– This paper aims to examine the consumption behaviour and effectiveness of coping mechanisms adopted by households living in disaster-prone regions of rural India to cope with climatic aberrations and extremes using household-level data. In developing countries like India, poor households living in rural regions face risks to their livelihood due to climatic aberrations like deficient monsoon spells and rainfall gaps. Although these risks are covariate, the impact depends on location and the relative capacity of the people to cope with them.

– Using household-level data, this paper attempts to examine the consumption behaviour and effectiveness of coping mechanisms adopted by households living in these areas to hedge against the risks. A tobit and a multivariate probit model is used in the process.

– Based on the empirical analysis, and subject to the assumptions and the usual limitations of data, the findings suggest that households resort to consumption smoothening by liquidating their assets or decreasing consumption.

– They adopt a wide variety of ex-post risk-coping measures with limited success to overcome the shocks to their livelihood. Household-specific characteristics like age and education level of the household head are important in the choice of a particular coping option along with other key variables.

1. Introduction

Climate-related aberrations and extremes like droughts, floods and hurricanes pose a significant problem to the livelihoods of people living in developing countries already struggling with a high incidence of poverty and increasing economic inequalities. This holds true for India also, where a majority of the population is employed in the agricultural sector, which is still highly dependent on rainfall (monsoon), although attempts have been made over the years to improve the efficiency of alternative sources of irrigation (Pandey et al., 2007). The risks to agriculture and the damages due to climatic aberrations and extremes will rise in future as the intensities of events like droughts, cyclones and floods will increase and there will be shifts in rainfall patterns (Mirza, 2003; Bouwer et al., 2007; Botzen and van den Bergh, 2009; IPCC, 2012). With regards to India, preliminary assessments reveal that the severity of droughts and intensity of floods in various parts of India might increase (NATCOM, 2004). Most of the river basins in India may experience constant water scarcity, and are likely to experience seasonal or regular water-stressed conditions. Although the most significant challenge facing countries like India is poverty, the impacts due to increase in climatic aberrations may increase the vulnerability of the population living in disaster-prone regions, and put additional burden on the poverty alleviation policies and programmes of the government.

Although the risks and shocks due to climatic aberrations are covariate, the impacts could be idiosyncratic depending on the resilience and adaptive capacity of the households in question. They reduce households’ income and consumption, destroy productive assets and pose a hindrance to other welfare measures (Ravallion and Chaudhuri, 1997; Dercon and Krishnan, 2000a and 2000b; Datt and Hoogeveen, 2003; Dercon et al., 2005; Christiaensen et al., 2007; Thomas et al., 2010). This either drives households into poverty or makes them more vulnerable if they are already poor. Households do take up various measures to cope with shocks, which are supported by themselves, civil society or the government. Hence, assessing the effectiveness and determinants of different interventions has relevant policy implications in the context of designing disaster reduction policy (Thomas et al., 2010).

The impacts of these climatic aberrations depend to the extent of the damage sustained by income-generating assets/activities and on the period of disruption of flows of goods and services. In developing countries, the primary impact of a disaster is on volatility of consumption due to the shocks in production. These production shocks are then transformed into consumption shocks because of underdeveloped and ineffective risk-management schemes (Matarira et al., 2013; Patnaik and Narayanan, 2010; Auffret, 2003). In view of this, the paper attempts to examine the impacts of climatic aberrations like droughts and rainfall gaps on the livelihoods of the vulnerable households. In focal terms, the study, firstly, analyses the consumption behaviour of the households, and secondly, examines the effectiveness of coping mechanisms adopted by the households to hedge against the shocks due to climatic aberrations. In the process, the paper also examines the relationship between household-specific characteristics like economic status, presence of migrants, age of the head of the household and the choice of a particular coping option. The study is with reference to Gorakhpur and Maharajganj districts in eastern Uttar Pradesh region of India bordering with Nepal, which is prone to droughts and rainfall gaps. The rest of the paper is organized as follows: Section 2 presents the review of literature on the impact of shocks on household consumption and effectiveness of coping mechanisms. Section 3 describes the study area, data collection methods and the sampling procedure used for the household surveys. While Section 4 describes the methodology of the study and the econometric issues, Section 5 presents the results and discussion. Finally, Section 6 presents the conclusions emerging from the analysis.

2. Review of literature

Disaster events result in a shortfall of income among households who smoothen their income and/or consumption to cope with the risks and shocks (Morduch, 1994). While income smoothing options are taken during ex-ante (i.e. before the shock having taken place – making conservation production and employment choices and diversification of income), consumption smoothing measures are adopted during ex-post (i.e. after the occurrence of shocks – like borrowing and saving, depleting and accumulating non-financial resources, adjusting labour supply and relief measures provided by the government after the shock). The presence of formal or informal insurance markets facilitates households in following their previous consumption paths in the aftermath of the disasters. Previous studies have shown that perfect risk-sharing exists based on a set of assumptions (Arrow and Hahn, 1971; Fafchamps and Lund, 2003; Coate and Ravallion, 1993). Also, over the years, a growing body of literature has tested whether households within villages, regions and even countries fully share risk. These studies test for full insurance by estimating consumption equations and testing whether household income affects household consumption given community consumption. Mace (1991) and Cochrane (1991) test the full consumption insurance model using US data. Studies focusing on developing countries include Townsend (1994), Morduch (1990) and Ravallion and Chaudhuri (1997) for India; Deaton (1991) for Cote d’Ivoire; and Udry (1990) for Nigeria. In the context of the determinants of adaptation measures, some recent studies have attempted to examine farmers’ adaptive behaviour in the context of Africa, Latin America, China and South Asia (Maddison, 2007; Kurukulasuriya and Mendelsohn, 2007; Nhemachena and Hassan, 2007; Seo and Mendelsohn, 2008; Hassan and Nhemachena, 2008; Gbetibouo, 2009; Deressa et al., 2009, 2011; Bryan et al., 2009; Deressa, 2010; Wang et al., 2010; Di Falco et al., 2011, 2012; Panda et al., 2013; Bahinipati, 2013), borrowing the conceptual framework from the agricultural technology adoption studies (Feder et al., 1985).

The findings from these indicate that households develop a variety of risk-coping mechanisms to hedge against the impacts (both ex-ante and ex-post). While ex-ante mechanisms may include options like crop and asset diversification, migration and specialization into low-risk activities, ex-post mechanisms may include strategies like dissaving, insurance, borrowing, sale of assets, help from community, monetary transfers from friends and relatives, etc. Although the risks are aggregate, the impact varies across households depending on key idiosyncratic characteristics which also facilitate coping (presence of assets, availability of income diversification options, etc.). However, as observed by Dercon (2002), individual savings and informal risk-sharing arrangements may offer a partial coping capacity. There are numerous studies that have tested the effectiveness of these mechanisms in the context of different countries (Rosenzweig and Binswanger, 1993, for India; Dercon and Krishnan, 1996, for Western Tanzania; Kurosaki and Fafchamps, 2002, in Punjab, Pakistan; Dercon and Christiaensen, 2007, for Ethiopia). Rosenzweig and Binswanger (1993) find that a one standard deviation decrease in weather risk raises average profits by up to 35 per cent among the lowest wealth quintile in semi-arid India. Porter (2008) argues that poor people in developing countries tend to face greater risks to their already low incomes and are also less equipped to deal with such risks due to fewer assets, fewer opportunities to diversify income, limited or no formal social insurance or social protection provisions and limited access to incomplete or even missing markets for credit and insurance.

The ex-post risk-coping strategies aim at stabilizing the consumption level of households by reducing consumption expenditure, use of credit by reallocating future resources for present consumption, selling of physical and financial assets after disasters, remittances, etc. The government also complements the risk-coping behaviour of households through various means like distribution of relief, direct public monetary transfers and workfare programmes. Informal arrangements like mutual transfers (monetary remittances) from relatives, friends and neighbours may also exist (Mace, 1991; Townsend, 1994). It is also observed that households often resort to using more than one coping mechanism to safeguard against climatic aberrations and extremes. Therefore, coping mechanisms cannot be considered in isolation, as pointed out by Attanasio and Weber (1993), and as Sawada and Shimizutani (2007) also argue that in case of extraordinary shocks, the assumption of separability of coping strategies can be problematic, as large shocks might substantially alter household preferences across goods and affect household’s consumption of different items simultaneously and not separately. Therefore, the pertinent question is whether informal coping mechanisms built around community or family relationships are helpful in overcoming the fluctuations in consumption faced by households in the aftermath of climatic aberrations and extremes.

3. Study area and data

The state of Uttar Pradesh is one of the largest and underdeveloped states in India. In terms of the Human Development Index, the state ranked 13 among the other Indian states, with a value of 0.38 for 2005. The annual per capita income for the state was around US$ 450 and having roughly 40 per cent of its population in the poverty group. As per the 2001 Census, Uttar Pradesh continues to be the most populated state in the India, with a population of over 166 million, of which approximately 80 per cent reside in rural areas, accounting for 16.4 per cent of the population of the country. During the past decade, incidence of severe droughts was reported in 2002 and 2004. The recurrence period of highly deficient rainfall in eastern Uttar Pradesh has been calculated to be 6 to 8 years. The areas relatively more vulnerable to drought are the Nautanwa and Laxmipur Blocks (administrative boundary within a district) in the Gorakhpur and Maharajganj districts of eastern Uttar Pradesh. Figure 1 shows the location of the study area in India. The incidence of drought and rainfall gaps is reported during the summer cropping season (October-June) when two principal cereal crops are grown (paddy and wheat). Out of these two cereal crops, paddy is the most widely cultivated cereal in the study area, although a few households also grow wheat. The direct impact of droughts and rainfall gaps is the resultant crop loss of the two principal cereal crops due to unavailability of water in the growing periods. The indirect impacts are mostly reduction in food availability and the associated health-related impacts due to malnourishment during the post-drought period.

The study is based on data from primary household surveys for drought-affected households (spread over a radius of 5-6 km). The villages were chosen based on a simple random sampling and a single level of stratification. Firstly, on the basis of the source of irrigation, all the drought-affected villages were divided into the following three categories:

villages where tube-well and canal irrigation were not available;

villages where canal irrigation was available; and

villages where group tube-well irrigation was available.

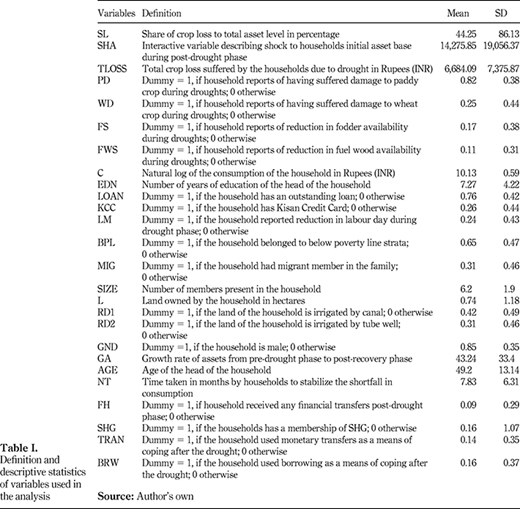

Secondly, from the above list of villages, households were drawn randomly and surveyed. Ten per cent of the total households were surveyed in each of these villages, which corresponds to approximately 120 households in total, out of which 32 belonged to the first category, 49 belonged to the second and the rest 39 were from the third, respectively. The surveys were undertaken in the year 2008 during the post-sowing season when there was comparatively lesser farming-related activities and the households were available for the survey. Also, this was a year free from climatic aberrations in that region and was also much after the previous incidence of droughts. Majority of the households reported agriculture as their primary source of income. However, some reported that agricultural labour and non-farm wage labour were a supplementary source of income. Table I defines the variables used in the analysis.

It can be observed from Table I that the average growth rate of household’s asset (GA) is around 43 per cent over a period of 10 years (base year 1998) with a low standard deviation. The observed growth rate is high because the assets are proxied by household expenditure. As households reporting higher expenditure also own higher assets, household expenditure is used to proxy for asset base, as also followed by Morduch (1999) and Dercon (2002) for Africa. Carter et al., (2007) reports similar impacts after Hurricane Mitch, which resulted in losses to plantations and land in Honduras. The share of household’s crop loss suffered to its total asset base stands high at 44 per cent. Similarly, the total loss (other losses including crop loss) suffered by the households in the sample is quite high, as the mean is around INR (Indian Rupees) 6,600 (around US$ 130-140). With respect to damage to paddy crop, the analysis shows that around 82 per cent of the households have suffered damage due to the droughts, although the scale varies from one household to another. Wheat crop loss is cited by 26 per cent of the households, as there are limited households cultivating wheat. During droughts, it is observed that there is considerable shortage of fodder for livestock and fuel wood for household use. We include these variables as shock variables in our analysis with an aim to find out how households cope with the shortage of these during droughts. In the present sample, 17 and 11 per cent of the households report shortage of fodder and fuel wood, respectively. In the study area, there are two major coping mechanisms that are used by the households to cope with post-drought impacts. Monetary transfers among friends and relatives, and borrowing (taking additional loans) are the most reported measures of coping by the households in the study area after the drought event. Other coping strategies like relief, selling of livestock, selling of household assets and selling of land were dropped from the analysis because only a small fraction of the households (below 0.05 per cent) reported having used these strategies as a means of coping. Similarly, the respondents report not receiving any relief from either governmental or non-governmental agencies.

In the sample, around 76 per cent of the households had outstanding loan. Around 24 per cent of the households reported to have suffered because of lack of access to labour markets during the drought period. While 65 per cent of the households are in the below poverty line category, 35 per cent of the households are above it. The mean age of the head of the household is around 49 years, the average family size is around 6 members and 85 per cent of the households are headed by males. The average time taken by households to reach back to their pre-drought consumption levels is around eight months. However, this is highly skewed, as the maximum value for the variable stands at three years, while the minimum value stands at zero. Kisan Credit Card (KCC) is a government initiative aimed at providing farmers with monetary compensation for their crop losses after disaster events. In the present sample, only 26 per cent of the households report having access to this card. The variable RD is a regional dummy capturing the households having access to irrigation from different sources. Around 73 per cent of the households have access to either canal or tube-well irrigation in their farming fields. The respondents also report the presence of out-migrants in their households, with around 31 per cent households having a migrant member in their family.

4. Methodology and econometric issues

Climatic aberrations like droughts are a gradual onset event where the event is spread over a period. The immediate and direct impacts are not so large as compared to the longer-term and indirect impacts. The direct impacts are generally negative, with an inverse relationship between the incidence of drought and agricultural production, irrigation, ground and surface water availability, etc. The micro impacts can escalate household food insecurity, water-related health risks and loss of livelihoods in the agricultural sector. While a general decline will be observed for water resources (in terms of quality and quantity), availability of food and fodder, household assets and private savings of the households and income inequality could increase (Rathore, 2005). The opportunities for farm, non-farm and other rural employment disappear because of production losses. Hence, people who lie perilously just above the poverty line fall back below it, while those who are already below poverty line are pushed further below.

In view of the difference in nature of impacts during a drought as compared to a flood or hurricane, we follow the framework of Carter et al. (2007) to examine the impact of droughts on the consumption behaviour of households. The consumption streams of households are divided into three phases:

the first phase is the years before the occurrence of drought (which are normal years);

the second phase is the occurrence of the drought phase, which may be a long period extending over several months; and

the recovery phase, that is the years following the occurrence of drought.

The econometric model adopted for examining the impact of drought on the livelihood of households captured through their consumption streams is represented by equations (1) and (2): Equation 1

where, Equation 2

Where, y*i is the asset growth for household i over time, stretching from the pre-shock period to the recovery period (several years after the shock). The household’s initial asset level, Ai, is included to know whether there is a single equilibrium asset level, towards which households grow. An estimate of β1 < 0 would show a convergent accumulation process with lower-wealth households growing rapidly towards the equilibrium level, while the asset growth of wealthier households would slow down and approach zero as the equilibrium level is reached. The point at which the growth rate equals zero would be a long-term equilibrium or steady-state asset position. The variable Xi measures the shock variables and other coping variables like household’s access to off-farm labour, access to financial and/or social capital. Finally, specification contains other control variables (gender, life cycle age of the households and other household-specific characteristics) that are represented by the vector Zi. The term ui is the well-behaved error term and measures latent, random factors that impact consumption growth of the households. From equation (1), it can be observed that the outcome variable in the present case turns out to be a continuous variable and for a number of observations, the value is missing or turns out to be an outlier because of the reporting bias of the households. Therefore, the dependent variable is censored whereby information for some of the observations is missing, although the corresponding information for the independent variables is present. The ordinary least squares estimate for such censored regression models will be biased and will have inconsistent parameter estimates. The bias will arise because there is no guarantee that the E(ui) = 0 because of the censoring of the sample and the error term might turn out to be heteroscedastic (Pindyck and Rubinfeld, 1991).

There are both ex-ante and ex-post measures of coping with extreme events like droughts. In India, the ex-ante coping options are generally based on top-down approaches and aim at pre-disaster preparedness. Ex-post coping mechanisms aim at consumption smoothening after the disaster and include measures like dissaving, insurance, borrowing, sale of assets, etc. It can also be in the form of reducing consumption expenditure, use of credit by reallocating future resources for present consumption, accumulation of physical and financial assets as a precautionary device, remittances, etc. They help in mitigating risk and reducing income instability, thereby smoothening consumption paths. For example, farmers manage agricultural production risks via crop diversification, intercropping, use of low-risk technologies and use of contracts such as sharecropping. However, when it comes to disasters like drought, ex-ante measures may not be effective in providing compensations ex-post, as they occur on an unprecedented scale and it may not be possible to fully hedge against them. As described in the preceding section, there are two major coping options that are used by the households and hence we study the effectiveness of these two:

monetary transfers; and

borrowing (taking additional loans).

Following Flavin (1999) and Sawada and Shimizutani (2007), the model used for the multivariate probit estimation is defined in equations (3) to (6): Equation 3,Equation 4

where, Equation 5,Equation 6

In the equations, S represents a matrix of household-specific shock variables generated by the droughts and that H is a matrix of household characteristics and other control variables. The variance-covariance matrix of ɛmi is symmetric and the covariances are assumed to be non-zero with the restriction condition var(ɛ1i) = […] […] = var(ɛni) = 1 for identification purposes. Under the assumption of joint normality of the error terms, a multivariate probit model is estimated. As one cannot directly observe the intensities of the risk-coping strategies, i.e. Δb and Δy, the dependent variables in the above equations indicate whether a household adopted a particular risk-coping option against the drought, which can be represented by a discrete variable, pm, m = 1, 2 (i.e. a dummy variable depicting whether a particular household adopted a particular risk-coping strategy).

The independent variables are a matrix of household-specific shock variables generated by the disaster, household characteristics and other control variables. To estimate the parameters under this setting, a log likelihood function is used, which depends on the multivariate standard normal distribution function. The empirical framework involves estimating multivariate binary-dependent variable models. The analysis utilizes the estimation process outlined by Cappellari and Jenkins (2003) to estimate the multivariate probit model using the method of simulated maximum likelihood (SIML), also known as the Geweke–Hajivassiliou–Keane (GHK) estimator using STATA. The GHK estimator expresses the multivariate normal distribution function as the product of sequentially conditional univariate normal distribution functions that can be easily and accurately evaluated. In the case of multivariate normal limited dependent variable models, the simulated probabilities of the GHK simulator are unbiased and are bound within the (0,1) interval and GHK is more efficient in terms of variance of the estimator of probabilities than other simulators like acceptance-rejection or stern simulator. It is consistent as the number of draws and the number of observations tends to infinity and thus satisfies the asymptotic property of maximum likelihood estimator (Cappellari and Jenkins, 2003).

5. Results and discussion

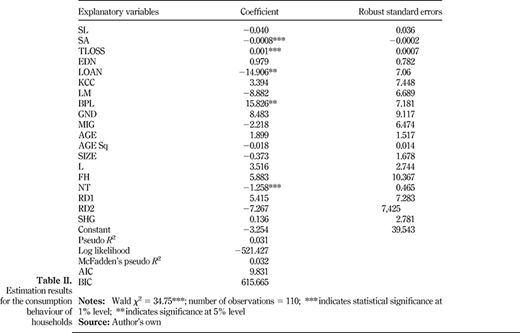

Two shock variables extensively impact the consumption behaviour of the households in the study area. These two variables (SA and TLOSS) are significant at the 1 per cent level. The interactive term (SA) exhibits a negative sign, suggesting that having higher assets magnifies the detrimental impact of shocks on the growth of assets, though the value is very low. The variable TLOSS, which depicts the crop loss suffered due to drought, appears with a positive sign, implying that the growth of the assets owned by households is positively related to the crop loss suffered by them. The results are presented in Table II.

The coefficient of the interactive variable (SA) encompasses many appealing findings. Though the coefficient value is not very large, it still portrays the negative impact of droughts on the asset base of the households. Hence, there is evidence that households engage in consumption smoothening by substituting their asset base. Households resort to liquidating their household assets to substitute for the shortfall in consumption during the drought phase and higher this asset base, the greater is the substitution.

The model also explores the degree to which social mechanisms, food aid, access to loans and access to labour markets bolster asset growth. None of the variables was significant, except access to loans. This variable is significant with a negative sign, indicating that having access to loans does not result in growth of assets over the years for the households. Most of the control variables are insignificant, except NT and BPL, which are significant with the expected signs. Therefore, it can be inferred that growth of assets after the drought is indirectly related to the time taken by the households to get back to their pre-drought consumption levels. Similarly, households living below the poverty line exhibit a direct relationship with the growth rate of assets. This confirms the neoclassical phenomenon of convergence in a microeconomic framework implying households living below the poverty line try to catch up with richer households over a period. The Wald chi-square value is very high at 34.2 and is significant.

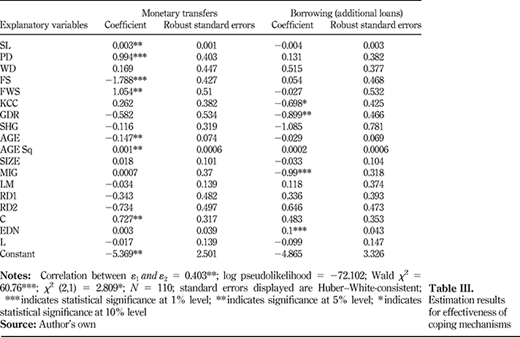

As described in the previous section, we use a multivariate probit model to study the effectiveness of coping mechanisms adopted by the households, and the results are presented in Table III. From Table III, it is observed that the Wald chi-square statistic is significant, implying the model is correctly specified. The chi-square statistic regarding the independence of error terms is significant and hence justifies the use of a multivariate probit model. Considering the case of monetary transfers from friends and relatives as a means of coping, we find some of the household-specific variables like age and presence of outstanding loan to be significant. The positive sign between loan and transfers suggests that if the household has an outstanding loan, it is less likely to use monetary transfers as a means of coping. The coefficients of the variables age and age squared suggest that age has a negative and non-linear impact on the probability of adopting monetary transfers as a means of coping, conditional on the age of the respondent. This implies households where the head is relatively young are not likely to adopt transfers as a means of coping. This is because younger people have access to other avenues to cover up the shortfall in their consumption/income rather than depend on receiving monetary transfers from relatives and friends. Alternatively, older people because of their social standing may prefer to depend on friends and relatives for coping rather than depend on borrowing. This may in fact reflect life cycle effects, where, under a finite horizon, the optimal amount of precautionary savings is a positive function of the length of the remaining life (Caballero, 1990). Households with higher consumption levels are also likely to resort to monetary transfers as a coping option.

The next coping option examined in the specification is the role of borrowing or taking additional loans by the households. Here none of the shock variables is significant; however, some of the household-specific variables turn up significant, like migration (showing presence of out migrants in the household). The negative sign here suggests that households with migrant members are not likely to resort to additional loans, and hence, remittances from migrant members are a decisive factor in the choice of borrowing as a means of coping. The insignificant location dummies indicate that having access to source of irrigation is not related to the choice of coping mechanism. The variable education (EDN) is significant with a positive sign, indicating that households with higher levels of education of the head use borrowing as a coping measure. Higher levels of education increase the access to multiple sources of income, thereby providing a steady source of consumption and guaranteeing regular payback of loans. The variable gender is also significant with a negative sign, suggesting that households where the head is male are not likely to resort to borrowing as a coping mechanism. It is also appealing to note that the variable KCC is significant with a negative sign. This is an initiative of the Central Government of India to help farmers with monetary compensation depending on the severity of damage suffered by their crops. In the present case, households having this card are not likely to use borrowing as a chosen method of coping. On perusal of the correlation coefficients between the two error terms, one can find a positive relationship which is statistically significant. This implies that they act as complements and households in the study area are likely to use a mix of these strategies to cover up the loss suffered due to droughts.

6. Conclusion

In this paper, we attempted to study the impact of shocks generated due to climatic extremes like droughts on the consumption behaviour of the households and analyse the effectiveness of various coping options used by the households to hedge against such events. We find that there is evidence of convergence of households in the bottom part of the consumption strata, towards the higher groups over a 10-year period. Households resort to consumption smoothening behaviour by liquidating their assets or decreasing consumption levels to cope with a slow-onset disaster like drought. The results suggest an inverse relationship between the asset level and time taken to reach back to pre-disaster consumption level. Also, the location of the households relative to sources of water for irrigation has no major impact on the consumption pattern of the households. Some household-specific characteristics like economic status of the households and the years of education of the head of the household are influential in determining the growth of the assets base of the household over the years.

With respect to effectiveness of coping mechanisms, it was found that the households adopt monetary transfers and borrowing as coping to overcome the shocks to their livelihood. However, we did not find evidence of full risk-sharing, as also observed by Alderman and Garcia (1992), Deaton (1992) and Morduch (2002). Specifically, monetary transfers from friends and relatives as a means of coping were resorted to by the households to cover up crop loss. Households having migrant members do not resort to borrowing as a coping strategy. Household-specific characteristic like age, gender and level of education of the head of the household play an important role in the choice of the coping mechanism. To sum up, the analysis indicates that no particular coping mechanism can help the households to fully hedge against the shocks, hence the focus should be to devise ex-ante measures for dealing with disaster impacts and educate the targeted population by disseminating information regarding these through multiple means like the use of information and communication technologies. From a policy perspective, as advocated by Dercon (2002) and Dercon and Krishnan (2002), concentration should be towards implementing resilience-enhancing measures which help to raise the levels of income and interventions that generate adequate employment opportunities for diversification of livelihood.

References

Further reading

About the authors

Unmesh Patnaik is a PhD in Economics from the Department of Humanities and Social Sciences, IIT Bombay, Mumbai, India, and currently teaches at the School of Habitat Studies, Tata Institute of Social Sciences, Mumbai, India. His research interests include applied econometrics, development economics and vulnerability and adaptation to natural disasters and climate change. Unmesh Patnaik is the corresponding author and can be contacted at: unmeshpatnaik@gmail.com

K. Narayanan is a Professor of Economics at the Department of Humanities and Social Sciences, IIT Bombay, Mumbai, India, and also holds Institute Chair Professorship. His research interests include development economics, industrial economics, international business, industry–environment linkages and socioeconomic impacts of climate change.