The alienation of megaproject environmental responsibility (MER) behavior is destructive, but its mechanism has not been clearly depicted. Based on fraud triangle theory and the fuzzy set qualitative comparative analysis (fsQCA) method, this study explored the combined effect of antecedent factors on alienation of MER behavior.

Based on the fraud triangle theory and literature review, eight influencing factors associated with the alienation of MER behavior were first identified. Subsequently, the fuzzy-set qualitative comparative analysis was used in this study to reveal configurations influencing alienation of MER behavior.

The study found nine configurations of MER behavioral alienation antecedent factors, integrated into three types of driving modes, i.e. “economic pressure + learning effect,” “institutional defect + moral rejection,” and “information asymmetry + economic pressure + expectation pressure.”

By analyzing the configuration effects of various induced conditions, this study puts forward a comprehensive analysis framework to solve the alienation of MER behavior in the megaprojects and a practical strategy to control alienation of MER behavior.

1. Introduction

In China, large-scale infrastructure projects such as airports, highways, high-speed rails, dams, and exhibition facilities have emerged one after another. The total construction of megaprojects and the scale of single projects are second to none worldwide (Shen et al., 2012). Megaprojects have an important effect on aspects such as social development, economic development, scientific and technological development (Pitsis et al., 2018; Wang et al., 2017), and become the lifeline of national economic and social development. Furthermore, megaprojects are usually a large spatial scale entity, and they have a huge scope of influence and radius of influence on the surrounding ecological environment. However, due to the complexity and diversity of the environmental issues (Wang et al., 2017), the negative effects of such construction activities on the surrounding environment and the degree of environmental damage are unknown and unpredictable. For example, the South-North Water Transfer Scheme involves numerous environmental problems that need to be considered and solved (Changming, 1998).

Megaproject environmental responsibility (MER) refers to the decisions and activities of participated stakeholders that benefit the environment during the entire megaproject life cycle (Wang et al., 2017). It is a concept imbedded in the idea of megaproject social responsibility and it is an important part and manifestation of megaproject social responsibility. Undertaking responsibility of environmental protection is core content of MER (Zhou and Mi, 2017). The sustainable development of megaprojects has attracted a sharp increase in attention; megaprojects increasingly emphasize the coordinated and unified development of society, the economy, and the environment (Wang et al., 2020). Improving the environmental performance of megaprojects is one of the most urgent and prominent goals of megaproject management (Locatelli and Mancini, 2013; Wang et al., 2017).

The alienation of MER behavior that project participants harm environment interests of megaprojects to serve their own interests is the antithesis of environmentally responsible behavior. Many environmental conflicts and devastation caused by alienation of environmental responsibility behavior occur in megaprojects (Lee et al., 2017). For example, Chile's government with an “economic growth first” mentality, formulates permissive institutions and pursuit of large-scale investment at a high environmental cost, such as the Ralco and Pangue dams (Nasirov et al., 2018; Risley, 2014). The Three Gorges Project has been controversial because of its ecological environment destruction (Wu et al., 2003). Environmental issues caused by improper behavior have elicited increasing attention worldwide, forcing megaprojects to solve environmental responsibility issues and to promote environmental management of megaprojects effectively (Wang et al., 2018).

However, the existing studies related to alienation of environmental responsibility behavior mainly focus on publicly listed firms (Lin et al., 2016; Wu et al., 2021; Wu, 2014; Zhang et al., 2020) with less attention in project settings, especially in megaproject settings. Compared with the traditional construction projects, megaprojects have become a new organizational context (Li et al., 2019). The inherent characteristics of megaprojects spark greater interest to megaproject-based alienation of environmental responsibility behavior research: (1) Megaprojects have significant environmental impacts (Wang et al., 2017). The potential risk of alienation of environmental responsibility behavior is enormous. The Three Gorges Dam will spend more than $26.45 billion on environmental governance over the next decade due to its huge impact on the environment (Stone, 2011). (2) The failure of megaprojects attracts more attention than its successes, and sometimes it is exaggerated by the media (Ma et al., 2017). Once alienation of environmental responsibility behavior occur in megaprojects, which attracts more attention than traditional projects, causing serious damage to the project image and corporate reputation. (3) Megaprojects are faced with complex internal and external environments and high levels of uncertainty and ambiguity (Nachbagauer and Schirl-Boeck, 2019), which induces opportunistic behavior tendencies (Wang et al., 2019). The probability of alienation of environmental responsibility behavior is higher in megaprojects than in traditional projects. In the light of the above characteristics, project managers try to curb alienation of MER behavior through a series of measures, such as environmental impact assessment, environmental supervision (Yang, 2017). Alienation of MER behavior is in the complex situation between stimulation and containment.Therefore, all the aforementioned analysis point toward the necessity of specific research on curbing alienation of environmental responsibility behavior within megaproject settings.

Furthermore, megaproject literature related to environmental responsibility behavior has focused predominantly on “doing good” (Wang et al., 2017, 2018), with negative accounts remain largely unexplored. The scattered studies have also focused largely on specific factors, such as environmental regulations, government subsidies, that affect some sort of alienation of environmental responsibility behavior in traditional construction project (He et al., 2020; Zhu et al., 2018). However, there is limited understanding about the various causal patterns involved in alienation of MER behavior. Aforementioned studies employ regression analysis or game theory, which might contradict the fact that behavior is generally driven by multiple components in combinational form (Michie et al., 2011). In addition, regarding implications on governance, previous research usually offer one optimized path rather than several alternative strategies, which is difficult for all managers or policymakers to follow due to the differences among megaprojects. Fuzzy-set qualitative comparative analysis (fsQCA) could provide a method for digging deeper into the data to reveal finer-grained detail about the research objective. With fsQCA, antecedent variables' potential interdependence, asymmetric data relationships, and multiple equal-effective paths to the same outcome can be recognized (Douglas et al., 2020). Therefore, to fill these voids and to offer insights into the alienation of MER behavior, the proposed question of this study is:

On the basis of fraud triangle theory, what configurations of factors are associated with the alienation of MER behavior, and how to govern this behavior?

To answer this question, this paper draws on fraud triangle theory and the fsQCA approach to explore the causal patterns of factors that induce alienation of MER behavior. Fraud triangle theory could be applied to dig deeper into the antecedents of alienation of MER behavior. Fraud triangle theory suggests that the causes of fraud usually comprise three factors: pressure, opportunity, and rationalization (Mansor and Abdullahi, 2015). Specifically, using a sample of 160 respondents and based on fsQCA, this paper explores the core and auxiliary conditions of the configurational effects on the alienation of MER behavior and identifies equivalent configurations that lead to the alienation of MER behavior. Instead of focusing on the independent effects between the alienation of MER behavior and its antecedents, the goal of this study is to capture configurations that induce alienation of MER behavior. This article therefore makes an important contribution to the budding literature on the alienation of MER behavior. The research results can provide a reliable theoretical basis and practical reference for the management of the alienation of MER behavior.

2. Theoretical background and research model

2.1 Defining alienation of MER behavior

Although alienated environmental behavior was mentioned by Peng et al. (2021), the notion of alienation of MER behavior has not been addressed directly in the literature, and the concept remains blurred and in need of definition. To that end, two main concepts as the main foundation are used for developing the definition of alienation of MER behavior. One is environmentally responsible behavior that is a generally accepted name. Various definitions of environmentally responsible behavior have emerged (Cottrell and Graefe, 1997; Mobley et al., 2010; Stern, 2000). Environmentally responsible behavior might include any of a wide range of actions and is often used interchangeably with other terms such as pro-environmental behavior, green behavior, environmentally friendly behavior, and eco-friendly behavior (Su et al., 2020). These definitions in common are to avoid the destruction of environmental resources and protect environmental resources. The other is alienation that is used and examined in a broad range of disciplines such as philosophy, sociology, psychology and organizational sciences (Chiaburu et al., 2014; Johnson, 1974). Alienation as a concept has lent itself to various definitions. Nair and Vohra (2012) reviewed existing concepts that have some overlap with alienation and found that alienation sometimes is viewed as the polar opposite of any one concept. The philosopher Hegel understood alienation as the transformation to the opposite of things, which is a philosophical concept (Rae, 2012). For instance, alienation and job involvement were obverse constructs (Chiaburu et al., 2014).Thus, the alienation of MER behavior could be defined from the irresponsible perspective.

Social irresponsibility and social responsibility are two ends of a continuum; a negative opinion that environmental degradation and pollution are inevitable and little precaution is taken reflects environmental irresponsibility (Jones et al., 2009). Generally irresponsibility involves “a gain by one party at the expense of the total system” (Armstrong, 1977) and is marked by short views, self-righteousness, hypocrite, and disdain for the common interest (Ferry, 1962). In this paper, alienation of MER behavior is referred to the specific irresponsible behavior that stakeholders participated through the whole project life-cycle, out of consideration of their own interests, harm environment interests of megaprojects. Considering self-interest includes seeking illegitimate interests, saving costs, and evading punishment. In the process of dealing with or responding to MER, environmental greenwashing, free-riding, collusion, and opportunistic behaviors all belong to the category of alienation of environmental responsibility behavior.

2.2 Fraud triangle theory

Fraud triangle theory is a classic theory to analyze fraud behavior, including three core conditions: opportunity, pressure, and rationalization (Cressey, 1953). The core framework of the fraud triangle is shown in Figure 1. These three factors do not act independently, but are interrelated and interactive (Burke and Sanney, 2018; Cressey, 1953). For example, although no reasonable excuse can address moral evasion, when the participating entity is under considerable pressure and in an environment with great opportunities for fraud, the participant is likely to commit fraud. Therefore, the fraud triangle theory and QCA fit well.

Fraud triangle theory has not only been used to study the problem of fraud (Awang et al., 2020) but also has been widely used to analyze the causes of various opportunistic behaviors such as CEO wrongdoing (Schnatterly et al., 2018), greenwashing (Kurpierz and Smith, 2020) and corruption in the construction industry (Bowen et al., 2012). Existing studies indicate the appropriateness of applying the fraud triangle theory to the study of opportunistic behavior in various fields.

2.3 Theoretical analysis

Williamson (1973) believed that the behavior of pursuing self-interest and employing deceitful strategies is opportunistic. The core characteristic of opportunistic behavior is to injure others for self-interest. Alienation of MER behavior refers to the action that project participants harm environment interests of megaprojects to serve their own interests. The alienation of MER behavior is, in essence, a behavior that damages the interests of others for one's interests, in line with the characteristics of opportunistic behavior proposed by Williamson. Therefore, adopting the fraud triangle theory to study the alienation of MER behavior is appropriate. Fraud triangle theory can organically integrate the internal and external situation characteristics of the organization into the analysis of the formation of opportunistic behavior and can reveal the complex equal-effective paths of the alienation of MER behavior.

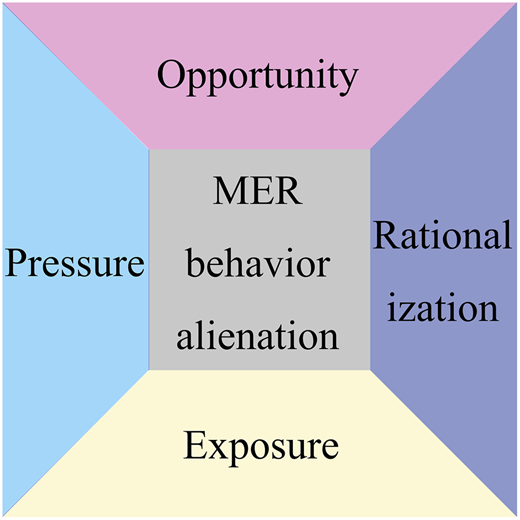

On the basis of a literature review and the incentive framework of opportunity, pressure, and rationalization in fraud triangle theory, this study preliminarily conducted semi-structured interviews with industry experts. They believed that using the fraud triangle theory to study the factors influencing the alienation of MER behavior is appropriate. However, the experts also pointed out that the fraud triangle theory was initially used to study the opportunistic behavior of enterprises or individuals. Megaprojects will have a huge effect on society, economy, and the environment at the community, regional, and national levels (Zeng et al., 2015), and their construction process is closely concerned by stakeholders such as the media, the public, and non-governmental organizations (NGOs). More attention should be paid to the influence of the supervision and exposure of organizations such as the media, the public, and NGOs on the alienation of MER behavior. Therefore, on the basis of the fraud triangle theory, combined with megaproject situations and expert opinions, this study adds the dimension of exposure and forms the research framework for the alienation of MER behavior in Figure 2.

2.3.1 Opportunity dimension

Opportunity is the internal and external condition for the alienation motive of environmental responsibility behavior to be transformed into actual action. Two main types of opportunities promote the alienation of MER behavior. The first is the institutional defect, namely, the lack of institutional supervision. The flexibility of environmental regulation policies and the uncertainty of regulatory effectiveness are important factors that induce greenwashing behavior (Feinstein, 2013). At the same time, the absence of supervision will lead to the ineffective implementation of relevant systems, resulting in the alienation of MER behavior. Environmental pollution problems are mostly caused by imperfect supervision systems and insufficient awareness of environmental responsibility (Zuo et al., 2017). Inadequate government supervision will trigger environmentally damaging greenwashing behavior of contractors (He et al., 2020). The existence of loopholes in the system or deficiencies in supervision undoubtedly creates an opportunity for the participant. Thus, project participants will take advantage of loopholes or defects of laws and regulations to seek improper benefits, especially in the context of low penalty costs after the discovery of the alienation of MER behavior.

The second type is cognitive information condition, namely, information asymmetry. Due to the complexity of its own and the external environment, large-scale projects are faced with high uncertainty. Therefore, project participants are often in situations of incomplete and asymmetric information (Wang et al., 2019). Information asymmetry increases the risk of environmental opportunism in the environmental field (Chen and Liang, 2016). Through comprehensive sharing and exchange of information in the process of megaproject construction, reducing information asymmetry among participating entities can promote themselves to fulfill social responsibilities of megaprojects to a certain extent (Wang, 2015). Thus, information asymmetry provides opportunities for the alienation of MER behavior and urges the participant to transform the alienation idea and intention of MER behavior into alienation action.

2.3.2 Pressure dimension

Pressure, including endogenous pressure of the organizations and exogenous pressure from the external environment, is the motive that directly drives the participating entities to implement alienation of MER behavior. Endogenous pressure mainly refers to the endogenous pressure on the subject formed by the profit-seeking nature of the subject in pursuit of profit maximization. Under the hypothesis of egoism, the alienation of MER is a rational choice of the participating units and a reflection of the profit-seeking nature. In other words, the pursuit of economic interests is the internal cause of the alienation of MER behavior. From the perspective of revenue-cost, the participating entity implements alienation of MER behavior because this behavior is expected to bring attractive economic benefits that are usually greater than the potential costs that may be paid. For instance, direct benefits brought by improving environmental protection are often lower than the cost input of contractors (Ofori et al., 2000). The investment of environmental protection measures and environmental protection equipment is the greatest obstacle for megaproject enterprises to adopt environmental management behavior (Zeng et al., 2003). The economic viability of contractors has a significant effect on their construction waste management behaviors. In the interview research process, interviewees even emphasized that if violating environmental or environmental laws and regulations is the most profitable choice, then they are likely to choose this choice, especially when they think that the consequences will not be serious (Wu et al., 2017). Therefore, driven by the nature of profit-seeking, the opportunism tendency of the participating units will be stimulated, and they will act improper environmental behaviors to seek their own interests, that is, they will implement alienation of MER behavior.

In the aspect of exogenous pressure, external expectation pressure is an important reason for the deceptive environmental behavior of the participating units. From the perspective of strategic management theory of environmental adaptation paradigm, only by adapting to the external environment can megaprojects and participating units survive and develop and achieve success. At present, the concept of sustainable development is increasingly emphasized in social development (Reyers and Selig, 2020), and the public has increasingly felt the importance of sustainable development. The public expects participating units to play a role in environmental protection. In this context, if the environmental pollution and ecological destruction of the participating units in megaprojects are exposed by society, the development and survival of the participating units will undoubtedly be inhibited. In an environment with high public expectations, participating entities are likely to cater to society's expectations with fraud, or even deceive the public, hide their negative aspects, and create a responsible image, such as implementing environmental greenwashing behavior.

2.3.3 Exposure dimension

Exposure is meant to expose or reveal. The exposure factors usually include two aspects: the probability of discovery or disclosure and degree of punishment (Ye et al., 2018). In this study, the concept of exposure is used to refer to the possibility that the alienation of MER behavior is exposed and the degree of punishment when the alienation of MER behavior is exposed. Exposure will affect the pre-judgment of the participating units and the decision of whether to perform alienated behavior. The pre-judgment of the participating units in the implementation of MER behavior is inclined to the decision with low exposure possibility. On the basis of government supervision, “dishonest list disclosure” can effectively curb the environmental greenwashing behavior of construction units in a high-speed railway project (He et al., 2020). The complexity of megaprojects leads to the complexity of MER alienated behavior to a certain extent, and information asymmetry exists between internal stakeholders and external stakeholders in megaprojects. External stakeholders such as the media and the public identify and discover MER alienated behavior with difficulty. Therefore, the possibility of MER alienated behavior being discovered and exposed is often small. Moreover, the exposed alienation of MER behavior, in reality, is only the tip of the iceberg. The possibility of exposure is very slight, undoubtedly providing a favorable external environment for the participating units to implement the alienation of MER behavior.

After the alienation of MER behavior is exposed, the government punishment is a conventional sanction means to eliminate alienated environmental behavior (He et al., 2020; Sun and Zhang, 2019). Minimize the probability of evading punishment and increase the cost of punishment for environmental violations, which can improve the effectiveness of environmental regulations and reduce the participating units' environmental opportunistic behavior (Min-li, 2011). After alienation of MER behavior is exposed, the participating entities will only be punished lightly, so they will frequently decide to implement the alienation of MER behavior. In addition, according to deterrence theory (Apel, 2013), when the punishment intensity is insufficient, it cannot form an effective deterrent effect. Thus, the participating entities may implement the alienation of MER behavior when the punishment for alienation of MER behavior is insufficient to form a deterrent effect.

2.3.4 Rationalization dimension

Rationalization is usually a self-deceiving reason. This concept indicates that the fraudsters must formulate some morally acceptable reasons before engaging in unethical behavior, rationalizing their improper behavior (Mansor and Abdullahi, 2015). Two common rationalizations are given for the alienation of MER behavior. The first is the learning effect, that is, the project participants learn from other persons in the social environment. Individual cognition and social environment can affect human behavior, and most of the human behavior is acquired through observing and learning the behavior of others (Bandura and Walters, 1977). When enterprises damage the natural environment without being punished, more enterprises will blindly follow this improper or even illegal behavior (Li and Wang, 2016). Similarly, the occurrence of the MER alienated behavior is likely because they have observed that other participating entities implement alienation of MER behavior for profit without being punished severely and then blindly imitate and learn such behavior. Thus, the learning effect likely affects the alienation of MER behavior.

The second rationalization is moral disengagement, that is, the specific cognitive tendency of the participating units, which will redefine the attribution of responsibility to minimize their own responsibility in the consequences of their actions (Cao, 2020). Moral disengagement, such as favorable comparison, attribution of responsibility, and moral defense, is often used by the participating entities implementing the alienation of MER behavior to excuse their own behavior. For example, this reason that “not for personal gain but for the smooth promotion of the project or the collective interests of the project” is often used as an excuse. Thus, the organization that implements the alienation of MER behavior may seek the moral criterion for its own unethical behavior through redefining its behavior and finally protecting itself from the rebuke of its conscience.

On the basis of extended fraud triangle theory, this study establishes a model to explore the configurational effect of eight factors (i.e. institutional defects, information asymmetry, economic pressure, expectation pressure, exposure possibility, penalties, learning effects, and moral disengagement) on the alienation of MER behavior and reveals the equivalent paths that result in high levels of alienation of MER behavior.

3. Methodology

3.1 Data analysis method

The occurrence of things or phenomena is often not the result of the independent action of the antecedent factors but rather the result of the joint action of many antecedent factors. Traditional quantitative analysis methods often focus on the net effect of a single antecedent factor on the results, such as structural equation models and linear regression (Rihoux, 2003). Although such research methods have applicability in the study of the effect of a single antecedent factor on the results, they ignore the correlation among the antecedent factors. From the perspective of configuration, QCA is suitable (Fiss, 2007). QCA can explore the configuration among antecedent factors and the combined effects of various configurations on the results (Liu et al., 2017). At present, most of the research on configuration theory adopts QCA.

QCA resides comfortably in a central position between qualitative and quantitative research (Rihoux, 2003). QCA can see a problem as the result of the interaction of multiple factors, the combination of which is called the configuration. In addition, QCA can use multiple case studies and Boolean algorithms to find the configuration and core factors that can produce a result. At present, QCA has been widely used in various disciplines. QCA has three main advantages. First, QCA is applied to a wide array of case samples (Kraus et al., 2018; Wagemann et al., 2016), and does not require a specified sample sizes compared with regression analysis. Second, fsQCA explicitly allows for equifinal causal conditions of different combinations, which is more in line with the epistemological basis of social science research (Wagemann et al., 2016). Third, the basic principle of QCA comes from set theory, which mainly emphasizes the asymmetric causal relationship between configuration and results, and avoids focusing on net effects and the threat of multicollinearity (Gligor and Bozkurt, 2020). QCA is a new method for analyzing complex causality in configuration problems based on Boolean algebra and set theory. As a new method that combines quantitative and qualitative comparative analysis, QCA provides a new approach for the study of complex causality in management.

3.2 Measures

The first part of the questionnaire has questions about the demographic profile of the responders (e.g. age, gender, education), and the second part has measures of the constructs chosen to be examined. A five-point Likert scale anchored from 1 (completely disagree) to 5 (completely agree) was employed. The respondents were asked to answer questions based on their last megaprojects experiences about project environmental practices. The measurements were initially developed and adapted from previous literature and ultimately revised by a pilot study showing in the supplementary file. The supplementary file presents all constructs along with descriptives and the literature adapted for questionnaire development.

3.3 Data collection

To ensure the validity of the survey data, this study followed standard questionnaire design norms and modified and improved the questionnaire through pre-test, forming the final questionnaire. This research takes the management personnel in megaprojects as the targeted respondent. Following the research of Wang et al. (2018) and Xie et al. (2021), China's megaprojects can be defined as mega infrastructure projects costing over 1 billion RMB. The investigated megaprojects include Humen Bridge; Hong Kong–Zhuhai–Macao Bridge; Nanning Airport terminals, Han Ten High-Speed Rail; Zhumadian International Conference and Exhibition Center; West Changzhutan Circle Inter-City Railway; JinHong Highway; Changjinghuang Railway; West Silver High-Speed Railway; Jiang Xining Wisdom Male High-Speed Highway; Beijing, Qingdao Metro Line 6; South Jade Railway, Long Tunnel Engineering Yong Railway; and Guangzhou Metro Line 11. The investigated megaprojects are distributed in all over China, reflecting the practice of megaprojects in China to a certain extent.

Questionnaire design and data collection took place from June 2020 to November 2020, when China was in a period of strict epidemic prevention and control. Given the impact of the COVID-19 epidemic, this study used an online questionnaire sent to management personnels of the investigated megaprojects. A snowball sampling technique often used in online questionnaires was utilized to maximize the number of qualified respondents (Biernacki and Waldorf, 1981). This method enables researchers to recruit respondents with similar experience or skills and has been widely used in several research fields. A total of 222 questionnaires were collected, and 160 valid questionnaires were obtained through three questionnaire screening procedures, with an effective recovery rate of 72.07%. The three screening processes are as follows. (1) The questionnaires with too short answer time and incomplete questionnaire filling were eliminated. (2) Questionnaires with the same answer rate of more than 80% were excluded. (3) The questionnaire item “Do you understand the performance of environmental responsibility in megaprojects?” was used. In addition, the questions of “not knowing much” and “not knowing at all” were removed. The detailed information of the interviewees is shown in Table 1. Although fsQCA is originally designed for small and medium samples, prior researches indicate that fsQCA is suited to analyse larger empirical data (>150) as well (Chuah et al., 2021; Sánchez-Mena et al., 2019).

Descriptive statistics of population variables (N = 160)

| Variable | Category | Number | Proportion |

|---|---|---|---|

| Organizational roles | Government | 3 | 1.9 |

| Owner | 48 | 30.0 | |

| Construction | 72 | 45.0 | |

| Supervision | 10 | 6.3 | |

| Design unit | 6 | 3.8 | |

| Operating unit | 0 | 0 | |

| Consultation unit | 13 | 8.1 | |

| Other | 8 | 5.0 | |

| Position | Grassroots managers | 38 | 23.8 |

| Middle managers | 53 | 33.1 | |

| Top managers | 58 | 36.3 | |

| Others | 11 | 6.9 | |

| Organizational ownership | Government | 5 | 3.1 |

| State-owned | 102 | 63.7 | |

| Private-owned | 45 | 28.1 | |

| Foreign-owned | 0 | 0 | |

| Other | 8 | 5.0 | |

| Gender | Male | 145 | 90.6 |

| Female | 15 | 9.4 | |

| Working years | Less than 5 years | 31 | 19.4 |

| 6–10 years | 35 | 21.9 | |

| 11–15 years | 40 | 25.0 | |

| 16–20 years | 20 | 12.5 | |

| More than 20 years | 34 | 21.3 |

The positions, roles, unit nature, and megaproject types and attributes of megaproject managers are diverse, reflecting the views of respondents from different backgrounds and ensuring the universality and reliability of the research results. From the perspective of gender, among the 160 respondents in this survey, the ratio of male respondents (145) to female respondents (15) is approximately 10:1, in line with the characteristics of the male/female ratio in the civil engineering industry. In addition, from the perspective of the education level of the respondents, 88.7% of the respondents have bachelor's degrees or above, indicating that the respondents have a high level of education and a strong level of understanding, which is conducive to reading and understanding the questionnaire to reflect real megaproject practice.

4. Results and analysis

4.1 Calibration of data

In QCA, the original data need to be calibrated and transformed into collective membership, and the calibration is the process of giving collective membership to the case. The fuzzy set method requires that the target set should be set according to the theoretical concept, and three calibration thresholds of full membership, intersection point, and complete non-membership should be set according to the research content to convert the initial data into the set membership value between 0 and 1 (Ragin, 2008). The calibration method for scale class data has two types: (1) 7 or 5 represents full membership in a category, 1 represents non-membership in a category, and 4 or 3 represents the crossover point of maximum ambiguity (Leischnig et al., 2014; Urueña and Hidalgo, 2016). (2) Raw data calibration was carried out with reference to the standards proposed by Charles Larkin that the values of the 95th, 50th, and 5th percentiles of the conditions and outcome were assigned as full membership, the crossover point, and full non-membership, respectively (Ragin, 2008).

However, the structure distribution of the data measured by the scale may be biased (e.g. all the data are distributed above 3), leading to conflict between distribution and scale (Zhang and Du, 2019). Therefore, to avoid the influence of the uneven distribution of scale data, the calibration method (2) was adopted in this study. First, three anchor points (95th, 50th, and 5th percentiles) of the data were calculated by SPSS (Table 2). Then, the calibration function of the fsQCA software was used to calibrate each variable in turn. When the fuzzy set membership score is 0.5, it is changed from 0.5 to 0.501 by referring to the practice of Fiss to ensure that no samples will be deleted in the standardized analysis (Fiss, 2011).

fsQCA data calibration threshold

| Variable | Calibration of data | ||

|---|---|---|---|

| Fully affiliated (95%) | Intersections (50%) | Not affiliated (5%) | |

| Alienation of MER behavior | 4 | 2.3077 | 1 |

| Institutional defects | 3.8333 | 2.3333 | 1 |

| Information asymmetry | 4 | 2.8333 | 1 |

| Economic pressure | 4 | 2 | 1 |

| Expectation pressure | 5 | 4 | 2 |

| Exposure possibility | 5 | 3.8 | 1.81 |

| Penalties | 5 | 3.6667 | 1 |

| Learning effects | 4.4875 | 2.5 | 1 |

| Moral disengagement | 4.4 | 3 | 1 |

4.2 Analysis of necessary conditions

Although analysis of sufficient conditional combinations is at the core of fsQCA, the necessity of each condition must be tested before constructing a truth table (Schneider and Wagemann, 2010). To identify whether any of the eight conditions were necessary for MERB alienation, we analyzed whether the condition was always present (absent) in all cases where the outcome was present (absent). As shown in Table 3, both the consistency and coverage levels of each condition were lower than the recommended threshold of 0.9 (Schneider et al., 2010), indicating that the condition variables could not fully explain the resulting variable. In summary, no one solitary condition constituted a necessary condition for alienation of MER behavior. Therefore, further conditional configuration combination analyses were required.

Result of necessary conditions

| Conditions tested | Consistency | Coverage |

|---|---|---|

| Institutional defects | 0.787 | 0.780 |

| ∼ Institutional defects | 0.549 | 0.542 |

| Information asymmetry | 0.798 | 0.792 |

| ∼ Information asymmetry | 0.517 | 0.510 |

| Economic pressure | 0.810 | 0.846 |

| ∼ Economic pressure | 0.524 | 0.492 |

| Expectation pressure | 0.603 | 0.571 |

| ∼ Expectation pressure | 0.700 | 0.725 |

| Exposure possibility | 0.567 | 0.577 |

| ∼ Exposure possibility | 0.782 | 0.754 |

| Penalties | 0.603 | 0.582 |

| ∼ Penalties | 0.731 | 0.742 |

| Learning effects | 0.784 | 0.809 |

| ∼ Learning effects | 0.510 | 0.485 |

| Moral disengagement | 0.775 | 0.807 |

| ∼ Moral disengagement | 0.505 | 0.477 |

4.3 Analysis of sufficient conditions

The truth table needs to be constructed before the influence factor configuration analysis. A truth table is a configuration table that, simply put, is a given combination of conditions associated with a given result, each of which may correspond to zero, one, or more than one sample (Rihoux and Ragin, 2008). This study has eight antecedent factors. Theoretically, 28 = 256 combinations of antecedent factors are possible, meaning that that the initial truth table has 256 items.

Before using fsQCA software to conduct standardized analysis, appropriate frequency thresholds and consistency thresholds need to be developed to reduce the number of initial combinations. By setting a certain threshold, the combination of influential factors that do not appear or rarely appear in real life can be eliminated to ensure that the combination of influential factors explored is based on a certain number of real cases rather than accidental. The truth table should consider not only the substance of evidence but also the characteristics of the research (Rihoux and Ragin, 2008). When the number of samples is large, a higher frequency threshold should be determined. When the study sample size is large, the question is no longer which combinations have examples but which combinations have sufficient sample examples to ensure that their subset relationship with the results is reasonable. In small and medium samples (typically less than 50 samples), a frequency threshold of 1 is appropriate, but for large samples (typically more than 150 samples), the frequency threshold for screening should be set higher (Ragin, 2008). In terms of the original consistency threshold, QCA method experts proposed different acceptable minimum thresholds, such as 0.8 and 0.75. The setting of the consistency threshold is not mechanical. Similar to the selection of frequency threshold, many factors need to be considered comprehensively (Zhang and Du, 2019). When the sample size was small, the consistency threshold should be higher, whereas, if the sample size was large, the consistency threshold could be lower (Schneider and Wagemann, 2012). At present, most studies adopt a consistency threshold of 0.8. In addition, some studies also proposed to set a threshold for PRI consistency, and the best minimum acceptable value for PRI consistency was 0.75 (Zhang and Du, 2019). In summary, based on comprehensive consideration of sample size and data structure, this study sets the frequency threshold as 2, the original consistency threshold as 0.8, and the PRI consistency threshold as 0.75.

4.4 Analysis of antecedent configurations

With the help of fsQCA3.0 software, this paper takes institutional defects, information asymmetry, economic pressure, expectation pressure, exposure possibility, disciplinary strength, learning effect, and moral disengagement as antecedent variables, and MER behavior alienation as result variable to conduct standardized configuration calculation. Finally, complex, simple, and intermediate solutions are obtained. Raw coverage represents the proportion of cases that can be explained by this combination of factors to cover the alienation result of MER behavior. Unique coverage refers to cases that can be explained only by this combination of factors. Consistency indicates whether the combination of antecedent factors is reliable in determining membership scores of simple or complex antecedents. Solution coverage shows the proportion of cases that can be explained by the combination of all antecedent factors in the understanding. Solution consistency reflects whether the combination of antecedent factors can effectively explain the result, that is, the degree of reliability.

The simple solutions and intermediate solutions are addressed, and the configuration that can lead to the alienation of MER behavior is shown in Table 4 according to the expression of research results commonly used in QCA.

Configuration table of the alienation of MER behavior

| Variable | Causal configurations | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

Institutional defects | • | ⊗ | ⊗ | ⊗ | • | ● | ● | ● | • |

Information asymmetry | • | ⊗ | — | ⊗ | • | • | • | • | ● |

Economic pressure | ● | ● | ● | ● | ● | • | — | • | ● |

Expectation pressure | — | — | • | — | ⊗ | ⊗ | • | • | ● |

Exposure possibility | ⊗ | ⊗ | • | • | — | ⊗ | ⊗ | ⊗ | • |

Penalties | ⊗ | ⊗ | ⊗ | • | • | ⊗ | ⊗ | • | • |

Learning effects | ● | ● | ● | ● | ● | — | • | — | ⊗ |

Moral disengagement | — | • | • | • | • | ● | ● | ● | ⊗ |

Raw coverage | 0.47 | 0.28 | 0.30 | 0.30 | 0.35 | 0.44 | 0.35 | 0.33 | 0.25 |

Unique coverage | 0.03 | 0.01 | 0.01 | 0.02 | 0.02 | 0.01 | 0.01 | 0.01 | 0.02 |

Consistency | 0.97 | 0.98 | 0.98 | 0.96 | 1.00 | 0.98 | 0.97 | 0.99 | 0.97 |

Solution coverage | 0.642726 | ||||||||

Solution consistency | 0.936769 | ||||||||

Note(s): “● ” indicates the existence of the core condition; “ ⊗” indicates the absence of the core condition “ •” indicates the existence of the auxiliary condition; “ ⊗” indicates the absence of the auxiliary condition, and “—” indicates “don’t care” | |||||||||

The configuration table shows that nine configuration factors cause alienation of MER behavior, and the consistency value of each configuration is all greater than 0.9, indicating that each combination has a relatively good explanatory power. In this study, the overall consistency is 0.936769 and the total coverage is 0.642726, indicating that these nine combinations have a strong consistency and can explain approximately 64% of cases with high explanatory power.

4.5 Robustness test

The robustness test is an important part of configuration analysis and has many patterns, such as adjusting calibration threshold, changing case frequency, changing consistency threshold, adding other conditions, and supplementing or eliminating cases (Skaaning, 2011; Zhang and Du, 2019). In this study, the robustness test was carried out by adjusting the calibration threshold. The original consistency threshold was adjusted from 0.8 to 0.85. Through comparative analysis of the two research results, the number of configurations and the core conditions have not changed significantly. Therefore, the research results obtained in this study are relatively stable.

5. Discussion

Corporate research (e.g. Lin et al. (2016)) reveals that alienation of environmental behavior is a harmful and negative practice, yet it has not been addressed in the megaproject context. The analyses of necessary conditions indicate that no single factor acts as the necessary condition for alienation of MER behavior. From the findings, three driving modes of alienation of MER behavior are concluded, namely, the “economic pressure + learning effect” driven mode, “institutional deficiency + moral dishonesty” driven mode and “information asymmetry + economic pressure + expectation pressure” driven mode.

The “economic pressure + learning effect” driven mode corresponds to configurations 1–5. The law of “economic pressure + learning effect” driving the alienation of MER behavior can be summarized as follows. High economic pressure and imitative learning are the key factors driving the alienation of MER behavior. This is similar to the findings of Wu (2014) and Wu et al. (2021) where financial constraints significantly positively correlated with environmental irresponsibility. By comparing configurations 1 and configurations 2–4, alienated opportunities plays a catalytic role in this driven mode. Looking closer at configurations 1 and configurations 5, when there are opportunities in this driven mode, penalties can curb alienation of MER behavior to a certain extent.

The “institutional defects + moral disengagement” driven mode corresponds to configurations 6–8. The law of “institutional defects + moral disengagement” driving the alienation of MER behavior can be summarized as follows. Institutional defects and moral disengagement are the key factors that drive the alienation of MER behavior. This is similar to the findings of Wu et al. (2021) who found that regulatory distance significantly positively correlated with environmental irresponsibility. Moreover, this configuration supports the opinion of Soltani (2014), that soft and flexible supervision, and the lax attitude of regulatory agencies have provided favorable conditions for unethical behaviors. By comparing configurations 7 and configurations 8, it is found that penalties plays a little promoting role in this driven mode. When comparing configurations 6 and configurations 7, expectation pressure does not promote the alienation of MER behavior as previously analysis. The reason may be that expectation pressure plays the effect of external supervision. and lack of preventive measures and disciplinary sanctions.

The “information asymmetry + economic pressure + expectation pressure” driven mode corresponds to configuration 9. Configuration 9 is the only one without rationalization. Information asymmetry, economic pressure, and expectation pressure are the core conditions and play a core role. This conclusion indicates that, although the participating entity have no rationalization and faces sufficient exposure, alienated pressure and opportunity may still drive the participating entity to engage in MER alienation behavior.

5.1 Theoretical implications

This study represents one of the first attempts to examine the alienation of MER behavior and its antecedent configurations. Our research results have two contributions to theory. First, our research has enriched the content of research related to MER from the fraud triangle theory. We have summarized the existing survival research literature by combining fraud triangle theory into eight variables and using QCA methods to offer an in-depth understanding of dynamic interactions between these factors and the alienation of MER behavior. This paper adds to MER literature by presenting conditions for alienation of MER behavior and expands the scope for application of the fraud triangle theory. Second, given the limitations of linear approaches to MER research (Wang et al., 2017, 2018), a novel and nonlinear analysis method, fsQCA, was adopted in the study. This study contributes to research on alienation of MER behavior by identifying several equivalent multidimensional paths for participating parties to implement such behavior. Lastly, the results support the criticism of Schuchter and Levi (2016) on the fraud triangle theory that an elimination of any one of the elements can extinguish the fraud. This confirms the characterization of the fraud triangle by Burke and Sanney (2018) that these elements are interactive.

5.2 Practical implications

Findings of this study have practical implications for the alienation of MER behavior governance. First, due to the asymmetry and complexity of causality of alienation of MER behavior, this study calls for a considerable shift in thinking on the governance alienation of MER behavior. Based on our results, for a complex configuration with multiple conditions that lead to the alienation of MER behavior, controlling or eliminating one condition cannot always reduce alienation. This study presents a more realistic view that governance measures cannot solely rely on the effect of each condition and that portfolio governance strategies could help project managers in addressing alienation of MER behavior. Moreover, strategies cannot be divorced from their contexts, and the matching of control measures and configurations is critical for addressing alienation of MER behavior. This study recommends that multiple configuration paths should be considered when considering alienation reduction. Project managers and policymakers should regard economic pressure and learning effects as a control measure group. Besides, institutional defects and moral disengagement are regarded as the other control measure group. Because these are the most critical combination leading to the alienation of MER behavior. Secondly, the study highlights the importance of economic pressure and learning effects, in explaining alienation of MER behavior, since they are present as core conditions in five out nine configurations. Megaproject participants should set reasonable financial objectives, and ensure reasonable allocation of funds as far as possible to reduce the economic pressure conditions that lead to the alienation of MER behavior. Moreover, the unethical tone at the top can influence the poor core values of organizations (Soltani, 2014), leading to alienation of MER behavior when facing financial pressures. Conversely, we should set an example and avoid wrong imitation. The leadership of TMTs in megaprojects should be strengthened, given that in the construction of the Shanghai World Expo, TMTs played an active spiritual leading role (Zhai et al., 2017). Lastly, exhaustive environmental information should be captured through information and communications technology in megaproject (Yang, 2017), which can compensate for regulatory deficiencies.

6. Conclusion

The alienation of MER behavior is the result of the combined effect of antecedent factors rather than the result of the independent effect of a single factor. The combination effect of fsQCA showed that nine configurations could lead to alienation of MER behavior. The core terms and conditions can be divided into three drive types, namely “economic pressure and learning effect,” “institutional defects + moral rationalization,” and “information asymmetry + economic pressure + expectation pressure.”

According to the results of configuration analysis and discussion, eight laws of alienation of MER behavior can be summarized as follows. (1) High economic pressure is an important basic factor driving the alienation of MER behavior. (2) Three combinations of core factors drive the alienation of MER behavior. (3) The combination of “alienation opportunity + insufficient exposure + high economic pressure + learning learning” is the most likely to drive the alienation of MER behavior. (4) In the context of the existence of alienating opportunities and the lack of exposure, when the deterrence effect is formed by increasing the intensity of punishment, the alienation of MER behavior can be restrained to some extent. (5) In the absence of alienating opportunities and in the context of insufficient exposure, the role of exposure factors in curbing the alienation of MER behavior will be limited. (6) Under a certain combination of “economic pressure” and “expectation pressure”, both types of pressure can lead to the alienation of MER behavior. (7) The combination of exposure factors of “strong punishment + low exposure possibility” could not effectively restrain the alienation of MER behavior. (8) Although sufficient exposure is present and the participant has a high perception of MER, opportunity and pressure factors will still drive the participant to practice alienation of MER behavior.

6.1 Limitations and future research

Megaprojects are characterized by numerous stakeholders, complex internal and external environments, and complex, uncertain factors. The alienation of MER behavior presents a high degree of uncertainty and complexity. This research involved 222 megaproject managers throughout China, which are representative of the whole country. Although the findings reflect the current situation in China, whether the findings can be extended to general projects or other countries in the world remains to be verified in the future.

Therefore, future studies can collect data from major foreign projects and explore the mechanism of MER alienated behavior abroad. The mechanism of MER alienated behavior between China and other countries could be compared to better guide the engineering construction industry in China's relevant enterprises to go abroad under the background of the belt and road initiative, participate in the construction of infrastructure megaprojects around the world, and effectively fulfill the social responsibility of megaprojects.

The anonymous reviewers and the editors of this paper are also acknowledged for their constructive comments and suggestions.

Funding: This work was supported by the National Natural Science Foundation of China (grant number 71871096) and National Natural Science Foundation of Guangdong Province (grant number 2021A1515012649).

Conflict of interest: No potential conflict of interest was reported by the authors.