This study, grounded in the theory of family financial socialization, aims to empirically investigate the influence of financial socialization within the family on the financial well-being of undergraduate students.

The data was collected using a purposive sampling method from undergraduate students of Punjab state. The research involved 242 university students in the state of Punjab. AMOS 20.0.0 was employed to assess the hypothesized relationships.

The results indicate a significant positive influence of family financial socialization on financial attitudes, financial self-efficacy and financial well-being among undergraduate students. Subsequent mediation analysis, utilizing bootstrapping in AMOS, revealed that both financial attitude and financial self-efficacy partially mediate the association between family financial socialization and financial well-being.

This study uniquely explores the direct and indirect effects of family financial socialization on undergraduate students’ financial well-being, highlighting the mediating roles of financial self-efficacy and financial attitude. It addresses a significant research gap in the Indian context, providing valuable insights for financial institutions and policymakers, suggesting strategies to enhance students’ financial well-being through targeted interventions based on family financial socialization.

Introduction

The overall well-being of an individual is very important, especially in terms of their financial situation. The study of a consumer’s money management, spending and investment behavior is becoming a crucial component in the field of financial well-being research. The complexity of making financial decisions has increased due to the accessibility of new financial services and products on a global scale. As the number of young people in the population rises, families are being required to make more informed financial decisions as a result of the economy’s bad tendencies. Additionally, the family serves as the main socialization agent, followed by siblings, friends, classmates and the media (Deenanath, Danes, & Jang, 2019; Rea, Danes, Serido, Borden, & Shim, 2019; Shim, Serido, Tang, & Card, 2015; Vijaykumar, 2022).

Now the structure of Indian families are changing from joint to nuclear (Vijaykumar, 2022). The majority of Indian youth are dependent on their parents, even after marriage, which causes them to lack confidence and well-being in taking financial decisions. Hence, the researchers are getting interested to investigate the methods to improve the financial well-being (Brüggen, Hogreve, Holmlund, Kabadayi, & Löfgren, 2017; Shim, Barber, Card, Xiao, & Serido, 2010). According to Shim et al. (2010), financial well-being is the overall satisfaction with one’s own financial situation. According to academic research, an increasing proportion of emerging adults in Western nations are experiencing financial struggle, which has a negative impact on well-being in a variety of spheres of life. Ndiango, Jaffu, and Kumburu (2023) demonstrated that the influence of personal values on research self-efficacy among academics in public universities in Tanzania means academics who prioritize openness to change values are driven by a desire for uniqueness and flexibility, enhancing their skills and confidence in research activities. Similarly, those who emphasize self-enhancement values are motivated by external rewards and social standards, boosting their confidence in research engagement. Mishra (2022) noted that both financial behavior and attitude can significantly impact financial well-being, with appropriate financial behavior and attitude potentially increasing chances of financial well-being by 50 and 18%, respectively, in comparison to those who are less proficient at exhibiting both.

Financial socialization is becoming a key concept that defines the financial behavior and financial well-being of emerging adults. According to Gudmunson and Danes (2011), financial socialization can come about as a result of discussions parents have with their children about money, children observing how their parents handle money, formal education in school, working a job and having first-hand experience with money. Various literature proposes that financial knowledge, financial self-efficacy and financial behaviors are all supposed to be influenced by financial socialization. Moreover, positive financial behavior influences positive financial well-being. A study by Ullah, Yusheng, Università, and Ss (2020) found that adults can enhance their financial well-being through the process of financial socialization. Therefore, the need for the investigation is evident from the prior literature. The emerging adults have been the focus of the majority of studies. This study aims to address the gap by focusing on the financial well-being of students, who are at a developmental stage where they are becoming more autonomous. Financial well-being and family financial socialization have received the least amount of research.

The specific objective of this study is to examine the direct and indirect effects of family financial socialization on financial well-being, with a focus on the roles of financial self-efficacy and financial attitude as mediators. This study makes a significant contribution by exploring the role of family financial socialization in influencing the financial well-being of undergraduate students, a relatively under-researched area. Additionally, the study examines the mediating roles of financial attitude and financial self-efficacy in the relationship between family financial socialization and financial well-being. According to Kaur, Singh, and Singh (2021), most research in financial well-being has been conducted in the United States, followed by Europe, with India lagging behind. Thus, this study addresses a critical gap by focusing on the Indian context, providing valuable insights for financial institutions and policymakers to enhance the financial well-being of young adults in India.

Literature review

Theoretical framework

This study adapted the family financial socialization theory proposed by Gudmunson and Danes (2011). Various evidence suggests that family financial theory gives a complete view of that, parent interactions influence financial attitude, financial satisfaction, financial capability and financial literacy. The term consumer socialization was introduced by Ward (1974), which describes a method by which young people acquire skills, knowledge and attitudes relevant to their functioning as consumers in the marketplace. However, Gudmunson and Danes (2011) claim that consumer socialization is limited to only children. Danes (1994) defined financial socialization as “the process of acquiring and developing values, attitudes, standards, norms, knowledge, and behaviors that contribute to the financial viability and well-being of the individual” (p. 128). Various literature has revealed that parents are the primary agents of the young adults, followed by siblings, friends, peers and media (Deenanath et al., 2019; Shim et al., 2015; Vijaykumar, 2022). The family financial socialization theory has been divided into two segments: financial socialization processes and financial outcomes. Both dimensions are necessary for this study. Individual and family characteristics that impact family interaction and relationships as well as purposeful financial socialization, are included in the family financial socialization theory. The outcome of this theory is financial attitude, knowledge and skills that affect financial behavior and financial well-being. The financial attitude, knowledge and capability play a mediating role between the financial process and socialization outcome (Kim & Torquati, 2020).

Financial well-being

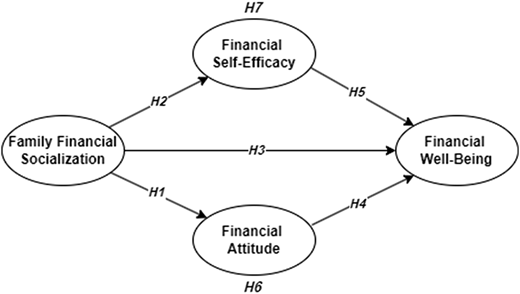

Now a days financial well-being is becoming popular in the field of behavioral financing. However, the term “financial well-being” has no commonly accepted definition (Brüggen et al., 2017). However, CFBP (2015) defines financial well-being as a state in which an individual can meet current and future financial obligations, feels secure about their financial future and has the ability to make choices that enhance their quality of life. Gutter, Garrison and Copur (2010) looked into the association among financial behavior and financial well-being and came to the conclusion that students’ good financial behavior is positively connected to their financial well-being and that their financial well-being will only be high if they have good financial attitudes. Similarly, a longitudinal study by Allsop, Boyack, Hill, Loderup, and Timmons (2021) the study had also concluded that a higher level of financial behavior provides higher financial satisfaction in emerging adults. Various researchers found relationship of various factors such as skills, attitude and knowledge with financial behavior, which directly effects the financial well-being of individuals (Selvia, Rahmayanti, Afandy, & Zoraya, 2021). However, this research will demonstrate how financial self-efficacy and financial attitude might influence financial well-being as a result of familial financial socialization. Additionally, prior research indicated that the majority of the study on financial well-being was conducted in developed economies. Therefore, it is necessary to do studies in other developing nations as well (Brüggen et al., 2017; Lusardi & Mitchell, 2014; Shim et al., 2010). Hence, based on the previous literature, Figure 1 demonstrates the proposed model of the study.

Family financial socialization

Adults acquire knowledge, skills from various socialization agents and improves their own behavior. According to previous studies, family is considered as one of the most important socialization agent. Jorgensen, Rappleyea, Schweichler, Fang, and Moran (2016), Rea et al. (2019) confirmed in their studies that better the family financial socialization then better the financial decisions will be. A longitudinal study by Shim et al. (2010) revealed that a positive change in financial socialization gives a positive change in financial attitude as well as financial controllability and financial self-efficacy. In order to explore the effects of financial socialization on young people’ financial and subjective well-being, the study by Khawar and Sarwar (2021) develops an integrated conceptual framework and revealed that through financial knowledge, motivating variables, financial ability and financial management behavior, early financial socialization experiences can specifically affect young adults’ subjective and financial well-being.

Mahapatra, Xiao, Mishra, and Meng (2024) examine the influence of parental financial socialization on the life satisfaction of college students in India, highlighting the mediating role of desirable financial behavior. Their findings indicate that direct parental teaching enhances students’ financial behavior, which in turn improves life satisfaction. Additionally, the study identifies that parental education negatively moderates this relationship, suggesting that higher parental education levels may reduce the effectiveness of financial socialization. In accordance with LeBaron-Black et al. (2022), to improve the financial well-being of the children, parents should provide experimental learning rather than straightforward lecturing. The recent study by Madinga, Maziriri, Chuchu, and Magoda (2022) states that a higher level of financial socialization provides a higher level of financial risk attitude. A study by Kaur (2024) demonstrates that family financial socialization explains 28.8% of the variation in financial self-efficacy among university students in Punjab. This means that students who receive more financial guidance from their families tend to have higher confidence in managing their finances, but other factors also play a role. Similarly, Ullah et al. (2020) emphasized the value of having conversations with parents and teachers, as it fosters greater confidence in handling money-related issues. Adults are also capable of handling financial issues, which will enhance financial well-being. Moreover, Sirsch, Zupan, Levec, and Friedlmeier (2020) investigate the impact of parental financial socialization on first-year university students in Austria and Slovenia. Their study reveals significant links between recollected parental socialization experiences and students’ financial outcomes, including self-perceived financial learning and behavioral control. Financial knowledge and behavioral control were found to mediate the relationship between socialization experiences and students’ financial behavior, relationships with parents, and financial satisfaction. Hence, based on the literature, the following hypotheses were formulated:

Family financial socialization positively influences financial attitude.

Family financial socialization positively influences financial self-efficacy.

Family financial socialization positively influences financial well-being.

Financial attitude

According to Marsh (2006), attitude refers to how a person feels about personal financial problems, as measured by the response to a statement or opinion. Similarly, Radianto (2020) defined that Financial attitude is a mindset that can influence how someone manages their finances. Researchers have discovered many money attitudes that pinpoint people’s actions when it comes to financial issues. As stated by Shim et al. (2010), financial attitude is a key aspect of financial well-being. Young adults’ financial literacy will rise if they receive adequate family support, according to a study by Yong, Yew, and Wee (2018) that looked into how financial literacy, attitude and knowledge relate to one another. The study established a direct correlation between financial knowledge and attitude and achievement oriented. Parental financial socialization plays a pivotal role in shaping financial attitudes among young adults. The findings indicate that parental financial socialization has a significant impact on Gen-Z’s financial attitude (F = 1.912, p < 0.05). The F-value suggests that the variance between groups is greater than the variance within groups, reinforcing the notion that differences in parental financial socialization significantly influence financial attitudes among young individuals (Abdul Ghafoor & Akhtar, 2024). Likewise, a study by Utkarsh, Pandey, Ashta, Spiegelman, and Sutan (2020) examined the financial well-being of first-year postgraduate students and concluded that financial attitude is a strong predictor of financial well-being. A longitudinal study by Serido et al. (2015) examined the influence of parental financial on students’ financial attitude and financial behavior and by supporting to Ajzen (1991), the results exerted that the financial behavior of the partner positively influenced the students’ financial attitude. Hence, the following hypothesis was formulated:

Financial attitude positively influences financial well-being.

Financial self-efficacy

According to Bandura (1977), self-efficacy denotes to people’s confidence in their capability to generate performance. Adding to the statement, Rothwell, Khan, and Cherney (2016) depicted that financial self-efficacy is the term used to describe a person’s attitudes, beliefs and level of independence when making financial decisions. Leon (2020) counsels that in the theory of social cognition, self-efficacy is a commonly accepted basis. Adding to that, Herawati, Candiasa, Yadnyana, and Suharsono’s (2020) study conducted on 518 undergraduate accounting students in Bali with the goal of analyzing the relationship between financial learning quality and parental socioeconomic status on financial self-efficacy revealed that financial learning quality and parental socioeconomic status have no direct impact on financial self-efficacy, whereas financial literacy has a direct impact. Also, Zhao and Zhang (2020) empirically investigate the impact of family financial socialization on individuals’ financial outcomes, including financial literacy, behavior and well-being, using data from 6,311 US respondents. Their study, grounded in family financial socialization theory (FFST), finds that parental financial socialization positively influences all three outcomes. This study is one of the first to empirically explore these relationships, highlighting the long-term impact of parental financial socialization on financial outcomes in adulthood. A recent study by Lone and Bhat (2024) investigates the influence of financial literacy on financial well-being among business school faculty members, emphasizing the mediating role of financial self-efficacy. Their study, conducted with 203 faculty members, employs structural equation modeling to reveal that financial literacy significantly enhances both financial self-efficacy and financial well-being. Notably, financial self-efficacy partially mediates the relationship between financial literacy and financial well-being. Based on this discussion, the study hypothesizes that

Financial self-efficacy positively influences financial well-being

Mediating role of financial attitude and financial self-efficacy

A study by Rothwell et al. (2016) in his empirical investigation, in which he aimed to make inferences about the mediation role of financial self-efficacy in the association among financial knowledge and higher education saving, is wholly positive and significant. A study by Amer Azlan et al. (2016) on 1728 undergraduate students demonstrated that positive financial literacy improves the financial attitude of the students, but the association between financial literacy and saving behavior is not mediated by financial attitude. A related survey by Susilowati, Kardiyem, and Latifah (2020) explored the Economics Faculty of State University of Semarang students with 230 respondents and resulted that financial attitude and literacy improved about money matters and increased their propensity to engage in better financial behavior, like on-time bill payment and having a balanced budget. Herawati et al. (2020) conducted a study on undergraduate accounting students in Bali. Using the proportional multi-stage random sampling technique, the 561 students were selected for the sample. The primary goal of the study by Zia-ur-Rehman et al. (2021) was to investigate several elements that ultimately influence an individual’s financial well-being of customers in Pakistan. The results demonstrated that individuals’ perceived self-efficacy improves as a result of transparently communicated information, which results in financial well-being. Zhao and Zhang (2020) investigated self-efficacy as a mediating function in the growth of students’ entrepreneurial intentions. But the author also revealed that self-efficacy is not playing a mediating role for gender. Also mediating role for self-efficacy in the relationship of all three variables, i.e. entrepreneurial experience, risk propensity and entrepreneurial intention. The hypothesis developed was as follows:

Financial attitude mediates the relationship between family financial socialization and financial well-being.

Financial self-efficacy mediates the relationship between family financial socialization and financial well-being.

Research methodology

Research design

To study the role of family financial socialization on financial well-being, a descriptive study with a quantitative approach was carried out on the university students of Punjab in various fields like commerce, arts, science and humanities in both public and private universities.

Participants and procedure

The data was collected using a purposive sampling method from undergraduate students of the Punjab State between the ages of 19 and 25 years. The rationale for selecting undergraduate students as the target audience was based on the supposition that this group is at a stage where they are overly dependent on their families and are transitioning from being dependent to being independent with regard to financial matters. Also, in accordance with Indian culture, most Indian young adults adhere to their parents’ rules and regulations (Vijaykumar, 2022).

The sample size for this study was determined using the “G*Power” software version 3.1.9.6 (Faul, Erdfelder, Buchner, & Lang, 2007), adhering to the guidelines established by Cohen (1998). An a priori sample size calculation, based on a medium effect size of 0.3, an alpha level of 0.05 and a power of 0.80, indicated that a minimum of 134 participants was required.

According to Cohen (1992), larger sample sizes increase the statistical power of a study, enhancing the ability to detect significant effects and relationships within the data. Consequently, the survey link, hosted on Google Forms, was distributed to 300 undergraduate students via social media platforms, such as Facebook, WhatsApp and email, following the recommendations of Carini, Hayek, Kuh, Kennedy, and Ouimet (2003), who found digital surveys to be more effective than traditional paper-based methods. This approach ensured a statistically robust sample, allowing for meaningful analysis and generalizable findings across the broader population of undergraduate students in the Punjab region. An 80.67% response rate was achieved, yielding 242 responses, which were complete and met the study’s criteria. Demographic information of the participants was computed (Table 1).

The demographic profile of the respondents shows a diverse range of characteristics. Age-wise, participants are spread across different brackets: 17.9% are 19–20 years old, 31.7% are 21–22, 23.2% are 22–23 and 27.2% are 24–25. The gender distribution is 58.5% female and 41.5% male. In terms of marital status, 11.6% are married while 88.4% are unmarried. Most respondents are undergraduates (75.4%), with the remainder having other qualifications. The fields of study include commerce (39.3%), management (26.3%), arts (12.9%), science (14.7%), engineering (4.9%) and other areas (1.8%). A majority of students attend public universities (90.2%), and family types are split between nuclear (53.1%) and joint (46.9%). Regarding living arrangements, 41.1% co-reside with parents, 25.4% live independently and 33.5% semi-reside with parents. Financial independence is reported by 31.3% of respondents. Employment status shows 44.2% are not working, 27.7% work full-time, 19.2% are self-employed and 8.9% work part-time. Monthly family income varies, with the largest groups earning Rs. 20,000–40,000 (28.1%) and above Rs. 80,000 (24.6%). Education levels of fathers indicate 38.8% have high school or lower education, while 33.0% of mothers have a similar education level. Employment status reveals that 36.2% of fathers are self-employed, while 84.4% of mothers are not employed.

Measures

The questionnaire was comprised of two sections: Section I consist of demographic details, and Section II consists of questions on family financial socialization, financial attitude, financial self-efficacy and financial well-being. All the statements were measured using a five-point Likert scale 1 (Strongly Disagree) to 5 (Strongly Agree). Before completing the questionnaire, students were provided with and signed a consent form to ensure informed participation.

Family financial socialization was determined using a six-item scale adapted from Shim et al. (2010), which included questions about “the discussion of family financial matters” and “parental teaching on the importance of savings.” Financial attitude was measured using a nine-item scale adapted from Shockey (2002), which included questions such as “the importance of controlling monthly expenses” and “establishing financial targets for the future.” The present study utilized a six-item financial self-efficacy scale developed by Lown (2011). The scale included statements such as “It is hard to stick to my spending plan when unexpected expenses arise” and “It is challenging to make progress toward my financial goals.” Financial well-being was measured using a six-item scale developed by CFPB (2015), which included statements such as “I could handle a major unexpected expense,” “I am just getting by financially,” and “I am concerned that the money I have or will save won’t be enough.” The descriptive statistics are as follows:

Table 2 indicate the descriptive statistics of key financial constructs, i.e. family financial socialization (FFS), financial attitude (FA), financial self-efficacy (FSE) and financial well-being (FWB) reveal that, parental discussions about saving had the highest mean (M = 4.07), while topics related to credit management, such as establishing a credit rating and using credit cards, had lower means (M = 2.90–2.98). In terms of financial attitude, respondents strongly valued saving (M = 4.05) and controlling expenses (M = 3.93), but adherence to structured financial planning, such as setting financial targets (M = 3.78) and following an expense plan (M = 3.78), showed slightly lower emphasis. Financial self-efficacy results indicated moderate confidence in managing finances (M = 3.15–3.93), yet challenges in problem-solving financial difficulties (M = 3.43) suggest room for improvement. Lastly, financial well-being scores reflected financial insecurity, with many respondents feeling they were just getting by (M = 3.40) and expressing concerns about insufficient savings (M = 2.90).

Data analysis

Procedure

The data analysis procedure in this study was conducted in accordance with the methodological approach outlined by Sachdeva and Lehal (2023). The SPSS 23 and AMOS 20.0.0 graphics programs were used to examine the information gathered from the surveys. Both the measurement model and the structural model were tested using AMOS 20.0.0’s maximum likelihood estimator. Because the accepted scales had adequate empirical and theoretical assistance, confirmatory factor analysis (CFA) was used directly rather than exploratory factor analysis (EFA) (Hurley et al., 1997). The factor structure was validated through CFA (Brown, 2015). Discriminant validity examined the impact of unrelated factors, whereas convergent validity evaluated the degree of correlation between the variables in the parent concept. The mediation impact of financial attitude and financial self-efficacy was examined using the bootstrapping approach.

Measurement model

To evaluate the validity and reliability of the constructs, a confirmatory factor analysis model was created using Analysis of Moments Structures (AMOS) version 20. First, we assessed the factor loadings (Table 3). Items with loadings greater than 0.60 were deemed acceptable, as shown in Table 3. (Hair, Black, Babin, & Anderson, 2010). Items that didn’t fit the requirements (FA7, FA8, FA9, FWB4, FWB5 and FWB6) were eliminated. According to Ab Hamid, Sami, and Mohmad Sidek (2017), the composite reliability (CR) values exceeded 0.70. Additionally, all components have Cronbach’s alpha coefficients above 0.70, indicating superior composite reliability.

The study also used the Fornell and Larcker (1981) criterion to evaluate discriminant validity. Table 4 demonstrates that the discriminant validity of the components was confirmed since the square root of the AVE was greater than the inter-construct correlations (Hair, Black, Babin, & Anderson, 2010). These findings therefore validated the validity of the constructs and the reliability of the instrument.

The results showed that the proposed model fit the data well. Tucker–Lewis Index (TLI) and CFI (comparative fit index) values should be more than 0.9 for a satisfactory model fit (Bentler & Bonett, 1980). Additionally, Hair, Black, Babin, and Anderson (2010) state that a model’s fit may be improved by ensuring that its root mean square error of approximation (RMSEA) and standardized root mean square residual (SRMR) values are less than 0.08. For an acceptable fit, the goodness-of-fit index (GFI) value should be more than 0.80. We were able to move forward with the structural model estimate and hypothesis testing as the model provided adequate support overall. In Table 5, the model fit index values are displayed.

Common method bias

When data is collected from the same respondents at a single moment in time, the likelihood of common method bias (CMB) increases (Podsakoff, MacKenzie, & Podsakoff, 2012). Four factors with Eigenvalues over 1 were identified by Harman’s single-factor test in SPSS; the first component only explained 46.83% of the total variance, which is less than the 50% criterion. This verified that CMB was not present.

Hypothesis testing

The hypothesis testing was assessed in order to determine the relationships between the variables, both direct and indirect via a structural equation model. Table 6 indicates that family financial socialization had a significant positive influence on all three aspects, i.e. financial attitude (β = 0.370, p < 0.005), financial self-efficacy (β = 0.187, p < 0.005) and financial well-being (β = 0.303, p < 0.005). Thus, H1, H2 and H3 were supported. Moreover, both financial attitude (β = 0.245, p < 0.005) and financial self-efficacy (β = 0.952, p < 0.005) had a significant positive influence on financial well-being. Thus, findings of the study also support H4 and H5.

The study then evaluated how financial attitude and financial self-efficacy mediate the relationship between family financial socialization and financial well-being. The results revealed a significant indirect effect of family financial socialization on financial well-being through financial attitude (β = 0.071, t = 10.232). Thus, H6 was supported. The study also found a significant indirect effect of family financial socialization on financial well-being through financial self-efficacy (β = 0.141, t = 3.559). Thus, H7 was also supported. Furthermore, the direct effect of family financial socialization on financial well-being in the presence of mediators was also found significant (β = 0.303, p < 0.005). Hence, both financial attitude and financial self-efficacy partially mediate the relationship between family financial socialization and financial well-being, as both the direct and indirect effects were significant (Table 7).

Discussion

The study employed structural equation modeling to support the model of family financial socialization theory put forth by Gudmunson and Danes (2011). The study particularly focused on the relationship between family financial socialization, financial attitude, financial self-efficacy and financial well-being of undergraduate students. The positive and significant relationship between the variables and overall model fit impart to validate the conceptual model of Gudmunson and Danes. The study also investigated how financial self-efficacy and financial attitude mediate the relationship between family financial socialization and financial well-being.

Findings of the study are similar to Kumar, Rani, Rani, and Sarker (2023), LeBaron-Black et al. (2022), Rea et al. (2019), Utkarsh et al. (2020) and Deenanath et al. (2019), that family financial socialization positively influences the financial attitude and financial self-efficacy, which in turn, positively affects the financial well-being. This outcome recommends that better parental financial communication allows the students to manage financial matters efficiently and confidently, which will improve the overall financial satisfaction of students. Moreover, a supportive family environment fosters open discussions about finances, which boosts students’ confidence in managing their own money. This empowerment allows them to make informed financial decisions, avoid debt and save for future needs, all of which contribute to improved financial well-being. Drever et al. (2015) state that parents are important socialization agents that help in improving the financial decision-making among adults. In the majority of the studies, financial attitude and financial self-efficacy were considered as important variables to measure the financial well-being and financial behavior of individuals (Shim et al., 2015; Sabri, Wijekoon, & Rahim, 2020; Vijaykumar, 2022).

The study’s findings also revealed a positive correlation between the financial attitudes of undergraduate students and their financial well-being. The literature supported this finding, as Pak, Fan, and Chatterjee (2023) demonstrate that positive financial attitudes lead to informed decision-making and reduced financial stress, all of which enhance financial stability and overall well-being of young adults. Empirical evidence supports that individuals with positive financial attitudes tend to achieve better financial outcomes. Similarly, the results of Fan and Park (2021) demonstrate financial self-efficacy positively influences the financial well-being of young adults because it boosts their confidence in managing money, leading to better financial decisions and behaviors. This empowerment helps them effectively handle financial challenges and reduces stress, thereby enhancing their overall financial stability and well-being. Empirical studies consistently show that higher financial self-efficacy is associated with improved financial outcomes.

The results of the present study revealed that both financial attitude and financial self-efficacy play a mediating role in the relationship between family financial socialization and financial well-being. These improved decisions, driven by positive attitudes and higher self-efficacy, lead to greater financial stability and overall well-being. This mediating effect highlights the critical role of family influence in equipping individuals with the necessary skills, knowledge and confidence to achieve and maintain financial success throughout their lives. The findings underscore the interconnected nature of family financial socialization, individual financial attitudes and self-efficacy in promoting long-term financial well-being. Various empirical studies were in support of this findings (Ariati, Dharma Buchdadi, & Gurendrawati, 2023; Zhao & Zhang, 2020). Overall, by demonstrating the significance of parental financial socialization in fostering financial well-being and outlining the impact of attitude toward money, this study makes a contribution to the field of young adults’ financial well-being. This shows that early parental involvement in the form of financial socialization at a young age can result in better financial well-being. According to Ullah et al. (2020), individuals’ interactions with others are likely to have an impact on their financial decisions.

Conclusion

This study is most likely investigating the financial well-being of students in the state of Punjab. Due to practical knowledge with money, age maturity enhances young adults’ financial well-being. In conclusion, this study validates that family financial socialization positively influences financial attitudes and self-efficacy, which in turn enhance financial well-being among undergraduate students. The findings align with previous research, highlighting that effective parental financial communication and involvement are crucial for developing confident and informed financial decision-making. The study also confirms that financial attitude and self-efficacy mediate the relationship between family financial socialization and financial well-being, these insights contribute to the understanding of how early parental guidance can shape the financial health of young adults, offering valuable implications for both educational practices and family financial education.

Implications

The findings of this study have significant implications for educators, policymakers and community organizations. Educational institutions should integrate financial education programs that highlight the role of family in financial socialization, thereby helping students develop positive financial attitudes and self-efficacy, which are critical for financial well-being. Additionally, policymakers and community organizations should promote family involvement in financial education initiatives through workshops and seminars aimed at parents, equipping them to effectively impart financial knowledge to their children. Financial literacy curricula should extend beyond technical skills to include fostering positive financial attitudes and self-efficacy, ensuring students are better prepared to manage their finances. Universities should also provide counseling and support services focused on building financial confidence and reducing financial stress among students. Policymakers can create programs that encourage both parents and children to make strong communication related to the importance of savings, family income, spending behavior and financial products. These positive discussions will enhance financial well-being. By addressing these areas, stakeholders can significantly improve the financial development and stability of undergraduate students.

Limitation and future insights of the study

This study is limited by its focus on a single geographic region, the state of Punjab, which may affect the generalizability of the findings to other regions or countries with different cultural or socioeconomic contexts. The sample size of 224 university students, while sufficient for the analysis, may not fully represent the diversity of financial experiences and backgrounds among undergraduate students. Moreover, data from a single informant were used in the study. To present a more complex view of this problem from several other perspectives, a multiple informant method is required. The study only looked at parents as a source of financial socialization; further research is required on other agents, including peers, teachers and groups. The study took into account the fewest possible variables. There should be a wider number of factors (e.g. financial knowledge, financial stress, behavior control, role modeling, parenting style and more).