Research dealing with earnings management in the public-sector context is expanding. This paper aims to review the existing literature to understand how research is developing and points out gaps deserving further investigation.

This study uses the structured literature methodology to investigate the state-of-the-art and future directions of the literature on earnings management in the public sector. In total, 78 articles were explored.

The critical analysis of the literature shows that different but related streams of literature are emerging, focused on both a macro- and a micro-level perspective (mainly local governments and state-owned enterprises).

This study is the first that offers a comprehensive review of the literature on the emerging topic of earnings management in the public-sector context. The structured literature review enables the identification of future directions for the literature in this field.

1. Introduction

Earnings management (EM) is a common practice in the private sector, and studies have adopted different theoretical approaches and research methods to investigate this topic (Dechow et al., 2010; Jones, 2011a). More recently, EM has attracted the interest of many public-sector scholars, who are motivated by the implementation of accrual accounting systems. Although both academics and practitioners were initially skeptical regarding accrual accounting in the public-sector context, even the most critical opponents agree that it is no longer possible to base the decision-making process only on cash accounting information (Bergmann et al., 2019). One of the key differences between cash and accrual accounting systems is that the latter relies heavily on professional judgment. Clearly, substantial discretion while recognizing revenues and expenses, and the reporting of assets and liabilities, can allow managers and politicians to more effectively convey information about their entity's financial performance and health. At the same time, in a highly political environment, there is always a risk that discretion under certain circumstances will be harmful, as it allows opportunism to enter financial reporting. Indeed, researchers are unveiling both opportunities and incentives to manipulate accounting figures in the public-sector context (e.g. Vinnari and Näsi, 2008; Pilcher and Van Der Zahn, 2010; Cohen, 2012).

More generally, the growing interest in EM in the public sector can be observed at both a micro- and a macro-level perspective. At a micro-level perspective, sub-national governments or entities operating within national or sub-national governments may be asked to achieve specific goals. Understanding how government officials exercise discretion over financial reporting is then considered essential for citizens, regulators and researchers to interpret and monitor financial performance (Beck, 2018). Although the bottom line is not considered as important as in the private sector, especially at a local government level, significant surpluses might be interpreted as a sign of excessive taxes, while deficits might be considered indications of poor financial management that could attract criticism from political opponents (Cohen et al., 2019; Donatella, 2020). Indeed, substantial economic and political consequences can derive from failing to achieve targets (Greenwood et al., 2017; Hodges, 2018), including those defined by supervising authorities. At a macro-level perspective, EM can be due to governments' need to comply with specific rules and achieve predefined objectives, such as those defined by international organizations (e.g. the World Bank, International Monetary Fund, European Union (EU), etc.).

Through a structured literature review (SLR) methodology, this study aims to provide an updated picture of the state of knowledge and pinpoint a future research agenda. A rigorous literature review can help to enhance knowledge on EM's related incentives and opportunities and inform policymaking and practice (Tranfield et al., 2003; Petticrew and Roberts, 2008). An SLR methodology allows the development of insights, critical reflection and future research paths (Massaro et al., 2016) by facilitating an investigation of strengths and weaknesses, the mapping of EM's evolution in the public sector and the discovery of under-investigated issues and topics.

Using as a background Alvesson and Deetz's (2000) critical management framework, and consistent with previous studies utilizing an SLR methodology (Guthrie et al., 2012; Dumay et al., 2016; Massaro et al., 2016; Bisogno et al., 2018; Santis et al., 2018; Bracci et al., 2019; Manes-Rossi et al., 2020), this study aims to answer the following research questions (RQs):

How is EM research in the public sector developing?

What is the focus and critique of EM literature?

What is the future of EM research in the public sector?

The remainder of the article is structured as follows. Section 2 explains the SLR methodology. Section 3 illustrates the development of EM research in the public sector (i.e. to answer RQ1), while Section 4 provides a critical analysis of the focus and critique of EM literature (i.e. to answer RQ2). Section 5 discusses the future agenda of EM research in the public sector (i.e. to answer RQ3), and Section 6 concludes the article and presents its limitations.

2. Research methodology

Massaro et al. (2016, p. 769) identified a “literature review continuum” that varies from a rapid review, characterized by few rules, to an SLR, where specific rules must be implemented. While the rapid review aims to summarize and interpret findings that have emerged from previous studies, an SLR goes further by providing a transparent research methodology for assessing and classifying each study included in the review and proposing future research directions. Starting from the research questions identified in the previous section, other steps are required to develop the data set and analytical framework, as outlined in the following sections.

2.1 Literature search

The first step in the SLR methodology is the selection of eligible articles to meet the study's research objective. This search was based on the following keywords: “earnings management” OR “creative accounting” OR “accounting manipulation” OR “financial performance adjustments” OR “financial reporting quality” OR “accruals quality” OR “opportunistic financial reporting” OR “surplus-deficit-management” AND “public sector” OR “government” OR “municipalit*.” The search was carried out by referring to abstract, title and keywords.

“Earnings management,” “creative accounting” and “accounting manipulation” were included as they are very common and frequently used interchangeably (Jones, 2011b). In addition, other alternative “labels” were included since they were used in the literature, specifically “financial performance adjustments” (Pilcher and van der Zhan, 2010; Arcas and Marti, 2016; Donatella, 2020), “financial reporting quality” (Greenwood et al., 2017) or “accruals quality” (Ballantine et al., 2008), “opportunistic financial reporting” (Beck, 2018) and “surplus-deficit management” (Stalebrink, 2007).

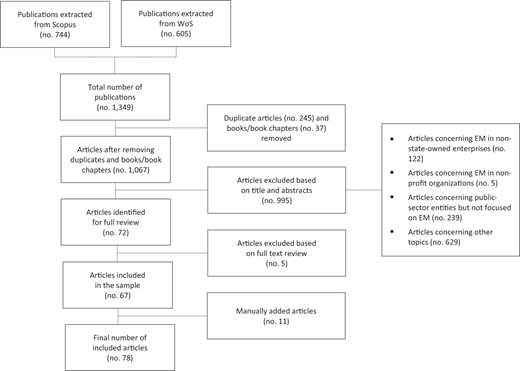

The databases used in this study were Scopus and ISI Web of Science (WoS). Several filters were used to limit the search for relevant articles. First, only articles published in English in peer-reviewed journals in 1980–2020 were included; this period was selected so as to include both recent and old articles, also considering that EM is quite a recent topic in the public-sector context. Second, the search was based on specific domains, which were chosen to take into account both the authors' background (Paoloni et al., 2020), and the micro/macro-level perspectives mentioned above. Accordingly, the search was not restricted only to the “accounting” domain, but also extended to related domains (such as economics, business, finance and public administration). Therefore, in the Scopus database, the search was limited to business, management and accounting; economics, econometrics and finance; and social science. In the WoS database, it was limited to business economics, government law and public administration. The initial search retrieved a total of 1,349 publications. After removing 245 duplicates and 37 books/book chapters, the data set consisted of 1,067 publications.

According to the SLR methodology (Bisogno et al., 2018; Santis et al., 2018; Manes-Rossi et al., 2020), the second step consists of assessing the relevance of selected articles (Petticrew and Roberts, 2008). Each article was scrutinized; its title, abstract and, whenever necessary, contents were carefully examined. The following criteria were used to select relevant articles:

The focus of the contributions had to be on EM in the public sector. As a result, articles centered only on non-state-owned enterprises (122 articles) or non-profit organizations (five articles) were excluded. However, contributions investigating state-owned enterprises (and, more generally, firms controlled by public-sector organizations) were included.

Articles regarding public-sector entities, whose main topic did not focus on EM (e.g. articles investigating financial reporting quality in general terms, without examining EM behavior), were excluded, resulting in the elimination of 239 articles.

Articles on other topics (e.g. financial reporting quality and disclosure issues, auditing regulations, creative finance, transparency, internal control quality) were not included, resulting in 629 articles excluded.

Due to these criteria, 72 articles were selected. Five further articles were excluded, after reading the full text, as they did not investigate EM in the public-sector context in depth. After a residual search, eight articles were manually added because of their diffusion in the literature. We also manually added three online first articles (Anagnostopoulou and Stavropoulou, 2021; Cohen and Malkogianni, 2021a, b) published early in 2021. The final selection included 78 articles, and a digital archive was created (see Section 8 “Articles included in the sample”). Figure 1 illustrates the selection process of articles included in the final sample.

2.2 The analytical framework and coding activity

The third step of the analysis consists of developing the analytical framework to codify and classify each article. To this end, previous SLRs (Guthrie et al., 2012; Dumay et al., 2016; Bisogno et al., 2018; Santis et al., 2018; Bracci et al., 2019; Manes-Rossi et al., 2020) were used as a reference, even though several changes were needed to maintain consistency with the aim of this study. The following nine categories were identified: (A) jurisdiction and organizational focus, (B) continent of research, (C) focus of the literature, (D) types of EM, (E) accounting system, (F) research method, (G) contributions and implications, (H) theoretical frameworks and (I) academics and practitioners.

Category (A) was defined with a broad meaning, as it includes both the “jurisdiction” and “organizational focus” criteria used in previous SLRs, implicitly considering state-owned enterprises as an additional jurisdictional level. As a result, this category includes the following sub-categories: (A1) central government, (A2) state/regional government, (A3) local government, (A4) state-owned enterprises and (A5) other.

Category (B), continent of research, was an adaptation of the “country of research” category of previous SLRs, as many articles focused on Asia and Europe. Therefore, this category includes the following sub-sections: (B1) Africa, (B2) America, (B3) Asia, (B4) Europe and (B5) Oceania. A residual sub-category, (B6) international, was also coded to classify articles investigating a sample of countries belonging to different continents.

Category (C), focus of the literature, was reshaped to emphasize the main issues under analysis. It consists of the following sub-categories: (C1) budget manipulation, (C2) financial statements manipulation, (C3) auditing, (C4) compliance with rules/regulations and (C5) other.

To support category (F), research methods, two additional categories were added. This includes categories (D), type of EM, and (E), accounting system, which is necessary to better understand how EM practices are investigated. Category (D) includes the following sub-categories: (D1) “real” EM, (D2) “accounting” EM and (D3) both. Category (E) consists of the following sub-categories: (E1) cash-based, (E2) modified-cash or modified-accrual, (E3) accrual-based and (E4) national/statistical data. A residual sub-category, (E5) mixed, was also coded to take into account the articles investigating more than one accounting system. Category (F), research methods, was obtained by slightly amending the category used in previous SLRs. It includes five sub-categories: (F1) quantitative empirical analysis, (F2) survey/interviews/other empirical, (F3) conceptual, (F4) commentary/normative/policy and (F5) literature review.

Finally, three categories were not changed: (G) contributions and implications, (H) theoretical frameworks and (I) academics and practitioners.

2.3 Developing reliability

During the second step of the analysis, the 1,067 contributions obtained from the search were equally divided among the two authors, who read the title and abstract to assess each contribution's relevance. Several meetings were held to resolve doubts and discuss articles of uncertain relevance.

The authors jointly defined the categories of the analytical framework while classifying relevant articles. Considering the importance of this step, a pilot test was carried out: The authors coded 20 articles separately to assess the framework's suitability and determine which criteria and attributes required changes. A meeting was then organized to compare and discuss results, and the authors agreed to revise the framework to improve its suitability. The categories that required in-depth discussion were (A) jurisdiction and organizational focus, (C) focus of the literature, (D) type of EM and (E) accounting systems. The authors achieved a consensus on the definition and the meaning of each category and sub-category to ensure inter-code reliability.

The following step consists of manually coding the 78 relevant articles. Each author conducted this coding, and the results were recorded in an Excel® file to facilitate the subsequent analysis. A meeting was organized to reach agreement on the final codification of each article.

Considering that all decisions were made by consensus during the process and agreement was then achieved step by step, the authors did not find it necessary to carry out a formal reliability check, such as Krippendorff's α (Krippendorff, 2018).

3. Development of earnings management research in the public sector

The following section answers the first research question: How is EM research in the public sector developing?

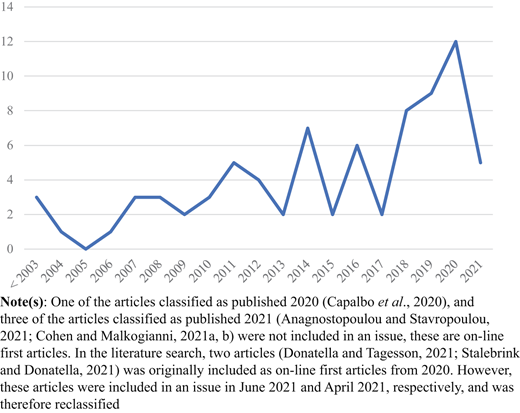

Figure 2 illustrates the distribution of articles per year in the period 1980–2021. Three articles (Anthony, 1985; Hale, 1988; Dafflon and Rossi, 1999) were published before 2003, and increasing interest in the topic can be observed from 2014 onward. About 65% of all articles (51 out of 78) were published in 2014–2021.

Table 1 displays the number of articles per source journal. It is worth noting that the publications were spread over a relatively large number of outlets: The 78 articles were published in 58 different journals. This indicates that there is no one leading journal for EM in the public-sector context. Therefore, to avoid a long list of journals, Table 1 includes only the journals where two or more articles were published.

Classification of articles by journals

| Code | Journal name | No | % |

|---|---|---|---|

| PMM | Public Money and Management | 6 | 7.7 |

| FAM | Financial Accountability and Management | 4 | 5.1 |

| CG | Corporate Governance: An International Review | 3 | 3.8 |

| JAPP | Journal of Accounting and Public Policy | 3 | 3.8 |

| JPBAFM | Journal of Public Budgeting, Accounting and Financial Management | 3 | 3.8 |

| IJAAPE | International Journal of Accounting, Auditing and Performance Evaluation | 2 | 2.6 |

| JAAR | Journal of Applied Accounting Research | 2 | 2.6 |

| JBF | Journal of Banking and Finance | 2 | 2.6 |

| JCAE | Journal of Contemporary Accounting and Economics | 2 | 2.6 |

| JMG | Journal of Management and Governance | 2 | 2.6 |

| RAS | Review of Accounting Studies | 2 | 2.6 |

| Total | 31 | 39.7 |

Each article's impact was assessed using the number of Google Scholar citations, which were downloaded as of February 8, 2021. Table 2 shows the top ten articles by citation. Considering that older articles have had more time to collect citations than recent articles, and to be consistent with previous SLRs (Dumay et al., 2016; Bisogno et al., 2018; Santis et al., 2018; Bracci et al., 2019; Manes-Rossi et al., 2020), a second ranking, based on the average citations per year (CPY), was developed. Table 3 shows the top ten articles by CPY (2021 − year published).

Top ten articles by Google Scholar citations (as of February 8, 2021)

| No | Reference | Article | Cit |

|---|---|---|---|

| 1 | Chen et al. (2011) | Effects of audit quality on earnings management and cost of equity capital: Evidence from China | 504 |

| 2 | Ding et al. (2007) | Private vs state ownership and earnings management: Evidence from Chinese listed companies | 455 |

| 3 | von Hagen and Wolff (2006) | What do deficits tell us about debt? Empirical evidence on creative accounting with fiscal rules in the EU | 331 |

| 4 | Chen et al. (2008) | Government assisted earnings management in China | 282 |

| 5 | Kao et al. (2009) | Regulations, earnings management, and post-IPO performance: The Chinese evidence | 199 |

| 6 | Wang and Yung (2011) | Do State Enterprises Manage Earnings More than Privately Owned Firms? The case of China | 164 |

| 7 | Rauch et al. (2011) | Fact and Fiction in EU-Governmental Economic Data | 156 |

| 8 | Vinnari and Näsi (2008) | Creative accrual accounting in the public sector: “Milking” water utilities to balance municipal budgets and accounts | 115 |

| 9 | Dafflon and Rossi (1999) | Public accounting fudges towards EMU: A first empirical survey and some public choice considerations | 103 |

| 10 | Eaton and Nofsinger (2004) | The effect of financial constraints and political pressure on the management of public pension plans | 89 |

Top ten articles by CPY (as of February 8, 2021)

| No | Reference | Article | CPY |

|---|---|---|---|

| 1 | Chen et al. (2011) | Effects of audit quality on earnings management and cost of equity capital: Evidence from China | 50.40 |

| 2 | Ding et al. (2007) | Private vs state ownership and earnings management: Evidence from Chinese listed companies | 32.50 |

| 3 | von Hagen and Wolff (2006) | What do deficits tell us about debt? Empirical evidence on creative accounting with fiscal rules in the EU | 22.07 |

| 4 | Chen et al. (2008) | Government assisted earnings management in China | 21.69 |

| 5 | Kao et al. (2009) | Regulations, earnings management, and post-IPO performance: The Chinese evidence | 16.58 |

| 6 | Wang and Yung (2011) | Do State Enterprises Manage Earnings More than Privately Owned Firms? The case of China | 16.40 |

| 7 | Rauch et al. (2011) | Fact and Fiction in EU-Governmental Economic Data | 15.60 |

| 8 | Ho et al. (2015) | Real and Accrual-Based Earnings Management in the Pre- and Post-IFRS Periods: Evidence from China | 13.83 |

| 9 | Lyu et al. (2018) | GDP management to meet or beat growth targets | 9.67 |

| 10 | Vinnari and Näsi (2008) | Creative accrual accounting in the public sector: “Milking” water utilities to balance municipal budgets and accounts | 8.85 |

Eight articles are included in both tables (von Hagen and Wolff, 2006; Ding et al., 2007; Chen et al., 2008; Vinnari and Näsi, 2008; Kao et al., 2009; Chen et al., 2011; Rauch et al., 2011; Wang and Yung, 2011). Notably, the articles achieving the highest number of citations investigated EM in state-owned enterprises, collecting citations from both private- and public-sector studies. Other articles focused on the macroeconomic level, with the main issue being to assess compliance with fiscal rules. Focusing on the CPY, Table 3 lists a more recent article (Lyu et al., 2018). It is also worth noting that other recent articles (not shown in the table) collect a high CPY (e.g. Donatella et al., 2019, whose CPY is 8). This shows the growing academic interest in citing the latest research on EM in the public sector.

4. Research on earnings management in the public sector: insight and critique

According to the code, as illustrated in previous sections, Table 4 shows the analytical framework results.

Analytical framework of EM in the public sector

| A | Jurisdiction and organizational focus | No | % | B | Continent of research | No | % |

|---|---|---|---|---|---|---|---|

| A1 | Central government | 9 | 11.5 | B1 | Africa | 2 | 2.6 |

| A2 | State/regional government | 4 | 5.1 | B2 | America | 9 | 11.5 |

| A3 | Local government | 26 | 33.3 | B3 | Asia | 30 | 38.5 |

| A4 | State-owned enterprises | 27 | 34.6 | B4 | Europe | 30 | 38.5 |

| A5 | Other | 12 | 15.4 | B5 | Oceania | 4 | 5.1 |

| Total | 78 | 100 | B6 | International | 3 | 3.8 | |

| Total | 78 | 100 | |||||

| C | Focus of literature | No | % | D | Types of EM | No | % |

| C1 | Budget manipulation | 1 | 1.3 | D1 | “Real” EM | 12 | 15.4 |

| C2 | Financial statements manipulation | 52 | 65.8 | D2 | “Accounting” EM | 49 | 62.8 |

| C3 | Auditing | 5 | 6.3 | D3 | Both | 17 | 21.8 |

| C4 | Compliance with rules/regulations | 11 | 13.9 | Totals | 78 | 100 | |

| C5 | Other | 10 | 12.7 | ||||

| Total | 79 | 100 | |||||

| E | Accounting system | No | % | F | Research methods | No | % |

| E1 | Cash-based | 3 | 3.8 | F1 | Quantitative empirical analysis | 69 | 88.5 |

| E2 | Modified-cash or modified-accrual | 3 | 3.8 | F2 | Survey/interviews/other empirical | 6 | 7.7 |

| E3 | Accrual-based | 57 | 73.1 | F3 | Conceptual | 0 | 0.0 |

| E4 | National/statistical data | 11 | 14.1 | F4 | Commentary/normative/policy | 2 | 2.6 |

| E5 | Mixed | 4 | 5.1 | F5 | Literature review | 1 | 1.3 |

| Total | 78 | 100 | Total | 78 | 100 | ||

| G | Contribution and implications | No | % | H | Theoretical frameworks | No | % |

| G1 | Theoretical/methodological implications | 6 | 7.7 | H1 | None proposed | 31 | 39.7 |

| G2 | Empirical/practical implications | 71 | 91.0 | H2 | Applies or considers previous | 47 | 60.3 |

| G3 | No implications | 1 | 1.3 | H3 | Proposes a new | 0 | 0.0 |

| Total | 78 | 100 | Total | 78 | 100 | ||

| I | Academics and practitioners | No | % | ||||

| I1 | Academics | 73 | 93.6 | ||||

| I2 | Practitioners | 1 | 1.3 | ||||

| I3 | Academics and practitioners | 4 | 5.1 | ||||

| Total | 78 | 100 |

The following sub-sections answer the second research question: What is the focus and critique of EM literature?

4.1 Jurisdiction and organizational focus

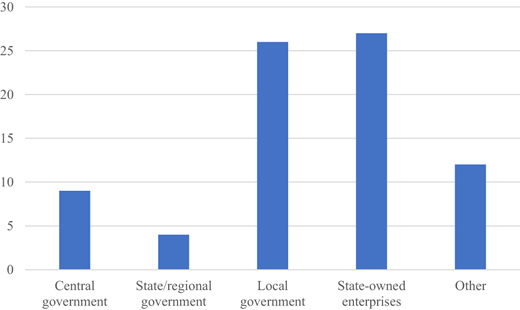

The first criterion is the jurisdiction investigated in the article. Figure 3 illustrates that the bulk of the articles focused on local governments and state-owned enterprises (26 and 27 articles, respectively). Nine articles investigated central governments, while only four articles were related to state/regional governments. Articles in the residual sub-category “other” mainly concentrated on EM in healthcare organizations (e.g. Ballantine et al., 2008; Greenwood and Zhan, 2019; Wen et al., 2019). As for articles focused on local governments, it seems that less recent studies (Stalebrink, 2007; Pinnuck and Potter, 2009) aimed to assess the magnitude of EM behavior, while more recent articles mainly studied the determinants of EM, especially focusing on the role of political factors and political competition (e.g. Kido et al., 2012; Ferreira et al., 2013, 2020; Cohen et al., 2019; Donatella, 2020).

Generally, the literature considers state- and non-state-owned enterprises to be comparable. Articles focused on state-owned enterprises, therefore, tend to adopt the same approaches used in studies concerning private-sector EM research and include data on enterprises both with and without state ownership. This allows scholars to analyze whether state-owned enterprises react differently to certain incentives compared to non-state-owned enterprises (e.g. Ding et al., 2007; Chen et al., 2011; Capalbo et al., 2014; Liu et al., 2014; Huang and Li, 2016; Wang et al., 2020). It is also worth noting that the vast majority of these articles focused on the Chinese context, and that some additional political factors are at play here that are not found in EM research outside the Asian context (e.g. Chen et al., 2008, analyzed local governments' incentives to help listed firms engage in EM to avoid firms within their jurisdictions falling below the delisting threshold imposed by the central government; Chi et al., 2016, investigated differences in the magnitude of EM between firms with and without political connections).

4.2 Continent of research

The geographical area of research is important for understanding the following:

At a macro-level perspective, how governments may react when fiscal rules and restrictions are fixed or imposed by international organizations; and

At a micro-level perspective, whether specific areas are more investigated than others, meaning that certain contexts could be more prone than others to the manipulation of accounting figures, taking into account that many local governments have implemented accrual-accounting systems.

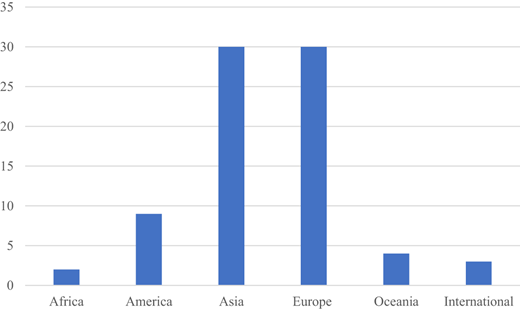

Figure 4 shows that both Africa and Oceania have contributed little to EM research in the public sector, with two and four articles, respectively. The majority of articles focused on Asia and Europe (30 out of 78, i.e. about 38% in both cases). Nine articles investigated America, while three studies concentrated on a sample of countries from several continents (Rauch et al., 2014; Reischmann, 2016; Kartiko et al., 2018).

As far as the Asian context is concerned, the bulk of articles (19 out of 30) investigated the Chinese context by focusing on state-owned enterprises. As already observed, such studies tended to use the same approaches adopted in private-sector studies, with the inclusion of ad hoc political variables to emphasize the effects of strict relationships with public-sector entities. This focus could be due to the ongoing process of privatization of state-owned enterprises in China or to changes in corporate governance mechanisms, such as those that occurred in Malaysia (i.e. Mohammad et al., 2012).

The European context is more articulated. Four articles investigated EM from a macro-economic perspective, mainly examining fiscal deficits in the EU context (Dafflon and Rossi, 1999; von Hagen and Wolff, 2006; Rauch et al., 2011; Maltritz and Wüste, 2020). Two articles concentrated on state/regional governments (Clémenceau and Soguel, 2017, 2018), and ten articles either concentrated on the local governments of a single country – including English local governments (Arcas and Marti, 2016), Greek municipalities (Cohen and Malkogianni, 2021a, b), Italian municipalities (Anessi-Pessina and Sicilia, 2020), Portuguese municipalities (Ferreira et al., 2013, 2020) and Swedish municipalities (Stalebrink, 2007; Donatella et al., 2019; Donatella, 2020; Donatella and Tagesson, 2021) – or took a comparative approach (Cohen et al., 2019, compared Greece and Italy). In addition to this, there is one case study analyzing one Finnish municipality (Vinnari and Näsi, 2008). Six articles analyzed healthcare organizations (Ballantine et al., 2007, 2008; Greenwood et al., 2017; Greenwood and Zhan, 2019; Ibrahim et al., 2019; Anagnostopoulou and Stavropoulou, 2021), while only three studies (Capalbo et al., 2014, 2020; Gaio and Pinto, 2018) concentrated on state-owned enterprises. The remaining articles focused on other issues (e.g. Pina et al., 2012, analyzed EM in UK executive agencies). This vivacity can be interpreted as a clear signal of the increasing academic interest in investigating EM behavior in the European context, mostly concentrating on the role of political factors. It is also worth noting that all micro-level studies in Europe have in common that they examine the EM practices of entities that have implemented accrual accounting systems.

4.3 Focus of the literature

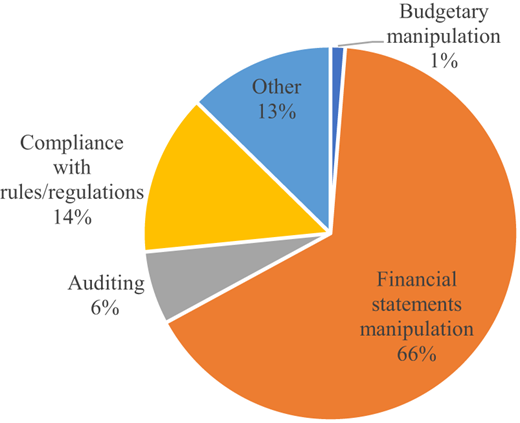

This category aims to illustrate the focus of the selected articles to reveal the most debated topic and point out under-investigated areas to identify gaps deserving further attention (Santis et al., 2018; Bracci et al., 2019). As Figure 5 illustrates, the bulk of the articles (52, or about 66%) investigated financial statements manipulation, while another 11 articles (about 14%) concentrated on EM because of the explicit need to comply with rules and regulations. Interestingly, only one article (Anessi-Pessina and Sicilia, 2020) investigated both budgetary and financial statements manipulation (therefore, it has been counted twice, with the total number being 79).

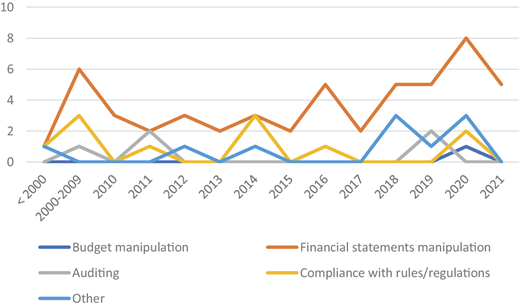

Figure 6 further shows the distribution of articles per focus and per year. While before 2000 and between 2000 and 2009 the total number of articles was meagre, an increasing trend can be observed in the following years, with a peak in 2019 and 2020, especially regarding articles focused on financial statements manipulation.

4.4 Types of earnings management

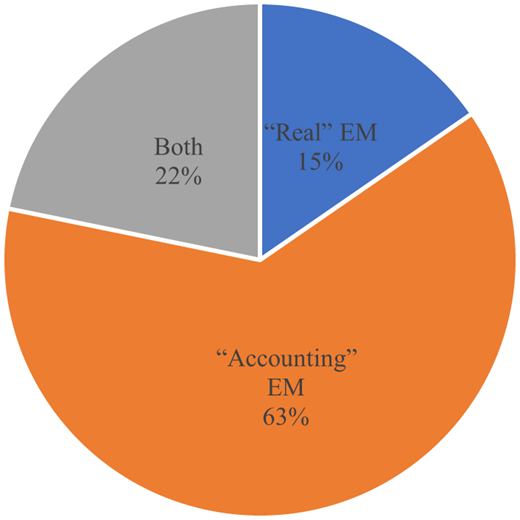

In EM research, a distinction is made between accounting EM (i.e. when discretion in the accounting process is used to alter reported financial information) and real EM (i.e. when transactions are structured to alter reported financial information). Category (D), types of EM, was designed to capture the EM practices investigated in the literature.

Figure 7 illustrates that about 63% of the articles (49 out of 78) examined accounting manipulation, while about 15% (12 out of 78 articles) investigated real manipulation. About 22% of the articles (17 out of 78) combined both types of EM. It is worth observing that real EM in state-owned enterprises has been widely researched (e.g. Chen et al., 2008; Ho et al., 2015; Fan and Song, 2019; Ben Rejeb Attia, 2020; Chen et al., 2020).

4.5 Accounting system

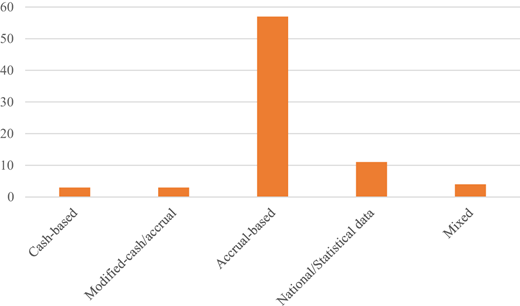

Figure 8 displays the results concerning category (E), which focuses on the accounting system. As expected, the vast majority of articles (57 out of 78, or about 73%) examined accrual-based systems. The reason is twofold: First, several articles investigated state-owned enterprises, which obviously adopt accrual systems; second, local governments in different contexts have implemented these systems (e.g. Cohen et al., 2019, examined EM in Greece and Italy; Donatella, 2020, investigated EM in Swedish municipalities, etc.). Obviously, the studies concentrated on macro-level (11 out of 78, or about 14%) referenced national/statistical data.

It is interesting to note that Beck (2018) refers to both modified and full accrual, while Hodges (2018) provides an interesting analysis by considering both accrual accounting (a micro-level perspective) and national data (a macro-level perspective).

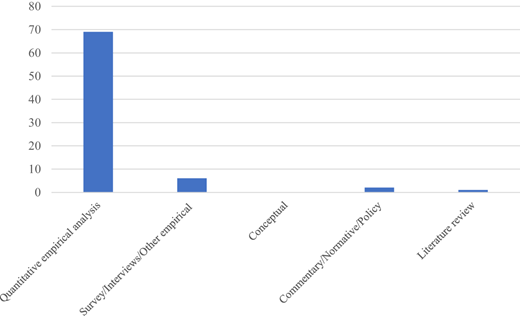

4.6 Research methods

Figure 9 illustrates the results for category (F), research method. This category aims to illustrate scholars' methodological approaches to gathering insights into EM in the public sector and how research is evolving between theoretical and empirical paths (Manes-Rossi et al., 2020). About 88% of the articles adopted a quantitative approach, as expected. More specifically, articles that examined accounting EM at a micro-level tended to estimate abnormalities in total accruals (i.e. as a proxy for EM) using the Jones model (Jones, 1991) or, more frequently, its modified versions (e.g. Dechow et al., 1995). The modified Jones model is frequently used, particularly in state-owned enterprises (e.g. Wang and Yung, 2011; Ho et al., 2015; Gaio and Pinto, 2018; Kim, 2018; Beladi et al., 2020). Although these models are used for analyzing accounting EM in sub-national governments and entities operating within national or sub-national governments (e.g. Pina et al., 2012; Ferreira et al., 2013; Greenwood and Zhan, 2019), several other approaches are also used. Some studies proposed their own models (e.g. Stalebrink, 2007; Felix, 2015; Clémenceau and Soguel, 2017; Beck, 2018). It is also worth noting that at the sub-national government level, it is common to find articles that focus on specific accruals, rather than total accruals. In particular, depreciation and/or impairment have been analyzed separately (Stalebrink, 2007; Pilcher and Van der Zahn, 2010; Clémenceau and Soguel, 2017; Drew, 2018) or in combination with other types of accruals (Pilcher, 2011; Arcas and Marti, 2016; Donatella et al., 2019; Donatella, 2020). Some articles focus on revenue manipulation in local governments (Anessi-Pessina and Sicilia, 2020; Donatella and Tagesson, 2021). For the purpose of identifying EM in sub-national governments and entities operating within national or sub-national governments, several scholars have relied on the Burgstahler and Dichev (1997) approach, testing for discontinuity in reported net income distribution (e.g. Ballantine et al., 2007; Ferreira et al., 2013, 2020).

Articles investigating EM at a macro-level perspective principally used the stock-flow adjustments approach, defined as the difference between the budget deficit and the change in public debt (von Hagen and Wolff, 2006; Reischmann, 2016; Maltritz and Wüste, 2020) or used Benford's law (e.g. Rauch et al., 2011, 2014). Six articles (about 8%) used other research methods, such as structured equation modeling (e.g. Mustapha et al., 2019; Ramandei et al., 2019), or were based on a questionnaire (Rahmatika, 2016). Only one article (Hodges, 2018) provided a literature review, even though it primarily aimed to assess if and how public-sector accounting harmonization could influence creative accounting and adopted a more restricted focus than the one used in this SLR. There were only two older commentary/normative/policy articles (Anthony, 1985; Hale, 1988).

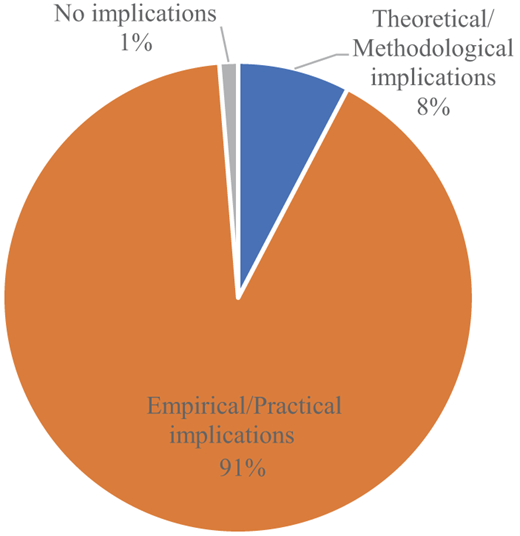

4.7 Contribution and implications, and theoretical frameworks

The results concerning categories (G), contributions and implications, and (H), theoretical frameworks, are jointly analyzed as they are strictly connected. As Figure 10 shows, the vast majority of the selected articles (71 out of 78, or 91%) emphasized more practical and empirical implications deriving from the research, while only six articles (about 8%) discussed theoretical implications.

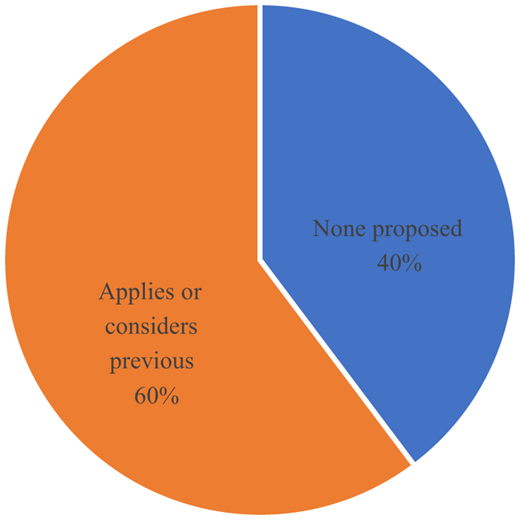

The theoretical frameworks used in a field indicate the level of maturity and novelty of existing studies, using as a proxy the number of frameworks and models discussed in previous research (Guthrie et al., 2012; Massaro et al., 2016; Bracci et al., 2019; Manes-Rossi et al., 2020). Figure 11 shows the results for category (H), theoretical frameworks. It is noteworthy no studies proposed a new framework. About 60% of the articles used an existing framework, while in about 40% of the cases, no explicit framework was proposed or used to guide hypothesis development. These results could be interpreted as a signal of the embryonal stage of EM research in the public sector. The main aim of studies included in this review appears to be, first, to understand whether public-sector entities manipulate earnings, and second, to ascertain the possible determinants and underlying motivations. It could be argued that studies on public-sector EM are in their first stage; quite frequently, scholars adopt the same approaches and methods used in private-sector research or develop hypotheses based on findings emerging from previous studies (e.g. Ibrahim et al., 2019). While the contributions that investigated local governments considered the New Public Management paradigm (Vinnari and Näsi, 2008), none sought to develop a new framework. However, it should be observed that several articles, rather than uncritically relying on theories imported from the private sector, used a theoretical lens that is specific for the public sector, such as the public motivation theory (Greenwood et al., 2017), public choice theory (e.g. Ferreira et al., 2013; Cohen et al., 2019) and politico-economic theory (Stalebrink and Donatella, 2021).

4.8 Authors

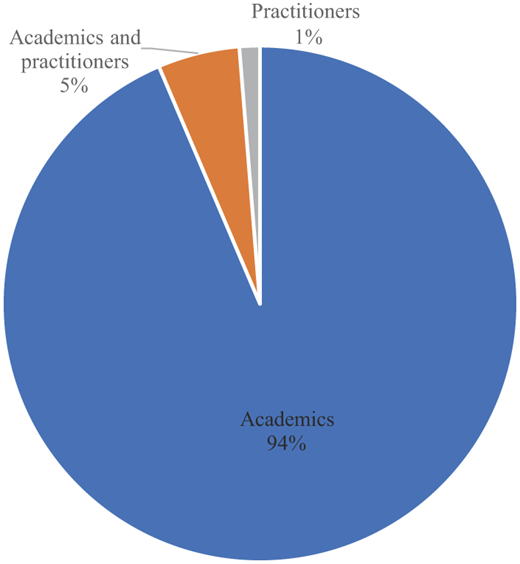

Category (I) refers to “academics and practitioners”; it aims to assess the extent to which EM studies include practitioners' points of view, either alone or jointly with academics. The inclusion of this category is motivated by the debate among academics and practitioners about public-sector accounting and accountability (Manes-Rossi et al., 2020), which has shown that academic research has had a moderate impact on accounting practices (Steccolini, 2019).

Indeed, the results emerging from the analysis (Figure 12) support the idea of such a limited influence, as 73 out of the 78 articles (about 94%) were written by academics, while only four articles (von Hagen and Wolff, 2006; Cheng et al., 2010; Melo et al., 2014; Kartiko et al., 2018) were written by a team that included at least one practitioner.

5. The future of earnings management research in public-sector organizations: developing future research paths

The results presented above illustrate that EM in public-sector organizations is an emerging area of research. The vast majority of articles have been published in the past decade, with an increasing trend from 2014 onwards. However, although the literature covers different jurisdictions and types of organizations from several continents, the number of published articles is still rather limited. More research is needed to offer further insight into the topic of EM in public-sector organizations. Towards this end, we propose several strategies to guide future research within the three streams of literature we identified on EM in public-sector organizations.

5.1 Three streams of literature

It is evident that this area of research is not particularly well integrated. There is a general separation between macro-level studies, which are rooted in the economics literature, and micro-level studies, with their origins in the accounting literature. The latter implicitly or explicitly tends to build on EM studies from private-sector organizations, in terms of theory and/or methods used.

Additionally, there is also a separation between micro-level studies centered on EM in state-owned enterprises on the one hand, and EM in sub-national governments or entities operating within national or sub-national governments on the other hand. This separation could be explained by most published articles on EM in state-owned enterprises focus on entities listed in China. The fact that these entities are publicly traded, along with country-specific differences between the political environment of China and those of America, Europe and Oceania can reduce the transferability of these results. However, neither Capalbo et al. (2014), who analyzed EM by unlisted state-owned enterprises in Italy, nor Gaio and Pinto (2018), who analyzed EM by both listed and unlisted state-owned enterprises in a large number of European countries, mention studies addressing EM in governments, or are cited by the studies centered on EM in a government setting. Instead, published articles on EM in state-owned enterprises tend to be cited by the private-sector EM literature.

Taking these factors into consideration, there exists three more or less parallel streams of literature on EM in public-sector organizations: one on national governments, another on sub-national governments and entities operating within national or sub-national governments, and a third on state-owned enterprises. As this research area matures, these streams of literature ought to be able to benefit more from each other.

The three streams of literature, individually and collectively, offer convincing empirical evidence that EM exists in public-sector organizations. Clearly, certain circumstances stimulate public-sector organizations to take advantage of discretion in the accounting process (i.e. they use accounting EM) or structure transactions (i.e. they use real EM) to pursue financial goals that are perceived to be consequential. However, the motivations for and impacts of EM are not as well understood as the basic issue of whether or not these practices exist in public-sector organizations. It is also noteworthy that the streams of literature, centered on national and sub-national governments or entities operating within them, have given scant consideration to enforcement mechanisms role in supporting high-quality financial reporting or national/statistical data. In the context of governments, only a few micro-level studies relate EM proxies to audit characteristics (e.g. Kido et al., 2012; Beck, 2018; Donatella et al., 2019; Stalebrink and Dontella, 2021) or auditees perception of the competence and expertise of their auditors (Anessi-Pessina and Sicilia, 2020). A more direct approach to measure the effect of audit was used by Greenwood and Zhan (2019), who drew inferences based on analysis of pre- and post-audit financial statements. Interestingly, their results indicate that audit adjustments are not homogeneous. Rather, auditors seem to be more prone to mitigate EM in situations of pre-audit deficit than pre-audit surplus.

5.2 Strategies for future research

Based on the insights from the critical analysis of the EM literature in the public-sector context, several potential future EM research paths can be identified. Below, several strategies are proposed to develop further insights into EM practices in the public-sector context.

First, there is potential for development in the positivistic approach that dominates the current literature. Most published articles on EM in public-sector organizations are based on quantitative empirical analysis. As EM cannot be directly observed, the outcome variables in these studies are typically designed to capture abnormalities in the financial reporting and/or transactions interpreted as EM. The indirect measures used to proxy EM in micro-level studies are typically influenced by the private-sector EM literature approach. For example, the Jones model (Jones, 1991) and the modified Jones model (e.g. Dechow et al., 1995) are widely used to proxy accounting EM. Undoubtedly, in micro-level studies centered on state-owned enterprises, this approach is as relevant as it is in research on the private sector. The essential difference between state- and non-state-owned enterprises lies in the ownership structure. By contrast, the transfer of approaches originally developed and used in private-sector EM studies may not be as straightforward for micro-level studies centered on sub-national governments or entities operating within national and sub-national governments. Here, differences in the nature of the underlying transactions exist, and there are also typically differences in the regulatory framework for financial reporting. Consequently, within this stream of literature, there are several examples of studies that adjust existing models to account for jurisdiction-specific circumstances (e.g. Ballantine et al., 2007; Beck, 2018; Drew, 2018). There are also studies using models with essentially no adaptions (e.g. Pilcher and Van der Zahn, 2010; Ferreira et al., 2013; Cohen et al., 2019; Ibrahim et al., 2019) or studies that develop their own models that are not directly related to private-sector EM research (e.g. Stalebrink, 2007; Felix, 2015). Considering the diversity of models used in micro-level studies, and the indirect nature of the measures produced by these models, this calls for method development research that systematically compares and validates different EM models and, if justified, develops new models and approaches. As long as there is no established consensus on what model(s) to use to estimate accounting EM, we suggest that multiple proxies be used for the sake of robustness.

Second, alternative approaches could be fruitful. Such approaches can include, but may not be limited to, survey or interview studies. Considering that EM is a sensitive matter, access can be an issue that hinders such research. However, there is considerable publicly available data that can be used in case studies. One such example is Vinnari and Näsi (2008). In their case study of a Finnish municipality, they relied on various data sources, including newspaper articles, personal contact with governmental officials, budgets, annual reports and other publicly available governmental documents.

Third, almost half of the reviewed articles do not explicitly use theory to guide their analyses. More developed theoretical frameworks can improve future empirical research and allow further insight into both the factors that stimulate public-sector organizations to engage in EM and the factors that mitigate such practices. Theoretical testing could be refined through both country comparisons and changes in regulatory frameworks.

Country comparisons would allow analyses of how differences in incentives (e.g. strong versus weak balanced budget requirements) and enforcement mechanisms (e.g. different audit systems) affect EM in public-sector organizations. Comparative analysis, such as of differences in administrative traditions, accounting systems (Brusca et al., 2015), characteristics of political and election systems (including controlling for the effects due to the election years; Cohen et al., 2019), and specificities in the regulatory framework for financial reporting, may also be fruitful.

Changes in regulatory frameworks could stimulate researchers to use an event study or natural experiment approach that allows them to test more precise predictions (e.g. to test for income-increasing/decreasing EM, rather than absolute EM). This approach is frequently used in micro-level studies on state-owned enterprises (e.g. Mohamad et al., 2012; Ho et al., 2015; He et al., 2020). The ongoing process of privatization of state-owned enterprises in China and elsewhere and the regulatory changes that have been adopted in recent years have enabled the extensive use of such designs. Within the two other EM literature streams in public-sector organizations, this type of design exists but is less common. One example is von Hagen and Wolff (2006), who analyzed reporting by national governments before and after the implementation of the Maastricht Criteria. Other examples are Drew (2018), who studied EM under the compulsory amalgamation of local governments in New South Wales, and Anagnostopoulou and Stavropoulou (2021), who investigated EM before and after some National Health Service (NHS) hospitals in England were granted foundation trust status allowing them more autonomy. Interestingly, the results emerging from this last study indicate that NHS hospitals were engaged in income-increasing EM before applying for foundation trust status, and that the reported financial performance declined after that status was received. This empirical evidence gives credibility to the concerns raised in the NHS hospital context years ago by Ballantine et al. (2007, p. 421), namely, that “… continuing poor financial performance can only be disguised through the use of ever increasing discretionary accruals which, when they are ultimately reversed, can lead to an apparently sudden, significant and unanticipated deterioration in financial performance.”

Fourth, there is a need for research exploring what, if any, impact EM has on public-sector organizations. The relationship between EM practices and financial performance has recently been analyzed in some studies (e.g. Anagnostopoulou and Stavropoulou, 2021; Cohen and Malkogianni, 2021b), but the topic deserves more attention in future research. Although income-increasing and income-decreasing EM will obviously with time neutralize each other, it can still be harmful. For example, if income-increasing or income-decreasing EM consistently occur in one direction over a long period, that would be at the cost of intergenerational equity (Vinnari and Näsi, 2008; Donatella, 2020). Furthermore, when managers and politicians use EM to avoid disclosing true financial performance and health, the role of financial reporting and national/statistical data in ex post accountability and/or ex ante decision-making may be compromised, potentially delaying or hindering appropriate actions. Obviously, EM is only meaningful to be engaged in by rational managers and politicians if at least some stakeholders are unable or unwilling to fully comprehend its impact on the reported financial performance (Fields et al., 2001). Merging literature on users' needs (van Helden and Reichard, 2019) and EM in public-sector organizations may, therefore, prove advantageous. Such an approach has the potential to improve our understanding of how different stakeholder groups are affected by EM.

6. Conclusions

Before this research, there was no systematization of EM research in public-sector organizations. By utilizing an SLR methodology, we have systematically analyzed 78 articles published on EM in public-sector organizations during 1980–2021. As our literature review illustrates, most of these articles present empirical research, typically using quantitative analysis and a single-country design. Only two older articles use a commentary/normative/policy approach (Anthony, 1985; Hale, 1988), and one more recent article uses a literature review (Hodges, 2018). However, the latter is partial in scope: rather than providing a complete review of the research field, the article consists more of an in-depth discussion that builds on a limited sample of prior empirical research.

The SLR methodology helped systematize the research on EM in public-sector organizations. EM is an emerging area of research that has yet to be integrated. There are currently three separate streams of literature on EM in public-sector organizations: one on national governments, another on sub-national governments and entities operating within national or sub-national governments, and the third on state-owned enterprises.

Several strategies to guide future research are proposed. Considering the variety of models used to estimate accounting EM, method development research is needed to compare and validate different models systematically. Future research should utilize a comparative methodology and, if possible, take advantage of reforms to improve theory testing. Moreover, it is suggested that alternative approaches be used for theory development and to explore what, if any, impact EM has in public-sector organizations.

Several policy implications also emerge from this SLR, which ought to be of interest to practitioners and standard setters. First, the vast majority of EM research in public-sector organizations is examined and found in accrual-based systems. From a standard-setting perspective, this highlights the risks of financial reporting that relies heavily on professional judgment. Second, research in all three streams of literature proves that strict financial performance requirements, linked to financial statements or national/statistical data figures, encourage EM behavior (e.g. Dafflon and Rossi, 1999; von Hagen and Wolff, 2006; Cheng et al., 2010; Kido et al., 2012). Therefore, higher levels of governments and international organizations should be attentive when monitoring information from financial reporting or national/statistical data, which serve to illustrate the adherence to the targeted financial goals.

This study, as with all literature reviews, is not free from limitations. Although it adopted an SLR methodology, some contributions may be missing. The criteria used for the search, selection and analysis of relevant articles may also have influenced the results. Therefore, the transparent research methodology used for assessing and classifying each article included in this literature review is crucial, as it will allow future research to replicate and/or extend this study.

The authors would like to thank participants at the EGPA PSGXII Athens Virtual Workshop, January 20-21, 2021, and especially Ioanna Malkogianni, for their helpful comments on an earlier version of this paper. The authors would also like to thank the two anonymous reviewers, and the Editor for his great support.