 2013; Siddiqui, 2013; Sullivan and Hannis, 2017), much of the research has revolved around the content and scope of biodiversity disclosures from a reporting perspective. In line with the emphasis on living organisms and their ecosystems as the basis of biodiversity (WWF, 2024), an organisation's biodiversity performance is then typically framed in terms of individuals of a certain species or the size or number of habitats protected (Cuckston, 2022; Maroun and Atkins, 2018). In this context, an account of performance is a description, often qualitative, of an organisation's activities and outcomes related to protecting and restoring species and habitats. For example, studies have found a tendency to single out “flagship species” (Cuckston, 2022) and mammals and birds (Weir, 2019).

A significant stream in the literature highlights limitations of corporate biodiversity disclosures, consistent with criticisms against sustainability reporting more broadly (e.g. Cho et al., 2015; Milne et al., 2006). This includes observations that disclosures are vague, inconsistent and rife with impression management and legitimation strategies (Adler et al., 2018; Boiral, 2016; Hassan et al., 2020; Lamont et al., 2023; Maroun and Ecim, 2024; Rimmel and Jonäll, 2013). Examples include the use of vague descriptions, statements about compliance and boilerplate repetition of missions and results year after year (Zhao and Atkins, 2021); this contradicts recommendations to use specific and transparent accounts regarding biodiversity and conservation (Lamont et al., 2023; Maroun and Atkins, 2018).

Studies have also found that reporting rates are low and seem to increase slowly (Adler et al., 2018). Boiral (2016) found that biodiversity represented 5% of mining companies' sustainability reports while Maroun and Ecim (2024) found an average of 322 words in the biodiversity disclosures of UK listed companies, which barely increased between 2018 and 2022. Adler et al. (2018) similarly concluded that only 10% of Global Fortune companies had any substantial biodiversity reporting. This tendency was confirmed in another study of Global Fortune companies (Hassan et al., 2022) and in a study of firms included in the Bloomberg index, where Carvalho et al. (2023, p. 2603) observed an increase to 29% of companies disclosing “any initiatives to ensure the protection of biodiversity” between 2004 and 2018. Prior studies identify significant variation in the type of biodiversity information included as well as a preference for some topics over others; more popular topics include afforestation activities and biodiversity assessments (Adler et al., 2018). In contrast, few firms report extensively on their impact on biodiversity loss, their offsets and targets, and biodiversity-related business risks (Adler et al., 2018; Maroun and Ecim, 2024).

Given these criticisms, several studies have sought to explain the current shortcomings of biodiversity reporting. A common explanation is that biodiversity is not easily measured nor reported at the organisational level, as many challenges and concerns require systemic change (Adler et al., 2018; Schaltegger et al., 2023). This may also mean that companies with indirect impacts on biodiversity struggle to disclose relevant information. Studies identify reporting readiness, partnerships with NGOs and industry sensitivity as success factors (Adler et al., 2018; Carvalho et al., 2023; Hassan et al., 2020; Roberts et al., 2023), stressing that the absence of these factors may limit the expansion of biodiversity reporting. Based on these observations, the fragmented state of biodiversity reporting is a concern because it limits clarity and comparability of disclosures, both across organisations and over time (Cuckston, 2022).

In contrast to most of the studies discussed thus far, which focus on accounting as a matter of disclosure, both Sobkowiak et al. (2020) and Weir (2019) illuminate the socially constructed nature of biodiversity performance. In a study of how the British government monitors progress on SDG-15, Life on Land, Sobkowiak et al. (2020) found that accounts of biodiversity were established gradually as a bottom-up, iterative process combining historical data with input from politicians, experts and external organisations, and that data availability influenced which indicators were used and thus how performance could be constructed. Weir (2019) similarly found that local conditions in UK councils, including a need to involve multiple actors, increased the complexity of biodiversity data collection, especially species and habitat monitoring and risk analysis. Initiatives to protect biodiversity would often clash with financial imperatives, leading councils to prioritise efforts based on the cost-efficiency of short-term conservation activities over long-term biodiversity gains. Taken together, these studies draw attention to how biodiversity accounts are shaped through data availability and negotiations with stakeholders. The resulting biodiversity disclosure depends on the setting in which the organisation operates and how goals, activities and performance are understood in that setting, for example by recognising complexity while reporting on outcomes for multiple actors and time horizons. Along these lines, a number of works have begun to explore how to address the shortcomings of biodiversity accounting by adopting an emancipatory approach.

A central tenet of the emancipatory approach is to unpack and reframe the term biodiversity, as in current usage it often serves as a “catch all phrase which means very little without an appreciation of specific species and their value to the ecosystem as a whole” (Maroun and Atkins, 2018, p. 111). Indeed, Jones and Solomon (2013) argue that the term “biodiversity” may obfuscate what is at stake and instead introduce “extinction accounting” as an alternative to “convey the urgency, the critical and crucial need for such accountability” (Jones and Solomon, 2013, p. 683), highlighting that biodiversity activities should be directed at preventing the extinction of species. However, Atkins and Maroun (2018) caution that “merely cataloguing, counting and recording species and extinctions per se is not an emancipatory approach and will not lead to extinction prevention.” (p. 759). Rather, concrete frameworks and methodologies are needed. Inspired by extant reporting frameworks, Maroun and Atkins (see also Atkins and Maroun, 2018) propose a multi-step accounting process which begins with describing the context, the areas where the company operates and how operations affect these areas. This should be followed by accounts of efforts to prevent extinction and rebuild habitats and the motivations for these. Next, the results of the efforts should be described and communicated externally. While the first steps could be described qualitatively, the latter steps should ideally include quantitative indicators (Atkins and Maroun, 2018), for example assessments of results compared to goals and discussions of acceptable levels of performance.

Overall, the emancipatory approach to biodiversity accounting appears to be a promising avenue for exploring how time is mobilised in accounts of biodiversity. The emancipatory studies, by unpacking the steps and processes involved in meaningfully accounting for extinction performance, offer a basis for exploring the role of time in greater depth. For example, some of these studies suggest that accounting, while still tied to the present, should be more forward-looking and proactive by including targets, descriptions of risks and plans for how future negative events may be prevented (Atkins and Maroun, 2018; Maroun and Atkins, 2018). We intend to advance this line of thinking, and thereby contribute to this expanding body of literature, by exploring the presence of temporal viewpoints in accounts of biodiversity and the implications for the role of time in framing biodiversity performance.

3. Calculation and time

Accounting can be described as an act of “framing” (Cuckston, 2022), particularly when it comes to non-financial performance as it is often less formalised than financial performance. The framing process is carried across three steps, described below.

The first step of framing involves defining the performance objects and bringing them into a single space, referred to as the calculative space (Callon and Muniesa, 2005; Cuckston, 2022). Defining the calculative space is often more complicated in non-profits whose aims are broader than those of a typical company. Cuckston (2022) therefore suggests identifying the problems that the non-profit aims to address and use them as the basis for assessing the level of performance against these goals. In the biodiversity context, firms may wish to account for specific species, particularly those facing extinction and thus the immediate risk of biodiversity loss (Adler et al., 2018; Roberts et al., 2023).

In the second step, other entities are brought into the calculative space and linked to the performance objects to enable comparison and joint measurement in order to determine performance (Callon and Muniesa, 2005). Linking can be achieved by showing how the problems outlined in the first step are addressed, for example, by describing the organisation's key activities and how they lead to the intended outcomes (Cuckston, 2022).

Finally, a result is extracted by attributing outcomes to the activities performed and showing how these make a difference to the performance objects (Cuckston, 2022). This amounts to an account of performance. It should be noted that the medium of the extraction could be almost anything, such as a list, a report, a sum or an evaluation (Cuckston, 2022; Sobkowiak et al., 2020), as long as it is sufficiently concrete to account for performance both within and outside the calculative space (Callon and Muniesa, 2005). As much accounting research has shown, numbers are particularly mobile (Robson, 1992) and are therefore suited to extract performance, but in the context of biodiversity it is common to find more qualitative accounts as well (Cuckston, 2022).

The three steps of framing allow biodiversity performance to be defined and measured, which resonates with the emancipatory approach to unpack and contextualise biodiversity accounts (Atkins and Maroun, 2018; Maroun and Atkins, 2018). However, performance, particularly when concerned with multiple and competing time horizons such as in the biodiversity case, must also be understood as temporal since account-givers are oriented in time when relating to performance (Chakhovich, 2019). In this paper, we operationalise this perspective by combining the idea of framing (Callon and Muniesa, 2005; Cuckston, 2022) with the notion of time rationalities (Chakhovich, 2013, 2019) as a sensitising device (Blumer, 1954) to guide our analysis.

Chakhovich (2013, 2019) developed the concept of time rationalities in the performance management context, using it as an alternative to the linear-quantitative view of time, which looks from the present towards either a short-term or long-term future to assess performance (Chakhovich et al., 2010; Chakhovich, 2013). Rather than focusing on the length of the time horizon, time rationalities explain how the base time from which the account-giver is looking (past, present or future) informs the understanding of performance. That is, the basis on which account-givers assess performance will change depending on which temporal direction they are facing, i.e. their temporal viewpoint. Performance objects, defined as the entities within the calculative space, are thus reliant on, and, in some cases, constrained by, time rationalities. Chakhovich (2013, 2019) identifies the following time rationalities:

Past-based rationality is looking from the viewpoint of the past. Past events, for example an index of historical data, determine the measures and experiences against which to assess present or future performance. In this sense, present and future performance is tethered to actions and outcomes in the past. This ensures continuity and consistency over time by incorporating history and tradition as a basis for assessing current or future outcomes (Chakhovich, 2019).

Present-based rationality is looking from the present (the most common view). Present actions are the basis of performance in the sense that “efficiency and effectiveness in the present are rationalised to lead to success in the future” (Chakhovich, 2019, p. 462). Making the link between actions in the present and the expected outcomes of these in the future can therefore require a leap of faith. This time rationality, often reflecting a sense of inertia, can even involve a conscious decision to distance actions in the present from both the past and the future in cases where those perspectives are not viewed as fruitful to assess performance (Chakhovich, 2019).

Future-based rationality is to look from an imagined future towards the past or present. That is, the future is defined first, and the present derived from that future state (Chakhovich, 2013). This requires a “leap into the unknown” in the sense of “freeing oneself from the chains of the present” (Chakhovich, 2013, p. 147). In this sense, future-based rationality is rather different from the past-based and present-based rationalities, which are anchored in something material in the organisation's past history or present context.

Time rationalities evidently play a role in how performance is framed, as all account-givers are necessarily oriented in time when considering organisational activities and outcomes (that is, they have a temporal viewpoint). However, the implications of time rationalities for the framing of performance have not been explored in prior work. In our application, we will use the steps of framing to identify how biodiversity performance is shaped in WWF Sweden's reports and apply the concept of time rationalities to identify how temporal viewpoints shape these accounts.

4. Research method

Most prior research has approached biodiversity accounting from a quantitative perspective, taking its point of departure in word counts, reading ease and other predefined items (e.g. Adler et al., 2018; Carvalho et al., 2023; Hassan et al., 2020; Hassan et al., 2022; Rimmel and Jonäll, 2013; Roberts et al., 2023). With the limited focus on time in the literature, we wanted to get close to accounts of biodiversity to see “what is going on” (Silverman, 2021) and therefore chose a qualitative approach. We opted for a single case, WWF Sweden, as the nascency of the topic calls for unveiling rich details rather than providing explanations based on comparison (Creswell and Poth, 2016). Our chosen case is instrumental (Stake, 1995), i.e. particularly illuminating for the purpose of exploring how time is mobilised in accounts of biodiversity. While companies can arguably have a significant negative impact on biodiversity, their reporting is still limited (Adler et al., 2018; Boiral, 2016; Roberts et al., 2023), whereas WWF have over fifty years of experience in biodiversity accounting. For our purpose, we therefore believed that more insight could be gained by studying an expert actor in the field (Maroun and Atkins, 2018). As Cuckston's (2022) analysis of WWF-UK shows, their reports offer detailed insight into how biodiversity performance is framed. As such, our case is intended to offer rich insights on a novel topic rather than a representative case of all possible practices.

WWF Sweden (henceforth WWF-SE), founded in 1971, is the Swedish branch of the global WWF network (henceforth WWF). The primary focus in Sweden and globally is to preserve biodiversity and a sustainable use of natural resources through funding of biodiversity projects, advocacy and partnerships with companies (WWF-SE, 2023). WWF-SE's accounts of biodiversity span several channels, including advertisements, their website, annual reports and social media. We opted to include the annual report, the main channel through which organisations account for performance, as well as Facebook, which has emerged as an important arena for non-profit organisations in recent years (Alexander et al., 2023; Bellucci and Manetti, 2017). Initially, we planned to include annual reports from the past five years in line with Cuckston (2022) but our initial analysis revealed significant differences, with the 2019 and 2020 reports offering less detail on key activities and outcomes. Therefore, we included the annual reports from 2021, 2022 and 2023, and WWF-SE's Facebook posts published in 2023 as our empirical material. In both instances, we focused on statements that we identified as containing an account of biodiversity performance (Alexander et al., 2023; Cuckston, 2022), see Table 1 for examples from the 2023 annual report. Many posts on social media contained similar information as the annual report but would often provide more details and content such as photos or videos. This, we believe, enriched the body of empirical material used to gain a sense of WWF's mobilisation of time in their biodiversity accounts.

To begin the data analysis, we read the reports (2021, 2022, 2023) and Facebook posts (2023) to gain an overview. We then conducted a close reading of the material in two rounds. During the first round, we organised the material in terms of how WWF-SE construct the calculative space, using Cuckston's (2022) framework as a guiding lens. Here, we collected quotes that could be linked to each step, compiling them in a single document to ensure comparability. During this round, we began to form an understanding of WWF-SE's approach to framing performance, which we document in the findings section (Section 5). The “theory of change” illustration, which was included in all three annual reports, proved particularly useful to construct a cohesive picture of how WWF-SE view the main entities and the relationships between them in the calculative space.

Once an overarching understanding of the calculative space had formed, we used the concept of time rationalities (Chakhovich, 2019) to analyse each step of the framing process. For example, applying present-based rationality highlighted WWF-SE's frequent references to the urgent need for action. In line with our explorative aim, the theoretical framework combining the notions of time rationalities and framing performance guided our analysis while allowing for inductively derived patterns throughout the process (Miles et al., 2014). Gradually, our observations of narratives reflecting different temporal viewpoints led to our conceptualisation of different roles of time in framing biodiversity performance. To assess the soundness of the emerging results, we continuously iterated between writing, reading the empirical material, discussing the interpretations among ourselves and relating our emerging insight to prior literature. During this stage of the analysis, we aimed to identify both explanations for how temporal viewpoints add to the complexity of biodiversity accounts and opportunities for the emancipatory approach to biodiversity accounting (Atkins and Maroun, 2018; Maroun and Atkins, 2018). In the paper, we refer to this approach as utilising a time-aware stance.

5. Empirical findings

In the following sections, we describe how WWF-SE frame their biodiversity performance according to the steps outlined in Section 3, focusing on how temporal viewpoints shape the construction of accounts.

5.1 Establishing the calculative space

A calculative space is established by identifying which entities to include in the framing process. In the context of non-profits, this often requires defining problems that organisations aim to address (Cuckston, 2022). Therefore, a key temporal consideration is which time horizon to draw on when identifying biodiversity challenges to tackle. For example, which issues are important because of negative historical trends, and which issues arise from visions of a better (or worse) future? The answers to these questions will determine which performance objects the organisation will report on, and thus what counts as a biodiversity performance.

WWF-SE establish the calculative space by introducing the biodiversity challenge of severely declining ecosystems, followed by presenting the overarching goals of the global WWF network to support biodiversity. There are three overarching goals to be achieved by 2030 (WWF-SE, 2022, p. 19):

Stopping habitat loss is linked to conservation activities regarding natural ecosystems by supporting or restoring their resilience against climate change.

Stopping extinction refers to activities aimed at maintaining or increasing populations of protected species by, for example, reversing the negative population trend of declining flagship species.

Halving the footprint of all production, consumption and emissions can be viewed as a supporting goal which contributes to the other two goals.

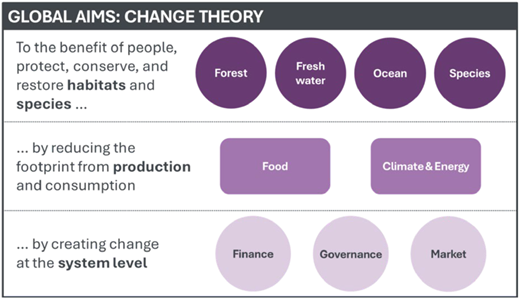

The goals introduce two performance objects, species and habitats, along with the activities WWF-SE will undertake in relation to these. In addition, three groups of activities targeting system-level change are introduced. A rendition, translated from Swedish, of what WWF-SE refer to as their “theory of change” is shown in Figure 1, which illustrates the performance objects at the top level and the enabling activities at the lower two tiers. Together, the three tiers explain not just what aims to strive for but also the means of achieving them, both through direct (at the top tier) and indirect (at the lower tiers) activities.

Time plays an important part in how WWF-SE establish the calculative space, particularly a view from the past. In their annual reports, WWF-SE present trends (typically negative) regarding biodiversity at both the global and Swedish level. Present aims and actions are related to a timeline of past performance. Past-based rationality (Chakhovich, 2013, 2019) thus becomes a way to tell a story of ecosystems in decline, whereby past trends of species and populations justify WWF's arguments for actions in relation to these trends. Quantifying the past through past-based rationality brings entities into the calculative space by framing patterns of decline in relation to the overarching aim of increasing biodiversity; this, in turn, underlines the need for actions in the present.

While past-based rationality can be a way to refer to successful historical cases to strengthen accounts of potential outcomes in the present (Chakhovich, 2019), in the WWF case past-based rationality is primarily used to highlight negative trends that need to be turned around. WWF-SE mobilise different time horizons for this, stating, for example, that, “150 years ago there were 500,000 rhinoceroses in Asia and Africa, today there are only 27,000 left” (WWF-SE, 2021, p. 19). This way of quantifying the past provides a baseline for measuring and assessing future outcomes and setting goals, which are converted into actions on a short time horizon as seen in the following quote:

To turn the trend of decreasing biodiversity and increasing climate change, humanity’s impact on the climate needs to halve by 2030, chiefly through changes to food and energy supply systems. (WWF-SE, 2022, p. 9)

In the quote, the future aim reflects the stated biodiversity challenges that WWF-SE aim to address. In this sense, mobilising time through past-based rationality adds valuable historical context to the accounts, thereby strengthening the argument. In addition, as an environmental advocacy organisation, WWF-SE looking from the past often serves the dual purpose of establishing a context for framing performance in concrete terms and of engaging the general public. The latter of these often plays out via WWF-SE's social media pages, where the quantified past is used to support donation appeals, as illustrated by the following quote:

Conflicts with humans is one of the reasons why lion populations have declined by over 75 percent in the past 50 years. /…/ With your support, it is possible to keep saving the lions. (WWF-SE, Facebook, 2023/01/04)

In WWF-SE's case, it was observed that the past was not used alone to account for performance, but rather that it was combined with other temporal viewpoints to establish the calculative space and the challenges to be addressed. Particularly, the near future was often mobilised to frame the goals and the need to act. Such present-based rationality (Chakhovich, 2019) uses the present as a starting point to make inferences. While the past-based rationality, supported by quantifications of trends, offers valuable context to make sense of current performance, the present-based rationality makes plans appear more actionable. A recurring approach for using present-based rationality is the reference to “if… then” scenarios, in which WWF-SE describe an undesired future to support the argument that the actions of today will carry into a cumulative performance in the future:

Our civilisation is under threat and a large share of the planet’s plants and animals are at risk of extinction locally if today’s rate of emissions continues. (WWF-SE, 2023, p. 8)

The use of the concept of the envisioned future occurring soon adds a dimension of urgency (Tregidga and Laine, 2022) to the narrative of ecosystems in decline. The emphasis on urgency stems from the shift from perceiving the present through the lens of a benign and rather distant future, to a malign, imminent future, driven by short-term action (or lack thereof). This is further illustrated by the introductory phrase in the Secretary-General letter “We live in a time of never before seen dangers to the planet” (WWF-SE, 2023, p. 2), which delineates the present from the past by describing it as the worst time yet for the climate. This creates a separation between the past and present, shifting the temporal focus of the account, as discussed by Chakhovich (2019) when describing potential roles of the present-based rationality. The purposeful use of the present-based rationality to describe how negative impacts will carry over into future outcomes is key to repositioning present biodiversity performance as both urgent and important, which aligns with how biodiversity is viewed in both literature and practice (e.g. Jones and Solomon, 2013; Schaltegger et al., 2023; World Economic Forum, 2020; WWF, 2024).

In sum, WWF-SE establish a biodiversity context and issue a call to action by deploying the past through quantifications of negative trends and by envisioning a critical state of biodiversity in the near future. The two approaches are informed by different temporal viewpoints: under the past-based rationality, future actions are defined based on events in the past which emphasises historical measures and outcomes, whereas present-based rationality often involves separating present from past.

5.2 Creating relations between the performance objects and activities

The second step of framing performance is to establish relationships between entities in the calculative space in order to determine whether the organisation's activities lead to the intended outcomes, i.e. performance (Cuckston, 2022). Linking is often complex due to the time lag between activities and outcomes, but it is also shaped by how the account-giver is oriented in time. For instance, looking from the present places less emphasis on outcomes further down the line, whereas looking from the future makes current plans contingent on expected future outcomes to determine whether goals have been achieved (Chakhovich, 2019). Therefore, the temporal viewpoint adopted by the account-giver can affect both the necessity to clearly link entities, and the timing of their assessment.

In WWF-SE's annual reports, relations between entities are elaborated through the theory of change (Figure 1), which explains how activities lead to the intended performance (Cuckston, 2022). Time is inherent to the linkages proposed in this theory; the steps are described as sequential in the sense that the bottom layer (focusing on system level support such as finance, advocacy and awareness-raising to change attitudes) enables the middle layer (focusing on more tangible practices aimed at reducing negative impacts), which in turn contributes to outcomes for the performance objects, species and habitats. Activities can target multiple levels, aiming for indirect outcomes at the lower tiers, or by targeting species or habitats directly.

Activities supporting lower tiers are often more temporally separated from impacts on specific species and habitats, which presents a challenge from a linking perspective. Indeed, WWF-SE account for multiple market and governance initiatives (bottom tier) without stating specific outcomes for species and habitats, since such outcomes may not yet have materialised. For example, an account of a new agreement among 11 South American and Asian countries is described as “a decisive step to decrease the threats to these endangered species and strengthen the possibilities of survival for the most vulnerable populations” (WWF-SE, 2023, p. 23). The activity has taken place and is framed as a step in the right direction – a “leap of faith” per present-based rationality (Chakhovich, 2019). In a similar vein, a Science-Based Targets for Nature programme, where WWF-SE are one of the initiators, is framed as a promising way forward:

The launch of the programme for scientifically based goals for nature is an important positive development to help companies to take measures related to nature in their operations, value chains, and holdings. (WWF-SE, 2023, p. 28).

When it comes to activities with a direct impact on species and habitats, one account references the “successful release of two thornback rays in the Gullmar fjord in Lysekil which gives hope for an endangered species” (WWF-SE, 2021, p. 68). The description suggests that performance has been achieved due to an expected future outcome for the thornback ray. Some direct activities recur in several reports without including accounts of cumulative results over time. For example, both the 2021 and 2023 reports describe positive outcomes for dolphin populations in Cambodia, which, following present-based rationality, focus on activities and outcomes in the present rather than cumulative progress from 2021 to 2023:

WWF Cambodia, authorities, and the local community undertook several activities to decrease the risk of bycatching dolphins in the illegal fishing. (WWF-SE, 2021, p. 33)

In Cambodia, WWF run an intensive conservation program to save the critically endangered population of Irrawaddy dolphins in the Mekong River. Through patrolling and collaboration with local communities, we reduce bycatch in fishing nets and combat illegal electric fishing, which positively impacts the dolphins' survival. (WWF-SE, 2023, p. 23)

Hence, despite articulating expected temporal linkages both in writing and visually, WWF-SE appear to struggle with consistently bridging the separation in time between activities (both direct and indirect) and outcomes. In contrast to the quantified past being used to create a sense of urgency to act in the first step of framing performance, these events are not yet anchored in demonstrable outcomes. In the absence of such evidence, WWF-SE manage the separation in time by extrapolating from the present into the future. As indicated by the above examples, WWF-SE typically use accounts based on optimism and hope about a future state, which, following present-based rationality, serve as proxy evidence of performance (Chakhovich, 2013). Thus, the activities described, such as restoring a marsh, establishing a stone reef, creating a wildlife corridor and deploying guards to confiscate illegal equipment, are all assumed to be measures of performance because they are positive steps towards the overarching aim of protecting species and reducing habitat loss. However, as WWF-SE do not provide quantitative evidence or explanations of how efforts translate into tangible performance, the connection between entities can be described as expectations-based rather than material. The accounts are often characterised by an unclear way forward from the present and, often, rather vague hopes for the future (e.g. “strengthen the possibilities of survival” and “help companies to take measures”). Some of the difficulty may be the result of the complexity of measuring outcomes (Sobkowiak et al., 2020; Weir, 2019), as extrapolating from the present requires some valuation, i.e. calculation in a broader sense (Callon and Muniesa, 2005; Cuckston, 2022). While hope and expectations may connect the present and the future, connecting the past and the present requires more substantial evidence, which is closely tied to extracting results.

5.3 Extracting a result

The third step of framing performance is to extract results regarding the performance objects. This is done by creating a new entity, such as a sum or an evaluation which is stable enough to travel outside of the calculative space so that performance can be reported and compared externally (Cuckston, 2022). Time, and timing, is crucial as it determines when, if and how performance can be extracted. As noted in the accounting literature, extraction typically takes place at specific intervals – month, quarter and year (Chambers, 1989; Ezzamel and Robson, 1995; Johnson and Kaplan, 1987) – though continuous models are increasingly common thanks to advanced accounting technologies (Al-Htaybat and Al-Htaybat, 2017; Izzo et al., 2022). The fact that biodiversity operates on the long time horizon of the planet's ecosystems (Rockström et al., 2009; Whiteman et al., 2013), i.e. beyond the usual planning horizon for firms (Freeman and Groom, 2013), may lead to tension regarding the extraction points and durations of performance, and is something organisations must consider when framing performance. This difficulty of choosing a suitable extraction point is evident in WWF-SE's annual reports, where different temporal viewpoints offer different ways of managing this difficulty. For example, WWF-SE extract results by describing impacts on species and habitats, such as hectares restored or the growth of populations of a species. They also repeatedly emphasise that protecting species and restoring habitats span long time horizons. Aside from some projects conducted as part of a temporary biodiversity programme ending in 2023, most accounts are framed not as final outcomes but as ongoing efforts. For example, WWF-SE have “continued” the work in specific projects (e.g. protecting sea turtles in Greece in 2022), things are “under construction” (e.g. a platform for innovation in sustainable food systems in 2023), and projects have been “initiated” during the past year with clearly defined objectives (e.g. One Health, a project supporting elephants, rhinoceroses and lions in 2023). Projects are not only described as ongoing, but, with few exceptions, often lack a clear conclusion or endpoint. Rather, WWF-SE often emphasise persistent difficulties and actions to address these, as seen in formulations about efforts to protect Irrawaddy dolphins, which are “still severely endangered” (WWF-SE, 2021, p. 33) and the struggle to save rhinoceroses “every day around the clock in the field” (WWF-SE, 2022, p. 19).

Although it is a challenge to extract performance, WWF-SE do so across multiple time horizons, reporting either activities, outcomes or both, using “ad hoc temporal brackets”. In some cases, the time horizon of both activities and outcomes is the past year, similar to conventional accounting (Chambers, 1989). Examples include 4,000 trees planted in Borneo (WWF-SE, 2022, p. 25), 200 hectares of restoration in Qinling (WWF-SE, 2023, p. 23) and zero rhinoceroses killed by poachers (WWF-SE, 2022, p. 19), where both actions and outcomes occurred during the past year. The latter example, in particular, is indicative of the difficulty of extracting a performance according to a conventional accounting horizon of the year: achieving zero biodiversity loss for one species when the time horizon of biodiversity is indefinite may appear relatively minor within broader ecological timescales, thus illustrating the limitations of present-based rationality (Chakhovich, 2013, 2019). It is therefore not surprising that WWF-SE also frequently account for activities and outcomes over longer time horizons, such as the report that 25 arctic fox pups were born in 2023 (WWF-SE, 2023, p. 21) as a result of 20 years of work supporting their habitat. Relatedly, WWF-SE, much like WWF-UK (Cuckston, 2022), often extract results from longer time horizons, such as ten years (black rhinoceros in Africa increased from 4,860 in 2011 to 5,630 in 2021), 13 years (the global tiger population has increased since 2010 to 5,574 in 2023, of which 3,682 in India) and 121 years (Indian rhinoceros increased from 100 in 1900 to 3,700 in 2021). In these cases, both the actions and outcomes last several years and are extracted at varying intervals using time horizons that appear more suited to the lifecycles of species and habitats than to conventional accounting cycles.

In addition to the ad hoc temporal bracketing spanning activities or outcomes, or both, beyond the conventional accounting brackets of a month or a year, WWF-SE also incorporate significantly narrower temporal brackets. One example of this is their annual live broadcast of fish migration, reported on Facebook:

During the month of May, the pike migration from Sörlebäcken at the High Coast was broadcast live in collaboration with the County Administrative Board of Västernorrland and showed how pike, whitefish and perch from the Bothnian Sea migrate to protected spawning areas in fresh water. […] WWF encourage the public to report migration sightings. More than 3,000 reports came in during the two weeks of broadcasting. (WWF-SE, 2022, p. 27)

The use of ad hoc bracketing is closely linked to the overall approach to accounting for performance by WWF-SE. Similar to the UK context (Cuckston, 2022), it is common for performance objects, i.e. species and habitats, to vary between years. Only the panda, tiger and black rhinoceros recur on an annual basis from 2021 to 2023. Some species appear in several but not all of the annual reports (arctic fox and African elephant) but more commonly, species are mentioned only once over the three-year period studied (e.g. snow leopard, Indian rhinoceros, Javan rhinoceros and gorilla). While accounts regarding the tiger contain comparable numbers across all three years, the majority of accounts follow a more idiosyncratic pattern, reflecting the present-based rationality where the connection between the past and the present is disrupted. Present-based rationality can be a deliberate approach to emphasise actions in the present without reference to past outcomes (Chakhovich, 2019). Rather than consistently drawing on past results as a foundation for present results (i.e. past-based rationality), results are based on what WWF-SE currently know about their performance. There are several conceivable reasons for this lack of consistency, one being the limited availability of biodiversity data on specific species in general (Sobkowiak et al., 2020) and another being that change may take more than three years to materialise in the context of biodiversity, thereby limiting the possibility of extracting relevant trends every year.

Another way in which WWF-SE diverge from the conventional accounting extraction points in favour of biodiversity's time horizons is by repeating past and ongoing efforts in multiple annual reports when accounting for present results. In line with past-based rationality, where past trends are related to current outcomes and thereby “prove” the strength of a performance (Chakhovich, 2019), WWF-SE acknowledge the path leading to the present, providing historical context for current results. An example can be seen in how WWF-SE describe their work with arctic foxes in 2022:

WWF have worked hard for 20 years to restore the arctic fox population in the southern Swedish mountains and that has generated tangible results. In 2022, nearly 30 active arctic fox lairs were found around the Helag mountains” (WWF-SE, 2022, p. 17).

Rather than merely accounting for the 30 lairs just found, WWF-SE convey that this result depends on both enduring and hard work on their part, combining the theme of perseverance with the principle of ad hoc temporal bracketing to reinforce the claim. Another account exemplifies a different type of perseverance: in Qinling, China, WWF-SE have been involved in restoring forests and establishing wildlife corridors to give pandas more space and improved access to food. Here, WWF-SE emphasise the long time horizon needed to achieve measurable results in many cases:

… the pandas started using the corridor already in 2015, but during 2023 we have documented for the first time that they eat the planted bamboo. Proof of the success of WWF’s work. (WWF-SE, 2023, p. 23)

Hence, biodiversity performance requires ongoing work over long time horizons, and, crucially, perseverance over time. WWF-SE demonstrating endurance and patience while waiting for nature's processes to unfold can thus be viewed as performance in its own right, albeit on a more qualitative level. Similar to the arctic fox example, extracting results requires an account of work done over the years leading up to the point of extraction in order to link activities to the measurable evidence of pandas benefitting from restored habitats. This way, WWF-SE are able to extract results in a way that is forgiving of the fact that clear results are not always reached or measured on a yearly basis while at the same time recognising WWF-SE's past perseverance. Perseverance can be seen also in accounts related to the lower tiers of the calculative space (Figure 1). On several occasions, WWF-SE refer to their enduring advocacy work (e.g. “after nearly two decades of intensive advocacy work” (WWF-SE, 2023, p. 48)) which occasionally pays off in terms of political attention or agreements in favour of biodiversity. However, as such outcomes do not directly impact the aim of stopping extinction and habitat loss, they may instead be regarded as outcomes that foster hope for future biodiversity performance (see section 5.2). In fact, even in the panda example described above, where WWF-SE highlight an outcome that is closely related to the goals of stable populations and restored habitats, they simultaneously write that “the panda corridor instils hope for maintaining the pandas and their unique habitat for future generations” (WWF-SE, 2023, p. 23). This again underlines the difficulty of extracting a result in the ongoing work to protect and strengthen biodiversity and to find alternative ways of framing performance.

6. Roles of time in framing biodiversity performance

Our exploration of how WWF-SE mobilise time, understood as temporal viewpoints, in their biodiversity accounts demonstrates that time can play multiple roles in the framing of performance. Throughout the three steps of framing performance, we found five roles: time as trend, urgency, expectation, snapshot and journey. Here, a role denotes a mode of mobilising time from a certain viewpoint within an account, each with its own advantages and limitations. Recognising these, i.e. adopting a time-aware stance, may prove valuable to biodiversity accounting as it makes organisations' impact on biodiversity more visible, specific and actionable. Thus, in the spirit of guiding emancipatory accounting practice (Maroun and Atkins, 2018), we discuss the roles below, showing how they support a time-aware stance to emancipatory accounting. The roles are summarised in Table 2.

Time as trend is characterised by quantifying the past through past-based rationality. That is, accounts are framed in relation to historical events or trends, which can make them more specific and concrete since the events occurred in the organisation's history. Thus, by looking from the past, time provides evidence that strengthens accounts made in the present, offering a context for extinction accounting in line with the emancipatory approach (Maroun and Atkins, 2018). Connecting past and present performance according to time as trend thereby adds credibility by providing a sense of continuity between outcomes in the past and ambitions in the present, and, thus, consistency over time. This is achieved by explaining how action (or inaction, in some cases) contributed to the current situation. As noted by Cuckston (2022), quantification plays an important role in benchmarking performance, though this is difficult in practice because the choice of measures of performance is often based on an ad hoc selection of species and habitats to report on. At the same time, a drawback of time as trend is that, regardless of how consistent and cohesive the historical data is, it will produce accounts firmly anchored to the past, which can lead to incomplete, biased, or unsuitable metrics that lack a future vision, be it promising or dystopic, to guide action in the present.

In contrast, the time as urgency role engages the near future as a threat to the present in order to stress the importance of acting now (Tregidga and Laine, 2022). While such calls for action may seem typical to NGO accounting (Cuckston, 2022), time as urgency is closely aligned with emancipatory biodiversity accounting's emphasis on firms establishing a “duty of accountability” (Maroun and Atkins, 2018, p. 109) by outlining their reasons for supporting conservation and restoration. Adopting the time as urgency role also invites organisations to consider targets and actions in the short term, which contradicts much of current reporting that treats biodiversity as solely a long-term concern (Boiral, 2016; Rimmel and Jonäll, 2013). However, framing the calculative space only in terms of near-future scenarios around threats and problems can also have a paralysing effect, which may hinder an organisation's capacity to act.

The time as expectation role may counterbalance dystopian perspectives invoked by other roles as it involves extrapolating from the present to future outcomes. While emancipatory studies have advocated the inclusion of more specific effects of the organisation's actions in reports (Atkins and Maroun, 2018), the WWF-SE case illustrates that even biodiversity-oriented organisations may struggle to provide concrete performance measures in practice, particularly if quantitative data is lacking. In such cases, time as expectation offers a way to demonstrate the effectiveness of one's actions through more qualitative, evaluative descriptions of expected outcomes of those actions. Our analysis of WWF-SE illustrates that one way to achieve consistent narratives is to describe the relationship between different types of actions and outcomes in sequential terms by showing expected positive outcomes with regard to both direct and indirect impacts. For some organisations, reducing emissions may constitute one of the more direct, material impacts they could have on biodiversity (Schaltegger et al., 2023). For others, the impact may be indirect, for example engaging in partnerships with NGOs (Maroun and Atkins, 2018) to build awareness and knowledge around an issue which is in a nascent stage from a reporting perspective (Adler et al., 2018; Roberts et al., 2023). As indirect activities in particular may appear both temporally and spatially distant from the species and habitats they aim to support, they may appear less rewarding. However, thinking about the organisation's efforts in a sequential manner could help outline a pathway of steps to be taken towards biodiversity goals.

The last two roles are time as snapshot (using ad hoc temporal bracketing) and time as journey (exhibiting perseverance). Both roles are ways to manage the schism of accounting cyclically (e.g. yearly, monthly or quarterly) for actions that, in reality, are continuous and extend into the foreseeable future without a natural extraction point. While emancipatory studies tend to agree that biodiversity performance, too, should be expressed in quantitative terms (Atkins and Maroun, 2018) and account for progress year on year (Zhao and Atkins, 2021), the case of WWF-SE illustrates several difficulties associated with this as well as the value of alternative approaches. First, extracting results yearly as an incomplete snapshot from a long time horizon of biodiversity projects can result in accounts that are either too idiosyncratic (Cuckston, 2022) or overly similar to previous years (Zhao and Atkins, 2021). The former (idiosyncrasy) comes with the risk of obfuscating comparisons, but could, at the same time, be a way of providing more continuous reporting of ongoing projects to stakeholders; time as snapshot can thus serve as an important communicative tool for accountability based on continuous updates to stakeholders (Alexander et al., 2023). Second, accounts that do not change year-on-year may obscure the urgency of acting now (Tregidga and Laine, 2022). Indeed, repeated accounts are often perceived negatively (Zhao and Atkins, 2021), as are vague descriptions of ongoing sustainability projects (Milne et al., 2006). However, the time as journey role shows that repeated accounts also provide evidence of perseverance for projects and goals with a long, even infinite, time horizon. This challenges the conventional stance on repeated accounts as something largely negative from a disclosure quality perspective. Maroun and Atkins (2018) similarly highlight that self-reflection, for example in conjunction with assessing outcomes versus targets, is an important element of emancipatory accounting. Such self-reflection could benefit from being anchored to a longer past, for example by using the perseverance lens, as the case of WWF-SE shows.

Common to all the five roles outlined thus far is that they allow us to identify a gap in practice, even for a recognised success case in biodiversity accounting, namely an absence of future-based rationality in how time is mobilised. When WWF-SE do invoke the future, it is not through future-based rationality but from the viewpoint of either the past or present. These roles anchor accounts to past measures and benchmarks (past-based rationality) or to hopes of outcomes extrapolated from the present (present-based rationality). Although the former helps ensure consistency in quantification over time (Cuckston, 2022), and the latter case helps emphasise urgency and the need for immediate action (Tregidga and Laine, 2022), the absence of a future viewpoint reflects a possible lack of envisioned different futures and possibilities, which could guide action (Chakhovich, 2019). Given the potential of future-based rationality as a way to “leap into the unknown” (Chakhovich, 2019), there is currently untapped potential when it comes to framing biodiversity performance, particularly when establishing the calculative space to identify targets and key performance objects. Based on this, and in line with the emancipatory aim of providing guidelines for action (Maroun and Atkins, 2018), we propose a sixth role of time that draws on future-based rationality (Chakhovich, 2019): time as imagination. This role is discussed below (and summarised in Table 3).

Time as imagination could allow organisations to explore visions of a future they wish to be part of, and thereafter determine which actions and targets are necessary in order to achieve that vision. Such an approach would be similar to how Science-based targets can be used, where global ecological concerns such as the planetary boundaries, rather than the organisation's current performance, determine what to strive for (Jabot, 2023). This is closely aligned with emancipatory accounting, which seeks to reimagine accountability and empower behavioural transformation (Atkins and Maroun, 2018). However, as noted by Mouritsen and Kreiner (2016), a “promise” regarding an envisioned future is intended to guide action, and as such, should appear achievable. If targets are set beyond the organisation's capability to extract results, the imagined future could appear speculative and disconnected from reality, which may reduce organisations' or stakeholders' willingness to take action. Another potential issue is that it is difficult to imagine the needs of future generations of stakeholders (Chakhovich and Virtanen, 2023), which could lead to less useful plans and targets being formed, even when future-based rationality is applied. It could therefore be helpful to tie the future vision to other roles of time to ensure linkages across time horizons, or to attempt to use a more concrete basis of imagining. Here, the body of literature examining the valuation of nature (e.g. Drupp et al., 2024; Freeman and Groom, 2013; Lamont et al., 2023) could provide some guidance. These studies have, for example, shown that the discounted value of costs and benefits depend greatly on the chosen time horizon (Freeman and Groom, 2013). By developing different scenarios, supported by quantification, which reflect different time horizons, values and assumptions about biodiversity loss, organisations could identify how present-day action amounts to different outcomes for species and habitats in the longer term. However, while the use of scenarios can be an effective planning tool in the management setting (Palermo, 2018), it should be noted that scenarios tend to be uncertain, particularly in the long-term (Freeman and Groom, 2013), and the credibility of planned strategies could be called into question if effects do not materialise at some point.

As illustrated by the discussion of the six roles, there are advantages and disadvantages to each way of mobilising time, as they may obscure or leave out key aspects that could be relevant to frame biodiversity performance cohesively. By taking a time-aware stance, for example by considering the advantages and limitations, or by combining multiple roles, some of the challenges for biodiversity reporting observed in prior studies, such as lack of data, idiosyncratic follow-up and poorly motivated efforts (e.g. Adler et al., 2018; Cuckston, 2022; Lamont et al., 2023; Maroun and Ecim, 2024; Sobkowiak et al., 2020; Weir, 2019) could be addressed and mitigated. Indeed, to achieve emancipatory biodiversity accounting, it is important to show clearly and consistently why and how the organisation contributes to conserving and restoring species and habitats (Atkins and Maroun, 2018; Maroun and Atkins, 2018). Adding to this body of literature, our findings show that mobilising only one role of time limits the potential to cohesively account for biodiversity performance and may detract from the organisation's ability to provide consistent accounts. Instead, combining numbers from the past (time as trend) with numbers from scenario modelling (time as imagination) could establish a more compelling extinction accounting context and ensure temporal consistency between targets and impacts. Another approach could be to use a combination of suitable temporal brackets (time as snapshot) at critical points of exhibiting perseverance (time as journey) to help solidify the relationship between past, present and future actions and outcomes in a meaningful way. Using roles in combination, in line with the time-aware stance, can thus help address one of the key concerns when framing biodiversity performance, namely how to reconcile the importance of urgency, the need for perseverance and the indefinite future during which biodiversity needs to be conserved. At the same time, there is clearly a value to each of the roles in their own right, and our knowledge of their advantages and disadvantages contributes to the nascent state of research on time in biodiversity accounting.

7. Conclusion

The issue of biodiversity spans multiple, often conflicting, time horizons, making it a ticking clock both in the sense of an urgent “ticking countdown” in the present and of something needing “continuously ticking efforts” over the long term. Based on a study of WWF Sweden's official accounts of biodiversity, informed by framing theory (Callon and Muniesa, 2005; Cuckston, 2022) in combination with the concept of time rationalities (Chakhovich, 2013, 2019), we explored how time, understood as temporal viewpoints, is mobilised in accounts of biodiversity. This point of departure draws attention to whether an account reflects a view from the past, the present or the future, enabling a more nuanced understanding of the role of time in the framing of biodiversity performance. By engaging deeply with time in biodiversity accounting and introducing what we refer to as a time-aware stance, our study adds insights that could “encourage changes in mindsets” (Maroun and Atkins, 2018, p. 107) and also acts as a step towards further theorisation of time in both biodiversity and sustainability accounting more generally, thereby responding to calls by, for example, Tregidga and Laine (2022).

We identified five different roles of time, which followed a view from either the past or the present. As the time rationalities framework (Chakhovich, 2013, 2019) also includes a future-based rationality not observed in the empirical material, we also propose an additional role: time as imagination. This role is intended to encourage organisations to move past the constraints of the past and present, and to envision different future states, outcomes and plans for biodiversity by looking from the future to guide action in the present. Each role was shown to provide opportunities and challenges for emancipatory extinction accounting (Atkins and Maroun, 2018; Maroun and Atkins, 2018; Zhao and Atkins, 2021). Moreover, while social and environmental performance is generally difficult to define and measure (Bebbington and Larrinaga, 2014; Cuckston, 2022; Gray, 2006; Luque Vílchez et al., 2023), the case of WWF-SE points to the potential of relying on multiple temporal viewpoints and combining several roles of time to frame biodiversity performance cohesively and comprehensively.

The results also extend the literature on biodiversity reporting by explaining how some of the shortcomings of biodiversity accounting identified in prior research, such as vague, brief and incomparable accounts (e.g. Boiral, 2016; Hassan et al., 2022; Rimmel and Jonäll, 2013), may stem from the complexities of time as a dimension of biodiversity performance. Researchers could therefore benefit from engaging more comprehensively with temporal viewpoints going forward, for example by extending the proposed framework with additional roles or by exploring interplays between them. Overall, our study illustrates that time is not merely a matter of a short or long horizon, but equally, a viewpoint which actively shapes the framing of performance and thus how biodiversity outcomes are described and communicated.

In proposing a time-aware stance, we also hope to inspire future research in biodiversity and sustainability accounting beyond our empirical case and setting. Although we chose to focus on a single sustainability topic to support a deeper understanding of its inherent complexities (Sobkowiak et al., 2020), biodiversity is a system-level concern that would benefit from relating organisational activities to the wider implications for other societal and planetary actors (Gray and Milne, 2018; Schaltegger et al., 2023). Relatedly, much of sustainability accounting is concerned with the paradox of long time horizons and urgency (Tregidga and Laine, 2022), a tension not unique to biodiversity. Therefore, our line of investigation focusing on temporal viewpoints may be meaningfully extended to other sustainability topics, for example other Sustainable Development Goals where similar temporal complexities persist. Finally, while many concerns in NGO accounting are transferable to for-profit context (Hall and O'Dwyer, 2017), we would encourage future studies to build upon and critically engage with our perspective across other sectors and contexts.

The authors would like to express their sincere gratitude to the two anonymous reviewers for their very helpful and inspiring comments.