This study investigates the impact of financial statements disclosed in accordance with the Turkish Tax Procedure Code (TPC) and International Financial Reporting Standards (IFRS) on stock prices at Borsa Istanbul. It aims to explore how each type of disclosure affects market reactions and the factors behind these responses.

We analyze cumulative abnormal returns (CAR) associated with mandatory TPC and subsequent IFRS disclosures using standard event study methodology. We also apply logistic regression analysis to identify the key factors driving these reactions, with a particular focus on the time lag between disclosures, which leads to information asymmetry.

The results indicate that mandatory TPC disclosures tend to elicit stronger negative market reactions, likely due to their tax-driven nature and limited informational value for investors. In contrast, IFRS disclosures help to reverse this negative reaction, making abnormal returns less negative and, in some cases, even positive. Furthermore, longer time lags between TPC and IFRS disclosures intensify negative market reactions, highlighting the role of information asymmetry.

This study offers new insights into how the dual-reporting system in Türkiye influences investor behavior, an area that has not been explored in the literature. By examining both the timing and content of disclosures, the findings provide valuable implications for investors, firms and regulators to better understand how financial reporting impacts market dynamics.

1. Introduction

Financial statements are a cornerstone of corporate communication, providing stakeholders with essential information to make informed decisions. For investors, these documents are particularly crucial as they offer insights into a company’s financial health, performance and future prospects (Kothari, 2001). The disclosure of high-quality and transparent financial reports is instrumental in mitigating information asymmetry between a company’s insiders and external investors, thus facilitating a more effective allocation of resources (Biddle et al., 2009). By narrowing the information gap between informed and uninformed market participants, it enhances investor confidence, leading to a lower cost of capital as firms with sound disclosure practices are perceived as less risky (Diamond and Verrecchia, 1991; Botosan, 1997; Easley and O’hara, 2004).

Since financial reporting is a primary mechanism for reducing information asymmetry, it plays a fundamental role in the proper functioning of efficient capital markets (Healy and Palepu, 2001). The extent to which corporate financial disclosures shape market behavior and asset prices is, therefore, best understood through the lens of the Efficient Market Hypothesis (EMH), which postulates that asset prices fully reflect all available information (Fama, 1970; Emery, 1974). The EMH classifies market efficiency into three forms: weak, semi-strong and strong. The weak form of efficiency assumes that stock prices reflect all historical market data, rendering technical analysis ineffective. The semi-strong form of efficiency assumes that stock prices adjust immediately to publicly available information. The strong form of efficiency holds that asset prices also contain private information, which prevents even insiders from consistently earning abnormal returns.

Given that financial reports constitute a main source of publicly available information, their impact on market efficiency is most directly aligned with the principles of semi-strong efficiency. In semi-strong efficient markets, stock prices are expected to respond quickly to financial report releases, ensuring that no investor systematically earns excess returns by analyzing the financial information published (Aggrawal and Agarwal, 2023). What happens, however, when multiple reporting regimes coexist, each with different disclosure timelines? The interaction between varying reporting standards and staggered release schedules raises critical questions about how efficiently markets process and incorporate financial information. Prior studies suggest that a fragmented approach in financial reporting standards (Barradale et al., 2022) and differences in the timing of disclosure (Chambers and Penman, 1984; Atiase et al., 1989) introduce information asymmetries that may distort market efficiency. Beyond regulatory differences, the way in which financial information is presented also significantly influences investor perceptions and market reactions (Elliott et al., 2015; Lachmann et al., 2015). Research reveals that investors do not process all financial information equally; they tend to fixate on salient figures such as earnings and headline financial metrics while underweighting other relevant data (Maines and McDaniel, 2000; Hirst and Hopkins, 1998). This selective attention, driven by cognitive constraints and bounded rationality, may exacerbate market inefficiencies, especially in an environment where multiple reporting standards operate in tandem (Elliott et al., 2011). Accordingly, it is plausible to presume that differences in financial reporting standards and the way information is presented are likely to yield diverse effects on market behavior.

Against this backdrop, Türkiye represents a special case in financial reporting due to its dual disclosure system, as listed companies are required to prepare two separate sets of financial statements: one in accordance with the Turkish Tax Procedure Code (TPC) and one in accordance with International Financial Reporting Standards (IFRS). The financial statements based on TPC are primarily for tax compliance and follow conservative accounting principles, where prudence often takes precedence over economic presentation. IFRS, on the other hand, provides a globally accepted, investor-oriented framework that emphasizes transparency, comparability and fair value measurement (Joos and Leung, 2013). This duality in reporting requirements leads to discrepancies in financial reporting and thus to potential confusion among investors and information asymmetries in the capital markets. The timing of financial disclosures adds another layer of complexity to investor decision-making. Although both TPC and IFRS reports are required, they are published at different intervals, with TPC reports disclosed first, preceding IFRS reports, creating a timing gap that affects investor reactions. This staggered disclosure process can create uncertainty, particularly for less-informed investors, as it may temporarily impede perceptions of a company’s financial position. To elucidate these issues, this study explores the following research question: “How does the disclosure of TPC and IFRS financial statements impact stock price movements in Turkish capital markets?”

To this end, we adopt a two-step empirical approach. First, we employ an event study methodology to analyze the abnormal stock returns surrounding the announcements of TPC and IFRS financial statements. This allows us to capture the short-term market reaction to each type of disclosure and determine whether investors perceive one reporting framework as more informative than the other. The findings reveal that mandatory TPC disclosures typically elicit negative abnormal returns, suggesting that tax-based financial statements may not provide sufficient transparency to investors. In contrast, IFRS disclosures reverse this investor response, reinforcing the notion that investors view IFRS reports as more reliable indicators of firms' financial health. Second, we apply logistic regression analysis to examine the factors influencing the likelihood of a favorable market reaction to IFRS over TPC disclosures, with a particular focus on information asymmetry. The results indicate that heightened information asymmetry substantially reduces the probability of a favorable market reaction to IFRS statements, while certain firm-specific characteristics also exert notable influence.

This study contributes to the literature in the following ways. First, it extends the literature on the impact of mandatory tax disclosure on investor behavior. We do so by examining the market reaction to the disclosure of tax-based financial statements. While the effect of tax disclosure depends on the institutional details and specific requirements of the disclosure mandate (Hoopes et al., 2024), we provide direct evidence from the marketplace to evaluate the success of the disclosure regime. More importantly, this study fills a critical research gap by providing the first comprehensive analysis of how a dual financial reporting system affects stock prices. It not only offers valuable insights into the intersection of financial reporting and market efficiency but also advances the understanding of the potential effects of reporting systems on investor decision-making and market dynamics in an emerging market setting. Further, this study introduces a novel two-step empirical approach that integrates event study methodology with logistic regression analysis. This combination allows for a systematic comparison of market reactions to different types of financial disclosures, distinguishing not only the immediate impact on stock prices but also the underlying factors—particularly information asymmetry—that drive differential investor responses. Unlike traditional event studies that focus exclusively on short-term price reactions, our approach incorporates a comparative approach, shedding light on the channels by which reporting standards influence investor confidence.

The remainder of the study is structured as follows: Section 2 reviews the literature, outlines the motivational background and develops the research hypotheses. Section 3 describes the data sources and methodology. Section 4 provides a detailed analysis of the main findings, while Section 5 concludes with practical implications and avenues for future research.

2. Literature review, motivational background and hypothesis development

2.1 Prior research

This study is positioned at the intersection of two key strands of financial reporting literature: (1) the effects of tax reporting on investor sentiment and equity prices, and (2) the impact of IFRS reporting on market reactions and investment decisions.

Research on corporate tax disclosure corresponds to the first strand. Lenter et al. (2003) suggest that disclosures deter tax evasion and enhance market efficiency, yet Hoopes et al. (2018) find that when mandated, they often trigger negative investor reactions due to regulatory scrutiny. Conversely, Huesecken et al. (2018) observe positive returns following unintended disclosures of tax avoidance, highlighting investor preference for certainty. Luo et al. (2024) demonstrate that detailed tax footnotes improve market valuation of tax avoidance by mitigating agency risks and increasing transparency. Investor characteristics also shape these effects. Genest and Wu (2022) find that less sophisticated investors misinterpret tax disclosures, leading to market disparities, whereas Khan et al. (2017) associate higher institutional ownership with increased tax evasion, implying strategic use of tax information. Industry and country-specific contexts also matter. Dutt et al. (2019) report neutral investor reactions to EU country-by-country tax disclosures. However, Müller et al. (2024) document a consistently negative reaction to these disclosures driven by concerns over proprietary costs associated with revealing sensitive business information. Interestingly, Kays (2022) finds that voluntary tax disclosures can counterbalance proprietary costs and attract positive market reactions. Allen and Uysal (2023) show that mandatory tax disclosure narrows the gap between reported and actual profits, improving transparency in Türkiye. In contrast, Hasegawa et al. (2013) find that ending mandatory tax disclosure in Japan had no effect on reported tax revenues, suggesting that disclosure mandates do not always alter firm behavior. Regulatory settings influence corporate tax strategies as well. Blank (2014) argues that tax secrecy may reduce managerial pressure but can encourage aggressive tax planning. However, it is important to recognize that tax aggressiveness is a corporate social responsibility issue. As Zeng (2016) suggests, firms that exhibit lower commitment to social responsibility are more inclined to engage in aggressive tax activities. De Vito et al. (2023) find that profit-taking taxes on banks led to negative market reactions, while Song et al. (2024) report that FIN 48 tax disclosures reduced the tax expense anomaly without improving predictability. Finally, firms adjust tax strategies based on disclosure policies. Donohoe and Gill (2011) reveal shifts in tax planning pre- and post-Schedule M-3 disclosure and Demeré (2023) finds that investors value tax disclosure more after syndicated loans, underscoring their growing role in financial decision-making. All these studies suggest that evaluating the impact of tax disclosure is essential for weighing its advantages and drawbacks as a regulatory mechanism (Hoopes et al., 2024).

Within the second strand of the literature, the potential impact of IFRS-based financial statements on investment behavior can be better grasped by considering previous research on the market reaction to IFRS adoption. Existing studies demonstrate that the response of the market to IFRS adoption is largely positive as investors perceive the benefits of harmonized accounting standards. Brüggenmann et al. (2013) investigate how individual investors react to IFRS adoption globally, suggesting that transparency improvements leads to increased investor confidence. Research on European markets reveals that IFRS adoption generally results in positive market reactions, particularly for firms with greater transparency and high-quality financial disclosures. Armstrong et al. (2010) examine market-adjusted returns for European firms and find that the IFRS adoption process has a significant market impact. Similarly, Christensen et al. (2009) and Horton and Serafeim (2010) assess IFRS reconciliation adjustments in the UK, providing evidence that the new standards are perceived as value-relevant by investors. By contrast, market reaction in the US is rather ambivalent. Joos and Leung (2013) study US investor sentiment surrounding key IFRS adoption events and find mixed reactions. Investors express skepticism regarding IFRS convergence, given the dominance of US GAAP. That said, Prather-Kinsey and Tanyi (2014) find a significant and positive market reaction to SEC announcements regarding potential IFRS adoption, indicating investor optimism about the transition to IFRS. The market reaction to IFRS is also shaped by the financial maturity of a country and the type of investors. For instance, a study by Klimczak (2011) on the mandatory IFRS adoption of Poland as an emerging economy provides no evidence of an abnormal reaction at the time of first IFRS statement publications. Florou and Pope (2012), however, show that demand from institutional investors, especially those with active, value-oriented and growth strategies, has grown post-IFRS adoption. Overall, while investor perceptions appear to vary depending on the context, it would not be a false assertion that IFRS adoption generally enhances the relevance of accounting elements, increases transparency, reduces the cost of capital and improves investment efficiency (De George et al., 2016).

2.2 Research gap and motivation

Despite extensive research on tax and IFRS reporting that paints a nuanced picture of their effect on investor behavior, prior studies have largely examined these topics in isolation. The literature on IFRS reporting highlights its role in enhancing financial transparency, investor confidence and market efficiency, with variations depending on jurisdiction and investor sophistication. Meanwhile, research on corporate tax disclosures presents a more complex pattern, showing that while transparency can deter tax avoidance, it also elicits mixed investor reactions due to concerns over regulatory scrutiny and proprietary costs. However, the interplay between IFRS- and tax-based financial reporting remains underexplored, particularly in markets with dual-reporting regimes. Table 1 provides a structured summary of existing research and gaps.

Summary of literature and identified research gaps

| Research area | Key findings in literature | Research gap |

|---|---|---|

| IFRS reporting | Enhances transparency, lowers capital costs, increases investment efficiency (Brüggenmann et al., 2013; Armstrong et al., 2010; Horton and Serafeim, 2010) | Prior studies focus on jurisdictions with a single reporting standard; little is known about the effects of IFRS in dual-reporting markets |

| Corporate tax reporting | Can reduce tax evasion and increase transparency but may also trigger negative investor reactions due to regulatory scrutiny (Hoopes et al., 2018; Luo et al., 2024; Genest and Wu, 2022) | Studies primarily analyze single-reporting contexts, overlooking how tax disclosures interact with corresponding IFRS reports |

| Dual-reporting systems | Limited empirical research on markets requiring both tax-based and IFRS financial statements (Allen and Uysal, 2023) | No comprehensive study has assessed how the disclosure process of tax and IFRS reports influences investor behavior |

Note(s): This table provides the justification of the research gap

Source(s): Authors’ own work

In this context, Türkiye presents a unique setting to address the research gap. The country’s dual financial reporting regime is the result of both domestic regulatory requirements and international accounting harmonization efforts. Listed companies have been mandated to adopt IFRS for over 2 decades to align with European Union regulations and global reporting standards (Simga-Mugan and Hosal-Akman, 2005). However, for tax compliance, firms must also prepare financial statements under TPC, which follows a conservative, tax-oriented accounting approach. While this duality allows companies to fulfill both domestic and international reporting obligations, it introduces significant challenges. For example, TPC-based statements prioritize tax compliance, often applying conservative asset valuation techniques for tangible and intangible assets (e.g. real estate, goodwill). In contrast, IFRS places greater emphasis on fair value measurement, offering investors a more transparent and comprehensive view of a firm’s financial position (Karapinar et al., 2012; Balsari and Varan, 2014; Bahadır et al., 2016). Additionally, differences extend to liability recognition, depreciation methods and financial asset classification, creating substantial inconsistencies between the two reporting frameworks.

Complicating this further, the Capital Markets Board—Türkiye’s primary regulatory authority overseeing capital markets—mandates the sequential disclosure of these statements. Specifically, TPC-based financial statements must be released before IFRS reports, as they are classified as a material event requiring immediate public disclosure. This is reasonable as such disclosures may equip market participants with essential information to evaluate the firm’s future cash flows in terms of amount, timing and uncertainty. However, this regulatory structure raises a crucial information asymmetry problem, as investors are initially exposed to tax-based financial data, which may not fully reflect a firm’s true financial health. Only later, when IFRS-compliant statements are published, is more comprehensive and internationally standardized financial information available. The fragmented regulatory approach followed by this staggered disclosure process motivates a systematic investigation into how Türkiye’s dual-reporting system affects stock price movements.

2.3 Hypothesis Development

Given the concerns surrounding market efficiency and investor asymmetry, we propose the following hypotheses:

Investor reactions differ significantly between TPC-based and IFRS-based financial disclosures, with IFRS reports eliciting stronger positive market responses.

Information asymmetry driven by the staggered disclosure practice leads to significant differentials in stock price reactions.

3. Data and methodology

3.1 Data

Our sample is drawn from the XU100 index, which represents 76% of the weighted free float market value as of 2022 years-end. The estimation sample therefore consists of 100 firms, but we construct our final sample by selecting only those with complete stock price and financial statement data for the period 2010–2022. After applying this criterion, the final dataset comprises 65 firms across manufacturing (30), financials (20) and other industries (15). The sample period begins in 2010, coinciding with the first TPC annual financial disclosures. We exclude years beyond 2022 due to the introduction of inflation accounting in financial statements, which could distort market reactions and hinder comparability. Not all firms provide TPC financial statements consistently across the period, resulting in 415 firm-year observations instead of the potential 845 (65 firms × 13 years). This sampling procedure is illustrated in Table 2.

Sample selection procedure

| Selection criteria | # of firms | # of obs |

|---|---|---|

| Initial firms/obs. in the XU100 Index | 100 | 1,300 (100 firms × 13 years) |

| Firms/obs. with incomplete data | −35 | −455 |

| Final sample of firms/obs | 65 | 845 |

| Firms/obs. with missing TPC disclosures | – | −430 |

| Final firms/obs. used | 65 | 415 |

Note(s): This table depicts the sample selection procedure

Source(s): Authors’ own work

Table 3 provides an overview of the summary statistics for the data used in our empirical framework, all from the Eikon database. Panel A shows that negative stock reactions to TPC disclosures (TPC CAR (0,20)) are reversed following IFRS announcements (IFRS CAR (0,20)), suggesting IFRS disclosures mitigate prior uncertainty. Since the IFRS pre-announcement window (IFRS CAR (−20,−1)) overlaps with the post-TPC window, the IFRS release appears to be a corrective mechanism. The summary statistics of firm characteristics in Panel B highlight substantial heterogeneity in company size, industry distribution and financial health. Notably, the average (median) time lag between TPC and IFRS reports is 19.59 (17.00) days, which is a considerable amount of time that could influence the incorporation of new financial information into stock prices.

Descriptive statistics (n:415)

| Data | Mean | Median | St. Dev | Min | Max |

|---|---|---|---|---|---|

| Panel A: Cumulative abnormal returns (CAR) | |||||

| IFRS CAR (−20,−1) (%) | −1.97 | −1.78 | 10.64 | −61.14 | 55.12 |

| TPC CAR (−20,−1) (%) | −0.21 | −1.26 | 11.15 | −39.59 | 75.53 |

| IFRS CAR (0,20) (%) | −0.90 | −0.46 | 12.58 | −61.89 | 74.84 |

| TPC CAR (0,20) (%) | −2.17 | −1.97 | 12.70 | −47.70 | 76.86 |

| Panel B: Model variables | |||||

| Total Assets (billion TRY) | 29.69 | 6.88 | 76.26 | 0.06 | 819.76 |

| Total Debt (billion TRY) | 8.11 | 1.77 | 22.44 | 0.00 | 262.37 |

| Total PPE (billion TRY) | 12.21 | 2.33 | 43.86 | 0.00 | 605.15 |

| Total Intangibles (billion TRY) | 1.38 | 0.09 | 6.81 | 0.00 | 112.37 |

| Market Cap (billion TRY) | 9.45 | 3.79 | 18.04 | 0.12 | 198.84 |

| ROA (%) | 7.60 | 5.63 | 10.60 | −22.44 | 65.83 |

| Tobin’s Q | 1.05 | 0.54 | 1.88 | 0.03 | 22.56 |

| IFRS-TPC time lag (days) | 19.59 | 17.00 | 13.36 | 1.00 | 104.00 |

Note(s): This table presents descriptive statistics of the data used in the study

Source(s): Authors’ own work

3.2 Methodology

3.2.1 Event study analysis

To assess the market response to TPC and IFRS disclosures, we employ a standard event study methodology, which allows us to capture their short-term stock price effects (H1). By measuring abnormal returns, we examine how investors react to the release of financial statements under these two distinct reporting frameworks. Abnormal returns (ARit) are defined in Eq. (1) as the difference between realized returns (Rit) and expected returns (ERit), calculated using a market model in Eq. (2):

Rit represents the return of stock i (e.g. a firm) on day t, while Rmt denotes the return of the market on the same day. The error term is a random variable with zero mean and finite variance, assumed to be uncorrelated with both market returns (Rmt) and other firm returns (Rjt, where i≠j). It is also assumed to be non-autocorrelated and homoskedastic. The coefficient measures the sensitivity of stock i’s return to the market.

Defining estimation and event windows is critical in event studies to isolate the market impact of financial disclosures. The estimation window establishes expected stock price behavior before the event, while the event window captures investor reactions. Following Armitage (1995) and Peterson (1989), we adopt a 100-day estimation window [−110, −11] and a 21-day event window [−10, +10], which includes the pre-event period [−10, −1], event day [0] and post-event period [+1, +10] (Basdas and Oran, 2014).

In the estimation window, we regress stock returns (Rit) on market portfolio returns (Rmt) to estimate expected returns (ERit) using α and β coefficients. Abnormal returns are then calculated by subtracting expected returns from realized returns. We use the XU100 market portfolio as a benchmark, with returns calculated as the percentage change between consecutive closing prices. CARs are obtained by summing the abnormal returns over the event window, providing an overall measure of the event’s impact, as follows:

To evaluate significance, we compute average cumulative abnormal returns (CAR) and apply parametric tests including the standard t-test and the Boehmer, Musumeci and Poulsen (BMP) test (Boehmer et al., 1991), which adjusts for event-related variance. Given the wide variation in the sample abnormal returns (see Panel A in Table 3), we also employ non-parametric tests to account for potential outliers. Non-parametric tests, KP and GRANK, from Kolari and Pynnönen (2010, 2011), account for cross-correlation and event clustering without assuming a normal distribution, making them robust to event-induced variance.

For robustness, we take into account the heterogeneity in the data and apply the event study analysis for relevant sub-samples. We also perform a comparative analysis of investor reactions to IFRS and TPC financial statements with tests of differences in means in order to provide further support for our hypotheses.

3.2.2 Logistic regression analysis

Following the event study, we conduct logistic regression to examine the factors influencing investor reactions to IFRS and TPC disclosures. This method estimates the probability that market reactions to IFRS disclosures are more favorable than those to TPC reports, allowing for a detailed comparison of how differences in financial disclosure timing and transparency influence stock price adjustments (H2).

Given their distinct bases of principles, investors may react differently to IFRS and TPC disclosures. To quantify this, we use the IFRS-TPC CAR differential as our dependent variable. A positive CAR differential suggests that TPC disclosures may not fully meet investor expectations, potentially signaling information asymmetry. Our method of measurement borrows from Mian and Sankaraguruswamy (2012), who define their dependent variable as the difference between the returns of high-news and low-news stocks to gauge the differential impact of market sentiment. In our setting, the dependent variable is binary, coded as 1 if the IFRS-TPC CAR differential is positive—indicating a more favorable market reaction to IFRS disclosures—and 0 otherwise. By doing so, our model compares the effects of transparency and conservatism in financial reporting on investor behavior.

To determine the independent variables influencing the IFRS-TPC CAR differential, our model incorporates key firm characteristics including firm size (Bamber, 1987), leverage (Dhaliwal et al., 1991), profitability and growth opportunities (Humphery-Jenner and Powell, 2011). Additionally, relying on our heuristic analysis, the time gap between IFRS and TPC announcements is added to measure information asymmetry (Yılmaz et al., 2020). We include a dummy variable to control for consolidated reporting requirements, as IFRS consolidation practices do not impact tax collection, potentially influencing investor sentiment. Finally, we account for differences in asset classification, particularly in property, plant and equipment and intangible assets, which may contribute to variations in investor perception.

We formulate the regression model as follows:

In Eq. (4), greater information asymmetry, reflected in a longer delay between TPC and IFRS disclosures, can prolong negative sentiment, reducing the likelihood of a positive IFRS-TPC CAR differential. Consolidated financial statements may mitigate this by improving transparency, leading to a more favorable market reaction to IFRS disclosures. Larger firms typically experience lower information asymmetry, raising the likelihood of a positive IFRS-TPC CAR differential. Leverage clarity in IFRS reports can improve investor sentiment, while higher profitability (ROA) and growth potential (Tobin’s Q) increase the probability of a positive CAR differential. Differences in IFRS and TPC accounting for PPE can create valuation uncertainty, while high intangible assets may reduce transparency, both potentially lowering investor confidence in IFRS reports. Variable definitions are provided in Table 4.

Variable definitions

| Variables | Definition | Expected sign |

|---|---|---|

| Dependent | ||

| CARIFRS-TPCi | The probability that the CAR difference between IFRS and TPC announcements for the specified event windows is positive (1 if positive, 0 otherwise) | |

| Independent | ||

| Asymi | Time lag between IFRS-TPC announcements (days) | – |

| Consi | Requirement to prepare consolidated financial statements (1 if mandatory, 0 otherwise) | + |

| Sizei | Total assets (in logarithmic form) | + |

| Levi | Total debt/Total assets | + |

| Profi | Return on assets (ROA) | + |

| Growi | Tobin’s Q = Market cap/Total assets | + |

| PPEi | Property, Plant, and Equipment/Total assets | – |

| INTGi | Intangible assets/Total assets | – |

Note(s): This table presents the definitions of variables used in the logistic regression analysis along with the expected signs of each variable of interest

Source(s): Authors’ own work

4. Results and discussion

4.1 Event study analysis

4.1.1 Main results

Table 5 presents the results of the event study, capturing short-term investor reactions to TPC and IFRS disclosures.

Market reaction to the announcements of financial reports (Entire Sample, n:415)

| Date | CAR (%) | Pos:Neg | t-test Prob | BMP | Prob | KP | Prob | GRANK | Prob |

|---|---|---|---|---|---|---|---|---|---|

| Panel A: TPC financial statements | |||||||||

| (−20,20) | −1.28 | 164:251 | 0.1153 | −1.50 | 0.1347 | −1.11 | 0.2679 | −1.60 | 0.1130 |

| (−10,10) | −0.85 | 172:243 | 0.1099 | −0.99 | 0.3206 | −0.74 | 0.4619 | −1.34 | 0.1847 |

| (−5,5) | −0.97 | 168:247 | 0.0096*** | −1.57 | 0.1176 | −1.16 | 0.2464 | −1.45 | 0.1516 |

| (−3,3) | −0.81 | 165:250 | 0.0058*** | −1.92 | 0.0555* | −1.42 | 0.1560 | −1.55 | 0.1254 |

| (−2,2) | −0.44 | 169:246 | 0.0686* | −1.38 | 0.1668 | −1.02 | 0.3059 | −0.86 | 0.3933 |

| (−1,1) | −0.34 | 177:238 | 0.0709* | −1.66 | 0.0965* | −1.23 | 0.3455 | −0.95 | 0.1130 |

| (0,10) | −0.16 | 185:230 | 0.6659 | 0.31 | 0.7588 | 0.23 | 0.8201 | −0.04 | 0.9675 |

| (0,5) | −0.32 | 186:229 | 0.6501 | −0.45 | 0.7369 | −0.34 | 0.2679 | −0.76 | 0.4500 |

| (0,3) | −0.56 | 168:247 | 0.0096*** | −2.29 | 0.0218** | −1.70 | 0.0893* | −1.87 | 0.0640* |

| (0,20) | −1.55 | 173:242 | 0.0047*** | −2.01 | 0.0447** | −1.49 | 0.1371 | −1.59 | 0.1143 |

| (12,20) | −1.63 | 164:251 | 0.0000*** | −4.09 | 0.0000*** | −3.03 | 0.0025*** | −2.43 | 0.0169** |

| (−5,20) | −2.20 | 156:259 | 0.0005*** | −2.62 | 0.0088*** | −1.94 | 0.0522* | −2.43 | 0.0168** |

| (−7,20) | −2.55 | 152:263 | 0.0001*** | −3.17 | 0.0016*** | −2.34 | 0.0191** | −3.06 | 0.0028*** |

| Panel B: IFRS financial statements | |||||||||

| (−20,20) | −1.76 | 170:245 | 0.0340** | −1.72 | 0.0863* | −1.60 | 0.1103 | −2.23 | 0.0283** |

| (−10,10) | −1.26 | 161:254 | 0.0218** | −1.29 | 0.1967 | −1.20 | 0.2294 | −1.92 | 0.0578* |

| (−5,5) | −1.29 | 169:246 | 0.0008*** | −2.05 | 0.0401** | −1.91 | 0.0560* | −2.00 | 0.0488** |

| (−3,3) | −1.20 | 162:253 | 0.0001*** | −2.41 | 0.0158** | −2.25 | 0.0246** | −2.81 | 0.0060*** |

| (−2,2) | −1.18 | 160:255 | 0.000*** | −3.21 | 0.0013*** | −2.99 | 0.0028*** | −2.99 | 0.0035*** |

| (−1,1) | −0.68 | 168:247 | 0.0004*** | −2.52 | 0.0118** | −2.35 | 0.0190** | −2.40 | 0.0185** |

| (0,10) | −0.89 | 183:232 | 0.0194** | −1.39 | 0.1646 | −1.29 | 0.1957 | −1.41 | 0.1609 |

| (0,5) | −1.23 | 171:244 | 0.0000*** | −3.15 | 0.0017*** | −2.93 | 0.0034** | −2.84 | 0.0055*** |

| (0,3) | −1.04 | 153:262 | 0.0000*** | −3.26 | 0.0011*** | −3.04 | 0.0024** | −3.21 | 0.0018*** |

| (0,20) | −0.28 | 194:221 | 0.6094 | −0.16 | 0.8718 | −0.15 | 0.8806 | 0.12 | 0.9077 |

| (12,20) | 0.55 | 207:208 | 0.1065 | 1.61 | 0.1077 | 1.50 | 0.1342 | 2.13 | 0.0359** |

| (−5,20) | −0.34 | 189:226 | 0.5808 | 0.11 | 0.9150 | 0.10 | 0.9209 | −0.41 | 0.9968 |

| (−7,20) | −0.41 | 186:229 | 0.5242 | 0.11 | 0.9168 | 0.10 | 0.9225 | 0.04 | 0.9709 |

Note(s): This table presents the event study results corresponding to the market reaction to the disclosure of TPC and IFRS financial statements. CAR is average cumulative abnormal returns. Standard t-test and the BMP test are parametric tests, while KP and GRANK are non-parametric tests. ***, **, and * denote 1%, 5%, and 10% significance levels, respectively

Source(s): Authors’ own work

In Panel A, the findings indicate a persistent negative abnormal return pattern, with declines starting before the official disclosure date. Notably, investors begin reacting negatively as early as five days prior to the TPC announcements, suggesting anticipation of adverse information. The most significant declines occur in (0, 20), (12, 20), (−5, 20) and (−7, 20) event windows, with CAR ranging between −1.55% and −2.55%. This reaction is likely driven by the conservative and tax-driven nature of TPC financial statements. Compared to IFRS, TPC-based financial reports lack investor-oriented disclosures and may provide a less optimistic representation of firm performance, which may even be due to an expected political backlash, i.e. changes in tax rules or regulation. These results align with previous research suggesting that mandatory tax disclosure can negatively influence market anticipations (Johannesen and Larsen, 2016; Hoopes et al., 2018). Furthermore, the persistence of negative CAR in wider event windows (−7, 20) and (−5, 20) reinforces the idea that mandatory TPC disclosures amplify uncertainty rather than resolve it. This is consistent with Müller et al. (2024), who argue that the costs associated with corporate tax disclosure may outweigh the potential benefits of an improved information environment from an investor perspective, evidenced by persistently negative sentiment.

Results displayed in Panel B reveal a reversal of the negative abnormal returns observed after mandatory TPC disclosures. This suggests that IFRS statements provide investors with higher-quality information and reducing uncertainty. This pattern aligns with the broader literature demonstrating the positive effects of IFRS reporting on financial transparency, investor confidence and market efficiency (Florou and Pope, 2012; De George et al., 2016). Furthermore, the overlap between the IFRS pre-announcement window (−20, −1) and the post-TPC event window (0, 20) confirms that the market reaction is interconnected. Investors appear to correct their assessments following the IFRS disclosures, probably based on the income tax information presented (Graham et al., 2012), leading to positive price adjustments. This corroborates with prior research demonstrating that investors react more favorably to comprehensive financial reporting standards than to localized tax-based reporting systems (Christensen et al., 2009; Horton and Serafeim, 2010).

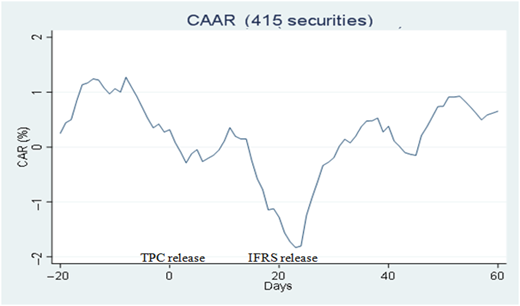

Taken together, our baseline results confirm H1. Figure 1 illustrates the combined investor reactions to the TPC and IFRS disclosures, clearly showing that the negative abnormal returns triggered by the TPC announcements begin to fade following the release of the IFRS financial statements.

A combined illustration of the market reactions to the announcements of TPC and IFRS financial statements. Source: Authors’ calculations

A combined illustration of the market reactions to the announcements of TPC and IFRS financial statements. Source: Authors’ calculations

4.1.2 Firm heterogeneity

We first examine differences in investor reactions between financial and non-financial firms. We then assess how the timing gap between TPC and IFRS disclosures influences abnormal stock price movements.

Panels A1 and A2 in Table 6 indicate that while investor reactions to IFRS disclosures remain largely similar across industries, mandatory TPC disclosures show significantly stronger negative responses for financial firms compared to non-financial firms. This discrepancy may be attributed to several factors. Financial firms operate under stricter regulatory and tax frameworks, which makes their financial disclosures subject to greater scrutiny. The conservative nature of TPC reports, with their tax-driven valuation methodologies, may amplify investor concerns in these firms, as tax obligations play a more critical role in shaping their financial performance. Additionally, financial firms typically have more complex financial structures, making their reporting less transparent. As a result, investors may perceive IFRS disclosures as more reliable, further intensifying the negative sentiment toward TPC announcements. These findings align with prior research suggesting that IFRS reports are generally considered more informative and value-relevant for financial firms (Abdallah et al., 2018) and reaffirms H1.

Market reaction to the announcements of TPC and IFRS financial statements (Different Subsamples)

| Date | Financial firms excluded (n = 283) | Financial firms only (n = 132) | High time lag between TPC-IFRS (n = 200) | Low time lag between TPC-IFRS (n = 215) | ||||

|---|---|---|---|---|---|---|---|---|

| CAR (%) | t-test Prob | CAR (%) | t-test Prob | CAR (%) | t-test Prob | CAR (%) | t-test Prob | |

| Panel A1: TPC financial statements (financial sector subsample) | Panel B1: TPC financial statements (time lag subsample) | |||||||

| (−20,20) | −1.18 | 0.2335 | −2.37 | 0.0901* | −1.73 | 0.1610 | −1.86 | 0.1016 |

| (−10,10) | −0.88 | 0.1765 | −1.30 | 0.1559 | −1.03 | 0.2015 | −1.55 | 0.0394** |

| (−5,5) | −0.68 | 0.1309 | −1.44 | 0.0247** | −1.23 | 0.0294** | −1.50 | 0.0044*** |

| (−3,3) | −0.84 | 0.0185** | −0.72 | 0.1453 | −1.00 | 0.0234** | −1.41 | 0.0006*** |

| (−2,2) | −0.54 | 0.0690* | −0.41 | 0.3263 | −0.39 | 0.2901 | −1.09 | 0.0016*** |

| (−1,1) | −0.45 | 0.0504* | −0.16 | 0.6134 | −0.26 | 0.3525 | −0.58 | 0.0257** |

| (0,10) | −0.23 | 0.6162 | −0.36 | 0.5747 | −0.04 | 0.9404 | −0.42 | 0.4147 |

| (0,5) | −0.26 | 0.4165 | −0.49 | 0.2895 | −0.27 | 0.5045 | −0.56 | 0.1336 |

| (0,3) | −0.75 | 0.0053*** | −0.39 | 0.2922 | −0.44 | 0.1799 | −0.92 | 0.0027*** |

| (0,20) | −1.67 | 0.0128** | −2.00 | 0.0325** | −1.75 | 0.0337** | −1.84 | 0.0159** |

| (12,20) | −1.66 | 0.0000*** | −1.95 | 0.0010*** | −1.82 | 0.0005*** | −1.73 | 0.0003*** |

| (−5,20) | −2.08 | 0.0061*** | −2.95 | 0.0057*** | −2.71 | 0.0041*** | −2.78 | 0.0015*** |

| (−7,20) | −2.65 | 0.0010*** | −3.05 | 0.0063*** | −2.92 | 0.0031*** | −3.16 | 0.0006*** |

| Panel A2: IFRS financial statements (financial sector subsample) | Panel B2: IFRS financial statements (time lag subsample) | |||||||

| (−20,20) | −1.83 | 0.0715* | −0.96 | 0.4959 | −2.86 | 0.0233** | −2.32 | 0.0425** |

| (−10,10) | −1.19 | 0.0773* | −1.01 | 0.2790 | −1.81 | 0.0312** | −1.87 | 0.0136** |

| (−5,5) | −1.32 | 0.0053*** | −1.17 | 0.0704* | −1.73 | 0.0031*** | −0.99 | 0.0558* |

| (−3,3) | −1.22 | 0.0010*** | −1.04 | 0.0395** | −1.97 | 0.0000*** | −0.78 | 0.0544* |

| (−2,2) | −1.17 | 0.0002*** | −1.12 | 0.0087*** | −1.68 | 0.0000*** | −0.54 | 0.1120 |

| (−1,1) | −0.66 | 0.0051*** | −0.69 | 0.0323** | −0.94 | 0.0014*** | −0.06 | 0.8311 |

| (0,10) | −0.71 | 0.1258 | −0.77 | 0.2360 | −0.98 | 0.0881* | −1.22 | 0.0200** |

| (0,5) | −0.98 | 0.0040*** | −1.33 | 0.0049*** | −1.35 | 0.0015*** | −0.81 | 0.0306** |

| (0,3) | −0.87 | 0.0015*** | −1.00 | 0.0085*** | −1.33 | 0.0001*** | −0.51 | 0.0880* |

| (0,20) | 0.11 | 0.8684 | −0.14 | 0.8837 | −0.67 | 0.4139 | −0.88 | 0.2422 |

| (12,20) | 0.78 | 0.0623* | 0.48 | 0.4106 | 0.28 | 0.5781 | 0.39 | 0.4059 |

| (−5,20) | −0.22 | 0.7679 | 0.02 | 0.9840 | −1.06 | 0.2593 | −1.07 | 0.2149 |

| (−7,20) | −0.16 | 0.8412 | −0.31 | 0.7786 | −1.13 | 0.2527 | −0.96 | 0.2842 |

Note(s): This table presents the event study results corresponding to the market reaction to the disclosure of TPC and IFRS financial statements based on different subsamples. CAR is average cumulative abnormal returns. ***, **, and * denote 1%, 5%, and 10% significance levels, respectively

Source(s): Authors’ own work

Further, Panels B1 and B2 offer insights into how the timing gap between TPC and IFRS disclosures affects market reactions. The sample is divided into two groups based on whether the time lag between TPC and IFRS disclosures is greater or less than the median of 17 days (see Table 3). The results indicate that companies with a shorter time lag experience more pronounced negative abnormal returns following mandatory TPC disclosures. This pattern suggests that uncertainty plays a crucial role in driving investor responses, as market participants anticipate the IFRS reports and may postpone their trading decisions until both sets of financial statements are available. Institutional investors, who can predict the sequencing of IFRS releases, may react by selling stocks immediately after TPC announcements and repurchasing them after IFRS disclosures to capitalize on valuation corrections. This implies that TPC reports may mislead less sophisticated investors, leading to premature trading decisions that are later reversed once IFRS statements provide a clearer financial picture. Conversely, firms that release IFRS statements later experience even stronger negative stock price reactions following TPC disclosures. A longer delay between TPC and IFRS disclosures prolongs market uncertainty, exacerbating negative price adjustments as investors lack immediate clarification regarding firm performance. When IFRS reports are released sooner, the market adjusts more quickly, leading to a less severe or even reversed negative reaction. This is in line with Landsman et al. (2012), who suggest that the information content of IFRS statements is increased by less delay in reporting, and strongly supports H2.

4.1.3 Tests of differences

We compare the abnormal returns of IFRS and TPC disclosures in the pre- and post-event period. Table 7 shows the results of tests of differences in means, shedding light on investor sentiment before and after each announcement.

Tests of differences in means (IFRS and TPC in pre- and post-event periods)

| Panel A: Pre-event period (−20,−1) | ||||

|---|---|---|---|---|

| Obs | Mean | St. err | ||

| IFRS | 415 | −0.0197 | 0.0052 | |

| TPC | 415 | −0.0021 | 0.0055 | |

| Diff | Prob | |||

| <0 | 0.0032*** | |||

| ≠ 0 | 0.0064*** | |||

| >0 | 0.9968 | |||

| Panel B: Post-event period (0,20) | ||||

|---|---|---|---|---|

| Obs | Mean | St. err | ||

| IFRS | 415 | −0.0091 | 0.0062 | |

| TPC | 415 | −0.0217 | 0.0062 | |

| Diff | Prob | |||

| <0 | 0.9767 | |||

| ≠ 0 | 0.0467** | |||

| >0 | 0.0233** | |||

Note(s): This table presents the results of tests of differences in means of IFRS and TPC CARs in the pre- and post-event periods. *** and ** denote 1% and 5% significance levels, respectively

Source(s): Authors’ own work

The findings indicate that investors react more negatively before the IFRS disclosures than before the TPC disclosures, suggesting that they anticipate IFRS reports as corrective disclosures that provide transparency. However, following the IFRS disclosure, investor reactions become significantly less negative compared to the post-TPC period. The restrictive focus of TPC reports may contribute to negative market sentiment, which is later partially reversed by the release of IFRS reports, perceived as more informative. The results underpin H1. The findings also suggest that uninformed investors who react solely to mandatory TPC statements may be at a disadvantage, as they base their decisions on disclosures that may not fully reflect firms’ economic realities. This misalignment underscores the potential risk of sequential reporting structures in capital markets, where early financial disclosures may introduce distortions that are only later corrected by more reliable financial statements. The results signify that IFRS reports serve as a stabilizing mechanism, mitigating the uncertainty created by tax-based disclosures.

Table 8 further examines how differences in the time lag between IFRS and TPC disclosures influence market reactions. Firms are categorized into two groups based on the median IFRS-TPC disclosure gap (17 days). The findings indicate no significant differences in investor reactions around IFRS disclosures in general. However, in shorter-term event windows, firms with a longer IFRS-TPC time lag experience more pronounced negative abnormal returns. These results suggest that when IFRS reports are released later, the prolonged period of uncertainty exacerbates market reactions to TPC disclosures. Investors may become increasingly cautious during this transitional phase, leading to stronger price adjustments. The negative sentiment is particularly evident in event windows such as (−1,1), where firms with a longer time lag exhibit significantly lower CAR. This pattern indicates that extended disclosure gaps heighten information asymmetry, making it more difficult for investors to assess firm value in the absence of IFRS reports.

Tests of differences in means (time lag differentials in different event periods)

| Panel A. Pre-Event period (−20,−1) | ||||

|---|---|---|---|---|

| Obs | Mean | St. err | ||

| Low time lag | 215 | −0.0191 | 0.0070 | |

| High time lag | 200 | −0.0268 | 0.0079 | |

| Diff | Prob | |||

| >0 | 0.2335 | |||

| ≠ 0 | 0.4671 | |||

| <0 | 0.7665 | |||

| Panel B. Post-event period (0,20) | ||||

|---|---|---|---|---|

| Obs | Mean | St. err | ||

| Low time lag | 215 | −0.0153 | 0.0087 | |

| High time lag | 200 | −0.0130 | 0.0081 | |

| Diff | Prob | |||

| >0 | 0.5778 | |||

| ≠ 0 | 0.8444 | |||

| <0 | 0.4222 | |||

| Panel C. Event period (−1,1) | ||||

|---|---|---|---|---|

| Obs | Mean | St. err | ||

| Low time lag | 215 | −0.0015 | 0.0029 | |

| High time lag | 200 | −0.0107 | 0.0037 | |

| Diff | Prob | |||

| >0 | 0.0244** | |||

| ≠ 0 | 0.0489** | |||

| <0 | 0.9756 | |||

| Panel D. Event period (−3,3) | ||||

|---|---|---|---|---|

| Obs | Mean | St. err | ||

| Low time lag | 215 | −0.0102 | 0.0051 | |

| High time lag | 200 | −0.0221 | 0.0054 | |

| Diff | Prob | |||

| >0 | 0.0555* | |||

| ≠ 0 | 0.1110 | |||

| <0 | 0.9445 | |||

| Panel E. Event period (0,3) | ||||

|---|---|---|---|---|

| Obs | Mean | St. err | ||

| Low time lag | 215 | −0.0066 | 0.0039 | |

| High time lag | 200 | −0.0148 | 0.0042 | |

| Diff | Prob | |||

| >0 | 0.0768* | |||

| ≠ 0 | 0.1537 | |||

| <0 | 0.9232 | |||

Note(s): This table presents the results of tests of differences in means of IFRS and TPC CARs in different event periods based on the time lag between IFRS and TPC disclosures. ** and * denote 5% and 10% significance levels, respectively

Source(s): Authors’ own work

For firms with shorter IFRS-TPC time lags, the immediate availability of IFRS disclosures provides a more rapid resolution of uncertainty, limiting the extent of negative market reactions. Overall, these findings emphasize the importance of disclosure timing in shaping investor sentiment. The results support that information asymmetry, as measured by the IFRS-TPC time lag, significantly influences stock price reactions (H2).

4.2 Logistic regression analysis

Building on the event study findings, we examine the factors influencing investor reactions to IFRS and TPC financial statement announcements. The logistic regression models are estimated across multiple event windows—(−1,1), (0,1), and (−3,1)—to capture variations in investor response timing. To address potential unobserved year-specific factors, fixed year effects are incorporated, and standard errors are clustered at the sector level to control for internal correlation among firms operating in similar market environments. The results are presented in Table 9.

Logistic regression results

| Beta | Odds ratio | St.Err | t-value | p-value | |

|---|---|---|---|---|---|

| Panel A: CAR(−1,1) | |||||

| Asymi | −0.015 | 0.985 | 0.008 | −1.91 | 0.056* |

| Consi | −0.037 | 0.964 | 0.277 | −0.13 | 0.894 |

| Sizei | 0.042 | 1.043 | 0.034 | 1.22 | 0.222 |

| Levi | 2.276 | 9.733 | 0.413 | 5.51 | 0.000*** |

| PPEi | −0.717 | 0.488 | 0.274 | −2.61 | 0.009*** |

| INTGi | −1.708 | 0.181 | 0.542 | −3.15 | 0.002*** |

| Profi | 3.136 | 23.021 | 1.032 | 3.04 | 0.002*** |

| Growi | 0.146 | 1.158 | 0.039 | 3.75 | 0.000*** |

| Constant | −1.648 | 0.192 | 0.956 | −1.72 | 0.085* |

| Pseudo R2 | 0.066 | ||||

| Panel B: CAR(0,1) | |||||

| Asymi | −0.013 | 0.987 | 0.007 | −1.77 | 0.077* |

| Consi | −0.040 | 0.672 | 0.404 | −0.98 | 0.325 |

| Sizei | 0.016 | 1.016 | 0.058 | 0.27 | 0.785 |

| Levi | 0.978 | 2.660 | 0.297 | 3.30 | 0.001*** |

| PPEi | −0.448 | 0.639 | 0.207 | −2.17 | 0.030** |

| INTGi | −0.306 | 0.737 | 0.601 | −0.51 | 0.611 |

| Profi | 1.900 | 6.683 | 0.903 | 2.10 | 0.035** |

| Growi | −0.014 | 0.986 | 0.021 | −0.64 | 0.521 |

| Constant | −0.690 | 0.502 | 1.389 | −0.50 | 0.619 |

| Pseudo R2 | 0.031 | ||||

| Panel C: CAR(−3,1) | |||||

| Asymi | −0.016 | 0.984 | 0.008 | −2.04 | 0.041** |

| Consi | 0.364 | 1.440 | 0.205 | 1.78 | 0.076* |

| Sizei | −0.082 | 0.921 | 0.062 | −1.31 | 0.190 |

| Levi | 1.189 | 3.285 | 0.512 | 2.32 | 0.02** |

| PPEi | −0.344 | 0.709 | 0.239 | −1.44 | 0.15 |

| INTGi | 0.419 | 1.520 | 0.837 | 0.50 | 0.617 |

| Profi | 2.622 | 13.761 | 1.311 | 2.00 | 0.046** |

| Growi | −0.061 | 0.941 | 0.032 | −1.90 | 0.057 |

| Constant | 0.799 | 2.224 | 1.350 | 0.59 | 0.554 |

| Pseudo R2 | 0.072 | ||||

Note(s): This table presents the results of logistic regression analysis for different event windows. ***, **, and * denote 1%, 5%, and 10% significance levels, respectively. Variable definitions are provided in Table 4

Source(s): Authors’ own work

The regression results confirm that information asymmetry plays a crucial role in shaping investor reactions. The likelihood of a positive IFRS-TPC CAR differential is significantly reduced by higher information asymmetry, as indicated by the consistently negative coefficient on the time lag variable. Odds ratios help to assess the practical impact of statistically significant relationships. Accordingly, firms with a longer time lag are approximately 2.5% (1–0.985) less likely to exhibit a positive IFRS-TPC CAR differential compared to those with a shorter time lag. Although marginally significant, the consistency of the negative coefficient confirms the robustness of this relationship, holding under various event windows, with control variables, sector-clustered standard errors and fixed year effects, all of which reduce bias but may also contribute to wider confidence intervals. This suggests that delayed IFRS disclosures systematically contribute to heightened investor uncertainty and weaker market responses, providing further support for H2 that greater disclosure delays prolong uncertainty, rendering weaker investor responses to IFRS announcements. Other factors, including leverage, property, plant, and equipment, intangible assets, profitability and growth opportunities, generally align with expectations. However, firm size and the requirement to prepare consolidated financial statements do not have a statistically significant impact on market reactions.

5. Conclusion

This study examines the impact of the dual financial reporting system in Türkiye, where firms are required to publish their financial statements under both TPC and IFRS. Using event studies and logistic regression, we analyze how these disclosures influence stock prices and investor behavior, identifying key differences in market reactions to TPC and IFRS-based reports. Our findings reveal that TPC financial statements generally trigger negative abnormal returns, whereas IFRS disclosures help to reverse these reactions, underscoring the higher transparency and decision-usefulness of IFRS for investors. The results also highlight that the extent of information asymmetry emerges as a key determinant of investor confidence and reaction to financial reports. Specifically, the time lag between TPC and IFRS disclosures significantly influences stock price reactions, with longer delays exacerbating negative abnormal returns. This suggests that investors have difficulty in interpreting financials when faced with incomplete or tax-driven information, leading to heightened uncertainty and market inefficiencies.

The practical implications of this study are far-reaching. For investors, the findings emphasize the importance of interpreting both TPC and IFRS disclosures holistically, rather than reacting solely to tax-based reports. Investors should be particularly wary of firms with high information asymmetry, as delayed IFRS disclosures tend to amplify negative market reactions. The study highlights that institutional investors may exploit these timing gaps, creating arbitrage opportunities, while retail investors are more vulnerable to misinterpretation based on TPC statements alone. Enhancing financial literacy programs and investor education initiatives could help mitigate uninformed trading behavior and improve market efficiency. The study also reveals the need for companies to strategically manage their financial disclosure processes. Reducing the reporting lag between TPC and IFRS financial statements is critical to minimizing market uncertainty and avoiding information asymmetry from distorting investor expectations. Firms should proactively address investor concerns by improving their disclosure practices, particularly for those with more complex financial information. In addition, firms can enhance investor relations by clearly communicating the differences between TPC and IFRS reports, helping market participants to better understand the relevance of each reporting standard. As mandatory tax disclosure tends to drive less favorable market reactions, firms with high information asymmetry should consider additional voluntary tax-based financial guidance. This would help to counteract investor uncertainty and reduce the risk of excessive negative market reactions during the information gap between disclosures. Regulators, particularly the Capital Markets Board and tax authority, should consider policies that promote a more synchronized reporting framework. Encouraging firms to release IFRS and TPC disclosures simultaneously or within a shorter timeframe could help reduce information asymmetry and prevent misleading investor reactions. Furthermore, policy adjustments that improve alignment between tax-based and IFRS-based reporting practices could improve market efficiency by minimizing discrepancies that create investor confusion. Another key implication is the potential reconsideration of tax policy based on IFRS statements. Given that IFRS-based financial reports are perceived as more reliable and informative, a closer alignment of tax reporting with IFRS could reduce complexity, enhance market transparency and boost investor confidence. The complexity of maintaining two separate financial reporting frameworks may create unnecessary administrative burdens for companies, investors and regulators. Simplifying the tax system to rely more on IFRS-based financial statements could foster a more efficient market.

Despite its contribution, this study has certain limitations. It focuses on XU100 index companies with complete data, limiting the generalizability of findings to the broader market. Future research could extend the dataset to all listed firms in Borsa Istanbul, capturing a more comprehensive market perspective. While annual financial statements are analyzed in this study, future research could also explore quarterly disclosures to assess whether interim reports generate similar market reactions. Sector-specific differences and investor heterogeneity also warrant further investigation. Future studies could analyze whether certain industries exhibit stronger market reactions to IFRS and TPC announcements or whether institutional investors interpret disclosures differently than retail investors. Another promising avenue for research is to further quantify the role of information asymmetry by exploring how investor sentiment and trading volumes fluctuate in the period between TPC and IFRS disclosures. Understanding the mechanisms through which investors process staggered financial disclosures would provide valuable insights into market dynamics.