The purpose of this paper is to show the existence results for adapted solutions of infinite horizon doubly reflected backward stochastic differential equations with jumps. These results are applied to get the existence of an optimal impulse control strategy for an infinite horizon impulse control problem.

The main methods used to achieve the objectives of this paper are the properties of the Snell envelope which reduce the problem of impulse control to the existence of a pair of right continuous left limited processes. Some numerical results are provided to show the main results.

In this paper, the authors found the existence of a couple of processes via the notion of doubly reflected backward stochastic differential equation to prove the existence of an optimal strategy which maximizes the expected profit of a firm in an infinite horizon problem with jumps.

In this paper, the authors found new tools in stochastic analysis. They extend to the infinite horizon case the results of doubly reflected backward stochastic differential equations with jumps. Then the authors prove the existence of processes using Envelope Snell to find an optimal strategy of our control problem.

1. Introduction

The main motivation of this paper is to prove the existence of an optimal strategy which maximizes the expected profit of a firm in an infinite horizon problem with jumps. More precisely, let a Brownian motion and an independent Poisson measure defined on a probability space and let be the right continuous complete filtration generated by the pair . Assume that a firm decides at stopping times to change its technology to determine its maximum profit. Let be the possible technologies set. A right continuous left limited stochastic process X models the firm log value and a process taking its values in models the state of the chosen technology. The firm net profit is represented by a function f, the switching technology costs are represented by and is a discount coefficient. Then, the problem is to find an increasing sequence of stopping times where optimal for the following impulse control problem

where denotes the set of admissible strategies. The Snell envelope tools show that the problem reduces to the existence of a pair of right continuous left limited processes . This idea originates from Hamadène and Jeanblanc [1]. Their results are extended to infinite horizon case and mixed processes (namely jump-diffusion with a Brownian motion and a Poisson measure). In [1] the authors considered a power station which has two modes: operating and closed. This is an impulse control problem with switching technology without jump of the state variable. They solved the starting and stopping problem when the dynamics of the system are the ones of general adapted stochastic processes.

The existence of is established via the notion of doubly reflected backward stochastic differential equation. In this context, another interest of our work is to extend to the infinite horizon case the results of doubly reflected backward stochastic differential equations with jumps. Specifically, a solution for the doubly reflected backward stochastic differential equation associated to a stochastic coefficient a null terminal value and a lower (resp. an upper) barrier is a quintuplet of -progressively measurable processes which satisfies

where is the compensated measure of

Another specificity of this paper is to promote a constructive method of the solution of a BSDEs with two barriers. Specifically, we do not assume the so called Mokobodski's hypothesis. Indeed this one is not so easy to check (see e.g. [2] in finite horizon and continuous case). Our assumptions are more natural and easy to check on the barriers in practical cases.

The notion of backward stochastic differential equation (BSDE) was studied by Pardoux and Peng [3] (meaning in such a case and ). To our knowledge, they were the first to prove the existence and uniqueness of adapted solutions, under suitable square-integrability and Lipschitz-type condition assumptions on the coefficients and on the terminal condition. Several authors have been attracted by this area that they applied in many fields such as Finance [1, 4–6], stochastic games and optimal control [7–10], and partial differential equations [11].

The existence and the uniqueness of BSDE solutions with two reflecting barriers and without jumps have been first studied by Cvitanic and Karatzas [4] (generalization of El Karoui et al. [5]) applied in Finance area by El Karoui et al. [6]. There is a lot of contributions on this subject since then, consisting essentially in weakening the assumptions, adding jumps and considering an infinite horizon.

The extension to the case of BSDEs with one reflecting barrier and jumps has been studied by Hamadène and Ouknine [8] considering a finite horizon . The authors show the existence and uniqueness of the solution using the penalization scheme and the Snell envelope tools. They stress the connection between such reflected BSDEs and integro-differential mixed stochastic optimal control. The authors' assumptions are: the terminal value is a square integrable random variable, the drift coefficient function is uniformly Lipschitz with respect to and the obstacle is a right continuous left limited process whose jumps are totally inaccessible. Hamadène and Ouknine [12] deal with reflected BSDEs in finite horizon, the barrier being right continuous left limited and progressively measurable. Hamadène and Hassani [9] proved existence and uniqueness results of local and global solutions for doubly reflected BSDEs driven by a Brownian motion and an independent Poisson measure in finite horizon. The authors applied these results to solve the related zero-sum Dynkin game.

Here the model is inspired from the papers [5, 8–10, 12]. But their results do not apply directly to the situation which here requires an infinite horizon. Moreover we connect the reflected BSDE with the impulse control problem. All these papers provide a solution to the reflected BSDE problem which are here extended to the case of infinite horizon by adding a discount coefficient and imposing admissibility conditions of strategies. In this paper, the drift function is assumed to be Lipschitz and non-increasing in It is proved that the reflected BSDE solutions are limit of Cauchy sequences in appropriate complete metric spaces. Another interesting area is the one of oblique reflections, meaning a multimodal switching problem, see for instance [13–15]. El Asri [14] considers the same problem proposed by Hamadène and Jeanblanc [1] and extends it to the infinite horizon case without jump of the state variable, namely a power station which produces electricity and has several modes of production (the lower, the middle and the intensive modes). Naturally, the switching from one mode to another induces costs. The optimal switching problem is solved by means of probabilistic tools such as the Snell envelop of processes and reflected backward stochastic differential equations. Moreover their proofs are based on the verification theorem and the system of variational inequalities that we do not use.

Our purpose is similar to the one in [16], but instead of using Snell envelope and fixed point theorem as they do, here the two barriers case is solved using comparison theorem in one barrier case and adding some assumptions on the drift coefficient g.

This paper is composed of six sections. Section 2 presents the impulse control problem and describes the corresponding model. Section 3 introduces a pair of right continuous left limited processes that allows one to exhibit an optimal strategy. Section 4 extends the doubly reflected BSDEs tools in the infinite horizon setting with jumps: first the case of a single barrier with general Lipschitz drift is solved, then a comparison theorem is proved, finally the uniqueness and the existence of solution for the doubly reflected BSDE under suitable assumptions are proved in case of drift non depending on state . Section 5 proves the existence of the required pair , and provides an application of these doubly reflected BSDE to a switching problem. Finally, with some simulations, the results allow to define an optimal strategy in Section 6. An appendix is devoted to an extension of Gronwall's lemma and some technical results.

2. Preliminaries and problem formulation

Let be a filtered complete probability space with a right continuous complete filtration generated by the two following mutually independent processes:

dimensional Brownian motion

a point process associated with a Poisson random measure μ on where for some endowed with its Borel σ-algebra , with compensator for a σ-finite measure λ on denotes the compensated measure associated with

Assume that a firm decides at random times to switch the technology in order to maximize its profit: the firm switches from the technology 1 to the technology 2 along a sequence of stopping times. An impulse control strategy is defined as a sequence where is a sequence increasing to infinity of -stopping times with . The sequence models the impulse time sequence of the system as follows: for every is the time when the firm moves from technology 1 to technology 2 and is the time when the firm goes from 2 to 1. A càdlàg process taking its values in is defined by

Given and a measurable map such that

the firm value is defined as where is the càdlàg process

where is the initial condition, and are two measurable functions satisfying the K-Lipschitz condition (thus the sublinear growth condition).

The instantaneous net profit of the firm is given in terms of a positive function f, depending on the technology in use and the value of the firm. Let and be the positive switching technology costs, if one passes from technology i to technology with regular enough assumptions which will be specified later. One considers a discount coefficient then, the profit associated with a strategy α is defined as

and the expected profit of the firm is defined by

The strategy is admissible if:

belong to We denote by the set of admissible strategies.

Here, the impulse control problem is to prove the existence of an admissible strategy which maximizes the expected profit:

The following notations will be used:

the σ algebra of -predictable sets on

Class [D] :

3. The impulse control problem

Section 5 shows that the problem reduces to the existence of a pair of càdlàg processes using the Snell envelope tools: this idea originates from Hamadène and Jeanblanc [1]. The existence of is established in Section 5 via the reflected BSDEs tools. Indeed, the solution of the reflected BSDE corresponds to the value function of an optimal stochastic control problem and these processes allow to build an optimal switching strategy. We based on [17] to use the fundamental optimal control concepts.

Assume that there exist two right continuous left limited, regular (meaning that the predictable projection coincide with the left limit) -valued processes and of class [D] and satisfying the properties

where are positive functions satisfying . Then Moreover, the strategy defined as follows:

is optimal for the impulse control problem (6).

The proof is based on the properties of the Snell envelope. The scheme of the proof is similar to the one in [18] and also [14, Appendix A, p. 246] as soon as the processes are regular. As a consequence of (7) and (8), remark that almost surely

4. Reflected BSDE with jumps and infinite horizon

In this section, the results from [10] are extended to infinite horizon reflected backward stochastic differential equations with general jumps, showing existence and uniqueness of an infinite horizon solution, imposing additional assumptions on the drift function and using appropriate estimates of the process Y. The following assumptions are done:

A map which is -progressively measurable and:

where the norm of is defined as

: An -progressively measurable map such that

Let the barriers and be -progressively measurable continuous real valued processes satisfying

To prove the existence of the solution for doubly reflected BSDE with jumps and infinite horizon, we first consider the case of a single barrier (Section 4.1) then a comparison theorem is proved in Section 4.2.

4.1 Reflected BSDE in case of a single barrier, infinite horizon

In this subsection, the case of infinite horizon reflected BSDE with one barrier and general jumps is considered.

Let be given. A solution of the reflected BSDE associated to is a quadruplet of processes satisfying for any :

, and ,

almost surely

- (3)

almost surely

- (4)

is a non-decreasing process satisfying and for any t

We then prove the following:

Let satisfy Hypotheses . Then there exists a unique process solution to the BSDE associated to .

Proof: (1) As a first step, the uniqueness of the solution is insured: if there exist two solutions, the proof of uniqueness is a standard one. For instance, look at Theorem 4.8 proof.

- (2)

Under the hypothesis Theorem 2.1 [10] can be applied: there exists a quadruplet verifying (actually restricted to ) and

Considering one has

Applying Itô's formula to the process between t and T yields

Using and and one has

so we get

Considering the decomposition: the Lipschitz property of the function g, the Cauchy-Schwarz inequality and the non-increasing property of the map for any and lead to

Thus for any

Remark that includes the jumps of the Poisson measure μ. So

Then, since and the third line in (16) is a martingale; thus taking the expectation of both sides with yields for any

On the one hand, Lemma 7.2 , we obtain for any T and any S:

On the other hand, we have

and from the Lipschitz property, we get

Using estimation (19), there exists a constant M, such that for any

If we subtract from the term we get

This implies that the expectation on the left tends to zero uniformly when is chosen small enough: indeed, since by Lebesgue's monotone convergence tends to 0 when T tends to infinity. Globally when T tends to infinity and we obtain using (19) that the sequence is a Cauchy sequence which converges in to the process . Thus Lemma 7.2 concludes that, t being fixed, is a Cauchy sequence in , its limit defines the -measurable random variable It is a family of random variables. We later prove that actually the limit Y is a process.

- (3)

Turning to Z and V, to deal with the convergence in respectively in , An argument similar to (63) shows that the sequence is a Cauchy sequence in , its limit defines a process Z which belongs to and is a Cauchy sequence in , its limit defines a process V which belongs to .

- (4)

We now prove that there exists a process which is the limit of a Cauchy sequence in .

(a) Coming back to (16), for all we get

The Burkholder-Gundy-Davis inequality gives the existence of a constant such that

for all . Similarly

Gathering these bounds yields

Choosing and such that using Lemma 7.2 and the facts that is a Cauchy sequence in , and is a Cauchy sequence in , then goes to 0 when S and T go to infinity.

- (5)

Now one proves the other items of the proposition: Item (2) According to (4.1) for all

and due to the almost sure convergence of a subsequence of and the continuity of the function g, the right hand side of Eqn (22) converges almost surely.

Thus is defined as the and almost sure limit of the right hand side of (22). Hence, for almost sure limit, we get the reflected BSDE (10).

Item (3) For any one has , and using almost convergence of a subsequence, one deduces Item (3).

On the one hand, for fixed the left continuous and right limited function is the uniform limit on of a sequence of step functions:

We now deal with the successive bounds

For fixed above, for any there exists such that

so the first and third terms in (24) are bounded

Remark that

We now fix and we remark that for any step function

Thus when T goes to infinity the second term in (24) satisfies

For any , using (25) and (26) the limit of (24) when T goes to infinity is bounded by This yields the fact that

Finally using (23) we get

Thus

which goes to 0 when T goes to infinity according to the convergence of to Y in and of in So the proof of (4) is done.

■

In case of a deterministic function g, meaning g is defined on , an alternative proof of Theorem 4.3 (under the same hypotheses) can be provided using penalization method, as for instance Section 6 in [6] concerning continuous case, but here directed by a pair Brownian motion-Poisson measure. We associate to where the function satisfies Assumption , since is obviously non decreasing and uniformly Lipschitz, the solution in of the following BSDE

Since is non decreasing, the standard comparison theorem proves that actually, for any fixed t is a non-decreasing sequence in , so it is almost surely and in convergent to the random variable Using similar arguments as those ones in (4.1) is a Cauchy sequence in so the limit defines the process Now it is standard [19] to prove the existence of a non decreasing process K such that

and the existence of such that

This alternative method allows us to prove the following result.

Under Hypotheses , g being defined on one has

Proof: The uniqueness of the solution (step (i) in the proof of Theorem 4.2) insures that this solution is the limit of the penalized Eqn (27): Y is the limit of the non-decreasing sequence

Reproducing Step 2 in the proof of Theorem 3.1 [16] leads for any k to

so is the Snell envelope of the process which is increasing almost surely towards the process Remark that both and J are of class since both are uniformly bounded with

Let us denote as the Snell envelope of process Y. Then Lemma A.1 in Appendix [10, 12] allows to commute the increasing limit and the essential supremum: on the left hand side, almost surely, on the right hand side which achieves the proof. ■

From now on, we consider a function g defined on satisfying Assumption

The following is an extension of Lemma 2.4 in [20]: in our case g is defined only on but the BSDE is directed by a mixed Brownian-Poisson process:

For let be the solution of the single barrier reflected BSDE associated to the barrier where and . Then almost surely for all

Proof: The proof is similar to the one in [18].

Let be the solution of the reflected BSDE associated to the barriers L and Then there exists a constant C such that

Proof: (1) By definition, we have

Using Itô's formula, one has

The last term on the right hand side of (32) is bounded: for any

Gathering these bounds and using Assumption yield

Let

Using extended Gronwall's Lemma 7.1 one has

Let us denote being a decreasing function.

(2)Coming back to (33) one has

■

4.2 Comparison theorem in case of a single barrier

The following proposition is an extension of Theorem 2.2 in [10] to infinite horizon.

Assume that and are solutions of the reflected BSDE with jumps (10) associated with and , satisfying Assumptions g being defined on being defined on and assume in addition that

Then, -almost surely.

If moreover is defined on then

Proof: Theorem 2.2 in [10] proves that for any almost surely, and in the case where does not depend on v,

Theorem 4.2 proof gives us the almost sure convergence of so the inequalities are preserved when T goes to infinity.■

Here we summarize the results concerning the reflected BSDEs: In case of a function g defined on satisfying the functions

satisfy Hypothesis : Lipschitz property and non increasingness with respect to y.

The -progressively measurable process which is the unique solution of the reflected BSDE associated with satisfies

- (2)

The -progressively measurable process which is the unique solution of the reflected BSDE associated with satisfies

Thank to Lemma 4.4, one has the following inequalities:

So as a consequence of Proposition 4.6, one has

4.3 Double barrier reflected BSDE with jumps and infinite horizon

Now one considers the problem of reflection with respect to two barriers L and U in the case of drift g being defined on and satisfying .

Let be given. A solution of the double reflected BSDE associated to is a quintuplet of processes satisfying for any :

and ,

almost surely

- (3)

almost surely

- (4)

are non-decreasing processes satisfying and for any t

Let satisfying Hypotheses , then there exists a unique solution to Eqn (4.7).

The proof is given in the following subsections.

4.3.1 Uniqueness of the solution

As a first result, one proves the uniqueness of solution when it exists.

If there exists a solution of (40) satisfying Items (1) to (4), it is unique.

Proof: The proof of uniqueness is detailed, even if it is really standard, for stressing the role of the assumption One assumes that there exist two solutions Then they satisfy

One has

Using Item (4) and the last line satisfies

since .

It follows that for any t

So , and as a consequence Thus there exists a finite variation process satisfying and But the assumption contradicts these equalities if : indeed as soon as and so would be equal to This concludes the proof of uniqueness.

4.3.2 Existence of the solution for double barrier reflected BSDE with jumps

Here one uses the so called penalization method: Let g satisfying be the drift parameter and introduce which obviously satisfies .

So according to Theorem 4.2, Hypothesis (H2) still being in force, for each there exists a unique solution of the reflected BSDE associated with , meaning

From Proposition 4.6, the sequence (resp ) is non increasing (resp. non-decreasing), let us denote their almost sure limits, consequence of monotonicity.

From the inequality it follows that belongs to for all

The proof of Theorem 4.8 is done in five steps.

Step 1: There exists a constant such that and one has

Its formula yields

By definition of the solution

Then, since , so

Thus, one has

Using the Cauchy-Schwarz inequality, for any , one has for any t and n

On the other hand, with (38), Lemmas 4.4 and 4.5, for any t and n one has:

Similarly for any one has

Note that the last line in the right hand side of (4.3) admits a zero expectation, and embedding the inequalities (44), (45) and (17) in the expectation of (4.3):

where k is the function defined as follows:

So one has

Gronwall's Lemma 7.1 is now used with and so

and

Then one has a bound for (46)

This bound and (44) end the proof.

Step 2: and

The proof is an adaptation of the one given in Step 3 [20, p. 169].

Let be the solution of the reflected BSDE with jumps associated to : so since and both applications and satisfy obviously Proposition 4.6 implies that -a-s and .

Let and ν be a stopping time such that: . Itô's formula is applied to the process between ν and :

This yields to

Using that, one has . This yields for any n:

Since U is right continuous then almost surely and in

In addition, one has

then due to Assumption

Finally with (38)

This last bound goes to 0 when n goes to infinity using Lebesque monotonous convergence Theorem. Consequently

Therefore P-a.s.

From this and “Section Theorem” [21, p. 220], it follows that, and then almost surely.

We now denote by the predictable projection for any X. Since , then and . So we deduce that , the semi-martingale U is regular and Lemma 7.3 proves that the processes are regular so . It follows that for all t almost surely.

Consequently, from a weak version of the Dini theorem [22, p. 202], one deduces that as Finally Lebesgue dominated convergence Theorem implies

Step 3: There exist an -adapted process and an -predictable process such that

By Itô's formula one has for any and for all t,

where denotes

Since then so

According to (7) in [20] so

Look at , product of going to 0 when in (Step 2) and of which is for all n bounded by the integrable random variable (see Lemma 4.4):

The second term in (49) is symmetrical and the sum is going to 0 in

It follows that and are Cauchy sequences in complete spaces then there exist processes Z and V, respectively -progressively measurable and -measurable such that the sequences and converge respectively toward Z in and V in .

Step 4: so defines a process in

Using and definitions, (so ) and applying Itô's formula between 0 and t to the process one has:

- (1)

First look at

For any the right hand side of this inequality is smaller than

which actually goes to 0 when n and p go to infinity using (50).

Concerning the supremum with respect to t of the absolute value of second line in (52) the Burkholder-Davis-Gundy and Cauchy-Schwarz inequalities are used: there exists a universal constant such that for any constant :

Similarly one has is an -martingale (see [8], p. 4) and once again the Burkholder-Davis-Gundy and Cauchy-Schwarz inequalities are used:

Using that and gathering all these bounds, it yields for any t:

Choosing c such that and using the limit (50), the processes , are Cauchy sequences respectively in and the almost surely convergent monotonous sequences , are Cauchy sequences in so is the sequence . Thus the sequence is a Cauchy sequence in This concludes Step 4 and proves item (1):

Moreover, since for all t is an almost sure limit of and is Cauchy sequence, one has two progressively measurable cadlag processes which are modification of each other so that is an -adapted right continuous left limited process belonging to .

Step 5: Existence of Item (4), Item (3)

By definition of for any and :

So, the right hand side of (53) converges almost surely and in to

and the non-decreasing process can be defined almost surely and in :

This proves Item (2) and the existence of the non-decreasing process in such that .

Then, using the differential of Equation (53) and multiplying by yield almost sure convergence:

The right hand side is almost surely finite since it is equal to

Remark that the sequence goes almost surely to and multiplied by n the limit cannot be finite unless thus Item (4) is proved:

Finally Item (3) is a consequence of

the fact for any n and and the almost sure convergence of sequence , so ,

above (55) gives .

5. Application to the impulse control problem with infinite horizon

In this section we use Proposition 3.1, and Theorem 4.8 with satisfying Assumption , a null terminal value, and barriers satisfying Assumptions . There exists a progressively measurable process such that:

So the main result can be proved: the existence of processes introduced in Proposition 3.1. This is the extension of Theorem 3.2 [1, p. 186] to the infinite horizon set up with jumps.

Assume that and are positive, satisfy , and satisfies . Then there exists a couple of -valued processes satisfying the assumptions in Proposition 3.1, in particular (7) and (8) meaning:

Proof: Theorem 4.8 is applied with . Since the random variables are integrable and satisfy , the following processes will be checked to satisfy Proposition 3.1 assumptions: are positive right continuous left limited regular processes of class [D] satisfying (7) and (8). The following processes are proposed:

First one remarks that as conditional expectation of non-negative random variables.

Second

are sum of an -martingale minus a right continuous left limited finite variation process so these processes are right continuous left limited.

- (3)

Third one has : indeed, using the facts that and are positive,

The facts that , Assumption and belongs to , proves that the martingale which bounds is uniformly square integrable. Thus Burkholder-Davis-Gundy inequality applied to this square integrable martingale M proves that As a byproduct, the process is of class [D] since for any stopping time θ,

One now turns to the checking of (7) and (8). Theorem 4.34 [23, p. 189], applied to the semi martingale with characteristics and there exists a couple of -progressively measurable processes such that for any t:

Using the third inequality of system (S), one has , and replacing by , one has Similarly, the fourth equality of system (S), meaning replacing by shows

As a result, the quadruplet satisfies the single barrier reflected BSDE:

Then Equality (29) in Proposition 4.3 is applied with Since the hypothesis is satisfied and one has

Similarly, using the third inequality of system (S), one has , and once again Equality (29) is used with Since , the hypothesis is satisfied and one has

hence the existence of the asked couple .

6. Numerical resolution

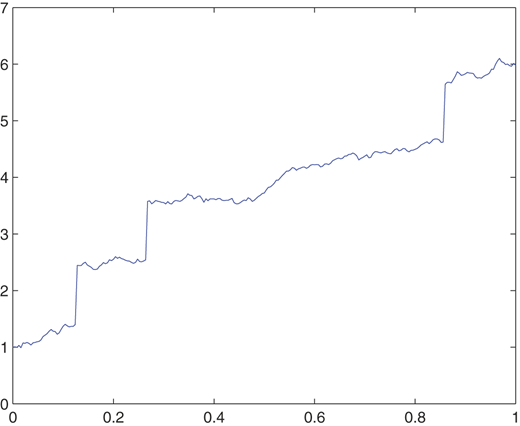

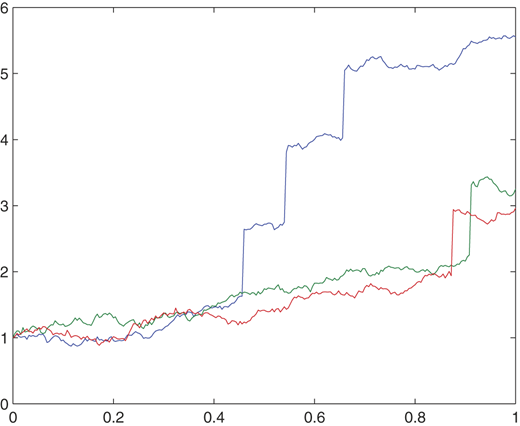

Recall that the optimal strategy is completely defined by the process Y and is obtained when Y reached successively the barriers L and U. As a result, solving numerically this strategy amounts to simulating sample path trajectories of the process Y. In recent years, several techniques have been proposed for the numerical solution of the process Y (for example the quantization algorithm, Malliavin calculus). Here the approximation by regression is chosen, which is well explained in [24, 25]. Our method is totally different from the method used in [26] which is based on the approximation of the Brownian and Poisson processes by a random walk. Recall once again that here the process X is the diffusion (4). For this application, a simple case of stochastic differential equation with jump is considered: Let are constant drift and diffusion coefficients; gives an information about the jump: the probability of the jump happening at time t and the relative amplitude of the jump. It will be represented by a log-normal random variables, λ is the yearly average of the number of jumps. Thus the firm log-value is modeled as

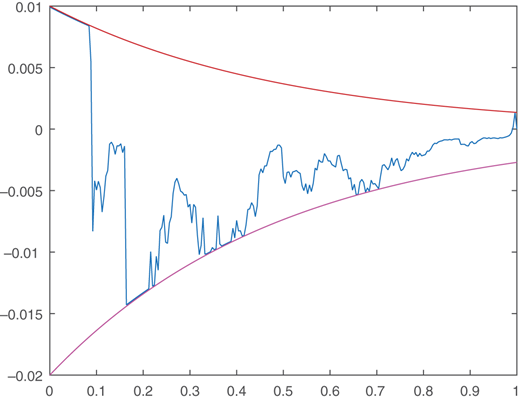

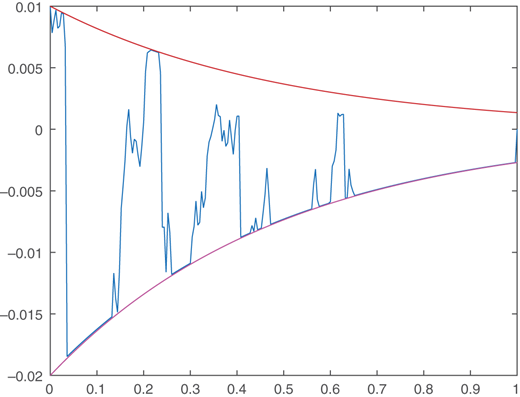

By using the classical Euler scheme for sample path trajectories of the process X where and , one has: (see Figures 1 and 2).

Let us now focus on our problem: namely, how to simulate the process Y, and therefore the optimal strategy. Recall that

which satisfy Hypotheses and .

First of all, when t tends to infinity, goes to 0, so a finite horizon T should be fixed such that More specifically, below the numerical samples show that as soon as the length of interval is negligible.

so the error is bounded by , the order of which being

To approximate the backward component the following discretization approximation scheme is introduced, for :

where To approximate the conditional expectation, here is adopted the Longstaff-Schwarz algorithm [25] which uses a regression technique (Least-Square Monte Carlo method). Taking the parameters , and the profits/costs functions

the evolution of Y is observed. Previously all the assumptions have to be checked:

- (1)

One notes that with : Assumption is satisfied since so thus

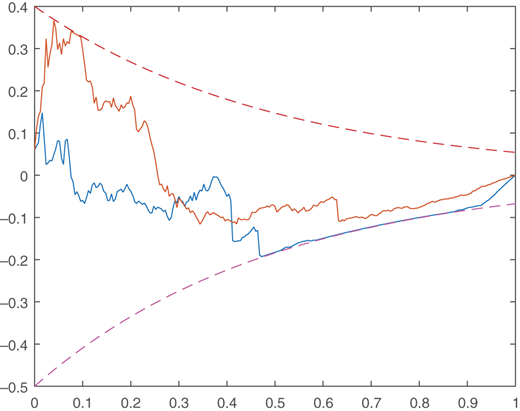

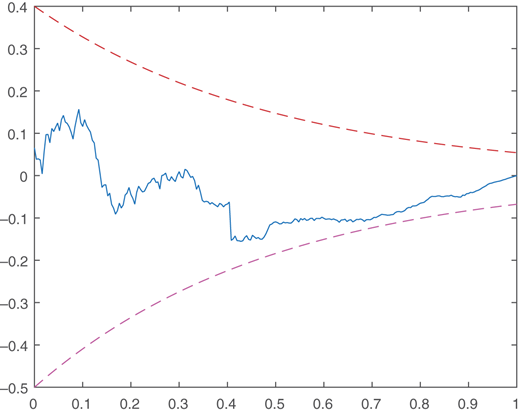

Interpretation: Recall once again that the optimal strategy is obtained when Y reached successively the barriers L and U. In Figures 3 and 4, the costs are higher than in Figures 5 and 6. In Figures 3 and 4, it could be not interesting to switch the technology. It is preferable that the firm takes the precaution of keeping long enough the technology 1, which will enable to obtain suitable expected profit.

In the case of reasonable costs, as in Figures 5 and 6, the firm can switch the technology more often: actually at times and (Figure 5), respectively in Figure 5, the firm can switch the technology at times and .

The authors would like to thank Monique Jeanblanc for her constructive comments and suggestions to improve the quality of our work.

References

Further reading

Appendix

For sake of completeness, references being out of our knowledge, here is provided an extension of Gronwall's lemma.

Lemma 7.1. Let g and ψ be positive functions, let D be a positive constant satisfying then

if

if then

Lemma 7.2. Assume that f and L satisfy respectively and let be the solution of the RBSDE:

where , , is a positive measure such that and Then,

where

and

Proof. Ito's formula and show

Using the Lipschitz property of g, we obtain

It follows that

Moreover, for any

(we use ). Applying Gronwall's lemma (see Lemma 7.1) to bound with and

Since ϕ is decreasing, we get

where Since ϕ is decreasing, we get

Similarly we get

Lemma 7.3. The solutions of the reflected BSDE (Theorem 4.2) and of the double reflected BSDE (Theorem 4.8) are regular.

Proof: Let T be a finite stopping time and be a non decreasing sequence of stopping times going to Using [VI 50 p. 125] [22], a sufficient and necessary condition for Y to be “regular” (meaning ) is

If the process Y is a solution to reflected BSDE, we get

So a sufficient condition is: for any predictable stopping time Under Assumption this condition is satisfied since under these hypotheses are continuous.