This article conceptualises how the economic well-being of an entrepreneurial household affects its members' mental accounting process to establish its affordable loss for a plunge decision.

The article used research literature to analyze the resources available for entrepreneurial endeavours against a household's ability to maintain acceptable minimum material living standards, juxtaposing income and wealth against competing consumption and investment opportunities.

Mentally accounting for whether household resources can meet minimum material living standards is central to entrepreneurs' ability to raise affordable loss and decide to invest in a new venture. The article proposes that entrepreneurial households establish affordable loss by availing their money exceeding that required to maintain acceptable minimum material living standards. In low-income households, the author assumes that members are not employed and can thus avail their time (versus money) towards affordable loss.

Economic well-being introduces mental accounts of income and wealth and a hedonic reference outcome in the material living standards of households required to meet basic needs. The article introduces the tension entrepreneurial households face between using their income and wealth towards investing in a new business and maintaining their material living standards. It introduces the idea that a loss can be “affordable” according to an entrepreneurial household's ability to remain above its acceptable minimum material living standard. This view prompts scholars to consider a household unit of analysis and avoid assuming an entrepreneur makes the plunge decision in isolation.

Introduction

Despite often equal chances of gains, many entrepreneurs focus instead on the potential loss of their resources in the worst-case scenario: business failure. They will seek opportunities to start a new venture only if they believe they can afford this loss (Sarasvathy, 2001). With increasing costs to start a new venture, decisions to take the plunge become increasingly likely when entrepreneurs can increase this affordable loss (AL). To raise AL, entrepreneurs adopt several strategies. They locate funds weakly coupled to repayment—for example, the patient capital of a loan from a family member (Dew et al., 2009). They invest in increments at a time (Jiang and Rüling, 2019). Instead of money, they may use their time, knowledge, and unused physical resources (Fischer and Reuber, 2011; Martina, 2020). These strategies have been theorised using a mental accounting process from behavioral economics (Dew et al., 2009).

As much as behavioural economics reveals how—through mental accounting--and why—loss induces painful emotions—entrepreneurs turn to the AL heuristic, we know little about what drives these loss concerns. Because entrepreneurship scholars have viewed resource availability in isolation from consumption, the field may have overlooked how an entrepreneurial household's concerns about losing their material living standards (MLS) influence whether losses are affordable. This article proposes that these concerns arise from entrepreneurs' attempts to preserve their family's economic well-being (EWB). EWB reflects a household's MLS based on its command over income, wealth, and resultant consumption possibilities (OECD, 2013). Maintaining an acceptable lower level of MLS, at least during the early years of entrepreneurship, challenges the maximizing assumption of traditional economics. Scholars may have overlooked this because they tend to ignore the influence of entrepreneurs' personal lives on their business endeavors (Jennings and McDougald, 2007).

This article asks how financial sources of EWB are mentally accounted for towards the ability for AL and the decision to start a new venture. It argues that entrepreneurs mentally accounting for whether household resources can meet minimum MLS is central to the ability to raise AL and make the decision to invest in a new venture. Households use the acceptable minimum material living standard as a reference point to guide their decision-making process. Money exceeding the meeting of this reference point is available for investment in new ventures. The article endeavors to make four contributions to the literature. First, the article introduces the entrepreneurial household as a vital setting for the plunge decision. The household reveals not only the entrepreneur's broad access to resources possessed by extended family members and associated business networks but also shows that concerns about risks posed to their material living standards have an important effect on perceptions of AL. Second, the article introduces the tension between investment and consumption decisions in applying the AL heuristic to entrepreneurial decisions. The article's third contribution presents the acceptable minimum MLS as a hedonic reference outcome in the evaluation step of the entrepreneurial household's mental accounting process. The acceptable minimum MLS is a crucial reference point for households, as it represents the baseline level of income and wealth needed to support their basic needs and maintain their current standard of living. Any investment in a new business must compete against the money required to maintain this minimum standard, which creates a tradeoff between current consumption and future investment. This helps us extend the entrepreneurial household's mental accounting process beyond categorizing sources and uses of money to evaluate the outcomes of any expenditure decision, which directly influences the AL heuristic and entrepreneurial decision. The article's fourth contribution is to introduce a diverse set of entrepreneurial household circumstances, with varying command over their income flows and wealth stocks. Thus, one learns about the likelihood of individuals from households with different incomes and wealth taking the plunge into entrepreneurship.

Entrepreneurs' affordable loss and mental accounting

AL is a decision tool entrepreneurs use to limit their losses to an affordable amount that can render their risk-taking acceptable (Sarasvathy, 2001). Practically, entrepreneurs use this tool when they have very little information about the gains of an opportunity. For example, entrepreneurs who experience uncertainty in pursuing creative opportunities rely on little information about existing customers and their desire for the proposed product or service compared to those who replicate existing opportunities. Creative-type opportunities exist in the minds of entrepreneurs. To make decisions, these entrepreneurs rely more heavily on information about their available resources, including their capital, to create and exploit a certain opportunity. Many entrepreneurs pilot their projects and implement them in stages, which help them gather information and learn about the opportunity as it is being created (Blank, 2013). This management of loss approach has the advantage of ensuring survival in case of failure.

AL has been delineated into ability and willingness components. While entrepreneurs may estimate the amount of resources they can access, ultimately, they must be willing to lose this amount. Ability does not depend on the new venture; it relies on resource access and varies from entrepreneur to entrepreneur. Willingness, on the other hand, relies on the product or service being created. For example, if a pilot project reveals small research, development, and commercialization costs, this may lead to a low willingness to invest large amounts despite one's ability to do so (Daniel et al., 2015). Willingness is thus influenced by the information one gathers during experimentation and commercialization of the opportunity.

Entrepreneurs assess their ability to take downside risks by categorizing and evaluating the various resources accessible to them as losable or not. The psychological process of mental accounting describes this process: as “a set of cognitive operations used by individuals and households to organize, evaluate, and keep track of financial activities” (Thaler, 1999: p. 183). Mental accounts of resources entrepreneurs deem not losable are off-limits in the plunge decision. For example, in an entrepreneurial household, a mental account of money for children's education may be off-limits for the new business because education prepares loved ones to handle future challenges. Still, a mental account of money budgeted for entertainment may be categorised as an AL.

Thus far, mental accounting theory has been applied to entrepreneurship to suggest that entrepreneurs raise AL from funds weakly coupled to repayment—for example, the patient capital of a loan from a family member or payments made from one's credit card on behalf of the new business (Dew et al., 2009). Entrepreneurs also treat the new business as a series of mini projects investing in increments at a time (Jiang and Rüling, 2019). Resources need not be monetary: households may be able and willing to “lose” time, knowledge, and unused physical resources (Fischer and Reuber, 2011; Martina, 2020). When households can raise levels of AL, then the likelihood of taking the plunge increases.

Apart from categorizing the sources and use of resources into mental accounts, entrepreneurs evaluate the outcomes of any expenditure decision. Outcomes are evaluated in terms of their hedonic consequences. Losses result in more severe emotions than equivalent gains (Kahneman and Tversky, 1979). Moreover, mental accounting theory contends that outcomes in different accounts are evaluated separately and are not fully fungible (Thaler, 1999): a loss in an income account budgeted for children's education may be too painful and not cancel out a gain in the wealth account, e.g., money applied towards a promising investment opportunity.

One way to view money off-limits for a new business is to develop mental accounts of household financial capital: current income, current wealth, and future wealth (Shefrin and Thaler, 1988). The current income mental account sees income flow into it regularly. Current income includes the wages of employed householders, money in cheque accounts, dividends, capital gains, drawings from householders owning businesses, rent from property, pension and other cash social payments, and social transfers such as education and health care received from governments (OECD, 2011: p12). Though it may vary from household to household, generally, current wealth reflects the capital value of assets. It is stock already possessed by a household. It may include shares, pensions, vehicles, and borrowings from home equity (OECD, 2011: p. 12). In entrepreneurship, one's wealth might also include the human capital deployed as sweat equity (Stiglitz et al., 2009). Sweat equity involves entrepreneurs investing their and other family members' time and labor in place of the money required to purchase labour and services from external parties (Bhandari and McGrattan, 2021; Martina, 2020). Future wealth can include home equity, human capital in households with students, and the capital value of pension funds and retirement funds. In the case of households with retirees or pensioners, payment from these funds becomes part of the current income, and the capital becomes part of the current wealth.

We possess little insight into how the three categories of mental accounts—income, current wealth, and future wealth—result in the propensity to “invest” in a new venture. While a startup can be treated as an investment activity, the above mental accounts have been used by behavioral economists to predict the consumption behaviour of households, not how they make the plunge decision into entrepreneurship. Households are more prone to use current income than current wealth for consumption; they are least likely to use future wealth. Current income directed towards investment delays consumption. Thus, households may only use income exceeding that used for consumption needs to invest in a new venture. Wealth appears better suited for investment purposes, especially for the up-front investment required to start a new venture.

Economic well-being and the ability to take the plunge

Insights about how entrepreneurial households juggle their investment decisions against consumption decisions can be provided by an economic well-being (EWB) perspective. EWB reflects a household's material living standards (MLS) based on its command over income and wealth and resultant consumption possibilities to fulfill its members' needs (OECD, 2013). Both income and wealth can provide them with the resources to satisfy the consumption required to meet their desired MLS. Whereas wealth can help smooth consumption during unexpected changes in income, income is the primary determinant of consumption.

Significantly, EWB shifts the unit of analysis from the individual to the household (Carter, 2011; OECD, 2013). The household is the center of an overlapping social system where extended family members and other business networks also come together (Pittino et al., 2020; Tagiuri and Davis, 1996). The household may also be the primary site of the entrepreneur's immediate effectual network of stakeholders (Sarasvathy and Dew, 2005). However, this paper constrains the set of individuals in the household in two ways. First, it considers just the potential investors of an entrepreneurial venture living in the same household. Second, it only considers extended family members in the same geographical location, making relying on those members to participate in a new business practical. From this network, entrepreneurs may depend on intangible resources such as knowledge and expertise and tangible ones such as sweat equity (Jones and Li, 2017; Lichtenstein and Brush, 2001).

Starting a new business is a challenging endeavor that requires significant financial resources, including capital investment, working capital, and startup expenses. Households can rely on their income and wealth sources to finance a new venture. However, they must also balance their desire to invest in a new business with their need to maintain their current material living standards.

In this context, MLS refers to the minimum level of material well-being that a household considers acceptable. This includes access to basic necessities such as food, shelter, clothing, and healthcare and discretionary spending on non-essential items such as entertainment and leisure activities. This minimum acceptable standard serves as a reference point for households as they consider how much money they can afford to invest in a new business without jeopardizing their well-being. Suppose entrepreneurial households go below the acceptable minimum MLS due to loss in consumption from loss in income and wealth mental accounts. In that case, members will feel pain, which may deter the household's ability for AL. Unlike children's education, entertainment is likely to be excluded. Education secures the family's well-being in the longer term, whereas entertainment probably does not. Further, one household's minimum requirement for children's education may mean expensive private education; another will be affordable public education.

The household may also serve as the “starting resource” base for tangible resources (Brush and Manolova, 2004: p. 39). For example, the entrepreneur can use money, equipment, and facilities that a household can often offer at a lower cost than external institutions (Alsos et al., 2014; Newbert and Tornikoski, 2013). In return, all the stakeholders connected to the household (including their consumption, income, and wealth) become, in part, the entrepreneur's concern. In other words, concerns about MLS extend beyond the individual entrepreneur and, therefore, affects the plunge decision.

Households cannot always rely on the current income mental account to fund MLS. Wealth comes to the rescue when income becomes volatile or insufficient to meet MLS. For example, when householders change jobs or limit working hours to enable studying or looking after children, they can use wealth to smooth consumption. This is likely the case in entrepreneurial households when the potential entrepreneur resigns from paid employment to focus on starting a new venture. While some households may have an employed spouse or another householder to subsidise the entrepreneur's consumption, others may have to rely on some current wealth. Thus, households that are “asset rich and income poor” generally possess higher MLS than revealed by their income alone (OECD, 2013, p. 36). In Table 1 present four household MLS based on their command over income and wealth.

The entrepreneurial decision in terms of affordable loss and economic well-being

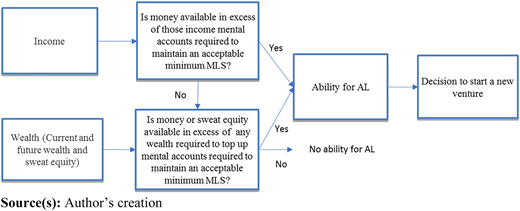

When households increase their ability for AL, then one or more members may take the plunge decision. Figure 1 shows how households assess their ability for AL to increase the likelihood of a plunge decision. Mentally accounting for whether household resources can meet the minimum MLS is central to the ability to raise AL and make the decision to invest in a new venture. Households use the acceptable minimum material living standard as a reference point to guide their decision-making process.

Mental accounting theory suggests that households may find it painful to use income flows to meet their basic needs towards investment opportunities. Thus, households may first assess whether their income flows can meet their minimum MLS. In some households, all mental accounts connected to meeting minimum MLS can be fulfilled by income, and surplus funds remain. In that case, this income surplus and any additional wealth can contribute towards their ability for AL. If income is inadequate to fulfill mental accounts connected to minimum MLS, householders may turn to their current wealth, if available. This wealth may also include sweat equity. Current wealth exceeding that required to top up the mental accounts to meet the minimum MLS can be used to raise the ability for AL. This mental accounting process may differ across the four households shown in Figure 1.

Households with wealth-reliant material living standards: In households with low regular income flow but high wealth stocks, members rely mainly on mental accounts of wealth to maintain the consumption required for acceptable minimum material living standards. Such households are likely run by retirees and pensioners without regular employment. There may also be young people who have inherited their parents' assets who may choose to use these, rather than paid employment, to fund their consumption needs, but this is likely to be the case for a minority of households because of the way inheritances are typically mentally accounted for. Any income that flows into these households becomes quickly absorbed in meeting household needs leaving no surplus for investment. They then turn to wealth stocks. With little regular income to replace withdrawals from wealth stocks, householders are likely to be concerned about depleting wealth stocks. Under these circumstances, these households reliant on wealth accounts are loss averse (e.g., Gachter et al., 2022). Householders thus ensure that funds from their pension and retirement funds are used to top up mental accounts to meet their minimum MLS before determining if a surplus can be risked towards investment into a new venture.

If these households insist on maintaining a high MLS, then a modest wealth surplus remains for investment. But wealth also includes the human capital deployed as sweat equity (Stiglitz et al., 2009). With members not employed in generating income, their wealth comprising of their skills and time can substitute for any monetary investment (Hulsink and Koek, 2014; Jones and Li, 2017). For example, entrepreneurs and family members may invest their own time and labor in place of the money required to purchase labour and services from external parties (Alsos et al., 2014; Bhandari and McGrattan, 2021; Carter et al., 2004; Martina, 2020; Stewart, 2003). This is frequently seen in a small services business where householders deploy their capital stocks to own and operate, e.g., a laundromat, while strenuously avoiding financial commitments to purchase capital equipment. Thus, I propose the following:

In entrepreneurial households with wealth-reliant MLS, householders will use mental accounts of time (versus money) and any wealth exceeding that used for acceptable minimum MLS in their assessment of AL; higher assessments of these items will increase the likelihood of a plunge decision.

Households with wealth and income-reliant material living standards: Both high wealth and high income maintain a high reference level of minimum MLS. Despite their high-income flows and stocks of wealth, we can expect members to be sensitive to losing this relatively higher minimum MLS (Boyce et al., 2013; Gachter et al., 2022). Mental accounting can thus feature prominently in these households to control downside risk. These households first draw on income to meet their acceptable minimum MLS. If this reference level is not reached, then wealth is also used. However, in the main, because these households have high income levels, we can expect acceptable minimum MLS to be met with income alone, leaving wealth accounts for risky investments. Thus, I propose the following:

In entrepreneurial households with wealth and income-reliant MLS, their assessment of AL will be driven mainly by wealth accounts; higher assessment of this item will increase the likelihood of a plunge decision.

Income-reliant household: In these households, no wealth is available to either top up mental accounts of consumption to maintain MLS or invest in a new venture. This household may feature young, employed people who have yet to own homes. An acceptable minimum MLS can be compromised if the income used for consumption is channeled to the new venture. Losses are affordable when they are sourced from income accounts that are in excess after accounting for consumption.

Spouses, for example, may use wage earnings to cover the entrepreneur's responsibility for household consumption—utility bills, for instance (Guo and Werner, 2016). Spouses and parents may also subsidize the entrepreneur's consumption: spousal employment benefits might fund an entrepreneur's health insurance (Wellington, 2006). To this extent, observe that goods and services owned by the firm may also be made available for personal and household consumption, which can lead to households maintaining MLS above the acceptable minimum (Carter et al., 2017). For example, householders may use the company car or printer. Thus, I propose the following:

In entrepreneurial households with income-reliant MLS, the assessment of AL will be driven by mental accounting of income above that required to maintain an acceptable minimum MLS; a higher assessment of this item will increase the likelihood of a plunge decision.

The poor household. In monetary terms, poor households possess neither adequate income nor wealth. Under these circumstances, the entrepreneurial endeavor may arise out of necessity—from a lack of employment alternatives—instead of a perceived profitable opportunity (Dencker et al., 2021). A lack of employment alternatives means they have time to be deployed toward sweat equity. Notwithstanding those circumstances, low-income households may maintain consumption and resultant minimum living standards through government benefits (Barrett et al., 2000) and social resources, such as strong kinship networks that strengthen access to resources (e.g., Khayesi et al., 2014). This combination of time and social resources contributes to the household's level of AL, with higher levels making it more likely an entrepreneur in the household takes the plunge. I propose:

Households with hardly any income and wealth mainly use accounts of time (versus money) in their assessment of AL; higher assessments of this item will increase the likelihood of taking the plunge.

Discussion

This article has sought to use the EWB perspective to draw insights about how entrepreneurs use mental accounting to assess their ability for AL in decisions about taking the plunge into entrepreneurship. The article is motivated by an intuition that the entrepreneur cannot be looked at in isolation when deciding to start an enterprise. However, scholars have viewed entrepreneurial decisions utilizing the concept of AL from an individual perspective. But in reality, when AL informs a plunge decision, entrepreneurs have some motivation beyond just themselves to minimize any loss. Entrepreneurs will be concerned about meeting the basic needs of not only themselves but also their loved ones. They are unlikely to consider risky investments if this collective economic well-being is threatened.

The article views four household contexts: high wealth, low income; low wealth, high income; high wealth and income; and low wealth and income. In entrepreneurial households with wealth-reliant MLS, the small income is quickly absorbed in meeting MLS with wealth to top this up. Householders will use accounts of time (versus money) and any wealth exceeding that used for acceptable minimum MLS in their assessment of AL. In entrepreneurial households with wealth and income-reliant MLS, income may be sufficient to meet MLS, leaving wealth for investments. Thus, the assessment of AL will be driven by wealth accounts. In entrepreneurial households with income-reliant MLS, the assessment of AL will be driven by income accounts that exceed the acceptable minimum MLS. Households with hardly any income and wealth may mainly use mental accounts of time (versus money) when they assess AL.

Contribution

The article endeavors to make four contributions to the extant literature. First, the article introduces the entrepreneurial household as an important setting for assessments of AL. This responds to calls by prominent entrepreneurship scholars to seek explanations of entrepreneurial decisions that go beyond the individual (Reuber et al., 2016; Welter, 2011; Zahra, 2007). Prior research has likewise argued for the shift in the unit of analysis from the entrepreneurial individual to the entrepreneurial household (Aldrich and Cliff, 2003; Alsos et al., 2014; Carter, 2011). This paper brings to the fore the importance of the household unit of analysis in effectual thinking and for an understanding of the AL heuristic (Sarasvathy, 2001). The household reveals not only the entrepreneur's broad access to resources possessed by extended family members and other business networks that have some association with household members but also shows that concerns about risks posed to MLS extend beyond the individual entrepreneur absorbed in the plunge decision.

Mental accounting research has yet to interrogate internal household interactions beyond individuals (Zhang and Sussman, 2018). Notably, this enables scholars to introduce the much-forgotten collective into entrepreneurship theorizing regarding AL and mental accounting. By locating the entrepreneurial decision within the entrepreneur's household, this article moves the conversation about the entrepreneurship phenomenon from the heroic individual to the more realistic collective. Around the world, the most accessible collective is usually found in the household. Indeed, entrepreneurship scholars have been calling for many years for the role of the entrepreneur's context to take its place in the entrepreneurial phenomenon (Romanelli, 1991; Welter, 2011; Welter and Baker, 2021). Even in strongly individualistic cultural settings, it may be worth locating the individual within a household context to understand better the resource availability of new ventures and the impact of the household on AL assessments (Alsos et al., 2014; Brush and Manolova, 2004).

Because the household unit can represent an overlapping social system where extended family members and other business networks come together (Tagiuri and Davis, 1996), the EWB construct can also incorporate the idea of an effectual network (Kerr and Coviello, 2019; Sarasvathy and Dew, 2005). Based on the household as a social system, EWB has the potential also to incorporate several other strands of research: family and social structure (Aldrich and Cliff, 2003), pre-existing social relations (George et al., 2016; Kerr and Coviello, 2020; Kotha and George, 2012), shared identity networks (Khayesi et al., 2014) and collective effectuation (Murphy et al., 2020; Strauß et al., 2021).

Second, the article introduces the tension between investment and consumption in applying the AL heuristic to entrepreneurial decisions. Current income directed towards investment delays consumption. I suggest that this tension is resolved by setting an acceptable minimum MLS dictating those aspects of consumption that cannot be delayed. Money available for investment is drawn from accounts that contain surpluses after meeting the consumption required to meet the acceptable minimum MLS. This perspective also enables scholars to recognize the conditions that allow entrepreneurial survival despite the often-negligible business income in the early years of new venture creation.

The article's third contribution introduces a hedonic reference outcome in acceptable minimum MLS. This helps us extend the entrepreneurial household's mental accounting process beyond categorizing to incorporating evaluation, directly influencing the AL heuristic and subsequent entrepreneurial decisions. Typically, consumption derives from current income flows (Kőszegi and Matějka, 2020). Investment into an asset, such as a new business, is not considered consumption but direct use of existing wealth, incurring debt, or as intermediate costs that are subtracted when deriving net business income as a part of household income (OECD, 2013). Indeed, a household planning to start a new venture may be willing to incur intermediate costs, like dropping its MLS to an acceptable minimum, to meet the venture's long-term income expectations. Though wealthy households appear better equipped for entrepreneurial investment, especially for the upfront investment required to start a new venture, this article shows how other households might decide around their acceptable minimum MLS to take the plunge decision. For example, in households with low-income flows, assuming members have access to time, sweat equity becomes pertinent.

The article's fourth contribution introduces diverse entrepreneurial household circumstances, with varying command over their income flows, wealth stocks, and acceptable minimum MLS. These variations are highlighted in Table 1. This has practical implications. For example, policymakers might do well to recognize the household as a unit of analysis when developing solutions to promote and support entrepreneurship. A household view allows policymakers to view the multiple sources of income and wealth to subsidize the new venture. It also cautions policymakers to weigh this resource availability against the household's capacity for risk-taking from fear of losing current EWB.

Furthermore, recognizing that an entire household risks certain resources may reflect entrepreneurial commitment more accurately to policymakers. Entrepreneurs will likely face pressure to work hard to make a new venture successful in return for household support. This might mean avoiding management decisions that jeopardize business earnings to maintain household living standards or reciprocating support from household members.

Practical implications

This article's framework shows that entrepreneurial households use the acceptable minimum MLS as a reference point to guide their decision-making process. After meeting this reference point, households will assess the surpluses available for any risky investment in a new venture. These surpluses make up a household's ability for AL, which significantly affects taking the plunge.

When households are considering starting a new business, they must first evaluate their financial situation. This includes mental accounting of their current income and wealth sources and any potential future earnings or investments. They must also consider their expenses, including their regular living expenses, debt payments, and any other financial obligations they may have. Once households clearly understand their financial situation, they can assess how much money they can afford to lose. This amount can be made available to invest in a new business. Put another way, if their current income and wealth sources exceed their acceptable minimum MLS, they may have surplus funds that increase their ability for AL and investment into a new venture. However, suppose their income and wealth sources are enough to meet their minimum acceptable MLS. In that case, they may need to prioritise maintaining their living standards over investing in a new business.

Notably, income is the primary determinant of the consumption that underlies households to meet their acceptable minimum MLS. People tend to spend what they earn. Therefore, entrepreneurs who rely on their income to support their MLS may face difficulty investing in a new business. The fear of insufficient money to meet their basic needs may dissuade them from investing in a new venture. They may prefer to maintain their current lifestyle, which can limit their investment options. For example, a household may need a certain amount of income to pay for rent, food, and other necessities. If investing in a new business would jeopardize their ability to maintain this minimum standard of living, they may choose not to invest.

On the other hand, entrepreneurs who have access to wealth sources may have a more flexible approach to investing. Wealth can help smooth consumption during unexpected changes in income. For example, if an entrepreneur experiences a temporary reduction in income, they can rely on their wealth to maintain their current standard of living. Wealth can also come to the rescue when income becomes volatile. Entrepreneurs with wealth may have a higher risk tolerance, as they have a financial cushion to fall back on if the venture fails. Often, wealth increases the ability for AL and the likelihood of the plunge decision.

All in all, households must weigh the benefits and risks of using income versus wealth to invest in their businesses. When households use a reference point such as the acceptable minimum MLS to guide their decision-making process, they may be more likely to use their income to support the investment if this standard is met. In contrast, they may rely on their wealth to invest in a new venture if this reference point is not reached. Notably, this article has suggested that we overlook time or sweat equity as a source of wealth. If we recognize this, we can see poor households also having the means to construct AL and plunge into new ventures.

Limitations and further research

This article presents several opportunities for further research. First, an economic perspective suggests that little resources may be left over for business endeavors because households may maximize their consumption to fulfill all their material needs. However, not all households with a strong command over resources may have needs requiring high consumption levels. For example, households may consume modestly, directing their income towards longer-term wealth accumulation or sharing their resources with extended family and the broader community. This ability to delay consumption or live modestly despite command over resources increases entrepreneurs' ability to source from their households the financial resources required for business endeavors. Further research is needed about the consumption behaviour and acceptable minimum MLS of entrepreneurial households and how these may affect their decision-making.

Next, scholars rarely consider entrepreneurs' home equity a valuable resource. While it may be the most significant component--settling the home bond--of many households” expenditures, it is also an essential asset against which entrepreneurs can raise finance. On the other hand, poor housing conditions can affect people's mental and physical health, family functioning, and basic social activities. Consequently, they cannot exploit the entrepreneurial opportunities available in their surroundings. The influence of housing conditions on entrepreneurs' decision-making is a significant opportunity for further research.

This article has viewed the entrepreneurial household's command over resources in current income/consumption flows and wealth stocks. Osberg and Sharpe's (2005) original conception also included income distribution and economic security. Further research can introduce the impact of household income distribution on entrepreneurial decisions. For example, elderly householders and children may earn little income and depend on entrepreneurs. Further research can also introduce the dimension of economic security. For example, some household members may face unemployment. This article has suggested that a household's low income and wealth may result from unemployment forcing entrepreneurial decisions around survivalist necessity-type ventures. On the other hand, this context requires a broader view of resources: strong kinship and time (instead of money) may also serve as vital resources for entrepreneurs (e.g., Khayesi et al., 2014).

Entrepreneurs who create opportunities may approach their ventures by investing incremental ALs at certain times and deciding whether to contribute additional resources or exit (Jiang and Rüling, 2019). Scholars need to test whether the present value of future losses may form part of the entrepreneurial household's mental accounting and AL. Smolka et al. (2018) have shown that, as time passes and more information about an opportunity becomes known, entrepreneurs combine the prediction of gains with the control of losses. Because the plunge decision is made upfront, scholars should test whether a crude present value calculation of future potential losses forms part of an entrepreneur's AL.

Importantly, EWB is centered on the entrepreneurial household, including the entrepreneur's immediate and extended family members. The entrepreneur's household features prominently in developing economies, where it can be a site of production and consumption (Gras and Nason, 2015). In advanced economies, as entrepreneurs increasingly exploit service and digital-type opportunities, they increasingly make their homes the site of their operations (Mason et al., 2011). Therefore, scholars will need to examine the implications of entrepreneurial household in advanced and developing economies.

Conclusion

EWB and acceptable minimum MLS affect how entrepreneurial households mentally account for any losses when assessing their levels of AL in the context of taking the plunge with a new venture. I argue that entrepreneurs' mental accounting of whether household resources can meet the minimum MLS is central to the ability to raise AL and make the decision to invest in a new venture. Households use the acceptable minimum material living standard, often equivalent to meeting their basic needs, as a reference point to guide their decision-making process. Only after meeting this reference point can households assess any surpluses available for AL and risky investments in a new venture.

Viewing entrepreneurs within the context of their households with the risks posed to the well-being of their loved ones helps scholars understand why the decision-making process for taking the plunge is unlikely to be entirely rational. Mental accounts of income and wealth and their evaluation of pain experienced by households when compromising acceptable minimum MLS may help scholars better understand why decisions about taking the plunge may deviate substantially from models that assume optimizing behavior. Scholarship can benefit from viewing the entrepreneur in the context of their household rather than in isolation. Entrepreneurs' outcomes are deeply connected to the EWB of their household members, particularly family members.

This article has highlighted ways entrepreneurs' resource access may be limited by the competing demands of their household members to deploy available resources towards desired EWB. Accounting for the income, wealth, and consumption of the many individuals connected to a household may also help scholars understand how the entrepreneur can survive the uncertain and irregular business during the early years of business creation. For the same reason, the entrepreneur may be under immense pressure to limit their “experiment” to a specific period beyond which the household may return to its desired living standard.

The author wishes to thank Nick Dew for his friendly reviews during the drafting of this article.