Public sector auditing research has changed rapidly over the past four decades. This paper aims to reveal how the field has developed and identify avenues for future research.

The authors used a structured literature review following Massaro et al. The sample comprises papers on public sector auditing published in accounting and public sector management journals between 1991 and 2020.

The present analysis highlights that academic research interest in public sector auditing has grown and become more diverse. The authors argue this may reflect a transformation of the public sector in recent decades, owing to the developing institutional logics of public sector reforms, from traditional public administration to new public management and now new public governance.

This paper offers a comprehensive review of the public sector auditing literature, discussing different perspectives over time. It also outlines the various public sector reforms introduced over the period of the study. In reviewing the existing literature, the authors highlight the themes for future research and policy settings.

1. Introduction

The practice of public sector auditing has changed over time and continues to develop (Hay and Cordery, 2018). In particular, the period since the 1980s has been characterised by significant developments in public sector auditing based on changing approaches to public administration (Troupin et al., 2010; Abbott, 1988).

Public sector auditing is a set of rules and practices that tabulate, numerate and comprehend a public organisation’s functions and activities. In contemporary times, public sector auditing has been shaped by market-oriented philosophies (Buchanan, 1993, 1997) and performance evaluation in the public sector (Knafo, 2019). As a result, public sector auditing has had different roles and functions over time. While traditional literature reviews (Hay and Cordery, 2018; Lapsley and Miller, 2019; Degeling et al., 1996) identify a large body of work, a comprehensive analysis of how the field has developed and changed over time has not been undertaken (Hay and Cordery, 2018).

We adopt a structured literature review (SLR) approach to address this gap. In doing so, we identify opportunities for future investigation. First, papers were extracted from SCOPUS and ISI Web of Science, according to a set of keywords and publication dates (Broadbent and Guthrie, 1992; Massaro et al., 2016). We complemented this approach with a traditional method for literature selection, using a set of inclusion criteria (Ardito et al., 2015) to draw in relevant articles missed in our initial search manually.

Based on the above, we identified two research questions incorporating the principles of critical research (“insight”, “critique” and “transformative redefinitions”) (Massaro et al., 2016):

What trends and themes stand out in the existing public sector auditing literature?

What are the main gaps in the existing public sector auditing literature?

We found that public sector auditing researchers have used various methods, including qualitative, single or multiple case studies and quantitative approaches. We also found that public sector auditing has changed substantially over time. In particular, new public management (NPM) and new public governance (NPG) philosophies have seen audit research shift from a focus on compliance to performance. Underpinning this shift is a change in how society conceives of the public sector’s role. Further, the analysis demonstrates how even theoretical approaches to public sector audits are consistent with the perspective of institutional logic associated with public sector reforms (traditional public administration, NPM and NPG). Finally, our review points to several possible future research avenues.

Our paper is organised as follows. Section 2 discusses public sector auditing over time, while Section 3 outlines the method used to select literature for review and examines in further detail some of the key publications in the public sector auditing field. The results are highlighted in Section 4, while Section 5 concludes, providing suggestions for future research directions.

2. Background

Before the 1980s, the underlying logic of the public sector was built on the Weberian model, also known as bureaucratic or traditional public administration (Troupin et al., 2010). Public sector auditing focused mainly on inputs, regulations and the correct use of public financial resources. Thus, the main aim of auditors was to assess the adequacy and accuracy of accounts to ensure that public sector activity – and hence the public sector organisation – was legitimate and spending taxpayers’ money appropriately (Troupin et al., 2010; Wiesel and Modell, 2014). Hence, a public sector audit focused on whether accounting practices were true and fair and followed the rules and regulations.

In the 1990s, with the advent of NPM, the traditional public sector audit was transformed. The managerial logic of NPM saw attention shift away from compliance with regulations. NPM introduced accrual accounting and associated financial statements into the public sector and made public sector auditing more like corporate audits, focusing on standards and formal annual financial statements. Control was broadened to consider outputs and efficiency. This period also saw the introduction of performance audits, which aimed to analyse the results achieved by individual public sector organisations. In this context, internal controls and internal audits became the critical purpose of the audit and citizens were relegated to passive and anonymous consumers (Almqvist et al., 2013; Wiesel and Modell, 2014). Guthrie et al. (1999) warned of an evaluatory trap created in the name of financial efficiency and accountability (Olson et al., 1998; Guthrie et al., 1999).

The 2000s saw the introduction of NPG logic. NPG can be understood as coordinating institutions and agencies in each policy area towards collective objectives. It describes the division of control and patterns of interaction among key (types of) actors in a specific policy area. According to NPG, public sector service delivery can be provided via multiple agencies (Almqvist et al., 2013; Wiesel and Modell, 2014; Powell et al., 2010; Fotaki, 2011). NPG expands the boundaries of single organisations by considering inter-organisational relationships and the engagement of diverse stakeholders (Klijn, 2012). In this context, where the citizen is at the centre of the institutional logic, the audit focuses on the quality of services provided, effectiveness and customer satisfaction, that is, on the outcomes. This approach to the public sector incorporates external government entities, such as state-owned enterprises and public and private partnerships, which can also be audited. Auditors working under an NPG logic use value for money (VFM) audits to assess how economic, effective and efficient is the management of the audited organisations (Morin, 2001).

3. Methodology

This section outlines the SLR approach. First, we selected and categorised relevant literature in the field. To do so, we developed a set of selection criteria and a streamlined review process, both detailed below.

3.1 Articles selection

Choosing specific search terms is key to an SLR (Cronin et al., 2008). To investigate trends in public sector auditing research, we chose the terms “audit”, “auditor”, “public sector”, “public administration” and “government” in the string “((audit*) AND (“public sector” OR “public administration*”) AND (government*))”[1]. We searched the string in two databases, SCOPUS and ISI Web of Science (WoS) and limited our search to titles, abstracts and keywords, as these are the parts of the articles that typically contain keywords (Dal Mas et al., 2019; Natalicchio et al., 2017; Paoloni et al., 2020). In both databases, we searched for papers published between 1991 and 2020 (30 years). WoS articles were only available between these dates and, for consistency, we kept the same parameters for Scopus. We conducted our search on 15 February 2021.

To avoid translation issues, we limited our search to articles written in English. We also limited our search by analysis area or broad discipline. For Scopus, these areas were business, management and accounting, “Social sciences” and “Economics, econometrics and finance”; for WoS, they were “Social sciences”, “Political sciences”, “Public administration”, “Economics”, “Business”, “Business finance” and “Management”. We considered these areas to be closely related to public sector auditing.

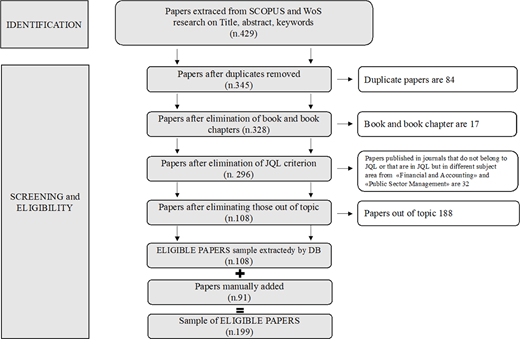

Our search initially identified 429 articles. After removing duplicate items (84) and documents classified as books or book chapters (17), 328 peer-reviewed journal articles remained. We only considered peer-reviewed articles to ensure that the publications included were of a rigorous academic standard (Podsakoff et al., 2005; Lockett et al., 2006).

Next, we weighed each article’s content against a set of “exclusion criteria” (Ardito et al., 2015), factors that might make an article inappropriate for review (see Table 1). Working together, we chose the exclusion criteria in advance. We decided not to consider articles from publications not included in our journal quality list (JQL). Also, we excluded articles classified in subject areas (Harzing, 2020) other than “finance and accounting” and “public sector management”. This is consistent with the previous literature, which emphasises that articles must be relevant to the investigated topic (Natalicchio et al., 2017; Crossan and Apaydin, 2010; Savino et al., 2017).

Another exclusion criterion identified was the article’s focus (Paoloni et al., 2020; Mauro et al., 2017). Although relevant to the topic we chose to analyse, many articles extracted from Scopus or WoS are about the private sector or only mention public sector audit in passing.

We manually worked individually to assess each article before comparing our results to minimise subjectivity and bias. In the first stage, the authors read the title, keywords and abstracts. If insufficient information was available from these, then the entire paper was read. Moreover, the authors worked alone and later compared their results to minimise subjectivity and bias (Paoloni et al., 2020). This process was followed throughout the codification of the articles analysed in this document. Ultimately, 188 articles were excluded, leaving 140 to be reviewed further. Using the exclusion criterion outlined above concerning the JQL list and subject areas, we excluded another 32 articles. This reduced the overall sample to 108 papers.

We then checked further to ensure that we included articles that the search engines had not extracted, perhaps because of the keywords used and included those articles. In other words, we applied inclusion criteria – considering factors that might make articles suitable for review (see Table 2).

We found an additional 91 articles using the inclusion criteria. Figure 1 highlights the articles obtained from each database and shows the articles added and eliminated through our inclusion and exclusion criteria selection process.

Our total sample for analysis comprised 199 papers.

3.2 Structured literature review framework

Consistent with other SLRs, we developed a classification framework (see Appendix) to ensure each article assessed consistently and comprehensively (Mauro et al., 2017; Anessi-Pessina et al., 2016; Broadbent and Guthrie, 2008; Goddard, 2010; Van Helden, 2005; Hart, 2018).

Data source (Mauro et al., 2017) – specific information about the journal (name, year of publication, volume and issue, first and last page numbers of the article and the total number of pages), title of the article, name(s) and affiliation(s) of the author(s), number of citations and keywords chosen by the authors.

Audit type – the type of audit referred to in the article:

financial;

performance; and

comprehensive (where a paper discusses more than one audit type).

- (3)

Research setting (Mauro et al., 2017) – the organisational context of the article:

federal;

central;

local;

agency;

national;

international;

cross-level; and

other – for example, decentralised entities, such as state-owned enterprises, public–private partnerships, etc., or entities operating in a specific public policy area (e.g. health care or education).

- (4)

Geographic context (Broadbent and Guthrie, 2008; Paoloni et al., 2020):

North America (Canada and USA);

Central and South America (Chile, Argentina, Dominican Republic, Brazil, Jamaica);

Australasia (Australia, New Zealand, New Guinea, Polynesia);

Asia (China, Japan, Korea, Singapore, Sri Lanka, Malaysia, Pakistan, India, Indonesia, Hong Kong, Thailand, Vietnam);

the U.K.;

Africa and the Middle East (Tanzania, Uganda, Botswana, South Africa, Nigeria, Ethiopia, Zambia, Israel, Lebanon, United Arab Emirates, Jordan, Saudi Arabia, Iran, Oman, Kuwait);

Eastern Europe (Hungary, Russia, Slovenia, Romania, Lithuania, Slovakia, Serbia, Croatia, Estonia, Poland, Czech Republic);

Northern Europe (Austria, Belgium, Denmark, Ireland, Finland, France, Germany, Netherlands, Scandinavia, Switzerland);

Southern Europe (Italy, Spain, Portugal, Greece, Turkey, Albania); and

Mixed (multiple countries in different geographic areas).

- (5)

Research method – the methods used to conduct the investigation:

literature review;

qualitative research (single, multiple or comparative case study);

quantitative research (single, multiple or comparative case study);

mixed, referring to articles using both qualitative and quantitative methods;

conceptual article; and

other (e.g. an experiment).

- (6)

Theories – which theory(ies) the authors applied:

systems-oriented theories, e.g. institutional, legitimacy and stakeholder theories;

economic theories, e.g. agency, principal–agent and moral hazard theories;

other – no previously classified theory(ies).

We also coded for “single theory”, “multiple theory” and “no theory”.

Table 3 shows the 31 units of analysis.

4. Analysis

Several patterns emerged from our analysis of the sample 199 articles (See Appendix, Table A1). We outline these in detail below.

4.1 Trends across the publication

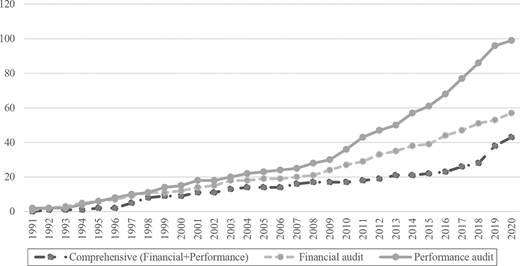

Our analysis shows that public sector auditing has been a growing research area for the past 10 years (see Figure 2).

Performance auditing was the subject of the highest number of articles (99), while 57 articles focus on financial statement auditing and 44 examine more than one audit type simultaneously (comprehensive auditing). Figure 2 highlights the development of performance audit, starting from its mention in 1993 to the peak of its attention from 2010.

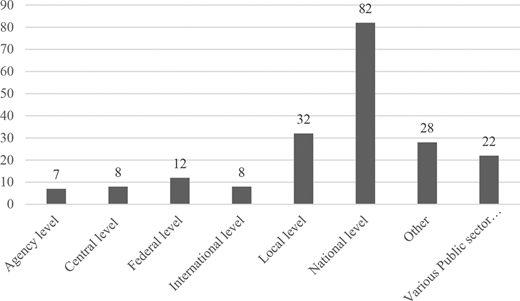

These articles also focused on the national-level (82), the local-level (32), the federal-level (12) and cross-level (22) of auditing, while international (8), central (8) and agency-level contexts (7) tend to be less explored (see Figure 3). The “other” category focused on public services such as schools and health-care organisations and included 28 papers.

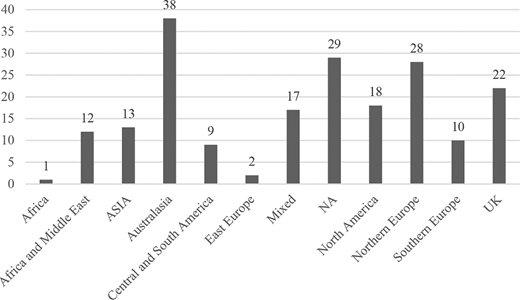

Several articles (29) are not tied to a particular geographic context but instead conceptual papers or literature reviews (see Figure 4). However, among those articles tied to a location, the majority focus on Australasia (38), countries in Northern Europe (28), the UK (22) and North America (18). Fewer articles survey Africa and the Middle East (13), Asia (13), Central and South America (9), Southern Europe (10) or Eastern Europe (2). Finally, 17 papers fall into the mixed category.

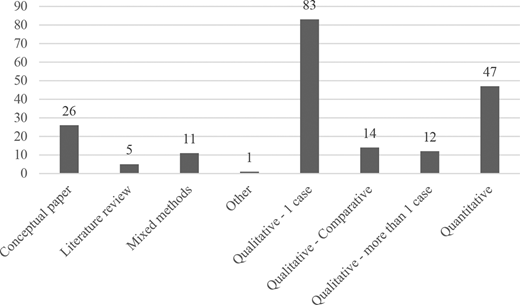

In terms of research methodology, qualitative methods were popular, which were used in 109 of the articles. Of these articles, 83 relate to a single case study, 12 adopt multiple case studies and 14 use comparative case studies. Additionally, 47 articles among our sample rely on quantitative methods, 26 are conceptual papers and 11 are based on mixed methods. Only five articles are literature reviews (Bonollo, 2019; Hay and Cordery, 2018; Mbewu and Barac, 2017; Thomas and Purcell, 2019; Nerantzidis et al., 2020) and only one (Guthrie and Parker, 1999) uses an experimental method (see Figure 5).

Many articles (153) do not apply any theoretical framework, consistent with previous studies (Goddard, 2010; Jacobs, 2012). Of those applying theory, 40 apply one theory, with 18 referring to system-oriented theories (i.e. neo-institutional, stakeholder and legitimacy theory), four referring to economic theories (e.g. agency theory, moral hazard theory) (Christopher and Sarens, 2018; Cordery and Hay, 2019; Heald, 2018; Raman and Wilson, 1994) and 18 referring to other theories (e.g. actor-network theory, paradox theory, organisational theory, political theory, psychological theories). A few articles (6) combine multiple theories, sometimes from the same group (e.g. institutional theory and legitimacy theory) and sometimes from different groups (e.g. agency theory with stakeholder and resource dependence theory) (Christopher and Sarens, 2018; Colquhoun, 2013; Goddard and Malagila, 2015; Justesen and Skærbæk, 2010; Lino and de Aquino, 2018; Stephenson, 2017).

To analyse the theoretical approach used by scholars in the eligible papers, we categorised the different theories used and allocated them as economic theories or systems-oriented theories. Theories that could not be allocated into these two sets were classified as “other” (see Figure 6). From 2009 onwards, scholars were more inclined to use theories in their work. Although all theories are more widely used in recent years than in the past, it is more common to see theories that are not strictly related to economic theories or systems-oriented theories (Jacobs, 2012; Hay and Cordery, 2018; Cordery and Hay, 2021). Theories used recently include psychological, sociological, pedagogical and organisational theories.

Our analysis reveals that theories began in the NPM period and consolidated in the NPG period. In the NPM period, economic theories (such as agency) dominated. These theories place the citizen as the principal, entrusting assets to managers, who are agents (Hay and Cordery, 2018). The auditors themselves are a party to another agency relationship and the principal does not know whether the auditor is performing the level of service agreed upon (Streim, 1994, p. 178). In the NPG period, citizens are positioned as co-producers (Almqvist et al., 2013; Wiesel and Modell, 2014; Mussari et al., 2021; Ruggiero et al., 2021), and involved in the decision-making process (Wiesel and Modell, 2014; Innes and Booher, 1999; Himmelman, 1994), which increases the need for legitimacy, rather than a narrow focus on effectiveness as in the NPM period (Cordery and Hay, 2021; Hay and Cordery, 2021). Based on the concept of isomorphism, institutional theory incorporates three types of pressure: coercive, mimetic and normative (DiMaggio and Powell, 1983). This theory became prevalent during the NPG period (see Figure 6) and other systems-oriented theories. Our detailed analysis shows that although scholars have adopted the more traditional isomorphism lens of institutional theory (Torres et al., 2019; Yang, 2020), new perspectives of institutional theory (such as institutional logics, work and entrepreneurship) are adopted to a lesser extent (Reichborn-Kjennerud et al., 2019). Nevertheless, because NPG is consistent with organisational sociology and network theory, attention is beginning to be paid to the psychological, behavioural and sociological aspects of auditors’ actions (socio-psychological; Bonollo, 2019) and how these may affect the community’s view of auditing and its functions.

4.2 Development of each audit type

To explore the development of public sector auditing, we discuss the type of public sector audit on which the paper is focused. The following discussion stems from the graphical representation of audit development in Figure 2.

4.2.1 Compliance and financial audit.

Several papers published in the first years of observation of this study focus on the quality of the financial audit performed and on the link between audit quality and fees payable, trying to identify what are the determinants of quality (Deis and Giroux, 1992; Ward et al., 1994), including, for example, the content of disclosures (Copley, 1991). In this context, Raman and Wilson (1994) conclude that it is not always possible to ensure a high-quality audit and, therefore, it would be helpful to identify the determinants of a quality audit for selection purposes.

Our analysis identifies a shift in research from the late 1990s to the early 2000s towards a focus on the characteristics of auditors and how this function can support public sector entities. There was also an examination of the role of auditors and their independence (Funnell, 1997; Jeppesen, 1998; English and Guthrie, 2000; De Martinis and Clark, 2003). Auditor independence was explored in papers examining political, entrepreneurial and professional leadership (Taylor, 1998). Audit Commissions became key actors in the governance of democratic communities (Humphrey, 2002) and are seen as the custodians of accountability (Coetzee and Msiza, 2018) in papers published from the early 2000s (Funnell, 2003). This saw the debate become focused on the collective responsibilities of audit, in which tension develops between the requirements of NPM and the role of audit and auditors. English (2003) argued that competition, a key feature of NPM, is not always an appropriate basis for reforming audit systems. In English’s study of the Australian state of Victoria, she finds that the reforms undertaken were politically rather than economically motivated. In the years immediately preceding 2010, researchers began to discuss fraud and corruption and how financial audits can combat these (Rahaman, 2009; Cooper and Catchpowle, 2009). This remains an area of interest as fraud and cronyism have grown exponentially in recent decades (Malau et al., 2019).

In the last decade, research has discussed the impact of NPG. An analysis of broader changes in the public sector has started to emerge (Chiang and Northcott, 2012; Pearson, 2014). This is reflected in papers examining the financial audit of services such as water and energy provided by external corporations (Haraldsson and Tagesson, 2014; Aadnesgaard and Willows (2016) or by quasi-governmental organisations (Oh and Lee, 2020).

4.2.2 Performance audit.

From the analysis of the articles published in the 1990s, we identify a strong interest in the internal functioning of government bodies when outsourcing the audit function. For example, Leeuw (1996) argued that the introduction of NPM saw more responsibility given to managers, which influenced performance auditing by focusing on public management principles such as economy, efficiency and effectiveness (Guthrie and Parker, 1999). In this context, Pendlebury and Shreim (1991) studied the attitudes of managers to audit, extending previous work that showed that external public sector auditors – usually engaged for non-financial reasons (Subramaniam et al., 2004) – were confident they had the skills to undertake this activity but that auditees did not necessarily share this view. Morin (2003) and Barzelay (1997) explored how external auditors carry out a performance audit and whether this increased the performance of public sector organisations. In a similar vein, Funnell et al. (2016) considered the crucial aspect of the independence of auditors in the performance audit area, an area also considered by other scholars, who saw internal performance auditors as consultants (Schillemans and van Twist, 2016) or management guides (Roussy, 2013). These audits aim to make managers more publicly accountable for their actions (Johnsen et al., 2001). Different authors analysed the effectiveness of the internal audit (Alzeban and Gwilliam, 2014; Erasmus and Coetzee, 2017; Mbewu and Barac, 2017), with Onumah and Krah (2012) identifying possible causes for any compromise of its efficiency. Consistent with reforms made according to NPM philosophies, some studies analysed privatisation and the market role in this scenario. Hepworth (1995) examined the impact of these factors on the audit function and its role in the accountability process.

Since the late 1990s, a change emerged in the topics researched, emphasising the characteristics of NPG. For example, Wilkins (1995) considered the quality of the processes that audit offices guarantee and focused on the different needs of the various citizens for whom public services are provided. Gunvaldsen and Karlsen (1999) focused on the centrality of the citizen, consistent with NPG thinking, discussing the community’s expectations concerning the Office of the Auditor General of Norway and how this is situated within the concept of legitimacy. The theme of expectations and perceptions taken up in later articles, such as that of Barrett (2010), highlights the contribution of the performance audit in improving (or otherwise) the public sector, according to different political and public expectations.

Changes in the performance audit and VFM auditing (Roberts and Pollitt, 1994) were analysed by Jacobs (1998), in which the changing role of VFM was highlighted as illustrating the contested nature of accounting technology. Several authors published articles in the 2000s analysing the significant influence of VFM auditing on government policies that have consequently changed the structure, organisation and provision of public services (Lapsley and Pong, 2000; Morin, 2001, 2004; Mulgan, 2001; Skaerbaek, 2009; Barrett, 2010; Kells, 2011; Reichborn-Kjennerud, 2014a; Raudla et al., 2016; Funnell, 2015; Reichborn-Kjennerud and Vabo, 2017; Mir et al., 2017; Reichborn-Kjennerud and Johnsen, 2018; Adi and Dutil, 2018; Thomasson, 2018; Nyikos and Soós, 2018; Torres et al., 2019).

In the context of NPG, some studies (Pollitt, 2006; Radcliffe, 2011; Reichborn-Kjennerud, 2013; Morin, 2016; Reichborn-Kjennerud, 2014b; Rosa and Morote, 2016; Gårseth-Nesbakk and Kuruppu, 2018; Svärdsten, 2019) discuss how the results of performance audit activities are communicated. Several studies undertaken since 2007 focused on external government entities, a feature of NPG (Pollock and Price, 2008; English et al., 2010). These studies find that performance audit on public–private partnerships, for example, can be instrumental in legitimising government policies (English, 2007). Approaches to internal audit have changed in recent years (Nerantzidis et al., 2020), with previous studies focusing on the independence of auditors and more recently published studies analysing the relationships between internal audit functions and financial management performance in the public sector (Iskandar et al., 2014) as the internal audit is seen as a component of the combined assurance model, together with the audit committee, management and external auditors. Finally, performance audit studies since the 2000s have examined corruption and ethics. Discussion of the ethical dimension of corporate governance (Fleming and McNamee, 2005; Appel and Plant, 2015; Barrett, 2019) and the internal audit function (Coram et al., 2008) reveals their roles in contributing to “risk management” (Coetzee, 2016) as they decrease corruption (Gustavson and Sundström, 2018), reduce conflicting management cultures (Christopher and Sarens, 2018) and limit whistleblowing by auditors (Rustiarini and Sunarsih, 2017).

4.2.3 Comprehensive audit.

Public sector auditing has undergone significant change in the period analysed in this literature review, shifting from providing oversight of proper management of resources, financial oversight and compliance (Guthrie, 1992) to a more consultancy such as role, in which management matters, including value-for-money and efficiency and effectiveness audits, are paramount (Monfardini and von Maravic, 2019). This new conceptualisation of audit also acts as a facilitator to implement public sector changes (Pallot, 2003). This transformation of the role of the audit (Schelker, 2012; Wilkins et al., 2017) is consistent with NPM principles (Hood et al., 1998) that stress managerial concepts such as efficiency and effectiveness. Consistent with this approach, some researchers argue that efficiency can be investigated or achieved through audit scrutiny (Radcliffe, 1998). However, evidence from previous studies (Seyfried, 2016) suggests that compromises are inevitable, for example, in terms of political pressures (Yamamoto and Kim, 2019). Our analysis reveals that audits conducted by government supreme audit institutions seek to understand if NPM has influenced audit reporting (Pollitt and Summa, 1997) and, in more recent years, whether reporting can deliver public value (Jeppesen et al., 2017; Cordery and Hay, 2019). Also, we find a study that investigates the impact of processes and internal and external factors on determining the effectiveness of the audit and whether this affects the implementation of the recommendations (van Acker and Bouckaert, 2019).

5. Conclusions and avenues for further investigation

Public sector auditing has attracted research interest over an extended period and our literature review has provided an answer to our first research question: What trends and themes stand out in the existing public sector auditing literature? The focus in the literature has changed over time, caused by developments in the public sector because of NPM and NPG.

We now turn to our second research question: What are the main gaps in the existing public sector auditing literature? Our analysis highlights that articles on public sector auditing no longer appear solely in accounting and auditing journal publications. Instead, the field has grown into a multi-disciplinary research area, attracting scholars and practitioners from various disciplinary backgrounds. This diversity suggests the possibility of a fascinating range of future research, some avenues for which are outlined below.

The adoption of NPM ideas has prompted a “marketisation” of the public sector. Further, the number of hybrid organisations (e.g. purchaser–provider models, contracting out, outsourcing, corporatisation, privatisation) has increased, driven by government policy based on NPM. These organisations create an entirely new set of auditing and accountability problems, which have received limited attention in the literature. Another avenue is to audit whole-of-government financial reports and governmental agency and decentralised entity reports (Pallot, 2003). Researchers could also consider how public sector organisations reshape auditing and accounting systems – not only as the “private” invades the “public” but as the “public” invades the “private”.

Another gap in the literature concerns public sector auditing in international organisations (e.g. the European Union, the North Atlantic Treaty Organisation and the United Nations). Researchers could investigate the role, identity and impact of supranational audit institutions such as the European Court of Auditors, which audits the European Union’s finances.

NPM has significantly affected the public sector over the past 40 years by reducing its size, reasserting political control and introducing NPM technologies (Guthrie et al., 1998; Guthrie et al., 1997; Olson et al., 1998). At the same time, NPM auditing practices have transformed the sector, making audit a central organising principle for society (Shore and Wright, 2015). Public sector organisations increasingly focus on the measures by which their performance is judged (efficiencies, costs and outcomes). While this has been studied, the implications of NPG in the public sector have been less explored and present an avenue for future research. Researchers could consider how a shift in focus from “compliance” to “outcomes” has affected public sector organisations’ audit performance. How have organisations fared when assessed in this context on their economy, efficiency and effectiveness? Moreover, what is the role of independent auditors and can they be genuinely autonomous if they are also pushing to introduce public sector reforms (Power, 1994)?

Earlier public sector auditing studies have sought to examine the efficiency and effectiveness of the audit to analyse the possible relationship between audit fees and the quality of the audit. However, more recently, fraud, corruption and ethical issues have emerged as key themes. While several articles have taken this focus, it remains a fruitful topic for examination, particularly concerning the audit of external entities and related part transactions (Cesário et al., 2020).

Further research on public sector auditing could also use multiples theories, system-oriented and economic theories and other theories closer to the NPG management logic, such as psycho-sociological theories. Past research has adopted established streams (especially isomorphism) of institutional theories (Hay and Cordery, 2021). We suggest future studies could use emerging streams of institutional theories (e.g. institutional logic, work and entrepreneurship) to analyse the exogenous pressures on the public sector and the role of public sector auditors in promoting and developing accounting and accountability changes within the public sector. Institutional logic has the potential to be integrated with other theories to cover the micro-dynamics involved in (re-)constructing auditing tools as they are implemented in everyday practices (Modell, 2009). Institutional logic can be combined with institutional work and entrepreneurship to investigate how actual auditing practices are translated in the public sector (Mouritsen, 2014). Institutional work also can be adopted to investigate the internal dynamics and the interactive nature of auditors’ relationship to institutional changes (Czarniawska, 2009; Mouritsen, 2014). Moreover, the role of auditors who enable changes (e.g. institutional entrepreneurs) could be investigated, considering their interests, identities, power and search for legitimacy.

Future research could also investigate public sector auditing in the emerging economies of Africa, Asia and South America, whether in single, multiple or comparative country studies. Additionally, little research exists on the role of the International Organisation of Supreme Audit Institutions’ (INTOSAI) Development Initiative (IDI) in developing countries in enhancing their performance and capacity (Gørrissen, 2020).

Researchers could also apply new research methods to the public sector auditing field. Multiple case studies and comparative country approaches would be of interest, especially those that use mixed methods. We see particular value in interpretive research for this field (Denzin and Lincoln, 2011), an innovative approach combining quantitative survey data and textual analyses with qualitative data from interviews and case studies. Generally, the field could benefit from comparing auditing practices in different jurisdictions and across Supreme Audit Institutions (SAIs) (including the Westminster, board and court models) (Bonollo, 2019; Hay and Cordery, 2018).

Future studies could also investigate international standardisation and harmonisation trends in public sector auditing. What auditing standards have been set for public sector organisations and are these different for the private sector? How do we assess the quality of those standards? Who sets the standards and what is their role in the field at large? We also call for more research on INTOSAI. As an independent, non-political organisation, INTOSAI acts as a recognised voice for SAIs in the international community, promoting good national governance and supporting SAI development, cooperation and performance improvement. We call for more studies on its role, governance, power, standard and impact on national SAIs. Researchers could also investigate SAIs’ independence, how they report findings, their media coverage and their methods for following up on audit results. More comparative studies could provide insight into different SAIs’ roles in policymaking and program evaluation (Bonollo, 2019; Johnsen et al., 2019; Reichborn-Kjennerud and Johnsen, 2018).

We also call for research into the role, identity, professional discretion, autonomy and image of auditors at different government levels (central, regional and local) and international organisations. Studies that discuss how auditors are selected, appointed and compensated in public sector organisations and their associated decentralised entities would be of value to the field (Radcliffe, 2012; Thomasson, 2018).

Finally, we call for a closer look at the opportunities and costs of digitalisation, digital technologies and big data for public sector auditing, auditors and audit institutions. Technology can strengthen public sector auditors’ investigative powers and increase transparency in their work (Antipova, 2019). Digital technologies may also help prevent fraud and corruption in public sector organisations. However, many questions remain about how technological change will shape public sector auditing in the future. What kinds of technologies are likely to exist and how will they affect the field going forward? What are the potential benefits and risks for auditors, auditees and audit institutions? Ultimately, new digital technologies will require audit institutions and auditors to adapt quickly in the face of significant change. We believe that scholars and practitioners could pay more attention to the dynamic capabilities of public sector auditors in terms of skills and competencies concerning new roles related to sustainability reporting and the U.N.’s sustainability development goals. Auditors and institutions will need research findings to reap the full benefit of future technological developments and tackle challenges along the way.

Acknowledgements Research financed by Norwegian Research Council, “Transformative Capabilities of Accounting Profession: Study of small and medium accounting practices”, grant ID: 301717.

Note

The asterisk (*) indicates that different suffixes were permitted.