Cryptocurrency, an emerging asset class, is a virtual form of currency that uses cryptography for security and operates on decentralised networks based on blockchain technology. It offers both challenges and opportunities for investors, particularly in terms of diversification, risk management and potential returns. Considering this, the present study attempts to investigate the sentimental factors influencing cryptocurrency while unravelling the intricate interplay among these factors.

To achieve this, interpretive structure modelling (ISM) identifies the hierarchical model of critical sentimental factors, while Cross-Impact Matrix Multiplication Applied to Classification (MICMAC) explores their dependency and driving power. Analytic hierarchy process (AHP) is adopted to rank the drivers.

Findings reveal that the pandemic, war, religiosity and economic uncertainty are top-level factors dominantly shaping cryptocurrency trends. Simultaneously, Google Search Trends and Herding emerge as the most dependent factors, influenced by sentiments that emerged from other factors.

The study unpacks implications, acknowledges limitations and proposes avenues for future research.

By exploring the interactive interrelationships among identified sentimental factors through ISM-MICMAC analysis and ranking via the AHP, this paper will have a great influence while contributing towards this evolving field.

1. Introduction

Cryptocurrencies have emerged as a novel class of alternative investment assets (Mundi and Kumar, 2022), offering substantial potential returns and significant market volatility. The cryptocurrency market has witnessed rapid development and continues to evolve (Peng et al., 2024). Various reasons fuel the global fascination with cryptocurrencies. First, financial investors are allured to high returns and the opportunity to diversify portfolios (Omane-Adjepong et al., 2019; Inci and Lagasse, 2019), especially considering the drastic price surges in cryptocurrencies over a short period. Second, some countries, such as South Korea, Germany and Japan, have officially recognised digital assets as a legal payment method (Hossain, 2023). Third, significant companies like Dell, Enercity and Microsoft have also embraced Bitcoin transactions (Sakho et al., 2019). Fourth, central banks worldwide are showing an increased interest in exploring the application of cryptocurrencies (Ozili, 2022). Lastly, introducing Bitcoin futures by certain exchanges has added another layer of curiosity to the cryptocurrency landscape.

Understanding the multifaceted nature of cryptocurrencies poses a significant challenge for the real economy, primarily due to their decentralised nature, disrupting traditional financial systems (Almeida and Gonçalves, 2022), and it is highly influenced by the sentiments of the investor and the market (Almeida and Gonçalves, 2023). Since it is profoundly shaped by the feelings of investors (Sharma et al., 2024) and sentiments of the market, which are highly dynamic therefore, it is essential to investigate the sentimental factors influencing cryptocurrencies to enhance the predictive accuracy of cryptocurrency prices.

While studies have begun to unravel the determinants of Bitcoin and other prominent cryptocurrencies (Ciaian et al., 2016; Ozili, 2022), the dynamic and decentralised nature of the cryptocurrency market necessitates ongoing exploration of these factors. This innovation empowers investors to participate actively in the cryptocurrency market and interests researchers to identify diverse elements influencing its price-driven returns on a continuous basis (Leshno and Strack, 2020). The literature has recognised that sentiments of the identified factors, such as news coverage, social media like Twitter and Google Trends, influence from celebrities, geopolitical events like the war, the impact of the pandemic, economic uncertainty, herding behaviour and religiosity, affect cryptocurrencies. Despite existing research shedding light on cryptocurrency pricing determinants, no study exhibits a comprehensive list of sentimental factors and their interaction. Prior studies have primarily concentrated on identifying the macroeconomic variables (Teker et al., 2020), demographic and psychological factors (Senkardes and Akadur, 2021) and fundamental factors (Sovbetov, 2018) that impact cryptocurrency. Considering the above, the present study aims to fill the literature gap and document the interrelationship among these identified factors. In the current context, due to the scarcity of empirical research, the present study contributes a novel view by identifying and modelling sentimental factors that influence cryptocurrency prices. Since sentiments play the most crucial role in shaping crypto prices (Sharma et al., 2024), understanding the integrated framework of these crucial sentimental factors is essential. To the best of the authors’ knowledge, this article is the first that identifies the various sentimental factors influencing cryptocurrency prices and then discloses the intricate interplay among these factors and provides a ranking of the identified factors. The study has the following research objectives (OB):

To identify and determine the key sentimental factors crucial in shaping cryptocurrency prices from literature.

To model and construct hierarchical linkages between these identified sentimental factors.

To examine the most significant sentimental factor in the view of driving and dependency power.

To understand the ranking of these factors, if any.

To accomplish these goals, a set of sentimental factors were discerned from literature support, and the nine most crucial sentimental factors were identified after rounds of continuous expert opinion. The study employs the ISM technique (Attri et al., 2013) to examine the interactions among these factors (Kaur et al., 2015) and the analytical hierarchy process (AHP) technique (Zahedi, 1986) which is used for ranking the identified factors. The ISM technique is utilised in tandem with Cross-Impact Matrix Multiplication Applied to Classification (MICMAC) analysis to assess the driving and dependent power of the factors (Fore and Mbohwa, 2015; Kaur and Shri, 2015). The research provides actionable insights for cryptocurrency stakeholders, including investors who can use the identified factors to anticipate trends, manage risks and optimize portfolios. Policymakers can benefit from understanding these factors to develop effective regulations that enhance market stability and protect investors. The remainder of the article is segmented into the following parts: Theoretical framework, Review of literature, Research methodology, Results of the study, Discussion and implications, Conclusion and Future research.

2. Theoretical framework

Unlike traditional financial markets, where rational behaviour is often assumed, cryptocurrency markets are driven largely by investor psychology, with cognitive biases and emotions playing a significant role in price formation and market behaviour. These markets often exhibit characteristics that deviate from the assumptions of rational behaviour, such as bubbles, crashes and extreme volatility, which are fuelled by investor sentiment rather than fundamental value (Yermack, 2015). The following Table 1 presents the list of the theories of behavioural finance and their relevance in understanding and exploring the factors of cryptocurrency prices.

3. Literature review

The concept of cryptocurrency can be traced back to the creation of Bitcoin by an anonymous person or group known as Satoshi Nakamoto in 2008. In their white paper, they laid the foundation for decentralized digital currencies, leveraging blockchain technology to ensure secure and transparent transactions without the need for a central authority (Nakamoto, 2008). Since then, cryptocurrencies have rapidly evolved from niche digital assets to mainstream financial instruments, prompting widespread interest among investors, policymakers and academics. Previous authors have identified factors contributing to the growth of the cryptocurrency market, factors influencing the development of the initial coin offering industry or have explored causal relationships among identified barriers to Bitcoin adoption (Kumar et al., 2022, 2023; Singh et al., 2023), but their study is limited to this specific context. This calls for a comprehensive understanding of the sentimental factors that collectively influence the cryptocurrency market, the interplay among these factors through ISM methodology, and finally a ranking of these significant sentimental factors that contribute to shaping cryptocurrency prices using AHP. To address this gap, a list of 11 sentimental factors was identified after a thorough literature review. Based on the experts’ opinion, a final list of nine key sentimental factors critical for shaping cryptocurrency prices was produced (OB 1). These factors are explained in the text below and summarized in tabular form in Table 2.

3.1 Media coverage

The sentiments emerging from news headlines can have a profound impact on cryptocurrency prices, often leading to rapid and significant price fluctuations. Positive publicly available information instils trust in investors, leading to increased volatility and confidence in this asset class (Kulbhaskar and Subramaniam, 2023). Whereas media coverage can also amplify fear among people by highlighting negative events, potential risks or crises. This can create a heightened sense of fear among the public, discouraging them from buying cryptocurrency (Kulbhaskar and Subramaniam, 2023). Previous studies have found that negative and positive tones in the news have cause-and-effect relationships with Bitcoin returns (Huynh, 2022). Additionally, news about Central Bank Digital Currency has a striking association with Bitcoin returns (Akin et al., 2023).

3.2 Social media platform

Social media platforms and cryptocurrencies have become increasingly interconnected, influencing each other. Despite the unregulated nature of the markets, investors consider issuers’ sentiments on Twitter as credible information influencing their actions (Zhang and Zhang, 2022). Fluctuations in Bitcoin prices are caused by sentiments generated by tweets from cryptocurrency influencers (Hamza, 2020). Social media platforms disseminate both happy and fearful information. They can amplify fear through the rapid dissemination of information, including sensational or misleading content. Fear is not only a response triggered by exposure to social media but also is an integral part of the content disseminated through this channel (Naeem et al., 2021). Also, social media platforms can spread fear and fraudulent schemes rapidly. Misinformation is a prevalent issue on social media where scammers mislead potential investors (Nghiem et al., 2021).

3.3 Google Search Trend

Sentiments from Google Search Trends, particularly through tools like Google Search Volume Index, provide valuable insights into the relationship between public’s interest and cryptocurrency markets. Online investor searches for cryptocurrency information impacts cryptocurrency prices, trading volume and volatility (Chuen, 2015) and the information transfer between Google Trend and daily crypto returns is found to be bi-directional (Aslanidis et al., 2022). Literature also highlights that Google Search value exercises significant influence on Bitcoin returns and can be a good predictor for cryptocurrency returns (Nasir et al., 2019).

3.4 Celebrities

Celebrities and cryptocurrency have become increasingly intertwined, with celebrities playing a significant role in the promotion, adoption and mainstream awareness of digital assets. Prospective investors may be influenced by the sentiments expressed through tweets from well-known celebrities on social media platforms while investing in digital assets (Ullah et al., 2022). Also, Ante (2023) provided significant empirical evidence for the impact of the sentiments of an influential person (Elon Musk) on cryptocurrency prices and trading volumes through social media networks. Similar results were demonstrated by Zhang and Zhang (2022), whose study explored the role of sentiments displayed on Twitter by cryptocurrency issuers on returns and trading volumes.

3.5 War

The intersection of war sentiments and cryptocurrency is complex. War introduces uncertainty, which impacts investors’ attitudes and sentiments, leading to volatility and changes in liquidity. The Ukraine–Russia war significantly affected global financial markets, influencing investor attitudes wherein they turned to cryptocurrency as a means of storing and transferring value without regulatory constraints (Chowdhury and Humaira, 2023). Further, the course of the war temporarily impacted the liquidity of some cryptocurrencies as many investors sought to avoid regulatory sanctions, which also led to improved trading (Theiri et al., 2022). During these geopolitical conflicts, short-term investors respond to the heightened uncertainty by seeking liquidity and thus contributing to the increased volatility in financial markets, including cryptocurrencies (Khalfaoui et al., 2023).

3.6 Pandemic

The sentiments during the COVID-19 pandemic had a profound impact on many sectors, including the cryptocurrency market. The pandemic is a significant source of fear. The health crisis and social disruption caused by the pandemic contribute to widespread fear (Galea et al., 2020). Moreover, cryptocurrency markets exhibit unprecedented levels of instability and irregularity during the pandemic, which also heighten investors anxiety (Lahmiri and Bekiros, 2020). The market’s instability is significantly riskier than traditional equities, leading to greater scepticism and fear among investors (Kumar et al., 2023).

3.7 Economic policy uncertainty

Lack of clear direction on monetary, fiscal or regulatory policies leads to volatility in the financial markets, which also extends to crytocurrency market. Instability in traditional financial markets during increased economic uncertainty make cryptocurrency a safe-haven asset (Bouri et al., 2017). Another reason for the increased demand of digital assets during economic uncertainity is their independence from central banks and governments (Ji et al., 2019). But the role of cryptocurrency as a safe-haven asset is inconsistent based on market condition and economic uncertainty (Shahzad et al., 2019).

3.8 Herd behaviour

Herd behaviour in the cryptocurrency market exhibits some unique characteristics due to the market’s distinct nature compared to traditional financial markets. Herding behaviour in cryptocurrency markets occurs when returns decline and the network effect of investors expands. This behaviour leads to market inefficiency, reducing the potential benefits of diversification as individual traders comply with the market consensus (Wanidwaranan and Termprasertsakul, 2023; Omane-Adjepong et al., 2021; Youssef, 2022).

3.9 Religiosity

Religiosity refers to the extent of an individual’s religious beliefs, practices and commitment. Religious factors shape an individual’s attitude towards financial tools like cryptocurrencies (Mnif et al., 2024). Religious sentiments and attitudes play a significant role in shaping individual’s views on cryptocurrencies. Different religious teachings and principles can influence how people perceive the ethical implications, risks and acceptability of using cryptocurrencies (Koeswandana and Sugino, 2023).

4. Research methodology

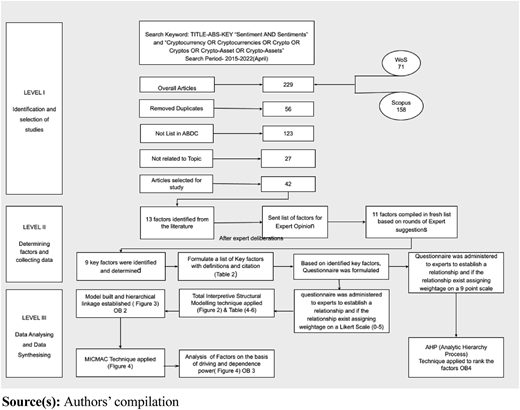

To achieve the study objectives, three levels of analysis have been adopted. The first level is the identification and selection of studies; the second is determining factors and collecting data, and the third is data analysing and data synthesis (explained in Figure 1).

4.1 Level 1: identification and selection of studies

At this level, an in-depth literature was carried out. Data were collected from SCOPUS and Web of Science by using keywords (“Sentiments AND Sentiment” and “Crypto OR Crypto-Asset OR Cryptocurrency OR Cryptocurrencies OR Cryptos OR Crypto-Assets”). Articles are about the time frame 2015–2022. Nevertheless, a few notable research articles on the topic have been considered. For details on screening criteria, refer to Figure 1.

4.2 Level 2: determining factors and collecting data

After a thorough review of the literature, eleven factors were identified. A consolidated list of sentimental factors was shared with the experts for their opinions, additions and deletions. For their participation, 25 experts were contacted and were explained about the research objectives and the present study. About 16 experts agreed to be a part of the study. Experts were selected based on their qualifications and knowledge in the field of study (Paridhi et al., 2024) (refer to Table A1 in the Appendix). The judgemental sampling technique was used, and a conventional decision-making procedure was used for selecting variables to gain expert opinion (Kharb et al., 2024a; Parameswar et al., 2023). After rounds of opinions from experts, a final list of nine variables was made. Thereafter a five-point Likert scale questionnaire was formulated (Kharb et al., 2024b), inputs of none, negligible and very low were taken as no and other inputs were taken as yes for further research.

4.3 Level 3: data analysing and data synthesising

The study at this level further unravels the intricate interplay among the identified factors. The primary objective is to discern the most influential sentimental factors that shape cryptocurrency prices. To achieve this objective, the research leverages the ISM technique (Attri et al., 2013). It is used to scrutinise the interactions among these factors, aiming for a more profound and refined comprehension of these intricate team-level constructs (Kaur et al., 2016). ISM is a valuable instrument for extracting well-structured relationships among intricate variables, predominantly relying on expert opinions gathered during brainstorming sessions (Warfield, 1974). Renowned for its effectiveness, ISM is an established methodology known for elucidating the connections between specific variables that characterise an issue or challenge (Sage, 1977). To ascertain the driving and dependent power of the identified factors, the ISM technique is supplemented by the MICMAC methodology. Further to give a ranking to the identified factors, the authors have applied AHP techniques.

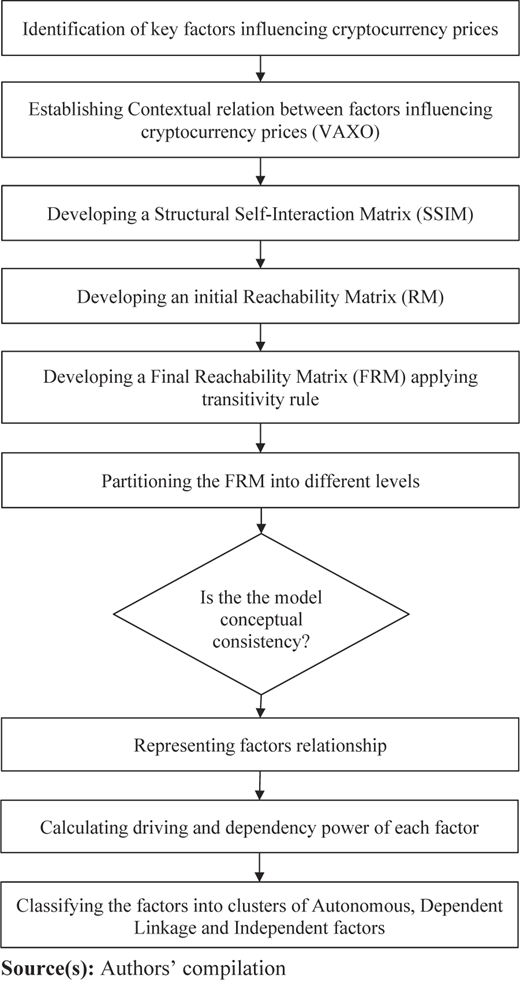

4.3.1 Interpretive structural modelling and MICMAC

Implementing the ISM methodology involves several steps (refer to Figure 2):

Create a well-organised structured self-interaction matrix (SSIM) by defining pairwise relationships between factors.

Generate the RM (reachability matrix) from the SSIM matrix and perform a transitivity check. This verification ensures that if Factor X is connected to Factor Y and Factor Y is connected to Factor Z, then Factor X must also connect to Factor Z (Table 3).

Following the transitivity check, segment the reachability matrix (RM) into distinct levels.

Generate the Level Partitioning and Canonical Matrix through continuous partitioning until the levels of all factors are based (Tables 4 and 5).

Derive a directed graph from the ultimate reachability matrix.

Transform the directed graph into the ISM model by substituting nodes with variable statements (Figure 3).

Execute MICMAC analysis by assigning variables to four quadrants according to their driving and dependence power. This categorisation aids in distinguishing variables as autonomous, dependent, linkage and driving variables (Figure 4).

For an in-depth exploration of the ISM and MICMAC methodologies, refer to the works of Sushil (2012), Attri et al. (2013), Janes (1988), Chander et al. (2013) and Bux et al. (2020).

4.3.2 Analytic hierarchy process

AHP stands out as one of the frequently employed multiple criteria decision-making (MCDM) methods for decision-making and analysis. AHP, considered one of the most robust MCDM methods, continues to be extensively employed as a reliable approach when evaluating a quantitative and qualitative dataset containing complex criteria and alternatives (Shri et al., 2023). Four processes are involved in applying AHP for a decision-making scenario (Zahedi, 1986). The results of AHP are shown in Table 6.

Step 1: The decision problem’s structural design.

Step 2: Comparing pairs of data and generating the judging matrix is step two.

Step 3: Establish local weights and comparative consistency.

Step 4: Local weights are accumulated.

AHP and its application concerns are covered at great length in many research articles (Saaty, 1990), review articles (Vaidya and Kumar, 2006) and books (Saaty, 1980). For detailed methodology, refer to Goepel (2018).

5. Result of the study

5.1 ISM analysis results

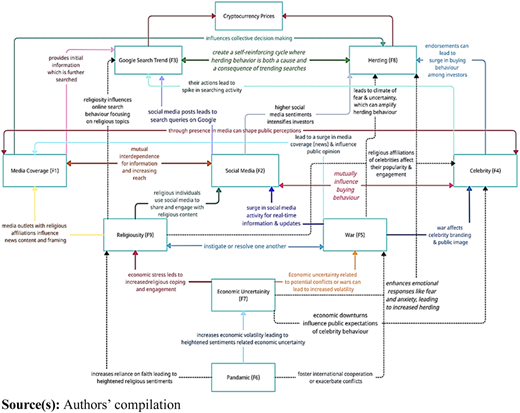

After five partitioning rounds, all the nine sentimental factors were at their levels. It is presented in Table 4. ISM hierarchical model is constructed based on these levels. ISM model in Figure 2 presents the interconnection of identified factors influencing cryptocurrency prices. The developed ISM model in Figure 2 addresses OB 2. It highlights the key factors, showing that sentiments during the pandemic are essential. Positioned at level V of the ISM model, the pandemic (F6) influences all the other factors in the hierarchical structure above it. Heuristic theory posits that investors rely on mental shortcuts or rules of thumb to make financial decisions, particularly in situations of uncertainty (Baker and Nofsinger, 2010). Sentiments during the situation of pandemic influence economic uncertainty leading to an increase in economic volatility (Qi et al., 2022). This in turn highlights the sentiments related to economic uncertainty. The bottommost variable is the most crucial factor that influences cryptocurrency prices and all other variables.

Level IV factor economic uncertainty (F7) affects factors at level III religiosity (F9) and war (F5). These factors both influence the factors above them and are influenced by the factors below. According to Ha (2014), economic stress during the Great Recession led to increased religious coping and engagement. Additionally, economic uncertainty related to potential conflicts or wars can lead to increased volatility (Al-Thaqeb and Algharabali, 2019). This resultant market volatility influences cryptocurrency prices. Economic stability can reduce investors’ trading frequency and bring stability to the market.

Level III has two factors: religiosity (F9) and war (F5). Their sentiments influence media coverage (F1), social media (F2) and celebrities (F4). The dynamic intersection between war and media coverage leads to a surge in media coverage (news) and influences public opinion (Kamalipour and Snow, 2004). Also, war influences social media (F2). During conflicts, there is often a surge in social media activity as people seek to share news, express opinions and engage in discussions about the war. Social media platforms become vital sources of real-time information and updates (Feng et al., 2021). According to herding theory, during uncertain times people follow the crowd as they feel that the crowd is better informed (Spyrou, 2013). This can influence the cryptocurrency market. A particular religion’s view on cryptocurrency can influence the investing activity of investors of that religion (Hasan, 2020).

At level II there are three factors: media coverage (F1), social media (F2) and celebrities (F4). Sentiments conveyed through news, social media and celebrity endorsements play a very important role in the study of factors influencing cryptocurrency pricing. Viral content on platforms like Twitter and Instagram often leads to increased search queries on Google (Mukherjee and Jansen, 2017), as users seek more information about trending topics. Further, celebrities can engage globally through social media and influence buying behaviour (Zafar et al., 2021). Media coverage provides initial information for social media and social media increases the reach of traditional media coverage (Vosoughi et al., 2018). Higher social media sentiments intensify investors and influence collective decision-making leading to herding behaviour (Yang et al., 2023). These factors influence level I factors Google Search Trend (F3) and Herding (F8). Google Search Trends can both reflect and amplify herding behaviour (Wanidwaranan and Termprasertsakul, 2023), which in turn affects cryptocurrency prices.

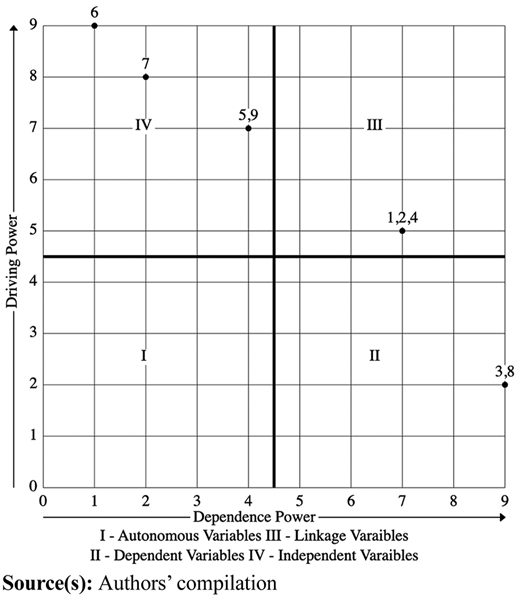

5.2 MICMAC analysis results and interpretation

MICMAC analysis scrutinizes the factors as driving and dependent powers. The sentimental factors under study are categorised into four clusters, as depicted in Figure 4 (OB 3). Cluster I consists of factors with weak driving power and low dependence, categorised as autonomous factors. These are those factors that are not associated with any other factor under study. In this study, Cluster I is empty, indicating all nine factors are related to each other somehow. The factors in this cluster have the lowest powers of driving and dependency. They are less intertwined with the rest of the framework. These factors are not considered in this study, and thus it can be concluded that all the factors are associated with cryptocurrency prices. Cluster II comprises dependent factors with high dependency but weak driving power. Cluster III includes linkage variables, exhibiting both dependence and high driving power. Lastly, Cluster IV consists of driving factors with low dependency but high driving power. In this study, none of the identified nine factors fall under the category of autonomous variables. Pandemic (F6), war (F5), religiosity (F9) and economic uncertainty (F7) emerge as initiating factors (Cluster IV), significantly impacting cryptocurrency prices with high driving power and low dependence power. These factors are highly unstable and need caution as they influence all others. Investors and policymakers should pay attention to these as they impact other dependent and linkage variables. Media coverage (F1), social media (F2) and celebrities (F4) serve as linking factors (Cluster III), influencing factors in Cluster II – herding behaviour (D8) and Google Search Trends (D3), which exhibit high dependence power and weak driving power.

5.3 AHP analysis results and interpretation

AHP results, presented in Table 6, elucidate the ranking of factors influencing cryptocurrency prices (OB 4). AHP, regarded as one of the most mature MCDM methods, continues to be extensively employed as a robust approach for navigating complex criteria and alternatives, whether presented in quantitative or qualitative datasets. It is observed after calculating the local weights that there is variation in relative weights, indicating that all the factors are not equally important for cryptocurrency pricing. Social media (F2) is at the first rank, followed by Google Search Trend (F3) and media coverage (F1) with priority weightage of 23.2, 22.6 and 19.5%. Since the cryptocurrency market is influenced by sentiments rather than fundamentals, investors should focus on the above-stated sentimental factors to understand the cryptocurrency market. Herding (F8) is at a lower level, having a priority weightage of 2.8%. Since herding is influenced by other factors that lead individuals to herd, therefore focusing on it is important for investors to wisely understand and interpret information available on different platforms. While religiosity (F9) has the lowest rank and the least priority weightage of 1.9%.

6. Discussion and implications

Cryptocurrency has gained attention from researchers, investors and industry due to its exceptionally high returns (Sharma et al., 2024). The present study identifies the sentimental factors affecting cryptocurrency prices and uses ISM-MICMAC analysis to understand their interrelationship. ISM is used to study contextual relationships between identified sentimental factors with the help of existing literature and the opinions of the experts. MICMAC is applied to explore their dependency and driving powers. After analysis, results show factors’ dependency and driving power, their interaction and focus on variables that have an important role in decision-making. At last, the authors have applied the AHP technique to rank the identified factors according to their importance, based on experts’ opinions. Google Search Trend (F3) and herding (F8) are performance factors and are at the highest level. Then at the next level are linkage variables building a linkage between the highest and lowest level factors, which are, media coverage (F1), social media (F2) and celebrities (F4). Lastly, the strategic variables at the lowest level of the framework are crucial, particularly in policy formulation and lay the basis for performance variables which are pandemic (F6), economic uncertainty (F7), war (F5) and religiosity (F9). Implementing strategies that consider all these variables can lead to needed results. Results show that the pandemic (F6) is a crucial strategic independent factor that has the highest level of dependency and driving powers leading to the next level factor of economic uncertainty (F7). The effect of external factors on the cryptocurrency market is intricate and multifaceted. The pandemic has significantly influenced the cryptocurrency market (Polat and Kabakçı Günay, 2021). Heightened media coverage surrounding COVID-19 has shaped investor perceptions and risk appetites, contributing to shifts in cryptocurrency prices (Chen et al., 2022). Thus, economic uncertainty influenced by global events and religious considerations can drive individuals to perceive cryptocurrencies as safe havens (Bouri et al., 2017). Mansour and Jlassi (2014) identified religious beliefs play a crucial role in influencing financial decision-making and risk perceptions. Media coverage (F1), social media (F2) and celebrities (F4) have moderate driving and dependence powers. They are affected by strategic factors pandemic (F6), economic uncertainty (F7), war (F5) and religiosity (F9) and will affect performance factors Herding (F8) and Google Search Trend (F3). Sentiments from media coverage (F1), social media (F2) and celebrities (F4) are pivotal components in this dynamics. Media, including traditional news outlets and social media platforms like Twitter, shape public perception and market sentiment (Drus and Khalid, 2019). News, influential tweets and celebrity endorsements can create market sentiment, driving increased interest and investment. This collective influence of sentiments influenced by Twitter, news and celebrities can drive individuals to seek further details online (Ripberger, 2011) and contribute to herding behaviour in the cryptocurrency market. According to the herding theory, herding occurs when investors follow the crowd rather than making independent decisions (Spyrou, 2013). The information and sentiments shared on Twitter and in news articles, particularly when endorsed or commented on by celebrities, can create a herd mentality among investors. The relationship of identified factors connects to Google search trends, which can be influenced by the collective sentiments expressed on Twitter, in the news and by celebrities. As herding behaviour intensifies, there is likely to be an increased interest and searches for cryptocurrency-related information on Google. Google Search Trends reflect the evolving sentiments within the market, capturing the dynamics influenced by the interconnected factors at play. The formulated model shows that all sentimental factors are interrelated based on dependency and driving powers, thus investors should focus on the sentiments floated on various platforms for wise decisions. As a result, looking at the extremely dynamic nature of the cryptocurrency market, this article examines sentimental factors influencing cryptocurrency prices and contributes significantly to literature and society by motivating people to make investments wisely and by considering all possible available information.

The study has various practical and theoretical implications. Firstly, the study examines existing literature and identifies nine sentimental factors, then applies ISM to highlight the hierarchical structure of sentimental factors influencing cryptocurrency pricing. The quantitative relationship between factors and cryptocurrency has been studied in literature, but the topic still needs to be covered from qualitative aspects. The existing literature from a methodological point of view has adopted structural equation modelling, multiple regression and financial modelling. To identify the relationship between sentimental factors affecting cryptocurrency prices, to the best knowledge of the authors, this study is the first of its kind which has segregated the sentimental factors, developed the hierarchical structure and allocated ranking using the ISM-MICMAC and AHP techniques. The study has identified the factors affecting cryptocurrency prices, explored their interrelationship and allocated ranking to the identified sentimental factors. The findings will assist stakeholders in the cryptocurrency ecosystem in numerous ways. For investors, the insights from the research offer a valuable tool for informed decision-making. Understanding the hierarchy and interplay of these factors will allow investors to anticipate market trends, identify risks and strategically position their portfolios (Inci and Lagasse, 2019). Additionally, the study provides a structured framework for evaluating factors, enabling investors to develop effective risk management strategies (Field and Inci, 2023), particularly during geopolitical uncertainty or global pandemics. Knowledge of critical factors also aids in crafting diversification strategies tailored to the cryptocurrency market dynamics. Policymakers can leverage these findings for regulatory insights, gaining a deeper understanding of the factors influencing cryptocurrency. This knowledge informs the development of targeted regulatory frameworks, fostering a more stable market environment. Policymakers can anticipate potential market impacts and proactively manage reactions to protect investors during crises, such as geopolitical conflicts or pandemics. The study’s comprehensive understanding of cryptocurrency dynamics contributes to a more resilient and informed ecosystem, enhancing stakeholder decision-making processes.

7. Conclusion and future research

This study has delved into the cryptocurrency market’s complex and multifaceted landscape, aiming to unravel the crucial sentimental factors affecting cryptocurrency prices and their intricate interplay. The article contends that there are many crucial sentimental factors influencing cryptocurrency prices that cannot be overlooked and states practical ways for implementation. The study has identified nine sentimental factors affecting cryptocurrency prices. By employing ISM-MICMAC and AHP techniques, authors have gained a deeper understanding of the relationships and hierarchy among these factors. The application of ISM, coupled with MICMAC analysis, has enabled a nuanced exploration of the driving and dependent powers of the identified factors. The study has divided the identified factors into dependent, linkage and independent variables based on their connections, as discussed in the earlier section, to provide information to the stakeholders. Pandemic (F6) is the fifth-level independent factor and economic uncertainty (F7) is at the fourth level. Religiosity (F9) and war (F5) are also the independent variables at the third level. Media coverage (F1), social media (F2) and celebrities (F4) are the linkage factors at level II. According to the herding theory, people follow the crowd, and thus these linkage variables play an important role in connecting the above-stated independent factors to first-level factors (Spyrou, 2013). Google Search Trend (F3) and hearding (F8) are at level I. Heuristic theory states investors, especially when faced with uncertainty, rely on cognitive shortcuts or rules of thumb to make financial decisions (Baker and Nofsinger, 2010). These heuristics reduce the complexity of analysing all available data, which speeds up analysis and simplifies decision-making. These unsophisticated noise traders in the cryptocurrency market are highly susceptible to the expectations and behaviours of others, often resulting in “herding behaviour”. Consequently, their decisions are frequently guided by heuristics rather than thorough assessments. These sentimental factors interact in complex ways, often leading to herding behaviour among investors, particularly during heightened uncertainty. Additionally, Google Search Trends reflect evolving market sentiments, highlighting that these interconnected sentimental factors influence cryptocurrency prices. The above findings shed light on the most influential sentimental factors shaping cryptocurrency prices, providing valuable insights for market participants, investors and policymakers. As the cryptocurrency market evolves, this study offers and contributes to the ongoing discourse and comprehension of the factors steering its dynamics. It provides a foundation for informed decision-making in this rapidly changing landscape.

While this study on the factors impacting cryptocurrency provides valuable insights, the reliance on expert opinions for constructing the ISM matrix introduces subjectivity and variations in expert perspectives may influence the model outcomes. The questionnaire bias and experts’ subjectivity in their replies may have impacted the results. Researchers benefit from the study’s invitation to further explore specific relationships and dynamics between identified factors. Further exploration can be done using quantitative techniques. Adopting primary data and questionnaires for analysing individual cryptocurrencies can provide valuable insights. Future studies can use structural equation modelling (SEM) to validate the developed model. This study uses ISM-MICMAC and AHP techniques, which in future studies can be combined with SEM. Future researchers can also apply the DEMATEL technique to investigate the interrelationship. Additionally, the study predominantly considers external drivers and future research could delve into internal factors within the cryptocurrency ecosystem. Exploring regional variations in the impact of factors and considering the evolving regulatory landscape are also avenues for future investigation.

Competing interests: No competing interest to declare.