The COVID-19 pandemic has driven the adoption of advanced technologies in auditing, including the use of drones for inventory observation. However, practitioners have expressed concerns about the additional litigation risks associated with these technologies. This study aims to investigate whether using drones for inventory observation may increase auditors’ legal liabilities. In addition, it explores how perceptions of conventionality and normalcy interact in auditor liability and their broader implications.

This research employs a 2×2 experimental design to examine the effects of inventory observation method (drones vs human staff) and consistency with audit industry norms (consistent vs inconsistent) on jurors’ negligence assessments. Participants assume the role of mock jurors in a hypothetical legal case involving allegations of insufficient inventory observation. The study manipulates the observation method and its alignment with industry practices with a view toward disentangling the constructs of conventionality and normalcy.

The findings show that jurors assign higher negligence to auditors using drones when their use is inconsistent with audit industry norms, compared to auditors relying on human staff. Conversely, when drone use aligns with audit industry norms, jurors attribute lower negligence compared to those not using drones. In addition, the results indicate that the perceived foreseeability of audit failure mediates this interaction effect.

This research contributes to the extant literature by addressing the distinction between the constructs of conventionality and normalcy. It also offers practical implications for auditors, emphasizing the importance of demonstrating due care when adopting new technologies to align with audit industry norms.

1. Introduction

The COVID-19 pandemic has driven the increased adoption of advanced technologies in auditing, enabling firms to adapt to challenges in maintaining audit quality with limited physical access (Sharma et al., 2022; Baatwah et al., 2023). Innovations such as remote auditing software, AI-driven analytics, blockchain and drones are increasingly being considered for use (Deloitte, 2018; PWC, 2019; Alma’aitah et al., 2024; CA ANZ, 2024; KPMG, 2024). These technologies support key activities such as remote document review, advanced data analysis and real-time transaction validation (Deloitte, 2018; KPMG, 2024). In particular, drones have emerged as a promising tool for inventory observation, offering an efficient alternative in terms of both speed and cost (PWC, 2019, 2024).

In practice, many audit firms have begun using drones, leveraging their capability for live video streaming and inventory count recording (Gilbert, 2017; PWC, 2019, 2024). Prior research has also emphasized the potential of drone technology in inventory observation. For instance, Christ et al. (2021) provided empirical evidence that drones, combined with automated counting software, can significantly enhance the efficiency of inventory counts. However, their interviews with audit partners also highlight concerns about increased litigation and regulatory risks associated with adopting this technology. Similarly, Fotoh (2025) suggested that despite expected benefits, preferences for physical counts and skepticism toward digital tools may continue, reflecting fears that excessive juror-assigned culpability could deter auditors from adopting innovative techniques (e.g. Peecher et al., 2013; Kang et al., 2015; Brown et al., 2020).

Psychology literature finds that, in general, individuals who use unconventional methods are judged more harshly than those who follow conventions, a phenomenon known as normality bias (Kahneman and Miller, 1986). Normality bias is frequently studied in the context of medical lawsuits, where conventional medical practices are also the most widely used. This context highlights the overlap between conventionality (i.e. having previously been used) and normalcy (i.e. being widely used within a reference group) (Baron and Ritov, 2004). For example, newer medical practices often have fewer trial records documenting their side effects (i.e. lower levels of conventionality) and are therefore used less frequently (i.e. lower levels of normalcy). Over time, as newer practices accumulate trial records, they may become “industry norms” (i.e. higher levels of normalcy) as they are no longer considered “new” (i.e. higher levels of conventionality).

However, this process may be slightly different in the context of audit practices. In auditing, the benefits of new technologies are arguably more immediate and measurable, as they manifest in improved speed, completeness and accuracy of work outcomes (e.g. Christ et al., 2021). Perceived risks of malfunction in auditing may also be relatively lower than in fields like medicine, where the consequences of failure are arguably more severe. Moreover, because the audit industry expects the rapid adoption of advanced technologies (PCAOB, 2017), audit industry norms (i.e. high normalcy) may shift even when these technologies are still perceived as “new” (i.e. have low conventionality). This suggests that, in auditing, normalcy and conventionality may at times diverge and that the legal implications of using new technology may also differ.

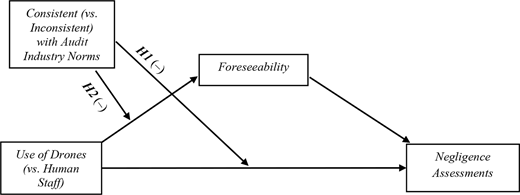

In this study, we investigate whether using drones (vs human staff) for inventory observation (i.e. conventionality) in an audit interacts with consistency (vs inconsistency) with audit industry norms (i.e. normalcy) and affects jurors’ negligence assessments. We employ a 2 (inventory observation method: drones vs human staff) × 2 (audit industry norms: consistent vs inconsistent) full factorial design. Participants are informed at the outset that inventory observation has traditionally been conducted by human staff (i.e. a more conventional method), while drones have only recently become available for this purpose (i.e. a less conventional method). Furthermore, the observation method is framed as either consistent (i.e. more normal) or inconsistent (i.e. less normal) with the practices of most other similar-sized audit firms at the time of the audit. Our juror instrument utilizes the Big Time Gravel case (Kadous, 2000, 2001), in which a hypothetical accounting firm is accused of insufficient observation of the client’s gravel inventory reserves.

Prior research suggests that when audit practices deviate from prior practices and an audit failure occurs, jurors may engage in counterfactual reasoning (e.g. Kadous and Mercer, 2012). Individuals readily question “what if” an alternative action had been taken when the conventions are not followed (Kahneman and Miller, 1986; Prentice and Koehler, 2002). We adopt the Culpable Control Model (Alicke, 2000), which builds on counterfactual reasoning theory, and propose that when an unconventional (vs conventional) method is used, jurors become more sensitive to other salient attributes. Specifically, when drones are used for inventory observation rather than human staff, we predict that jurors will assess the auditor’s foreseeability of audit failure as greater when drone use is inconsistent with audit industry norms. Compared to using human staff, this heightened foreseeability assessment may also increase the likelihood of higher negligence assessments.

Our findings have several notable implications. First, we consider practical implications for auditors when adopting new audit technologies. We find that jurors assign higher negligence when auditors use a less conventional method (e.g. drones) and when the use of this method deviates from established norms. This suggests that being an early adopter of audit technology may heighten legal liabilities, a concern previously expressed by audit partners (Christ et al., 2021). However, our findings also indicate that jurors assign lower negligence even when auditors use drones, provided its use aligns with audit industry norms. This implies that as newer audit technologies such as drones become more widely adopted within the audit industry, the failure to implement them, thereby not adhering to the audit industry norms, may also increase potential legal risks.

Second, we contribute to the extant literature on auditors’ legal liability and audit technologies. Prior studies have found that auditors can experience greater legal liability when emerging technologies are used in ways that reduce perceptions of human oversight (e.g. Shivram, 2024; Kipp et al., 2020). On the other hand, jurors may be more lenient when the technologies demonstrate enhanced audit quality (e.g. Barr-Pulliam et al., 2022; Libby and Witz, 2024). Our study adds to this line of literature by suggesting that adopting innovative techniques does not necessarily increase litigation risks; alignment with audit industry norms may play an important role. Moreover, our findings indicate that foreseeability mediates negligence assessments. In this regard, if auditors fail to demonstrate due care and diligence in the audit processes, the perceived foreseeability of adverse audit outcomes could increase (Backof, 2015). This may suggest that when auditors demonstrate due care and diligence in the process of adopting new technology, they may be able to reduce the foreseeability of an audit failure, potentially reducing the associated legal liability.

Finally, we also contribute to the literature on normality bias. In prior studies, conventional methods often aligned with industry norms (Baron and Ritov, 2004). For instance, medical research frequently shows that doctors who use newer practices, inconsistent with industry norms, are judged more harshly than those who follow conventional, widely accepted practices (e.g. Prentice and Koehler, 2002). The distinction between conventionality and normalcy is also often not evident in accounting research. For example, Kadous and Mercer (2012) investigated how jury verdicts are influenced by the precision of accounting standards and by whether aggressive revenue-recognition choices align with industry reporting norms that are widely accepted and, presumably, conventional. Koonce et al. (2015) also explored investor reactions to managers’ derivative use depending on whether the practice aligns with widely accepted industry norms. In contrast, our study differentiates between conventionality and normalcy, and demonstrates that the two constructs could interact. Our findings suggest that separating the two constructs may be informative in contexts where conventional methods and industry norms are not fully aligned, such as in cases involving innovative audit approaches or evolving reporting practices.

The remainder of the paper is organized as follows. Section 2 presents relevant theories and hypotheses developed for the study. Section 3 describes the methodology used to test the hypotheses, and Section 4 summarizes our results and analyses. Finally, Section 5 concludes the paper with discussions.

2. Theory and hypotheses

2.1 New technologies in auditing and drone-enabled inventory observation

The growing adoption of various new technologies has significantly transformed traditional audit practices (Sharma et al., 2022). For example, remote auditing software enables auditors to perform key activities like document review, interviews and data analysis through secure online platforms (Alma’aitah et al., 2024; Serag and Daoud, 2021). In addition, AI-driven analytics use machine learning algorithms to analyze vast financial data sets, detect anomalies and flag potential risks or irregularities (Han et al., 2023). Moreover, blockchain technology, known for its immutable and transparent ledger capabilities, facilitates real-time transaction verification (Han et al., 2023).

Because the Federal Aviation Administration (FAA) implemented new drone regulations (FAA, 2021), camera-equipped drones have been widely adopted in many industries to assist operational processes (PWC, 2024). In the audit context specifically, drones support tasks such as verifying inventory, observing client activities and assessing asset values (Appelbaum and Nehmer, 2017). For instance, drones equipped with cameras or Radio Frequency Identification (RFID) tracking systems can navigate through the client facilities and help verify records while transferring real-time footage (Appelbaum and Nehmer, 2017). These technologies are particularly useful for clients with a large inventory (Sidhu, 2018) or in environments where human access is limited, such as mining or polluted sites (Sidhu, 2018), or during public health crises, such as COVID-19 (Ho, 2020). While such innovations may enhance audit efficiency, auditors must still comply with established auditing standards (e.g. AU-C 501; ISA 501), which outline processes for obtaining audit evidence through physical observation.

Several audit firms have already adopted drones as a supplementary tool for their inventory counts. For example, Ernst & Young has used drones in inventory counts for a trucking company (Rinaldi, 2019), PWC has also used drones for the stock counts in a coal reserve (PWC, 2019) and PWC UK has a dedicated team and specialists for using drones for inventory observation (PWC, 2024). Yet despite these examples, concerns about early-adopter risk and inadequate guidance persist among audit partners (Christ et al., 2021), thereby slowing the pace of widespread adoption.

While drone-enabled inventory observation is expected to improve the completeness and speed of inventory observation (Ovaska-Few, 2017; Sidhu, 2018; Christ et al., 2021), potential risks and challenges remain. For instance, although drones can scan codes on the outside of boxes into which goods can be placed, they cannot independently determine whether the interior of the boxes needs to be investigated (Sidhu, 2018). Further, similar to a human auditor visiting the client site, if the visit is arranged much in advance, clients can move inventories between the sites, fraudulently increasing the volume of inventory at the site where the visit is expected to occur (Sidhu, 2018).

In addition, the use of such emerging technologies in auditing has generated a range of ethical and practical challenges. For instance, Lehner et al. (2022) indicated that AI-based decision-making in accounting raises ethical concerns in human-machine collaboration, particularly regarding objectivity, accountability and transparency. Similarly, some empirical studies also highlight risks of bias, opacity and auditor overreliance on AI (e.g. Ayling and Chapman, 2022; Kokina et al., 2025), underscoring the need for robust audit frameworks tailored to digital environments. This means that although drone-enabled inventory observation may generally increase audit accuracy and completeness by allowing auditors to access more inventories through an enhanced verification process, it still bears some of the audit risks associated with traditional inventory observation, as well as other unexpected challenges.

2.2 Using new audit technologies, normality bias and auditor liability

A growing body of literature explores the effects of using advanced technologies in auditing. Many studies focus on whether individuals oppose or appreciate judgments provided by new audit technologies. For example, Commerford et al. (2022) found that auditors are more skeptical of judgments made by artificial intelligence (AI) audit systems compared to those made by human specialists. Similarly, Emett et al. (2023) reported that auditors perceive data processed by algorithm-based analytics as being of lower quality than data processed by human staff.

In terms of jurors’ evaluations during audit failures, Kipp et al. (2020) found that jurors are more likely to deliver negligence verdicts when auditors use algorithm-based analytics instead of human-prepared analyses. In contrast, Barr-Pulliam et al. (2022) showed that mock jurors assign fewer negligence verdicts when auditors use data analytics over traditional audit sampling, particularly when the analytics demonstrate greater completeness and accuracy. Furthermore, Libby and Witz (2024) observed that jurors assign fewer negligence verdicts when AI performs analytical procedures than when humans conduct the same procedures, especially in cases involving auditor independence conflicts. Collectively, the existing literature suggests that individuals may hesitate to rely on new audit technology when its benefits are unclear (e.g. Commerford et al., 2022; Emett et al., 2023; Kipp et al., 2020) but tend to evaluate it more favorably when its benefits are clearly substantiated (e.g. Barr-Pulliam et al., 2022; Libby and Witz, 2024).

As previously discussed, psychology literature identifies a phenomenon known as normality bias, where individuals judge those who deviate from norms more harshly even when outcomes are identical (Kahneman and Miller, 1986). For instance, Prentice and Koehler (2002) found that jurors judge physicians more harshly when they deviate from conventional and normal medical practices. This is likely because deviations encourage counterfactual reasoning, leading individuals to speculate about what might have occurred had a more normal action been taken (Kahneman and Tversky, 1982; Prentice and Koehler, 2002; Feldman et al., 2020). In accounting, studies have explored various types of norms across different contexts. Sunder (2005) classifies accounting norms into conventions (i.e. past practices), socially accepted norms (i.e. current industry standards) and professional standards. Kadous and Mercer (2012) observed that mock jurors assign more negligent verdicts to auditors when they deviated from the industry norms. Koonce et al. (2015) distinguished between industry norms and firm-specific norms in examining how these affect investor reactions to firms’ derivative use. However, to the best of our knowledge, conventionality and normalcy have not yet been separately tested in investigating juror judgments of norms in the case of an audit failure.

Research suggests that information about conventions is more mutable than other attributes when jurors assign blame for an adverse outcome (Kahneman and Miller, 1986). Specifically, when a convention is violated, the mutability of other salient attributes increases (Kahneman and Miller, 1986). If jurors assess case attributes with heightened sensitivity due to a violation of conventions (Kahneman and Miller, 1986; Alicke, 2000), any salient attributes, whether positive or negative, are likely to be evaluated more critically. Consistent with this reasoning, organizational behavior research shows that individuals’ acceptance of novel options depends heavily on which features are made salient – for instance, clearly specified benefits tend to increase acceptance (Connolly and Reb, 2003). In medical research, Betsch et al. (2012) observed that individuals are less likely to accept a new vaccination when they are exposed to information about its adverse effects. Taken together, these findings are consistent with Spranca et al.’s (1991) evidence that individuals exhibit stronger moral and evaluative reactions to outcomes when salient features are made prominent.

We argue that when a less conventional method (e.g. the use of drones) is employed in an audit, jurors are more likely to react sensitively to attributes such as whether the method was consistent (vs inconsistent) with audit industry norms, compared to when a more conventional method (e.g. human staff) is used. Therefore, we propose that if an audit firm uses drones for inventory observation and an audit failure occurs, jurors will assign a lower (higher) level of negligence if the use of drones was consistent (inconsistent) with audit industry norms at the time of the audit. This tendency, however, is expected to be less pronounced when human staff are used as the primary method for inventory observation. Our first hypothesis formally captures this interaction between the inventory observation method and consistency with audit industry norms:

In the case of an audit failure, jurors will assign higher (lower) negligence to the auditor if drones are used for inventory observation and if drone usage is inconsistent (consistent) with the audit industry norms at the time of the audit.

2.3 Culpable control model and norm distinction

In terms of the cognitive process that jurors go through when attributing blame, the literature on counterfactual theory and the literature on the Culpable Control Model suggest that jurors attribute blame for an adverse outcome by engaging in counterfactual reasoning, questioning “what if” an alternative action had been taken in the given circumstances (Kahneman and Miller, 1986; Miller and McFarland, 1986; Alicke, 2000). The literature finds that individuals perceive unconventional attributes more prominently than other attributes because being unconventional encourages individuals to consider “what if” scenarios (Kahneman and Miller, 1986; Prentice and Koehler, 2002; Kadous and Mercer, 2012). That is, conformity or nonconformity with conventions is naturally used as a focal comparing point in evaluating an event or circumstance (Kahneman and Miller, 1986). During this process, jurors evaluate the causal relationships between various possible attributes and the adverse outcome (Kahneman and Miller, 1986).

The Culpable Control Model (Alicke, 2000) argues that blame attribution begins with people’s spontaneous affective reactions to harmful events and the people involved. Spontaneous affective reactions subsequently influence the assessment of the involved actor’s control over the harmful event, including evaluations of causation, foreseeability and intent regarding the adverse outcome (Alicke, 2000). While causation pertains to whether the actor’s behavior directly contributed to the outcome, foreseeability concerns whether a reasonable actor could have foreseen the consequences, and intent relates to whether the actor deliberately caused the damage (Alicke, 2000). Foreseeability is often a key factor in negligence judgments (Lagnado and Channon, 2008), whereas causation and intent are typically examined when assessing deliberate misconduct. That is, in an audit failure setting where intentional harm is less evident, jurors are more likely to focus on foreseeability as their basis for negligence judgments.

Prior research suggests that in auditing, the foreseeability perceived by jurors may increase if auditors fail to demonstrate due care and diligence in the audit process (Backof, 2015). Applied to the context of technology adoption, if professionals exercise due care and diligence in adopting new technology, for example, by having thoroughly evaluated the technology’s historical error rates, monitoring its real-time performance (Price et al., 2019; Gerke et al., 2020), and verifying vendor qualifications (PCAOB, 2022), the foreseeability of adverse outcomes may be reduced.

Our earlier discussion indicates that, if jurors notice that an action is not consistent with the conventions, they evaluate other salient attributes with greater sensitivity (Alicke, 2000). Attributes assessed with heightened sensitivity are more closely linked to the actor’s perceived foreseeability of the adverse outcome (Lagnado and Channon, 2008). That is, if drones are used (a less conventional approach) rather than human staff (a more conventional approach), and if this approach is inconsistent with the audit industry norms (i.e. other salient attributes), this inconsistency would be assessed with heightened sensitivity. Similarly, if drones are used instead of human staff, and if this approach is consistent with audit industry norms, it would also be assessed with heightened sensitivity, resulting in a decreased perception of the auditors’ foreseeability of the audit failure. According to the Culpable Control Model, heightened foreseeability leads to increased negligence assessments; conversely, decreased foreseeability leads to decreased negligence assessments (Backof, 2015; Alicke, 2000). This suggests that auditors’ foreseeability is likely to mediate the interaction between the inventory observation method, audit industry norms and negligence assessments, leading to our second hypothesis:

In the case of an audit failure, if drones are used for inventory observation and their use is inconsistent (consistent) with the audit industry norms, auditors’ foreseeability over the audit failure will be assessed higher (lower) than when human staff is used, resulting in increased (decreased) negligence assessments.

Our model incorporates a mediated moderation effect, which means that perceived foreseeability mediates the interaction between drone usage and audit industry norms on negligence assessments. Figure 1 shows our theoretical model graphically.

3. Methodology

We employ a 2 (inventory observation method: using drones vs human staff) × 2 (audit industry norms: consistent vs inconsistent) between-participants experimental design. In each of the four research conditions, the background information included the following description of the use of human staff and drones in inventory observation:

Traditionally, human audit staff visit the client’s site in person to investigate a sample of assets. In recent years, drones and automated counting software have also become available for use in audit inventory observation.

We provide this description to participants at the start of the task to ensure that all participants know that using human audit staff (drones) for inventory observation is a more conventional (less conventional) audit practice. The task is adapted from Kadous’ (2000, 2001) Big Time Gravel Case, an inventory observation case for gravel reserves. [1]

3.1 Participants

For the 2 × 2 between-participant experimental design, we recruited 200 Amazon Mechanical Turk workers who are US citizens and at least 18 years old. Amazon Mechanical Turk workers are frequently used as proxies for jurors (e.g. Grenier et al., 2015; Maksymov and Nelson, 2016; Brown et al., 2019). The participants were assigned to one of four research cells at random.

In their response to the experimental materials, 59 participants (29.5%) indicated that they have CPA qualifications; 26 participants (13.0%) indicated that they are attorneys, 21 of whom also indicated that they are CPAs. Participants with these professional qualifications may be more knowledgeable about audit failure issues and may offer different judgments. Robustness testing after excluding these participants had no effect on the statistical inferences of our later reported results. Some prior research indicates that gender, education level and juror experience may affect juror judgments. In our data, 123 (61.5%) of the participants indicated that they are male, 136 (68.0%) indicated that they have at least some college education and 55 (27.5%) indicated that they have served as a juror in the past. The statistical inferences of our results reported later do not change when gender and education levels are included as covariates in the analysis, or when participants who have never served as jurors are excluded. We also inquired about participants’ prior knowledge about drone technology and, if so, the nature of their prior experience with drone technology (e.g. positive vs negative). The mean of the participants’ prior experience valence is 0.443, where −1 indicates negative and +1 indicates positive, suggesting that their overall experience with drone technology was positive. Furthermore, the extent to which participants feel positive or negative about drones based on prior experience does not differ significantly across the two manipulations (two-tailed p = 0.256 for inventory observation method; p = 0.803 for consistency with audit industry norms).

3.2 Procedure

Participants completed the experimental task online. They began by reading general information about the study. They were told that the research task was about juror assessments of auditor liability in the case of financial statement fraud and that they would be acting as jurors in a hypothetical lawsuit based on the facts presented in the case. They were required to complete the task in one sitting and on their own. Those who agreed to participate went on to the next page, which asked about their age and citizenship. Only those who identified as being at least 18 years old and as US citizens were allowed to proceed to the next page.

Participants were then given general instructions for the main experimental task, which required them to read accounting and auditing concepts as well as case details from a hypothetical accounting firm that failed to detect fraud. They were informed that they would be given review questions and that they would only be allowed to proceed if they correctly answered all the review questions. The review questions were true/false questions about accounting concepts and case facts, and they were provided to encourage diligent information processing (Peecher and Piercey, 2008).

The next page introduced accounting and auditing concepts, such as financial statements, materiality and the purpose of the external audit process, auditor negligence and inventory observation in audits. According to the research materials, one of the important duties of auditors is to ensure that the actual value of the client’s assets is not materially different from what is reported in the financial statements. It also stated that human audit staff have traditionally visited the client’s site in person to investigate a sample of assets, but in recent years, drones and automated counting software have become available for asset observation.

Participants then read an introduction to the case facts and a transcript from the negligence lawsuit, which included the plaintiff’s and defendant’s opening statements, witness testimony and closing statements. The legal context is such that an audit failure occurred due to inadequate auditing of the client’s inventory. Specifically, the defendant audit firm used a drone for inventory observation (or human staff, depending on the research condition) and failed to detect that the client fraudulently inflated their inventory balance. Further, we disclosed that the majority of other similar-sized audit firms have used (or have not used, depending on the research condition) the previously stated observation method for inventory. The client fraudulently moved gravel reserves between their various sites to appear to have sufficient inventory, which the audit firm overlooked. That is, the audit failure is not due to the inferiority of the inventory observation method used at the client site; rather, it is due to whether the audit firm exercised sufficient skepticism regarding their client site visits.

The case facts stated that Big Time Gravel (the audit client) materially overstated its gravel inventory by double-counting the reserves at the sites where the audit firm did not observe. In terms of inventory observation method, participants who were in the human staff (drone) condition read the following from the case transcript:

At the end of 2017, Jones & Company completed their inspection of half of our sites, using their audit staff specifically trained (their drones specifically designed) for the inventory observation, and watched (filmed) our lot managers pace off the sizes of the piles. I think the auditors reviewed the managers’ calculations afterwards.

The transcript also stated whether or not this method was in accordance with the audit industry standard at the time of the inspection. Participants in the research condition of being consistent (inconsistent) with audit industry norms read the following:

The inventory observation method of using audit staff (using drones) was consistent (inconsistent) with the method being used by most other similarly-sized audit firms at the time of the inspection.

Participants were then asked to choose whether the auditor was negligent, as well as the likelihood of the auditor’s negligence on an 11-point scale (0 = not at all likely, 10 = extremely likely). Participants then read brief descriptions about compensatory and punitive damages. If they deemed the audit firm to be negligent, they were asked to indicate a dollar amount for each of the compensatory and punitive damages that they recommended be awarded to the plaintiff on an 11-point scale in million-dollar increments (0 = $0 m, 10 = $10 m). The questions on the next pages probed the participants’ beliefs about the factors influencing their negligence verdicts. On an 11-point scale, participants were asked to indicate how important they thought it was that the defendant auditor used an inventory observation method that had been used in previous audits (salience) on an 11-point scale (0 = very low importance, 10 = very high importance). The other question asked participants to indicate the extent to which they thought it was important that the defendant auditor used an inventory observation method that most other audit firms were using at the time of the audit, on an 11-point scale (0 = very low importance, 10 = very high importance).

The questions on the subsequent few pages were designed to elicit information about cognitive factors involved in the Culpable Control Model. We included all eight questions from Backof (2015), employing the same 11-point scales. Only minimal wording adjustments were made (e.g. presenting them as direct prompts rather than questions), with a view toward preserving the original meaning and structure.

Specifically, we asked the participants for their spontaneous affective reactions to the defendant auditor (0 = very negative, 10 = very positive), as well as their affective reactions to the plaintiff (0 = very negative, 10 = very positive). We also asked participants to rate the extent to which the defendant auditor should have predicted the audit failure (0 = very little extent, 10 = very high extent) and the extent to which the defendant auditor should have controlled the quality of the inventory inspection (0 = very little extent, 10 = very high extent). In addition, we asked participants to rate the extent to which the defendant auditor was responsible for the plaintiff’s loss (0 = not at all responsible, 10 = completely responsible) and the extent to which the auditor intended to conduct a quality audit (0 = not at all intended, 10 = completely intended). Moreover, we asked about the likelihood that the auditor was aware of the client’s fraud but chose not to report it (0 = definitely had no knowledge, 10 = definitely had knowledge). Finally, we asked participants to rate the defendant auditor’s compliance with auditing standards (0 = no compliance, 10 = full compliance). The full set of questions is available in the supplementary file, which contains the complete research instrument.

The final section of the instrument included questions to check the manipulation regarding the inventory observation method used in the case material (i.e. drones or human staff) and whether the use of this method was stated as consistent or inconsistent with audit industry norms at the time of the audit. We also asked participants on an 11-point scale how familiar they were with drone technology (0 = not at all familiar, 10 = very familiar) and the nature of their knowledge about drones (−1 = negative, 1 = positive). The demographic questionnaire asked participants about their gender, education level, experience as a juror, and whether they were a CPA or an attorney.

3.3 Dependent variable

We use jurors’ assessments of auditor negligence as the dependent variable. This includes the negligent verdict, which can be either negligent or not negligent, and the assessed likelihood of negligence, on an 11-point scale.

3.4 Process variables

According to studies on normality bias, the bias may affect jurors’ emotions and attribution of blame. We therefore include questions in our experimental instrument that allow us to measure jurors’ emotional reactions and attribution of blame, using Backof’s (2015) questionnaire, which is based on Alicke’s (2000) Culpable Control Model. As previously discussed, these questions include participants’ spontaneous affective reactions as well as their assessment of the auditors’ foreseeability, causation and intention in relation to the audit failure. We use foreseeability as a mediating variable, which is the average of jurors’ assessment of the extent to which the auditor should have been able to predict the failure and should have been able to control the quality of inspection. [2]

4. Results

4.1 Manipulation checks

In total, 41 participants (20.5%) failed one or both of the manipulation checks and are excluded from the analysis reported here. [3] The remaining 159 usable responses are reasonably well balanced across experimental conditions as shown in Table 1. The remaining sample included 45 participants who identified as being a CPA and/or an attorney. [4]

Table 2 presents descriptive statistics for our key variables of interest. Notably, 81.8% of participants, on average, deemed the defendant auditor to be negligent. Also, on average, our participants assigned a higher-than-midpoint assessment for the foreseeability of the fraud by the defendant auditor, the auditor causation for the loss and the intention by the defendant auditor to conduct a quality audit. On average, our participants had a slightly positive spontaneous affective response to the auditor.

4.2 Tests of hypotheses

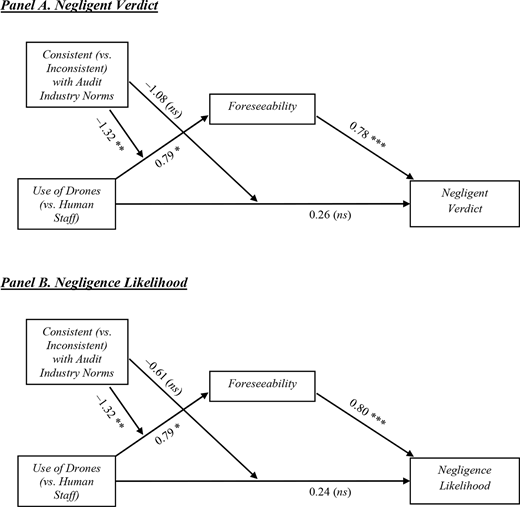

Negligence assessments by experimental condition are reported in Table 3. The patterns of means are consistent with our expectations, in that participants on average assess higher (lower) negligent verdict percentages (Panel A) and negligence likelihoods (Panel B) when drones are used for inventory observation, if most other firms use human staff (drones) for inventory observation at the time of the audit. The data in Table 3 suggest an interactive effect, as predicted by H1.

Specifically, our H1 predicts that, in the case of an audit failure, jurors will assess higher (lower) negligence when drones are used for inventory observation, if most other firms use human staff (drones) for inventory observation at the time of the audit, compared to when human staff is used for inventory observation. That is, the difference between audit industry norms conditions will be more evident in the drones condition than in the human staff condition. Table 4 presents our ANOVA results, for both negligent verdict percentages (Panel A) and negligence likelihood (Panel B) as the dependent variable. For negligent verdict percentages, we find a statistically significant interaction effect between observation method and consistency with audit industry norms (F = 3.81, one-tailed p = 0.026). We also find a significant interaction effect for negligence likelihood (F = 6.61, p = 0.006).

Separately, for negligent verdict percentages (as reported in Table 3 Panel A), we find a negative (but not statistically significant) simple effect of the use of drones (as compared to human staff) when consistent with the audit industry norms (mean values of 73% vs 84%; t = −1.55, one-tailed p = 0.126) but a significantly positive effect of the use of drones (as compared to human staff) when inconsistent with the audit industry norms (92% vs 79%; t = 2.00, p = 0.049). These statistical inferences are consistent when we use negligence likelihood as the dependent variable. A statistically significant negative simple difference between the drones and human staff conditions is observed (reported in Table 3 Panel B) when consistent with the audit industry norms (6.16 vs 7.03; t = −2.04, p = 0.045) but a positive difference when inconsistent with the audit industry norms (7.69 vs 6.89; t = 2.36, p = 0.021). This means that participants assessed negligence likelihood to be higher when drones (rather than human staff) are used for inventory observation and it is not the audit industry norm, but they assessed higher negligence likelihood when human staff (rather than drones) are used, if that is the audit industry norm. In short, the results support our H1.

Our H2 predicts a mediation effect of foreseeability. Specifically, it predicts that, if drones are used rather than human staff for inventory observation, and if using drones is inconsistent (consistent) with the audit industry norms at the time of the audit, auditors’ foreseeability over the audit failure would be assessed higher (lower) than when human staff is used (the conventional approach), resulting in increased (decreased) negligence assessments. Our ANOVA and simple effect test results reflect data patterns consistent with this prediction. Our ANOVA results using foreseeability as the dependent variable, as presented in Table 5, indicate a statistically significant interaction effect between industry observation method and consistency with audit industry norms (F = 5.68, one-tailed p = 0.009). Untabulated simple effects also show a negative and significant difference between the drones and human staff conditions when consistent with the audit industry norms (mean values of 6.32 vs 7.11; t = −2.18, p = 0.032) but a positive and marginally significant difference when inconsistent with the audit industry norms (7.71 vs 7.17; t = 1.91, p = 0.060).

To test our full mediated-moderation model, we use the Hayes Approach to conditional process analysis, with Model 8. The results of that analysis are presented in Table 6, for both negligent verdict percentages (Panel A) and negligence likelihood (Panel B). Consistent with our earlier ANOVA for H1, when foreseeability is not included in the model, the interaction term between observation method and consistency with audit industry norms is negative and significant for negligent verdict percentages (one-tailed p = 0.025) and for negligence likelihood (p = 0.005). And, consistent with our earlier analysis for H2, when foreseeability is used as the dependent variable, the interaction term is negative and significant (p = 0.009). When foreseeability is included as a mediator, it is a significant positive predictor of both negligence verdict percentages (p < 0.001) and negligence likelihood (p < 0.001). More notable, though, regardless of whether negligent verdict percentages or negligence likelihood is used as the dependent variable, the interaction term is no longer significant in the model (p = 0.144 and p = 0.106, respectively). This therefore reflects a full mediation of the moderation.

Figure 2 shows the standardized factor loadings for the components of our mediated-moderation model, showing again that after inclusion of foreseeability as a mediator in the model, there is no longer a significant interaction between consistency with audit industry norms and inventory observation method in predicting negligent verdict percentages (Panel A) or negligence likelihood (Panel B). Moreover, consistent with H2, we observe a significant negative interaction between consistency with audit industry norms and inventory observation method in predicting assessments of foreseeability (the mediator).

4.3 Additional analysis

4.3.1 Culpable control model.

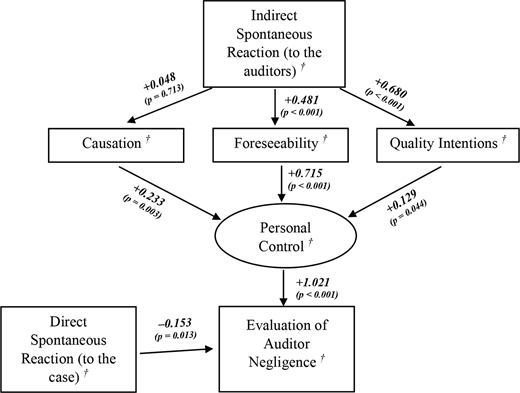

Prior literature indicates that normality bias and omission bias affect how jurors attribute blame. Specifically, normality bias affects jurors’ attribution in that it influences jurors’ assessment of the auditors’ foreseeability over the audit failure. We use Alicke’s (2000) Culpable Control Model to explore the specific attribution processes through which jurors attribute blame for the audit failure, which leads to their negligence assessments. Our test results show that, consistent with prior research, participants’ indirect spontaneous reactions influence their assessments of foreseeability, causation and quality intention regarding the auditors’ culpability for the audit failure, and then these factors ultimately influence their evaluations of auditor negligence. In addition, consistent with our prediction that foreseeability plays the role of the mediator between the attributes and negligence assessments, the causal link between foreseeability and negligence assessments is statistically significant. Figure 3 shows the standardized loadings for our Culpable Control Model analysis, which are generally consistent with Backof (2015) and other related studies.

4.3.2 Salience of normalcy vs conventionality.

Our theory assumes that participants will perceive audit industry norms to be more salient when a less conventional practice such as drone observation is used. In our experimental materials, we asked participants the extent to which they believed that it was important for the defendant auditor to use an inventory observation method that most other audit firms were using at the time of the audit. The mean response was 7.09 (standard deviation = 2.02), with the response scale ranging from 0 (very low importance) to 5 (moderate importance) to 10 (very high importance); this suggests that participants, on average, perceived that information about audit industry norms is of high importance. We also asked participants the extent to which they believed that it was important for the defendant auditor to be using a previously used inventory observation method. The mean response for this question was 6.91 (standard deviation = 2.05), with the same response scale range/labels; this suggests that participants, on average, also perceived that conventionality information is important. Notably, when drones are used (less conventional approach), as compared to when human staff is used (more conventional approach), audit industry norms are perceived to be more important (t = 2.25, one-tailed p = 0.026, untabulated). This result is consistent with our theoretical assumption that, when a less conventional audit practice is used, information about audit industry norms becomes more salient, compared to when a more conventional audit practice is used.

4.3.3 Familiarity.

A newer approach is less familiar and might be avoided due to unknown consequences of the approach. That is, any tendency to avoid using a newer approach might decline as familiarity with the approach increases. Alternatively, as jurors become more familiar with drone technology, and as they become more aware of accuracy and completeness benefits that the technology can bring for the audit firm, they may judge an audit failure more harshly, thinking that the audit firm could have better utilized the technology. As an additional analysis, we test whether familiarity with the drone technology might reduce (or increase) the negligence assessments of the jurors. Our results show a statistically significant correlation effect between familiarity and negligence likelihood (Pearson correlation = +0.23; two-tailed p = 0.003). This suggests that, as familiarity with the drone technology increases, the jurors assess higher negligent likelihood, which is consistent with our expectation. When we rerun our statistical analyses for H1 and H2, using ANCOVA with drone familiarity as a covariate, our statistical inferences reported earlier are unchanged. Specifically, we continue to find a significant interaction effect between inventory observation method and consistency with audit industry norms on negligence assessments (for negligent verdict percentages, F = 3.66, one-tailed p = 0.029; for negligence likelihood, F = 7.09, p = 0.004, untabulated). Also, the interaction effect between inventory observation method and consistency with audit industry norms on foreseeability also remains statistically significant (F = 7.16, p = 0.004, untabulated). In short, we observe a tendency to assess higher negligence in our setting as familiarity with the drone technology increases, but our statistical inferences reported earlier remain even after including familiarity with the drone technology as a covariate in our statistical tests.

5. Discussion and conclusion

In recent years, audit firms have increasingly explored the use of advanced technologies in auditing (Gilbert, 2017; PWC, 2019). Both academics and practitioners have highlighted the potential benefits of such innovations, including the use of drones for inventory observation (Sidhu, 2018; PWC, 2019). However, practitioners have expressed concerns about increased litigation risks when employing technologies that lack a history of widespread use (Christ et al., 2021).

In this study, we investigate whether and how the use of drones in an audit interacts with consistency with the audit industry norms regarding the inventory observation method (i.e. method used by other audit firms), affecting jurors’ negligence assessments of the auditor in the case of an audit failure. Building on the theory of normality bias, we predict and find that jurors assess higher negligence when auditors deviate from the prevailing industry practice norms, either by using drones when most firms do not, or by not using drones when drone-enabled inventory observation is the norm. Utilizing the Culpable Control Model, we find that perceived foreseeability of an audit failure by the auditors is the mediating variable influencing the interaction between the inventory observation method and consistency with audit industry norms.

This study offers practical implications for audit firms. Our results suggest that while adopting drones for inventory observation may increase legal liabilities when most other audit firms have not yet adopted the technology, failing to adopt drones may similarly increase legal liabilities if the technology has already become the audit industry norm. Additional analyses reveal that jurors’ negligence assessments increase as familiarity with drone technology grows.

This finding suggests that, as jurors become more familiar with drone technology, they may begin to hold auditors to higher standards regarding its use. Accordingly, audit firms might consider not only monitoring technological trends but also proactively educating stakeholders, including jurors, on the appropriate and evolving use of such technologies in audit practices. Furthermore, failing to adopt widely accepted technologies could increasingly be perceived as negligence, underscoring the importance of both innovation adoption and stakeholder communication.

Related to practical implications, we also asked our participants how much they would award to the plaintiffs in damages. Their response was up to $10m each in $1m increments for both compensatory damages and punitive damages. Regardless of whether human staff or drones were used for inventory observation, the average damage awards were higher when that observation method was inconsistent with audit industry norms. However, the penalty in damage awards for being inconsistent was almost $1m more on average for drone usage as compared to human staff, indicating that failing to align with audit industry norms when adopting drone technology could potentially be costly.

This study also contributes to the accounting literature by examining the effect of using drones for inventory observation on juror judgments. Emerging research has explored the impact of advanced technology in audits on jurors’ decisions, and we contribute to this body of work by distinguishing between conventionality and normalcy in the context of advanced technology adoption. Furthermore, our study extends the psychology literature by examining the mechanisms through which normality bias influences jurors’ blame attribution, particularly when conventionality and normalcy are treated as distinct constructs.

Although not the focus of this study, our data unexpectedly show that, in the research conditions where human staff rather than drones performed the inventory observation, the effect of audit industry norms was not statistically significant. In our research materials, to disentangle normalcy from conventionality and maintain internal validity, we informed all participants that, traditionally, human staff have conducted inventory observations in audits, whereas drones have only recently become available. It is possible that participants found this information more salient than the details related to audit industry norms, resulting in the observed lack of statistical significance for industry norm differences in the human staff condition.

Our study also has other limitations, which provide several avenues for future research. First, we adopt the Culpable Control Model (Alicke, 2000) to consider evaluations of foreseeability, causation, and intent regarding the adverse outcome. Only foreseeability is considered in our analyses as a mediator because it is often acknowledged as the key factor in negligence judgments. Potential roles of causation and intent could be examined further in future studies. Second, we take a narrow view when referring to “industry norms” as prevailing practices within the audit profession, where the emerging practice of using drones has not yet been standardized per se. Although our study has identified several known cases of drone usage in audit firms, the specific extent to which audit firms currently rely on drone technology remains unknown. Future research could address this gap by systematically documenting the degree of adoption across firms. In particular, as drone usage becomes more widely integrated into audit practice, an important question is whether the relationship between inventory observation methods and negligence assessments will change over time. Furthermore, future work could also examine whether reliance on human staff remains necessary, or whether drones alone can sufficiently fulfill the inventory observation function.

Finally, prior studies frequently have observed that industry norms influence accounting stakeholders’ judgments. To the best of our knowledge, however, only a few research conditions in prior studies have documented circumstances where stakeholders could become less sensitive to industry norms. This issue has not been a primary focus of investigation. Given that industry norms often serve as a critical comparative basis for evaluating accounting practices or values, it would be valuable to explore the contexts or circumstances in which accounting stakeholders may become less sensitive to these norms.

Acknowledgements

The authors thank the editor and two anonymous reviewers for their helpful comments. Dr Downen also acknowledges a summer research grant provided by the Cameron School of Business at UNCW.

Notes

The time of the incident has been modified to make it more current and include our manipulations of interest. Further details about the task are provided in the Procedure section below.

The correlation between foreseeability and causation is statistically significant (Pearson correlation = 0.596, p < 0.001). Our statistical inferences reported later remain the same when we either use foreseeability or causation separately as a single mediator.

Including these 41 participants in the analysis does not change our statistical inferences reported.

Excluding these participants does not change the inferences of our results. Using the reduced sample (n = 114), we still find that the interaction term between observation method and consistency with audit industry norms has a significant effect on negligent verdict (H1: F = 4.08, one-tailed p = 0.023), on negligence likelihood (H1: F = 4.49, p = 0.018) and on foreseeability (H2: F = 5.61, p = 0.010).

References

Supplementary material

The supplementary material for this article can be found online.