The purpose of this study is to evaluate how global agricultural stock markets reacted to African Swine Fever (ASF) outbreaks in China and Germany in 2020, and to identify which agricultural sub-industries were most affected. The study also aims to provide insights into how market responses differ between major importing (China) and exporting (Germany) countries and is hence a comparative case analysis of these two specific ASF outbreaks.

An event study methodology is applied using daily data from a global agricultural MSCI Index. Cumulative abnormal returns (CAR) following these two ASF outbreak announcements are estimated for the full global agricultural MSCI Index and for four agricultural sub-industries and compared. Multiple model specifications and placebo events are used to test the robustness of these results.

The results show statistically significant negative CAR for the MSCI agricultural index following ASF outbreak announcements in both China and Germany, with stronger effects observed for the Chinese outbreak. The sub-industries “agricultural products and services” and “packaged foods and meats” primarily drive the negative market reactions in response to both outbreaks. These findings remain robust across alternative specifications.

The study highlights the vulnerability of global agricultural markets to animal disease outbreaks and underscores the need for investors, policymakers and firms to account for sector-specific and country-specific risk exposures. Understanding which sub-industries are most affected can support the development of targeted risk-mitigation and crisis-response strategies.

This study provides the first comprehensive assessment of ASF’s impact on the global agricultural sector using a broad-based agricultural MSCI Index. By comparing market reactions between a major importer (China) and a major exporter (Germany) and examining heterogeneous effects across sub-industries, it offers novel insights into investor behavior and the economic consequences of animal disease outbreaks.

1. Introduction

Pork is one of the most consumed meats globally (OECD/FAO, 2023). Global pork consumption increased from 63.5 million tons in 1990 to 115 million tons in 2023 (FAOSTAT, n.d.). In 2032, pork consumption is expected to grow globally by 11%, whereas poultry and beef meat consumption is expected to increase by 15% and 10% in the same time period (OECD/FAO, 2023). The forecast for global pork production is estimated to be 115.6 million tons in 2024, which is 1% less than in 2023 (116.2 million tons). China, the European Union (EU), and the United States (U.S.) are the top 3 producing countries, with China being the largest importer and the EU the largest exporter (USDA, 2024). The national and international pork markets experienced major disruptions following the confirmed outbreak of African Swine Fever (ASF). ASF is a fatal viral infection of pigs, which is considered to be the most important of all pig diseases (e.g. Penrith et al., 2013) with a major socio-economic effect (Penrith et al., 2004).

In general, animal disease outbreaks are one of the most prominent risks in the meat sector (OECD/FAO, 2023), and they can also have profound psychosocial effects on affected farmers, as demonstrated by a case study on Mycoplasma bovis following the 2017 outbreak in New Zealand (Noller et al., 2022) [1]. Animal diseases like ASF are not unidimensional and their economic effects are visible in the whole value chain (Zinsstag et al., 2007; Rich and Wanyoike, 2010; Pendell and Cho, 2013; Houser and Karali, 2020), for instance due to changes in food consumption and preferences among consumers (Luo et al., 2023) and a reduction in production and export quantities (Niemi, 2020). Thus, economic losses in the field of production, trade, consumption, and finance due to animal disease outbreaks are noticeable (Tozer et al., 2015; Çakır et al., 2018) and observable in the firms’ stock market values (Thompson et al., 2019). For example, Biden et al. (2024) estimate that a generic disease outbreak in the Canadian pork industry, which led to potential border closures and large-scale animal depopulation, resulted in Canadian economic impacts exceeding 3.6 billion U.S. dollars. Kashyap et al. (2024) use an online survey experiment and find that demand for unprocessed pork products in the U.S. is predicted to shift downward by approximately 32% in the event of an ASF outbreak, while the total annual welfare loss in the pork market is estimated at 55.46 billion U.S. dollars. Animal disease outbreaks can cause abnormal stock market returns and increasing price volatility in livestock markets (Houser and Karali, 2020; Xiong et al., 2021). To investigate and assess the effect of an animal disease outbreak on stock markets, an event study approach has been proven suitable (e.g. Henson and Mazzocchi, 2002; Xiong et al., 2021).

While event studies are commonly applied to investigate stock market reactions, the methodology is versatile and can be used to assess the effect of events on a wide range of financial instruments and economic indicators. In the context of stock markets, it enables researchers to quantify the effect of an event by analyzing abnormal returns. Specifically, event studies aim to measure how the market incorporates new information related to the event into asset prices (Sorescu et al., 2017). Event studies are based on critical assumptions for efficient capital markets: Stock prices reflect publicly available information and stock prices change instantly to reflect new available information (Fama, 1970; MacKinlay, 1997). In the context of animal disease outbreaks, Jin and Kim (2008) studied the outbreak of Bovine Spongiform Encephalopathy (BSE) in 2003 in the United States. The study showed that beef sector stock prices were negatively affected, while sectors providing substitutes were positively affected. Thus, their research highlights the need for differentiating between agribusiness firms which are integral parts of the value chain and other agribusiness firms which are part of the sector in general. Pendell and Cho (2013) focused on the foot-and-mouth disease (FMD) in Korea and found expected negative reactions by investors in the pork and feed industry. Thompson et al. (2019) studied the effect of the outbreak of the Highly Pathogenic Avian Influenza (HPAI) in the U.S. in 2014–2015 and also showed that the effect differed across firms specialized in poultry marketing and firms marketing other meats besides poultry. Recently, Xiong et al. (2021) used an event study approach to investigate pork firms’ stock price response to the ASF outbreak in China based on ten Chinese firms and fifteen global hog firms from eight exporting countries. Their findings showed positive abnormal stock returns for pork firms following the ASF outbreak (Xiong et al., 2021). However, ASF not only directly affects pork-producing and processing firms but also the broader agribusiness sector through its intersectoral linkages (You et al., 2021; Mason-D’Croz et al., 2020). Furthermore, pork markets respond differently to ASF outbreaks, leading to heterogeneous effects across countries (Niemi, 2020). Consequently, there remains a gap in understanding how ASF outbreaks affect the global agricultural sector as a whole and how these effects vary across different agricultural sub-industries. To date, no study has compared market reactions to ASF outbreaks between major importing and exporting countries using a comprehensive global index.

Against this background, this research aims to assess the market reactions of the agribusiness sector in general, and agribusiness sub-industries in particular, in response to the reported ASF in China and Germany [2] to the ASF outbreaks by employing an event study approach based on data from MSCI ACWI Select Agriculture Producers Investable Market Index (henceforth, MSCI ACWI SAP IMI) index. Specifically, we examine the outbreaks reported in Germany on September 10, 2020, and in China on October 22, 2020. These events provide a unique opportunity to compare market reactions in a major exporting country (Germany) and a major importing country (China). While the first ASF outbreak in China occurred in 2018 and had substantial economic effects (Chand, 2020), we focus on the outbreak of October 22, 2020, alongside the German outbreak of September 10, 2020. This timing is particularly relevant for our analysis, as it closely coincides with the first confirmed ASF case in Germany. It enables a more direct and timely cross-country comparison within a consistent market context and helps control for broader structural changes in the pork industry that had already taken place during the earlier phases of ASF spread. We deliberately do not focus on the 2018 outbreak in China in this analysis, as there is evidence that Chinese authorities attempted to under-report cases (Gale et al., 2023) and did not communicate the outbreak promptly or transparently (Inouye, 2019), making it challenging to accurately estimate its effect on the stock market. We hypothesize that both outbreaks will elicit statistically significant negative market reactions, consistent with the broader literature on animal disease shocks (e.g. Pendell and Cho, 2013; Biden et al., 2024; Tozer et al., 2015; Çakır et al., 2018; Mason-D’Croz et al., 2020; Wang et al., 2024). At the same time, we examine whether the magnitude of these reactions differs between the two cases.

This dual perspective not only sheds light on the localized effects of ASF but also provides a comparative analysis across international markets, highlighting the global implications of regional strategies and investor responses. Focusing on ASF outbreaks in China and Germany, rather than in pork-producing countries such as Canada, Denmark, Spain, or the U.S. [3] is particularly interesting for several reasons. First, the timing of ASF outbreaks in China and Germany aligns more closely, providing a more comparable basis for analyzing the stock market responses in both countries. China, being the world’s largest consumer and producer of pork, faced a devastating ASF outbreak that had a considerable effect on global pork markets, while Germany, a major exporter, experienced its own ASF challenges, which affected trade and market dynamics [4]. In contrast, countries like Spain either had different timelines or experienced a lesser effect on global pork supply chains, complicating the comparability of market responses. By focusing on China and Germany, the analysis can better capture the immediate economic repercussions of ASF on the global market. Furthermore, this study aims to differentiate the reaction of agribusiness firms which are an integral part of the pork processing value chain and directly affected by the ASF from agribusiness firms which are part of the whole agribusiness sub-industries and only indirectly affected. To do this, we differentiate between four sub-industries ((1) agricultural and farm machinery, (2) agricultural products and services, (3) fertilizer and agricultural chemicals, and (4) packaged foods and meats) and investigate the stock market reaction of these four distinct agricultural sub-industries to the reported ASF outbreaks. Hence, this research marks the first estimate of the economic effects of the ASF outbreak on agribusiness firms in major importing and exporting countries, respectively.

Our results show that the global MSCI ACWI SAP IMI responded with statistically significant negative cumulative abnormal returns (CAR) to the announcement of the ASF outbreak in Germany in September 2020. These results are robust across different event study specifications and placebo events. Furthermore, the comprehensive MSCI ACWI SAP IMI also reacted to the announcement of the ASF outbreak in China in October 2020, as shown by the statistically significant negative CAR. Again, these results are robust across different event study specifications and placebo events. These placebo estimates help reduce concerns that the stock market reacted to other events (e.g. COVID-19 (Nguemgaing and Sant’Anna, 2022; Höhler and Lansink, 2021)) or that the results are driven by market seasonality. When comparing the magnitudes of the effects across the preferred estimation specifications, the CAR in response to the announcement of the Chinese ASF outbreak was larger than that in response to the German ASF outbreak. The German ASF outbreak triggered a market reaction with CAR between −0.1 and −1.4%, while the Chinese outbreak caused a stronger negative association, with CAR ranging from −0.6 to −2.0%. These values indicate considerable market repricing in response to anticipated disruptions in supply chains, commodity prices, and firm profitability. Even a 1–2% decline in a globally diversified agricultural index represents substantial losses in market value, highlighting the tangible economic consequences of ASF outbreaks for investors and the broader agricultural sector. We interpret these results as robust associations.

By analyzing market reactions at the level of globally diversified agricultural equity indices, this article complements existing firm-level ASF studies (e.g. Xiong et al., 2021) by capturing broader financial market spillovers. This perspective allows us to assess how outbreaks in major pork markets propagate through global agribusiness portfolios and across agricultural subsectors. These findings provide new insights into how global agricultural markets react differently depending on the source of the shock, importing versus exporting countries, and highlight heterogeneity in investor responses across economic contexts, which prior research has not fully examined. This study helps investors and policymakers understand short-term market fluctuations and agribusiness performance, supporting more informed decisions during future ASF outbreaks. First, by analyzing CARs, we examine how investors respond to ASF outbreaks in key pork-producing and pork-consuming countries, namely China and Germany, major exporters and importers in the global market. Second, using the MSCI ACWI SAP IMI index, which includes companies across agriculture, we assess the vulnerability of agribusiness firms, distinguishing directly and indirectly affected sub-industries to identify differential risks and inform resilience strategies. Third, abnormal stock returns reveal industry-level responses, offering policymakers insights for mitigating economic effects and designing targeted financial incentives to promote preventative measures. Finally, comparing China and Germany highlights regional differences in market reactions, informing cross-border risk management and offering lessons for other pork-importing or -exporting countries preparing for future ASF or similar animal disease outbreaks.

2. Material and methods

2.1 Data

To address our research questions, quantifying the effect of ASF outbreaks in China and Germany on international stock markets, we rely on an MSCI index [5]. MSCI is a leading provider of global equity indices, covering a wide range of developed and emerging markets. Its indices are designed to be comprehensive and representative of the underlying markets (MSCI, 2023a), offering a clear advantage over manually constructing an index from Chinese and German firms.

Moreover, MSCI indices are built using a transparent methodology that ensures balanced representation of key sub-sectors and geographies. This allows the market impact of ASF to be assessed in a way that reflects broader economic conditions rather than an arbitrary subset of firms. Using a widely recognized MSCI index also enhances replicability: other researchers can verify and build on the analysis since the index composition and methodology are publicly available. In contrast, a self-constructed list of firms lacks transparency and may raise concerns about subjective selection. Accordingly, inclusion in the MSCI index serves as the criterion for selecting firms in each country for this study.

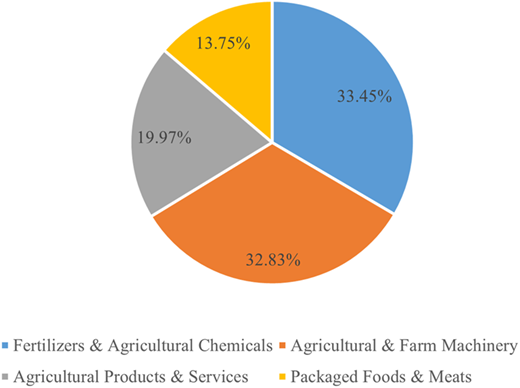

For this analysis, we rely on MSCI ACWI, which is a market-cap-weighted stock market index of 2,935 constituents throughout the world, covering approximately 85% of the free-float-adjusted market capitalization in each of the 47 national markets (MSCI, 2023a). To investigate the effect on the global agricultural market, we incorporated the MSCI ACWI SAP IMI in our analysis. This allowed us to specifically examine companies within the agricultural industries that exhibit high sensitivity to underlying prices of agricultural commodities. The index has four sub-industry weights: fertilizer and agricultural chemicals (33.2%), agricultural and farm machinery (33.2%), agricultural products (19.3%), and services and packaged foods and meats (14.3%) (compare Figure 1). Countries across the entire agricultural sector are relevant to this analysis because agricultural supply chains are highly interlinked, with some commodities reused in processes such as pork fattening. Consequently, a holistic approach, rather than focusing solely on publicly listed pork companies, is more comprehensive. This is particularly advantageous given the difficulty of identifying firms not clearly integrated into the pork supply chain, which would otherwise require subjective judgments rather than relying on a third-party index, such as MSCI.

Sub-industry weights of MSCI ACWI SAP IMI. Source: Own illustration based on the March 2023 version of the fact sheet of MSCI (2023a)

Sub-industry weights of MSCI ACWI SAP IMI. Source: Own illustration based on the March 2023 version of the fact sheet of MSCI (2023a)

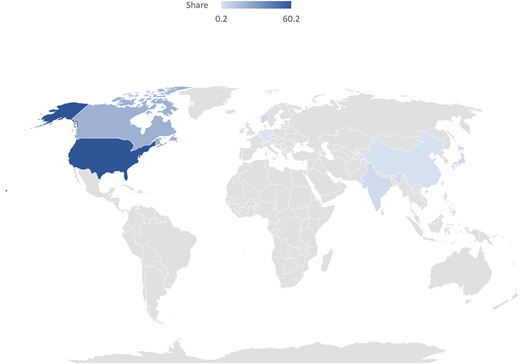

Examining the country weights in the MSCI ACWI SAP IMI (see Figure 2 and Figure A.1 in Appendix), most weight is given to firms from the U.S. (60.15%), followed by Canada (6.54%), Norway (4.21%), India (3.98%) and Japan (3.83%) [6]. Since 60.15% of the index weights are based on U.S. companies and to control for potential coinciding events in the United States that might drive the observed effects during the two ASF events, we searched the archives of The New York Times and The Washington Post, two major newspapers in the United States, for the two respective event dates. We did not find any articles indicating a major shock or major policy announcement on those days, which may drive the results on the global agricultural market [7]. This reduces concerns that the supply chain results are explained by unrelated events in the United States.

Country weights of MSCI ACWI SAP IMI. Source: Own illustration based on the March 2023 version of the fact sheet of MSCI (2023a)

Country weights of MSCI ACWI SAP IMI. Source: Own illustration based on the March 2023 version of the fact sheet of MSCI (2023a)

The index is derived from the ACWI IMI equity universe, which includes large, mid, and small-cap securities across 23 developed markets and 24 emerging markets countries (MSCI, 2023b).

The number of constituents for the MSCI ACWI SAP IMI contains 157 companies (see also Table 1). Several of these companies listed in the MSCI ACWI SAP IMI are also part of other MSCI indices, such as the MSCI ACWI Agriculture and Food Chain Index (MSCI, 2024) [8]. However, as the MSCI ACWI SAP IMI is the major global index, we decided to focus on this comprehensive index in our analysis instead of other smaller agricultural MSCI indices. We downloaded the stock data from Yahoo Finance (2023), Investing (2023), and NASDAQ (2023) in the local currency for the time period March 2018 to March 2023. Before compiling it into a final dataset, we converted all values into the U.S. Dollar using daily closing spot exchange rates.

Summary statistics for the MSCI ACWI SAP IMI

| Listed constituents | |

|---|---|

| MSCI ACWI SAP IMI | 157 |

| Sub-sectors | |

|---|---|

| Fertilizers and Agricultural Chemicals | 52 |

| Agricultural and Farm Machinery | 52 |

| Agricultural Products and Services | 31 |

| Packaged Foods and Meats | 22 |

In summary, ASF is a shock with worldwide implications, affecting international supply chains, commodity prices, and sectoral profitability beyond national borders. Many firms in the index, regardless of their listing country, operate globally and derive substantial revenue from markets influenced by ASF, including China and Germany. As such, the index reflects internationally integrated investor expectations and the cross-country transmission of sector-specific risk. Moreover, relying on a transparent, externally constructed index avoids subjective firm selection and enhances replicability and generalizability. Overall, the MSCI ACWI SAP IMI provides a suitable benchmark for assessing global agricultural market responses to ASF outbreaks.

2.2 Event study

An event study is applied to assess the association of a specific event (T0) on a particular variable of interest, in our case, the event is the announcement of the ASF outbreaks in China and Germany and the variable of interest is the financial market response, measured as changes in the stock market. The event day for the outbreak in Germany is September 10, 2020, the day the outbreak was first reported, while the event day for the outbreak in China is October 21, 2020, the day the outbreak was first reported in China [9]. An event study allows us to identify causal effects shortly after the events have occurred. However, we interpret our results as robust associations. Event studies have been widely used in agricultural economics (e.g. Dai et al., 2013; Kong, 2012; Nguemgaing and Sant’Anna, 2022; Xiong et al., 2023; Li et al., 2024). In a standard event study, it is assumed that market prices already incorporate all publicly available information, and any price changes would occur only due to unexpected events (MacKinlay, 1997).

The core of an event study is the assessment of abnormal stock returns (ARs) (MacKinlay, 1997), which we use to measure financial market responses to the two events in question (first reports on the ASF outbreak in China and Germany in 2020). A normal return is the expected return without conditioning on the occurrence of a defined event. The ARs are the changes in stock prices surrounding the occurrence of an event, accounting for the effects resulting from both industry and market-wide influences (MacKinlay, 1997). Thus, the objective is to determine whether the two events of interest lead to statistically significant changes in stock market prices.

The AR is the actual ex-post return of the stock over the event window, minus the normal return of the firm over the same period. To estimate the ARs, we first need to determine the normal return of our sample stocks. To calculate the AR for stock i on event date t within the event window, we use the following equation:

ARi,t is the abnormal return, Ri,t is the actual return and E(Ri,t) is the expected normal return for the event date t and stock i. Xt indicates the conditioning information for the normal return model (MacKinlay, 1997). We estimate the expected (normal) return with a market model, as this is commonly done (e.g. Xiong et al., 2023). The market model relates the return of the index under study to the return of a broad market benchmark, capturing the portion of the index’s movements explained by general market fluctuations [10].

The average returns of the respective MSCI Index before the events of interest are used as market value to calculate expected normal returns during the evaluation window. AR observations must be aggregated to draw inferences for the respective two events of interest (reported ASF outbreak in China and Germany in 2020). The ARs only measure the change in returns for a given day. Therefore, ARs are aggregated over time into a measure of CAR, the total effect of the respective incident (MacKinlay, 1997). We calculate CARs by accumulating the day-by-day AR for the five-day event window (T = 5) surrounding the events (T0 − 2, T0 + 2). To ensure robustness we also use event windows of nine and 13 days. For firm i’s stock return, calculated over a time interval t (t = 1,2,…,T), CAR are:

CARs are the abnormal returns observed during the period encompassing the two events of interest. The average index performance serves as a reference point, indicating how the stock would have performed if these events had not occurred. Therefore, the disparity between the actual stock performance and the normal performance, which defines the CARs, highlights the return patterns attributed to these events (Dai et al., 2013). Under the null hypothesis (H0), the ASF outbreak in the two respective countries has a statistically insignificant association on the stock market performance, measured as CAR. Hence, the CAR will be statistically insignificantly different from zero (equation (3)). Under the alternative hypothesis (H1), the two events have a statistically significant association on the CAR of the respective MSCI index. This can be formalized as:

First, we establish the event and its related periods: the ASF outbreaks (T0), which we are going to investigate. The estimation window represents the period during which we estimate the stock’s regular behavior in relation to the market. The event window encompasses the period in which we assess the AR associated with the incident and the investor’s response to the event. This approach allows for the examination of the periods surrounding the event (MacKinlay, 1997). As mentioned above, we utilize a 5-day event window (T0 − 2, T0 + 2) to calculate CAR in this study. Given the rapid pace of reactions in financial markets, it is crucial to pinpoint the timing of events with utmost accuracy. Establishing a precise time stamp enables analysis within a narrow time frame surrounding the event, thus safeguarding against market reactions being influenced by unrelated news (Born et al., 2014). In other words, the relatively narrow event window takes into account that the effects of an ASF outbreak are swiftly evolving as investors adapt and learn in response to such an event within a short time span. Furthermore, as the year 2020 was marked by considerable financial turbulence, due, for example, to the COVID-19 pandemic (Nguemgaing and Sant’Anna, 2022; Höhler and Lansink, 2021), it presents a challenge when attributing abnormal returns solely to ASF outbreaks. To address this, we use narrow event windows (T0 − 2, T0 + 2) in our preferred estimation specification, which helps isolate the immediate market reaction to ASF-related news from broader market movements, such as those driven by the pandemic.

Additionally, a longer window cannot distinguish between the reaction of the investors and other events that might have occurred or market noise. We apply an estimation window of 245 days prior to the event window, because 245 trading days are approximately one year. We select this estimation window, as it is commonly selected (e.g. Acemoglu et al., 2016; Xiong et al., 2021, 2023). In addition, the use of a one-year estimation window takes into account the existing price seasonality. The event window itself is not included in the estimation windows to prevent the event from influencing the normal performance model parameter estimates (MacKinlay, 1997).

The identification strategy relies on the assumption that the sole reaction of the stock market is the policy announcement. Given that returns fluctuate daily due to numerous factors, any other event (i.e. COVID-19 pandemic (Höhler and Lansink, 2021; Brueckner et al., 2023; Nguemgaing and Sant’Anna, 2022) or other geopolitical events (Lee, 2019; Höhler et al., 2024)), announcement, or data in any of these countries that influences returns and coincides with ASF outbreaks on the same day poses a potential challenge to the identification process. Concerns about potential confounding effects from sector- and firm-specific events, such as earnings announcements, may arise. However, annual earnings announcements for stock market companies typically occur in the first quarter of the year. Since the ASF outbreaks of interest in our case took place in September and October, respectively, we do not consider earnings announcements a major threat to our estimation strategy.

To ensure robustness, we also use event windows of different lengths, as done by Kong (2012). We re-estimate the event study using different event windows (t = 9 and t = 13 days). We also shorten the estimation window and use 123 days, which is equal to half a trading year. Lastly, we employ a placebo regression by using the dates from one year later than the actual ASF outbreaks as event dates (T0 + 1 year) [11]. This test helps to control for seasonality by checking whether observed effects could be attributed to recurring seasonal patterns. If the estimated effects during the placebo period are similar in magnitude and statistical significance to those of the original event, it suggests that seasonality might be driving the results rather than the actual event. Conversely, if the placebo regression shows no statistically significant associations, no large coefficients, or an effect in the opposite direction, this strengthens the validity of the original findings by confirming they are not confounded by seasonal fluctuations. We implement the placebo regression with an estimation window of 245 days and event windows of five and nine days.

The regression equation used in an event study is given by:

Here, CARi,t represents the variable of interest for index i (MSCI ACWI SAP IMI) at time t. α is the intercept, γ are the coefficients for the event dummy variables Di during the event window and ɛi,t is the heteroskedasticity robust error term (Miller, 2023).

To examine which of the four sub-industries of the MSCI ACWI SAP IMI and which world region drives the effects of the ASF outbreaks in China and Germany, we run the event study introduced in equation (3) separately for each sub-industry and for three regional components.

In summary, the event study relies on CAR, which tracks a stock’s performance over a specified period surrounding the event, with the abnormal component representing the difference between the actual stock returns during this period and the expected or normal returns. This study focuses on two ASF outbreak announcements, one in China and one in Germany, because these events represent the most economically consequential ASF shocks during the period under consideration. Our aim is not to estimate an average effect across many outbreaks, but to conduct two separate event studies on the same global agricultural index (MSCI ACWI SAP IMI) to examine and compare how markets respond to ASF outbreaks in distinct economic contexts: a major importer (China) and a major exporter (Germany). This design enables a direct comparison of market reactions to shocks originating from countries that play fundamentally different roles in global agricultural trade. We expect both outbreaks to generate statistically significant negative market reactions, consistent with the broader literature on animal disease shocks (e.g. Pendell and Cho, 2013; Biden et al., 2024; Tozer et al., 2015; Çakır et al., 2018; Mason-D’Croz et al., 2020; Wang et al., 2024). At the same time, we are particularly interested in whether the magnitude of these reactions differs across the two cases.

3. Event study results

The results of the event study for the ASF outbreaks in China and Germany on the CAR of the MSCI ACWI SAP IMI are presented in the following Section. The event day for the outbreak in Germany is September 10, 2020, the day the outbreak is first reported, while the event day for the outbreak in China is October 21, 2020, the day the outbreak is first reported in China. In the preferred specification, we use an estimation window of 245 trading days, equivalent to one year, and an event window of five days. Additionally, we provide the point estimates and 95% confidence intervals.

3.1 Event study results – China

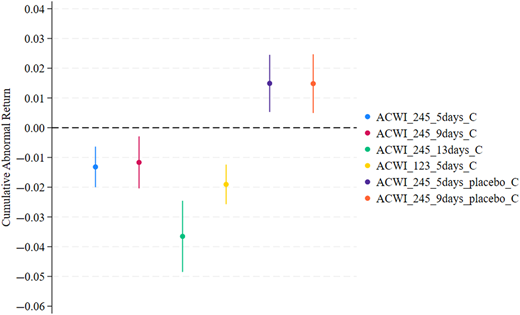

Focusing on the graphical representation of the results of the ASF outbreak in China in Figure 3, the ASF outbreak led to a statistically significant negative CAR in our preferred estimation specification, which uses an estimation window of 245 days and an event window of five days. Increasing the event window from five to 13 days, while keeping the estimation window at 245 days, resulted in an increase in the effect size, and the results remained statistically significantly negative. Using the shorter event windows closer to the event dates reduces the influence of other events or market turbulence such as COVID-19. The main findings are robust to the extraordinary market conditions of 2020.

Results of the event study: outbreak of the Chinese ASP (October 22, 2020). Note: ACWI refers to MSCI ACWI SAP IMI. Point estimates (see points in Figure) and 95% confidence intervals (see lines in Figure) are presented. Heteroskedasticity-robust standard errors are applied. The results are also presented in Appendix. Source: Own illustration

Results of the event study: outbreak of the Chinese ASP (October 22, 2020). Note: ACWI refers to MSCI ACWI SAP IMI. Point estimates (see points in Figure) and 95% confidence intervals (see lines in Figure) are presented. Heteroskedasticity-robust standard errors are applied. The results are also presented in Appendix. Source: Own illustration

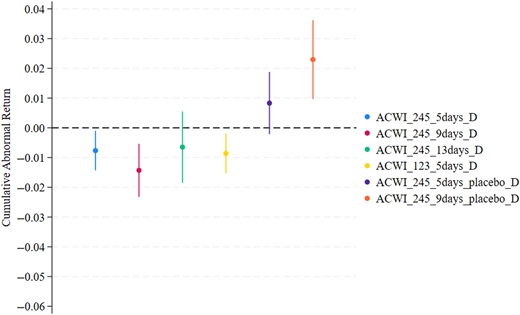

Focusing on the robustness of the results of the ASF outbreak in China in Figure 3 and Table A.1 in Appendix, decreasing the estimation window from 245 days to 123 days and using an event window of five days does not change the effect of the ASF outbreak on the MSCI ACWI SAP IMI. The effect size even increases compared to the results with the 245-day estimation window using five and 9 day as the event window. When we focus on the placebo regressions, we see that the results for the estimation window of 245 days and event windows of five and nine days are positive and statistically significantly. As the estimated coefficients are different in the direction, the magnitude and the level of statistical significance in the placebo period, these tests strengthen the validity of the original findings by highlighting that they are not confounded by seasonal fluctuations. The positive CARs during the placebo period may reflect other market dynamics unrelated to ASF outbreaks, especially given the complex, interconnected nature of global agribusiness markets. Based on the results and the robustness checks, we can conclude that the ASF outbreak in China had a statistically significant negative effect on the CAR of the global MSCI ACWI SAP IMI. The two placebo estimations reduce seasonality concerns, strengthening the argument that the preferred estimates capture the specific stock market response due to the ASF outbreak in China.

Comparing these results to those of Xiong et al. (2021), who used an event study to analyze the stock price response of ten Chinese pork firms and fifteen global hog firms from eight exporting countries, reveals important differences. Their findings, which are based on a relatively small and selective subset of companies, showed positive CARs for pork firms following the ASF outbreak in China (Xiong et al., 2021). In contrast, this study uses a broader global agribusiness index (MSCI ACWI SAP IMI), which includes firms from multiple countries and sub-industries beyond hog producers. The difference in scope is key, while Xiong et al. (2021) capture localized positive effects on Chinese hog firms benefiting from supply shortages and price increases, this study identifies overall negative market reactions across a wider range of agribusiness firms facing risks related to supply chain disruptions, regulatory uncertainty, and international trade effects. Thus, the negative CARs reflect broader market concerns and risk spillovers beyond the immediate gains to hog producers.

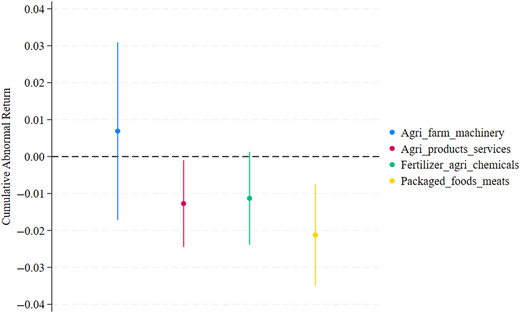

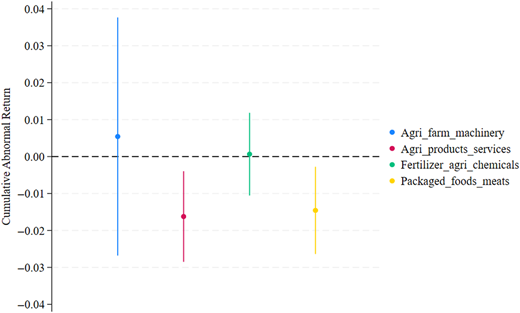

To investigate which of the four sub-industries of the MSCI ACWI SAP IMI drive the effect of the ASF outbreak in China, we ran the event study, as introduced in equation (3), separately for the following sub-industries: agricultural and farm machinery, agricultural products and services, fertilizers and agricultural chemicals, and packaged foods and meats, using the preferred specification of a 245-day estimation window and 5 event days. The results are graphically represented in Figure 4 and also shown in Table A.3 in Appendix. As shown, the negative and statistically significant CAR in the MSCI ACWI SAP IMI is driven by the sub-industries of agricultural products and services and packaged foods and meats. The CAR for the other two sub-industries, agricultural and farm machinery and agricultural chemicals, remains statistically insignificant. The findings of the sub-sector event study focusing on four agribusiness sub-industries suggest that companies directly involved in the production and processing of animal products are more vulnerable to ASF-related market shocks. In contrast, firms providing agricultural inputs or equipment appear less affected, which may indicate that ASF affects stock performance mainly through disruptions in the animal products supply chain rather than through the broader agricultural input sectors.

Results of the event study: outbreak of the Chinese ASP (October 22, 2020) - Results by sub-industry. Note: Sub-industry 1 is agricultural and farm machinery, sub-industry 2 is agricultural products and services, sub-industry 3 is fertilizer and agricultural chemicals, and sub-industry 4 is packaged foods and meats. Point estimates (see points in Figure) and 95% confidence intervals (see lines in Figure) are presented. Heteroskedasticity-robust standard errors are applied. The results are also presented in Appendix. Source: Own illustration

Results of the event study: outbreak of the Chinese ASP (October 22, 2020) - Results by sub-industry. Note: Sub-industry 1 is agricultural and farm machinery, sub-industry 2 is agricultural products and services, sub-industry 3 is fertilizer and agricultural chemicals, and sub-industry 4 is packaged foods and meats. Point estimates (see points in Figure) and 95% confidence intervals (see lines in Figure) are presented. Heteroskedasticity-robust standard errors are applied. The results are also presented in Appendix. Source: Own illustration

Running the analysis, as introduced in equation (3), of the shocks separately for the MSCI ACWI IMI by its regional components (North America, Europe, and Asia) reveals notable differences across regions. The negative CARs observed for the Chinese ASF outbreak observed before at the aggregate level turn positive and statistically significant for North American firms. In contrast, the responses of Asian and European firms are smaller and generally not statistically significant. Detailed estimates are reported in Table A.5 of Appendix.

3.2 Event study results – Germany

Focusing on the graphical representation of the results of the ASF outbreak in Germany in Figure 5, the outbreak led to a statistically significant negative CAR in our preferred estimation specification, which uses an estimation window of 245 days and an event window of five days. Increasing the event window from five to nine days, while keeping the estimation window at 245 days, resulted in an increase in the effect size, and the results remained statistically significantly negative. However, further increasing the event window to 13 days, still using an estimation window of 245 days, caused the effect to become statistically insignificant. This result is expected because the larger the event window, the more other events affect the stock markets, which in turn makes it difficult to estimate the specific effect of the ASF outbreak. Using shorter estimation windows closer to the event dates reduces the influence of earlier 2020 market turbulence.

Results of the event study: outbreak of the German ASP (September 10, 2020). Note: ACWI refers to MSCI ACWI SAP IMI. Point estimates (see points in Figure) and 95% confidence intervals (see lines in Figure) are presented. Heteroskedasticity-robust standard errors are applied. The results are also presented in Appendix. Source: Own illustration

Results of the event study: outbreak of the German ASP (September 10, 2020). Note: ACWI refers to MSCI ACWI SAP IMI. Point estimates (see points in Figure) and 95% confidence intervals (see lines in Figure) are presented. Heteroskedasticity-robust standard errors are applied. The results are also presented in Appendix. Source: Own illustration

Focusing on the robustness of the results of the ASF outbreak in Germany in Figure 5 and Table A.2 in Appendix, using an event window of five days and decreasing the estimation window from 245 days to 123 days does not change the effect of the ASF outbreak on the MSCI ACWI SAP IMI. When we focus on the placebo regressions using an event window of five days and an estimation window of 245 days, but with the event date set one year after the actual event date, we see that the results are positive and statistically insignificant. Increasing the event window from five to nine days in the placebo regression yields positive and statistically significant effects. Again, as the estimated coefficients are different in magnitude and level of statistical significance in the placebo period, these tests strengthen the validity of the original findings by confirming that they are not confounded by seasonal fluctuations. Based on the results and the robustness checks, we can conclude that the ASF outbreak in Germany had a statistically significant negative effect on the global MSCI ACWI SAP IMI. Again, the placebo regressions reduce concerns regarding the seasonality of the indices that drive these effects and strengthen the argument that we capture the specific stock market response due to the ASF outbreak in China.

To investigate which of the four sub-industries of the MSCI ACWI SAP IMI drive the effect of the ASF outbreak in Germany, we ran the event study, as introduced in equation (3), with our preferred specification (an event window of five days and an estimation window of 245 days) separately for the following sub-industries: agricultural and farm machinery, agricultural products and services, fertilizers and agricultural chemicals, and packaged foods and meats. The results are graphically represented in Figure 6 and also shown in Table A.4 in Appendix. The negative and statistically significant CAR in the MSCI ACWI SAP IMI is primarily driven by the sub-industries of agricultural products and services and packaged foods and meats, firms directly involved in animal production and processing. These sectors are most immediately affected by ASF-related disruptions in the pork supply chain, regulatory responses and heightened market uncertainty. In contrast, input-supplying sub-industries such as agricultural and farm machinery and agricultural chemicals exhibit no statistically significant CAR, suggesting a lower sensitivity to ASF shocks. This pattern mirrors the response observed during the Chinese ASF outbreak, reinforcing the interpretation that market effects are concentrated among firms closely linked to animal protein production rather than the broader agricultural sector.

Results of the event study: outbreak of the German ASP (September 10, 2020) - results by sub-industry. Note: Sub-industry 1 is agricultural and farm machinery, sub-industry 2 is agricultural products and services, sub-industry 3 is fertilizer and agricultural chemicals and sub-industry 4 is packaged foods and meats. Point estimates (see points in Figure) and 95% confidence intervals (see lines in Figure) are presented. Heteroskedasticity-robust standard errors are applied. The results are also presented in Appendix. Source: Own illustration

Results of the event study: outbreak of the German ASP (September 10, 2020) - results by sub-industry. Note: Sub-industry 1 is agricultural and farm machinery, sub-industry 2 is agricultural products and services, sub-industry 3 is fertilizer and agricultural chemicals and sub-industry 4 is packaged foods and meats. Point estimates (see points in Figure) and 95% confidence intervals (see lines in Figure) are presented. Heteroskedasticity-robust standard errors are applied. The results are also presented in Appendix. Source: Own illustration

Running the analysis, as introduced in equation (3), separately for the MSCI ACWI IMI agricultural index by regional components (North America, Europe, and Asia) again shows that the negative CARs following the German ASF outbreak announcements are primarily driven by firms listed in North America. Responses among Asian and European firms are smaller and generally not statistically significant, indicating that the overall index reaction is largely shaped by the North American component. Detailed estimates are provided in Table A.6 of Appendix.

Comparing the magnitudes of the effects for our preferred estimation specifications (an event window of five days and an estimation window of 245 days), one can see that the CAR in response to the announcement of the Chinese ASF outbreak is larger than the CAR in response to the German ASF outbreak. The 95% confidence interval for the German ASF outbreak ranges between −0.014 and −0.001, while it ranges between −0.020 and −0.006 for the announcement of the ASF outbreak in China. Interpreting these confidence intervals, a CAR of −0.014 to −0.001, observed for the German ASF outbreak, corresponds to an abnormal decline in value of 1.4%–0.1%, indicating a modest negative market reaction to the event. This means the stock price fell about 0.1%–1.4% more than expected during the event window, reflecting investors’ negative response. Similarly, a CAR of −0.020 to −0.006, observed for the Chinese ASF outbreak, corresponds to an abnormal decline in value of 2.0% to 0.6%, indicating a more pronounced negative market reaction. A decline of up to 2% in a globally diversified agricultural index entails considerable market value losses, illustrating the material economic repercussions of ASF outbreaks for investors and the agricultural industry. Additionally, the sub-industry of packaged foods and meats reacted more strongly to the ASF outbreak reported in China compared to the outbreak reported in Germany.

Placing these results into the broader literature, we compare the magnitudes of the ASF-related CARs to those observed around other well-documented agricultural and macroeconomic shocks, including major COVID-19-related announcements in 2020 (e.g. Nguemgaing and Sant’Anna, 2022; Höhler and Lansink, 2021) and key market reactions to the Russia–Ukraine invasion (Höhler et al., 2024). Evidence from the COVID-19 pandemic suggests that nationwide announcements did not generate statistically significant average CARs for meat processing companies in the United States, although individual firms experienced temporary negative CARs around specific events (Nguemgaing and Sant’Anna, 2022). At the broader market level, the most severe phase of the COVID-19 pandemic was associated with substantial declines in cumulative stock returns, with reductions of around 24–33% points across firms in the “fever” phase (February 24 to March 20, when the first coronavirus deaths in Italy were reported) and the “below-peak” phase (March 23 to April 29) (Höhler and Lansink, 2021). Similarly, the Russia–Ukraine invasion triggered negative cumulative average abnormal returns (CAAR) across several agri-food sectors, including −4.9% for agricultural machinery, −1.5% for packaged foods and meats, and −5.9% for soft drinks (Höhler et al., 2024).

4. Discussion and implications

4.1 Understanding market responses

This article contributes to the literature on heterogeneous firm responses within the agricultural sector to different types of shocks, including animal disease outbreaks (e.g. Korean FMD, ASF), trade conflicts, the COVID-19 pandemic and the Russian invasion of Ukraine (Pendell and Cho, 2013; Xiong et al., 2021, 2023; Höhler and Lansink, 2021; Höhler et al., 2024; Nguemgaing and Sant’Anna, 2022). By identifying the mechanisms driving investor behavior and market dynamics, the analysis provides a basis for more targeted strategies, such as improved risk assessment, to mitigate the economic effects of ASF and similar shocks. The research demonstrates substantial market responses to ASF outbreaks within the agricultural sector. The German ASF outbreak triggered a market reaction with CAR between −0.1% and −1.4%, while the Chinese outbreak caused a stronger negative effect, with CARs ranging from −0.6% to −2.0%. Given the large market capitalization and diversified composition of the MSCI ACWI SAP IMI, even CARs of this magnitude can correspond to economically meaningful changes in aggregate market value. In practical terms, a 1–2% decline in a globally diversified agricultural index represents substantial losses in market value, underscoring the real economic consequences of ASF outbreaks for investors and the broader agricultural sector [12].

The market response to the ASF outbreak in China differed in magnitude from the response in Germany, even within the same agricultural sub-industries. The stronger negative effects observed in China suggest that regional factors, such as production scale, market importance, and information dissemination, shape investor behavior and market dynamics (Gao et al., 2022). As the world’s largest pork producer and consumer (USDA, 2024), China is particularly vulnerable to ASF-related disruptions, which likely led investors to anticipate more severe supply chain shocks and financial losses, resulting in larger negative CARs. In contrast, although the German outbreak also generated statistically significant negative CARs, the magnitude was smaller, albeit still economically meaningful. This more muted response likely reflects the relatively lower importance of pork production within Germany’s agricultural sector. Differences in information transparency may further contribute to these patterns. Evidence suggests that the initial ASF outbreak in China in 2018 was not communicated fully or transparently (Gale et al., 2023; Inouye, 2019), potentially amplifying market uncertainty. In contrast, more transparent and timely information dissemination in Germany may have facilitated faster market adjustment, leading to smaller observed CARs.

Höhler et al. (2024) show that firms in the food value chain were negatively impacted by the Russian invasion of Ukraine. Stock prices of brewers, packaged food and meats, soft drinks and tobacco firms were negatively affected by the invasion, which is in line with the results of the ASF outbreak and the observed responses in our analysis. Regarding our analysis, the observed impacts on agricultural products and services firms, beyond just packaged foods and meat companies, highlight the interconnected nature of the agricultural sector. This suggests that investors anticipate ripple effects throughout the agricultural supply chain, not just in directly pork-related businesses. However, Höhler et al. (2024) also show that fertilizers and agrochemicals firms overall achieved higher profitability in 2022 compared to previous years.

4.2 Assessing sector vulnerability

The analysis of sub-industries within the MSCI ACWI SAP IMI reveals that the agricultural products and services and packaged foods and meats segments drive the statistically significant negative CARs for the outbreak in China and Germany. This indicates a higher vulnerability to the effects of ASF outbreaks in these sub-industries, which are directly involved with animal products (like packaged meat). This differential effect can be attributed to several factors: (1) Supply chain positioning: sectors directly linked to pork production, such as packaged foods and meats, face immediate challenges in sourcing and pricing, while machinery and fertilizer companies are more insulated from these direct effects [13]. (2) Revenue dependency: firms in the packaged foods, meats & agricultural products and services sectors derive a larger portion of their revenue from pork-related products or services, making them more vulnerable to ASF-related market shocks. (3) Flexibility in product substitution: packaged foods and meat companies may struggle to quickly replace pork with alternative protein sources, especially in markets with strong pork consumption preferences, whereas machinery and fertilizer products are often applicable across various agricultural sectors. (4) Investor perceptions: the stronger market reaction in certain sectors may reflect investors' viewing these industries as more indicative of ASF’s economic effect. (5) Geographical considerations: the larger reaction to the Chinese outbreak likely reflects China’s dominant position in global pork production and consumption, with companies heavily exposed to the Chinese market perceived as particularly vulnerable.

Putting our results into a bigger context, these findings are partly in line with Höhler and Lansink (2021), who show that the coronavirus disease led to a reaction in the stock market, highlighted by increased price volatility in the stock prices of food distributors. Höhler and Lansink (2021) also observe that low price volatility was found in the stocks of food retailers. This contrasts with the results of the ASF outbreak we presented in the previous Section, where our findings indicate that companies listed in these sub-industries of packaged food and meats were statistically significantly negatively affected by the ASF outbreak in China and Germany. This highlights that different sub-industries respond differently to various kinds of shocks.

4.3 Policy implications

The substantial market repercussions documented in our study underscore the need for robust policy frameworks to mitigate the economic effects of animal disease outbreaks. Policies promoting rapid reporting and containment can limit market disruptions, as timely detection helps prevent local outbreaks from escalating into wider epidemics. This highlights the critical role of public institutions in raising awareness before and during ASF outbreaks, as noted by Kashyap et al. (2024). Initiatives such as the “African Swine Fever (ASF) – Situation Reports” provided by the World Animal Health Information System (WAHIS) offer essential updates on the disease globally and regionally, based on official country submissions (WOAH, 2025). Strengthening such systems ensures timely and accurate information sharing, while enhancing disease control authorities’ capacity, through additional staff and financial resources, can reduce severe sector-wide consequences, even if it imposes short-term burdens on individual farmers. Finally, policies fostering cross-border collaboration, particularly in regions like Europe and Asia, are crucial for sharing best practices and coordinating emergency responses, thereby improving preparedness for future outbreaks.

4.4 International comparisons

The above-mentioned difference in market reaction highlights the need for globally oriented risk assessment strategies that account for the varying importance of national markets in the global pork supply chain. The differential effects observed between these two major pork-producing countries also provide insights into the role of market structure and regulatory environments in shaping economic resilience to disease outbreaks. Germany, as part of the EU, operates within a different regulatory framework compared to China, which may influence both the spread of diseases and the market’s response to outbreaks. These comparative results have implications for multinational companies and investors, informing more sophisticated risk assessment and portfolio management strategies. Companies operating in both European and Asian markets might need to adjust their risk mitigation strategies to account for these regional differences in market sensitivity to ASF outbreaks. Furthermore, the comparison offers valuable lessons for other pork-producing and consuming countries. It suggests that the economic effect of an ASF outbreak may vary considerably based on a country’s position in the global pork market, its regulatory environment and its integration with global agricultural supply chains. This international perspective emphasizes the need for tailored approaches to disease management and economic support measures across different regions. It also underscores the importance of international cooperation in disease prevention and control, as the economic repercussions of outbreaks clearly transcend national borders.

5. Conclusion

This study provides novel insights into the global economic effect of ASF outbreaks on agricultural stock markets by analyzing globally diversified agricultural equity indices. This approach captures broader market spillovers and allows us to assess how outbreaks in major pork markets affect global agribusiness portfolios and subsectors. Using an event study methodology on the MSCI ACWI SAP IMI, we find that ASF outbreaks in China and Germany produced statistically significant negative CARs, with the effect more pronounced for the outbreak in China. The German outbreak triggered CARs between −0.1% and −1.4%, while the Chinese outbreak generated larger negative returns, ranging from −0.6% to −2.0%. We interpret these results as robust associations. We further interpret that these market reactions reflect broader economic consequences, including reduced investor confidence in related industries. Given the large capitalization and diversified composition of the MSCI ACWI SAP IMI, even modest CARs translate into economically meaningful changes in aggregate market value. Such magnitudes are consistent with event studies on sectoral or diversified indices, where cross-firm and cross-regional diversification typically dampens the price response to sector-specific shocks (e.g. Oberndorfer et al., 2013).

This study makes several novel contributions to the literature on the economic effects of animal disease outbreaks. First, by utilizing the MSCI ACWI SAP IMI, we provide the first comprehensive analysis of ASF’s effect on the global agricultural sector as a whole and for its sub-industries. Second, our comparison of China and Germany offers unique insights into how ASF outbreaks affect major importing versus exporting countries differently. Third, our sub-industry analysis reveals important variations in vulnerability across different agricultural sectors. These findings advance the understanding of how animal disease outbreaks affect global markets. In detail, the findings highlight the vulnerability of the global agricultural sector to animal disease outbreaks and underscore the importance of effective disease prevention and management strategies. The differential effects observed between China and Germany emphasize the need for context-specific approaches in addressing such outbreaks, taking into account factors such as market size, production scale and information dissemination practices. The sub-industry analysis reveals that the agricultural products and services and packaged foods and meats segments are particularly susceptible to ASF-related market shocks.

The goal of this analysis is to understand specific ASF outbreaks and their immediate associated market consequences. The study is a comparative case analysis between China and Germany and these two specific ASF outbreaks. Hence, we avoid making any generalizable claims about all ASF events globally. The insights derived pertain to how these particular outbreaks affected globally diversified agricultural equity indices, while recognizing that responses to other ASF outbreaks could differ depending on timing, location, and market conditions. Future research incorporating additional outbreaks, as data availability improves, could further strengthen the external validity of these results. Furthermore, this work could be extended by examining the longer-term effects of animal disease outbreaks on financial markets and the broader economy, including potential structural changes in the affected industries. In addition, future studies could explore the effectiveness of various policy interventions, such as market support programs, trade regulations, public communication strategies and biosecurity measures, in mitigating the economic fallout. Comparative analyses across countries or regions with different institutional capacities and policy responses could provide valuable insights into best practices for managing future outbreaks and enhancing resilience in the agri-food sector.

Notes

Wang et al. (2020) evaluate the effect of different supply chain disruption scenarios (including shortages and price jumps in corn supply, shortages of market hogs to packing facilities, disruptions in breeding stock adjustments and disruptions in pork imports) on the Chinese hog market to simulate and project the effect of COVID-19 on hog production and pork consumption in China. Wang et al. (2023) introduce a shocks, cycles and adjustments (SCA) model to assess the effect of various shock scenarios, including a further wave of ASF, on China’s hog market, revealing that while production and economic adjustment lags lead to predictable hog cycles, external shocks cause irregular cycles with varying phases and amplitudes.

China reported the first confirmed ASF outbreak in August 2018 (Chand, 2020). In Germany, the first case of ASF in wild boar was confirmed in September 2020 (Sauter-Louis et al., 2022).

ASF has never been detected in Canada and the United States (Kashyap et al., 2024; Government of Canada, 2025).

In China, many policies aimed at reducing future ASF outbreaks are being developed and tested. For example, Gao et al. (2022) investigate Chinese hog farmers’ willingness to adopt genomics technology to breed ASF-resistant hogs, finding that while most farmers are risk-averse, they would adopt the technology if it considerably reduced the risk of infection.

The MSCI data contained here is the property of MSCI INC. (MSCI). MSCI, its affiliates and its information providers make no warranties with respect to any such data. The MSCI data contained herein is used under license and may not be further used, distributed or disseminated without the express written consent of MSCI.

Germany accounts for 0.20% and China for 1.50% of the index weights.

While the U.S. Senate voted down a $300 billion stimulus package on September 10, 2020, much of the information about the bill’s prospects had been widely discussed in the media beforehand (see, for example, Washington Post (2020), a major U.S. newspaper). As a result, stock prices likely incorporated this information prior to the final vote, reducing the likelihood that the Senate decision itself confounded the observed abnormal returns around the German ASF announcement. Hence, following Fama (1970)’s efficient market hypothesis, these information have already been incorporated by the market actors.

The MSCI ACWI SAP IMI contains approximately 25% of companies listed in the MSCI ACWI Agriculture and Food Chain Index (as of March 2023).

While parts of the event study literature increasingly rely on intraday data to isolate market reactions from within-day noise, this approach requires precise time stamps for the disclosure of the event. In our case, ASF outbreak information is only publicly identifiable at the daily level, which prevents the construction of intraday event windows. For this reason, and consistent with studies using daily data for events with date-level disclosure, we focus on daily abnormal returns rather than shorter intraday intervals.

Formally, the market model is specified as:

(2)

where Ri,t is the return of the agricultural index on day t, Rm,t is the return of the market benchmark, αi and βi are estimated over the pre-event estimation window and ϵi,t is the error term. The market return in our specification corresponds to the return of the MSCI ACWI IMI.

Given evidence of selective placebo reporting (Dreber et al., 2024), we follow the convention in the literature and implement a one-year placebo test.

The magnitude is similar to other event studies focusing on stock markets, such as Oberndorfer et al. (2013) for German firms and Hwang (2013) for U.S pharmacy firms.

For more information about Chinese pork supply chain networks, see Cai et al. (2020).

The supplementary material for this article can be found online