Nuclear power is being promoted by a segment of the environmental community as an acceptable energy source to fight man-made climate change because it does not emit greenhouse gases. Missing in the literature is a discussion and analysis of the impact of electricity deregulation on the ability of nuclear power to obtain the requisite debt and equity financing within deregulated electricity markets, and in turn, on the potential number of new nuclear power plants that could help fight global warming. The purpose of this paper is to provide timely and salient policy guidance for the efficient allocation of resources to reduce greenhouse gases based on a new model linking debt and equity financing with a change in power plant revenue risk.

A theoretical model is put forth that links the availability of debt and equity financing to the change in revenue risk created by electricity deregulation and then tests this model by performing a qualitative phenomenological analysis.

The analysis supports a conclusion that electricity deregulation has a negative effect on the ability to attract nuclear plant debt and equity financing. As such, nuclear power may not be a viable option to reduce greenhouse gases within deregulated markets.

This paper fills certain gaps in the literature by creating a theory-based model that links debt and equity financing with a change in power plant revenue risk, performing a qualitative phenomenological analysis that finds support for the negative relationship between electricity deregulation and an increase in power plant revenue risk and establishing that this increase in revenue risk affects some types of power plants such as nuclear power more than others.

1. Introduction

Carbon dioxide (CO2) has been identified as the largest contributor to global warming and the generation of electricity from nuclear power does not emit CO2 (Jaforullah and King, 2015; Penn, 2022; Tollefson, 2021; York and McGee, 2017). This has led to a renewed interest in nuclear power, and the governments of numerous countries including the USA have made international commitments to reduce CO2 emissions. The United Nation’s 26th Climate Change Conference of the Parties (COP26) codified nuclear power as an acceptable energy source for meeting these commitments (Almer and Winkler, 2017; Dimitrov, 2016; Tollefson, 2021). Following suit, the European Union (EU) announced its acceptance of nuclear power as a part of its strategy to meet its climate targets under the European Green Deal (CNN, 2022; Gillet, 2022).

Overlooked in these international agreements is the question of whether nuclear power will have the ability to attract the requisite debt and equity financing due to the changes in financial risk caused by electricity deregulation. To address this question, a theoretical model is put forth that links the availability of debt and equity financing to the change in revenue risk created by electricity deregulation and then tests this model by performing a qualitative phenomenological analysis that finds support for the model.

Power plant financing is critical because the construction of a nuclear power plant is a major cost commitment. Recent data on actual construction costs for a 1,000-MW nuclear power plant exceeds $10bn (King, 2017). Long-term debt financing is relied upon to pay for much of a power plant’s construction costs and 20-year financing terms are common (Harmon and Reynolds, 2003; IAEA, 2017; Joyner, 2013; Wealer et al., 2021). The quality of a power plant’s income stream, as viewed by both lenders and investors, depends on the projections of revenue and the perceptions of revenue risk. Lenders place great weight on the reliability of the projected income stream to repay the loans (Harmon and Reynolds, 2003; IAEA, 2014; IAEA, 2017), and equity investors place similar weight on the reliability of the projected income stream to provide a return on and return of equity (Brigham and Crum, 1977; Brigham and Ehrhardt, 2017; Grinyer, 1976).

This emphasis on income stream reliability helps to explain why all previous nuclear power plant financings (Kumar, 2021; World Nuclear Association, 2022), have relied on the monopoly status of the electric utility, with its legislatively anointed captive market, to provide an income stream sufficient to ensure debt coverage, provide a return on and of equity and cover nuclear-related risks to the satisfaction of the lenders and equity investors (Grantham, 2017; Harmon and Reynolds, 2003; IAEA, 2014; IAEA, 2017). But after the passage of legislation enacting electricity deregulation, electric utilities are not permitted to own regulated power plants in about two-thirds of the US market where electricity is no longer generated by monopolies and state regulators no longer ensure coverage of cost and revenue risks (Ward, 2011; White, 1996). Rather, electricity is generated and sold on a competitive basis by nonutility Independent Power Producers (IPPs), and in many states, end-use customers are now able to choose among competing electricity suppliers (Ward, 2011; White, 1996).

These competitive, deregulated markets are preferred by economists because they provide greater economic efficiencies than monopoly markets (Isser, 2003; Mankiw, 2015; McConnell et al., 2021; White, 1996). However, the policymakers at recent environmental forums such as COP26 have overlooked any consideration of the impact of this electricity deregulation on the ability of new nuclear plants to obtain the debt and equity financing needed for construction and, in turn, on the potential number of new nuclear power plants that could help fight global warming.

Dansky and Cudmore (2022) put forth that various federal actions to encourage competition in the electric generation market such as the Energy Policy Act of 1992 increase power plant revenue risk, and this makes it more difficult to attract the debt financing that is needed to construct a nuclear plant. This paper extends Dansky and Cudmore (2022) by establishing that these regulatory changes have also led to increased minimum required return on equity hurdle rates which increases the difficulty of attracting equity financing. It also extends Dansky and Cudmore (2022) by performing a qualitative phenomenology analysis that finds support for the negative relationship between electricity deregulation and revenue risk. As such, this paper fills certain gaps in the literature by:

establishing the existence of two theory-based causality pathways (debt and equity) by building on the financial and economic theories, constructs and principles of the Capital Asset Pricing Model, Efficient Market Hypothesis (EMH), Price Elasticity and the Law of Supply and Demand;

creating a theory-based model that links debt and equity financing with a change in power plant revenue risk;

establishing that there is a relationship between the deregulation of the electric industry and an increase in power plant revenue risk;

establishing that the increase in power plant revenue risk arising from electricity deregulation affects the ability of all power plants to attract debt and equity financing;

establishing that the deregulation of the electric industry affects revenue risk for certain types of power plants more than others, and consequently, affects the ability to attract debt and equity financing into the US nuclear power sector;

performing a qualitative phenomenological analysis that finds support for the negative relationship between electricity deregulation and an increase in power plant revenue risk; and

providing timely and salient policy guidance for the efficient allocation of resources to reduce greenhouse gases based on the new model linking debt and equity financing with a change in power plant revenue risk.

The scope of this paper is narrowly limited to the changes in revenue risk that are associated with the deregulation of electricity markets and its likely impact on debt and equity financing. There are numerous other risks that may influence the financing of a nuclear plant (Bemš et al., 2015; Fishman, 2018; Frye, 2008; Harmon and Reynolds, 2003; IAEA, 1997; IAEA, 2017; Wealer et al., 2021) and the theory-based model established in this paper (item #2 above) is also expected to be capable of analyzing these other financing risks. As such, it likely has wide academic and practical applications.

Moreover, while this paper focuses on the USA, it might apply to any country that deregulates its electricity markets. Electricity deregulation has been described as “one of the largest single industrial reorganizations in the history of the world” (Kwoka, 2008:165). Various academicians in multiple disciplines in numerous countries are studying electricity deregulation (Harrison and Welton, 2021; Hill, 2021; Lee et al., 2021; York and McGee, 2017), as well as developing technologies to reduce man-made climate change (Lopes et al., 2022; Mora et al., 2019; Muther et al., 2022; Wang et al., 2023). Resources are, by their nature, scarce (Barney, 1991; Peteraf, 1993) and there is value in knowing whether scarce resources should be directed to the further development of nuclear power or toward the development of other CO2-free technologies. This paper is intended to help inform that decision.

Finally, although there has been much theoretical and anecdotal discussion regarding the hypothesized linkage between electricity deregulation and financial risk over the past 30 years, this paper is the first to provide analytical support for the relationship between electricity deregulation and power plant revenue risk, and in turn, its impact on the availability of debt and equity financing. This paper does not take a position for or against any electric generation technology. Rather, it is the authors’ intent to simply point out the effect of the Smithian “invisible guiding hand” on market efficiency as it applies to the allocation of debt and equity within the electric generation sector.

2. Conceptual development

2.1 Economic and technical issues create financing implications

Nuclear power is not the only technology that could be used to reduce CO2. Each technology has its limitations (Cudmore, 2011; Muther et al., 2022; USSD, 2015; Wu et al., 2016) which help to maintain nuclear power’s status as an option to combat man-made climate change. However, imposed as a constraint on the economic and technical viability of nuclear power is that it has a high fixed capital cost (a high per kilowatt cost) and a low variable cost (a low per kilowatt-hour cost) (EIA, 2017; King, 2017). This characteristic has important financing implications. Capacity factors of 90+ percent represent the critical range of operation if nuclear power is to be cost-competitive. In other words, it is important to maintain a high quantity of output (Q) to keep average fixed costs (AFC) down. Thus, by operating at a high capacity factor (i.e. baseload unit), the high fixed costs of a nuclear plant can be allocated over a greater quantity of kilowatt-hours to minimize AFC.

Thus, it is economics and not physics that restrict nuclear plants from being dispatchable (IAEA, 2009), that is, the ability to increase and decrease output during the course of a day to meet changes in electric demand because this would lower Q and, in turn, increase AFC. A dispatchable nuclear plant would thus have insufficient cash flow to meet its debt and equity obligations.

This principle that nuclear plants cannot be dispatchable also applies to any of the proposed advanced nuclear plant designs that may provide inherently safer shutdown capability, as well as modular construction techniques to reduce construction schedules and costs (NuScale, 2023; Penn, 2022; Terra Power, 2023; WSJ, 2021). These new designs do not alter the high fixed cost/low variable cost relationship that is inherent to nuclear power, and it is this relationship, as noted above, that dictates whether a power plant can be economically operated as a dispatchable unit. The new designs do not alter the economic and technological issue at the center of our analysis with its important financing implication that nuclear plants are designed for, and require, baseload operation. The key point is that the findings of this paper are generalizable to both existing and advanced nuclear plant designs.

The conundrum, whether analyzing existing nuclear plant technology or a proposed advanced modular design, is that the price (P) of the generated power must remain low enough to ensure that the plant will be called on (dispatched) to sell a high quantity (Q) of the plant’s output, and thus be a baseload unit, yet the total revenue (TR = P × Q) must be large enough to cover all costs, including the plant’s high capital costs. This is a tight operating window and the nuclear plant must be able to satisfy this constraint over the plant’s life, despite changes in competing technologies, regulations and customer demand to attract financing (Fight, 2006; Yescombe, 2002). The debt and equity financiers of the nuclear plant seek to have this operating risk minimized (Fight, 2006; Yescombe, 2002) because the tight operating window leaves little cushion to absorb the effects of the long-term revenue risks as discussed in the next section.

Before deregulation, nuclear plant owners were able to eliminate this dispatch risk by designating each nuclear plant as “must run.” Today, under deregulation, this ability no longer exists because the dispatch sequence is determined by an independent system operator (ISO) and not by the owner of the power plant (FERC, 1999; FERC, 2023; Isser, 2003). An ISO is an independent regional organization that oversees the operation of the electric transmission network and manages the wholesale electric market. The creation of ISOs was mandated by Federal Energy Regulatory Commission (FERC) Order 2000 to further increase competition in electricity markets (FERC, 1999; FERC, 2023; Isser, 2003).

2.2 Price and output quantity risks

Lenders and equity investors have concerns about long-term price certainty for all types of power plants, not just nuclear. The concern is that the power plant will remain capable over the long term of selling its output at a price that is high enough to cover its costs. Adding to this concern is the possible emergence of any new, competing technology that can sell electricity at a lower price. The ISO will sequence the new technology to run each day ahead of the older technology. When this occurs, the new technology will push the older plant “up the dispatch curve” which will result in a shortfall of total revenue for the older technology and affect its ability to make payments to lenders and investors (Harmon and Reynolds, 2003; IAEA, 2014; IAEA, 2017).

Before deregulation, power plant owners were able to eliminate this long-term price risk based on US Supreme Court decisions such as Smyth v. Ames and Hope Natural Gas v. Federal Power Commission which established the “used and useful” doctrine for regulated monopoly utilities (Brown, 1944; Cabot, 1929; Pechman, 1993). Under this doctrine, once a power plant is deemed to be used and useful by the appropriate regulatory body, then the prudently incurred costs, including the plant’s fixed capital and the variable fuel costs, plus a reasonable rate of return, continue to be included in the electric rates charged to customers (Brown, 1944; Cabot, 1929; Pechman, 1993). Today, under deregulation, this ability no longer exists.

Another financing concern is price volatility. Each power plant within an ISO region competes with each other based on price. Daily prices are submitted by all power plants to the ISO, much like a limit order for the sale of stock on a stock exchange. The submitted electric prices are combined with the estimated daily market demand by the ISO to create a daily dispatch curve (a supply and demand curve that instructs the power plant owners when to turn their power plants on and off each day). The actual interaction of supply and demand, as it changes throughout the day, determines the actual wholesale prices received and the quantity of electricity sold that day by each power plant (Condemi et al., 2021; EIA, 2012; Ward, 2011; Zhongyang, 2022). The supply and demand curves for electricity are inelastic (Burke and Abayasekara, 2017; Deng and Oren, 2006; Fan and Hyndman, 2011; Wakashiro, 2019), and because of the continually changing interaction of supply and demand throughout the day, electricity prices determined by the market can be more volatile than regulated prices (Beecher and Kihm, 2016; Deng and Oren, 2006).

Before deregulation, power plant owners were able to eliminate this price volatility through the above-noted “used and useful” doctrine by which this volatility was smoothed out by the periodic rate-making process. Today, under deregulation, this process no longer exists.

Lenders and equity investors are also concerned about long-term output quantity certainty for all types of power plants. One concern is that a power plant is unable to generate power at full output for technical reasons, such as the historical need for many nuclear plants to plug leaking steam generator tubes, which reduces output (USNRC, 2023). Before deregulation, power plant owners were able to eliminate this long-term output quantity risk based again on the “used and useful” doctrine so long as the owner took reasonable efforts to repair the problem. (The prudently incurred repair costs would also get to be included in the rates charged to customers.) Today, under deregulation, this ability no longer exists.

Another long-term financing concern relating to output quantity is the ability of a power plant to maintain a market for its output. Before deregulation, all of a utility’s retail customers were captive – they could not switch electric providers no matter how high the regulators set the electric rates or how volatile. From the viewpoint of the lenders and investors, these captive customers provided the ultimate credit support for the utility’s construction plans. Today, under deregulation, this ability no longer exists, and electricity customers are now able to choose among competing electricity suppliers (Ward, 2011; White, 1996) much the same as customers choose among competing cell phone carriers.

2.3 Impact of deregulation on new power plants

As of 2024, the regulatory structure affecting the construction of new power plants is divided. In two-thirds of the US electricity market, the role of the regulated utility is now limited to distributing the electricity generated by nonregulated power plants (Ward, 2011; White, 1996). In the other one-third, regulated utilities can continue to own regulated electric power plants because some states never enacted the federal regulations to deregulate (Electric Choice, 2023; Flores-Espino et al., 2016) due to countervailing political pressure (Harrison and Welton, 2021). Consequently, nuclear power remains potentially financeable in the one-third of the US market that remains regulated.

On the contrary, the underlying basis that supported the financing of power plants has changed within two-thirds of the market, and it is this two-thirds of the market that is the focus of this paper. To summarize the discussion of subsections 2.1 and 2.2, the transition from cost-of-service regulation to deregulation is expected to result in the following changes to revenue risk:

an exposure to baseload output quantity uncertainty due to ISO dispatch rules;

an exposure to price competition from existing and future power plants located within the same ISO region;

an exposure to wholesale price volatility amplified by the inelasticities of the electricity supply and demand curves;

an exposure to output quantity uncertainty as retail customers, who are no longer captive, can switch electric suppliers; and

an exposure to future changes in law and regulation regarding the sale of electricity.

The above changes in risk exposure, individually or in combination, are thus hypothesized to increase power plant revenue risk as follows:

Electricity deregulation increases price risk.

Electricity deregulation increases output quantity risk.

2.4 The impact of risk on debt financing

Nonregulated electric power projects (referred to under the federal statutes as IPP projects which may include the unregulated affiliate of a regulated utility) use project financing (Buscaino et al., 2012; Jadidi et al., 2020; Kaminker, 2017; Mora et al., 2019). Project financing can be defined as a separable capital investment owned by a special purpose company in which the lenders look to the cash flow of the project to service their loans, as well as to provide the return on, and return of, the participants’ equity contributions (Buscaino et al., 2012; Klompjan and Wouters, 2002). The advantages of project financing are the availability of nontraditional loan sources, off-balance sheet treatment and the ability to prevent recourse to an affiliate in the event of a project’s default (Klompjan and Wouters, 2002). The disadvantage of project financing is that the lenders only look to the cash flow of the project to service the loan (Fight, 2006; Yescombe, 2002) which limits the pool of projects that can satisfy the loan covenants.

A primary task for lenders is to determine whether the project will generate enough cash flow to cover the debt and pay dividends to the equity participants, and this determination considers all project risks and uncertainties (Buscaino et al., 2012). There are a limited number of banks that provide project financing for power plants, and many of these banks typically work together in a consortium to dilute lending risk. Based on the risks of a power plant project, the lender(s) will establish a minimum debt coverage ratio (DCR) and then calculate whether the project’s cash flow meets this minimum criterion (Boykin and Hoesli, 1990; Klompjan and Wouters, 2002; Schaeffer, 1982). The DCR measures the cash flow available to pay current debt obligations and is calculated by taking net operating income and dividing it by total debt service (Brigham, 1979). If the project’s pro forma financial statements indicate that the minimum DCR will not be satisfied, the lender(s) will either impose a new, lower debt:equity (D:E) ratio that will satisfy the minimum DCR requirement or choose not to participate as a lender to the project. Therefore, revenue risk affects the willingness to lend.

Boykin and Hoesli (1990) provided the merits of using DCR as the basis for arriving at a project’s D:E ratio. By adjusting a project’s pro forma minimum DCR, lenders are able to account for a project’s risks, such as those associated with price and output quantity (Boykin and Hoesli, 1990; Klompjan and Wouters, 2002; Schaeffer, 1982). This is the primary tool used by lenders for this purpose (Boykin and Hoesli, 1990). Increasing the interest rate offered to a project is also a method used to account for risk, however, a change in the interest rate is captured in the calculation of the DCR (Brigham, 1979) and, thus, ultimately, the DCR remains the primary tool.

A lender’s insistence on imposing a higher minimum DCR, while holding the project’s capital costs, revenue and all other nondebt expenses constant will, by definition, lower the D:E ratio and thus require an increase in the quantity of equity (Brigham, 1979). This creates a problem for the equity investors: it reduces their return on equity (ROE).

The above financial concepts (DCR and D:E ratio) have been tested extensively and supported in academic literature for four decades (Brigham, 1979; Brigham and Ehrhardt, 2017). The financial literature appears to be devoid of any work that would suggest the contrary; that an increase in perceived risk would result in a decrease in the DCR, or that an increase in the DCR would result in an increase in the D:E ratio. Therefore, it is reasonable to assume that the directional relationships incorporated into this paper’s model will hold. This leads to the following hypotheses:

An increase in price risk reduces the willingness of lenders to provide debt financing for new electric power plants.

An increase in output quantity risk reduces the willingness of lenders to provide debt financing for new electric power plants.

2.5 The impact of risk on equity

The impact of risk on the valuation of equity has been well-studied in the literature. The seminal work by Akerlof (1970) relates risk and uncertainty to the valuation of a good or service. Seminal works by Sharpe (1964), Modigliani and Pogue (1974), Grinyer (1976) and Brigham and Crum (1977) all address the relationship between risk and return, develop a relationship called the Capital Asset Pricing Model (CAPM), suggest that assets with the same risk should have the same rate of return on equity and suggest that assets with higher risks should have higher returns (Brigham and Crum, 1977; Grinyer, 1976; Modigliani and Pogue, 1974; Sharpe, 1964). The CAPM has been around for at least five decades (Fama et al., 1969; Sharpe, 1964) and the concepts, principles and models developed in these earlier works remain relevant today (Brigham and Ehrhardt, 2017; Ross et al., 2016). The literature appears to be devoid of any research that would suggest that there is no relationship between risk and return or that the relationship operates directionally opposite. Therefore, it is reasonable to assume that the directional relationships incorporated into this paper’s model will hold.

In addition to the static analyses noted above, Fama et al. (1969) demonstrated that stock prices will adjust their valuation due to an adjustment of the imputed cost of equity upon the arrival of new risk information. For example, Pinches and Singleton (1978) showed that a change in a company’s bond rating due to a change in perceived risk will result in a change in the company’s stock price due to the capital markets processing the new information efficiently. More recently, Nukala and Prasada Rao (2021) performed a case study analysis of two hypothetical companies that reaffirmed the above-noted relationships in Fama et al. (1969) and Pinches and Singleton (1978). The above relationships in Fama et al. (1969) were also recently reaffirmed by Heinlein and Lepori (2022) in their analysis of stock valuations in the UK after the introduction of new macroeconomic information, and as such, lend further support for this paper’s model.

The above reference to market efficiency upon the arrival of new risk information emanates from the EMH, often attributed to Samuelson (1965) and Fama (1965). Asset values change over time to reflect new information, and new information takes many forms, such as a change in management or a new tariff (Fama, 1965). EMH assumes that market participants have processed all available information and have made valuation adjustments based on that information (Colin-Jaeger and Delcey, 2020). The concept has been tested extensively and supported in both academic and popular literature (Malkiel, 2003), and more recent academic literature continues to support the principle that “prices of financial assets fully reflect all available information” (Delcey and Sergi, 2019, p. 2). This includes information regarding the deregulation of electric markets and, as such, changes in revenue risk arising from deregulation will get reflected in the minimum required ROEs of electric projects.

In summation, this paper proposes that when the electric generation market transformed from regulation to deregulation, the new information was processed into new equity valuations due to a change in the imputed cost of equity. As such, increases in revenue risk would necessarily increase the minimum required ROE required by the equity investors of an electric power project in accordance with both EMH and CAPM. This leads to the following hypotheses:

An increase in price risk reduces the willingness of investors to provide equity financing for new electric power plants.

An increase in output quantity risk reduces the willingness of investors to provide equity financing for new electric power plants.

The change in revenue risk from deregulation is believed to be unique to each project as debt lenders and equity participants vary from project to project, and perceptions of risk vary. Moreover, as established earlier, baseload power projects such as nuclear should be affected by the exposure to output quantity risk greater than a technology that is designed to be dispatchable. While every electric generating project should face increased revenue risk from deregulation (see H1a and H1b), baseload projects with their high fixed cost/low variable cost structure that are vitally dependent on maintaining a high Q to ensure a low ATC, such as nuclear, face an even greater revenue risk. This leads to the following hypothesis:

Because revenue risk affects different types of electric power plants differently, the willingness of lenders and investors to provide debt and equity financing differs for different types of electric power plants.

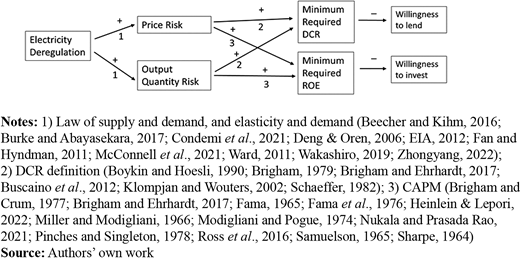

2.6 The proposed model

The proposed model (see Figure 1) operates as follows: Revenue is the product of price and output quantity, and as such, revenue risk can be divided into price risk and output quantity risk. Changes in market structure (e.g. deregulation) cause an increase in electricity price risk and/or electric output quantity risk. An increase in price risk and/or output quantity risk as perceived by the project’s lenders increases the minimum DCR that is imposed on the project by the debt lenders, and in turn, this causes a decrease in the project’s D:E ratio. As noted in Section 1, the model establishes two pathways; this is the model’s debt pathway.

Concurrently, an increase in price risk and/or output quantity risk as perceived by the project’s equity participants increases the minimum ROE hurdle rate that is imposed on the project by its equity participants. This is the model’s equity pathway.

As depicted in the model, the change in perceived revenue risk is accounted for, from the lender’s perspective, by the change in the DCR, and from the equity perspective, by the change in the minimum required ROE. The quantity of revenue is not a variable in the analysis; it is held constant as our concern is limited to the changes in revenue risk.

3. Methodology

There are only about 20 banks in the world that provide financing for power plants (Yescombe, 2002) and there are only three firms in the USA that provide electric utility bond ratings: Standard and Poor, Fitch, and Moody’s. Because of the complex and very specific nature of power plant financing, it is necessary that the data be collected from those finance executives who have prior experience with the financing of electric generation projects, are familiar with electricity deregulation and are familiar with those financing risks that are specific to the electric industry so as to reduce sampling error (Bansal, 2017). Moreover, to maintain data independence, respondents are limited to only one per company, given that coworkers in power plant financings work closely together in a small team (with shared decision-making). To do otherwise would be to potentially reduce data independence (Frost, 2019).

This suggests that the study is unlikely to be able to survey a statistically significant number of respondents having the prescribed qualifications. Per Creswell (2007), a qualitative approach may then be more suitable for the problem being studied, and there is ample precedent in economics and finance research for the use of qualitative methods. For example, see Starr (2014) for a survey of the growing use of qualitative methods in economics, and see Baker et al. (2008), Crawford (2012) and London et al. (2006) for specific applications.

A phenomenological approach is adopted as the best fit for this study (Allemang et al., 2021; Creswell, 2007; Giorgi, 2006, 2008, 2010; Moran, 2018; van Manen and van Manen, 2021). There is certainly the occurrence of a phenomenon – the passage of various legislation that deregulated the electric industry such as the Energy Policy Act of 1992. The lenders and investors within the electric power industry lived through and consciously experienced the impacts of deregulation on electric power generation.

Ten interviews were conducted which satisfied the minimum sample size criteria (Bougie and Sekaran, 2020; Creswell, 2007; Giorgi, 2008; Morgan, 2011). Four of the interviewees were previously known to the researchers from involvement in various regulatory proceedings and power plant financings. The remainder were obtained by referral (snowball sampling). Snowball sampling is commonly used in qualitative research and is “a recognized and viable method of recruiting study participants” (Leighton et al., 2021, p. 37). This method can create sampling bias that could impact the application of study results to larger populations (Leighton et al., 2021), but arguably, this concern is not warranted here given the small population of banks that provide power plant financing. Moreover, this analysis possesses high ecological validity because it investigates actual practices and conditions in the electric generating industry in response to actual changes in regulations. Ecological validity acts to increase external validity (Bornstein, 1999; Studebaker et al., 2002).

The interviews took place between June 13, 2022, and August 1, 2023. Eight of the interviews were conducted via telephone, and two made use of video conferencing. The interviewees were asked seven specific open-ended questions which allowed them to provide as much insight as they wished. Less structured approaches such as this enable the researcher to focus on the particular phenomenon being studied, rather than on the comparability of data across individuals (Maxwell, 2013).

As a final comment for this Section 3, the proposed area of research is focused on the relationships between deregulation and price risk, and deregulation and output quantity risk. No research is proposed for the other causal relationships within the model. These other relationships, as discussed in subsections 2.4 and 2.5, have already been well-researched and well-established over the past four decades. It is this paper’s findings regarding the relationships between deregulation and price risk, and deregulation and output quantity risk, that make new, unique and substantive contributions. In addition, it is the application of these new findings to the existing, well-established relationships that make additional new, unique and substantive contributions.

4. Findings and data analysis results

The ten people interviewed demonstrated extensive experience with the financing of electric generating projects and comfortably satisfied the minimum requirements described in the previous section (i.e. prior experience with the financing of electric generation projects, familiarity with electricity deregulation and familiarity with the financing risks specific to the electric industry). The experience of these interviewees ranged from 15 to 40+ years (see Table 1) with the average being greater than 30 years.

Six of the interviewees worked in the electricity industry both before and after the passage of the Energy Policy Act of 1992 and thus experienced the transition from regulation to deregulation. The remaining four interviewees had extensive experience working postderegulation on both regulated utility and nonregulated IPP financings, which afforded exposure to, and experience with, the differences between regulated and deregulated frameworks. Seven of the interviewees worked as investment bankers serving the electricity industry and three worked as consultants to the investment banks that serve the electricity industry. The three consultants also had prior experience working at one or more state and/or federal regulatory agencies that were charged with enacting the deregulation statutes. Five of the ten interviewees had experience with both lending and equity investing. Thus, all ten of the interviewees, individually and together, met the requirements of the analysis outlined in Section 3 as well as having significant subject matter experience, which all led to increased analysis validity.

4.1 Recurring themes

Each interviewee pointed to one or more phenomenological lived experiences to support the increase in revenue risk arising from the deregulation of the electricity market. There was a substantial overlap in their responses as is evident in the thematic summaries that follow. As a group, they addressed the revenue risk categories identified by the researcher in subsection 2.3.

Several themes emerged during the coding process that appeared in every interview. It is noteworthy that nothing was said in an interview that countered the lived experiences of other interviewees or that affected reaching saturation. In that regard, the phenomenological data analysis proceeded straightforwardly, and saturation was reached early in the interview process. Despite saturation being reached, and additional interviews providing repetition of the themes, the interview process continued until all ten interviews were conducted.

The following themes emerged and were universally supported by all the interviewees:

The change from cost-of-service regulation to deregulation affected the revenue stream of power plants.

This change increased revenue (price and output quantity) uncertainty.

This uncertainty increased price and output quantity risk.

Lenders and equity investors made changes in response to the increase in uncertainty and risk.

4.1.1 Theme #1: The change to deregulation affected the revenue stream.

Emerging from the coding process is that each of the interviewees opined that the change from cost-of-service regulation to deregulation affected the revenue stream of a power plant. Interviewees F, G, K, P and S (interviewees are not identified by name but by a single letter) each made specific statements regarding deregulation’s removal of the revenue guarantees associated with a power plant’s capital cost that were an integral part of cost-of-service regulation, and R mentioned the lack of these guarantees on both capital and variable costs. As an illustration, fuel costs are variable costs that were treated as a cost pass-through to the ratepayers under cost-of-service regulation (i.e. added to the price of the electricity as revenue), but under deregulation, the power plant owners assume all fuel cost risk.

Interviewees M and R both noted the change in price volatility that stems from the switch from regulated average cost pricing to deregulated marginal cost pricing, which can be evidenced in the ISO bidding systems because the clearing prices (the price of the highest bid power plant being dispatched at that moment) are designed to reflect marginal costs. This change to marginal cost pricing affects both capacity (kW) and energy (kWh) prices, and F, G, H, P and S all noted how market signals in the deregulated ISO bidding systems are now all short-term (such as every 15 min for the kWh energy component) and reflect short term supply and demand inelasticities whereas under cost-of-service regulation the kWh energy prices were typically established annually during rate case hearings. F noted how the bidding system set up by one ISO does not allow capacity (kW) prices to be bid separately and distinct from energy (kWh) prices but must be incorporated into a single daily energy price. R noted how deregulation led to more competition which fueled “the juices of capitalism” and led to lower prices for electricity. Lower electricity prices from competition were also discussed by B, C, F, G, H and S. In summary, all of the interviewees stated at least one way in which deregulation changed the revenue stream for power plants and none of the interviewees stated anything to the contrary.

4.1.2 Theme #2: Increase in uncertainty.

The coding process showed that each of the interviewees made at least one statement that the change from regulation to deregulation increased revenue (price and output quantity) uncertainty. Some of this uncertainty comes from the removal of cost-of-service regulatory set prices which was noted by P, F, G and R. Also, F, G, H, P and S all mentioned that market signals in the IOS bidding systems are now short-term (as discussed in subsection 4.1.1), thus adding uncertainty to any projection of long-term electricity prices used to secure debt and equity financing. M noted that the process of bidding, in and of itself, adds uncertainty to the revenue stream because a power plant never knows from day to day which bids, theirs and those of its competitors, will be accepted, nor do they ever know the relationship of their bid to others. H and P both noted that output quantity is a function of bid prices, and, similar to the preceding statement by M, power plant operators are blind to the prices bid by individual competitors which creates uncertainty. P notes that the power plant operator can regain some control over the output quantity by bidding a very low price to the ISO to ensure baseload operation “but loses all price certainty in doing so.” This is due to the tradeoff between price and quantity in the daily bids made by the power plant operators to the ISO. At the other end of the spectrum, a power plant operator can seek price certainty but in doing so loses all quantity certainty because that price may be too high in a competitive market to provide the needed quantity of hours of generation.

Interviewee B noted that under deregulation the introduction of new, competing technology adds uncertainty compared to cost-of-service regulation where inefficient plants were able to operate so long as the plant was deemed “used and useful.” K noted that there is greater uncertainty under deregulation for those power plants, such as coal and natural gas, that now have to maintain a long-term “spark spread” between revenue and fuel costs to pay for the plant’s fixed capital costs.

Providing more support for this increase in uncertainty, a majority of the interviewees (B, C, G, H, K and S) point to the efforts of some IPPs to sell all or a portion of their electric output via long-term contracts directly to large, credit-worthy industrial companies or sell directly via long-term contracts to regulated utilities that are looking to add renewable energy (specifically wind and solar) into their generation mix pursuant to regulatory directives. This approach bypasses the uncertainty of the ISO bidding systems but the opportunities for this approach are limited. Also, when these long-term contracts are entered into pursuant to a regulatory directive, S noted that the regulatory “stamp of approval” can add additional long-term certainty compared to the ISO bidding systems.

In summary, all the interviewees stated at least one way in which the change from regulation to deregulation increased revenue (price and output quantity) uncertainty. In addition, none of the interviewees stated anything to the contrary.

4.1.3 Theme #3: Increase in risk.

The coding process showed that it was universally supported by the interviewees that the change from cost-of-service regulation to deregulation increased revenue (price and output quantity) risk. As noted by F, “without used-and-useful, risk goes up”. B noted that the “risk profile changed for the entire industry”, and H, K, P and S all noted that without cost-of-service regulation significant risks shifted from the utility’s ratepayers to the investors. B and C noted that the increase in risk was evidenced by the across-the-board downgrading of utility bond ratings by the rating agencies after deregulation. B noted that some lenders changed their practices, in response to the increase in risk after deregulation, to only provide financing for projects that have established a multi-year operating history and by doing so, “reduce the risk profile.” In addition, B noted that the lenders now needed to consider “more variables in their loan analyses” than before, and this increase in complication added to the lenders’ risks.

Additional support for the increase in revenue risk was that numerous utilities sold off their generation assets, as discussed by B, K, R and S. According to R, “numerous utilities exited the [electric generation] business because they didn’t have the risk appetite” that came with deregulation. A first-hand account of this selling-off of generating assets was provided by K who, in addition to being an investment banker, also sits on the Board of Directors of an electric utility that sold off its generating assets in response to deregulation.

Another first-hand account comes from S who provided expert testimony before the New York Public Service Commission (NYPSC) in regard to multiple utilities in New York State auctioning off their nuclear power plant assets because of the change in revenue risk being shifted from the utility’s ratepayers to the utilities’ stockholders. S believes that the testimonies of multiple parties in NYPSC Case 98-E-0405 and Case 0l-E-0011 strongly suggest that deregulation increased revenue risk, and points to the difference in the two auction bid prices received from the winning bidder for two of the nuclear plants. One bid reflected future electricity sales into the deregulated ISO bidding system and the other bid reflected future electricity sales pursuant to a long-term power purchase agreement (PPA) to be made with the multiple utilities that sold the nuclear units. The PPA provided that the two nuclear plants would run as baseload units for 10 years, thus eliminating output quantity risk during that period. In addition, the PPA also provided that the output would be sold at a fixed price during those 10 years, thus reducing price risk. It is important to note that the fixed price for electricity over the 10-year period was neither higher nor lower than the price projection made by the NYPSC and, as such, only served to reduce price risk. Therefore, the reduction of revenue risk by incorporating a PPA into their bid (while all else was held constant in the two bids) resulted in a higher bid price. This is fully consistent with the discussion in Section 2 and fully supportive of the proposed model. That is, the reduction in risk resulted in a lower required ROE, and in turn, increased the value of the power plants.

In summary, all the interviewees stated at least one way in which the change from regulation to deregulation increased revenue (price and output quantity) risk. Moreover, none of the interviewees stated anything that suggested otherwise.

4.1.4 Theme #4: Lenders and equity investors made changes in response to the increase in risk.

Emerging from the coding process was that there was unanimous support by the interviewees that the power plant lenders and equity investors were impacted by the increase in revenue risk. Interviewees C, F, G and M all expressed that both lenders and equity investors experience more risk under deregulation. As noted by F, both lenders and equity investors were affected by the removal of regulated cost-of-service guarantees. K and M said that lenders responded to this risk by increasing interest rates and K noted that this negatively affected DCRs. K recounted his involvement with the financing of two similar power plants except that one project had a PPA and the other sold its output into the competitive wholesale market. K noted that the power plant with the PPA was perceived by his lending team as having less risk. The power plant that sold its output into the competitive wholesale market had stricter loan covenants imposed on it including a higher DCR. This is as predicted by the proposed model, i.e. higher perceived risk results in a higher DCR.

In addition, seven of the interviewees (B, C, G, H, K, R and S) recalled situations when lenders mandated lower D:E ratios to compensate for the increased risk, again as predicted by the proposed model. Another two interviewees (M and P) stated that they believed this practice did occur but couldn’t recall specific instances where they witnessed this behavior by the banks. R also said that the lenders reacted to the increase in risk by cutting back on the number of loans, and these loans often were of a shorter term. While the shorter term reduced risk to the lenders, it negatively impacted the debt coverage ability of the projects which led to a lower D:E ratio, again consistent with the proposed model.

On the equity side, C, K and R each noted that the equity investors sought higher minimum ROEs to compensate for the increased risk. Similarly, G stated that the higher minimum ROEs are being driven by the increase in uncertainty. This is exactly what is predicted by the proposed model.

Also on the equity side, S pointed to testimony that was given by a utility executive in NYPSC Case 0l-E-0011 that nuclear plants were designed for an earlier regulatory structure (i.e. where baseload operation was at the discretion of the utility) and not designed for the new deregulated structure where the nuclear plants are dispatched by the ISO. As a result, this testimony stated that nuclear power plants now require a higher ROE to account for this output quantity risk. Similar thoughts were echoed by C; that a nuclear plant in a deregulated environment would need a higher ROE than other types of power plants to account for output quantity risk and opined (based on his current job establishing credit ratings) that any company that chooses to pursue the development of a nuclear plant would have its debt downgraded due to the risk of being able to achieve this higher ROE. Once again, this is consistent with the proposed model.

In addition to many utilities selling off their generating assets due to the increased risk, which was discussed in subsection 4.1.3, R stated that numerous deregulated IPP companies also exited the power plant development business because they did not have the appetite for the increase in revenue risk. To put this in context, under the first wave of deregulation after the passage of the Public Utility Regulatory Policies Act of 1978, the deregulated IPP companies were legally entitled to a long-term power sales agreement with the local electric utility; typically 15 years. However, under the second wave of deregulation after the passage of the Energy Policy Act of 1992 (EPA of 1992), IPP companies were no longer legally entitled to these long-term contracts. The legislation replaced them with the creation of the ISO bidding systems. The change from the long-term contracts to the ISO bidding systems increased revenue risk, and as discussed by R, a number of firms exited the business because they could no longer earn a return on equity commensurate with the increased risk. C noted that the introduction of competition into the deregulated markets lowered electric prices which lowered IRRs, and this exacerbated the inability of some IPPs to earn a return on equity commensurate with the increased risk.

Finally, M believes that the response of equity investors to this increased risk has been the “drive to wind and solar.” Per M, wind and solar do not have fuel risk, are less complicated to construct and operate and have fewer moving parts, thus reducing some amount of risk to the equity investors. In a similar vein, G noted that from a lender’s perspective, the risk profiles of wind and solar are the “closest thing there is in the energy business to an annuity.”

To summarize this section, whether it is the “drive to wind and solar,” the exiting of some firms from the market, the selling off of generating assets or the reduction in D:E ratios to name a few, all the interviewees identified observable “fingerprints left behind at the scene” to support that electricity deregulation did increase revenue (price and output quantity) risk. Moreover, none of the interviewees stated anything that suggested otherwise.

4.2 Discussion and synthesis of the research

As discussed above, the relationship between electricity deregulation and revenue (price and quantity) risk is supported, and this support was found via a qualitative phenomenology study that interviewed ten people who had significant experience with the financing of electric generation projects, familiarity with electricity deregulation and familiarity with the financing risks that are specific to the electric industry. Specifically, as stated by the interviewees, electricity deregulation increased revenue risk due to several factors including an increase in price volatility arising from the ISO bidding systems, the creation of shorter-term price signals, an increase in long-term uncertainty, a decrease in quantity certainty, an increase in the exposure to technology change, the removal of regulated revenue guarantees and the shifting of risks from the utility’s ratepayers to the investors.

Evidence of the existence of this increase in price and quantity risk was provided by the study participants through several phenomenological lived experiences including the downgrading of utility bond ratings by the rating agencies right after the passage of the EPA of 1992, a change in lending practices regarding an asset’s operating experience, loan term length, interest rates, higher DCR and lower D:E ratios, the selling off of generating assets by utilities, a difference in power plant valuation with and without a long-term PPA, the exiting of multiple IPP companies from the industry due to an increase in higher minimum ROEs and the drive to less complicated technologies such as wind and solar. Some of these lived experiences directly relate to lenders and some of these lived experiences directly relate to equity owners, but most of the lived experiences listed above relate to both lenders and equity owners.

We can conclude that the lived experiences summarized in subsections 4.1.1 through 4.1.4, above, provide support for H1a and H1b, i.e. that electricity deregulation increased power plant revenue (price and output quantity) risk relative to cost-of-service regulation. This increase in risk is linked to an increase in the minimum required DCR via the existing, well-established financial relationships reviewed in subsection 2.4. In turn, this reduces the number of power plants that will qualify for a loan, and thus on the margin shrinks the pool of potential borrowing candidates. Therefore, with support found for H1a and H1b, the qualitative phenomenological study also provides support for hypotheses H2a and H2b through the existing, well-established financial relationships reviewed in subsection 2.4. That is, the increase in revenue (price and output quantity) risk reduces the willingness of lenders to provide debt financing for new electric power plants. At the same time, this increase in risk is linked to an increase in the minimum required ROE via the existing, well-established relationships reviewed in subsection 2.5. In turn, this reduces the number of power plants that will qualify for an equity investment, and thus on the margin shrinks the pool of potential investment candidates. Therefore, with support found for H1a and H1b, the qualitative phenomenological study also found support for H3a and H3b through the existing, well-established financial relationships reviewed in subsection 2.4. That is, the increase in revenue (price and output quantity) risk reduces the willingness of investors to provide equity financing for new electric power plants.

4.2.1 The willingness to provide financing differs for different types of electric power plants.

Also arising out of the qualitative study was the phenomenon that different types of power plants are affected by revenue risk differently. For example, it was supported that deregulation exposed all types of power plants to price volatility amplified by the inelasticities of the electricity supply and demand curves. However, it was also supported that baseload power plants, with their high fixed cost/low variable cost structure, are vitally dependent on maintaining a high Q to ensure a low ATC, and thus have a higher exposure to output quantity uncertainty than other types of power plants due to ISO dispatch rules. Thus, some types of plants are exposed to additional forms of revenue risk than others. By applying the above model’s relationship between deregulation and risk, this additional risk further increases the minimum required DCR and the minimum required ROE for those types of power plants. The existence of this additional risk provides support for H4, i.e. the willingness of debt and equity investors to provide financing is found to differ for different types of electric power plants. Because nuclear power is a baseload technology that has a higher exposure to output quantity uncertainty due to the ISO dispatch rules, it will be less attractive to investors vis-a-vis other technologies.

5. Contributions of the research, implications, limitations and recommendations

5.1 Contributions of the research and implications

This paper fills a gap in the literature by establishing the existence of two causality pathways (debt and equity) by building on the financial and economic theories, constructs and principles of the Capital Asset Pricing Model, EMH, Price Elasticity and the Law of Supply and Demand. Building on this, it fills another gap in the literature by creating a theory-based model that links the change in power plant revenue risk with the ability to secure debt and equity financing. The model can be modified to address other forms of risk beyond revenue risk. As such, it provides a framework that can be used by both academicians and business practitioners to relate risk and project-financed investment decisions.

This paper fills a gap in the literature by establishing that the deregulation of the electric industry increases power plant revenue risk which negatively affects the ability of all power plants to attract debt and equity financing. It also fills a gap in the literature by performing an analysis that provides support for this relationship, and it does so by making use of a technique, phenomenological analysis, that is less common in economics and finance.

The paper found that certain types of power plants such as baseload units are affected more than others, and as a result, it is more difficult for nuclear power to attract the requisite financing within deregulated electricity markets. This suggests that any reliance on nuclear power to reduce greenhouse gases will be limited to those jurisdictions that remain regulated. This implication applies to both the traditionally larger 1,000 MW projects and the proposed smaller modular projects in the 100–300 MW range; this because they both have a high fixed cost/low variable cost structure, which is vitally dependent on maintaining a high Q to ensure a low ATC.

This paper, therefore, fills a gap in the literature by providing timely and salient policy guidance for the efficient allocation of resources to reduce greenhouse gases based on a new model linking debt and equity financing with a change in power plant revenue risk. Electricity deregulation was instituted to reduce monopoly markets and increase economic efficiency through competition (Isser, 2003; White, 1996), and it has largely succeeded (Csereklyei and Stern, 2018; Fabrizio et al., 2007; GAO, 2002; Lei et al., 2017; Musco, 2017; Switzer and Straub, 2005). If electricity markets are to remain deregulated and continue to provide the benefits of competition, then the key policy implication of this paper is that scarce resources should be redirected toward other carbon-free options that have a higher likelihood of securing debt and equity financing.

5.2 Limitations and recommendations for future study

The scope of this paper was narrowly limited to the changes in revenue risk caused by the deregulation of the electricity industry that affects the availability of debt and equity financing. There are a multitude of other risks that may affect the financing of a power plant including construction costs, construction schedule, insurance, political risk, decommissioning and spent fuel storage. These risks can also be analyzed using the model developed herein, and this is recommended for future analysis.

Electricity deregulation has taken place in numerous countries around the globe, however, the regulations are country-specific. This paper was constrained to one country, the USA, to ensure data validity and not introduce data variability due to differing regulations. Further research could be carried out by looking at the effect of deregulation on revenue risk in other countries, such as Canada and the UK, which also have deregulated electric markets.

Declarations: The authors declare there are no conflicts of interest concerning the research, authorship and/or publication of this article. The authors also declare there are no sources of funding concerning the research, authorship and/or publication of this article. The research protocol was reviewed and approved by the Florida Institute of Technology IRB (Date: May 18, 2023; IRB Number: 23-072), and voluntary informed consent was provided by each survey participant.