This study aims to provide an overview of blockchain technology (BT) adoption within the auditing domain. It focuses on three stages of BT adoption, i.e. pre-implementation, implementation and post-implementation.

Of the 2,610 initial sources, we selected and analyzed 63 relevant articles from the Scopus database.

This study uncovered a promising and multidisciplinary field of research primarily driven by scholars with less practitioner involvement. Review and conceptual research were the most prevalent, highlighting the need for significant efforts in developing empirical research. This study provides a framework for BT adoption. It offers valuable insights into the adoption approach, covering the period from when organizations justify the need for adopting BT in auditing to the stage when they experience its full potential and derive various benefits. For the future research agenda, we posted 35 research questions about building a comprehensive approach to BT adoption.

This study approached BT adoption in auditing through the lens of three stages, i.e. pre-implementation, implementation and post-implementation.

Introduction

Over the last dozen or so years, the volume of financial data has been constantly increasing. It challenged accounting and auditing practices and required the employment of advanced data analytics methods and the upskilling of professionals to analyze data effectively, correctly interpret the analysis, and apply professional judgment (Andiola, Bedard, & Kremin, 2019; Puthukulam, Ravikumar, Sharma, & Meesaala, 2021; Lugli & Bertacchini, 2022). Simultaneously, financial statement regulators and users expect auditors to provide reliable assessments of financial statements and to detect fraudulent financial reporting (Hegazy & Tawfik, 2015; Jaakkola, 2020). Thus, risk assessment, materiality, sampling, and internal control testing constituted the most frequently identified issues in the European Union market for statutory audits of public interest entities (EU, 2021). These above factors have led to a demand for automating complex and time-consuming accounting and auditing procedures (Abdennadher, Grassa, Abdulla, & Alfalasi, 2022). Consequently, accountancy and audit firms must employ various technologies for data collection, storage, processing, analysis, and exchange to facilitate and improve the efficiency and effectiveness of their work and ensure the security, transparency, and credibility of provided services (Agustí & Orta-Pérez, 2022).

Despite the relatively young age of blockchain technology (BT), academics have shown a growing interest in adopting it for accounting and auditing purposes over the past few years (O’Leary, 2017; Parmoodeh, Ndiweni, & Barghathi, 2023). They revealed that BT holds significant potential to transform and enhance accounting and financial auditing practices (Rozario & Thomas, 2019; Schmitz & Leoni, 2019; Han, Shiwakoti, Jarvis, Mordi, & Botchie, 2023) while addressing common deficiencies that audit firms’ internal quality control systems identified (Calderon, Song, & Wang, 2016; Aobdia & Petacchi, 2019). In this study, we expanded on the work of Bellucci, Bianchi, and Manetti (2022), who conducted a systematic literature review on BT in accounting and underscored the importance of integrating BT within auditing. Further, in the systematic literature reviews, Secinaro, Dal, Mas, Brescia, and Calandra (2022) and Lardo, Corsi, Varma, and Mancini (2022) focused on accounting issues with limited references to auditing. The authors highlighted the urgent need for research efforts in the field of BT for auditing. These endeavors should delineate how auditors should conduct audit activities integrated into BT, how they will manage various stakeholders, how audit practices will evolve, and how to harness BT to enhance auditing capabilities. Moreover, Lombardi, De Villiers, Moscariello, and Pizzo (2022), Sargent (2022), and Silva, Inácio, and Marques (2022) conducted content and bibliometric analyses, focusing on BT as a disruptive force shaping the auditing field. Lombardi et al. (2022) underscored the necessity for reevaluating auditing practices and the accounting profession in the context of BT adoption, emphasizing the need to consider the systematization of audit activities and procedures. Notably, Sargent (2022) observed a disparity in the treatment of BT consensus verification features between IT and accounting literature, highlighting a growing interest in the application of BT in auditing but also indicating limited convergence and collaboration between IT and financial experts in this area.

Furthermore, the increasing interest in adopting BT for auditing purposes in recent years extends beyond the academic sphere to include auditing practitioners (EY, 2023; Deloitte, 2017a; KPMG, 2018). According to recent industry reports (CPAB, 2019; Deloitte, 2020; EY, 2020b), scholars expect BT to considerably impact accountants, auditors, and regulators, particularly concerning the initiation, processing, recording, reconciliation, auditing, and reporting of transactions. Large corporations, institutions, and leading audit firms have already adopted BT (Bellucci et al., 2022). They have established BT labs, developed BT-based solutions, and offered consulting services to help clients navigate BT-related opportunities and challenges (Deloitte, 2017b, c; EY, 2020a).

Considering the discussion above, the motivation for this review article came from four key observations. First, BT has the potential to address present challenges in auditing. Second, BT is becoming more popular and generates interest within the audit professional communities. Third, the literature review focused primarily on BT in accounting issues, with some cross-references to auditing. Fourth, despite the growing discussion on the potential of BT for auditing, the literature does not present details on the adoption of BT in auditing. We believe it is urgent to fill this gap with systematic insights into the whole process of BT adoption for auditing, especially when adopting BT in auditing means disruption of former auditing practices and capabilities.

We comprehensively reviewed the literature on BT adoption in auditing to identify and synthesize the most significant and reliable contributions and highlight potential directions for further research, with a particular focus on the adoption process of BT in auditing. The analysis aligns with the three stages of BT adoption outlined in the frameworks proposed by Ross and Vitale (2000) and Themistocleous, Soja, and Cunha (2011), i.e. pre-implementation (planning and designing), implementation (initial usage and stabilization), and post-implementation (continuous improvement and transformation).

Following the introduction, we will present the methodology for the systematic literature review (SLR), including the use of the PRISMA model, the research questions, and the data collection and analysis tools. Subsequently, we will present the research findings with a visualized bibliometric network created using VOSviewer’s map. We will then address the discussion and the research findings. Next, we will suggest future research avenues. Finally, we will present the contribution of this research to both science and practice and its limitations.

Research methodology

Research protocol

We adopted a systematic approach to a literature review due to its advantages (Snyder, 2019; Xiao & Watson, 2019). First of all, SLR is the most appropriate research method for identifying the body of relevant literature and its analysis, as well as for a critical evaluation and synthesis of an emerging research area, i.e. the adoption of BT in auditing. Moreover, SLR can provide practitioners with a valuable overview of the issue, assisting them in finding evidence to inform their decisions on adopting BT in auditing, i.e. whether it is worth it and how to adopt BT.

To minimize bias, reduce mistakes, and ensure the protocol robustness, we built on other literature reviews in emerging research areas (Büyüközkan, Ilıcak, & Feyzioğlu, 2022), especially in BT and accounting (Bellucci et al., 2022), BT and auditing (Lombardi et al., 2022; Han et al., 2023), and the adoption of BT at all (Tiron-Tudor, Deliu, Farcane, & Dontu, 2021; Vacca, Di Sorbo, Visaggio, & Canfora, 2021). We employed the PRISMA Statement (Page et al., 2021a), which supports us in improving the reporting of systematic reviews.

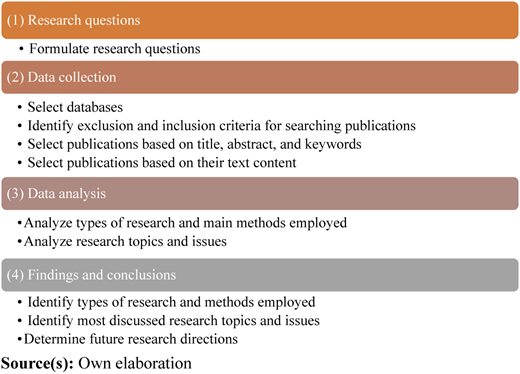

Considering all the above issues, we indicated four steps in our research protocol, as presented in Figure 1.

Research questions

Research questions that the literature review intends to answer constitute the basis of auditable and replicable SLR (Lombardi et al., 2022). The questions define the research subject, object, and scope (Booth, Papaioannou, & Sutton, 2012; Büyüközkan et al., 2022; Bellucci et al., 2022). According to Massaro, Dumay, and Guthrie (2016), the SLR needs to answer the question about an existing state of knowledge before it can answer a question about a path toward future research.

Therefore, we addressed the following three research questions:

What are the most conducted types of research on BT adoption in auditing?

What are the most discussed research topics and issues on BT adoption in auditing?

What are the potential research directions of BT adoption in auditing?

Data collection

Literature search

We may consider some exclusion and inclusion criteria parameters as typically implemented in the research string. Therefore, these criteria were part of the research string refinement process. Consequently, we selected Scopus as other published bibliometric studies in highly reputable peer-reviewed journals have also used it (Lardo et al., 2022; Secinaro et al., 2022; Han et al., 2023).

We used searching by titles, abstracts, and keywords with the query string:

TITLE-ABS-KEY (blockchain AND audit*)

Exclusion and inclusion criteria

Applying exclusion and inclusion criteria aims to select only relevant articles to answer the formulated research questions. Considering many potentially relevant records, we followed the exclusion criterion reported recently in several studies (Büyüközkan et al., 2022; Secinaro et al., 2022).

We formulated the applied exclusion and inclusion criteria as follows:

Language restriction: English;

Document type selection: articles;

Period limitation: 2017–2024;

Citations criteria excluded.

The literature research included publications in English and articles published during the last seven years, from 2017 to 2024 (up to the end of September). We chose this period because although BT emerged in 2008 (Nakamoto, 2008), the BT era for accounting and auditing began in 2017 (Coyne & McMickle, 2017; Dai & Vasarhelyi, 2017; Deloitte, 2017a). We excluded earlier years as BT was an emerging topic that, at the same time, was subject to rapid advancements. Moreover, previous literature reviews by Pizzi, Venturelli, Variale, and Macario (2021) and Lombardi et al. (2022) analyzed publications related to BT and auditing from the earlier period. They identified only a few articles, and after their reviews, we did not consider them in our analysis due to their very general findings.

Articles selection process

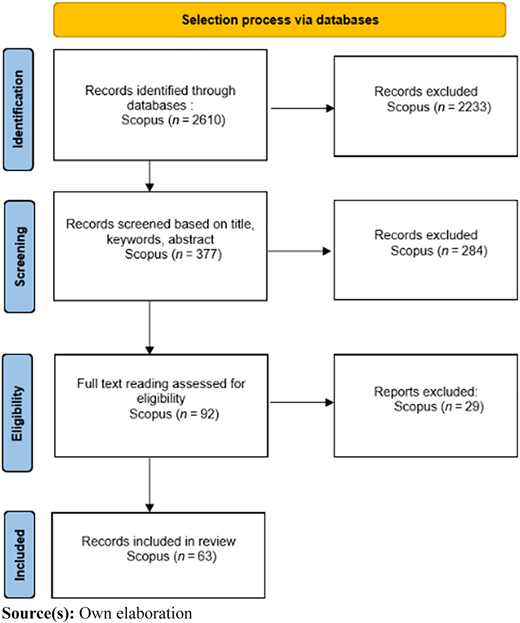

Figure 2 details the study selection process. The initial step in the PRISMA flow diagram consists in identifying studies. This involves a search using the refined research string and reporting the number of results obtained.

In the first step that we made using search engines, we examined all the titles, keywords, and abstracts of all articles based on the query string presented in the above section. We identified a total of 2,610 articles in Scopus. Then, following the SLR methodology (Snyder, 2019), we applied the established inclusion and exclusion criteria to the initial search results. This way, we excluded 2,233 articles, and 377 articles remained for further screening.

In the screening step, we looked for relevant articles by reading the title, keywords, and abstracts of 377 articles. Two researchers performed this step independently to reduce potential researcher bias. After completing their analyses, the researchers compared their findings and resolved any discrepancies or concerns. The aim was to identify all relevant studies that could provide insights into the examined topic. As a result, we selected 92 articles for further analysis.

In the eligibility step, at least two researchers read the full texts of all 92 articles to identify the final set of articles. We excluded articles that did not directly address our research questions, specifically those retrieved by our search string, but focused on peripheral topics outside BT adoption in auditing. The complete eligibility assessment of the 92 remaining studies allowed us to identify a final set of 63 articles for data analysis and synthesis.

In the selection process, we did not exclude articles solely because researchers published them in lower-ranking journals. However, to evaluate whether the analyzed articles appeared in top-tier journals, we checked if Scopus and the Australian Business Deans Council (ABDC) list and the Web of Science (WoS) database indexed them (Garanina, Ranta, & Dumay, 2022; Secinaro et al., 2022; Jayasuriya & Sims, 2023). In total, ABDC indexed 54 out of 63 articles, and WoS indexed 50 out of 63 articles. Table 1 shows the number of articles finally classified for the analysis and clustered into the journal categories.

Data analysis

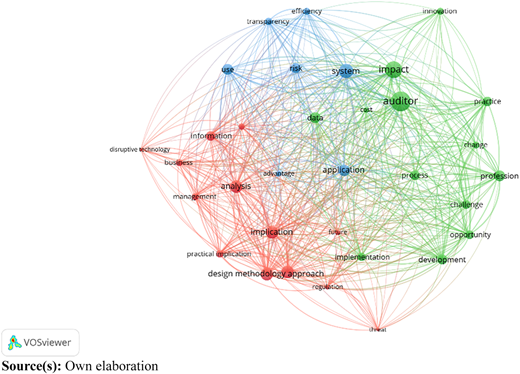

We used Microsoft Excel software, especially multi-dimensional tables and graphs, to describe collected articles and group them by the type of study (articles). We analyzed the most discussed topics and issues on BT adoption in auditing using the VOSviewer software that creates a co-occurrence network of keywords. In the co-occurrence analysis of keywords, the software determines the items’ relatedness based on the number of articles in which keywords occur together (Bellucci et al., 2022). Moreover, it provides a clustering function, which assigns keywords to clusters based on their co-occurrence procedures (Abdennadher et al., 2022). The inspiration behind this study was mainly the cluster analysis approach used in the research related to BT in auditing (Lombardi et al., 2022), digital transformation in internal auditing (Pizzi et al., 2021), and BT in accounting (Belluci et al., 2022; Lardo et al., 2022).

We chose analysis keywords by occurrence frequency to establish an adequate threshold. We set the number of keyword occurrences to three as a minimum threshold level (Shah, Lei, Ali, Doronin, & Hussain, 2020). In the first analysis step, VOSviewer extracted 164 keywords that occurred three or more times. Then, we manually excluded keywords irrelevant to our analysis, i.e. not strictly related to BT adoption in auditing. Finally, we used 33 keywords to build the map. VOSviewer transformed the data into a visual form and classified the frequently occurring keywords into three main clusters in the network visualization view differentiated by blue, red, and green colors (Figure 4). Keywords with similar colors belong to the same cluster. Keywords with larger circles and map labels represent greater importance and significance. Furthermore, the closer keywords are next to each other, the stronger their relatedness in terms of co-occurrence (van Eck & Waltman, 2010). Figure 4 shows keywords with higher weights more prominently and close to each other than keywords with lower weights. Moreover, keywords with only a few relations with other keywords can potentially become new research topics.

Most discussed topics and issues on BT adoption in auditing by keywords analysis

Most discussed topics and issues on BT adoption in auditing by keywords analysis

Research findings

Types of research on BT adoption in auditing

Articles distribution by research type

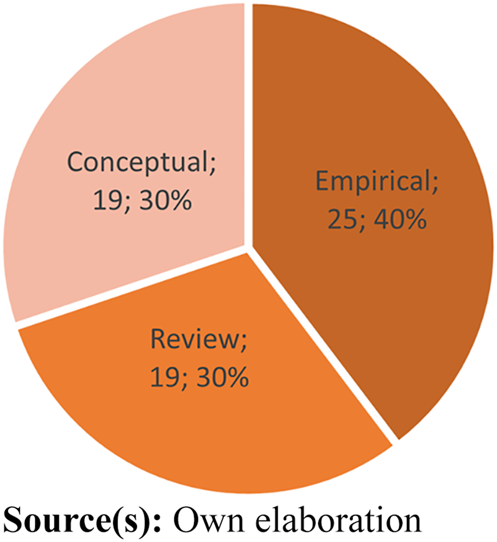

We examined the articles’ distribution by research type to answer the question RQ1. We identified three groups of articles in the literature based on research type, i.e. review, conceptual, and empirical ones. Review articles summarize current knowledge on a specific research topic (Palmatier, Houston, & Hulland, 2018). Conceptual articles can relate to conceptual integration across multiple theoretical perspectives, changing the scope or perspective of an existing theory, categorizing variants of concepts, and building a theoretical framework that predicts relationships between constructs (Jaakkola, 2020). In turn, empirical articles gain knowledge using direct and indirect observation and employ quantitative and/or qualitative research methods to analyze the collected data (Powner, 2015). These three approaches can provide a broader perspective on current knowledge, knowledge gaps, and future research agenda for BT adoption in auditing.

Accordingly, we divided the selected articles (N = 63) into three groups: reviews, conceptual, and empirical articles (Figure 3). We observe that the conceptual and review articles dominated the selected articles. The review articles comprised conceptual articles – 19 items, and the empirical articles – 25 items. Appendixes A, B, and C (Ziemba, Renik, Maruszewska, & Mullins, 2025) present three groups of articles that we identified for analysis in the context of research type.

Review research on BT adoption in auditing

Out of 63 articles included in this study, we found and examined 19 review articles in detail (Ziemba et al., 2025; Appendix A). Scholars designed the review articles to present the current knowledge on BT adoption in auditing and map topics and issues for future studies (Palmatier et al., 2018).

By analyzing these articles, we concluded that 12 of them used SLR, whereas six employed the critical literature review and one bibliometric review. The authors of seven SLR articles focused mainly on BT adoption in accounting, with some references to auditing. The next two articles by Pizzi et al. (2021) and Mugwira (2022) examined the adoption of emerging technologies, i.e. artificial intelligence, BT, and Big Data in auditing. Only three articles discussed strictly BT adoption in auditing (Lombardi et al., 2022; Sargent, 2022; Silva et al., 2022). Lombardi et al. (2022) investigated main emerging research areas, such as BT, as a tool for audit professionals to improve business information systems to save time and prevent fraud and smart contracts, enabling Audit 4.0 efficiency, reporting, disclosure, and transparency. Silva et al. (2022) enhanced these areas. They added new implications of BT for auditing, e.g. governance, transparency, and trust, real-time auditing, auditor’s new professional roles, triple-entry bookkeeping in BT, and permissioned access to auditor/privacy in access. It is disturbing to find that although Sargent’s (2022) research shows a growing interest in the topic of BT for auditing, there seems to be little convergence and collaboration between the IT and financial communities regarding this matter.

Generally, the review articles that contributed to the debate between practitioners and scientists delivered a “state-of-the-art” snapshot of BT adoption in auditing. Most of these articles provided a general overview of BT in accounting and auditing, attempting to define the concept, the impact of BT on auditing, and implications for accountants and auditors’ professions. The authors mainly discussed two issues. First, the authors highlighted common ground and suggested potential effects of BT on accounting, including auditing. Second, they examined features of BT, approaches, and tools that enable BT innovation absorption in organizations.

Conceptual research on BT adoption in auditing

Out of 63 articles in this study, we found 19 conceptual articles and examined them in detail (Ziemba et al., 2025; Appendix B). The conceptual articles’ design aimed to propose new concepts, frameworks, and models and finally extend existing theories that can help analyze the phenomena of BT adoption in auditing (McCallig, Robb, & Rohde, 2019; Liu, Robin, Wu, & Xu, 2022). They attempted to broaden understanding and expand scientific theories and explanations.

Examined conceptual articles provided a roadmap to tackle the challenges of BT adoption in auditing and gave a critical perspective on the issue. Generally, the authors of these articles tried more or less successfully to “review extant research on this technology and assess the impact of BT in the audit profession, including risks, change in procedures and additional opportunities” (Bonyuet, 2020). Scholars chose qualitative research most often, which aligns with the research findings of Secinaro et al. (2022). This method mainly served to identify patterns and behaviors related to BT adoption and understand experiences across BT adoption. Three of the articles provided some models of BT adoption. McCallig et al. (2019) proposed the ideal model of the audit process to confirm customer balances and the real model of a secure audit process with data stored on BT. Rozario and Thomas (2019) also suggested two models, i.e. interlinked BT ecosystem and BT smart audit procedures for revenue.

Empirical research on BT in auditing

Out of 63 articles in our study, we found only 25 empirical articles and examined them in detail (Ziemba et al., 2025; Appendix C). This type of article is the most numerous of the three types.

In the case of most empirical articles, scholars designed them to quantitatively evaluate how BT adoption in auditing changes the auditing profession and how audit procedures adjust when audited clients utilize BT. The phenomenon of BT adoption in auditing is mostly described with the use of interviews conducted among audit stakeholders and auditors, mainly from Big4 audit firms.

Due to the small number of empirical articles, it is mainly possible to indicate the use of semi-structured interviews as qualitative methods. Two articles used survey research, one employed a Delphi study, and one used an experiment as a quantitative method. These articles mainly employed descriptive statistics, regression, variance, correlation analyses, and PLS-SEM. Alshurafat, Al-Mawali, Obeid, and Shbail (2022) employed the technology acceptance model (TAM) to examine the impact of technostress on auditors’ acceptance of the use of BT. Furthermore, Ferri, Spanò, Ginesti, and Theodosopoulos (2021) harnessed an integrated theoretical frame, merging the third version of TAM and the unified theory of acceptance and use of technology (UTAUT). Based on an application of structural equation modeling (SEM), we proposed and verified the theoretical model of BT adoption intention. In research published in 2024, we observed an increase in the investigation regarding the behavioral intention to use new technologies and its four key factors: performance expectancy, effort expectance, social influence, and facilitating conditions (Alkhwaldi, Alidarous, & Alharasis, 2024; Majeed & Taha, 2024). The empirical research encompassed only a few countries, i.e. Australia, Canada, Indonesia, Croatia, Jordan, Germany, Iraq, Italy, Switzerland, Turkey, the United Arab Emirates, China, and the USA. Nevertheless, scholars publish more and more articles of an empirical nature from year to year.

Generally, the literature does not sufficiently empirically examine BT adoption to gain knowledge on it using direct and indirect observation and employing quantitative and/or qualitative research methods. The fact that BT in auditing is a scarcely empirically explored topic seems to be an advantage with potential for the future. We may consider this a major challenge for researchers and practitioners alike.

Most discussed research topics on BT adoption in auditing

In addressing RQ2 and RQ3, an analysis of keyword co-occurrence based on their connections revealed three main clusters, highlighting thematic groupings within the literature and providing insights into the primary focus areas in BT adoption research for auditing (Figure 4):

Cluster #1 (red) included 13 keywords, such as adoption, analysis, business, design methodology approach, and management, indicating a focus on the pre-implementation stage of BT adoption in auditing. This cluster comprised 27 articles, detailed in Appendixes A to C (Ziemba et al., 2025).

Cluster #2 (blue) included the following seven keywords: advantage, application, efficiency, and transparency, focusing on the implementation stage of BT adoption in auditing. This cluster, the most numerous with 43 articles, is detailed in Appendixes A to C (Ziemba et al., 2025).

Cluster #3 (green) included 13 keywords such as auditor, challenge, change, cost, development, impact, and opportunity, focusing on the post-implementation stage of BT adoption in auditing. This cluster contains 26 articles detailed in Appendixes A to C (Ziemba et al., 2025).

Discussion

BT pre-implementation

Considering Themistocleous et al.’s (2011) and Ross and Vitale’s (2000) studies, at the BT pre-implementation stage, users carefully plan and design BT solutions tailored to specific auditing requirements. They determine how BT will be organized to support auditing processes. Primarily, they establish the goals and objectives of BT adoption, create a plan for employing BT to support auditing processes, and design BT-enabled auditing processes.

The 29 articles, including 11 reviews, eight conceptual, and 10 empirical articles, present the issues of this BT adoption stage. The research discussions focus on planning and designing BT in auditing practices to meet the demands of its multiple users, i.e. auditors, accountants, tax authorities, regulators, and other organizations while emphasizing its integration with auditing processes and information systems. Table 2 presents three identified research streams with correlated modus operandi and future research directions. Appendix D (Ziemba et al., 2025) provides further details.

Research streams, modus operandi, and future research agenda for BT pre-implementation

| Modus operandi (research findings) | Future research agenda |

|---|---|

| 1. Choice of BT type and integration of BT with AIS | |

| The choice of BT in auditing varies based on its type and consensus protocol, with permissioned BT offering enhanced control, security, and selective information sharing. Integrating BT into AIS requires a three-tier architecture, improving data management, application logic, and interface functionality, which automates repetitive tasks and ensures transparency, precision, and data immutability, aligning with International Financial Reporting Standards. While fully automating audits is not feasible due to the transactions’ complexity, a hybrid audit model combining BT-based and traditional procedures is necessary to meet human expertise and reasoning requirements |

|

| 2. Factors influencing BT adoption in auditing | |

| The success of BT adoption in auditing depends on several intertwined factors. Key elements include technological complexity, scalability, suitable architecture, and BT cybersecurity, as well as critical decisions on control, data ownership, privacy, and access. Moreover, organizational willingness, influenced by performance expectancy, social influence, and auditors’ perceptions of usefulness and ease of use, along with auditors’ knowledge of BT and a consensus among auditors, regulators, and stakeholders to address concerns such as costs and data privacy, are crucial to fully integrate BT into the auditing ecosystem |

|

| 3. Steps, tasks, and processes of BT pre-implementation | |

| BT pre-implementation involves internal discussions on its applicability, education on BT, strategy creation, and use case design. It also includes assessing costs and benefits, advising clients, managing risks, and expanding advisory services. Moreover, a BT adoption strategy should encompass forming partnerships, navigating technological changes, designating maintenance responsibilities, sourcing talent, ensuring compliance, and understanding the impact on business processes |

|

Source(s): Own elaboration

The existing studies are often still fragmentary and scattered. They show little consideration for conceptualizing and operationalizing the pre-implementation stage of BT adoption in auditing. Thus, research must examine many issues. A primary area for further research is identifying the optimal type of BT for integration with Accounting Information Systems (AIS) (Rozario & Vasarhelyi, 2018; Tan & Low, 2019; Tiron-Tudor et al., 2021). Different BT types, such as permissioned versus permissionless, impact data transfer, sharing, and security, all of which are critical for reliable financial reporting (McCallig et al., 2019; Schmitz & Leoni, 2019). Permissioned BT, favored in business settings, offers control and security advantages suited to auditing. However, the field requires more studies to assess which BT models best support selective data access and stakeholder needs, especially for regulatory compliance and information sharing among auditors and regulators. This research can guide AIS design to enhance data transparency and security in auditing, clarifying user roles, data access levels, and privacy requirements.

Furthermore, BT adoption in auditing is under the influence of technological, organizational, and social factors, including technical complexity, scalability, cybersecurity, and managers’ willingness to adopt BT (Bonsón & Bednárová, 2019; Ferri et al., 2021; Akter, Kummer, & Yigitbasioglu, 2024). Auditors’ understanding of BT’s functions and risks is crucial as it supports bridging technical and auditing needs (Mugwira, 2022; Jayasuriya and Sims, 2023). Research should explore strategies to improve manager and auditor knowledge, address cost and data privacy concerns, and build stakeholder consensus to ensure BT’s seamless integration in auditing.

Finally, implementing BT in auditing requires a structured pre-implementation process, including cost-benefit analysis, control design, and governance, which are essential for successful adoption (Liu et al., 2022). Key steps like internal education, BT strategy development, and selecting relevant use cases are necessary for successful adoption. Collaborative efforts among stakeholders are also crucial to establish standards and compliance protocols. Research on best practices in pre-implementation can offer a roadmap to a scalable, resilient BT infrastructure aligned with auditing demands.

BT implementation

Our research findings also pertain to the second stage of BT adoption in auditing, i.e. implementation. Considering the studies of Themistocleous et al. (2011) and Ross and Vitale (2000), at this stage, users configure and test BT to align with auditing requirements, acquire the necessary skills to ensure successful adoption, integrate BT into auditing processes, convert existing auditing processes to BT-enabled ones, and ensure that BT works correctly. At this stage, integrated BT solutions work smoothly within the auditing framework, and the early benefits of BT start to emerge. Still, we can also observe the negative effect of the perceived adequacy of accounting standards on the intention to use BT (Juma’h & Li, 2024).

We found the issues of this BT adoption stage mainly in 43 articles, including 13 reviews, 12 conceptual, and 18 empirical articles. The discussion revolves around the initial usage of BT in auditing and the efforts to make such usage stable and reliable. Table 3 presents three research streams with correlated modus operandi and future research directions. Appendix E (Ziemba et al., 2025) provides further details.

Research streams, modus operandi, and future research agenda for BT implementation

| Modus operandi (research findings) | Future research agenda |

|---|---|

| 1. Examples of implemented BT solutions in auditing | |

| Implementing BT in auditing faces resistance due to auditors’ lack of IT training and perceived risks. Moreover, the company’s ICT development phase influences auditors’ readiness and their perceived adequacy of accounting standards. Furthermore, the governmental adoption of BT sets expectations for private entities to follow suit |

|

| 2. Enhanced audit efficiency | |

| During the initial usage stage of BT in auditing, the process requires developing new audit procedures to address previously unknown risks, such as data security and privacy. Meanwhile, BT adoption mitigates traditional risks. Audit procedures should focus on verifying internal controls over transaction registers, necessitating new control procedures for the IT environment. The stabilization phase sees increased audit efficiency due to the low cost, transparency, and traceability of BT, as well as the shift from annual audits to real-time auditing |

|

| 3. Stabilization of BT adoption in auditing through smart contracts | |

| Smart contracts, which activate transactions based on predefined rules, are an extension of many database configurations but offer unique benefits when used with BT, such as increased assurance and lower costs, enabling continuous audits. In the stabilization stage, smart contracts facilitate automatic execution and recording of transactions, enhancing control for both audited and audit companies. Moreover, they enable real-time preparation of financial reports and allow both parties to program business logic that notifies participants of errors |

|

Source(s): Own elaboration

On the one hand, the existing articles do not provide universal insights into the implementation stage of BT adoption, particularly concerning the initial usage and stabilization of BT in auditing. This gap exists among auditors interested in BT applications for audit procedures and those dealing with BT because the audited client uses BT, for example, in crypto currencies. On the other hand, blue cluster #2 articles pinpoint BT as a disruptive factor in changing auditing (Pizzi et al., 2021; Garanina et al., 2022). They indicated the advantages of BT use in auditing: increased data collection availability, sufficiency, transparency, traceability, and performance efficiency. They also presented some new risks and changes in the assessment of client risk since, in the case of an audited client using BT, audit processes and procedures require change (when compared to the traditional ones). Moreover, the literature raises financial constraints as adopting BT requires highly developed technological resources that small audit firms might not possess (Mugwira, 2022; Huang, Wang, & Yen, 2024). As BT in auditing is at its infant stage when it comes to the application by auditors, the field needs more research regarding the main predictors of BT application in auditing and detailed training activities that are better targeted at auditors to foster their confidence and competence in using BT and thus increase their performance and effort expectancy (Ferri et al., 2021). Further, the field requires a thorough understanding of the scope of BT implementation in auditing to know what exact audit procedures are subject to changes and the possible ways of limiting new risks. Finally, the discussion requires a more strategic approach with regard to efficiency as it needs defining from the perspective of multiple software that the audited entity and the audit firm use. Thus, this would enable continuous audit optimization and continuous process improvement.

BT post-implementation

The upcoming section focuses on the primary findings related to the final stage of BT adoption, namely, BT post-implementation. Considering the studies of Themistocleous et al. (2011) and Ross and Vitale (2000), at this stage, users concentrate on enhancing both BT and the auditing processes it supports. They meticulously assess BT’s functionality and define modifications, updates, and changes to adapt to evolving auditing requirements and standards. Continuous learning in both BT and auditing becomes imperative. The ongoing efforts in this stage aim to optimize BT’s performance and functionality within the auditing context.

Considering articles related to this subject, we identified five research streams based on the content of 26 articles, including eleven reviews, seven conceptual, and eight empirical articles. The discussion focuses on improving and transforming implemented BT, particularly examining how BT is continuously enhanced, optimized, and changed to meet evolving auditing needs and standards and better serve the auditing processes. Table 4 presents five identified research streams with correlated modus operandi and future directions. Appendix F (Ziemba et al., 2025) provides further details.

Research streams, modus operandi, and future research agenda for BT post-implementation

| Modus operandi (research findings) | Future research agenda |

|---|---|

| 1. Changes and impact of BT adoption on the auditing profession | |

| BT can transform the auditing profession and complement traditional auditing roles by automating procedures, influencing tasks, skills, and education requirements, and supporting auditors in their analytical and judgmental tasks |

|

| 2. Legal and professional regulations required by BT adoption in auditing | |

| The main obstacle to BT adoption in auditing is the lack of clear guidelines, regulations, and standards, necessitating the development of new legal frameworks, auditing standards, and compatible accounting policies. To overcome this, existing practices require an update or replacement. Moreover, they require the introduction of specific regulations tailored to clients using BT for statutory accounts and financial transactions |

|

| 3. Future opportunities related to BT adoption | |

| BT adoption in auditing presents more opportunities than challenges, offering an enhanced ability to anticipate financial difficulties and assess future profitability. It improves analytical procedures, reduces audit time and costs, increases efficiency, enhances the reliability of financial statements, and mitigates risks. Additionally, BT simplifies auditing and reduces fraud detection costs through its tamper-proof and immutable nature |

|

| 4. Challenges of BT adoption in auditing | |

| BT faces challenges related to scalability, flexibility, architecture, and cybersecurity. Auditors must adapt to new procedures for reviewing transactions and verifying digital assets, as well as upgrading IT skills, strategic decision-making, and data analysis and visualization tools. The auditing profession needs to adjust to accommodate the BT requirements |

|

| 5. Changes in BT adoption in auditing | |

| Blockchain technology can significantly improve audit quality, transparency, efficiency, and trust and enable real-time auditing. Its implementation in auditing can enhance outcomes, potentially transform company operations, and complement traditional auditing at a low cost. While BT offers solutions to current accounting challenges through multi-party validation, successful adoption requires auditors and audit firms to manage emerging challenges |

|

Source(s): Own elaboration

Exploration of numerous research studies ensures a comprehensive understanding of the changes that have emerged or will arise in the auditors’ profession during the BT post-implementation stage. Despite the various transformations related to automating audit evidence, reporting, or processes and adjusting procedures and auditing standards to this new technology, the auditing profession should continue to uphold the auditor’s role as a certifier of veracity (Silva et al., 2022). The literature on BT adoption concludes that we will still need independent judgment from auditors in the future, and we will not entirely replace them (Tan & Low, 2019; Bellucci et al., 2022). Moreover, BT can support auditors’ professional roles in the future rather than replace them because audit procedures will still need human intervention (Parmoodeh, 2023). However, auditors should reskill and upskill their knowledge and experience to provide complex transformation and development of BT adoption.

To summarize, scholars often see BT as a disruptive technology that can bring fundamental changes (Mugwira, 2022; Salim, Barachi, Halstead, & Babreak, 2022). By trying to explore BT’s disruptive impact on auditing, Lombardi et al. (2022) proved that this research topic is relatively unexplored. They highlighted the necessity of investigating research areas and future implications: BT as a tool for improving the audit profession; new standards and guidelines as a BT challenge for auditing; future audit opportunities and risks of BT adoption; and reconsidering audit procedures. Hakami, Sabri, Al-Shargabi, Rahmat, and Nashat Attia (2023) also indicated future research, such as the potential benefits and challenges of using BT and the implications for auditing standards and regulations and investigating BT usage for digitalizing audit evidence.

Framework for BT adoption in auditing

Based on the research findings, this section proposes a phased framework for BT adoption in auditing to guide the audit industry through each stage, from initial planning to continuous optimization (Table 5). We designed this framework to systematize the BT adoption process in auditing by specifying clear objectives, tasks, and results for each adoption stage, addressing theoretical needs (advancing research on BT in auditing), practical requirements (facilitating effective BT adoption), and societal goals (enhancing public trust in audit practices).

Framework for BT adoption in auditing

| Objectives | Tasks | Expected outcomes |

|---|---|---|

| Pre-implementation stage: planning and designing | ||

| Planning and preparing for BT adoption by identifying organizational needs, defining the strategic goals for BT in auditing, and addressing initial concerns regarding integration with existing systems |

| A well-defined BT adoption plan tailored to organizational and auditing needs, with trained staff and a strategic roadmap for BT integration |

| Implementation stage: initial usage and stabilization | ||

| Integrating BT into audit workflows, addressing technical and procedural challenges while ensuring regulatory and audit standards alignment |

| A functional BT audit environment that enhances audit efficiency and reliability, enabling real-time and transparent data auditing with improved compliance |

| Post-implementation stage: continuous improvement and transformation | ||

| Optimizing BT-based audit processes to adapt to evolving requirements and leverage BT’s full potential to enhance audit quality and stakeholder trust |

| A refined and optimized BT-enabled audit framework that supports continuous improvement, maintains compliance and strengthens stakeholder confidence through enhanced transparency and security |

Source(s): Own elaboration

This proposed framework supports both researchers and practitioners in understanding the stages, objectives, tasks, expected outcomes, and continuous improvement needed for successful BT adoption in auditing. Through this framework, organizations can integrate BT more effectively into auditing practices, leading to a more transparent and efficient audit process that meets evolving market and regulatory demands.

Conclusions

Research contribution

This study provides a twofold contribution. First, it presents the research state and future research agenda on BT adoption in auditing, distinct from the accounting issues, by using a hybrid approach containing bibliometric analysis, analysis of research types, data analysis visualization, and discourse analysis concerning BT adoption. The authors of prior systematic literature reviews focused mainly on BT in accounting (Bellucci et al., 2022; Garanina et al., 2022; Lardo et al., 2022), with some references to auditing treated as an extension of accountants’ work, which intends to serve the purpose of possible corrections of accounting entries. In contrast, we treated auditing as an independent professional activity that required the creation of tools from the perspective of auditors’ needs and not as an extension of accounting entries.

Secondly, we approached the topic of BT in auditing by framing its examination within the context of BT adoption, encompassing three pivotal stages: pre-implementation, implementation, and post-implementation. Despite prior literature reviews on BT in auditing (Lombardi et al., 2022; Sargent, 2022; Silva et al., 2022), this study brings a novel contribution by offering a comprehensive perspective on BT adoption within the field. Furthermore, this study tackled the challenge of fostering collaboration between IT and auditing experts in the context of BT for auditing, as emphasized by Sargent (2022). Recognizing the adoption of BT as a multi-stage process, it becomes evident that these endeavors inherently require collaboration between IT professionals and BT users.

Research, practice, societal, and education implications

Our findings on BT adoption in auditing underscore its significant implications across multiple domains. Below, we summarize vital implications across research, practice, society, and education.

In the research domain, there remains a notable gap between theoretical models of BT in auditing and empirical validation in real-world settings. Most existing studies rely on conceptual frameworks and literature reviews rather than hands-on data from practice. Bridging this gap requires more empirical research confirming BT’s impact on audit quality, data security, and operational efficiency. Future studies should consider methodologies like case studies or field experiments to evaluate BT’s tangible effects on audit processes, focusing on its influence on cost reduction, fraud prevention, and stakeholder trust. Moreover, frameworks such as TAM and UTAU models could clarify which factors influence BT adoption among auditing professionals.

Regarding practical applications, BT offers considerable commercial benefits for the auditing profession. Enhanced transparency, improved data reliability, and reduced fraud are key advantages that make auditing processes more efficient and potentially lower operational costs. These commercial impacts position BT as a valuable tool for firms seeking a competitive edge by offering more accurate and dependable audit services. To fully harness these benefits, audit firms must focus on building practical guidelines for implementing BT, including training auditors in digital auditing skills and ethical considerations. Upskilling initiatives should emphasize BT’s technical features, such as smart contracts and data security, equipping auditors to manage the nuances of a BT-enabled audit landscape.

Educational institutions also play a critical role in supporting BT adoption in auditing by incorporating digital audit skills into accounting and auditing curricula. Preparing students with hands-on knowledge of BT will enable future professionals to meet the evolving industry needs. Beyond formal education, continuous learning remains essential for practitioners. Ongoing professional development in BT will help auditors and regulators stay updated with advancements, best practices, and regulatory changes, ensuring they are well-equipped to handle new challenges and capitalize on emerging opportunities.

Overall, BT technology holds transformative potential for auditing, offering substantial benefits across research, practice, public trust, and education. Coordinated efforts among researchers, practitioners, policymakers, and educational institutions will be essential to realize BT’s full potential, reinforcing both the integrity and adaptability of the auditing profession in a rapidly evolving technological landscape.

Research limitations

Scholars should interpret the results of this study concerning its limitations. The primary constraint refers to the emerging BT that requires knowledge development through future studies to propose a comprehensive and detailed picture of BT adoption for auditing improvement. Other limitations concern the literature review approach. First, we focused on studies included in the Scopus database. Nevertheless, all analyzed articles were also present in the ABDC and WoS databases, ensuring the scientific robustness and reliability of our data source and research findings. Second, we excluded publications in languages other than English. Next, the review only encompassed articles from 2017 up to September 2024. Finally, the choice of keywords used in this research was limited, outlining the boundaries of our review study. While there are typical limitations for all systematic reviews, our choice of databases, language, publication date, and keywords might have excluded potentially relevant studies. However, as we have identified and examined a significant body of literature (at least two researchers read the full text of all 92 articles to determine the final set of articles), we believe that the finally chosen 63 studies state a robust representation of the overall area of BT adoption in auditing.

The author extends sincere gratitude to the anonymous reviewers for their invaluable comments and suggestions, which significantly enhanced the quality of this article.

References

The supplementary material for this article can be found online.