This article compares the environmental and welfare effects of three policies in a polluting managerial duopoly with homogeneous goods: an emissions tax, an abatement subsidy and a policy mix of those two instruments.

The article analyzes an emissions reduction policy selection in a managerial duopoly using a game theoretic approach to investigate the strategic interactions among firms and among firms and the government.

The provision of a “green” subsidy that reduces the cost of investing in an end-of-pipe cleaning technology always leads to higher abatement levels than under an emissions tax. Nonetheless, an emissions tax decreases production and, consequently, lowers environmental damage, which has a positive effect on welfare. When societal awareness is negligible and the technology inefficient, the government can nudge the firms’ abatement activities via a “green” subsidies policy, leading in some cases both to the highest welfare and lowest environmental damage. However, when the cleaning technology is adequately efficient, the environmental tax produces the lowest environmental damage. This positive effect counterbalances the negative impact on profits and consumer surplus due to output contraction, leading to the highest social welfare.

This is a theoretical article that does not refer to empirical data. However, we formulated some suggestions/insights for empirical analysis.

This work studies the impact of optimal emissions reduction policies when firms active on the market are managerial ones, a subject that lags in the literature and provides some policy insights.

Introduction

In the last decade, public opinion seems to have been more sensitive toward environmental issues (waste management, sewage, depletion of natural resources, biodiversity loss, nano plastics, emissions of SOx, NOx, particulate matters, and COx) and related environmental damage (i.e. the environment’s deterioration). For example, the “People’s Climate Vote” of the UNDP and University of Oxford (2021), the world’s largest survey of public opinion on climate change, and the historical trend emerging from the polls conducted for the US by the consulting group Gallup (2024) clearly describes those worries. Remarkably, among the environmental issues, various global surveys report that “climate change” catalyzes public opinion’s concerns (Dechezleprêtre et al., 2022; Edelman, 2023).

Consequently, policymakers in several countries have listed climate change high in their agenda (see The Economist, 2019; 2021, 2023). As part of the Paris Agreement, adopted in December 2015 during the United Nations Climate Change Conference (COP21), many of the 196 signatory countries – both industrialized and developing – are now designing, submitting, and implementing nationally determined contributions (NDCs). These efforts increasingly focus on policy measures aimed at reducing greenhouse gas (GHG) emissions, reflecting unilateral commitments to cut emissions associated with their industrial activities (UNEP, 2023) [1].

Indeed, climate change (induced by increasing global temperature) results from GHG emissions generated by highly polluting industries. Of all GHG emissions, carbon dioxide historically represent the largest majority (75.01% in 2022), followed by methane (19.47% in 2022), nitrous oxide (5.51% in 2022), and limited traces of other gases such as hydrofluorocarbons and sulfur hexafluoride (0.01%) (Jones et al., 2024). Consequently, efforts and environmental actions are largely (but not exclusively) [2] directed toward the economies “decarbonization” (i.e. reduction and eventually elimination of CO2 emissions).

Since the market itself is unable to internalize these environmental damages, governments started to design intervention policies. In the last decades, governments have gradually displaced the former “command-and-control” (such as limits or bans) emissions reduction policies with “market-based” mechanisms such as emissions trading, environmental/emissions taxes, tax credits, and pollution abatement (green R&D) subsidies. The rationale for this change is that the latter measures are more flexible than the former ones and allow to reach a preset emissions reduction target at a lower economic cost, or alternatively, for a given cost, to achieve it in the most efficient way, as several early empirical studies have found (see, e.g. Tietenberg, 1990). By means of market-based tools to decarbonize economies, governments/policymakers and regulators influence the choices of polluting economic agents because a price is assigned to the pollution generated, incentivizing them to lower their emissions (Smith, 2011).

We may classify market-based mechanisms into quantity-based (quantity regulation) policies, such as transferable emissions quotas and emission standards, and price-based (price regulation) policies. Among the price-based mechanisms, authorities implement emissions (carbon) taxes. Given that pollution creates an externality leading to a divergence between its private and social costs (which is equal to the marginal damage from the pollution), to control such an externality, the Pigouvian tax is in principle applied by policy-makers (Baumol, 1972). In the specific case, taxing pollution at its social marginal damage would equate private and social marginal costs, ensuring an efficient market outcome. However, because of market distortions, some economists have argued that the optimal tax on pollution will be lower than its marginal damage. To be precise, authorities need to use two policy instruments to correct the environmental externality and the market distortion (see, e.g. the discussion in Cropper & Oates, 1992), or the optimal emissions tax must be equal to the marginal damage of pollution divided by the marginal cost of public funds [3].

Emissions taxes are widespread in Europe. Finland was the world’s pioneering country in setting a carbon tax, already in 1990. Since then, 20 more European countries (14 member states of the European Union, EU) have recently implemented such taxes levied on all direct and indirect production of GHG emissions, regardless of the industrial sector. Carbon taxes are also levied in the four European Free Trade Association countries (Eurostat, 2023a). Outside Europe, the following countries levy carbon taxes (in increasing tax rate order): Japan, Singapore, Argentina, Mexico, Chile, Colombia, South Africa, Canada (at the sub-national level), and Uruguay (the highest, indirect, world tax rate) (The World Bank, 2024) [4].

However, environmentally beneficial, or “green”, subsidies can be an alternative option to control GHG emissions. In EU countries, subsidies to protect the environment, such as for installing cleaner energy and research on environmental issues (“green” R&D), are in place only in 11 member states, plus Switzerland and Norway. The data of those 13 countries reported to Eurostat in 2020 reveal that environmental transfers range from 1.2% of GDP in Malta to 0.8% in Romania and Bulgaria, down to 0.3% in Sweden, Portugal, Ireland, and Luxembourg (Eurostat, 2023b). From a wider perspective, OECD countries have directed 9.4% of the public resources for policies with positive environmental implications to green R&D subsidies (OECD, 2023). Moreover, the OECD (2023) reports that, among member countries, environmental subsidies represent 26.4% of the policy instruments for the environment implemented among all instruments used to control air pollution. Therefore, those measures lag relatively behind even if, according to recent estimates, investment in green R&D technologies that would reduce the cost of abating carbon emissions seems to be the most effective climate policy, with a return of $11 climate benefits per dollar spent (Lomborg, 2020).

The adoption of cleaner technologies to improve environmental quality is relevant in several industries, often those oligopolies-dominated, where strategic interactions between firms and between firms and regulators are important. Moreover, another characteristic feature of oligopolies is the presence of large managerial firms that separate ownership and control.

In this article, we analyze emissions reduction policies and tools governments can use to incentivize managerial firms’ abatement emissions via end-of-pipe technologies, contributing to the longstanding debate on instrument choices, and focusing in detail on price-based mechanisms [5]. In detail, this article evaluates the environmental impact of emissions tax, abatement subsidy, and their joint use in a policy mix in the presence of a social planner (government/regulator) that aims to maximize the overall welfare.

In a companion article to the present one, Buccella, Fanti, and Gori (2024) analyze a polluting entrepreneurial Cournot duopoly with homogeneous goods, comparing the environmental, public finance, and welfare impacts of the above-mentioned three policies (emissions tax, abatement subsidy, policy mix). According to the results, taxation disincentivizes production, leading to the lowest environmental damage, which positively affects welfare except for inefficient technology. Moreover, the positive effect on the environment, jointly with the tax revenues the government collects, more than offsets the negative impact on profits and consumer surplus due to output contraction. Consequently, social welfare improves. The government designs a policy providing a subsidy only when societal awareness is insignificant and technology is inefficient.

The present model extends Buccella et al.’s study (2024) by developing a basic three-stage game in a polluting managerial duopoly in which, in the first stage, a social welfare maximizing government optimally chooses the emissions reduction policy tool (emissions tax, “green” subsidy or their policy mix) for the polluting industry. In the second stage, owners set the managerial incentive in the standard sales delegation contracts. In the third stage, managers choose output and abatement levels. Considering the key (exogenous) parameters of the model, i.e. the degree of societal awareness and the index of technological progress [6], the next step in the process is an analysis of the equilibrium outcomes when there is universal adoption of abatement technologies under the three emissions reduction policies, giving a first tentative insight about the policy design that may facilitate the transition toward a more sustainable production process, with positive impact on the environment.

The main results are as follows. The provision of “green” subsidies decreases the cost of investing in an end-of-pipe technology and leads to abatement levels higher than an emissions tax. An emissions tax shrinks production and thus the environmental damage, with a positive impact on social welfare. When the social concern toward the environment is low, and the state of the abatement technology is inefficient, the government can nudge the managerial firms’ abatement activities via “green” subsidies, yielding in some cases both to the highest welfare associated with the lowest environmental damage. When the social concern increases, and the abatement technology is adequately efficient, the policy mix of emissions tax and subsidies leads to the highest welfare with the second-best environmental damage. On the one hand, to keep abatement levels high, the government provides subsidies whose rates, due to large volumes of production with managerial delegation, are not too high and, therefore, costly for the government. On the other hand, to curb emissions, an emissions tax is introduced to disincentivize excessive production. Nonetheless, with managerial firms, some subsidization of abatement activities is always required.

The remainder of the article goes as follows. Section 2 presents a review of the relevant literature related to emissions reduction policies. Section 3 describes the model, derives the relevant outcomes, and finally compares the environmental and welfare impacts of the two environmental policies. Section 4 closes with an outline of the future research agenda.

Literature review

The environmental economics literature has devoted large efforts to evaluate policies aiming to cut emissions.

Since the 1990s, focusing on price-based mechanisms [7], economists have investigated the impact of emissions taxes in polluting markets, analyzing optimal emissions tax/subsidy in Cournot oligopoly. See, for instance, the groundbreaking studies of Requate (1993a, b) and Simpson (1995) and the subsequent extensions of Carlsson (2000), Poyago-Theotoky and Teerasuwannajak (2002), David (2005), Requate (2006), and Moner-Colonques and Rubio (2015) [8].

Moreover, scholars have investigated the use of subsidies on “green” investments (i.e. adoption of emissions-reducing technologies) to diminish the environmental impact of industrial production and improve welfare in oligopolies. Indeed, large-scale climate objectives can justify the increasing use of green subsidies by governments, oriented mainly toward programs supporting innovation related to green technologies and clean energy to accelerate their adoption and diffusion. To conceive and design appropriate emissions reduction policies, those studies analyze the effects on welfare of “green” subsidies either as an emissions reduction policy alternative to emissions taxes (see, e.g. Conrad & Wang, 1993; Ouchida & Goto, 2014; Lee & Park, 2021a), or as a tool used in combination with an emissions tax, i.e. a policy mix (see Poyago-Theotoky, 2003; Ben Youssef & Dinar, 2011; Gautier, 2015; Kim & Lee, 2024); or both cases as in Buccella et al. (2024).

Conrad and Wang (1993) measure the impact of a change in emissions taxes and, as an alternative policy, abatement subsidies on the output level of single firms and overall industry production and the number of firms operating in the industry. They study three market structures, i.e. perfect competition, oligopoly, and a dominant firm with a competitive fringe. The key difference between the two policies is that a firm that would not generate profits under an emissions tax can be profitable with the provision of a subsidy. Though the effects of those emissions reduction policies on the industry’s emissions are qualitatively similar, they are quantitatively different and indeed shape the structure of the polluting sector. Indeed, those authors emphasize the regulatory (pro/anti-competitive) aspects of those emissions reduction policies, an aspect disregarded in the current article, given the fixed duopoly structure.

Ouchida and Goto (2014) and Lee and Park (2021a, b) turn their attention to the role of emissions reduction policies as a tool to correct not only the environmental externality due to pollution but also the externality linked to the technological innovation process (due to its public good nature in presence of spillovers). Ouchida and Goto (2014) develop a Cournot duopoly with firms adopting an end-of-pipe technology to abate emissions and analyze how emissions taxes and abatement subsidies as alternative policies can affect the decision whether to coordinate emission-reducing R&D activities in the presence of technological spillovers. They find that, no matter what the organization of R&D activities is, the social welfare under a time-consistent emission tax/subsidy policy is always higher than without intervention. Moreover, if the environmental damage is adequately small, then, in equilibrium, the government always sets an abatement emissions subsidy. Furthermore, total emissions with a subsidy are lower (larger) than those under no intervention if (1) the damage is sufficiently small, and (2) the cost of the R&D investment in abatement technology is low (high) [9].

Lee and Park (2021a, b) also compare emissions taxes and green R&D subsidies, both in private and mixed duopoly markets, allowing for environmental R&D spillovers. The authors concentrate on the nexus between R&D spillovers and technology efficiency for degrees of social awareness such that both policy tools can be implemented. The article shows that when environmental R&D is efficient (inefficient), an R&D subsidy leads to a higher (lower) welfare level than an emissions tax, regardless of spillovers’ degree, because of a lower social cost. Consequently, for an abatement subsidy policy to be advantageous, a higher spillover rate suffices for a lower R&D efficiency. When a publicly owned firm operates in the market, the government is encouraged to adopt a subsidy policy, but it can also use a privatization policy. With inefficient green R&D and a low (high) spillover rate, the government should opt for an emissions tax and (not) privatize the state-owned firm. With efficient green R&D, a subsidy is better; however, privatization always damages welfare [10].

Those works relate to the current paper because of their comparative analysis of the different emissions reduction policies. However, rather than concentrating on the potential free-rider problems related to technological innovation, by assuming the absence of spillovers, this paper focuses more on the environmental and public finance impacts of those policies.

The contributions of Poyago-Theotoky (2003), Gautier (2015), and Kim and Lee (2024) analyze the effects of a policy mix based on a concurrent emissions tax setting and the provision of an abatement subsidy [11]. In a duopoly characterized by product differentiation, the work of Poyago-Theotoky (2003) analyses (under both Bertrand and Cournot competition) the optimal environmental policy mix when firms invest in environmental R&D to abate emissions. The social welfare maximizing government uses the combination of emissions reduction tools to address the market failure at work: under-production due to production technology, including emissions, over-production due to the pollution externality, and, even without spillovers, under-investment in R&D due to imperfect competition. The subsidy on green R&D is used to solve the R&D market failure, while emissions tax is addressed to product market failures, no matter what the competition mode is. The game has a three-stage structure. At stage one, the government commits to fix the optimal rates of the emissions reduction policy tools; at stage two, firms choose their level of environmental R&D; at stage three, firms compete in the market. The key findings are as follows. Under quantity (price) competition, the emission tax is always (generally) lower than the marginal environmental damage. However, with close substitute products, the emission tax equals the marginal damages, i.e. it approaches the first-best tax. Moreover, the emission tax under Cournot is always lower than under Bertrand competition. Concerning the R&D subsidies, both the degree of product differentiation and the initial emissions coefficient are decisive in defining their size. However, in general, the less differentiated products are, the higher the subsidy tends to be under Bertrand competition.

Ben Youssef and Dinar (2011) also use a three-stage game. At stage one, to incentivize abatement activities, the government chooses both a tax per unit of pollution and a subsidy per unit of R&D level of firms. R&D activities do not generate spillovers. The authors find that, with homogeneous goods, if the marginal damage cost of pollution is sufficiently low, then the regulator subsidizes pollution to rectify the distortion due to the output contraction of oligopoly. Moreover, if the marginal damage of pollution is sufficiently high, then the regulator taxes the R&D investment because firms may overinvest in research. Likewise, Gautier (2015) studies how product differentiation affects optimal policy and industry emissions in a Cournot oligopoly in which a social welfare maximizing government simultaneously chooses abatement subsidies and emission taxes, considering both an exogenous and endogenous number of firms. A high degree of differentiation leads the government to increase the tax rate because the available abatement technology can make subsidies too costly. Moreover, industries with high product differentiation may experience a rapid increase in emissions. To face this issue, environmental R&D needs incentivizing policies. As industries change their pollution-intensive degrees, the government adjusts the optimal policy, and its fine-tuning varies across industries depending on the different degrees of product differentiation because it needs to weigh the environmental damages as well as the distortions on the product market.

Kim and Lee (2024) study the interaction of the policy combination of emission taxes and green R&D subsidies emissions with the shadow cost of public funds and the efficiency of R&D, considering the presence of a public firm. The authors find that the policy mix can be implemented if the shadow cost is neither high nor low. However, the R&D efficiency of the green technology needs to be high. The privatization of public firms leads to a decrease of both the emission taxes and green R&D subsidy rates, with a consequent increase (decreases) in the possibility of implementing the policy mix of the emission tax (green subsidy) and is only implementable in the presence of a public firm. Finally, privatization is welfare improving when the shadow cost is low and green R&D is rather inefficient. The policy insight is that public ownership acts as a substitute for environmental policies; the shadow cost of public funds and the efficiency of green R&D play a pivotal role when privatizing public firms.

Those articles are associated with the present work because of their analysis concerning the simultaneous use of emissions reduction policy tools. Nonetheless, only Kim and Lee (2024) are concerned about the public finance aspects of those interventions. Moreover, given the presence of public firms in their study, those authors consider the role of the privatization policy as well, an aspect which is abstracted from the present work because the focus is on managerial private oligopoly firms.

Indeed, closely related to the focus of this work, the literature has expanded the basic oligopoly market framework by assuming a separation between ownership and control in firms and incorporating managerial delegation. In fact, firms in several oligopoly industries are usually run by managers. Regarding managerial delegation, in a duopoly context with homogeneous products, Bárcena-Ruiz and Garzón (2002) study the effects of delegating to managers the sales and pollution abatement choices in the presence of environmental tax and damage. In their model, environmental R&D does not generate spillovers. Pollution creates environmental damage distortion. However, managerial delegation allows firms to expand production levels: in such a way, the product market distortion (underproduction) is partially and indirectly corrected by the exercise of the market power of oligopolists. Given the presence of a manager, an additional stage is introduced in the game structure after the regulatory stage, in which owners decide (via a take-it-or-leave-it offer) or bargain with managers the size of the managerial incentive. Due to the larger production with respect to entrepreneurial firms, both environmental damage and marginal environmental damage are larger under managerial delegation, leading the government to set a higher environmental tax. Nonetheless, with expanded output, both environmental damage and consumer surplus increase; however, the positive effect of the latter overcomes the negative of the former, leading to an increase in social welfare. Pal (2012) extends the framework of Bárcena-Ruiz and Garzón (2002) to product differentiation, analyzing both quantity and price competition.

Poyago-Theotoky and Yong (2019) examined different managerial compensation contracts in a Cournot duopoly, for instance, an incentive-based executive compensation contract (a form of “self-regulatory” initiative) to stimulate better environmental performance (emissions reduction), conventionally denoted as “green” delegation versus the standard sales delegation. They build a three-stage game in which owners design the compensation contracts for their managers in the first stage before the emission tax level is set by the environmental regulator. Then, in the second stage, the regulator and the managers simultaneously decide on the emission tax and abatement levels, respectively. In the final stage of the game, managers choose output. In this framework, the emission tax acts as the policy-driving force directing firms to take on the “green” contract. By means of an exogenous comparison, the authors show that the efficiency level of green R&D investments is critical to determining the impact of an emissions tax on green R&D decisions. Buccella, Fanti, and Gori (2022) further extend Poyago-Theotoky and Yong (2019) developing a non-cooperative game with managerial quantity-setting firms in which owners endogenously choose whether to delegate output and abatement decisions to managers via a “green” delegation contract or a sales delegation contract. A substantial difference with respect to Poyago-Theotoky and Yong (2019) is that the government commits at the first stage to levy an emissions tax to incentivize firms’ emission-reduction actions. They show that, in such a game-theoretic approach, a plethora of equilibrium can emerge, depending on the public awareness toward environmental quality, ranging from the coordination game to the “green” prisoner’s dilemma [12].

Interestingly, Park and Lee (2023) propose a managerial contract which includes both environmental incentives and sales delegation in the compensation scheme. Park and Lee (2023) build a managerial delegation model with green R&D, which leads to the following results: (1) higher incentives than those under a single incentive scheme; (2) larger production and abatement efforts; (3) lower total emissions; and (4) profitability improvement than under a sales delegation. Therefore, an emission tax policy, together with firms’ compensation schemes embedding environmental performances, can curb market failure and improve welfare [13].

In a polluting managerial oligopoly, Xu, Yin, and Lee (2024) consider owners offering double managerial delegation contracts linked to relative profit performance and environmental performance incentives in the presence of emission taxes. They found that under quantity (price) competition, the government sets higher (lower) emission taxes, whereas the owners of the firm fix lower (higher) environmental performance and negative (positive) relative profit performance bonuses, leading to lower (higher) welfare levels. Considering the endogenous competition mode game, quantity (price) competition emerges in equilibrium when both green willingness to pay and product differentiation are low (high). Therefore, public education on eco-friendly behavior is vital for enhancing environmentally related incentives in the design of managerial delegation contracts. Noteworthy, fierce competition may harm consumers and society.

Unlike Lee and Park (2021a, b) and Kim and Lee (2024), this article investigates only private markets (therefore, there is no room for the privatization policy) as in Buccella et al. (2024), nonetheless, with respect to the latter work, it extends the analysis by considering the presence of managerial firms, in which ownership and control are separate. Moreover, it does not consider the presence of technological spillovers concerning the investment in “green” technology, therefore not focusing on the R&D investment distortion. Furthermore, with respect to Lee and Park (2021a, b), it differs about the production technology (convex) and environmental damage function (linear). However, as in Lee and Park (2021a, b) and Buccella et al. (2024), this paper stresses the role played by the interaction of societal awareness and technology in the choice of the optimal emissions reduction policy; nonetheless, with respect to Lee and Park (2021a, b), and similarly to Buccella et al. (2024), it performs an in-depth analysis of the impact of those policies on environmental quality, public finances, and overall social welfare.

The model

In a polluting duopoly sector of the economy with managerial firms, firm 1 and firm 2 produce homogeneous goods, and , and compete in quantities. Each firm uses a linear technology to produce the goods, leading to constant (marginal) costs, , which are set equal to zero for analytical tractability without loss of generality. Industrial production causes units of emissions (pollution), equal to (Ulph, 1996), in which is the abatement level to reduce the environmental impact. Abatement derives from an end-of-pipe cleaning technology available on the market to each firm. Such a technology treats the pollutant at the last stage of the production process, just prior to the release in the environment. One might think of exhaust-gas cleaning equipment such as “filters in a refinery’s pipe for CO2 reduction” (Asproudis & Gil-Moltó, 2015, p. 169) or scrubbers on smokestacks to reduce SOx emissions (flue gas desulfurization installation), which are not directly linked to output. However, the current state of the technology does not allow the complete elimination of emissions, i.e. [14].

Once the managers have decided on the abatement level, firm faces a fixed cost for the adoption of the abatement technology, given by , where the parameter , an exogenous index of technological progress, scales up/down the total investment cost. Lower values of reflect an efficiency improvement of the abatement technology so that the investment cost is less expensive. However, the adoption of the abatement technology displays decreasing returns to investment.

The index measures the environmental damage due to industrial production and assumes that (1) the environmental damage is a convex function of total pollution; and (2) the damage is exogenous for consumers (see van der Ploeg & de Zeeuw, 1992; Ulph, 1996). The exogenous parameter represents the weight the government attributes to the environmental damage, i.e. how the society (indirectly) cares about the environment: higher values of imply, ceteris paribus, that the society worries more about environmental issues.

The (inverse) market demand is linear, , in which is a positive parameter measuring the market size, is its slope, and is total supply. Without loss of generality, the demand parameters are fixed equal to [15]. Owners delegate the choice of output and abatement to managers by offering them a “take-it-or-leave-it” linear retribution scheme (e.g. Fershtman & Judd, 1987), with structure with the fixed part, assumed equal to zero, and the manager utility, given by , in which are the firm profits, and the incentive parameter attached to sales.

To evaluate the impact of each emissions tax and abatement subsidy, we built a three-stage non-cooperative game in which, at stage one (the regulator stage), a social-welfare-maximizing government commits to set optimally the rate of the environmental instrument(s); at stage two, owners set the managerial bonus in a standard sales delegation contract; at stage three (the market stage), managers simultaneously choose output and how much pollution to abate through a cleaning technology, taking as given the government’s choice. As usual, one uses backward induction to solve the game.

Emissions reduction policy 1: emissions tax

Consider first the case in which a social welfare maximizing government levies an optimal emissions tax per unit of output to incentivize emissions abatement (see, for instance, Buccella, Fanti, & Gori, 2021, 2024). The tax base of the firm i is (i.e. the remaining pollution); the government’s tax revenue per firm is , with to guarantee non-negative managerial bonuses in a duopoly [16]. Thus, the firm profit function and its manager utility are, respectively:

in which the superscript ET stands for “emissions tax.” At stage three of the game, managers simultaneously choose output and the abatement level. By cutting emissions, firms decrease production costs by an amount equal to the reduced tax burden. Making use of the profit function, maximization of the manager’s utility (1) with respect to and leads to the following first-order conditions:

The successive principal minors of the Hessian matrix and reveal that the stationary point is a maximum. The system of reaction functions (i) in (2) leads to the equilibrium output

An emission tax per unit of output increases the firms’ marginal production cost. Therefore, an increase in the tax rate shrinks output, i.e. . By abating emissions, firms decrease the fixed cost of the end-of-pipe technology as well as the per-unit marginal cost. On the other hand, the technological index affects only the cost-effectiveness of the end-of-pipe technology while it does directly affect the output decision.

At stage two, owners fix the optimal incentive of the managerial contract that maximizes (4), leading to the managerial bonus reaction function, . Solving the system of the bonus reaction functions, the equilibrium bonus is

Direct analytical inspection of (5) reveals that the higher the emissions tax rate is, the lower the bonus owners offer to their managers as owners soften output expansion to reduce the tax burden. Substituting (5) into (3) and using (ii) in (2), one obtains the expressions for producer surplus (), consumer surplus (, government’s budget (, and environmental damage under ET:

Social welfare is defined as , and at stage one the government sets the emissions tax that maximizes it:

The second-order condition for a maximum is satisfied. From (6), one derives that a positive optimal emissions tax exists (i.e. ) if and only if the environmental social awareness is sufficiently large, that is, .

Emissions reduction policy 2: emissions abatement subsidy

Let us now consider the case in which the government incentivizes emission cuts via a subsidy per each unit of pollution abatement (see Lee & Park, 2021a, b; Buccella et al., 2024). Thus, the government spends an amount of per firm. The profit function of firm and its manager utility are:

in which the superscript AS stands for “abatement subsidy.” As before, at stage three of the game, managers simultaneously choose output and the abatement level. Abatement decisions reduce the cost of the investment in cleaning technology. Maximization of the manager’s utility in (7) with respect to and leads to the first order conditions

The Hessian matrix reveals that the successive principal minors are and , therefore negative definite: the stationary point is a maximum. The system of reaction functions (i) in (8) yields in equilibrium:

An abatement subsidy incentivizes firms to reduce emissions, decreasing the fixed cost of the end-of-pipe technology. However, the per-unit marginal cost of production is unaltered: the managers’ production choices are subsidy-independent. Making use of (9) and condition (ii) in (2), one obtains the expressions for the profits

At stage two, owners fix the optimal incentive of the managerial contract that maximizes (10), leading to the managerial bonus reaction function, . Solving the system of the bonus reaction functions, the equilibrium bonus is

From (11), note again that the bonus is now unaffected by the emission reduction policy because it is not directly linked to output production. Using (11) and condition (ii) in (8), the expressions for the producer surplus, consumer surplus, the government’s budget, and the environmental damage under AS are:

The social welfare is , and at stage one, the government fixes the subsidy to maximize it:

The second-order condition for a maximum is satisfied. Equation (12) implies that an optimal feasible abatement subsidy exists (i.e. ) if and only if the environmental social responsiveness is not too large, i.e. . Analytical inspection of (12) also revealed that, if , then the conditions , , and are satisfied. Given the optimal subsidy in (12), the equilibrium profits of firm , the abatement level, the environmental damage and social welfare under AS are derived, reported in Table 1.

Emissions reduction policy 3: policy mix

Finally, let us investigate the case in which the government adopts a price-based policy mix of emissions tax and abatement subsidy to induce managerial firms’ emissions reduction activities. This policy allows the government to collect tax revenues, but, at the same time, it must incur expenditures to provide the subsidy.

The profit function of the firm and its manager utility now read:

in which the superscript PM stands for policy mix. As in the previous cases, at stage three of the game, managers decide on output and the abatement level at once. Maximization of the manager’s utility in (13) with respect to and leads to the first-order conditions

The Hessian matrix of (14) reveals that the signs of the successive principal minors are and , therefore is negative definite, and the stationary point is a maximum.

The system of reaction functions (i) in (14) yields the identical equilibrium output as in (3) and together with condition (ii) in (14), one gets the expressions for the profits

At stage two, owners set the optimal bonus of the managerial contract to maximize (15), leading to the reaction function, . Solving the system of the bonus reaction functions, the equilibrium bonus is

Substituting (16) in the output expression (3) and making use of condition (ii) in (14), one can derive after standard calculations the expressions for the producer surplus, consumer surplus, the government’s budget, and the environmental damage under PM are:

The expression of social welfare is now , and at stage one the government sets the rates of both emissions reduction policy tools (tax and subsidy) to maximize it:

The Hessian matrix of the social welfare expression reveals that the sequence of principal minors is and , therefore is negative definite: the stationary point is a maximum. Analytical inspection of (17) reveals that and : for the government, the two emissions reduction policy tools work as strategic substitutes. Solving the system of the first-order conditions in (17) results in the next optimal values of the two tools:

The government, with the design of the policy mix, attributes a different share of emissions tax and abatement subsidy on the public budget, which leads to a surplus or a deficit depending on the value of the parameters. Analytical inspection of (18) shows: 1) under policy mix, a positive optimal emissions tax exists if and only if the environmental awareness is appropriately large, that is, if and 2) the abatement subsidy always satisfies the condition . Moreover, if the condition holds, then the technical feasibility conditions , , and are always satisfied.

Price-based emissions reduction policies comparison and discussion

This subsection compares the outcomes under the three price-based emissions reduction policies to study their impact on managers’ pollution abatement decisions, environmental damage, public finances, and social welfare.

Some preliminary observations are in order. Let us consider the impact of the emissions reduction policies on the bonuses owners choose for the managerial contract.

1) Without considering the optimal emissions reduction policy rates, the bonuses the owners choose for the managerial contracts are such that . 2) Since in equilibrium , then .

Proof: The proof is straightforward because it follows from 1) a comparison of Equations (5), (11), and (16), and 2) direct analytical inspection after inserting Equations (6) and (17) into (5) and (16).

The rationale for this result is as follows. Emissions levels are directly linked to production. However, production choices do not depend on the size of the subsidies, which simply reduces the fixed cost of the abatement investment. On the other hand, taxation has a direct impact on the marginal production cost. Therefore, owners offer bonuses that are negatively related to taxes to avoid managers’ excessive output expansion. Moreover, since abatement activities are partially incentivized via the subsidy in the case of the policy mix, the government can set a lower tax rate when combined with this tool. Therefore, the owners do not need to contract too much output, and they can offer managers an incentive bonus higher than with the emissions tax alone.

As in Buccella et al. (2024), simple analytical inspection shows that and , and and : the higher the weight the government attaches to the environmental quality, the higher are the optimal emissions tax and subsidy rates the government sets to cut emissions when those tools are used separately. However, in the case of their simultaneous use, the government increases the tax and decreases the subsidy because the former tool has a positive impact on public finances while the latter worsens them.

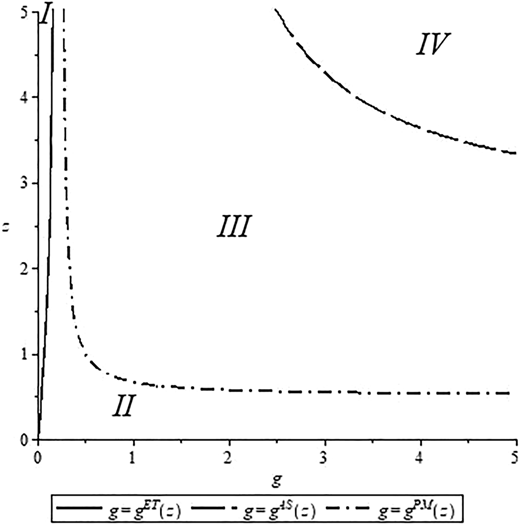

To begin with the comparisons, one must first characterize the parametric regions in which the three policies are technically feasible. Figure 1 graphically represents those areas.

1) For (Region I in Figure 1), the abatement subsidy is the only feasible emissions reduction policy. 2) For (Region II in Figure 1), abatement subsidy and emissions tax are both feasible. However, the emissions tax under the policy mix is still negative and unfeasible. 3) For (Region III in Figure 1), the government can implement all three emissions reduction policies. 4) For (Region IV in Figure 1), the emissions tax and the policy mix are the feasible policies.

Proof: The proof is straightforward, because it is sufficient to collect all the information obtained from the previous subsections. Indeed, 1) for , and , and; 2) for , and ; 3) for , , , and ; 4) for , , , and .

Lemma 2 qualitatively replicates the results of Lemma 1 in Buccella et al. (2024). In region I, the abatement subsidy is the unique, technically feasible policy that allows for cutting emissions. This result occurs because, with low environmental awareness, society prioritizes the negative impact of an emissions tax on production: the loss in consumer surplus outweighs the improvement in environmental quality. Thus, to incentivize emissions reduction, the government should provide an abatement subsidy because it does not affect the output level decision of managerial firms.

Nonetheless, a comparison between the feasibility thresholds of the three policies with entrepreneurial firms in Buccella et al. (2024) and those with managerial firms in the current framework reveals that, quantitatively, all of them shift leftward in the latter case (analytical details available upon request). In other words, the government can implement the emissions tax at lower levels of societal awareness. The rationale for this difference is that managerial firms, as well-known, have production levels larger than entrepreneurial ones. Therefore, at a given low level of environmental awareness, the larger production volume makes the negative impact of output reduction from taxation less significant for welfare.

Having identified the feasibility areas of the three policies, it is now possible to study their impact on the environment, public finances, and overall welfare. Let us first consider the abatement levels under the three policies. The analysis led to the following Lemma.

The equilibrium abatement levels under the three emissions reduction policies, , , and , are such that: 1) in region I, ; 2) in region II, ; 3) in region III, ; and 4) in region IV, .

Proof: The result directly derives from the comparison of the expressions of the abatement levels in Table 1.

Lemma 3 mirrors Lemma 3 in Buccella et al. (2024). The intuition behind this result is as follows.

In region I, the abatement subsidy is the only available emissions reduction. In region II, the emissions tax and the abatement subsidy are feasible. However, the provision of a “green” subsidy incentivizes abatement activities more than the emissions tax. The reason for this result is that abatement levels are linked to production, and the choice of output is subsidy-independent. On the other hand, taxation negatively impacts production. In region III, all policies are feasible. The mechanism in place is as in region II. However, as Lemma 1 shows, the emission tax leads owners to set a bonus that limits managers from significantly expanding production. This results in the lowest levels of production and abatement. Finally, in region IV, only the emissions tax and the policy mix are feasible; the abatement subsidy alone becomes too expensive for the public finances. In this region, characterized by high environmental awareness and low technological efficiency, the emissions tax rate, used as a single policy tool, is relatively high. Therefore, owners reduce the managerial bonus, with a substantial contraction of output levels. With a larger production due to a lower emissions tax rate in the policy mix, to keep abatement levels high, the combination with the abatement subsidy is required.

The results on abatement activities allowed us to consider the overall environmental damage, yielding the following Lemma.

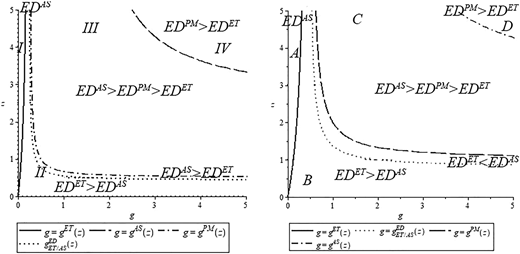

The ranking of the equilibrium environmental damages under the three emissions reduction policies are (see Figure 2): 1) in region I, ; 2) in region II, for , , while for , where ; 3) in region III, ; 4) in region IV, .

Environmental damage in equilibrium, managerial firms (left box) vs entrepreneurial firms (Buccella et al., 2024) (right box)

Environmental damage in equilibrium, managerial firms (left box) vs entrepreneurial firms (Buccella et al., 2024) (right box)

Proof: We obtained the results directly by comparing the expressions of the environmental damages in Table 1.

The interesting result of Lemma 4 relates to region II, in which the environmental damage under emissions tax can be higher than under abatement subsidy. The intuition behind this result is as follows. Due to taxation, managers receive a bonus inducing them to sell fewer products; with lower production levels, emissions are reduced as well. Nonetheless, the output restriction is small when (1) societal awareness is adequately low, for whichever technological level, and (2) the technology is inefficient, irrespective of the environmental awareness. In those cases, the emissions tax rate the government sets is low. As a consequence, the sales bonus owners offer decreases by a small amount, with a minor impact on output, the abatement level managers choose is still relatively low with respect to that of subsidization, and the overall effect is that emissions, and environmental damage, increase. This pattern replicates the one in Lemma 4 of Buccella et al. (2024). However, a graphical comparison (see Figure 2 above) reveals that, with managerial firms, the area in region II where enlarges and the area in which virtually vanishes. This is because the presence of sales delegation, even if the emissions tax reduces the value of the managerial bonus, leads to a percentage contraction of the production volumes lower than in the case of entrepreneurial firms.

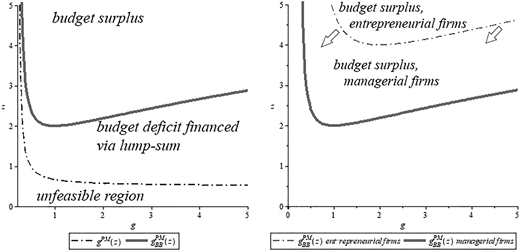

Now, let us study the impact on public finances, i.e. the effects of fiscal policy. An emissions tax allows the government to collect tax revenues, generating a budget surplus. The provision of an abatement subsidy creates a budget deficit; to finance the emissions reduction policy and have a balanced budget, the government can impose a lump-sum tax transfer (e.g. from consumers).

The case of the policy mix is more interesting. A closer analytical inspection of the budget expression under policy mix in Table 1 leads to the following Lemma.

The optimal emissions reduction policy mix generates 1) a budget deficit for that can be financed via a lump-sum transfer and 2) a budget surplus for where .

Proof: The result directly follows from the analysis of the numerator of the expression in Table 1.

In Figure 3, the left box, is the locus of pairs such that the government realizes a balanced budget; i.e. the share of the two policy tools on the final budget is identical. Inefficient abatement technology makes the cost of emissions reduction quite high. Subsidizing emissions abatement incentivizes both production and related abatement, but it generates further emissions, increasing environmental damage. However, subsidization is costly for the government, which decides to assign a larger weight to the emissions tax in the policy mix. The right box of Figure 3 compares the positive impact on the fiscal budget of the emissions policy mix when firms are managerial and entrepreneurial as in Buccella et al. (2024). An economy with managerial firms expands the parametric region in which the government implements the policy mix, generating a surplus. A direct comparison of the tool rates under policy mix with Buccella et al. (2024) reveals that and . The rationale for this result is straightforward: given the larger volumes of production in the industry with managerial firms, subsidizing emissions abatement activities can be expensive. Therefore, the government must reduce the subsidy rate, and to curb production and related emissions sets a higher tax rate.

Optimal emissions reduction policy mix and government budget with managerial firms (left box) and a comparison with entrepreneurial firms (right box)

Optimal emissions reduction policy mix and government budget with managerial firms (left box) and a comparison with entrepreneurial firms (right box)

One is now able to compare the overall welfare outcomes under the three price-based emissions reduction policies and derive the ranking of the most preferred ones for a social welfare-maximizing government, considering both the environmental and fiscal impact.

First, a comparison of the social welfare outcome reveals the following Lemma.

In region III, if , and if , where.

Proof: Considering Lemma 1, the proof follows from simple comparison of the welfare expressions in Table 1.

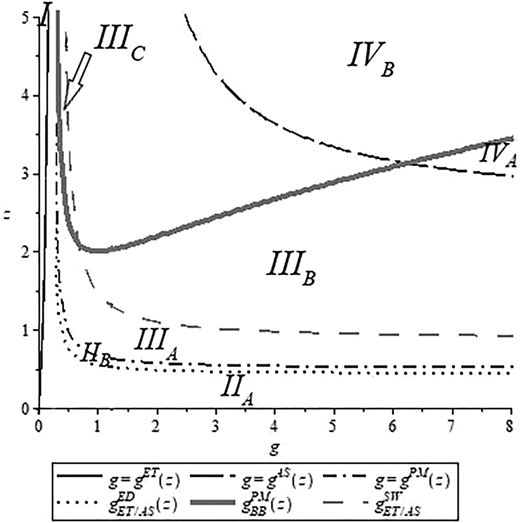

Making use of Lemmas 1–6, and the equilibrium values of the social welfare in Table 1, the next Proposition holds as follows.

The conditions , , , , and generate a set of parametric regions in which the emissions reduction policy of a social welfare maximizing government characterize as follows (see Figure 4):

in Region I: an abatement subsidy policy with a budget deficit financed via a lump sum transfer;

in Region II:

an abatement subsidy with a budget deficit financed via a lump sum transfer, generating the lowest environmental damage in Region IIA;

an abatement subsidy with a budget deficit financed via a lump sum transfer with the highest environmental damage in IIB;

in Region III:

a policy mix with a budget deficit financed via a lumpsum leading to second-best environmental damage in regions IIIA and IIIB;

a policy mix with a budget surplus leading to a second-best environmental damage in regions IIIC and IIID;

in Region IV:

a policy mix with a budget deficit financed via a lump sum leading to the highest environmental damage in region IVA;

a policy mix with a budget surplus leading to the highest environmental damage in region IVB;

Proof: (1) The result derives because, in region I, the abatement subsidy policy is the only feasible environmental policy. (2) In region II, both emissions tax and abatement subsidy are feasible, and analytical inspection reveals that , and from Lemma 4, one gets that in IIA, , and in IIB. 3) In region III, the ranking of the environmental damage is always . From Lemma 6, one has that, in region IIIA, the ranking of social welfare outcomes is while in region IIIB is , and from Lemma 4 one gets that the policy mix generates a budget deficit. On the other hand, in region IIIC, the ranking of social welfare outcomes is , in region IIID is , but from Lemma 5, one gets that the policy mix now generates a budget surplus. 4) In region IV, both emissions tax and the policy mix are feasible, and analytical inspection reveals that ; from Lemma 4, one gets that , and Lemma 5 reveals that the policy mix generates a budget deficit in IVA and a budget surplus in IVB.

As in Buccella et al. (2024), a consequence of Lemma 2 is that a low societal awareness (combined a fortiori with an inefficient abatement technology) can induce the government to nudge abatement activities only via subsidization. A substantial difference between this article and Buccella et al. (2024) is that a tax alone as an optimal emissions reduction policy does not arise, while the subsidy tool can be more extensively used. The rationale for this result is that more elevated production volumes with managerial firms lead the government to set a subsidy rate sufficiently low that does not generate large budget deficits. Thus, Proposition 1 suggests the following recipe for the policy makers: with managerial firms, the welfare-preferred price-based emissions reduction policy tool always includes the subsidization of abatement activities.

Conclusions

We analyzed the environmental and welfare effects of an emissions tax and an abatement (“green”) subsidy policy in a polluting managerial duopoly with homogeneous products. The “green” subsidy reduces the cost of investing in an end-of-pipe technology and leads to higher abatement levels than an emissions tax. However, an emissions tax decreases output, and thus the environmental damage, which positively affects social welfare. Having identified the feasibility space of the two policies, we obtained some policy insights. When societal awareness is low and the state of the cleaning technology is inefficient, the government can incentivize the managerial firms’ abatement activities via “green” subsidies, which lead in some cases both to the highest welfare associated with the lowest environmental damage. When societal concern increases and the cleaning technology is adequately efficient, the environmental tax generates the lowest environmental damage, and this positive effect tends to counterbalance the negative impact on firms’ profitability and consumer surplus because of output contraction, leading to the highest social welfare.

Although interesting, these results call for some robustness checks. The validity of those results requires tests in the presence of “green” compensation schemes related to environmental performances (emissions-cutting) that companies offered their managers, as in the works of Poyago-Theotoky and Yong (2019) and Buccella et al. (2022, 2023a, b), and Park and Lee (2023) (quoted in the literature review), and in Xu and Lee (2023). Furthermore, managerial delegation contracts require an in-depth analysis in contexts in which different ownership structures, such as common ownership or cross-ownership, exist (see Xing & Lee, 2024a,b), or in presence of consumers showing environmental awareness (Xu & Lee, 2024; Xing & Lee, 2024c). One limitation of this work is that emission taxes may induce owners to design other compensation schemes encouraging managers to invest in technologies that reduce pollutant emissions, a case here not considered. Finally, we find that another suitable step would be to conduct an empirical analysis to test the theoretical predictions concerning the design and implementation of the environmental policies.

Notes

Kiuila, Wójtowicz, Żylicz, and Kasek (2016) pinpoint that unilateral carbon abatement policies can be ineffective because a large part of emissions reduced in a set of countries (for instance, those included in Annex I of the Berlin mandate in 1995) may be offset by an increase in emissions in the rest of the world. Therefore, only a global action could result in global climate protection: regional policies can prove to be insufficient.

For instance, Shindell (2015) proposes an economic valuation framework, the Social Cost of Atmospheric Release, which extends the previous Social Cost of Carbon used exclusively for carbon dioxide, to assess the impact of a broader range of pollutants, not only on climate damages but also on health impacts of air quality.

No matter whether policy makers use a first- or second-best Pigouvian approach, an estimate of the marginal damage from CO2 emissions remains necessary (Metcalf, 2021).

The US have not implemented a carbon tax, neither at federal nor at state level. Nonetheless, there are a few studies that have analyzed the potential distributional (per income levels and across regions) effects of the introduction of a such a tax (see, e.g. Hassett, Mathur, & Metcalf, 2009; Mathur & Morris, 2014). Kiulia and Ślezinsky (2003) have conducted a similar study for Poland. Making use of 30 years of data on carbon taxes in several European countries, Metcalf and Stock (2023) have estimated their macroeconomic impacts on GDP and employment growth rates, finding a zero/modest positive impact on these variables. Moreover, for a $40/ton CO2 tax covering 30% of emissions, they found a cumulative emissions reduction on the order of 4 to 6%.

Various environmental policy instruments concerning issues not related to climate change were introduced in many countries already in the early 1970s (e.g. in the US and Germany), and in the 1980s and 1990s in all Europe (for example, the acid rain control policies, see Smith, 2011).

Geels, Sovacool, Schwanen, and Sorrell (2017) underline that the process of decarbonization needs a transformation of “sociotechnical” systems, i.e. the interlinked mix of technologies, infrastructures, organizations, markets, regulations, and user practices. Given the choice of the exogenous parameters of the model, this work allows to conduct, in an extremely simplified framework, a preliminary “sociotechnical” analysis of different emissions reduction policies.

With regard to quantity-based mechanisms (not covered in this article), the following researchers studied the subject of emissions standards in oligopoly markets: Besanko (1987), Ebert (1999), Montero (2002), Moraga-Gonzalez and Padron-Fumero (2002), Farzin (2003), Bruneau (2004), Kayalica and Lahiri (2005), Amir and Nannerup (2005), Requate (2006), Lahiri and Ono (2007), Carrión-Flores and Innes (2010), Heuson (2010), Perino and Requate (2012), Bárcena-Ruiz and Campo (2017). Amir, Gama, and Werner (2018), and Garella and Trentinaglia (2019). On the other hand, tradeable emissions permits are the focal point of studies by Mørch von der Fehr (1993), Sartzetakis (1997, 2004), Carraro (2002), Liski and Montero (2005), David and Sinclair-Desgagné (2005), Requate (2006), Meunier (2011), Tanaka (2012), Hepburn, Quah, and Ritz (2013), and more recently Garcia, Leal, and Lee (2018).

Scholars have further investigated the impact of emissions taxes on additional aspects in oligopoly contexts. In a polluting Cournot duopoly with firms adopting an end-of-pipe technology, Poyago-Theotoky (2007) studies the impact of emissions taxes on coordination in emission-reducing R&D activities with spillovers (which generate the market failures due to the public good nature of the knowledge and information concerning the innovation process), analyzing whether this is socially desirable when the government is unable to pre-commit to the tax rate. The key results are as follows. When the environmental damage is small, the R&D investment and social welfare under coordination are higher than under independent R&D. The same result occurs for large damages when the available R&D technology is efficient. On the other hand, when the environmental damage is large and R&D technology inefficient, the opposite result holds. In a corrigendum, Poyago-Theotoky (2010) shows that, when Cournot duopolists create large product market inefficiencies, a negative emission tax (i.e. emission subsidy) can be partially justified to corrects them. Moreover, recently, scholars have extended the basic oligopolistic framework to include into the analysis further elements the earlier literature has not considered: Ouchida, Okamura, and Orito (2019) and Buccella et al. (2021) explore the endogenous decision whether to abate emissions in the presence of emissions taxes, while Bansal and Gangopadhyay (2003) consider taxation with consumers environmentally concerned, and Xu, Chen, and Lee (2022) and Xu and Lee (2022) firms engaging in environmental corporate social responsibility. Despite their relevance, this article does not cover these subjects.

Other recent works analyzing the organization of environmental R&D activities in presence of emissions tax/subsidies are Nimubona and Benchekroun (2015) in vertically related markets with upstream eco-firms, Ouchida and Goto (2016a, b) who consider different environmental R&D organizations mode (environmental research joint venture cartelization environmental R&D competition, environmental R&D cartelization, and environmental research joint venture competition), Iida (2020) in an international trade context, Wu, Zhang, and Chen (2021) and Yang, Kong, Liu, and Ang (2022) in a full green supply chain. Moreover, other significant branches of the literature analyze (1) the link between environmental policies and market structures, see the works of Lee (1975), Smith (1976), Oates and Strassmann (1984), Conrad and Wang (1993), Lee (1999) Althammer and Bucholz (1999), Katsoulacos and Xepapadeas (1996), Fujiwara (2009), Cato (2010), Lambertini, Poyago-Theotoky, and Tampieri (2017) and Espínola-Arredondo, Munoz-Garcia, and Liu (2019), inter alias; and (2) product differentiation and different types of competition, see the contributions of Requate (1993b), Innes and Bial (2002), Brécard (2011) and Lee and Xu (2018). Those topics, however, are beyond the scope of this research.

Bian and Zhao (2020) analyze the effects of emissions abatement subsidy and emissions tax on a supply chain in which the manufacturer invests in emissions abatement technology and distributes products via competitive retailers. The provision of subsidies gives the manufacturer greater incentives than taxation to cut pollution, leading to higher profits for the distribution channel. Nonetheless, when abatement activities are costly and emissions highly damaging, the tax policy should be implemented because the subsidy policy leads to lower social welfare and environmental performance. Moreover, if the environmental damage of production is high under the subsidy policy or low under the tax policy, then the manufacturer has no incentive to improve abatement efficiency.

In a vertically related market, David and Sinclair-Desgagné (2010) study a policy mix of emissions taxes and abatement subsidies when downstream polluting firms buy end-of-pipe emissions-reduction technologies from an upstream oligopolistic eco-industry. In such a framework, taxing emissions while subsidizing polluters’ abatement efforts do not lead to the first-best social welfare. The rationale for this result is that firms in the eco-industry would be allowed to increase their prices to grab the subsidy provided to downstream polluters. However, if the government subsidizes the output of the eco-industry, the opposite holds. If public transfers create distortions, social welfare can be higher if the regulator sets only emissions tax. However, if the eco-industry is concentrated, to subsidize abatement activities of suppliers while taxing emissions is optimal.

A few contributions consider emissions reduction policies in the presence of institutional actors in labor markets such as unions (see, inter alias, Campo, 2004; Bárcena-Ruiz & Garzón, 2003, 2009; Bárcena-Ruiz, 2011; Wang & Ouattara, 2020; Buccella et al., 2022).

Lee and Park (2021b) investigate the strategic use of corporate environmentalism in a managerial delegation contract in a duopoly with product differentiation in which polluting firms buy abatement technology from an eco-industry. A cost pass-through effect under price competition exists, which can restrict the output of polluting firms but increase their profits. Under an abatement subsidy policy, the government can induce the firm’s profitable environmental concern to be socially desirable by substituting the output-restriction behavior with the adoption of abatement technologies: Pareto-improving alignment between private and social incentives is feasible and attainable.

Buccella et al. (2021, Appendix A) provide analytical details supporting the assumption of an abatement technology not allowing an entire pollution elimination. This assumption follows Ulph (1996), and it differs from Asproudis and Gil-Moltó (2015) where emissions are , with a fraction of total production.

Indeed, neither the market size, nor the slope of the market demand and the average and marginal costs affect the feasibility thresholds, profit differentials, environmental damage, and social welfare functions in our quantity-setting duopoly.

This assumption does not need to hold in a more general oligopolistic competition framework, especially when an endogenous market structure with free entry. In fact, the emission tax might be much higher than (or equal to) marginal damage, depending on the curvature of market demand (Lee, 1999). We are grateful to an anonymous referee for having signaled this result.