The purpose of this paper is to analyze the extant research on management accountants (MAs) to unravel the complexity and intricacies of this kaleidoscopic occupation and identify avenues for future research.

A literature review of 154 papers focusing on MAs was carried out. The analysis primarily adopted the “becoming”, “doing”, and “relating” perspectives suggested by Anteby et al.’s (2016) framework on occupations. However, an additional perspective, labeled “making sense”, was added and used to review the extant research on MAs, given the pivotal role played by the cognition–action processes that individual MAs undertake and their influence on occupational dynamics.

The study analyzes how MAs enter the occupational community and the challenges they face (“becoming”), the intricacies of their tasks and their struggles for jurisdiction over both traditional and emergent activities (“doing”), and opportunities relating to the establishment of relationships with other occupational groups (“relating”). This social perspective on the MAs’ occupation is underpinned by a cognitive approach through which the ways in which MAs scan and interpret the environment in which they operate influence their actions (“making sense”) – that is, how MAs become part of the occupation, how MAs perform their tasks and how MAs relate to other occupations.

This paper disentangles the major challenges to MAs’ occupation and encourages the adoption of a meta-framework that integrates cognitive and social approaches to obtain a more comprehensive understanding of MAs. The proposed meta-framework may also be used to explore other occupational groups, including established staff functions such as IT and HR, as well as nascent occupations like data scientists and sustainability managers.

1. Introduction

Over the past few decades research on management accountants (MAs) or controllers [1] has gained traction within academia, as attested by the publication of numerous studies that shed light on MAs’ complex and multifaceted role within organizations (e.g., Burns and Baldvinsdottir, 2005; Byrne and Pierce, 2007; Goretzki et al., 2013). Research on MAs continues to represent a thriving field that lies at the center of a stimulating international academic debate (Cinquini et al., 2025; Franke and Hiebl, 2023; Järvenpää et al., 2023; Wiegmann et al., 2024). Both in theory and in practice, the development of the MAs’ occupation has progressed along different paths under the influence of several factors, including country-specific differences (Thaller et al., 2024). In some countries, MAs are already recognized as members of a distinct profession while elsewhere, MAs continue to be perceived as an occupation (Ahrens and Chapman, 2000; Heinzelmann, 2016).

From a sociological perspective, early contributions on professionalism distinguished clearly between occupations and professions, conceptualizing professionalization as a standardized process through which an occupational group attains the professional status (Abbott, 1988; Macdonald, 1995; Sarfatti Larson, 1977; Wilensky, 1964). This process is characterized by several key elements: the consolidation of a distinct body of specialized knowledge, the establishment of standardized training, the formation of a professional association, the attainment of legal recognition and regulatory protection and the development of a formal code of conduct (Wilensky, 1964). However, more recent studies have questioned the dichotomy between occupations and professions and the assumption of a standardized trajectory of professionalization (Evetts, 2003). Scholars increasingly acknowledge the potential existence of alternative pathways toward legitimacy and recognition, shaped by different institutional contexts, historical periods and organizational factors (Noordegraaf, 2007).

Consequently, this shift in perspective has led to a growing scholarly interest in occupational groups employed by organizations for whom the organizational dimension has been instrumental in shaping their knowledge and expertise (e.g., Muzio et al., 2011; Noordegraaf, 2007; Suddaby and Viale, 2011). This is the case for MAs—information workers (Goretzki et al., 2018a) whose expertise is embedded in the production, interpretation and dissemination of management accounting information in organizational contexts. Therefore, that which MAs are and do and the ways in which they relate to other occupational groups are dependent on the context in which they work, rendering the MAs’ occupation kaleidoscopic (Goretzki and Strauss, 2017).

Against this backdrop, this paper aims to initiate a new conversational direction in research on MAs with the goals of elucidating the intricacies of the MA’s occupation, unravelling its complexity and opening up new research avenues (Healey et al., 2023; Post et al., 2020). From a methodological perspective, this study includes a theoretically grounded review and discussion of extant literature on MAs (Breslin and Gatrell, 2023; Hiebl, 2023a; Hoon and Baluch, 2020). In this, we draw on Anteby et al.’s (2016) framework of occupation, which proposes the adoption of three theoretical lenses—“becoming”, “doing” and “relating”—when examining occupations to show “how occupational members learn to be part of the collective, what activities they engage in, and how they relate to others outside their groups” (Anteby et al., 2016, p. 188).

Our findings highlight various pathways toward and challenges to entry into the MAs’ occupational community (“becoming”), the multifaceted nature of their activities and their battles for jurisdiction over both traditional and emergent tasks (“doing”), and opportunities and criticisms relating to the establishment of relationships with other occupational groups (“relating”). The analysis also reveals that such a social view on the MAs’ occupation should be enriched with a cognitive perspective, given that MAs themselves are found to play a critical role in shaping their occupation through sensemaking processes (Gioia and Chittipeddi, 1991; Thomas et al., 1993). Therefore, a “making sense” perspective has been added to further disentangle the complexity of the MAs’ occupation.

The remainder of this paper is organized as follows. Section 2 presents the theoretical background, Section 3 illustrates the methodology, and Sections 4 and 5 analyze the extant literature on MAs. Section 6 discusses key findings and outlines potential directions for future research. The final section offers some concluding remarks.

2. Theoretical background

Occupations may be categorized as socially constructed realities that evolve over time (Berger and Luckmann, 1967). Building on this, Anteby et al. (2016, p. 187) define occupations as social entities that comprise a category of work, the actors understood—either by themselves or by others—as members and practitioners of this work, the actions enacting the role of occupational members and the structural and cultural systems upholding the occupation. According to this definition, a profession is conceived as a restricted sector of a given occupation that is able, by means of a professionalization process, to convince its stakeholders to be an “exclusive occupational group applying somewhat abstract knowledge to particular cases” (Abbott, 1988, p. 131). Professions are distinguished from occupations in particular by autonomy, specialized knowledge and authority over clients and subordinate occupations (Abbott, 1988; Hodson and Sullivan, 2012).

In light of the above, Anteby et al. (2016) conclude that an investigation of occupations inherently implies an investigation of professions, since the latter are a subset of the former. This aspect is of particular importance for the present study, given that, as previously stated, the development of the MA’s role both in theory and in practice is progressing in different ways worldwide (Thaller et al., 2024). Thus, Anteby et al.’s (2016) framework offers a fruitful theoretical lens through which to analyze occupations, professionalization processes and professions simultaneously, thereby offering an opportunity to interpret the overall literature on MAs.

Anteby et al.’s (2016) framework proposes the adoption of three lenses to explore different features of occupations: “becoming,” “doing,” and “relating.” The “becoming” lens focus on “the processes by which new members are inducted into established occupational communities as well as the individual-level transformations that occur among newly inducted members” (Anteby et al., 2016, p. 190). Adoption of this perspective entails focusing on the individual’s entry into an occupational community and on how the latter itself socializes new members by sharing its culture—that is, its values and norms. The “doing” lens, in turn, analyzes the tasks and practices that are inherent to a specific occupation. Given that members of an occupational community play an active role in crafting their activities, this lens also elucidates competition over tasks among “adjacent occupations”—that is, “occupations in closely related task domains” (Cacciatori, 2012, p. 1565) and the associated implications in terms of power and status (Anteby et al., 2016). Finally, the “relating” lens investigates the positive and collaborative relations among occupational groups within and beyond the organizations. Specifically, the “relating” lens analyzes the entire network of relationships that an occupation can build in its ecosystem of stakeholders.

Each of these lenses captures different aspects of an occupation. To further grasp occupations’ multifaceted nature, Anteby et al. (2016) introduced sub-categories within each lens that they refer to as “lens-filters” (Table 1).

The overarching “becoming” lens, which explores how individuals become part of an occupational group, is classified into three filters: “becoming socialized,” “becoming controlled,” and “becoming unequal” (Anteby et al., 2016). The “becoming socialized” filter highlights how newcomers gain admission to an occupational community, how they learn to belong to it and, in doing so, how they undergo cognitive and behavioral transformations to be accepted. This filter also sheds light on the boundaries that occupational communities establish between themselves and other occupations. The second filter—“becoming controlled”—focuses on the organizational dynamics that shape occupational members’ transformation, analyzing the mechanisms that render their work coercive and the workers themselves less free. Therefore, this sub-category helps researchers make sense of the different forms of control that occupational members may experience as they seek acceptance within a professional community (Anteby et al., 2016). Finally, the adoption of the “becoming unequal” filter permits an investigation of how the socialization of occupations results in social inequality and occupational segregation. Elements such as the unequal distribution of workers—in terms of gender, race and ethnicity, for example—and the unequal economic rewards lie at the core of this filter. In this regard, inequality arises not only from the demand-side, which gives rise to the image of the “ideal worker,” but newcomers themselves also play a pivotal role in shaping inequality owing to their individual opinions as to whether and how they can become members of an occupational community. This is exemplified by women’s relative lack of professional confidence compared to men (Anteby et al., 2016).

Shifting the attention from how individuals become members of an occupational community to what they do, Anteby et al. (2016) classified the “doing” lens into the following three lens-filters: “doing tasks”, “doing jurisdiction”, and “doing emergence”. The “doing tasks” filter focuses on the activities performed by occupational members and how these tasks influence their identity, sense of dignity and perception of their work as meaningful. Notably, this view helps illuminate the meaning that individuals attach to their work—for example, whether they regard their occupational activities as “dirty work” (Hughes, 1951) or “necessary evils” (Molinsky and Margolis, 2005)—and the practices in which they engage with the aim of influencing other people’s perceptions of their activities, such as language, rhetorics and other symbolic modes of expression. Interestingly, this filter also permits researchers to investigate the heterogeneity of tasks performed by people who belong to the same occupational community and to reveal how this heterogeneity impacts work outcomes, including inequality-generating mechanisms (Anteby et al., 2016).

The “doing jurisdictions” filter focuses on how occupational communities redefine and negotiate their jurisdictional boundaries in response to competing groups. Notably, conflicts over task jurisdiction can drive institutional changes, creating new opportunities for occupations. Thus, this filter ensures an investigation of the professionalization process of those occupational groups that aim to achieve the “monopoly” over a field of knowledge. Finally, the “doing emergence” field explores how new occupational communities may emerge when “groups of individuals start doing what other groups do not do or start doing differently what others already do” (Anteby et al., 2016, p. 208). Such a situation may arise when an occupational group begins performing tasks that have been hived off by another occupation or when “non-work” activities become legitimated as “work” activities in pursuit of recognition and legitimacy.

Finally, Anteby et al. (2016) classified the “relating” lens into the following filters: “relating as collaborating”, “relating as coproducing” and “relating as brokering”. The “relating as collaborating” filter facilitates the examination of the mechanisms and processes that enable collaborative relationships both within and across occupations, such as the use of boundary objects (Star and Griesemer, 1989). The “relating as coproducing” filter, in turn, focuses on how occupations interact with their stakeholder networks to co-develop expertise and authority thanks to their complementary roles, knowledge and skills. Therefore, this filter also allows researchers to examine the relationship between occupational communities and their clients, shedding light on how they can collaborate to achieve shared objectives. Finally, the “relating as brokering” filter focuses on how certain occupational groups make complex webs of relations work by connecting different actors and mediating diverse interests. To fulfill this role effectively, such occupational groups must develop relational and communicational skills and competencies.

The framework by Anteby et al. (2016) serves as a valuable lens for organizing and reviewing the extant literature on MAs. In fact, as observed above, MAs represent an occupational group whose knowledge and expertise are, to a significant extent, developed and shaped within the specific context in which they operate. Consequently, what MAs can be(come) and do, as well as how they relate to other occupational groups varies across contexts (Goretzki and Strauss, 2017). In this respect, Anteby et al.’s (2016) framework provides a nuanced understanding of occupations by considering not only how individuals enter an occupational community, but also the activities they perform and the relationships they can establish with other occupational groups. From this perspective, it broadens the range of lenses for analyzing an occupation, thereby enabling a more comprehensive discussion of a body of literature that, as previously noted, has evolved along multiple and diverse research trajectories over time.

3. Research method

3.1 Data collection

This theory-led literature review is based on a systematic search of relevant contributions on MAs. Accordingly, we first defined the inclusion and exclusion criteria (Denyer and Tranfield, 2006; Hiebl, 2023b; Petticrew and Roberts, 2008; Tranfield et al., 2003). More specifically, we decided to include papers written in English and published in journals listed in the Academic Journal Guide (AJG) ranking. In line with previous literature reviews (e.g., Boomsma, 2024; Ndemewah and Hiebl, 2022), we also decided to exclude non-empirical studies to focus only on prior empirical findings that can be compared and reinterpreted to propose novel insights.

To guarantee a coverage that is as comprehensive as possible (Hardies et al., 2024; Hiebl, 2023a, 2023b), we conducted a database-driven search using EBSCO, Scopus and Web of Science (Gusenbauer and Haddaway, 2020; Hiebl, 2023b). The search for relevant studies was carried out within the business, management and accounting subject area and no limitation on the year of publication was placed.

We used the following keywords as search terms: “management accountant,” “controller,” and “management accounting.” The term “management accountant” was selected because it is normally used to refer to the organizational actors responsible for the design, implementation and maintenance of management accounting systems within organizations. The word “controller” was used as a term often applied to professionals operating as MAs in many countries—in particular, German-speaking countries, Italy, The Netherlands and the Nordics (Ascani et al., 2021; Eskenazi et al., 2016; Granlund and Lukka, 1998; Messner et al., 2008). Finally, we used “management accounting” as a keyword to narrow the search to our field of interest given that the word “controller” is also used in research fields that are not strictly connected to management accounting, such as engineering. As such, the resulting research string was as follows: <“management accountant*” OR “controller*” AND “management accounting”>.

3.2 Data analysis

The search process, which was limited to titles, abstracts and keywords, yielded a total of 1,322 papers [2]. After we had removed 258 duplicate articles, a total of 1,064 papers remained. Of these, 938 papers were excluded after screening their titles, abstracts and, when necessary, full texts, as they did not meet the inclusion and exclusion criteria previously identified. For instance, we excluded several papers that mentioned MAs in their abstracts or keywords but for which MAs were not the focus of the study. In these cases, MAs were only interviewed to collect empirical data about certain management accounting practices which, instead, represented the actual topic under investigation. This process identified 126 papers for the review. We then carried out extensive snowballing, reviewing both references to and citations of the publications previously identified (Hardies et al., 2024; Hiebl, 2023b; Webster and Watson, 2002). This step resulted in the inclusion of 27 additional papers. A final search was conducted on May 19, 2025, to ensure that the sample included the most up-to-date research in the field. This additional search allowed us to add the paper by Kunz et al. (2025a) bringing the final data set for the review to 154 papers.

Regarding the analysis of the selected articles, we first collected information on the years of publication, journals and the countries and contexts of research. This allowed us to obtain a comprehensive overview of the literature. Then, we individually analyzed all papers and met several times to discuss the main themes and to develop an overall understanding of extant literature on MAs which served as a basis for further analysis. A key finding that emerged early on was that the MAs’ role is highly complex, making it imperative that extant research incorporate a multiplicity of perspectives and methodologies to provide a holistic understanding of the phenomenon under investigation.

To shed light on the intricacies of the MAs’ occupation and provide novel insights (Breslin and Gatrell, 2023; Hiebl, 2023a; Hoon and Baluch, 2020), we adopted Anteby et al.’s (2016) framework, applying the “becoming”, “doing” and “relating” perspectives to the 154 papers since, as stated above, this is a valuable lens for unpacking the multifaceted nature of the MAs’ occupation. The “becoming” lens was used to analyze and interpret papers focused on how newcomer MAs gain admission to management accounting functions within organizations and how they undergo transformations to be accepted. We adopted the “doing” lens, in turn, to explore papers on MAs’ tasks and practices and associated work outcomes. We also looked for signals of jurisdiction over tasks and whether MAs compete with other occupational groups. Finally, we applied the “relating” lens to papers focused on cooperation, collaboration and brokerage between MAs and their main stakeholders.

However, as the article analysis progressed, we realized that the a priori adoption of Anteby et al.’s (2016) framework was not conducive to fully representing the actual facets of literature on MAs. More specifically, although Anteby et al. (2016) emphasize that the ways in which members individually interpret their participation to occupational communities (p. 197) and make sense of their tasks (p. 203) are fundamental to exploreoccupations, they do not explicitly consider individual sensemaking processes (Gioia and Chittipeddi, 1991; Thomas et al., 1993). In fact, Anteby et al. (2016) address topics related, for example, to MAs’ perceptions of meaningful work and identity through the lens of “doing tasks”—an approach that does not legitimate the valuable insights into these topics that the literature on MAs already offers. Therefore, to further elucidate the cognition processes that individual MAs undergo, an additional lens labeled “making sense” was added.

Given that some papers investigate different interrelated phenomena to provide an exhaustive understanding of extant literature, we adopted a concept-centric approach according to which papers can fall in more perspectives (Webster and Watson, 2002). For each perspective, we analyzed the dominant research methodologies and theoretical underpinnings and identified the most-researched countries. Following the analysis of the papers, we met several times to discuss and refine our findings. The results of this analysis are discussed in the following sections (see supplementary materials).

4. Overview of literature on MAs

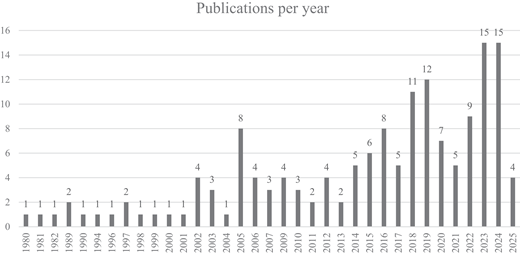

An analysis of publications per year reveals that MAs began to attract scholarly attention during the 1980s in the wake of Hopper’s (1980) contribution. Although during the 1980s and 1990s a few studies focused on MAs, interest in the topic has grown since the 2000s. The 2000s–2010s marked the establishment of research on MAs as a distinct field of study, with numerous studies exploring the complexity of MAs’ roles within organizations. As Figure 1 illustrates, a fruitful debate on MAs continues, as demonstrated by the publication of 55 of the 154 studies between 2020 and 2025. This recent growth may be partially attributed to the fact that MAs’ occupation is influenced by several dynamics that occur within specific historical contexts. In particular, digitalization and sustainability have emerged as two key phenomena, and this has prompted scholars to explore their influence on MAs, thereby contributing to the expansion of this research area.

Shifting the attention from the trend of publications to the distribution of papers across journals, as represented in Table 2, the selected papers have been published in 49 journals. This widespread distribution highlights the broad academic interest in this topic. Notably, papers on MAs appear not only in accounting journals but also in journals that focus primarily on other disciplines, such as information systems, management, strategy, education and organizational behavior. While these diverse perspectives have significantly enriched the academic debate on MAs, this heterogeneity further underscores the need for analyzing the extant body of literature in depth.

Although the understanding of the geographical contexts in which research on MAs has been conducted is shaped by a key limitation—namely, that the sample comprises only English-language journals—it should be underlined that Europe is the most investigated continent and that only a few studies have been carried out elsewhere, such as in North America, Asia, Africa and Oceania. Most European studies have been carried out in the UK or Ireland and German-speaking countries, such as Austria, Germany and Switzerland. Such contexts are associated with a long-standing tradition of research in management accounting and controlling respectively (Ahrens, 1997; Burns et al., 1999; Messner et al., 2008). An increasing number of recent studies have been conducted in Nordic countries, such as Denmark, Finland and Sweden, in The Netherlands, and in France, as well as in Southern and Eastern Europe, including Italy, Portugal and Slovenia. A remarkable number of papers adopt a comparative perspective in examining MAs in different European countries, thus contributing to a broader understanding of country-related differences.

Notably, the analysis highlights the widespread exploration of MAs in the context of private companies, while research on public sector organizations remains limited. Most studies examining private companies focus on medium and large enterprises, although interest in smaller companies is increasing.

The next section discusses the extant literature on MAs, structured around the perspectives identified through our data analysis: “becoming” management accountants, “doing” management accountants’ tasks, “relating” to other occupations and “making sense” of management accountants’ occupation. Each subsection discusses key findings and areas of ongoing debate, while also enabling the identification of directions for future research.

5. Findings

5.1. “Becoming” management accountants

Less than one-fifth of the studies under review examine the factors that contribute to individuals “becoming” MAs. Particular attention is paid to how MAs “become socialized,” focusing on the role that education programs (Budding et al., 2022; Hassall et al., 2005; Novin et al., 1990) and teaching methodologies (Flamand and Jaumier, 2023; Jakobsen et al., 2019) play in shaping future MAs’ competencies. This issue has resurfaced over multiple years, and the need to continuously update the training offerings emerges clearly because the skills and knowledge required for MAs are constantly evolving (Howcroft, 2017).

In this regard, the studies highlight the importance of newcomers’ acquisition of key competencies, such as strong accounting skills (Adhariani, 2020; Budding et al., 2022; Novin et al., 1990), competencies pertaining to digital technologies (Spraakman et al., 2015) and business analytics (Oesterreich et al., 2019), and sustainability knowledge (Halari and Baric, 2023; Schaltegger and Zvezdov, 2015). Meanwhile, the literature appears to converge on the idea that becoming socialized as MAs also implies the need to develop soft skills and managerial competences (Adhariani, 2020; Hassall et al., 2005; Montano et al., 2001; Siriwardane et al., 2015). This is attested by job advertisements that show how companies seek “hybrid MAs” (Rieg et al., 2023) who act as “number crunchers” but are also able to critically analyze, interpret and interrogate results (Ala-Heikkilä and Järvenpää, 2023; Ott, 2023). Further evidence in this regard is provided by interviews with MAs’ employers (Lepistö and Ihantola, 2018). During recruitment processes, employers tend to take technical skills for granted and prioritize charismatic candidates who can add value to the organization (Lepistö and Ihantola, 2018). Literature has also emphasized that the public image of MAs, as portrayed in professional journals, plays a key role in socializing newcomer MAs by shaping their expectations regarding the cognitive and behavioral skills that MAs should possess (Baldvinsdottir et al., 2009, 2010; Goretzki et al., 2022).

It is worth noting that most of these studies have been conducted in German-speaking or Nordic countries, where universities play a key role in educating MAs and professional bodies do not regulate entry requirements as the Chartered Institute of Management Accountants (CIMA) does in Anglo-Saxon contexts. However, research findings pertaining to German-speaking countries reveal that, although the professional association of controllers—that is the Internationaler Controller Verein (Goretzki et al., 2013)—does not formally regulate the requirements for the occupation, it plays a key role in promoting the development of MAs’ skills and competencies and in fostering a sense of exclusive community that influences MAs’ socialization.

Notably, a very limited portion of the studies focused on how MAs “become controlled.” Among these, Lambert and Pezet (2011) used a single case study to analyze the behaviors that MAs themselves adopted within the management accounting department to present themselves and be recognized as “producers of truthful knowledge” within the organization (Lambert and Pezet, 2011, p. 10). In a similar vein, Goretzki and Pfister (2023) revealed MAs’ conflicts in developing productivity measures that are paradoxically also used to assess and control their own productivity. Interestingly, several studies also explored the factors that push MAs to sacrifice part of their freedom to become and act as expected. In this regard, drawing on a large sample of business unit MAs and respectively using electroencephalographic (EEG) and functional magnetic resonance imaging (fMRI), Eskenazi et al. (2016) and Slapničar et al. (2021) reported the neurobiological traits that lead MAs to control their behavior by misreporting because of the pressure to satisfy managers that they perceive. Together, these findings suggest that once MAs realize the paradox inherent in their being controllers while simultaneously feeling controlled, they submit themselves to these control logics and regulate their behavior to safeguard their role.

Finally, scant attention has been paid to how MAs “become unequal.” From a demand-side perspective, Ala-Heikkilä et al. (2024) and Cimirotić et al. (2017) address the topic of gender by investigating how female MAs can advance their careers within organizations. While Cimirotić et al. (2017) illustrated the factors that enable women to reach leadership positions in management accounting functions or hinder them from doing so, Ala-Heikkilä et al. (2024) point out that to construct their identity as professionals, female MAs require male support, raising concerns about potential risks for the company itself. This stream of research is at its initial stage focusing attention only on gender inequalities from a demand-side perspective, thus failing to highlight other inequalities, how they affect the MAs’ occupation and what actions may be undertaken to help reducing inequalities. However, it is worth noting that an examination of these issues would reveal only one facet of the phenomenon, as it remains plausible that MAs themselves may unconsciously engage in self-sabotaging practices that shape inequalities and undermine their occupation.

Overall, although some studies have begun to explore how MAs enter the occupation, this line of research remains nascent, particularly in relation to the dynamics of inequality. With the exception of some studies (Adhariani, 2020; Novin et al., 1990; Siriwardane et al., 2015; Spraakman et al., 2015), the research examined explored this issue in the European context—particularly in German-speaking and Nordic countries which lack any standardized professional path toward becoming MAs. The need to obtain a preliminary overview of such heterogeneous phenomenon has likely driven scholars to adopt quantitative methodologies for the purpose of gathering information from large data sets. Studies that have explored how professionals become MAs from a qualitative perspective have primarily relied on identity theories (e.g., Alvesson and Willmott, 2002; Ashforth et al., 2008; Giddens, 1991; Sveningsson and Alvesson, 2003) and sociological theories (e.g., Barthes, 1964; Foucault, 1966, 1982) to interpret their empirical findings.

5.2. “Doing” management accountants’ tasks

Proceeding to the “doing” lens, more than half of the studies under review focus on what MAs do within organizations. Significant focus is afforded to what tasks MAs do (Anteby et al., 2016) by exploring MAs’ activities (Budding et al., 2019; Newman et al., 1989 ), their heterogeneity according to their position within organizations (Rosenberg et al., 1982; Rosenzweig, 1981) and their changes in relation to the degree to which MAs are involved in decision-making (Byrne and Pierce, 2007; Coad, 1999; De Loo et al., 2006; Enslin, 2023; Enslin et al., 2023a, 2023b; Lambert and Sponem, 2012; Mouritsen, 1996; Puyou and Faÿ, 2015; Wolf et al., 2015; Zoni and Merchant, 2007).

Research has also shown how MAs’ tasks change when they experience the famed transition from the role of “bean counter” to that of “business partner” (Friedman and Lyne, 1997; Paulsson, 2012; Yazdifar and Tsamenyi, 2005). Nevertheless, evidence from surveys on large sample of MAs (Bogt et al., 2016; Rieg, 2018; Szukits, 2019) as well as from cross-sectional field studies and case studies (Bruesch and Quinn, 2024; Graham et al., 2012; Karlsson et al., 2019a) indicates that, in practice, when such a transition occurs, although MAs increasingly perform more strategic activities, they often continue to carry out traditional tasks, such as data provision. Therefore, according to several authors who report “hybrid” roles for MAs, it would be more appropriate to talk about role “extension” than an actual role “change” (Burns and Baldvinsdottir, 2005; Karlsson et al., 2019a; Rieg, 2018; ten Rouwelaar et al., 2021). This view is further confirmed by Rautiainen et al. (2024) who, by adopting an identity perspective to explore the influence of Robotic Process Automation (RPA) software on MAs within a Finnish bank, conclude that MAs must develop a fluid identity that allows them to flexibly switch between tasks that pertain to very different roles, i.e. bean counters, business partners and IT specialists. The complexity of MAs’ role extension/change requires the adoption of theoretical approaches that enable researchers to disentangle the interrelated factors influencing the transition. For this reason, scholars mainly resorted to theories such as the institutional theory (e.g., DiMaggio, 1988; DiMaggio and Powell, 1983; Seo and Creed, 2002), the contingency theory (e.g., Fisher, 1995, 1998) and the role theory (Kahn et al., 1964; Katz and Kahn, 1978).

Of particular interest is the bulk of research that has provided a deeper understanding of how ethical values (Ariail et al., 2024; Musbah et al., 2016) and the ways in which organizations promote ethical behaviors (Hirth-Goebel and Weißenberger, 2019; Ziegenfuss et al., 1994) influence MAs’ performance in their activities (Hiller et al., 2014; Shafer, 2002; Shafer et al., 2002). Although findings suggest that organizational values appear to be more relevant than professional codes of conduct in driving MAs’ behaviors (McGregor et al., 1989; Musbah et al., 2016), when organizations promote unethical behavior—for example, protecting the interests of the organization at the expense of the stakeholder—MAs experience the ethical pressure caused by organizational–professional conflict, which ultimately limits their tasks (Hiller et al., 2014; Shafer, 2002; Shafer et al., 2002). This trend is particularly pronounced in countries where MAs are organized into a profession and must thus adhere to an ethical code of conduct established by a professional institute. Accordingly, most of these studies have been carried out in North America, where MAs are acknowledged as a professional group with a code of conduct established by the Institute of Management Accountants (IMA).

Notably, the literature exploring MAs’ tasks also reports evidence of business unit MAs, whose main responsibility is to support local managers’ decision-making processes, engaging in “necessary evils” (Molinsky and Margolis, 2005)—a “necessary evil” being an “act that causes emotional or physical harm to another human being in the service of achieving some perceived greater good or purpose” (Molinsky and Margolis, 2005, p. 245). This happens because business unit MAs, positioned between corporate finance functions and operational managers, must deal with this dual responsibility. Examples of “necessary evils” include data misreporting (Maas and Matějka, 2009), profit manipulation (Lambert and Sponem, 2005) and budgetary slack practices (Davis et al., 2006; Hartmann and Maas, 2010; Indjejikian and Matějka, 2006). It should thus be underlined that misreporting is not only a practice through which MAs regulate their own behavior in response to managerial pressure (i.e. “becoming controlled”); it is also a strategy for navigating conflicting managerial expectations (i.e. “doing tasks”).

Shifting the focus from “doing tasks” to “doing jurisdictions” (Anteby et al., 2016), a notable strand of research examines the processes by which MAs become professionalized across different countries. These studies emphasize the roles that educational requirements and professional bodies play in establishing a “monopoly” over the profession. With the exception of Brandau et al. (2014), who provide interesting insights on Latin America, all studies explore the European context, focusing primarily on a comparative analysis of the UK and German contexts. In the UK, CIMA offers membership and educational training at the end of which MAs are qualified and recognized as professionals in management accounting (Ahrens and Chapman, 2000; Heinzelmann, 2016; Montano et al., 2001). By contrast, in German-speaking countries, controllers are not organized into a formal profession, and their education depends on universities and private institutes (Ahrens and Chapman, 2000; Heinzelmann, 2016). Interestingly, these heterogeneous approaches to MAs’ education and recognition in the European context can represent an obstacle to labor mobility for MAs within Europe (Heinzelmann, 2016). The issue of professionalization has also been investigated at an organizational level through case studies conducted in family firms (Goretzki et al., 2013; Hiebl and Mayrleitner, 2019). This trend is in line with those sociological studies that suggest that professionalization can also occur within organizations (Muzio et al., 2011; Noordegraaf, 2007; Suddaby and Viale, 2011). For instance, Goretzki et al. (2013) illustrated the case of a newcomer “strong” CFO who drove the professionalization process for MAs by enhancing their status and recognition within the organization.

Scholars have also investigated how cultural and institutional changes create new opportunities for defining the jurisdictional boundaries of the MAs’ occupation within organizations. For example, factors such as national culture (Curtis et al., 2016; Granlund and Lukka, 1998), the adoption of laws and regulations (Holmgren Caicedo et al., 2018; Janin, 2017; Järvinen, 2009; Lantto, 2014; Oppi and Vagnoni, 2020; Steens et al., 2020) and the influence of the COVID-19 pandemic (Kunz et al., 2025a) and economic crisis (Endenich, 2014) have empowered MAs to redefine the content of their work.

In line with this, the literature reports that operational managers have undertaken some activities traditionally pertaining to MAs over the years, thus expanding their own competencies into the sphere of management accounting (Ezzamel and Burns, 2005; Lambert and Sponem, 2012; Mouritsen, 1996). This has often led to tensions between MAs and operational managers (Ezzamel and Burns, 2005; Johnston et al., 2002; Oppi and Vagnoni, 2020; Vaivio, 2004), as the production of accounting information has become a source of conflict and competition—that is, “doing jurisdictions” (Anteby et al., 2016). In this vein, a valuable branch of literature examines how MAs negotiate the content of their work and thus their jurisdictional boundaries with IT-related occupations. Several studies have explored how the use of Enterprise Resource Planning (ERP) systems impacts MAs’ tasks (Granlund and Malmi, 2002; Sánchez-Rodríguez and Spraakman, 2012; Scapens and Jazayeri, 2003), demonstrating how their adoption gives rise to “ambiguous” consequences for MAs. Interestingly, a shift in responsibilities and tasks from MAs to IT staff and vice versa is found, either fostering a “hybridization” of roles (Caglio, 2003) or creating competition between these groups (Carlsson-Wall et al., 2022; Newman and Westrup, 2005).

In this regard, the ongoing digitalization process of the management accounting function has led to an increase in research on the potential professional competition between MAs and data scientists. Recent qualitative and quantitative studies suggest that data scientists can win such a competition owing to their expertise in digital technologies (Andreassen, 2020; Oesterreich et al., 2019), potentially confining MAs to narrower and more specialized roles (Andreassen, 2020). Although the results illustrate that the use of digital technologies can be a source of role conflict and ambiguity for MAs (van Slooten et al., 2024), MAs have yet to fully exploit the opportunities that these technologies offer in both large firms (Boerner et al., 2025; Spraakman et al., 2021) and SMEs (Trinh, 2024).

By contrast, the advent of digital technologies has recently given rise to a fruitful debate about the new opportunities for the MA occupation (i.e. “doing emergence”). Several studies suggest that MAs can enhance their relevance within organizations owing to their knowledge of the business and their technical skills in filtering and interpreting large volumes of data and in selecting the most relevant information to support decision-making processes (Cavélius et al., 2020; Järvenpää et al., 2023; Mudau et al., 2024; Oesterreich et al., 2019; Robalo and Moreira, 2020; Szukits, 2022). In this regard, the literature emphasized that, to fully grasp the opportunities that digitalization creates, MAs should develop expertise in data analytics, data mining, econometrics and statistics (Franke and Hiebl, 2023; Oesterreich et al., 2019; Steens et al., 2024). These skills would be valuable for MAs not only in terms of improving the quality of data-driven decision-making (Franke and Hiebl, 2023) but also in terms of understanding data scientists’ logic and data management templates (Berlinski and Morales, 2024). This is becoming increasingly important as MAs and data scientists are expected to collaborate in designing management accounting systems guided by IT-driven templates for organizing and presenting information (Berlinski and Morales, 2024).

Similarly, the growing importance of sustainability in companies’ agendas has led to new emerging tasks for MAs. Schaltegger and Zvezdov (2015) identified a potential role for MAs as gatekeepers of sustainability information for decision-makers, a view that more recent studies (Kunz et al., 2025b; Wenzig et al., 2023) have confirmed. However, although this line of research remains in its infancy, the results appear to converge on MAs’ limited involvement in sustainability-related management accounting practices (e.g., Egan and Tweedie, 2018; Hoang et al., 2020; Mistry et al., 2014). The barriers that contribute to the scarcity of their involvement may be found in MAs’ innate focus on financial metrics, a lack of adequate technical skills and the perception that sustainability falls outside their domain (Halari and Baric, 2023; Kunz et al., 2025b; Wenzig et al., 2023). To overcome these barriers and encourage MAs to seize these emergent opportunities, Kurki and Järvenpää (2024) have highlighted the need for a clear mandate from upper management to involve MAs and support their acquisition of adequate knowledge through participation in sustainability-related activities.

Although both digitalization and sustainability issues have the potential to broaden the scope of the MAs’ tasks or compromise the boundaries of their jurisdiction—thus showing the two sides of the same coin (i.e. “doing emergence” versus “doing jurisdiction”)—what appears to differ is MAs’ attitude toward these two phenomena. Regarding digitalization, MAs are willing to compete with data scientists to carve out a role for themselves in the use of these technologies; meanwhile, although MAs could play a more central role in sustainability, they appear hesitant to engage with this topic, resulting in a lack of rivalry with sustainability managers. The potential competition with data scientists may arise from the fact that the skill set that MAs are expected to develop primarily centers on technical competencies, while accounting expertise and business knowledge remain central to their domain. In the context of sustainability, however, this dynamic shifts due to the emergence of the sustainability manager’s role, which assumes responsibility for the broader sustainability agenda. In this context, while MAs may merely contribute to specific tasks—such as the measurement of sustainability-related performance—it remains their responsibility to eventually integrate these aspects into the management control systems.

5.3. “Relating” to other occupations

Although only a limited portion of the studies adopted a “relating” perspective on MAs (Anteby et al., 2016), existing research provides valuable insights into how MAs interact with their stakeholder ecosystems. Notably, regarding “relating as collaborating” (Anteby et al., 2016), the literature mainly explores MAs’ collaboration with operational managers to shed light on their so-called business orientation, which is expected to favor collaborative relationships (Hadid and Al-Sayed, 2021; Jakobsen, 2024; Järvenpää, 2007; Pavlatos and Ioakimidis, 2024). This collaboration may be fostered not only by organizational factors, such as the existent culture (Hadid and Al-Sayed, 2021; Järvenpää, 2007; Pavlatos and Ioakimidis, 2024), but also by individual factors, such as the MAs’ attitudes toward experimentation with new management accounting tools to support decision-making processes (Coad, 1999; Emsley, 2005; Emsley et al., 2006; Emsley and Chung, 2010; Pavlatos and Ioakimidis, 2024; Vedd and Kouhy, 2005).

Interestingly, a line of studies acknowledges the key role that MAs play when they are involved in cross-functional projects. Notably, these contributions recognize MAs’ ability to add value to strategic topics, such as strategy formation (Ahrens, 1997; Aver et al., 2009; Erhart et al., 2017; Fourné et al., 2023) and the implementation and use of strategic management accounting tools (Hadid and Al-Sayed, 2021; Pasch, 2019; Vedd and Kouhy, 2005). In this regard, the literature highlights how these strategic practices may serve as “boundary objects” across occupations that favor collaboration between different groups and facilitate managers’ acceptance of MAs as business partners (Windeck et al., 2015).

Furthermore, studies acknowledge that the collaborative relationships that MAs build with other groups foster innovation (Rodgers et al., 2022) and support the coproduction of knowledge and expertise. This knowledge is ultimately embedded in the tools that are co-produced through cross-functional collaborations (Cinquini et al., 2025; Henttu-Aho et al., 2023), i.e. “relating as coproducing” (Anteby et al., 2016). Research in this domain explores MAs’ involvement in rolling forecasts (Henttu-Aho et al., 2023), strategic capital investment projects (Karlsson et al., 2019b) and project management (Malagueño et al., 2021), demonstrating how new insights emerge to enhance decision-making. Though limited, these studies are characterized by the use of different theories that include actor–network theory (Latour, 1987, 1999, 2005) and pragmatic constructivism (Nørreklit, 2017; Nørreklit et al., 2010), which consider the roles of human and non-human actants and highlight MAs’ role as mediators of different interests (Henttu-Aho et al., 2023; Karlsson et al., 2019b).

This “mediator” role that MAs play is relevant to the filter “relating as brokering” (Anteby et al., 2016). As information workers positioned between top management and operational managers, MAs inherently act as brokers within organizational boundaries. Management of the complex web of relations that derives from their dual responsibility—“functional responsibility” versus “local responsibility” (Maas and Matějka, 2009)—is particularly challenging for MAs, considering that different groups of actors hold different expectations regarding the MA’s role (Byrne and Pierce, 2018; Hopper, 1980;Matanovic et al., 2022; Nitzl and Hirsch, 2016; Pierce and O’Dea, 2003; ten Rouwelaar et al., 2018; Wiegmann et al., 2024). Therefore, MAs often resort to “tactics” that pertain to the use of information that they obtain from their privileged position (Goretzki et al., 2018a, 2018b; Mack and Goretzki, 2017; Puyou, 2018). For example, Goretzki et al. (2018a) demonstrated that the skillful management of information—that is, “‘what’ should be reported, ‘how’ it should be reported and ‘when’ it should be reported” (p. 8)—represents a crucial means by which MAs can “present themselves as competent and trusted partners to all their stakeholders” (Goretzki et al., 2018a, p. 8). Furthermore, studies highlight that the characteristics of management accounting tools and how they are used by MAs—for example, the interactive or diagnostic use of a Performance Measurement System (PMS) (Simons, 1995)—influence their brokerage role within the organization (Baraldi et al., 2023; Goretzki et al., 2018b; Hartmann and Maas, 2011; Henttu-Aho, 2016; Wiegmann et al., 2024). For instance, Goretzki et al. (2018b) demonstrated how business unit MAs used self-developed spreadsheets as devices with which to actively influence the construction of central forecasting systems and mediate between local and corporate interests. MAs’ brokerage role has also been discussed in connection with their involvement in sustainability practices by Schaltegger and Zvezdov (2015) who, as noted above, defined MAs as gatekeepers or brokers who select sustainability-related information produced by sustainability managers and oversee its exchange among managers and toward the top management. The brokerage role provides MAs with privileged access to information, potentially enhancing their strategic significance within organizations. However, while MAs may be regarded as valuable partners, this role could potentially lead to their “social isolation,” as they may find themselves intentionally excluded from meetings to prevent them from accessing “secret” information.

5.4. “Making sense” of management accountants’ occupation

A recent line of studies has started exploring how MAs interpret their role and the implications of this sensemaking activity (Gioia and Chittipeddi, 1991; Thomas et al., 1993) on their recognition as members of the MA community, on their activities and on their relationships with other organizational groups.

Studies demonstrating how MAs’ worldview of the MA community is shifting are particularly relevant. Thaller et al. (2024) found that younger MAs increasingly prioritize job satisfaction over company objectives performance, leading to frequent lateral moves and shorter retention periods per position. This poses new challenges for companies, which must offer attractive career opportunities if they are to retain talented MAs. Tensions also arise from misaligned role expectations between MAs and their employers or operational managers (Ala-Heikkilä and Järvenpää, 2023). This raises an additional challenge for organizations, considering that newcomer MAs are willing to change companies frequently if they are not satisfied (Thaller et al., 2024). By comparing these results with those concerning how MAs become socialized within their occupational group, the attention appears to shift from the analysis of factors that operate at the macro level—such as national educational programs—and the meso level—such as employers’ requirements—to factors that operate at the individual level, such as MAs’ personal expectations and satisfaction, revealing the need to consider the more intrinsic motivations that inspire individuals to work as MAs.

This aspect is particularly relevant, given that a significant body of literature has begun to focus on how MAs attach meaning to their tasks and their relationships with other organizational actors according to their understanding of the MA’s role and their aspirations (Ahrens and Chapman, 2000; Burghardt and Moeller, 2024; Goretzki and Messner, 2019; Horton and Wanderley, 2024; Morales, 2019; Rautiainen et al., 2024; Taylor and Scapens, 2016; Tillema et al., 2022; van der Steen, 2022). This perspective offers an alternative view of MAs’ work, which has recently been examined through identity theories. In this regard, the Alvesson and Willmott’s (2002) framework on identity regulation, the Ashforth et al. (2008) social identity theory and the concept of “identity work” (Sveningsson and Alvesson, 2003), have been used to understand how MAs interpret and redefine their tasks and interactions to align what they actually do with what they aspire to do.

In this regard, studies exploring MAs’ tasks have incorporated the concept of “dirty work”—that is, “work that is perceived as degrading, humiliating and demeaning to those performing it” (Hughes, 1951 in: Brown, 2015, p. 28)—to understand how MAs attach negative meanings to aspects of their work. These studies reveal that MAs often feel devalued when performing tasks that they consider misaligned with their ambitions (Heinzelmann, 2018; Lepistö et al., 2018; Morales and Lambert, 2013). Examples of activities that create frustration for MAs often relate to the use of technologies, such as data cleaning activities (Heinzelmann, 2018; Morales and Lambert, 2013). However, the vignette about the “deviant accountant” reported by Morales and Lambert (2013) underscores the importance of challenging the assumption that MAs only consider tasks that are traditionally linked to business partner models to be rewarding. The deviant accountant strategically reframed “dirty work” as a resource with which to attain recognition and consolidate power within the organization. Relatedly, Hiller et al. (2014) demonstrated that as MAs gain recognition within organizations, they develop a stronger identification with the values of the MAs’ occupation, which include integrity, respectability and trustworthiness. MAs thus become less willing to compromise their ethical values for the sake of the company to such an extent that they consider leaving the company to safeguard their ideals.

6. Discussion

The aim of this paper was to analyze the extant literature on MAs to disentangle the occupation’s complexity, to understand the intricacies of MAs’ realities and to delineate new research avenues. The adoption of Anteby et al.’s (2016) framework helped elucidate “local variations and global influences” (Goretzki and Strauss, 2017) pertaining to how MAs enter the occupational community (“becoming”), the activities they perform and the struggle for gaining jurisdiction over specific tasks (“doing”) and how they establish collaborative relationships with other occupational groups (“relating”). Nevertheless, our analysis of the literature on MAs provided an opportunity to recognize that the ways in which individual MAs interpret the environment in which they operate can profoundly influence their entry into a professional community and how they make and assign sense to their tasks and relationships with other organizational members (“making sense”). More specifically, research reveals that the way individuals make sense of the values that should guide their work as MAs plays a key role in shaping both their entry into the occupation and their decision to remain within a company (Ala-Heikkilä and Järvenpää, 2023; Thaller et al., 2024). In addition, how MAs interpret their tasks (Morales and Lambert, 2013) and construct meaning around their perceived usefulness for recognition (Morales, 2019) significantly influences their willingness to engage in these tasks. A similar dynamic emerges in their interactions with other organizational actors. The way MAs make sense of both intra- and inter-functional interactions—what Goretzki and Messner (2019) call “backstage and frontstage interactions”—plays a crucial role in shaping how they decide to interact with other occupational groups. Taken together, these findings suggest that adopting a sensemaking perspective is pivotal to gaining an in-depth understanding of the complexity of MAs’ roles and shedding light on the intricacies of the MAs’ occupation.

Probing the sensemaking research further, the literature posits that sensemaking involves the interaction of information seeking, meaning ascription and action (Gioia and Chittipeddi, 1991), including key cognition–action processes of environmental scanning, interpretation and the associated responses (Gioia and Chittipeddi, 1991; Thomas et al., 1993). In particular, scanning refers to information gathering that is an antecedent to interpretation and action. In scanning the environment in which they are involved, actors have access to more information than they can use, and so they must be selective when choosing useful information (Thomas et al., 1993). Therefore, individuals scan according to their perceptions of the necessity for information and, consequently, they differ with respect to the amount of information used. Once information has been collected, individuals assign meaning to this incoming information by interpreting it (Thomas et al., 1993). These meanings attached to issues are often the result of the categories—the cognitive classifications that group objects and events (Rosch, 1978)—that individuals use [see Morales (2019) on how MAs categorize their activities]. Therefore, interpretation mobilizes actions in a particular direction, and effective actions often depend on the ability to implement decisions based on scanning strategies and subsequent interpretations of strategic information (Thomas et al., 1993). In this light, the sensemaking processes of scanning and interpretation have implications for action (Thomas et al., 1993) that, in our case, correspond to how individuals become MAs, how MAs perform tasks and how they relate to other occupational groups. For instance, the “deviant accountant” (Morales and Lambert, 2013) exemplifies the MA’s ability to scan and interpret the context in which they are involved and that permitted them to implement successful actions (i.e. perform routine tasks) to gain recognition within the organization.

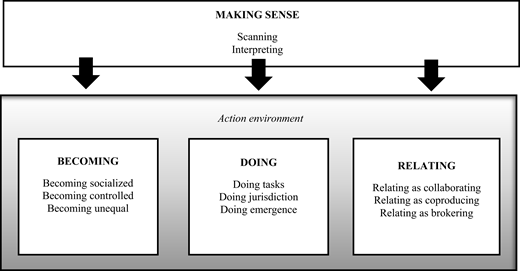

Thus, the sensemaking perspective can represent an additional foundational layer for understanding occupations that enriches the Anteby et al.’s (2016) framework. In particular, the “becoming,” “doing,” and “relating” lenses offer a social perspective on the ways in which occupational members interact to become part of their professional community, to perform their activities and to establish relationships with other organizational actors. However, research on MAs also highlights that the ways in which individuals interpret their own roles and make sense of tasks and interactions play a critical role in shaping the dynamics through which MAs enter the occupation, perform their activities and relate to others. Therefore, the ways in which individuals scan and interpret reality influence their actions (“making sense”)—that is, how they become part of the occupation (“becoming”), how they perform their tasks (“doing”) and how they relate to other occupations (“relating”). Including a sensemaking perspective permits to enrich the social view of occupations with a cognitive lens to develop a meta-framework that provides a more holistic understanding of the MAs’ occupation and a conceptual basis on which to advance research on MAs (Figure 2). In the sections that follow, we highlight several relevant new research areas that lie at the intersection of individual sensemaking and social construction processes that warrant further investigation.

6.1. “Making sense” of “becoming” management accountants

Studies that align with the “becoming” perspective (Anteby et al., 2016) have mainly explored how MAs enter the occupation by adopting the national and organizational perspectives of analysis (Hassall et al., 2005; Montano et al., 2001; Siriwardane et al., 2015). These specific focal points stem from the country-specific differences in education systems and in the occupation’s organization according to national laws and regulation, demonstrating the absence of a standardized pathway for entry into the MAs’ occupation (Heinzelmann, 2016). Moreover, at an organizational level, the requirements for “hybrid MAs” (Rieg et al., 2023) who possess complementary skills and competencies in addition to charisma (Ala-Heikkilä and Järvenpää, 2023; Lepistö and Ihantola, 2018; Ott, 2023) may influence MAs’ entry into the occupation. However, apart from a few exceptions (e.g., Thaller et al., 2024), the extant literature pays only limited attention to the role that MAs themselves play in deciding whether and how to enter the occupation according to their individual perceptions and understandings (“interpreting”). Future research should thus explore the motivations that guide individuals to enter the profession in greater depth. In addition, considering that applicants actively choose the companies to which they submit their CVs, it would be interesting to explore the information that future MAs scan prior to their employment in organizations with the aim of elucidating the factors—such as ideals, work–life balance and career progression—that inspire their choices (“scanning”). In this line, it could also be interesting to explore how and why MAs decide to work in e.g. non-profit or public sector organizations, where criticisms related to the adoption of non-economic logics often emerge (Kunz et al., 2025b). Future research should also investigate the factors that contribute to shaping MAs’ self-perception and ability to positively or negatively influence their understanding of their role. Understanding the factors that lead MAs to develop a negative interpretation of their role would be particularly relevant not only theoretically but also in practice to prevent the harmful influence of these factors on MAs (“interpreting”).

Finally, more attention might be paid to the role that professional associations play in influencing MAs’ perception of their occupation. This is because the extant literature suggests that, in some countries, although they do not regulate the MAs’ profession and grant qualifications, professional associations are central to creating a sense of community and promoting the MAs’ occupation (Goretzki et al., 2013; Schäffer et al., 2014). Further investigation of this topic would also enhance our knowledge regarding how professional associations can reduce the professional–organizational conflict that MAs often experience (Hiller et al., 2014; Shafer, 2002; Shafer et al., 2002).

Future research might also further investigate the inherent control paradox that characterizes the MA’s occupation (“becoming controlled”) and leads MAs to submit themselves to control procedures (e.g., as “producers of truthful knowledge” in Lambert and Pezet, 2011). In this regard, research should seek to determine whether and how digital technologies represent a new form of control that, while enhancing control procedures, limits MAs’ freedom and creativity. Finally, concerning the “becoming unequal” perspective, it would be interesting to investigate the factors that contribute to the disparities within the MAs’ occupation in terms of gender, race or ethnicity and to determine whether and how MAs experience and make sense of these inequalities (“interpreting”). In this regard, it is also worth investigating how universities, professional associations and policymakers negotiate challenges linked to inequality and foster inclusivity.

6.2. “Making sense” of “doing” the management accountants’ work

The “doing” perspective (Anteby et al., 2016) is the most frequently adopted theoretical lens through which MAs are explored. The questions of what MAs do and what skills they must develop to carry out their daily activities have attracted the attention of several scholars over time (e.g., Coad, 1999; Järvenpää, 2007; Oesterreich and Teuteberg, 2019). It is worth noting that this is an area in which the boundaries between the “doing,” “becoming,” “relating” (Anteby et al., 2016) and “making sense” (Gioia and Chittipeddi, 1991; Thomas et al., 1993) perspectives often blur. In fact, the literature has emphasized that MAs’ tasks (“doing tasks”) are shaped not only by the role that they are formally called on to fulfill but also by other organizational actors’ expectations (Lepistö and Ihantola, 2018; Rieg et al., 2023) – namely, the ways in which MAs “become socialized” (Anteby et al., 2016). In a similar vein, conflict and competition over tasks with competing groups (“doing jurisdiction”) as well as interactions and collaboration with managers and top management (“relating as collaborating”) appear to play a significant role in influencing what MAs do within organizations (Ahrens, 1997; Fourné et al., 2023; Vedd and Kouhy, 2005). In addition, MAs themselves tend to mold their work according to the ways in which they interpret their role and their aspirational goals (“making sense”) (Ahrens and Chapman, 2000; Goretzki and Messner, 2019; Morales, 2019; Morales and Lambert, 2013; Taylor and Scapens, 2016).

Against this backdrop, one area that requires particular attention concerns how MAs themselves understand artificial intelligence (AI) and its potential influence on their role (“scanning”). This is because it has been found that AI’s increasing influence on MAs’ work requires them to navigate different tasks and be fluid to remain important within organizations (Rautiainen et al., 2024). This issue is highly relevant given the literature’s contrasting findings regarding digital technologies’ effects on MAs’ occupation (Berlinski and Morales, 2024; Carlsson-Wall et al., 2022; Franke and Hiebl, 2023). Therefore, future research might devote particular attention to the potential “dark side” of digitalization, investigating how the use of AI might engender situations of anxiety, stress and lack of stimulation for MAs (“interpreting”), which are found to represent potential barriers to the digital transformation of the finance function (Firk et al., 2024). In this vein, another aspect that may warrant greater attention in the coming years is MAs’ potential disconnection from others and the solitude they may experience if digital technologies increasingly interact directly with managers, thereby relegating MAs to a more “behind-the-scenes” role. Research on these topics implies a greater focus on personal emotions (Amslem and Gendron, 2019; Bhattacharjee and Moreno, 2017; Repenning et al., 2022) that paves the way for fruitful interdisciplinary collaborations between researchers working in different yet complementary fields.

6.3. “Making sense” of “relating” to other occupations

The “relating” perspective is the less adopted one in explorations of MAs. Research on MAs’ attempts to build collaborative relationships has followed two main trajectories. Papers adopting the “relating as collaborating” filter illuminate MAs’ potential contribution to strategic and innovative processes within organizations (Ahrens, 1997; Erhart et al., 2017; Pasch, 2019). From this perspective, the establishment of strong collaborations between MAs and the other managers is understood as a condition for the facilitation of the making of strategic decisions or the adoption of management accounting innovations. The second trajectory of analysis entails contributions that, through the “relating as brokering” filter, have revealed the pivotal role that MAs can play in mediating among different interests, especially when targets need to be defined during the budgeting process (Hartmann and Maas, 2011; Mack and Goretzki, 2017; Wiegmann et al., 2024).

In light of the above, it becomes clear that studies on how MAs interact with other actors to coproduce expertise and authority—that is, “relating as coproducing” (Anteby et al., 2016)—are lacking. With reference to this, it would be of considerable interest to highlight the domains of potential coproduction, particularly in the areas of digitalization and sustainability. Regarding digitalization, research would benefit from the adoption of a socio-material analysis (Orlikowski and Scott, 2008) to disentangle how technology can influence the establishment of interactions between MAs and other organizational actors, such as IT managers, or external stakeholders, such as IT consultants. Such analyses should take into consideration how the coproduction of new knowledge, essentially driven by the adoption of new technologies, can influence MAs’ role or authority. Additionally, it is worth revealing the contradictions that may emerge from the collaborations that are necessary to establish technologies among different actors and criticisms that must be managed, drawing from studies that have already begun to emphasize digitalization’s potential to be a double-edged sword for MAs (van Slooten et al., 2024).

The adoption of a “relating as coproducing” perspective would be even more relevant to sustainability practices, given that the findings in this regard appear to be quite granular and inconsistent (Halari and Baric, 2023; Kurki and Järvenpää, 2024; Wenzig et al., 2023). New research opportunities arise from the exploration of sustainability as a stimulus for MAs to establish complementary relations with other actors, such as sustainability managers, in an attempt to coproduce new knowledge and expertise (“relating as coproducing”). The extant literature has frequently highlighted the necessity of intervention and collaboration with other actors and groups owing to the lack of legal requirements in producing management accounting information and the need to match different goals and expectations (Ezzamel and Burns, 2005; Mouritsen, 1996; Vaivio, 2004). When it comes to sustainability issues, this fact is exacerbated by the need to produce documents such as sustainability reports that require the production of information that is not directly managed by the management accounting department, and which often implies gathering information and engagement with different stakeholders.

Overall, an approach to studying MAs that adopt the “relating as coproducing” lens may be of particular importance in shedding light on how new practices and trends can shape MAs’ competencies and skills over time and on how collaborations with internal and external actors should be managed to establish a mutual transfer of knowledge from which MAs can benefit in their daily activities.

Finally, most studies notably focus on the internal relationships that MAs develop within organizations, devoting only scant attention to relationships with actors outside the organization (for an exception, see Janin, 2017). Rather, MAs are increasingly involved in meetings with external stakeholders, such as bank representatives, and thus, future studies should investigate how MAs make sense of their “external” accountability (“interpreting”). In this regard, the findings indicate that MAs engage with a variety of actors who influence the context of their work, often prompting—or even compelling—them to adopt a different façade in each interaction. However, limited attention has been paid to how MAs adjust their behaviors to fit the context in which they operate and the stakeholders with whom they engage (“scanning”). Such personalized engagements pose challenges for future research seeking to investigate the implications of the MA’s chameleon-like traits.

7. Concluding remarks

In recent years, researchers have become increasingly interested in the professional development of occupational groups whose knowledge and expertise are shaped by the organizational contexts in which they operate (Muzio et al., 2011; Noordegraaf, 2007; Suddaby and Viale, 2011). This interest is also evident in research on management accounting, which has recently focused on the study of MAs, a kaleidoscopic occupation (Goretzki and Strauss, 2017) whose characteristics often depend on the national and organizational context in which they operate.

With the aim of illuminating the intricacies of MAs’ realities, unravelling its complexity and opening up new research avenues (Healey et al., 2023; Post et al., 2020), we conducted a theory-led literature review (Breslin and Gatrell, 2023; Hiebl, 2023a; Hoon and Baluch, 2020) drawing on Anteby et al.’s (2016) framework to organize and interpret the extant findings. In particular, Anteby et al.’s (2016) lenses for exploring occupations—“becoming,” “doing” and “relating”—and their respective lens-filters represented a valuable theoretical foundation for reviewing and interpreting the extant literature on MAs. However, extant research on MAs has also demonstrated that such an occupation is not only the result of social construction processes (Anteby et al., 2016). More specifically, it emerges that the social constructions of the MAs’ occupation are both influenced by and, in turn, exert influence on individual sensemaking processes (Gioia and Chittipeddi, 1991; Thomas et al., 1993). In this regard, the “becoming”, “doing” and “relating” perspectives can be enriched by incorporating a “making sense” perspective which captures individual cognitive processes and deepen our understanding of how individual sensemaking both shapes and is shaped by the social constructions of occupations. In line with this, it should be emphasized that this meta-framework would be useful for further exploring not only MAs but also other occupations. On the one hand, the adoption of this meta-framework may offer novel insights into the exploration of other established staff functions—such as IT or HR—which, like MAs, are often engaged in negotiating their domains of influence vis-à-vis other organizational functions and in seeking legitimacy for their role within organizations. On the other hand, it may also help illuminate the challenges faced by nascent occupations—such as data scientists or sustainability managers—which frequently operate without clearly defined jurisdictional boundaries and still lack a consolidated professional identity (Goretzki et al., 2023).

This paper contributes to the extant literature on MAs by providing an in-depth analysis of the current state of research that can serve as a valuable resource for future investigations. Some recent papers reviewed the existing literature on MAs, focusing on specific aspects, such as MAs’ roles and identities (Wolf et al., 2020) or the digitalization of the management accounting function (Arkhipova et al., 2024; Nielsen, 2022), and their specific foci offer valuable insights into the abovementioned topics. This paper, by contrast, expands the perspective from which MAs are observed by offering an in-depth overview of the intricacies of the MAs’ occupation. In particular, the mutual influence among the “becoming,” “doing,” “relating” (Anteby et al., 2016) and “making sense” (Gioia and Chittipeddi, 1991; Thomas et al., 1993) analytical perspectives along with their different evolutions across contexts and over time represent a challenge for future research on MAs. Although our findings depend on the body of literature selected and the theoretical approach that we followed to analyze the data and interpret the results, this paper illustrates that opportunities for future research are abundant and that additional avenues on the intersection between the “becoming,” “doing,” “relating” and “making sense” perspectives might certainly be proposed.

Supplementary material

The supplementary material for this article can be found online.

Acknowledgements

The authors would like to thank the editor Lukas Goretzki and the two anonymous reviewers for the constructive review process.

Notes

For the purpose of this paper, we consider the terms “management accountants” and “controllers” to be synonymous.

The search, based on the criteria outlined in Section 3.1, was conducted on July 17, 2024, and later updated on January 9, 2025.