This paper presents the design and implementation of a maturity model for assessing the cost measurement and management capabilities of organisations. Beyond capability evaluation, the model is also designed to provide guidance for improving the competitiveness of value chains across a focal company and its suppliers. Thus, it can also be used to improve inter-organisational performance.

The research, which is interventionist in nature, was developed through a collaboration between the authors and two manufacturing companies that co-funded the design and development of the model. The study follows a constructive research approach, applying established principles, instructions and known development steps to the design and implementation of a maturity model.

The paper introduces a maturity model centred on cost measurement and management capabilities by presenting its constituent parts and functioning. The model is called Cost Management Maturity Model (CMMM).

CMMM is a managerial tool that companies can use to assess the maturity of their cost measurement and management capabilities and then derive directions for improvement. It is also a tool that managers can use in the context of inter-organisational relationships to align the cost-related capabilities of a network of companies, such as a supply chain. This has the result of strengthening inter-organisational collaborations to reduce costs and improve value creation.

This paper presents an original four-level, pyramid-shaped maturity model that advances prior endeavours to this end within the realm of managerial costing. Unlike existing models, CMMM boasts a wider scope of inquiry that includes attention to cost management and inter-organisational contexts. It also provides a structured and replicable yet flexible maturity evaluation method founded on a questionnaire and an associated scoring method.

1. Introduction

Maturity models (MMs) have been widely used in range of research fields associated with management. Being concerned with organisational capabilities and their improvement, MMs are analytical instruments that display logical and gradual development paths ranging from basic to advanced levels (e.g. De Bruin et al., 2005; Wendler, 2012). As such, companies have relied on MMs to assess the state of specific capabilities of note and to derive new directions for their development to a desired or required level (Pöppelbuβ and Röglinger, 2011).

The very variety of maturity assessment models and frameworks in the context of performance measurement and management indicates that MMs are not only well-established tools (e.g. Meyer, 2008; Bititci et al., 2011; Aho, 2012; Marx et al., 2012; Jääskeläinen and Roitto, 2015; Lebedev, 2019; Lawson et al., 2019; Gregory and Riedel, 2020), they are also a useful way for businesses to tackle issues of performance measurement and management (Bititci et al., 2015). In this paper, we focus on one specific aspect of performance measurement and management that is critical to business, that being cost measurement and management.

In the context of cost measurement and management (hereafter, simply managerial costing), the evidence confirms that the cost models currently used by many companies are dated and underdeveloped (Lawson et al., 2019). As a result, the cost information used to support critical management decisions could be based on minimal cost models, which often fail to consider the complexities of contemporary business environments (Lawson et al., 2019). Consequently, there is a need for widespread improvement of the managerial costing capabilities within businesses. Such improvements are even more important in the context of a value chain where the participating companies engage in different forms of inter-organisational cost management (IOCM) to improve the competitiveness of their offerings and, as a result, their overall financial performance. Previous studies have shown that an advanced, well-developed cost measurement system is an important enabler of cost management actions at the inter-organisational level (e.g. Caglio, 2018). The more accurate a piece of cost data is, the more aligned the costing methods and practices are among interrelated companies, and the greater the expectation of more meaningful and effective the IOCM actions undertaken across those companies. Aligning the level of managerial costing capabilities between companies engaging in IOCM collaborations is therefore an essential requirement for effective cost management actions. There is also preliminary evidence to suggest that a purposely-developed MM may play a role in enabling such an alignment (Magnacca et al., 2022).

In this paper, we present an MM called the Cost Management Maturity Model (CMMM). The model was specifically designed to help organisations assess and develop their current managerial costing capabilities in the context of a focal company and its suppliers. Thus, the model is primarily designed to be used in inter-organisational settings. Specifically, the model enables the evaluation of a supplier’s capability level against the average capability level of peer companies and against the capability level that is required to effectively engage in cost management activities with the focal company.

Notably, however, just because the model was designed for use in an inter-organisational context does not mean it cannot be used for a single organisation alone. The model is still just as effective when deployed at the organisational level. There may simply be some differences in the operational modalities of the model given that references to other organisations and data may be missing at times. Such instances will be pointed out and discussed as they arise.

The model outputs gaps in the capabilities of an organisation’s managerial costings with directions to help fill these gaps based on the organisations’ specific intra- and inter-organisational needs. In doing so, CMMM ultimately aims to improve the competitiveness of both individual companies and value chains in the market.

The remainder of the paper is organised as follows. Section 2 outlines the foundations of MMs, provides a review of existing MMs in the domain of cost measurement and management, and positions the MM presented in this paper in the literature, along with its theoretical underpinnings. Section 3 presents the methodology of the study and the setting of the research. Section 4 introduces CMMM, along with its design choices and ways of functioning. It also presents the tests we undertook to verify the model and demonstrate how it works in practice. Finally, Section 5 concludes the paper and suggests directions for future research.

2. Background

2.1 Maturity models

The concept of maturity denotes an evolutionary progression from an initial state to a desired end state. Therefore, “maturity” refers to various objects of analysis, including processes, capabilities and, particularly, the sophistication of particular objects (Mettler, 2011). According to the original connotation assigned to maturity in the field of information systems and later in the field of performance management (Bititci et al., 2015), maturity – in this paper – is considered to be a metric that evaluates an organisation’s capabilities (Rosemann and de Bruin, 2005). As a useful managerial tool for assessing and suggesting improvements to specific capabilities (Pöppelbuβ and Röglinger, 2011), an MM is therefore regarded as a practical tool for assessing an organisation’s capabilities in a specific domain of interest.

The variety of available MMs is as wide as the imagination of their creators. Nevertheless, all MMs do share some fundamental elements. They can all: (1) identify capabilities of interest; (2) model a set of levels or stages describing the development state of the examined capabilities (in a simplified way); and (3) specify the criteria and instruments used to measure the maturity of the capabilities of interest (De Bruin et al., 2005; Marx et al., 2012; Wendler, 2012).

Existing MM research covers three main areas: development, implementation, and validation (Wendler, 2012). Activities in the area of MM development deal with conceptualising and establishing new MMs. Researchers working in MM implementation are interested in applying MMs to maturity assessments in specific practical contexts. Finally, MM validation concerns the corroboration of existing MMs, primarily by conducting case studies and interviews. These three areas form a stepwise research cycle that, ideally, should be completed for each newly developed MM (Wendler, 2012). Accordingly, this paper presents a novel MM that progresses through all three outlined steps, with the capability of interest being managerial costing within organisations.

2.2 Maturity in the field of managerial costing

Managerial costing is “costing done purely for the organization to use internally to ensure that information for decisions reflects the characteristics of the organization’s resources and operations” (White and Clinton, 2014, p. 5). Managerial costing supports managers in their analysis and decision-making activities and helps to optimise an enterprise’s strategic goals, such as accruing maximum benefits for the minimum cost (White and Clinton, 2014).

The literature relating to managerial costing practices and their maturity is largely a mix of monographs and related scientific publications. The monographs have mainly been published by leading associations in the field of accounting (e.g. Professional Accountants in Business Committee, 2009; Cokins, 2012; White and Clinton, 2014; Lawson et al., 2019). Of these, three stand out – one published by the International Federation of Accountants (IFAC) (the Costing Levels Continuum Maturity Framework (Cokins, 2012)), and two published by the Institute of Management Accountants (IMA) (the Conceptual Framework for Managerial Costing (White and Clinton, 2014) and a six-step methodology for developing an appropriate costing model for economic decision-making (Lawson et al., 2019)). These documents focus on the issue of accurate cost measurement, namely responding to the principle of causality, i.e. the ability to reflect the cause-and-effect relationships in an organisation’s operations.

The Costing Levels Continuum Maturity Framework by Cokins (2012) is a first attempt by a leading association in the field of accounting to introduce the concept of maturity as a possible way to sustain costing improvements in organisations. Based on the “fit for purpose” assumption (Professional Accountants in Business Committee, 2009), this framework highlights the importance of implementing costing systems that balance the accuracy of the measurement with the actual needs of the organisation, i.e. the framework strikes a cost-benefit trade-off. It provides a maturation path that companies can use to assess their current level of development in costing practices and also potentially decide what level of maturity they should be aspiring to. The first levels of the maturation path are focused on cost measurement capabilities, while the subsequent levels are concerned with using the cost information for planning purposes. Each costing level is distinguished by the extent to which the organisation understands and effectively integrates two principles. The first is the relationship between the supply and demand of resources; the second is how costs behave within consumption relationships. Given the administrative effort and, consequently, the costs required to achieve higher levels of maturity, each organisation needs to ask itself whether “the climb is worth the view” before aiming to proceed to the next level.

The Conceptual Framework for Managerial Costing is only indirectly related to maturity. It does not provide an MM. Instead, it outlines some internationally-accepted cost measurement principles and concepts for evaluating different approaches to costing. In this way, it helps organisations to determine their cost information needs, while also identifying the strengths and weaknesses of their current costing approaches (White and Clinton, 2014, p. 31). To this end, after identifying causality as the key principle of modelling a cost measurement system, the framework provides foundational concepts that can either be used to design and develop effective cause-and-effect costing models or to evaluate existing models. These foundational concepts include: (1) the constructs that comprise an organisation’s operational model, i.e. managerial objectives and resources; (2) the characteristics of these constructs, e.g. cost, homogeneity, traceability, capacity, work, etc.; (3) the relationships between the constructs in the model, i.e. responsiveness and attributability; and (4) the nature of the data needed for the model, i.e. integrated data orientation (White and Clinton, 2014). Hence, the framework includes a set of questions that helps companies to reflect on whether their currently implemented practices are appropriate or not. Compared to the two general principles that Cokins’ model is based on, the Conceptual Framework for Managerial Costing provides a much more advanced and detailed theoretical foundation for assessing and developing managerial costing practices within organisations.

Building on the Conceptual Framework for Managerial Costing, Lawson et al. (2019) provide a six-step process for organisations to follow to increase the sophistication of their current managerial costing models. Step 1 involves the organisation conducting a quick eight-question assessment of how effective its managerial costing systems are. Next, the organisation analyses its strategy and business environment. This serves to focus attention on what information the organisation needs, which, in turn, helps to determine what information the cost model should provide. The subsequent steps include: considering whether the organisation’s current models are based on causality and the foundational concepts outlined in White and Clinton (2014); evaluating the sophistication of current costing practices; choosing an appropriate level of sophistication in costing practice by comparing decision-making needs with a gap analysis; and finally, implementing the new cost model.

The contribution of Meyer (2008), who introduced the Full-cost Maturity Model, is based on approximately the same logic as Lawson et al.’s (2019) six-step process, except that it explicitly refers to the concept of maturity. This tool was conceived to support an organisation’s budget and planning processes. It is based on the premise that “traditional budgets don’t support rational financial decision making […] because they forecast the cost of expense codes, but not the cost of an organization’s products and services” (Meyer, 2008, p. 10). Hence, this model’s focus is on cost planning. It provides organisations with a go-to standard to correctly plan the full costs of their products and services. It also defines five capability levels, the idea being that each organisation should find its own ideal level. As an organisation moves up the capability scale, the benefits increase, but the mechanics of costing also become more challenging. Each level of the model builds on the previous level, so that investments made when implementing practices to support a lower level of the model are never lost. Thus, depending on need, organisations can evolve their cost planning methods and tools in stages and to different levels of detail. Moreover, according to the model, not every organisation has to reach the highest level of capability. Rather, the idea is for organisations to work through five basic steps: (1) evaluate the current situation; (2) define the target state; (3) analyse the gaps between the current state and the target state; (4) acquire and/or implement any necessary tools, methods, training or cultural changes; and (5) assess the organisation’s needs and willingness to progress to the next level. The level of sophistication and functionality of the managerial costing system is assessed by referring to cost measurement practices and not to the ability of using such measurements for cost management interventions, e.g. initiatives to reduce costs or to improve the ratio between costs incurred and the value created by the product or service offered.

Departing from the realm of monographs and documents issued by authoritative professional accounting associations and entering the realm of research papers, Lebedev (2019)’s management accounting MM is the contribution that most closely aligns with the focus of this paper. Lebedev proposes an MM for assessing the state of management accounting within organisations. The framework gives insights on what one can expect to find within an organisation in terms of management accounting knowledge and practices. However, in general, it does not go into the details of the practices, and it only assesses maturity levels according to a set of archetypes, e.g. bean-counter, historian, reporter, advisor, and so on. Since managerial costing is a specific subset of management accounting, Lebedev’s framework, may give insights on what one can expect to find within an organisation in terms of managerial costing knowledge and practices.

Further, based on a search of the main scholarly databases (see [1] for the search terms), to the best of our knowledge, Gregory and Riedel’s (2020) article in the form of a proceeding is the only work that specifically concerns costs and maturity. Notably, there are other works that are concerned with maturity in the context of performance measurement and management, but these have a broader focus beyond costing alone (e.g. Bititci et al., 2011; Marx et al., 2012; Bititci et al., 2015; Jääskeläinen and Roitto, 2015), which confirms the relevance of maturity models for business in general and performance management in particular. Gregory and Riedel’s focus is on engineer-to-order (ETO) companies, which are manufacturing companies that operate in industries characterised by “individualized products, low volumes, low standardization, high complexity, long lead times and a project based approach for order processing” (Gregory and Riedel, 2020, p. 573). Their article presents a “product cost maturity model” on the premise that cost efficiency has become more important for ETO companies in recent years. The authors point out that, historically, a key competitive advantage for ETO firms has been their ability to satisfy unique client needs and to master the associated complexity of their requests. The cost of a product and its sale price were therefore less significant for this kind of businesses. The aim of Gregory and Riedel’s model is not to improve a single product’s cost performance. Rather, its aim is to improve the efficiency of the entire company’s organisational processes, thereby gaining general firm-level cost advantages. As the authors state: “a product cost maturity model is needed especially for ETO companies, which should not be focused on a single product’s cost structure, but rather on the company’s ability for (cost) transformation and resulting cost efficient processes” (Gregory and Riedel, 2020, p. 574). Accordingly, their maturity model derives a set of success factors from the literature that provides a basis for evaluating the current state of a company and that serves as a landmark for future development. “Success factors are actions or processes that can be controlled by management to achieve an organization’s goals” (Gregory and Riedel, 2020, p. 575). Soft and hard success factors, divided respectively into three categories (leadership, employees and cost culture) and two key areas (projects and processes), constitute the foundation of this product cost maturity model. However, currently, their model is still at the conceptual development stage.

All in all, although existing contributions to the maturity of managerial costing confirm a trend, they also reveal a number of shortcomings. The path traced over the years, especially more recently, indicates that most studies are partial attempts to progress in the same direction: assessing the maturity of an organisation’s managerial costing capabilities and provide the enterprise with tools to improve their current capabilities. Although these works represent important advances, they nevertheless leave several aspects in their wake that require further consideration, analysis, and development.

First, these works propose conceptual approaches to analysing current managerial costing capabilities. For instance, White and Clinton (2014) suggest fundamental concepts that must be considered when assessing a company’s managerial costing capabilities. However, these concepts only provide a general framework which must be complemented with tools applied by skilled professionals. Therefore, the problems of conceptual refinement and operationalisation within specific local contexts remain. Second, early attempts to assess maturity (e.g. Meyer, 2008; Cokins, 2012; Lawson et al., 2019) lacked a structured method for actually measuring maturity, such as a scoring tool. Therefore, applying these contributions depends very much on the subjectivity of those using them. Third, the focus of most existing works is limited to measuring costs (Cokins, 2012; Lawson et al., 2019), the issue of managing costs is not considered. This is a serious limitation considering that a key aim of managerial costing specifically concerns optimisation, namely realising the maximum benefits for the minimum cost (White and Clinton, 2014). Additionally, the focus of existing works is too broad, as it tends to encompass management accounting as a whole (Lebedev, 2019). Consequently, it is too general to be effective at assessing and improving specific managerial costing capabilities. Finally, and related to the previous points, existing works do not explicitly consider the value chain and, more specifically, the relevance of inter-organisational relationships. Yet these relationships are becoming increasingly important for companies seeking to operate in the marketplace while remaining competitive and profitable.

2.3 Theoretical framework

From a theoretical point of view, this study embraces Malmi and Granlund (2009)’s notion of management accounting theory. According to Malmi and Granlund, instead of borrowing theories from domains other than management accounting to explain management accounting, one should recognise that there is a management accounting theory, or better still, a set of management accounting theories that not only explain how management accounting should be done or changed to ensure better organisational performance, but also why. According to this view, the theoretical underpinnings of management accounting practices can be found within the management accounting discipline itself from among its foundational theoretical concepts and principles. Accordingly, to develop the MM presented in the following sections, we built on the theory of managerial costing as a set of propositions explaining how cost measurement and cost management should be done and why (e.g. Professional Accountants in Business Committee, 2009; White and Clinton, 2014; Datar and Rajan, 2018). In addition, we also built on the concept of maturity as already applied in the field of management accounting (e.g. Cokins, 2012; Bititci et al., 2015; Lebedev, 2019). In this way, our work is consistent with the first of five stages of development in new managerial practice, as conceptualized by Ansari et al. (2007)’s knowledge progression framework. This framework maintains that the first step of development is to focus on describing the new practice, developing its conceptual framework and foundation, making a case for its use, and suggesting the likely benefits that may accrue to an organisation from adopting the practice. In later stages, when, say, studying the social and behavioural aspects resulting from following a practice, theories from outside of management accounting (as an example among many, the contingency theory) can be used to explore and explain management accounting, as also Malmi and Granlund (2009) argue.

3. The research objectives, methodology and setting

Consistent with the current trend to develop the concept of maturity in the field of managerial costing, and considering the shortcomings currently affecting the state of MM development in this field, the objective of this study is to present an MM designed to assess and develop the cost measurement and management capabilities of an organisation or network of organisations. To this end, we undertook an interventionist research project (e.g. Jönsson and Lukka, 2007; Suomala et al., 2014) following a constructive approach (Kasanen et al., 1993). Building the model followed the phases of MM design and development established in the literature (De Bruin et al., 2005; Pöppelbuβ and Röglinger, 2011).

3.1 The constructive research approach

The constructive research approach is an option when conducting interventionist management accounting research within the broad scope of the case study method (Lukka, 2003). Concretely, it is a research practice geared towards “producing innovative constructions intended to solve problems in the real world and, by that means, to make a contribution to the theory of the discipline in which it is applied” (Lukka, 2003, p. 83). Conducting a methodologically sound constructive research project means adhering to the following principles (Kasanen et al., 1993; Lukka, 1999, 2003):

- (1)

The focus of the research project should be on real-world problems that require solutions;

- (2)

The research process should be based on teamwork between the researchers and the practitioners who are facing a problem that requires a solution;

- (3)

The researchers and the practitioners involved in the research project, drawing on both practical and theoretical inputs, should engage in an iterative process of knowledge and idea exchange with the aim of learning and progressing through experience, i.e. developing initial ideas and prototypes, small-scale implementations, revisions, and tests;

- (4)

The output of the research should be an innovative artefact, e.g. a model, a system or a tool, that serves as a solution to the original problem; and

- (5)

The workable solution developed should be linked to existing theoretical knowledge.

Thus, the constructive research approach provides a way of conducting case study research that involves a strong problem-solving intervention, followed by an attempt to draw theoretical conclusions based on empirically developed solutions and existing theoretical knowledge (Lukka, 1999).

3.2 The research setting

The interventionist research reported in this paper is based on a field study that involves a major manufacturing company and one of its strategic suppliers [2]. The major manufacturing company is Nuovo Pignone Tecnologie s.r.l. – a Baker Hughes company, and the supplier is Sime s.r.l. We subsequently refer to the company Nuovo Pignone Tecnologie as Company A and to the supplier Sime as Company B. Both organisations co-funded this research project, along with the Tuscany Region and the Department of Economics and Management of the University of Pisa.

In its role as the focal company, Company A’s motivation for promoting and participating in this study was to gain access to an MM that could evaluate the managerial costing capabilities of its suppliers. Company A wanted to use the assessment results to recommend improvements to its suppliers’ costing systems when required and, eventually, to improve the effectiveness of IOCM collaborations. Company B participated in the project as a key representative of Company A’s strategic suppliers.

As authors, we played the role of interventionist researchers with the task of developing the MM expected by Company A. The MM presented in the remainder of this paper emerged from meetings, discussions and interviews with representatives of both Companies A and B that were held over a period of 19 months (from June 2021 to January 2023). More specifically, these interactions comprised 50 events (formal meetings, informal meetings, and interviews) with the project participants and the companies that participated in the pilot application of the model totalling over 55 h of face-to-face contact. This constituted the iterative process of knowledge and idea exchange between the researchers and practitioners. This is a fundamental process that is recognised in the field of the constructive research approach as learning and progressing through experiences towards solutions to the given problem. This process was complemented by numerous hours of reflection on the part of the researchers and study-related work when not in the field.

3.3 The standard phases and elements of developing a maturity model

The literature provides numerous detailed instructions on how to construct an MM. Of these, De Bruin et al.’s (2005) development framework involves six phases (see Figure 1).

This paper covers the activities undertaken as part of the first four steps: scope, design, populate and test.

The scope phase concerns two main decisions: on the focus of the model (i.e. the domain in which the model is going to be designed and used) and on the definition of the actors who will be involved in the model’s development (i.e. the development stakeholders). The focus of the model differentiates it from other existing models and also determines its specificity and extensibility. To this end, it is useful to examine the literature in the domain of reference, specifically to understand past developments and to identify issues and pose challenges. Finally, the objective and purpose of the model must be defined in this stage, e.g. Is the model intended to be descriptive? prescriptive? comparative? Or all of the above? Maturity models are commonly designed to assess a current situation, i.e. the as-is state of a certain object of investigation. This is what is known as a descriptive model. Alternatively, the goal of a prescriptive model is to derive and prioritise certain improvement measures and, thus, to prescribe a path to reach a desired state of capability or maturity. Additionally, a model might make useful comparisons between different subjects in relation to the same object of investigation – this is a comparative model (Pöppelbuβ and Röglinger, 2011).

Next comes the design phase, where the following aspects must be defined. First, the audience of the model must be determined. Who is the model intended for? What is the audience’s demand for the model? What will the audience expect when using the model? And how will the model be used by them? Second, one needs to reflect on the structure of the model, bearing in mind that a common design principle of MMs is to represent maturity through successive levels that follow some logical progression. Each level should have a concise label that provides a clear indication of its intent. The level corresponding to each label must be accompanied by a description that summarises the specific maturity stage, i.e. its major requirements and measures. The final aspect to consider during the design phase is how maturity will be represented. Common options include expressing it as an average, as an overall maturity assessment, and as separate maturity assessments for various discrete areas.

The main activity of the populate phase is to define the content of the model. The model must be filled in, which means one must decide what should be covered by the maturity assessment and how this is to be measured. The objective is to identify domain components and sub-components that are mutually exclusive and collectively exhaustive (MECE). As an aside, the MECE principle is well-known in several fields of managerial practice and is recommended as a general design principle for developing maturity models (De Bruin et al., 2005). In an established field, domain components can be identified by referring to existing knowledge. Thereafter, interviews with topic experts can be used to confirm and/or integrate the retrieved knowledge. The last step of this phase is to determine how, i.e. by what means, to measure maturity.

The last phase to be discussed in this paper is the testing phase, where the model is tested, refined if necessary and, ultimately, validated.

4. The Cost Management Maturity Model (CMMM)

This section presents the MM developed in the field as a result of our research project. Called CMMM, the model’s description begins by clarifying the object of analysis and its application domain. Next, we provide details of development stakeholders and the target audience of the model. This is followed by a discussion on the model’s purpose and an explanation of the model’s structure, its content, and its current functioning.

4.1 Scope

CMMM focuses on cost measurement and management capabilities of organisations. More specifically, it focuses on product cost measurement and management. Hence, CMMM assesses the maturity of a company in terms of its ability to measure and manage the cost of the products it offers. Companies A and B are both industrial stakeholders. They helped to develop this model in conjunction with us as researchers – a model that should fulfil the purposes identified in the literature as being typical of an MM, noting that we are specifically referring to descriptive, prescriptive, and comparative purposes.

- (1)

Descriptive purpose. CMMM assesses the current capability level (i.e. maturity) of a company’s cost measurement and management practices. When applied at the inter-organisational level, thus, in the framework of a relationship that involves a focal company and a group of its suppliers, the process and the results of the assessment allow all participating enterprises to map the current maturity of their capabilities. Additionally, the companies should be able to estimate the capability level required to effectively collaborate within an IOCM initiative. In other words, any given company should be able to detect critical capability gaps that must be filled to perform at the level demanded by the inter-organisational collaboration. Beyond measuring managerial costing capabilities maturity, CMMM also provides insights into the internal consistency of the various elements and approaches at play in cost measurement and management systems.

- (2)

Comparative purpose. The results of the evaluation allow peer comparison. Graphs and statistics can show the position of a company in relation to both the average and the top performers. This model usage function is certainly feasible when it is applied in an inter-organisational context, with the aim of concurrently evaluating different business organisations. Conversely, the comparative use of the model, unless there are public data or other information available to the company using the model, becomes void due to a lack of comparison terms.

- (3)

Prescriptive purpose. One of the main outputs of CMMM is to provide directions for future improvement in the form of priority interventions.

4.2 Design

CMMM is designed as a self-assessment instrument. The results of the model provide feedback to the users on each company’s current capabilities and, especially when used in the context of an inter-organisational relationship, on benchmarks derived from peer comparisons. In this latter case, the focal company can strategically use these results to detect capability areas amongst its suppliers that are, on average, deficient. This may prompt different forms of training to further develop the supplier’s capabilities. Forms of training that a focal company can organise include initiatives like webinars and workshops, or meetings where the best practices of the top performers in a certain capability are shared amongst the participating companies. Whatever the method, the goal is to improve the whole value chain’s market competitiveness by pursuing higher levels of maturity in cost measurement and management.

4.2.1 Structure of the model

CMMM is a pyramid-shaped model comprising four successive MECE maturity levels that are not only linked to one another but also follow a progressive logic (see Figure 2).

The first level (L_01) constitutes the basics of the model. This level tests the company’s capability to classify direct and indirect costs and variable and fixed costs, as well as capture levels of detail in these classifications. This is the starting point for correctly measuring and managing costs within an organisation. Accordingly, level L_01 forms the foundation of the pyramid. Presumably, a company that can rely on a comprehensive, well-structured and detailed cost database, i.e. a company that is mature in the cost classification area, is in a position to successfully implement effective cost measurement practices.

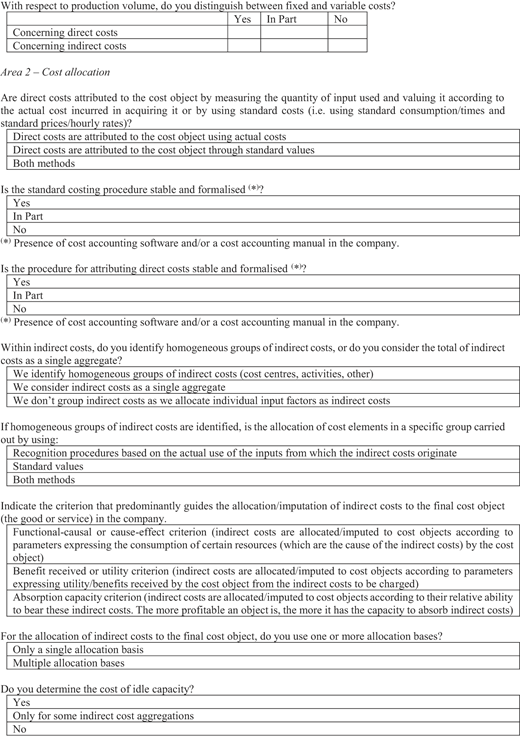

The second level (L_02) assesses a company’s cost allocation capabilities. Measuring the cost of a certain object of analysis requires a correct allocation of both direct and indirect costs to the object of analysis. Therefore, at this level, CMMM assesses the maturity of a company’s cost allocation capabilities concerning both direct and indirect costs.

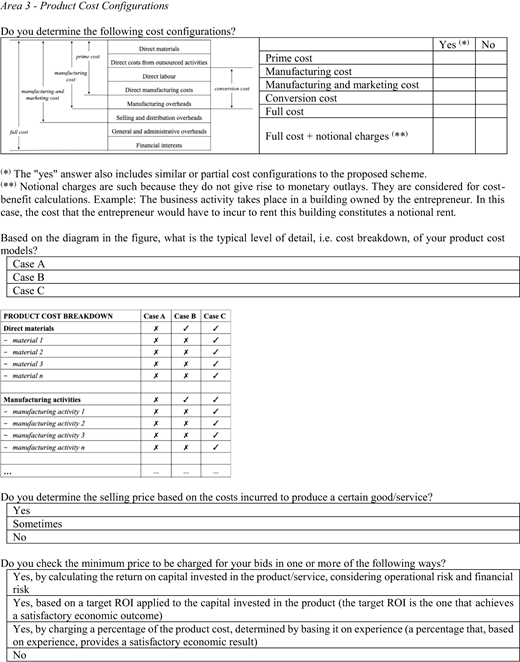

A company with a reliable cost database that allocates direct and indirect costs in accordance with the best theoretical principles of costing should be capable of calculating different cost configurations. A cost configuration is an aggregation, more or less extensive, of direct and indirect costs. As an example, the first question in section 3 of the questionnaire ( Appendix) presents a schema of the main possible cost configurations that a company can calculate. Companies can rely on these configurations: (1) as a solid and truthful foundation for negotiating with partners; (2) as a way of setting the market price for their products; and (3) for evaluating profitability in the case of a price taker company. Thus, the third level of the pyramid (L_03) explores the extent to which the company uses its cost database and costing practices to correctly determine available cost configurations; it also investigates the degree of granularity of such configurations. This can fulfil different decision-making needs and purposes. Further, at this level, CMMM also tests the maturity of a company when facing basic price setting problems.

The knowledge and conscious use of cost configurations, their high granularity, and the ability to correctly determine sales prices are fundamental elements of being profitable and competitive in the market – especially in the context of an inter-organisational relationship between a focal company and its suppliers. The knowledge and conscious use of cost configurations and the high granularity of these configurations on the part of two actors participating in an inter-organisational relationship allow them both to align cost data, share this data, and reciprocally understand the meanings embedded in the data. In other words, it allows them to effectively communicate. This forms the basis of IOCM actions. Further, the ability to correctly determine sale prices guarantees the quality of transactions between companies in the value chain and avoids losing competitiveness due to excessively high prices charged by suppliers or the damage caused by too low or even negative profit margins achievable by suppliers.

As a result, when a company is mature in its cost classification and cost allocation capabilities and is aware of and able to manage cost configurations and prices, CMMM suggests that the company has all the credentials to successfully undertake cost management initiatives. Hence, the fourth level (L_04) of the maturity model investigates the capability of the company to work on cost-out programmes, both at an intra- and inter-organisational level. To this end, the fourth level tests a company’s ability to identify the cost drivers of its products and to forecast how current inflationary and deflationary trends in labour costs and the price of raw materials and energy will affect the cost of its products. This level also evaluates a company’s knowledge and application of cost management approaches and practices, and finally, it determines the company’s attitude towards exchanging reliable cost information through an open-book accounting approach.

The model is purposefully designed as a pyramid because it stresses the importance of establishing a solid foundation before expanding to the next level. The more solid the foundation, the more solid the capabilities that are built on top of the foundation. Accordingly, where gaps exist, action must first be taken at lower levels. Only when these gaps have been filled is it possible to ascend. From this perspective, CMMM provides indications on where to intervene and on the preferred priority of these interventions. Moreover, the indications reflect a Paretian logic. The Pareto principle, also known as the Pareto rule, states that 80% of the consequences result from 20% of the causes, thus asserting an unequal relationship between inputs and outputs (Wikipedia, 2022). In the case of the CMMM, the idea is that the majority of a company’s maturity (i.e. the 80% of the Pareto rule) comes from the basics of cost classification and cost allocation (i.e. the 20% of the Pareto rule). Accordingly, the more mature a company is at the initial levels, the less it has to do in terms of training at the later levels because the foundations are solid.

4.3 Content

The content of the model consists of a questionnaire and an associated scoring method. The questionnaire is the instrument used to gather data from a company on its current cost measurement and management capability levels. The scoring method translates the responses into scores to obtain quantitative measures of maturity. The questionnaire and the scoring method were both implemented using IT as this made distribution easier, allowed the companies to respond to the questionnaires online, and automated the process of calculating the results. However, it is worth noting that these IT tools are not a necessary condition for using CMMM. They simply made our job easier.

4.3.1 Questionnaire

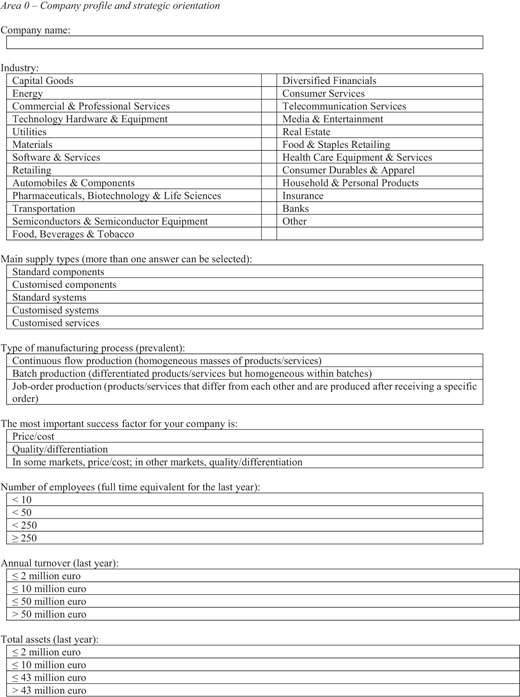

The questionnaire that was developed and used in the project consists of 91 multiple-choice questions grouped into five different areas – four of which are directly linked to the maturity levels of CMMM (see Table 1 for the groupings and the Appendix for the questionnaire). Consistent with De Bruin et al. (2005), the questions were derived from the following operative approach. As a start, the researchers reviewed the relevant literature in each area of the questionnaire (e.g. White and Clinton, 2014; Wouters and Morales, 2014), and then drew up a list of possible questions to include for each area. Interviews and focus groups were then conducted with Companies A and B to confirm, modify and/or supplement the questions.

The first area – Area 0 – contains questions about the demographics of the respondent company and its strategic orientation:

- (1)

name;

- (2)

industrial sector;

- (3)

size;

- (4)

type of offer, i.e. whether the company offers standard items or customised products;

- (5)

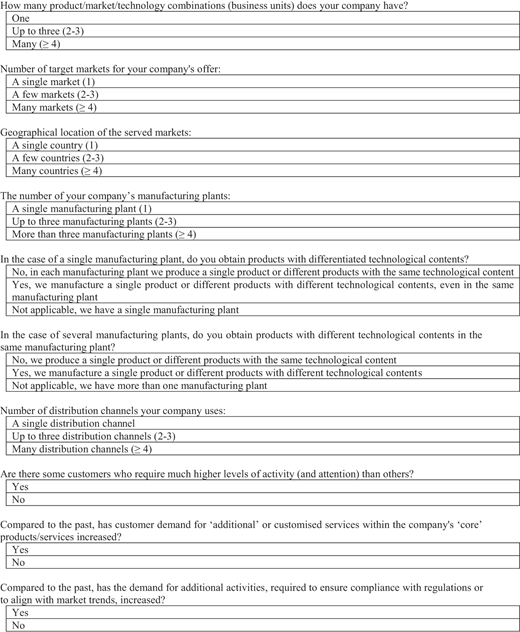

structural and manufacturing complexity;

- (6)

information needs for decision-making; and

- (7)

presence of cost management enablers.

The degree of structural and manufacturing complexity refers to aspects like the number and diversity of product/technology/market combinations of the company, the number of manufacturing plants, and the number of distribution channels that collectively determine the structural and manufacturing complexity of a certain business reality. Research, which is based on contingency theory (Otley, 1980, 2016), suggests that improvements to a firm’s performance are often functions of the alignment between the functionality and sophistication of costing systems and a company’s operating environment (see, for instance, Chenhall, 2003 or Al-Omiri and Drury, 2007).

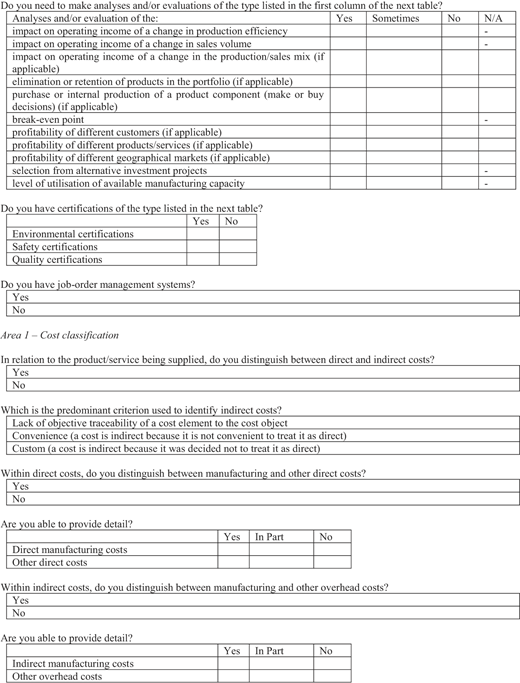

Information needs for decision making refers to the data, analyses, and assessments that are required to support decisions about the current operations of the company (e.g. make or buy decisions, investment evaluation analyses, break-even-point assessments). In this regard, the information needs of a company are usually dependent on its structural and manufacturing complexity and its strategic plans.

Based on ideas by Ferdows and De Meyer (1990), cost management enablers are environmental certifications, safety certifications, quality certifications, and job-order management systems.

Overall, this information contextualises the analysis of maturity with respect to a particular company, while also linking it to the company’s strategic goals. The data collected in Area 0 reflects choices regarding competitive strategy and company structure encompassing factors such as the types of offerings, production/distribution structure, and key informational needs to support the formulation and implementation of strategy. Consequently, Area 0 facilitates the evaluation of the managerial costing system’s maturity level in light of the organisation’s operational needs and strategic orientation. Considering the expectations emerging from this information, it allows for consistency checks across various parts of the company’s managerial costing system and the contextualization of the maturity assessment results, while deriving improvement directions at the operational level that align with the strategic level. Actually, it is reasonable to expect a higher level of maturity from a company with a high degree of structural and manufacturing complexity and high information needs than from a company with a low degree of structural and manufacturing complexity and moderate information needs. When it comes specifically to inter-organisational relationships, cost management capability expectations are different for a supplier of standard items than for a supplier that delivers customised products to the focal company. In the latter case, the supplier is much more likely to undertake IOCM programmes with the focal company and, therefore, its maturity on cost management capabilities is expected to be higher than that of a supplier who provides the focal company with standard products (for which the scope of intervention to review the design or reduce the cost of the product at an inter-organisational level is very limited, if not existent).

Sections 1 to 4 of the questionnaire contain questions aimed at analysing the current capability levels of the responding company on issues covered in each of the outlined areas. The questions test the company’s knowledge and ability to apply, in practice, what the literature identifies and recognises as key, theoretically-sound principles of managerial costing (e.g. White and Clinton, 2014; Datar and Rajan, 2018).

The questionnaire is supplemented with a document containing instructions for its completion and a glossary. To avoid misunderstandings or misinterpretations, the glossary clarifies the terminology used in the questionnaire, aligning it with the terminology currently used inside the organisations.

4.3.2 Scoring method

Scoring is based on a simple method that is already in use in the field of MMs applied to performance management issues (Jääskeläinen and Roitto, 2015). Each answer receives a score that can be 0, 0.5 or 1. The format of the questions is multiple-choice, meaning that a number of response options are available for each question. Answers that denote a high level of maturity, as determined by the costing literature (e.g. White and Clinton, 2014; Datar and Rajan, 2018), are assigned a score of 1. Answers that indicate a sufficient or moderate level of maturity are assigned a score of 0.5, and answers that denote the lack of maturity are assigned a score of 0 (Table 2).

Maturity is represented both by discrete measures per area and by an overall maturity score. The sum of the scores obtained in each area represents the company’s maturity level for that area. The overall maturity of the company is the result of the sum of the scores per area, with each score weighted consistently with the rationale associated with the pyramid-like structure of CMMM (see the level descriptions in Section 4.2.1). The weighting percentages are given in Table 3.

Recalling the pyramid structure of CMMM, weight is distributed in a decreasing manner, starting at the base of the pyramid and ascending to its apex. Since the capabilities monitored at the higher levels build on those of the lower levels, a greater weight is given to the capabilities monitored at the first level of the pyramid. When proceeding to the higher levels, the weights decrease. An exception to this is the last level of the pyramid, which departs from the logic of the previous levels in that cost management capabilities depend both on the capabilities of the previous levels and on other capabilities unrelated to them [3].

Both the discrete scores and the overall score are considered in light of the company’s profile and strategic orientation (i.e. the outcome of the Area 0) but also in light of the scores obtained by the company’s peers (when CMMM is applied with an inter-organisational scope). If this analysis demonstrates that some form of improvement is advisable because the overall score is inappropriate, given the company profile and its strategic orientation, or is much lower than the average score of peer companies, a capability gap exists. In this event, the respective area scores suggest where, i.e. in which capability area, training is needed and the pyramid structure of the model prioritises the interventions.

For certain questions that test basic or fundamental capabilities, the scoring method introduces a double weight so that these questions have a greater influence on the final score than other questions. Further, the scoring method includes a control system that checks the consistency between answers given to different questions. An “alert” appears if there is a lack of consistency. For instance, a warning or alert sign would display if a company declared that it is important to involve suppliers in new product development but then, as a subsequent response, stated that it did not want to engage in open book accounting activities with its suppliers. In this case, the responding company would be required to review its answers, and specifically to check if the alert was due to a mistake made when completing the questionnaire or if it denotes an actual problem.

4.4 Test

The model was tested through a pilot application with Company A and a cluster of 11 suppliers selected by Company A, including Company B. A kick-off meeting was organised to introduce CMMM to the suppliers, along with a request that they complete the questionnaire by involving representatives of various business functions who had the necessary company expertise and knowledge to answer all the questions. Since both the focal company and the suppliers completed the questionnaire, our final dataset comprised 12 complete questionnaires.

The testing was divided into two phases: creating a maturity profile based on data collected through questionnaires and validating the maturity profile through subsequent informal catch-up meetings with each respondent company. To create the maturity profile, the answers in response to the questionnaire were elaborated on according to the outlined scoring method. Missing data in areas 1, 2, 3, or 4 was interpreted as an absence of maturity and a score of zero was assigned to the questions with missing answers.

The outcome of this phase was a maturity profile for each respondent company comprising both discrete measures of maturity per area and an overall maturity score, along with succinct bullet-point remarks on potential improvement opportunities. Figure 3 shows an example of a company’s maturity profile template (the company’s name is fictional).

In a subsequent informal catch-up meeting, each company that completed the questionnaire discussed its own maturity assessment result, presented in the format shown in Figure 3. The aim of these catch-up meetings was to verify that the maturity profile identified by CMMM accurately reflected the business situation. It was also an opportunity to check for inconsistencies (or alerts) between the areas and to review the answers given in cases of misinterpretation or because the questions had been answered incorrectly. Ultimately, these catch-up meetings validated the maturity assessment’s results.

5. Discussion and conclusions

This paper recommends CMMM as a tool that companies can use to assess and develop their managerial costing capabilities. Through an interventionist case study, the paper illustrates the design choices, the development, and the practical application of this tool. To highlight the differences between this model and existing ones along with the additional benefits CMMM aspires to bring to the table, Table 4 (on the next page) provides a summary of the characteristics of existing MMs in the field of managerial costing in terms of goal, scope, method of assessment, and expected outcome. On this basis, we then pinpoint the elements and innovations of our proposal compared to existing models to clearly highlight how CMMM differs from other MMs and with what benefits.

CMMM shares similarities with existing models in its attention to the elements of cost measurement. However, its focus extends far beyond mere cost calculation, encompassing pricing considerations and, notably, an organisation’s capabilities to manage costs. Furthermore, and unlike other models, CMMM seeks to grasp the appropriateness of practices in relation to the specific organisational context in which they are used. It thus allows the user to make a kind of relativization of the maturity assessment on the basis of the characteristics of the organisational context where it is applied. Unlike other MMs, CMMM’s scope transcends individual organisational boundaries to encompass inter-organisational relationships, positioning itself as a tool to improve collaborative endeavours. The maturity assessment of CMMM is grounded in a structured and replicable methodology that supports genuine comparability among organisations. Additionally, its unique pyramid structure inherently identifies priority areas for intervention. The idea is to facilitate improvements to managerial costing systems while mitigating time and resource inefficiencies and avoiding potentially ineffective interventions rooted in weak foundations. The overarching objective of CMMM is to enhance both organisational and inter-organisational performance, fostering market success, competitiveness, and value creation, as we showed in the previous sections.

The study’s starting point was grounded in both practical and theoretical premises.

In practical terms, the research serves as an example of the constructive research approach (Lukka, 2003). It was designed to respond to the real-world need of a large manufacturing company for a tool to assess the cost measurement and management capabilities of its small-to-medium-sized suppliers, as well to initiate a process of capability improvement. By enhancing its suppliers’ capabilities, the aim of the manufacturing company was to strengthen its inter-organisational relationship with them, and especially to improve the quality (i.e. efficiency and effectiveness) of IOCM actions in view of higher levels of competitiveness concerning the value chain’s offer to the market.

What prompted this research was evidence that firms frequently need to improve their costing capabilities (Lawson et al., 2019). Although an MM could provide possible support in this respect, suitable tailor-made models on both cost measurement and cost management capabilities, also effective in an inter-organisational setting, were notably absent in the literature. This research therefore advances existing knowledge by offering an MM that can be used to improve organisations’ calculation and cost management capabilities. Further, in the IOCM context, the model can support the alignment of the participating entities’ capabilities, thereby improving the competitiveness of conjoined cost management actions. Moreover, CMMM’s design and implementation seize the opportunity to support the future development of MMs in the field of managerial costing, encouraging the growth of this relevant study area.

From the testing and pilot phases of the model, we can confirm Lawson et al.’s (2019) findings that firms still face challenges regarding the “basics” of cost measurement. In our assessments, we detected deficits in both Areas 1 and 2 amongst the 11 suppliers that participated in the model’s testing. Therefore, researchers have the opportunity to produce real impacts if they focus their research projects on these aspects or if they generate solutions that promote the development of companies in these areas.

The strength of the model’s analytic power has been proved and it can serve as a starting point for capability development programmes, as well as to position and benchmark initiatives in relation to other organisations. CMMM’s data supports the process of gaining an awareness of the user company’s current capability level. On the part of a focal company that decides to use the maturity model to engage its suppliers in the assessment, CMMM enables comparative analyses of the different suppliers and provides the focal company with indications that might be useful when designing and organising supplier-specific training events and activities or for other purposes (e.g. confirming or revoking the “strategic” status of a supplier). As suggested in the IOCM literature (e.g. Caglio, 2018), aligning the level of managerial costing capabilities between companies engaging in IOCM collaborations is an essential requirement for increasing their effectiveness. Therefore, setting shared improvement targets based on the levels suggested by the MM should improve IOCM actions between the suppliers and the focal company. Similarly, the maturity level assessment of suppliers should serve as a basis for improvement when they independently plan any enhancements of their managerial costing systems. In this regard, CMMM offers practitioners an easy-to-implement tool that can be used to improve the maturity of a company’s managerial costing system, with all the strategic implications that derive from better capabilities in measuring and managing costs (e.g. Porter, 1985; Shank and Govindarajan, 1993). Since the current stage of our research does not provide evidence to support this, future research will allow further in-depth studies and reflections on this issue. This will include consideration of the cost-benefit trade-offs inherent at various levels of the pyramid concerning the planning and implementing of managerial costing enhancements and the associated cost of such implementations.

The participants’ initial experience of using the model, the results of its testing, as well as their feedback on the pilot test suggest that the model can indeed be applied to different manufacturing and organisational contexts, both with an intra- and inter-organisational level aim. It also provides a reliable representation of the current status of cost measurement and management capabilities within an organisation. In this sense, the pyramid-shaped CMMM serves as a valid theoretical framework for describing and analysing managerial costing within organisations. Consistent with Lukka and Kasanen (1995)’s methodological work on the issue of generalisability in accounting research, we conclude that CMMM can work for companies beyond those originally involved in its development and testing.

To conclude, there are some limitations of this study to consider, as well as future avenues for research. CMMM is a new managerial tool and, although it is the outcome of an almost two-year period of research and development and has been tested and validated, we still assume that there is room for improvement. This improvement may derive from future applications and the testing of the model on a much larger participant base. Although different industrial sectors were represented in the participant group, only 12 Italian companies participated in the testing of the model. In particular, we heartily believe that CMMM would benefit from further large-scale testing. Considering that the development process and the decisions made during the current process are transparent and clear, this should allow future researchers to undertake independent, third-party assessments of the proposed MM’s validity. As Mettler (2011, p. 88) states: “An extensive search within the relevant literature demonstrated that the great part of the developed maturity assessment models does not disclose its research method and their underlying design decisions. However, the externalisation of this knowledge has an important consequence”. In this regard, it is important to emphasise that the choices regarding the weighting of scores are decisions that have been made in agreement with the two companies that financed and helped to develop the MM. According to the research participants, the proposed weights are capable of effectively operationalizing the CMMM. Nevertheless, future users of the model may certainly decide to adopt different weights. For example, situations could arise where a company assigns greater weight to one level of the pyramid rather than another, like in cases where variable costing is used instead of full costing. In such cases, the weights of both the questions and the levels of CMMM can be calibrated accordingly.

Finally, to enhance the model’s efficacy, the development of supplier-specific, tailored parts of the questionnaire should be considered. In this regard, Cooper and Slagmulder (1999) distinguish between common suppliers, subcontractors, major suppliers, and family members. This taxonomy could be reflected in CMMM. In this way, the core of the model would remain the same, but it would be possible to fully capture the peculiarities of different supply relationships. Additionally, in this process of further enhancing and refining CMMM, introducing questions aimed at exploring the maturity of managerial costing in relation to mega-trends in accounting are contemporary but also forward-looking topics deserving considerable attention. Initial topics for consideration include the digital transformation, the big data revolution and its widely varied emerging technologies, and the increasingly pronounced attention to nature and biodiversity conservation.

The research presented in this paper was conducted within the framework of the CONTROL (COst maNagemenT matuRity mOdeL) project, funded by the Tuscany Region (Italy), Nuovo Pignone Tecnologie s.r.l. (Baker Hughes), Sime s.r.l., and the Department of Economics and Management of the University of Pisa, in collaboration with the Sant’Anna School of Advanced Studies of Pisa and the University of Florence. The authors acknowledge the contributions of Nuovo Pignone Tecnologie s.r.l. (Baker Hughes), Sime s.r.l., and all the companies that participated in the pilot application of the Cost Management Maturity Model to this research.

Notes

The search was conducted using the following search strings: (1) “cost measurement” OR “cost accounting” OR “cost management” AND “maturity”; (2) “costing” AND “maturity”; (3) “costing system*” AND “maturity”; and (4) “managerial costing” AND “maturity”.

Based on various criteria and parameters, Nuovo Pignone Tecnologie s.r.l. designates certain suppliers as strategic partners, aiming to strengthen collaborative relationships with them.

For instance, the use of the cost management method known as “modular design”, according to which “products are designed in such a way, that a wide variety of final products can be produced using a limited number of modules that are adjusted and/or combined with different parts and other modules” (Wouters and Morales, 2014, p. 267), depends on key capabilities other than cost measurement capabilities.

References

Appendix