The increased interest among academicians to explore more about tax management behavior is evident in the literature on corporate tax avoidance. This paper aims to illustrate the multiple aspects that influence the tax avoidance behavior of corporations and its impacts through the systematic review method.

This study used “Tax Avoidance” OR “Tax Aggressiveness” OR “Tax Planning” as search strings to extract the relevant literature from the Scopus database. This study is a comprehensive analysis of existing literature on corporate tax avoidance behavior. Further, the keyword network analysis has been used to find out the most explored and dry research areas related to corporate tax avoidance behavior using VOSviewer software.

The study finds that taxation decision is an important managerial decision. Managers adopt tax avoidance tactics to boost postax profits to meet the shareholders’ expectations, particularly of risk-averse shareholders, and sometimes for their benefit also. With this, this study also finds that firms’ characteristics, political connections and corporate social responsibility activities also impact taxation decisions. In addition, the study identifies that tax-avoiding behavior has a contradictory impact on firm value, market growth and corporate transparency disclosure decisions.

The study assists the researchers by providing a brief overview of tax avoidance behavior, for corporates in understanding the implications of tax avoidance, and for policymakers to fix the taxation loopholes and bring necessary tax reforms.

This study adds to the existing literature by providing a thorough overview of theories, determinants and outcomes of corporate tax avoidance behavior.

1. Introduction

Tax is the largest source of income for the government, and a major portion of it comes from direct taxes (Gober & Burns, 1997). Corporate tax is a type of direct tax and it is the responsibility of the companies to make the payment of their fair share of tax to the government (Rao & Chakraborty, 2010). The taxes are the fixed charge against the company’s profit and reduce the available distributed profit to the shareholders (Putra, dwi, & Sriwedari, 2018).

Companies adopt acceptable (tax management) and non-acceptable (tax evasion) methods to reduce their tax liability (Aliani, 2013). Tax avoidance is legal and is done by taking advantage of tax loopholes, in contrast, tax evasion violates taxation rules and is punishable and unacceptable (Fisher, 2014).

Corporate tax avoidance is arising as a matter of public concern and getting researchers’ attention continuously (Desai & Dharmapala, 2006; Hanlon & Heitzman, 2010; Huang, Ying, & Shen, 2018; Putra et al., 2018). Tax avoidance activities are the result of privileges and reliefs provided by the government to the companies. Companies are adopting different techniques such as more investment in fixed assets, profit shifting to tax haven countries, base erosion, thin capitalization, IP structuring, etc., for reducing their tax liability (Ey, 2014). Around $650bn in revenue has been lost by governments across the world due to the shifting of nearly 40% of total profits by multinational companies to tax haven countries.

There is not any universal definition of tax avoidance. The concept of tax avoidance has been defined by different authors in their own words, such as Hanlon and Heitzman (2010, p. 137) describe tax avoidance as “a continuum of tax planning strategies where perfectly legal activities are at one end, and more aggressive activities would be closer to the other end”, and Dyreng, Hanlon, and Maydew (2010) state that all financial transactions that lead to a reduction in tax liability reflect the tax avoidance behavior of the firm.

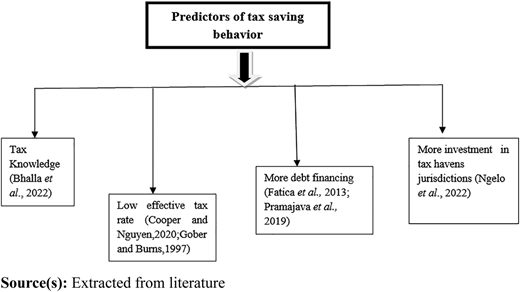

Tax avoidance is a legal way of reducing the tax burden (Slemrod, 2004; Slemrod & Gillitzer, 2014). While tax evasion refers to the destruction of original documents, the production of fake financial statements, the alteration of original entries and any other activity that accounts for tax sheltering (Gottschalk, 2010; Malkawi & Haloush, 2008). The available literature (Foster Back, 2013; Lenz, 2020) states tax avoidance, tax management and tax planning are all simultaneous terms while tax evasion is an unlawful act of tax reduction. The firms having the following features are considered “low-tax” firms (Figure 1).

The paper has been categorized into the following sections. The second section briefly explains the theories of corporate tax avoidance behavior and theoretical background of the study, the third section is related to research methodology, the fourth section is related to results, the fifth section is about keywords networking analysis and the last section reports the conclusion, implications and unexplored areas for further research.

2. Theories of corporate tax avoidance

Tax avoidance decisions are considered as the shifting of funds from the government to the businesses by legal means (Khuong et al., 2020). However, the adoption of tax avoidance behavior in an organization is influenced by (a) agency issues arising from the separation of management and shareholders, (b) social needs and (c) the legitimacy of tax avoidance decisions.

1. Traditional concept and agency theory

Traditional theory suggests that tax avoidance activities reduce tax liability and increase the shareholders’ value (Boussaidi & Hamed-Sidhom, 2020; Nugroho & Agustia, 2017). While on the other hand, tax planning is considered the managers’ follow-up action, making tax reductions by not violating the taxation provisions (Putra et al., 2018). To avoid detection from taxation authorities, managers create sophisticated transactions for tax avoidance purposes. Managers use these transactions to hide their tax avoidance practices from the taxation authorities, but sometimes also for hiding from investors.

2. Social obligation approach

Tax avoidance behavior is considered a sign of irresponsible behavior toward society (Hoi, Wu, & Zhang, 2013; Chircop, Fabrizi, Ipino, & Parbonetti, 2018). Slemrod (2004) explained that the firms with high corporate social responsibility (CSR) scores are more cautious about tax avoidance practices. These firms avoid tax-aggressive decisions because the detection of such behavior offsets the positive effects of CSR practices (Lanis & Richardson, 2015) and also causes reputational damages to the firms (Ortas & Gallego-Álvarez, 2020). In contrast, Landry, Deslandes, and Fortin (2013) and Mahon (2002) stated that corporate tax avoidance behavior leads to more tax administration penalties and reputational costs to the firm. CSR disclosure is considered a risk management function by the firms and is preferred to strengthen investors’ beliefs and community concern toward the firm performance (Hanlon & Slemrod, 2009). More tax-avoiding firms disclose high CSR practices to hide such practices (Abdelfattah & Aboud, 2020; Gras-Gil, Palacios Manzano, & Hernández Fernández, 2016).

3. Legitimacy approach

Like other taxpayers, it is also the right of the company to minimize its tax obligations but within the boundaries of the law (Hasseldine & Morris, 2013; Whait, Christ, Ortas, & Burritt, 2018). Managers do not consider tax avoidance as unacceptable and enormous activity. Instead, it is a choice-based decision adopted for higher profits, status and high remuneration expectations (Sikka, 2010). Tax avoidance decisions, on the other hand, have been subjected to a slew of criticisms. Transfer pricing schemes have been used by some big firms, like Apple, Starbucks and Google, to evade taxes (Barford & Holt, 2013). Tax avoidance activities are considered inconsistent with societal expectations and create legitimacy risks for organizations (Christensen & Murphy, 2004).

2.1 Theoretical framework

A review-based study is considered the relevant form of research because it addresses all research evidence related to a particular research area (Baumeister & Leary, 1997; Murata, Wakabayashi, & Watanabe, 2014). The publications in the finance and accounting sectors have been selected for review purposes. Accounting scholars have a comparative advantage in reading and assessing income and expenditure measures from financial statements while financial literature deals with agency issues in the organization. Both of these theories are related to tax avoidance issues and are considered appropriate for review. By considering the significance of the review-based study, different authors have carried out the review-based study on tax avoidance behavior from different perspectives such as tax planning behavior of multinational enterprises (Cooper & Nguyen, 2020; Wang, Xu, Sun, & Cullinan, 2020), family firms (Khelil & Khlif, 2022), determinants (Sritharan, Salawati, Sharon, & Syubaili, 2022), proxies (Lee et al., 2015), institutional ownership (Putra et al., 2019), CSR disclosure (Jiang, Zhang, & Si, 2022) and corporate governance (Kovermann & Velte, 2019). Still, there is a lack of work that gives a thorough overview of the factors that contribute to tax avoidance decisions in corporations. This study is the first thorough, in-depth systematic study to provide insight into the theories, causes and effects of corporate tax avoidance behavior.

3. Research methodology

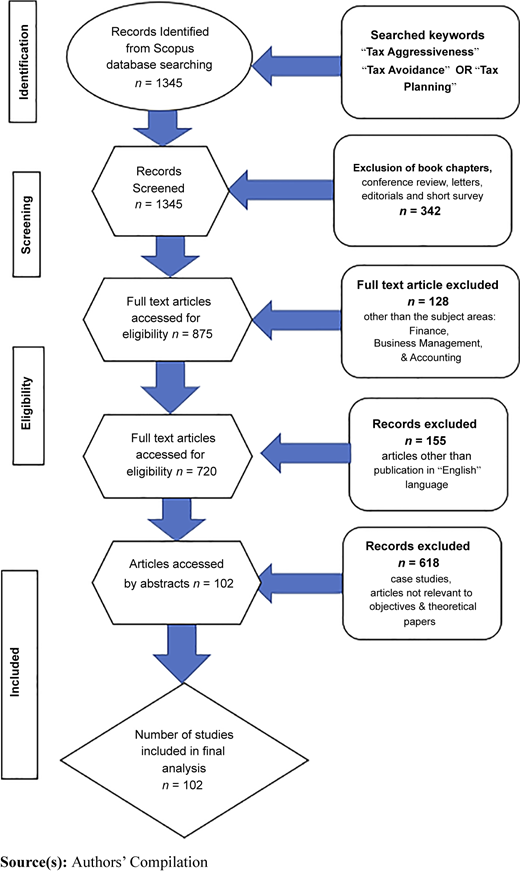

To select the relevant literature, a comprehensive search was conducted in the Scopus database, the most extensive database consisting of peer-reviewed journals (Cooper & Nguyen, 2020). “Tax Avoidance” OR “Tax Aggressiveness” OR “Tax Planning” were the three search keywords used to extract the relevant studies from the database and a total of 1345 records were identified in this stage. Then the authors applied the PRISMA approach for the selection of relevant papers (Figure 2). PRISMA guidelines ensure the quality of selected papers and also address the misinterpretation issues in the reviewed articles (Moher, Liberati, Tetzlaff, & Altman, 2009; Mengist, Soromessa, & Legese, 2020). Then, the research articles published in the English language in the Economics, Econometrics and Finance, and Business Management and Accounting domains were retained. This criterion limited the number of articles to 720. Case studies and conceptual papers were also excluded and finally 102 articles were considered for the systematic review.

A systematic review is a form of review analysis that is conducted to identify the research evidence to answer research questions and also to suggest the scope for policy framework and future research work (Aromataris & Pearson, 2014; Darzi, Islam, Khursheed, & Bhat, 2023). For creating the keyword networking diagram, VOSviewer software has been used. VOSviewer software tool was created by Eck and Waltman in 2010 and is used for creating and exploring bibliometric maps (Arruda, Silva, Lessa, Proença, & Bartholo, 2022).

4. Results of systematic analysis

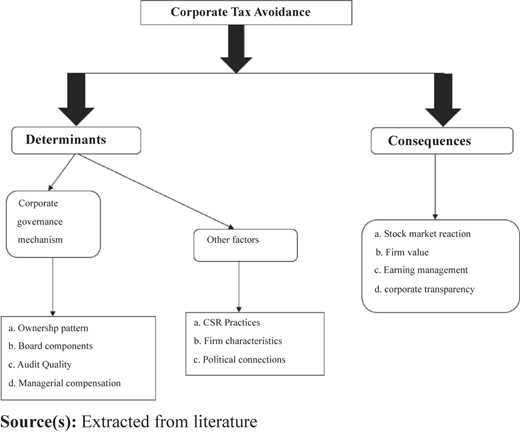

This part is divided into two subsections, the first one explains the factors that contribute to tax avoidance and the second part describes the effects of such behavior (Figure 3).

4.1 Factors affecting the corporate tax avoidance decisions

Factors that contribute to corporate tax avoidance have been grouped into seven categories, with each category having many subcategories. Table 1 displays the impact of corporate governance mechanisms on corporate tax avoidance practices and the impact of other identified factors in Table 2.

Effects of corporate governance components on corporate tax avoidance

Source(s): Authors’ compilation

Effects of factors (other than corporate governance mechanisms) on tax avoidance

| Determinants | Findings | Research papers | Related theory | |

|---|---|---|---|---|

| e | CSR practices | |||

| CSR disclosure | Less TA | Gulzar et al. (2018), Lanis and Richardson (2015), Laguir, Staglianò, and Elbaz (2015), Mao and Wu (2019), Park (2017) | Social responsibility theory | |

| More TA | Abdelfattah and Aboud (2020), Alsaadi (2020), Arifin and Rahmiati (2020), Zeng (2019) | |||

| f | Firm’s characteristics | |||

| Leverage | Less TA | Kismanah et al. (2018), Lin, Tong, and Tucker (2014) | Traditional theory | |

| More TA | Hamilah, 2020 | |||

| No impact | Salman (2018) | |||

| Size | Less TA | Salman (2018) | ||

| No impact | Hamilah (2020), Kismanah et al. (2018), Mulyati, Subing, Fathonah, and Prameela (2019) | |||

| More TA | Suchayo et al. (2020) | |||

| Capital intensity | More TA | Salman (2018) | ||

| Inventory intensity | No impact | Urrahmah and Mukti (2021) | ||

| Profitability | More TA | Firmansyah and Bayuaji (2019), Salman (2018) | ||

| Less TA | Kismanah et al. (2018) | |||

| g | Political characteristics | |||

| Political connections | More TA | Suchayo et al. (2020), Wahab et al. (2017) | ||

| No impact | RestiYulistia et al. (2020) | |||

Source(s): Authors’ compilation

1. Ownership pattern

The ownership structure is considered a significant predator of the tax avoidance behavior of the firm (Hanlon & Heitzman, 2010). The impact of ownership structure on tax avoidance does not show consistency in the result. In concentrated ownership, majority shareholders exploit the tax-saving benefits at the expense of minority shareholders (Ying, Wright, & Huang, 2017). Family-based firms are more engaged in tax avoidance than non-family-based firms because of higher ownership and more opportunities to seek high profit as they are the founding members (Gaaya et al., 2017; Kovermann & Wendt, 2019; Supantri & Rahmiati, 2020; Ying et al., 2017). In contrast to the above findings, Alkurdi and Mardini (2020), Bauweraerts, Vandernoot, and Buchet (2020), Landry et al. (2013), Moore, Suh, and Werner (2017), and Sánchez-Marín, Portillo-Navarro, and Clavel (2016) suggested that family firms are more concerned about their reputation and prefer to avoid tax aggressive decisions. Alkurdi and Mardini (2020), Khurana and Moser (2013), Resti Yulistia, Minovia, and Anison (2020), Wahab et al. (2017), and Ying et al. (2017) concluded that as the percentage of institutional ownership increases, the tax avoidance level starts to decline because of the better monitoring of managers’ performance. But Bird and Karolyi (2017) and Khan et al. (2017) suggest that an increment in institutional ownership results in more tax avoidance due to their concern about high market value. Insiders have voting rights in dual-class ownership, which implies less pressure from outsiders to use tax avoidance strategies (McGuire, Wang, & Wilson, 2014). Bradshaw, Liao, and Ma (2019), Chan et al. (2013), Liu and Lee (2019), and Mafrolla (2019) stated that tax avoidance decisions generate short-term benefits for the company. But state-owned firms are more concerned with long-term goals than with profit maximization, indicating a negative attitude toward tax avoidance decisions.

2. Board components

The board’s efficiency varies depending on its independence, size, ethnicity, gender diversity, professional knowledge, etc. The presence of more independent directors reduces the likelihood of the adoption of tax avoidance behavior because of effective monitoring of boards’ tax minimization behavior (Alkurdi & Mardini, 2020; Zaqeeba & Iskandar, 2020). Cho and Yoon (2020) suggested that religious diversity onboard has a significant impact on tax planning decisions. In comparison to concentrated board religion, boards with varied religions show a higher rate of tax avoidance. Gender diversity on board leads to less tax avoidance because feminine characteristics are associated with less risk-taking and more moral choices (Francis, Hasan, Wu, & Yan, 2014; Richardson, Wang, & Zhang, 2016; Lanis, Richardson, & Taylor, 2017; Hoseini, Safari Gerayli, & Valiyan, 2019; Jarboui, Kachouri Ben Saad, & Riguen, 2020). Hoseini et al. (2019) claimed that large boards are less effective than small boards due to many perspectives in taking any decision. But chances of accounting fraud increase with the increment in board members (Zemzem & Ftouhi, 2013) which lead to more tax avoidance.

3. Audit quality

Audit quality is an important element of corporate governance that reduces the conflicts between management and shareholders and prevents managers to indulge in fraudulent and accounting-manipulating activities (Abdel-Wanis, 2021). Gaaya et al. (2017) claimed that the companies audited by the Big Four are less likely to participate in tax avoidance because of the risk of reputational cost and litigation cost, and adopt fair tax auditing practices. Similarly, the presence of more independent directors in the audit committee and audit tenure negatively impacts tax avoidance decisions. The presence of more independent auditors in the audit committee results in effective monitoring and less tax avoidance (Deslandes, Fortin, & Landry, 2020). This study also stated that auditors with large tenure favor less tax-aggressive strategies due to having more in-depth knowledge of the company’s operations and more effectiveness in detecting tax-evading practices.

4. Compensation

Managerial ability is characterized as the better assessment of risk and return related to investment decisions (Gober & Burns, 1997). The attitude of key personnel toward tax avoidance decisions could be affected by remuneration incentives (Walsh & Ryan, 1997). Equity-based incentives align the interest of owners and agents and encourage management to undertake risky decisions such as tax avoidance to increase posttax income (Taylor & Richardson, 2014). But, tax avoidance decisions with short-term benefits might have a long-term reputational damaging effect on the firm and such activities may bring additional costs to the firm such as penalties, auditing firms’ intervention, reputational damage, etc. (Huang et al., 2018; Sudirjo, 2020). In contrast to this, Phillips, Pincus, and Rego (2003) found the insignificant effect of CEO after-tax compensation on such decisions due to their unwillingness to take on additional compensation risk.

5. Corporate social responsibility (CSR) disclosure

Corporate actions have a substantial impact on local communities and civil society organizations (Dyreng et al., 2010). CSR practices are defined as all actions taken by companies to have a positive impact on the environment and society. Firms consider tax avoidance practices as socially irresponsible decisions and avoid such practices (Gulzar et al., 2018; Lanis & Richardson, 2015; López-González, Martínez-Ferrero, & García-Meca, 2019; Mao & Wu, 2019; Mao, 2019; Park, 2017). In contrast to these findings, Alsaadi (2020) and Arifin and Rahmiati (2020) found that firms also use the benefits of tax savings to fulfill their responsibility toward society and publicly display good CSR scores, safeguarding themselves from unfavorable consequences of such action in the event of detection (Jiang, Zheng, & Wang, 2021; Zeng, 2019).

6. Firm characteristics

Firm characteristics have a significant impact on tax avoidance practices. The impact of tax-avoiding behavior on firm size has been explained through political cost and political power theory. Political power theory states that large-sized firms are more engaged in tax avoidance activities due to high economic and political power (Sucahyo, Damayanti, Prabowo, & Supramono, 2020). While political cost theory (Salman, 2018) states that large firms are under more pressure to disclose performance transparency to regulatory bodies compared to small-sized firms, which shows a negative attitude toward tax avoidance decisions. Contradictory to political power and political cost theory, Kismanah et al. (2018) concluded the insignificant relationship between tax avoidance and firm value. The firms use debt (leverage) in their capital structure as a tax shield because interest payable on debt is deductible expense before calculating tax liability (Loney, 2015). The study (Firmansyah & Bayuaji, 2019; Salman, 2018) found a positive relationship between tax avoidance and profitability. Firms with more fixed assets have a low effective tax rate (ETR) because depreciation on the fixed assets is allowable as a deductible expense from profit (Salman, 2018). Large inventories enhance a company’s overall financial burden due to higher transportation, warehouse, maintenance and storage expenses and such decisions do not affect the companies’ tax burden (Urrahmah & Mukti, 2021).

7. Political connections

Politically connected firms face the burden of disclosure transparency and official intervention and thus engage in more tax avoidance practices. These political connections provide special rights to the firms and firms adopt more tax-aggressive practices due to less audit risk (Kim & Kim, 2016; Wahab et al., 2017). Same in this regard, the study (Resti Yulistia et al., 2020) claimed that these political ties can assist businesses in easy access to government contracts but do not have any impact on tax avoidance decisions.

4.2 Consequences of tax avoidance decisions

The adoption of tax avoidance tactics may have many economic ramifications for businesses. The detection of illegal tax avoidance behavior results in lawsuits, penalties and a loss of reputation for the companies. Table 3 shows the probable outcomes of tax avoidance activity as extracted from the literature:

Consequences of tax avoidance behavior

| Outcomes | Effect of tax avoidance practices | Authors | |

|---|---|---|---|

| a | Stock market response | Negative | Hanlon and Slemrod (2009) |

| Positive | Blaufus, Möhlmann, and Schwäbe (2019), Jia and Gao, 2021 | ||

| b | Firm value | Increases | Chyz (2013), Guenther et al. (2017), Li et al. (2019), Lim (2011), Wahab and Holland (2012) |

| Declines | Park et al. (2016) | ||

| c | Earning management | Negative | Putri et al. (2016), Balakrishnan et al. (2019), Susanto, Pirzada and Adrianne (2019) |

| d | Corporate transparency | Decreases | Balakrishnan et al. (2019) |

Source(s): Authors’ compilation

1. Stock market reaction

The stock market is significantly affected by the disclosure of tax management strategies. The market value of the company declines in case of the detection of any illegal tax managing practices (Hanlon & Slemrod, 2009). The stock market reaction also depends on the news related to the legitimacy of tax minimization strategies. The stock market behaves negatively in case of tax evasion (illegal) news but there is no adverse reaction when the company is engaging in tax avoidance (legal) practices (Blaufus et al., 2019).

2. Firm value

Two distinct viewpoints have been proposed based on existing literature to explain the influence of tax avoidance on corporate value. The tax-saving concept shows that tax avoidance decisions minimize the tax liability of the firm. As a result, the profit goes up, which positively impacts the firm value (Lim, 2011; Abdul Wahab & Holland, 2012; Chyz, 2013; Guenther, Matsunaga, & Williams, 2017; Bimo, Prasetyo, & Susilandari, 2019; Li, Lu, & Li, 2019). While Park et al. (2016) stated that if there are not any incentive alignment contracts between managers and firms, then because of the rent extraction behavior of managers, tax avoidance decisions deteriorate the firm value.

3. Earning management

Frank, Lynch, and Rego (2009) and Kubick and Lockhart (2016) suggested that the increasing gap between taxable and book income could be the outcome of earning management decisions rather than tax-saving decisions. Earning management is the manipulation of financial statements to falsely report the high profits of the company for misleading investors and other related parties (Madan & Bhasin, 2016). Putri, Rohman, and Chariri (2016), Balakrishnan, Blouin, and Guay (2019) and Susanto et al. (2019) stated that the adoption of tax avoidance practices is mainly oriented toward earning management behavior.

4. Corporate transparency

Tax-avoiding activities increase the information complexities in organizations due to the adoption of tax-saving methods (Drucker, 2023). Information asymmetry in financial disclosure increases when firms are engaged in tax-avoiding behavior (Balakrishnan et al., 2019). Companies resist disclosing more about their taxation strategies to avoid penalties in case of detection of any illegal practice by auditing firms.

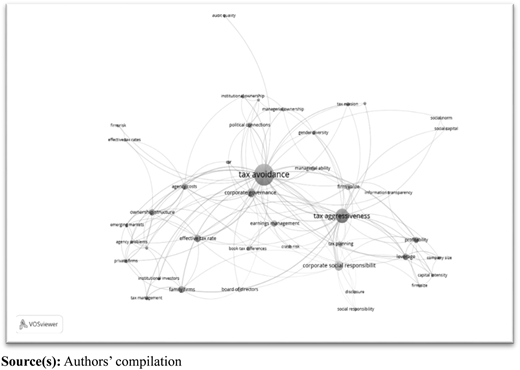

5. Keyword network analysis

The term “keyword networking diagram” has been considered one of the important tools to find the most researched areas and also emphasizes the presence of patterns and trends in a particular field (Goyal & Kumar, 2021). The enormous bubbles in Figure 4 represent the areas that have been thoroughly researched, while the small bubbles indicate the subjects that require further investigation. Thicker lines mean more frequent co-occurrences. The smaller the distance between the nodes, the stronger the relationship they have. Table 4 represents the number of research occurrences based on the keyword co-occurrence network, which identified 266 keywords in 102 research articles. Tax avoidance is the most frequently used keyword with 82 occurrences, tax aggressiveness with 34 occurrences, tax planning with 6 occurrences and tax management with 3 occurrences. This demonstrates that authors have considered the terms “Tax Avoidance”, “Tax Aggressiveness”, “Tax Management” and “Tax Planning” interchangeably.

6. Conclusion

Tax avoidance is defined as the legal “transfer of revenue” from the government to corporations. This saved income could be utilized by firms for productive purposes and could be exploited by managers for personal gain at the expense of investors. It has been observed that agency theory significantly affects managers’ tax planning decisions. Managers feel pressured because of the high expectations of owners, especially from riskless shareholders and adopt tax avoidance strategies to improve posttax income to fulfill the owners’ expectations, and sometimes for their benefit.

The reviewed literature shows that the effect of various ownership structure forms on tax-avoiding behavior has unpredictable outcomes. The study finds that institutional investors put some of their money into other businesses in the hopes of earning dividends and profits, which shows a positive attitude toward tax management decisions. The literature reveals family firms are more concerned about their reputation in society, which affects their tax-avoiding behavior. The attitude of state-owned firms was found to be negative toward tax-avoiding decisions, because of their concern toward securing the government revenue. The study also reveals that firms are more likely to employ tax avoidance tactics when equity incentives are offered to executives.

The effect of corporate governance on firms’ tax-sheltering practices is also explored in this study. The percentage of independent directors, gender diversity, board size and audit quality parameters have been used for evaluating the impact of corporate governance frameworks on tax avoidance behavior. The presence of more independent directors on the board is linked to effective monitoring and better control, which can limit tax-sheltering decisions. Gender diversity on boards shows a negative attitude toward managing the tax aggressively due to the risk-averse behavior of the women. Smaller boards are considered more effective than larger boards due to fewer communication and coordination problems, however, the influence of board size on tax sheltering behavior is not always consistent. This study also suggests that auditing by Big Four auditing firms reduces the possibility of a firm’s engagement in earnings manipulation. Other than corporate governance mechanisms, tax avoidance decisions are also affected by various firm characteristics such as the use of leverage capital, the use of capital-intensive products, and firm size as explained in the existing literature. Companies usually benefit from the advantage of using debt to finance operations which is in the form of a debt tax shield. A company’s investment in fixed assets is referred to as capital intensity and charged depreciation on these assets is a deductible expense which further reduces the tax liability of the firm.

Tax avoidance behavior is considered a sign of irresponsible behavior toward society, the literature states that firms with high CSR scores are more cautious about tax avoidance practices. These firms avoid tax-aggressive decisions because the detection of such behavior offsets the positive effects of CSR practices and also causes reputational damages to the firm. On the other hand, some studies claim that firm with more tax avoidance practices discloses high CSR score to show a positive attitude toward their social responsibilities, which means that there is no stable relationship between firm tax avoidance practices and CSR score.

The associated costs and advantages of such decisions affect shareholder perceptions of the tax avoidance strategies of the firms. If any firm is found to be engaged in illegal tax avoidance by auditing firms, it will have to pay a penalty as imposed by taxation authorities. When such behavior is discovered, the firms’ reputations are also harmed, which causes share values to drop. Also, tax-aggressive firms have a less transparent information environment and do not disclose all information related to their tax management strategies.

Keyword network shows that the three terms, “Tax Planning”, “Tax Avoidance” and “Tax Aggressiveness”, have been used in the same context in the existing literature. This networking map also suggests that board gender diversity, board size, market reaction, disclosure transparency, capital market pressure, social capital and executive compensation have not been explored in-depth and can be regarded as emerging avenues for future research.

7. Practical and theoretical implications

This study provides an overview of the factors that contribute to tax-avoiding practices. This study is helpful to corporates to understand the effect of tax-saving decisions on their performance. This study is useful to the policymakers to understand the different practices adopted by the firms for reducing their taxation and liabilities and also to formulate policies for fixing these gaps. This systematic study can add greater clarity to other review analyses such as the bibliometric review method and meta-analyses, as well as to empirical studies.

8. Scope for future research

This study provides a thorough coverage of existing literature on corporate tax avoidance and is helpful for new researchers who want to understand this concept and also for those who are looking to explore new directions in the same field. One of the major issues that academicians confront when conducting a study on corporate tax avoidance is related to its measurement. The actual picture of overall tax avoidance by various firms can be obtained either from taxation authority or by the tax returns filed by the company, which in both cases is difficult to obtain. Salihu, Obid, and Annuar (2013), in their study on corporate tax avoidance measures, conclude that the availability of data and predetermined objectives of the study influence the choice of tax avoidance measures. This study is focused on identifying causes and outcomes of corporate tax avoidance behavior, with no discussion on tax avoidance assessment methodologies. To gain a better knowledge of firms’ tax avoidance behavior, measurement techniques for tax avoidance practices could be investigated further. The articles published only in the Scopus database were used for review purpose, which limits the generalization of the findings. So, future consideration of other databases such as “EBESCO”, “Web of Science”, “Google Scholar” or “Dimensions” can be significant to explore new directions related to corporate tax avoidance behavior.

The authors gratefully thank the constructive comments and suggestions from the editor and anonymous reviewers.