This study challenges the endemic techno-optimism of digital financial inclusion (DFI) discourse. Beyond technology adoption, institutional quality theory is postulated as the critical determinant of the efficacy and sustainability of DFI outcomes. The study further presents a conceptual distinction between symbolic and substantive inclusion.

A theory-building approach is adopted through a systematic synthesis of multidisciplinary literature spanning financial inclusion, digitalization, governance and institutional economics. An integrative framework is proposed, with institutional quality as the mediating construct and leadership support and regulatory capacity as institutional enablers that strengthen the effectiveness of institutional mediation.

In the absence of strong governance in the form of regulatory coherence, administrative capacity and enforcement, symbolic inclusion predominates, providing nominal market access that often increases user risk without delivering financial security or agency. Substantive inclusion occurs when robust institutions bridge the digital interface, transforming technological potential into developmental impact. Weak digital governance is a major source of variability and systemic vulnerability in DFI initiatives.

Policy should prioritize the quality of institutional infrastructure (e.g. consumer protection and reducing regulatory arbitrage) over the speed of digitalization. Sustainable financial inclusion requires active governance alongside market innovation.

The research centers governance in the DFI debate and provides an institutional critique of existing metrics. Its framework offers scholars and practitioners a socio-technical tool to evaluate the actual quality and developmental implications of digital finance in developing markets.

1. Introduction

Digitalization has become a central feature of contemporary economic development, with financial inclusion (FI) frequently identified as a key outcome. In emerging and developing markets, governments and development agencies have made heavy investments in digital payment systems, financial technologies (FinTech), mobile banking services and algorithmic credit-scoring systems with the express goal of reaching historically marginalized groups with financial services (Muat, Mahdzan, Sukor, & Fachrurrozi, 2025; Kumari & Giri, 2025; Chowdhury et al., 2025). Existing literature consistently documents positive links between digital financial development and outcomes such as poverty reduction, income stability and business performance (Hussain, Ur Rehman, & Iqbal, 2025; Campanella, Ferri, Serino, & Zampella, 2025; Al-Okaily & Al-Okaily, 2025). Despite these positive claims, FI outcomes remain uneven. In many contexts, progress is fragmented and, in some cases, reversible. While digital infrastructure has expanded rapidly, governance systems have not developed at the same pace. This gap raises fundamental questions about the sustainability and quality of digitally driven FI. Recent research has been attracted to the presence of paradoxical results (digital finance) and the increased risk exposure, misuse and regulatory vulnerability (Brown & Piroska, 2022; Jalal-Eddeen, 2025). Within some institutional contexts, digital platforms have created new exclusionary practices by introducing opaque algorithms, poor consumer protection regimes and asymmetries of information to the low-income user. These contradictions challenge prevailing inclusion narratives and suggest that digitalization, in isolation, may generate new vulnerabilities even as it promises access.

Conversely, one of the weaknesses in existing studies is that much of the research in the field of financial inclusiveness has been dominated by a technology-focused epistemology. Empirical models still give preference to the measures of adoption, including account ownership, the frequency of transactions, platform usage and institutional quality, which is often turned into a control variable or left out completely (Sha’ban, Girardone, & Sarkisyan, 2020; Valera, Lei, & Fong, 2025). Although several studies have admitted the role of regulatory capacity and policy credibility, these dimensions are still under-theorized (Aldieri, Barra, & Vinci, 2025; Banihani, Kamel Qawqzeh, Hanna Zawaideh, Mohammad Al Ebbini, & Zakaria AlQudah, 2025). Consequently, digitalization is often treated as a standalone technological solution rather than a governance-dependent process. Additionally, the study of FI was also developed in an econometric tradition, largely emphasizing quantifiable results more than the systemic explanation. As it has produced strong quantitative data on performance measures and behavioral reactions (Lee, Wang, Chang, Wu, & Li, 2025; Abouelfarag & Elboghdadly, 2025), it has sacrificed conceptual clarity on institutional causality. The literature seldom clarifies why digital finance is successful in some places and a failure in others, and there is no adequate explanation based on how governance asymmetries affect the inclusion outcomes in different jurisdictions (Labhard, Lehtimäki, & Baccianti, 2025). This study therefore contends that the prevailing literature suffers not from insufficient data but from insufficient theorization. It suggests that digital financial inclusion (DFI) cannot be properly understood without placing the quality of institutions at the crux of analysis. Financial systems are not merely embedded in institutions; they are fundamentally shaped by them. Law, regulation, administrative capacity and political commitment do not simply enable digitalization but rather determine the meaning, reach and risk profile of digitalization. Where governance systems lack legitimacy, autonomy or enforcement capability, digital finance is unlikely to create durable inclusion. Instead, it may institutionalize precarity and formalize informality. Existing studies on DFI focus on large aspects such as adoption, including account ownership, mobile payment frequency and platform usage. Few explore the mediating role of institutional quality in the effectiveness of these interventions, so it is unclear how some populations are protected while others continue to be vulnerable. This gap limits our understanding of the conditions under which digital finance produces substantive inclusion rather than mere symbolic access.

Hence, the core argument of this paper is that digitalization produces FI outcomes through institutional quality, which determines whether inclusion is symbolic or substantive. This paper has three objectives: (1) to theorize the distinction between symbolic and substantive FI; (2) to position institutional quality as the central mediator of DFI outcomes and (3) to provide a conceptual framework to guide future empirical and policy research on DFI in emerging markets.

Symbolic inclusion refers to nominal access without protection, participation without power and usage without security. The distinction between symbolic and substantive inclusion draws on broader institutional and critical perspectives that differentiate between formal access and effective participation within socio-economic systems (Scott, 2008; Alvesson & Deetz, 2000). Symbolic inclusion reflects a condition in which individuals are formally integrated into financial systems through digital access, yet remain structurally exposed due to weak regulatory protection, limited accountability and asymmetries of information. In contrast, substantive inclusion denotes a condition in which institutional arrangements actively enable secure participation, enforce rights and reduce vulnerability. This distinction therefore shifts the analytical focus from access-based metrics toward the quality and consequences of inclusion. Rather than treating inclusion as a binary outcome, the framework conceptualizes it as a continuum shaped by institutional capacity, where digital participation may coexist with financial insecurity under weak governance conditions.

Substantive inclusion, by contrast, requires governance systems capable of ensuring accountability, enforcing rights and sustaining trust. This distinction is largely absent in existing scholarship, where access is often equated with inclusion and reach with equity. By theorizing this distinction, this study advances a governance-centered redefinition of FI. This conceptual paper therefore seeks to reposition institutions from the periphery to the core of digital finance discourse. Drawing on insights from FI, digitization governance and innovation diffusion literature, the paper constructs a synthesizing conceptual framework that frames institutional quality as the institutional foundation of digital financial effectiveness. By so doing, it questions techno-deterministic assumptions and pushes towards a form of institutional realism that recognizes administrative capacity as the main limiting factor of reform results. Yet, policy discourse continues to frame digital expansion as inherently stabilizing. This misalignment between narrative and empirical reality underscores the urgency of a conceptual reframing. In Sub-Saharan Africa, mobile money adoption has grown rapidly, yet studies show persistent financial vulnerability among low-income users due to weak regulatory oversight (Kumari & Giri, 2025; Brown & Piroska, 2022). This demonstrates that technological expansion alone does not guarantee equitable or sustainable inclusion. This distinction addresses a critical gap in FI research, where access and usage are frequently conflated with meaningful inclusion outcomes.

Furthermore, the study adds to the theoretical body of knowledge by linking the theory of inclusion and institutionalist economics. While early institutionalist scholarship focused on the role of public institutions in economic coordination (Figart, 2013), studies of inclusion have, in the last few years, largely abandoned institutional explanations and instead focus on behavioral and technological models. This paper revisits the institutionalist tradition and adapts it to the context of digital finance. In doing so it produces a socio-technical rather than technological theory of inclusion. Finally, the paper offers a structured research agenda for future scholarship. Rather than calling for additional metrics or datasets, it calls for conceptual recalibration. It argues that until governance capacity is analytically foregrounded, DFI will remain poorly understood and inconsistently realized. Through its framework, the paper invites scholars to move beyond surface indicators and interrogate the institutional architectures beneath them.

The central research question guiding this study is.

How does institutional quality mediate the transformation of digital financial expansion into substantive financial inclusion?

To address this question, the study examines how governance capacity, particularly regulatory coherence, administrative effectiveness and leadership support, shapes trust, risk exposure and distributional outcomes within digital financial systems.

2. Literature review

2.1 Financial inclusion (FI) as a development construct: from access to agency

FI has been transformed into a more multi-dimensional development construct to include capability, resilience and participation in socio-economic activities besides a simply defined goal of access to banking. Initial conceptualizing considered inclusion to be access to formal financial services and access to deposit accounts and credit facilities. Nonetheless, recent research has broadened this definition to encompass financial ability, well-being and pathways of inclusive development (Muat et al., 2025; Abouelfarag & Elboghdadly, 2025; Mathonsi & Saba, 2025). The evolution is an indication of the conceptual changes in not providing infrastructure but an outcome-based measurement; however, theory has not kept up with the same level. However, empirical evidence confirms that expanded financial participation influences economic performance in both household and national contexts, affecting income stability, consumption smoothing and poverty dynamics (Kumari & Giri, 2025; Hussain et al., 2025). FI is not, however, equally valuable in all contexts. The results of cross-country research indicate that the results are deeply differentiated based on the regulatory coherence, educational level and institutional legitimacy (Sha'ban et al., 2020; Valera et al., 2025). Consequently, the literature lacks a stable theoretical framework capable of explaining why FI succeeds in some settings while stagnating or generating adverse effects in others. This conceptual gap forms the basis for the present study's institutional critique. Policy-wise, all these dimensions align well with Sustainable Development Goal (SDG) 1 (No Poverty) and SDG 10 (Reduced Inequalities) due to their focus on available financial architecture. Nevertheless, in the absence of effective governance frameworks, digital inclusion policies can make SDG promises counterproductive by simply placing risk on populations that were already at risk instead of protecting them against market shocks (Koudalo & Toure, 2023). Therefore, the promise of inclusion about development cannot be separated from institutional design.

2.2 Digital financial inclusion and the technological turn

DFI represents the technological arm of inclusion policy, premised on the belief that innovation can leapfrog institutional deficiencies. Empirical research overwhelmingly attributes improvements in inclusion outcomes to digital platforms, citing mobile payments, online lending and algorithmic financial assessments as drivers of efficiency and outreach (Lee et al., 2025; Dianda, Thiombiano, & Okey, 2025). Studies emphasize that digital interfaces reduce transaction costs and spatial constraints, enabling previously excluded populations to participate in formal finance. Nonetheless, DFI research exhibits a persistent bias toward functional adoption metrics. Adoption is frequently taken as evidence of efficacy, with limited interrogation of distributional consequences or governance conditions (Rajpal & Manglani, 2025; Srivastava & Shunmugasundaram, 2025). These discoveries undermine the existing discourse of digital neutrality and suggest that FinTech can make asymmetries systemic as opposed to breaking them down.

2.3 Governance, regulation and the institutional mediation of digital finance

Institutional quality remains the under-theorized axis of digital finance. Regulatory frameworks determine the legitimacy and stability of financial systems, influencing consumer behavior and market confidence (Aldieri et al., 2025). Where regulatory quality is strong, digitalization enhances economic performance. Where it is weak, innovation accelerates institutional decay. Banihani et al. (2025) empirically demonstrate that information system governance of FinTech determines FinTech maturity and continuity in operations. Similarly, as shown by Tariq, Chen, Tariq, and Sumbal (2025), digitalization affects sustainability only through the mediation of governance. These studies add a critical perspective to the linear model of innovation leading to performance and propose a mediating relationship between technology and impact. Trust becomes a key element in the literature on governance. Xia, Lu, Lin, Nord, and Zhang (2023) show that mechanisms of governance are as influential as technological reliability toward determining adoption and continuity. However, the concept of trust is hardly included in FI schemes, although it is a systemic requirement. However, the study of Brown and Piroska (2022) also indicates how regulatory sandboxes, even though being promoted as innovations in governance, tend to be deregulation tools that permit market participants to experiment publicly. This redefinition of FinTech as the system instead of being a system of governance reveals inconsistencies in the policy of digital inclusion. Lack of institutional responsibility means that digital finance is being conducted in regulatory grey zones that are eroding social trust. Hence, FI cannot be advanced without institutional consolidation.

2.4 Institutions, innovation and organizational transformation

Digitalization influences organizational responses, which are influenced by organizational contexts. Innovations in organizations are found in the literature to be dependent on the relationship between the management support, the quality of information and the integration of structures (Al-Hashimy, Yao, & Pitchay, 2025; Wahab, Hamzah, & Sohal, 2025). These studies emphasize that systems fail not because of code but because of governance deficits. This point is furthered in Cozzarin (2017) and López (2024) by demonstrating that digital technologies only lead to productivity gains when they are incorporated into consistent organizational frameworks. Equally, Hempell and Zwick (2008) disclose that the diffusion of innovation is not a matter of hardware only but work organization. These lessons are a challenge to the belief that financial institutions present in developing countries can follow the same innovation paths as those witnessed in the developed markets. Without organizational coherence, digital systems increase complexity without improving capability. Furthermore, the institutional dimension thus bridges micro-level technological choice with macro-level inclusion outcomes. However, this theoretical integration has not been systematically applied in FI research, thereby obscuring organizational failure as a pathway to policy failure.

3. Methods

This study employs a theory-building method and is based on structured literature synthesis under the established guidance for conceptual development (MacInnis, 2011; Jaakkola, 2020). To ensure analytical transparency and rigor, the study adheres to a systematic literature review protocol developed by Tranfield, Denyer and Smart (2003) and Denyer and Tranfield (2009) to enable development of a theoretically grounded conceptual framework. The review was designed around three analytically defined domains: digitalization, FI and institutional governance. Digitalization refers to digital financial services, FinTech adoption, mobile banking and algorithmic financial systems; FI refers to access, usage, financial capability and welfare consequences, and institutional governance refers to regulatory quality, enforcement capacity, digital governance and institutional trust. These domains were not simply used as keywords but as conceptual inclusion criteria in the process of screening and analysis.

A structured search was performed using five major academic databases – Web of Science, Scopus, ScienceDirect, Business Source Complete and Google Scholar – to ensure a broad disciplinary coverage and minimize database bias (Mongeon & Paul-Hus, 2016; Haddaway, Collins, Coughlin, & Kirk, 2015). Search strings were used to combine key constructs using Boolean operators, such as “digital financial inclusion” OR “FinTech adoption” OR “digital payments” AND “institutional quality” OR “governance” OR “regulatory capacity” AND “financial inclusion outcomes” OR “inclusive growth” OR “financial access.” The review was limited to peer-reviewed journal articles published between 2013 and 2025 in order to reflect current developments in digital finance and governance. The initial search produced 368 articles, which were reduced to 274 records after duplicates were removed. A title and abstract screening stage excluded 162 articles that did not adequately address the analytical domains, leaving 112 studies for full-text assessment. Following detailed evaluation, a final sample of 54 articles was retained for synthesis. Articles were excluded if they addressed only adoption of technology without reference to inclusion outcomes, considered FI without digital or institutional facets or had no conceptual or empirical relevance to governance mechanisms. This staged filtering process, consistent with Preferred Reporting Items for Systematic Reviews and Meta-Analyses-informed review logic (Petticrew & Roberts, 2006), ensured the final sample represented the intersection of the three analytical domains.

To enhance conceptual precision, the inclusion criteria were operationalized such that studies were retained if they addressed at least two of the three analytical domains, with priority given to studies examining the interaction between digitalization and inclusion or governance and inclusion. Studies integrating all three domains were given particular analytical weight during synthesis. The retained literature was analyzed using a thematic coding procedure following Braun and Clarke (2006). The analysis proceeded in three iterative stages: open coding, where recurring concepts such as access expansion, financial vulnerability, algorithmic opacity, trust deficits and regulatory gaps were identified; axial coding, where these concepts were grouped into higher-order categories including symbolic inclusion, substantive inclusion, institutional mediation, governance capacity and trust formation, and selective coding, where these categories were integrated into a coherent explanatory structure linking digitalization, institutional quality and inclusion outcomes.

This synthesis process directly resulted in the development of the conceptual framework and related propositions (S1–S5). Specifically, the differentiation between symbolic and substantive FI became inductive through common trends in the literature in which greater digital access coincided with enduring susceptibility in weak institutional settings. Likewise, institutional quality has been found as a mediating process through sustained evidence that governance systems modulate the transformation of digital access into developmental outputs. Other constructs, such as trust, digital governance and financial literacy, were also introduced as complementary or conditional factors that determine this relationship. In this way, it is ensured that the framework is not deductively imposed but inductively based on systematically synthesized literature. The study has some limitations, even though it was undertaken with these attempts to guarantee rigor. The search is limited to English-language peer-reviewed articles, which might miss pertinent grey literature or region-focused research. Despite the employment of several databases to cover the area better, certain publication bias might still exist. Moreover, even though thematic analysis offers a methodological method of synthesis, it entails subjective coding to classification. Lastly, the proposed framework is not empirically tested being a conceptual study and hence needs to be validated in upcoming empirical studies.

4. Conceptual framework development

Building on the systematic literature synthesis described in Section 3, this section develops the conceptual framework by integrating the identified thematic patterns into a coherent explanatory structure. The framework is derived inductively from the reviewed literature and reflects recurring relationships between digitalization, institutional quality and FI outcomes. The following propositions (S1–S5) are formulated based on these synthesized insights.

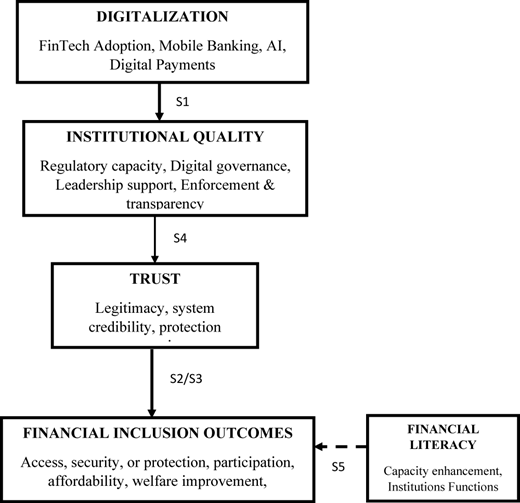

Figure 1 presents the conceptualization of digitalization as an independent construct and institutional quality as the mediating mechanism within FI frameworks. The framework adopts a holistic interpretation of digitalization that extends beyond technological availability to include digital usage capability, platform sophistication, FinTech deployment and algorithmic integration in financial service delivery. The conceptualization of digitalization in the present research is thus a systemic change to the process of financial intermediation including digital payments and mobile banking, artificial intelligence-based credit checks and automated service platforms (Lee et al., 2025; Rajpal & Manglani, 2025). Institutional quality is positioned as the central mediating mechanism through which digitalization influences FI outcomes (Aldieri et al., 2025; Banihani et al., 2025). In this framework, institutions are not just background conditions but active determinants of system performance. They organize incentives, limit opportunism and identify the rights and obligations of financial actors. Whereas most studies assume that increased platform usage is indicative of inclusion, this framework contends that increased usage without protection generates symbolic inclusion, involving exposure without empowerment and access without agency. By contrast, substantive inclusion is only possible where digital diffusion is subject to effective regulatory and supervisory institutions. This conceptual distinction forms the theoretical core of the paper. To address these limitations, this study develops a socio-technical framework in which institutional quality mediates the translation of digital access into substantive FI outcomes. Building on the literature, the paper formulates five theoretical suppositions (S1–S5) that explain how digitalization, institutional quality and governance interact to produce either symbolic or substantive inclusion.

Digital governance operates as the connective mechanism linking technological advancement to institutional performance. Drawing on evidence that digitalization influences sustainability outcomes through governance mediation (Tariq et al., 2025), the framework incorporates digital governance as the operational site of institutional influence. Digital governance encompasses regulatory frameworks, compliance architecture, data protection systems and supervisory technologies. It reflects the institutionalization of digital systems and governs how information asymmetries, algorithmic decisions and platform responsibilities are managed (Brown & Piroska, 2022; Xia et al., 2023). Trust is part of the framework as one of the latent results of the quality of governance and a predictor of continued usage. Research has always indicated that trust reflects the outcomes of institutional quality and supports continued engagement with digital financial systems (Xia et al., 2023). In cases where the governance systems are reputable, users view digital platforms as legitimate. Where they are weak, platforms are interpreted as predatory. This conceptualization reframes trust not as a psychological variable but as an institutionally produced outcome. Trust arises not from technical architecture but from regulatory assurance. Nevertheless, organizational capacity functions as an enabling construct within the framework. Evidence suggests that technological performance is contingent upon managerial support, system integrity and accounting information quality (Al-Hashimy et al., 2025; Wahab et al., 2025). The framework therefore recognizes that institutions operate through organizations. FI does not fail abstractly; it fails institutionally and organizationally. Weak organizational integration fragments policy implementation and weakens regulatory enforcement, thereby undermining inclusion outcomes.

Nevertheless, the framework also integrates financial literacy as a complementary but insufficient condition for inclusion. While literacy promotes better financial well-being (Muat et al., 2025; Philippas & Avdoulas, 2020), it cannot replace regulatory protection. Overemphasizing literacy runs the risk of placing the burden from creating change on individuals rather than on institutions. In digital spaces that are marked by the algorithmic opacity, literacy without institutional accountability leads citizens to exploitation rather than empowerment (Jalal-Eddeen, 2025). From a developmental point of view, the framework is consistent with multiple SDGs and FI. Its outcome orientation promotes SDG 1 (No Poverty) and SDG 10 (Reduced Inequalities) through the perspective of inclusion as an enhancement of welfare rather than expansion of access. Digital innovation connects with SDG 9 (Industry, Innovation and Infrastructure), while governance mediation ensures compatibility with SDG 8 (Decent Work and Economic Growth) by resisting exploitative digitization. In the end, the model reveals five theoretical suppositions that can undergo empirical testing in subsequent research as follows.

Digitalization influences FI outcomes through the mediating role of institutional quality;

Institutional quality mediates the relationship between digitalization and FI outcomes;

Weak digital governance structures transform FI into symbolic rather than substantive participation;

Trust in digital financial systems is an institutionally produced outcome rather than a purely technological or behavioral variable and

Financial literacy enhances inclusion outcomes when supported by regulatory protection and governance capacity.

5. Discussions and findings

5.1 Symbolic versus substantive digital financial inclusion

In this paper, it is determined that the DFI cannot be evaluated based on access, adoption and usage criteria alone. Although existing studies have linked an improved level of digital access to inclusive growth (Abor, Amidu, & Issahaku, 2018; Sha'ban et al., 2020; Mathonsi & Saba, 2025), there is evidence that extended access is often accompanied by enduring financial vulnerability and decreased welfare benefits (Koudalo & Toure, 2023; Kumari & Giri, 2025).

We therefore theorize the phenomenon as symbolic inclusion, in which users engage institutionally in electronic financial systems without becoming financially empowered. Research indicates that the presence of general access to electronic money or mobile finance does not ensure any significant inclusion, especially in an environment where there is a weak institutional regulation (Dianda et al., 2025; Lai, Xie, Cao, & Zhang, 2022). Alternatively, substantive inclusion takes place when digital finance increases the ability of users to handle risks, accumulate assets and interact with financial systems safely and foreseeably. This distinction clarifies why access-based measures of FI tend to overestimate developmental outcomes. Under conditions of weak institutional quality, digital access may increase participation at the same time as it increases exposure to financial risk, creating symbolic rather than substantive inclusion. Nonetheless, the analytical distinction between symbolic and substantive inclusion is thus not only descriptive but also explanatory. It reflects a structural divergence in outcomes, in which the same levels of digital access can lead to fundamentally different effects on welfare depending upon institutional mediation. This dispels an important ambiguity in the literature whereby increased usage is often equated with improved inclusion without taking into consideration underlying governance conditions. Within this framework, symbolic and substantive inclusions are alternative outcomes of the same process of digitalization, which are differentiated by the mediating role of institutional quality. This adds to the argument that DFI can't be understood in isolation from the structure of governance.

5.2 Institutional quality as a structuring mechanism

Institutional quality operates as the central structuring mechanism through which digital finance translates into either symbolic or substantive inclusion. In previous research, the quality of the institutions is usually considered a control variable (Aldieri et al., 2025; Valera et al., 2025); however, the synthesis in this context shows that regulatory capacity, the credibility of the enforcement and the coherence of the governance actively influence the functioning of digital platforms and the distribution of risks. In the absence of regulation or inadequate enforcement, providers can use a lack of transparency, pricing and consumer protection to put their users at financial risk (Brown & Piroska, 2022; Jalal-Eddeen, 2025). Instead, the robust institutional structures integrate accountability, foreseeability and other protections into digital financial systems and significantly coordinate platform incentives with inclusion goals (Labhard et al., 2025; Tariq et al., 2025). This confirms the hypotheses of the proposition S2, which says that the institutional quality is not just contextual but causally patterns the inclusion outcomes.

5.3 Trust, risk and exposure

Trust in digital finances becomes one of the major facilitators of the inclusion outcomes. Although platforms contribute to convenience, the long-term commitment relies on the trust of the regulatory protection, data governance and redress (Xia et al., 2023). The lack of enforcement or systems that are poorly controlled undermines trust, despite users still using it out of need or lack of any other options (Jalal-Eddeen, 2025; Nizam & Rashidi, 2025). This creates a paradox: individuals may gain digital access while remaining financially vulnerable. The discovery is in line with the media reports about weakly regulated digital finance being associated with unlawful fundraising, over-indebtedness and financial turmoil (Lai et al., 2022; Koudalo & Toure, 2023). S3 is verified, indicating that mistrust in poor institutional settings transforms the digital inclusion into monetary susceptibility.

5.4 Non-linear and context-dependent inclusion

The trends of DFI are non-linear and situation specific. The institutions can create convenience and limited empowerment at an early stage, yet after some point, weak institutional capability can generate decreasing or negative returns (Kumari & Giri, 2025; Ozili, 2025). Digital penetration on a global scale shows that the same level of digital penetration produces varied inclusion effects through differences in regulatory and governance quality (Sha'ban et al., 2020; Valera et al., 2025). Digital growth can increase exposure and risk in less regulated environments and power in highly institutionalized ones (El Yamani et al., 2025; Abouelfarag & Elboghdadly, 2025). Furthermore, this confirms the hypothesis of S4, which states that the connection between digital finance and inclusion is non-linear and institutional strength mediates the connection.

5.5 Implications for digital financial inclusion theory

Collectively, the findings develop the theoretical knowledge of DFI because it incorporates both institutional and trust mechanisms. First, symbolic and substantive inclusion can help understand why access-based metrics overestimate the effects of digital finance, and institutional quality operates as a central structural mechanism shaping DFI outcomes. Second, the relationship between trust and risk provides an explanation of how weak institutions are turned into vulnerability in financial terms. These lessons expand the conceptual framework by providing a mechanistic explanation of why analogical digital finance interventions have varied effects on institutional settings.

6. Research implications

The study makes a valuable contribution to the theoretical discussion on FI and digitalization, as it explains the interaction between institutional quality, leadership support and governance structures in shaping DFI outcomes, the ability of the regulatory framework and the factors of user-centered adoption. The combination of these aspects provides a more detailed framework of how digital financial services can lead to cost-effective economic engagement, especially in less developed economies (Muat et al., 2025; Ozili, 2025; Abouelfarag & Elboghdadly, 2025). By emphasizing the mediating role of institutional quality, while positioning financial literacy and digital adoption as complementary conditions, the study contributes to the existing body of literature on FI by arguing that the simple availability of digital platforms is not sufficient to promote sustainable inclusion results (Hussain et al., 2025). It is a theoretical contribution to the current knowledge regarding inclusion as a multi-layered concept that bridges the technological and institutional dimensions with the behavioral dimension that has not been covered comprehensively in previous research. Practically, the findings will highlight the necessity of the holistic approach to the strategies of DFI. It is advised that policymakers, regulators and financial institutions develop interventions that would build institutional capacity, implement regulatory frameworks and enable leadership engagement to facilitate adoption and usability of digital financial services (Aldieri et al., 2025; Banihani et al., 2025; Tariq et al., 2025). These interventions can decrease socio-economic inequalities and promote sustainable economic development by explicitly connecting the concept of digitalization with fair access, which will lead to SDG 8 (Decent Work and Economic Growth) and SDG 10 (Reduced Inequalities). The implications of the conceptual model on future empirical research are also quite considerable. Having introduced leadership support and the quality of the regulation as complementary institutional conditions, it will be possible to quantitatively validate the importance of this set-in various contexts, and the researchers will be able to test how these two variables relate in terms of their strength in mediating the efficacy of digital financial services (Almazrouei, Alvarez-Torres, Schiuma, & Lopez-Torres, 2025; Wahab et al., 2025; Srivastava & Shunmugasundaram, 2025). Moreover, the model encourages cross-country comparisons, especially in emerging economies, to evaluate the effects of the socio-cultural, technological and institutional differences on the adoption, use and outcomes of adoption (Chowdhury et al., 2025; Lee et al., 2025; Valera et al., 2025). Such research could generate actionable insights into context-specific strategies for enhancing inclusion while minimizing digital divides. From a policy innovation standpoint, the study encourages regulators to move beyond conventional access-focused frameworks toward integrated digital financial governance that incorporates oversight, risk management and social accountability (Banihani et al., 2025; Jalal-Eddeen, 2025; Xia et al., 2023).

7. Theoretical contribution

This research theoretically contributes in many ways to the existing literature on FI, digitalization and governance frameworks. The study first broadens the conceptual understanding of FI by linking it to a wider institutional and governance context and pointing out the interaction between digital infrastructure, institutional quality and regulatory capacity (Muat et al., 2025; Ozili, 2025; Abouelfarag & Elboghdadly, 2025). In their work, the authors usually focus solely on the provision of financial services or the use of digital payments (Hussain et al., 2025; Kumari & Giri, 2025); however, the present research reveals that genuine inclusion necessitates a multi-dimensional perspective, which, among other things, entails leadership support, policy coherence and socio-economic enablers. Incorporating these elements, the paper moves forward the theoretical debates on FI as a result of both structural and behavioral determinants.

The theoretical information emphasizes that on the one hand, leadership engagement and regulatory control are not additional but fundamental to the implementation of DFI strategies, and on the other hand, they facilitate the integration of those strategies into the existing framework. In this framework, these elements operate within the broader mediating role of institutional quality rather than as independent moderating factors. Additionally, the paper is instrumental in emphasizing the growing relevance of digitalization in achieving the SDGs with special regard to SDG 8 (Decent Work and Economic Growth), SDG 9 (Industry, Innovation and Infrastructure) and SDG 10 (Reduced Inequalities) (Mendiola-Contreras & Horna-Saldaña, 2025; Lee et al., 2025; Afrida et al., 2024). The authors intuitively conceptualize DFI as a technologically driven development that needs institutional support. This construct provides a foundation for future research that seeks to move beyond simplistic access metrics and engage with more sophisticated indicators of effective inclusion, sustainability and governance. By integrating institutional theory, legitimacy theory and elements of political economy, the study offers a theoretically grounded framework that informs both scholarship and policy in the emerging field of inclusive digital finance.

8. Practical implications

The results of the present research have serious practical consequences by showing the willingness of the policymakers, financial organizations and development agencies to help improve FI with the help of digitalization. First of all, the DFI concept points out that mere access to financial services cannot produce any significant socio-economic outcomes (Muat et al., 2025; Abouelfarag & Elboghdadly, 2025; Hussain et al., 2025). Hence, the work of the field has to be not only the extension of digital payment facilities but also the deepening of the institutional systems, such as the regulation and administration, among other aspects. The mediating effect of institutional quality featured in the paper implies that companies and service providers in the financial services sector should operate in an environment where the rules, norms and enforcement mechanisms are well-developed to transform digital access into physical benefits to under-banked groups (El Yamani et al., 2025; Chowdhury et al., 2025). Secondly, the role of leadership support in pushing forward digital inclusion initiatives has been highlighted by the study (Tariq et al., 2025; Banihani et al., 2025). In the case of financial institutions and FinTech companies, it is essential to investigate effective measures, including the role of top management support to push forward FI initiatives, along with promoting financial literacy initiatives. Leadership plays a critical role in fostering organizational cultures that value both technological innovation and equitable access, thereby amplifying the impact of digital finance interventions (Almazrouei et al., 2025; Sandeep & Lavanya, 2025).

Third, the regulatory bodies can apply the knowledge revealed by the study to improve policy interventions to narrow the digital financial divide. The research findings show that regulatory quality strengthens the effectiveness of institutional mediation, which has either been positive or negative, on the enabling of digital financial services (Aldieri et al., 2025; Labhard et al., 2025; Ozili, 2025). In this scenario, it is very crucial for policymakers to resolve the issue of well-balanced technology and FinTech laws that should not have an adverse effect on FI and financial stability and, furthermore, should not cause financial exclusion (Kumari & Giri, 2025; Nandy, Kumar, & Chauhan, 2025). By implementing a comprehensive strategy that involves technology, literacy and strong institutional support, the practitioners will be able to remarkably raise the level of effectiveness of the digital inclusion programs.

9. Conclusion

This work provides a detailed concept-based analysis on the relationship between digitalization, FI and institutional qualities, identifying the overarching importance of leadership commitment and regulatory strength. Via a review of the most up-to-date literature, it is clearly shown here how FI has gone beyond technology and is dependent on institutions, governance and strong organizational support (Muat et al., 2025; Abouelfarag & Elboghdadly, 2025; Hussain et al., 2025). The concept-based framework for discussion below outlines how institutional strength mediates the relationship between DFI and socio-economic outcomes by structuring how digital systems generate inclusion benefits (Aldieri et al., 2025; Banihani et al., 2025). The result is important confirmation of the role of a total, integrated approach to FI which combines technology, financial education, governance and strictly regulated regimes to increase the overall efficiency and benefits of DFI (Mendiola-Contreras, Monica, Horna Saldaña, 2025; Valera et al., 2025). These are useful and important gains to improve greater FI benefits, financial well-being and work to minimize inequalities and are to greatly assist women, rural and youth beneficiaries (Dutta & Stivers, 2025; Afrida et al. 2024). The study further establishes that DFI contributes directly to the advancement of key SDGs, notably SDG 8 (Decent Work and Economic Growth), SDG 9 (Industry, Innovation and Infrastructure) and SDG 10 (Reduced Inequalities), by promoting equitable access to financial services and fostering inclusive growth (Ozili, 2025; Lee et al., 2025). In addition to theoretical contributions, this study offers actionable insights for policymakers, financial institutions and development agencies seeking to maximize the impact of digital financial systems. The emphasis on institutional quality, leadership support and regulatory capacity provides practical guidance for designing interventions that are resilient, inclusive and sustainable. When considering the future of DFI, this conceptual piece lays the groundwork for regional and socio-economic validation of its proposed relationships, and a concrete roadmap for the research is laid out by Kumari and Giri (2025) and Nandy et al. (2025). FI is most successful when underpinned by solid institutions, capable leadership and fair regulations, and it can be given a real boost by connecting the adoption of new technologies with governance and policies, enabling the building of financial systems that are not only innovative but also fair and sustainable.