Purpose

The challenge of accessibility to adequate housing in several countries by a large percentage of citizens has given rise to different housing programs designed to facilitate access to affordable housing. In South Africa, the National Housing Finance Corporation (NHFC) was created to provides housing loans to low- and middle-income earners. Thus, the purpose of this study was to evaluate the implication of the macroeconomic risk elements on the performance of the NHFC incremental housing finance.

Design/methodology/approach

This study used a mixed-method approach to examine the time-series data of the NHFC over 17 years (2003–2020), relative to selected macroeconomic indicators. Additionally, this study analysed primary data from a 2022 survey of NHFC Executives.

Findings

This study found that incremental housing finance addresses a housing affordability gap, caters to disadvantaged groups, adapts to changing macroeconomic conditions and can mitigate default risk. It also finds that the performance of the NHFC’s incremental housing finance is premised on the behaviour of the macroeconomic elements that drive its strategy in South Africa.

Originality/value

Unlike previous works on housing finance, this case study of the NHFC considers the implication of macroeconomic trends when disbursing incremental housing finance to low- and middle-level income earners as a risk mitigation measure for the South African market. Its mixed method use of quantitative and qualitative data also allows a robust insight into trends that drive investment in incremental housing finance in South Africa.

Introduction

The overall perception of housing as a lifelong process and the capital-intensive nature, incremental housing, also known as self-help housing, has historically proven to be the preferred housing option across developing countries (Amoako and Frimpong Boamah, 2017). According to Ntema (2011), this mode of home ownership, which is often attributed to JFC Turner’s work, has always existed as “conventional wisdom” and predates many others such as mortgages, social housing and public–private partnerships. The author goes on to say that JFC Turner’s advocacy for self-help housing only added to a system that already existed in Africa and other developing countries outside of Africa. Owning a home, by building incrementally, offers an opportunity to save cost on recurring rental expenses and could even turn into an income or capital generation option for those who seek income or capital returns. However, despite these desires coupled with the capital-intensive nature, home ownership is only easily financed by a few who want it. This is particularly so for many Africans whose access to formal housing financing is almost impossible.

In South Africa, National Credit Regulator (2014) reports that it has recorded a significant fall in new mortgages from more than 100,000 per quarter (in the fourth quarter of 2007) to approximately 33,000 per quarter by the second quarter of 2009. Furthermore, Business Tech (2021) reports that 40,000 mortgages are provided quarterly on average. These numbers declined to 12,000 in the second quarter of 2020 during the pandemic but recovered to 53,000 in the second quarter. When compared with South Africa’s approximately 3.7 million housing gaps, which is estimated to be growing at 178,000 annually, mortgage finance is not performing well in the pursuit of housing affordability as is the case in other countries across Africa. The considerable impact of a state-owned institution in South Africa is the first of its kind for incremental housing finance.

The herculean task of achieving home ownership through formal financing options makes several households use their savings and an incremental building process to own a home. Therefore, housing financing is usually informal in most developing regions of Africa. Accordingly, this informal financing system accounts for more than 90% of housing acquisitions through incremental self-help housing (Donkor-Hyiaman, 2016). According to Gilbert (2000), incremental self-help housing is predominant in developing countries because of the poor economic status of households and the fact that formal lenders are hesitant to lend funds to low-income families. However, considering how prevalent this mode of homeownership is, this study sought to investigate the National Housing Finance Corporation (NHFC) as a proof of concept to justify investment and the widespread adoption of incremental housing finance.

Some studies have argued that profits could be made if some of the practices and procedures of formal institutions were aligned to incorporate incremental self-help housing (Also see, Teye et al., 2013; Donkor-Hyiaman, 2016; Iyandemye and Barayandema, 2018). In 1996, the South African Department of Housing established a development finance institution known as the NHFC. Its role was, among other things, to identify and design innovative approaches for mobilising finance from the private sector and other development finance institutions where the public sector cannot intervene. This home financing model is the incremental housing finance designed to support the low- and middle-income earners. This financing arrangement is believed to de-risk the sector because the amount and the repayment plan are designed to reflect the income power of the concerned groups which is worth investigating.

In the past, studies on incremental housing development and finance, like Habitat for Humanity (2014), have recognised the difficulty that economic instability poses to private sector investors, financiers and lenders. Similarly, previous studies have identified the GDP, employment, household income, interest rate and inflation rate as significant macroeconomic considerations for incremental housing financing (South African Housing and Infrastructure Fund, 2020; Marais and Cloete, 2015; Amoako and Frimpong Boamah, 2017; Van Noorloos et al., 2020; Habitat for Humanity, 2014). However, these studies have yet to work extensively on incremental housing finance solutions within Africa. Therefore, this study looks at the macroeconomic factors affecting incremental housing finance investors and decision makers within the NHFC as a case study for understanding opportunities for growth. This is necessary because it reveals the potential risk factors critical to the growth or otherwise of incremental housing finance in South Africa. This is also necessary because it would provide ways by which, if inimical, these could be avoided so that the essence of its development could not be jeopardised, thereby creating inclusion for a large segment of the population without a place called home.

The study, however, found the need to pay particular attention to macroeconomic risk factors within the context of the NHFC, which is concerned with piloting incremental financing as an impact investor in South Africa. Understanding macroeconomic trends’ role in risk mitigation within the NHFC will provide a basis for scaling incremental housing finance and private sector investments across other African countries. The following section concentrates on the literature review. After that is third section, which dwelt on the research methodology. Fourth section is an analysis and discussion of the results. Finally, fifth section is recommendations and concluding remarks.

Literature review

Though profit is the primary investment goal, buyers and renters seek housing financing that is within their purchasing power. As a result, the need for housing financiers to be profitable places a strain on a specific population segment. Thus, Ferguson and Smets (2010) observed that homeownership finance for low- and middle-income populations appears to be hampered and out of reach in most emerging markets. Solutions to Africa’s growing demand for affordable housing continue to be scarce, ranging from mortgage financing to outright government provision or subsidies. Consequently, slums house approximately one billion people, or one-third of the world’s urban population (UN-Habitat, 2005), with Africa hosting a large number.

For a lot of households, buying a home requires huge capital and mortgage lending is one of the options for financing this need. However, in several developed and developing economies, inadequate access to mortgage finance and issues of affordability continue to motivate a need to research other instruments for financing housing (Melzer and Hayworth, 2018). With the predicted growth in urban population across developed and developing economies, housing needs are bound to become more urgent and sophisticated. According to the report of the World Bank Group (2015), Africa is urbanising faster than income is growing and consequently effective demand for housing is low. Furthermore, financial institutions providing mortgage financing apply strict loan criteria, offer high and variable interest rates and require short repayment periods. This approach makes mortgage housing finance unattainable for a lot of Africans (Nyasulu, and Cloete, 2007).

In Rwanda, major commercial banks in the mortgage market provide costly middle- and short-term home loans, conditioned loan to value (LTV) ratio and conditioned payment-to-income ratio which creates limited housing affordability (Iyandemye and Barayandema, 2018; Fuchs, 2018). What this implies is that only high-income households with collateral assets, and who are capable of shorter repayment periods often qualify for mortgage finance. This is similarly the case as reported in studies undertaken in Ghana, South Africa, Zimbabwe, Namibia, Nigeria, Uganda and Tanzania (see The World Bank, 2011; Quansah and Debrah, 2015). This is because most low-income earners struggle to repay mortgage loans, especially the amount needed for housing. Consequently, the objective of affordable housing provision for low-income earners is inhibited in most developing countries.

To stem the expansion of informal settlement and slums, governments must explore a variety of financing solutions for housing modification, development and incremental housing across Africa. Many studies on the subject matter have attempted re-inventing or modifying mortgage finance and adapting it for the African market (Nyasulu and Cloete, 2007; Melzer and Hayworth, 2018; Akenga et al., 2015; Nyanyuki and Omar, 2016). However, other studies have highlighted the need to bridge the gap between profitability for housing investors and affordable housing finance innovation (Standish et al., 2005; Gaspar, 2017; Sharam et al., 2018). These authors report a link between growing demand for affordable/incremental housing and an over-reliance on government funding, as well as the proliferation of formal mortgage finance systems that are often inaccessible to low- and middle-income groups. Some studies like Burgess (1978), Watson and McCarthy (1998) and Muller and Mitlin (2007) have argued that the solution to affordable housing finance lies in increased government spending. However, while failing to consider the macroeconomic context, such strategies have also inadvertently put pressure on public funds for other infrastructural projects (Gardner et al., 2019).

Other researchers have suggested that access to increased private financing would be instrumental to improving incremental housing finance in emerging markets like South Africa (Mehlomakulu and Marais, 1999; Pugh, 2001; Groves, 2004; Marais et al., 2008). To provide access to high-quality housing in emerging economies, there must be a supply of affordable housing finance for the low- and middle-income sector. To private investors, however, low- and middle-income homeowners are frequently seen as high-risk and unappealing. Furthermore, Akenga et al. (2015) were able to classify macroeconomic risk as a significant factor that impedes mortgage performance. However, Klug et al. (2013) posit that the affordable risk housing represents for investors in the South African market is often mitigated by partnerships with the government. Therefore, the enabling role of government is essential for private investors to embrace incremental housing financing as most African households rely on incremental housing development, which does not conform to the formal mortgage finance model (Groves, 2004).

In Ghana, Prime-Stat PVC Ltd. (2018) opines that macroeconomic shocks can influence mortgage lending growth. Their report also affirms that, among other risk factors, the mortgage-to-GDP ratio, high-interest rates, foreign exchange instability and inflation significantly impact long-term lending. They described these factors as relating to the country-specific characteristics that may limit the lending capacity of institutions. This makes it difficult to attract private investment into the housing finance sector for alternatives like incremental housing finance. Out of the 40% of FDI financing flowing into sub-Saharan Africa (SSA) for real estate, Prime-Stat PVC Ltd. (2018) also notes that most development finance institutions (DFIs) focus on mortgage financing, which is historically out of reach for the majority. However, their report could have been more active on macroeconomic indicators’ role in the growth or lack of financing for incremental housing. This is the case for several similar studies (Gasparėnienė et al., 2016; Nyanyuki and Omar, 2016; Fuchs, 2018).

Fuchs (2018) also explored the impact of macroeconomic management practices on housing finance costs. They opine that high policy interest, which is rife in most African countries, needs more confidence in the macroeconomy. This study explores little about macroeconomic impacts on lending for incremental informal housing. This leaves too much room for speculation about the larger informal housing finance markets in developing economies.

Akinwunmi (2009) notes that many countries in East Asia and Pacific, South Asia, Europe and Central Asia, Latin America and the Caribbean, Middle East and North Africa and SSA have explored other innovative financial products because of their struggle with macroeconomic constraints to formal housing finance. Furthermore, a most significant input to this risk that the macroeconomy poses to lenders can be found in Habitat for Humanity’s (2014) report. Their study recommends risk mitigation approaches for informal housing finance, including asset–liability matching, fixed rates, individual loans, education and prioritising women. It also demonstrates the same appreciation for the impact of macroeconomic factors on lending growth and innovation.

These assertions still need to be tested in many African countries, necessitating research into institutions that may have adopted a similar paradigm when approaching informal housing finance. Therefore, this literature review demonstrates the need for more information on housing policy evolution to accommodate the incremental housing needs of low- to middle-income groups in developing African economies. Similarly, it becomes imperative to investigate the challenges posed by macroeconomic drivers on private investment in incremental housing as a part of policymaking. This study also explores the risk mitigation measures that encourage innovation in housing finance and influence the role of public and private sector stakeholders. This study also considers the peculiarities of local economies like South Africa and the macroeconomy’s insight concerning affordable housing finance products.

Data and methodology

According to Holden and Lynch (2006), the subjectivist approaches phenomenon from a detailed view of an individual perspective. This informs the use of mixed methods appropriate to examine reality from the perspective of housing finance in Africa as a different construct from that of other developed nations. Affordable housing finance and incremental housing methods are novel in the fields of research. This makes it highly difficult to rely on a positivist research approach that upholds quantitative data above all else. The need to explore multiple sources of information is predicated by the fact that financial innovations are still evolving phenomena in Africa and are not widely adopted yet. Morgan (2007) supports the use of a “pragmatic approach” to serve as justification and guidance for social science research methods. Pragmatism offers a suitable basis for a mixed method that uses both qualitative and quantitative methods. According to Shaw (2010), critiques of this method are often concerned with lack of rigour in justifying the mixed method, an inability to demonstrate an understanding of the philosophical implications, lack of quality criteria and lacking skills to use both the quantitative and qualitative methods. However, Shaw (2010) goes further to justify the suitability of this method for social science research as it brings together a realist and constructivist approach for both the physical and social worlds, respectively. This study believes that the pragmatist mixed method approach brings together elements of quantitative and qualitative research under a single approach. Furthermore, pragmatism advocates rigour through a consistent and coherent use of mixed methods based on the researcher’s worldview.

Study population, variables and data collection

The NHFC, having integrated with the Rural Home Loan Fund (RHLF), is the national institution responsible for the creation of informal housing finance products. This makes the NHFC the focus institution and thus the study population for the primary and secondary data collection regarding incremental housing finance. The NHFC’s end user is defined as any South African household with a monthly income of R1,500–R15,000 (low- to middle-income household also known as the gap market). The unique position of the NHFC, as it bridges private and public interests, makes it the ideal case study for this research. A mixed method analysis is done in two stages to demonstrate the implications of macroeconomic trends on incremental housing finance.

First, a quantitative analysis compares time series data of NHFC Annual Incremental Housing Loans with time series data of three macroeconomic variables including:

interest rate;

inflation; and

unemployment.

These three macroeconomic indicators were identified from previous literature like Quansah and Debrah (2015), Poon and Garratt (2012); Teye et al. (2013), Akenga et al. (2015); Prime-Stat PVC Ltd. (2018); and Donkor-Hyiaman (2018). These variables also frequently occur in archival reports of the NHFC which confirms their relevance for decision makers. The secondary macroeconomic data were collected from the World Bank Data Portal and Stat SA website. The study used descriptive time series to illustrate the trends in secondary data collected by examining the NHFC’s report over 17 years between 2003 and 2020 to measure the implications of macroeconomic trends for the institution’s incremental housing finance interventions.

Second, primary data was collected through an electronic survey of nine NHFC Executives (NE) who were identified as core decision-makers on the financing products. According to Becker et al. (2023), case studies can use one participant or a small group of participants. Therefore, the total of nine executives supports the case study approach for understanding the organisational phenomenon in a real-life context. Five out of the nine executives responded to the survey. This was followed up by semi-structured personal interviews.

The qualitative analysis of NHFC annual reports served to validate the findings from the descriptive analysis of the survey responses. Using Atlas Ti, the reports were organised chronologically, and critical themes regarding low-income housing finance emerged. Again, based on the research objective, key search terms, including incremental housing, affordable housing challenges, macro economy, low-income housing, housing finance and performance challenges, guided the analysis. Atlas Ti is primarily used for qualitative data analysis and reporting. The annual reports were coded according to select concepts related to the comprehensive case study of incremental housing finance for low- and middle-income earners in South Africa.

This study, in line with similar research works (see, e.g. Akinwunmi, 2009; Akenga et al., 2015; and Iyandemye and Barayandema, 2018), builds a case study using the primary and secondary analysis of the NHFC as a means to explain the relationship between the macroeconomy and incremental housing finance investments.

Results and analysis

In this section, the time series data on major incremental housing indicators were used to give insight into its development. Although formal housing finance may not be accessible to many South Africans, it is essential to consider how significant efforts to enable accessibility to incremental housing finance had made to improve the situation. Accordingly, the NHFC’s report in Table 1 summarises the information.

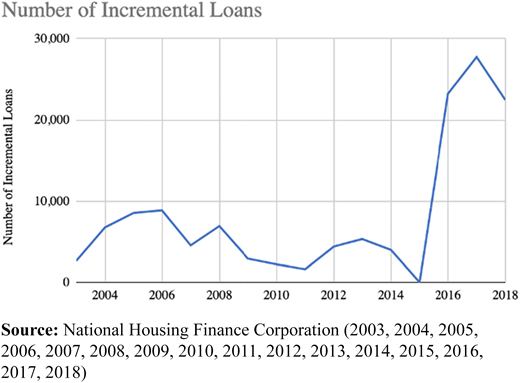

Table 1 shows the NHFC’s report between 2003 and 2020. The report reveals that incremental housing finance is a major contributor of funds to the investment portfolio of the NHFC. There is evidence of growth in the number and value of incremental loans provided. The number of incremental housing loans rose from 2,636 in 2003 to 32,687 in 2020 and from R615m to R724m in value. This sets a tone for how incremental housing finance investment is perceived in terms of profitability. Instead of viewing incremental housing finance purely as a risky venture, there is evidence of high returns for this mode of financing.

The NHFC has also reported more consistent participation by banks. This could be attributed to the steady growth in the institution’s lending capacity for low-income housing and the confidence the NHFC’s impact investing efforts have introduced to the sector. Furthermore, the impact of the macroeconomy on incremental housing finance is evidenced by NHFC’s records of higher disbursement per recipient, but fewer incremental loans like the institution experienced in 2006. This suggests that the housing market could have experienced a significant rise in prices, including construction costs. Gardner et al. (2019) similarly explained this phenomenon as the result of the impact of inflation on the delivery rate and quality of subsidised housing across South Africa. Although not many people could access incremental loans in 2007, those who did, required a lot more financing to build incrementally.

While this suggests that harsh economic conditions impede the institution’s incremental housing finance performance, the NHFC continued to exceed disbursement and housing delivery targets. Therefore, it is possible to conclude that incremental housing finance proves resilient as a valuable component of affordable housing finance investment. The institution’s reports noted that South Africa’s affordability challenges in 2012 influenced the increased shift to incremental housing. The Centre for Affordable Housing Finance in Africa (CAHF) and South African Cities Network (SACN) (2014) similarly discussed the affordability challenge and the financing gap it created in 2012, which could explain the shift to incremental financing. This suggests that incremental housing finance adequately addresses the affordability challenges experienced with formal/mortgage financing. However, as shown in Table 1, there was a noticeable growth pattern until 2015, when a significant setback impacted the unsecured lending process of the institution. The reports between 2015 and 2020 were significantly silent about the performance, growth or decline of incremental housing finance as a part of the institution’s investment in low-income affordable housing. This period of significant global economic shock due to the COVID-19 pandemic in 2020 is difficult to assess.

Incremental housing finance and macroeconomic trends

In Figure 1, from 2004 to 2014, which is 10 years, the number of incremental housing loans provided by the NHFC is at most 10,000 annually. Minor growth peaks experienced are in 2006, 2008 and 2013. Marais and Cloete (2015) explain these peaks as part of the shift in focus of lending intermediaries from mortgage to incremental housing alongside better regulation and prudent lending behaviour. They note that South African low-income markets were actively repaying loans considering the low interest rate and inflation and the government were actively attracting private sector players into housing provision even in the wake of a global crisis. However, a sharp fall in 2015 preceded a considerable leap that took the incremental loans provided to more than 20,000 annually between 2016 and 2018.

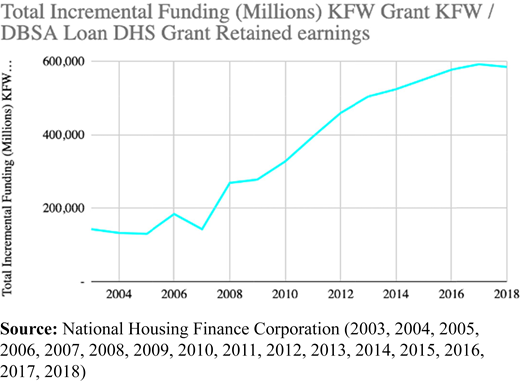

The NHFC’s report on investment received annually for incremental housing finance was obtained to demonstrate how much faith stakeholders have placed in the product as an alternative to formal financing. In Figure 2, there is a steady and consistent rise in funding received from 2004 to 2018. This suggests that the unsecured lending/incremental housing finance option continued to meet demand and proved viable for further investment commitment.

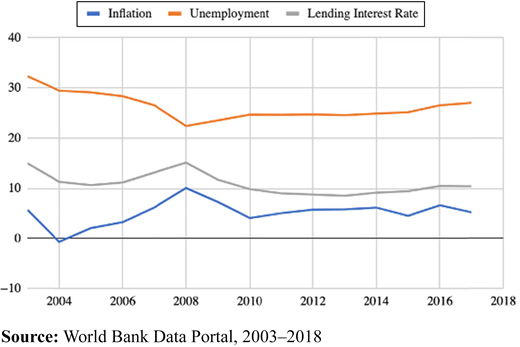

Considering the time series data demonstrated in Figures 1–3, it is possible to deduce that a stable macroeconomy is vital for incremental housing finance and investment growth in South Africa. Although this does not prove causation, the figures provide insight into how the macro economy, and incremental housing finance have performed relative to one another in the 15 years recorded. Noticeably, the interest rate reduction in the latter parts of 2004 improved affordability for many low- to moderate-income households. Consequently, the total lending and advance portfolio increased by 9% from R615m to R673m in 2004.

Macroeconomic trends affecting incremental housing finance.

This section considers data on the risk factors affecting the performance of incremental housing finance in South Africa. The NHFC is the primary entity that manages incremental housing financing in the country, among other financing options. Thus, the results stemmed from the data extracted from the annual reports of the NHFC. The performance risk faced by the NHFC is directly related to the value of incremental financing and some macroeconomic indicators.

Table 2 shows the macroeconomic trends the NHFC recorded between 2003 and 2020. There are notable changes in interest rate direction, unemployment, GDP, household disposable income and inflationary trends impacting investors in incremental finance. Increased house price was often attributed to a hike in interest rates and this explained the disparity between increasing value of disbursements compared to the number of loans disbursed. The susceptibility of the target market of the NHFC to job losses and increasing unemployment in economically volatile times was reported as a significant impact.

In 2007, the interest rate jump caused an increase in overall revenue for the NHFC. However, the organisation experienced higher impairments or defaulting from two major intermediaries, which suggests that interest rate jumps may be more favourable for incremental housing investors but would reduce its value for the target market. Furthermore, the report in 2008 stated that the continued interest rate growth, fuel hikes, rising inflation and energy problems threatened households’ ability to repay loans and the development of some planned affordable housing projects. However, the study found that incremental housing is a risk-resilient approach to increasing the affordable housing finance portfolio of the NHFC in times of economic uncertainty. Ferguson and Smets (2010) also agree that small incremental loan facilities like these can help housing microfinance institutions diversify their risk. It also addresses a major question raised by Van Noorloos et al. (2020) which borders on how microfinance institutions can collaborate with state stakeholders and banks to create lending instruments that address the risk, return and cashflow challenges of the low-income target market.

Influence of macroeconomic market risk on the growth of incremental housing finance in South Africa.

This section is focused on evaluating the implication of macroeconomic risk factors on the growth or performance of NHFC incremental housing finance in South Africa. The qualitative data extracted from surveys demonstrate key NHFC stakeholders’ perception of how the institution influences housing finance affordability and the macroeconomic environment’s role in growing incremental housing finance. The data collected is summarised in Table 3.

As seen in Table 3 in 2009, a recorded 4.5% interest rate reduction eased the borrowers’ debt burdens. In the wake of the 2008 global financial crisis and recovery efforts, including interest rate reductions, the NHFC continued to grow its incremental housing finance portfolio. This growth was because of the growing preference for unsecured lending as many more households could ‘not qualify for a formal mortgage. However, in 2010, it significantly disbursed less to incremental housing finance. The organisation’s risk management was heavily challenged by the rapidly changing global economic environment and the lagging recovery in the local economy. The 2010 report states that:

The Year under Review: The 2009/2010 financial year was difficult, particularly in the development and financing of human settlements. This is despite the successful global policy stimuli, which have edged the world economy into a recovery and rebuilding phase.

Between 2008 and 2010, the impact of the reserve bank’s interest rate reduction only slightly improved affordability for incremental homeowners. This slight impact was counteracted by the increasing unemployment, which increased the debt burden of many households in the incremental housing target market. However, from 2012 onward, the NHFC recorded a significant shift from mortgages to incremental housing finance. This shift was attributed to the preference for unsecured lending by banks in South Africa. The pursuit of economic recovery likely influenced the heightened commitment to informal/incremental housing finance. Banks, representing the private sector, are attracted to the instrument when traditional lending becomes more expensive and inaccessible for larger proportions of the population. This agrees with the findings of researchers like Mehlomakulu and Marais (1999), Pugh (2001); Groves (2004); and Marais et al. (2008) that private sector participation is critical to the growth of innovative solutions like incremental housing finance. The study also found that, in periods of high inflation trends, the cost of funding incremental housing also increases, which often reduces the growth of the instrument but does not stop disbursements. Also, the study’s finding that interest rate reductions improved the finance availability to low-income groups agrees with Ferguson and Smets (2010); and Fuchs (2018) that the higher interests rates charged against families without bank records is unsustainable and increases default risk. The reports between 2003 and 2020 demonstrate the value of incremental housing finance within the NHFC’s portfolio experienced continued growth through DFI partnerships, and disbursements to intermediaries. However, years like 2010, 2014, 2015 and 2020 experienced a fall in the value of the NHFC’s incremental housing portfolio. These were attributed to macroeconomic factors like slowing GDP growth, low disposable income, rising unemployment, rising energy cost and the COVID-19 pandemic.

NHFC perception of the relationships and impact of macroeconomic indicators on incremental housing finance and investments

To further examine the NHFC’s decisions and investment as they are impacted by macroeconomic indicators, survey responses are illustrated below. The role of macroeconomic trends in the growth of investment and the value of incremental housing in the NHFC portfolio are further explained using the results of the survey of Nes.

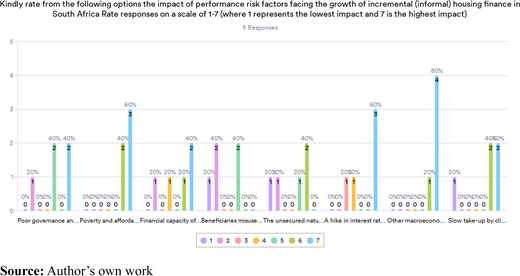

Figure 4 considers incremental housing finance performance risks independently. The survey respondents rated the macroeconomic trends to be of higher significance than any other factor influencing growth. In total, 80% of the respondents rated this risk four on a scale of 1–7. This suggests that the macroeconomic changes play a significant role in incremental housing finance provision.

According to NE1 interviewed:

Incremental housing finance is primarily accessed by low-income earners who are most susceptible to economic shocks that we are seeing currently in the market. Low economic growth and high unemployment are major challenges. Few working people have too many mouths to feed, thereby leading to the failure to meet the affordability assessment test and ability to take incremental housing loans.

This result implies that many who qualified for incremental housing loans were not favoured because of the impact of changing macroeconomic conditions on their household income. Also, it is important to note that major economic shocks might affect the ability of these low-income households to prioritise the repayment of housing loans.

Respondent NE2 stated that the NHFC found that since the start of the COVID-19 pandemic, several incremental housing finance recipients or the target market focused on consumption.

According to NE2 interviewed:

Recipients often use their creditworthiness to purchase for consumption – i.e., survival rather than to build assets. This leads to them being too indebted to then borrow for housing.

Considering how impacted incremental housing finance is by macroeconomic challenges, it becomes critical to determine whether it can improve affordability in housing provision.

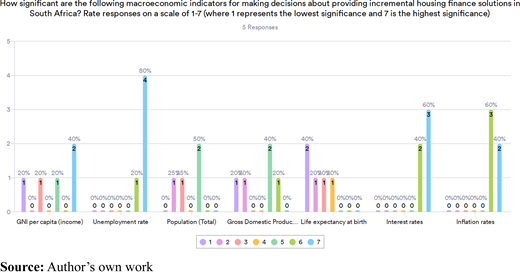

As seen in Figure 5, three top macroeconomic indicators that influence incremental housing finance, according to this survey, are unemployment, inflation and interest rates. NE1 explains their position further:

Unemployment is significant in that with high unemployment, the market is reduced for incremental housing finance, plus the fact that few members of households who still have jobs have a high dependency rate. Interest rate is also significant as it impacts the loan repayment ability. The inflation rate is significant in that as the inflation rate increases, it erodes disposable income and reduces the affordability levels for incremental housing loans–it ultimately leads to the postponement of housing improvement decisions as households opt to put food on the table rather than improving housing conditions now!

The above comment by the NE1 demonstrates the impact of unemployment, inflation and interest rates on disposable income. It ties back to the fact that macroeconomic influences severely affect low-income households by determining how much pressure is on their consumption needs compared to their need to repay housing loans. Considering that incremental loans are unsecured, these factors must be considered when making decisions about lending for incremental housing. In responding to the interview about the role of these macroeconomic indicators, another NE stated that incremental lenders prioritise the unemployment rate as a basis for deciding how aggressively to access the market.

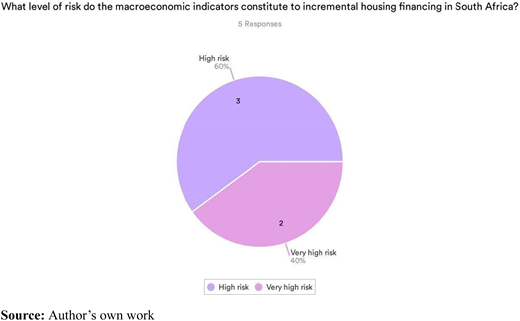

Considering how severely the macroeconomy impacts incremental housing finance, Figure 6 shows the Nes’ risk perception. Most respondents believe that macroeconomic changes constitute High Risk (60%) or Very High Risk (40%). This confirms the notion that the incremental housing finance market caters to a target market that is high risk, especially in response to economic shocks.

As shown in Table 4, NE1 holds that:

The market for incremental housing finance in South Africa is mainly low-income earners susceptible to macroeconomic shocks due to high inflation rates, unemployment rates, low economic growth, etc.

Marais and Cloete (2015) similarly agree that the incremental housing finance target market is heavily affected by macroeconomic pressures, which are further influenced by the global economy. This suggests that in developing incremental housing finance, these target markets must be considered based on the level of risk they are exposed to due to macroeconomic shifts in inflation, unemployment and other growth indicators.

It was also the consensus that people within the incremental housing finance target market tend to prioritise consumption when the economy declines, and inflation rises. According to NE3, most of the low-income groups:

They must switch their spending from houses to food and utilities to survive. Research by TPN indicates that unsecured loans are the second last on a priority list for payment in economic distress (after school fees).

This suggests that it can anticipate changes in repayment commitments based on inflation trends.

Conclusions

This study of the NHFC’s approach to incremental housing finance risk was necessitated by the challenges assailing formal or mortgage financing in most African and other developing economies. There has been a growing interest among researchers in designing risk-resilient innovative housing finance solutions that harness public and private capacity to finance housing. More importantly, the need to understudy existing models like the NHFC that will benefit from access to private financing has become critical to understanding the macroeconomic trends and risks they pose to informal/incremental housing finance. By focusing critically on the NHFC, an apex financier in one of Africa’s top economies, this study demonstrates the capacity of the state and private entities to create inclusive financing instruments collaboratively. This also demonstrates that in looking at the behaviour of incremental housing target markets, many of the theories that suggest this to be a risky market have not fully explored the reality of low-income borrowers. This study further extends the debate between neoliberalist ideals and state-controlled housing. The findings suggest that there is a nexus between the two almost opposite approaches to housing provision. The sustainability of the framework it proposes hinges on the idea that a well-functioning housing market must not rule out government intervention and vice versa.

South African low-income borrowers have historically proven that even in times of economic recession and slow recovery, incremental loan repayment remains a priority. This significantly stands out against a backdrop of findings like that of Gilbert (2000) in which they report that mortgage lending is sensitive to large macroeconomic fluctuations in exchange rates, inflation and employment. This study finds that unlike other formal financing options, incremental housing finance repayments are not much affected by economic recession and high interest which typically threaten mortgage repayments. However, the institutional executives still base their perception of their investment in the low-income market on assumptions that the macroeconomic shocks affecting some beneficiaries are significant for assessing and anticipating the market. However, the historical capacity of incremental housing finance and the low-income target market as found in the NHFC annual reports makes a strong case for private and public sector investment in this mode of financing affordable housing. It is also important to note that the result of this study shows that the negative risk perception of low-income groups and the consequent high interest charges may be the cause of increased default risk. Furthermore, the NHFC reports demonstrate the inclusive nature of incremental financing. By including women and more black homeowners, it expands homeownership to historically excluded groups as recommended by Habitat for Humanity (2014).

This makes the financing option further attractive to private sector investors during economic crises. It is also important to note that labour unrest, strikes and unemployment spikes negatively impact investment in incremental housing finance which might be a consequence of the perception that incremental housing finance for low-income groups is a riskier venture than other formal options like mortgage. However, the results of this study suggest that incremental housing finance is resilient and that low-income households prioritise repayments even in times of economic uncertainty. Another negative effect of not assessing the low-income target group appropriately is that homes built using incremental housing finance are undervalued as growth rates, cash flow predictions and business risk modelling valuation assumptions are directly impacted during times of economic uncertainty.

Despite the value of the research conducted, it was not without its limitations. Acquiring reports and especially quantitative data regarding incremental housing within NHFC proved difficult because of a lack of uniform reporting methods across years. The dichotomy between the RHLF and the NHFC before the merger also made it difficult to collect data from both entities. Beyond the achievement of this study, more research is needed to determine how well this model will perform in other less-developed African countries. Pilot studies and cases can bring more practical outcomes for deploying incremental housing finance in more countries across Africa.

To maximise the development of policy and financing instruments for housing in the low-income target groups, this study recommends as follows:

The role of the government as a housing provider should transform into that of an enabler by establishing institutional entities like the NHFC. Incremental housing finance should be implemented by such apex financing bodies funded or subsidised by the state for on-lending to retail intermediaries.

Macroeconomic data should be collected regularly and used in anticipating the performance of incremental housing finance funds. This will ensure that public and private stakeholders are making informed decisions about financing the low-income target market and how to minimise default.

Risk mitigation practices must consider the macroeconomy a significant risk when disbursing incremental housing finance.

In less developed countries, incremental financing must be prioritised as an alternative approach suited to self-help housing needs.

The authors acknowledge the support of the IREBS Foundation for African Real Estate Research and the executive staff members of the National Housing Finance Corporation (NHFC).

Funding: This research has been supported by the IREBS Foundation for African Real Estate Research and the University of Pretoria Postgraduate Bursary. The funding was provided for the completion of a doctoral thesis including data gathering, research design and reporting.

Disclosure statement: The authors state that there are no competing interests to declare.