This paper aims to investigate the relationship between circular economy (CE) investments and corporate controversies, focusing on how these investments affect a firm’s reputation and stakeholder relationships. By integrating CE practices such as energy efficiency, waste reduction and water reuse, companies can minimise their environmental impact and mitigate controversies that may harm their reputation.

The study uses a cross-sectional research design and ordinary least squares (OLS) regression to analyse data from 2,762 firms listed in the Morgan Stanley Capital International All-Country World Index index. It evaluates the influence of various CE practices on companies’ ESG-related controversy levels, using data on environmental investments and stakeholder perceptions.

The results indicate a significant negative relationship between investments in CE practices – particularly in CO2 management, waste reduction and water stress management – and corporate controversies. Firms that prioritise environmental sustainability through these investments will likely experience lower controversy, thereby enhancing their reputation and stakeholder trust.

This paper contributes to the expanding literature on CE practices by examining the under-researched area of how such investments affect stakeholder perceptions and corporate controversies. The findings offer practical implications for companies aiming to enhance their sustainability efforts and improve their corporate image, as well as for policymakers seeking to promote environmental responsibility within corporate governance.

1. Introduction

The increasing complexity of global sustainability challenges – such as climate disruption, water scarcity and resource depletion – has led to growing scrutiny of how corporations manage their environmental responsibilities. As firms are held accountable not only for financial outcomes but also for their social and ecological footprints, the integration of environmental, social and governance (ESG) principles into corporate strategies has become a defining feature of modern business (Albitar et al., 2020; Baldini et al., 2018). The stakeholder-driven nature of ESG performance underscores the need for organisations to adopt proactive and transparent sustainability practices that are both operationally effective and socially legitimate.

In this context, the adoption of circular economy (CE) practices – centered on resource efficiency, waste minimisation and closed-loop systems – has been positioned as a key enabler of sustainable transformation (Ghisellini et al., 2016; Kirchherr et al., 2017). CE initiatives such as carbon management, water recycling and pollution prevention are increasingly embedded within firms’ environmental strategies. Existing studies have extensively documented the efficiency-related and ecological outcomes of these practices, showing improvements in material productivity, energy use and reductions in emissions (Walker et al., 2021; Yin et al., 2023; Kirchherr et al., 2017). However, the literature has paid significantly less attention to the reputational and stakeholder-related implications of CE investments, particularly their capacity to prevent or mitigate ESG-related controversies.

This omission is not merely anecdotal but substantiated by several systematic reviews. For example, in their meta-analysis on CE performance outcomes, Yin et al. (2023) identify that while environmental and economic performance are frequently assessed, reputational risk and stakeholder perceptions remain underexamined dimensions. Similarly, Kirchherr et al. (2017), in their conceptual synthesis of over 100 CE definitions, highlight that most of the CE literature is framed through an environmental or operational lens, with minimal incorporation of legitimacy oriented constructs such as stakeholder trust or corporate controversy. The scholarly focus has therefore been skewed towards the technical and efficiency aspects of CE implementation, at the expense of understanding its potential reputational and institutional benefits.

Moreover, studies on ESG controversies have remained mainly disconnected from the CE discourse. Research in this area has predominantly focused on the financial consequences of controversies (Li et al., 2019; Friede et al., 2015), the role of corporate governance in preventing them (Brammer et al., 2012) or the effects of ESG disclosure and ratings (Dorfleitner et al., 2021). What is lacking is a systematic investigation into how specific environmental practices – particularly those rooted in CE logic – may act as preventive levers against controversy. This is a critical gap, especially given that ESG controversies often originate from failures in managing resource-intensive domains such as carbon emissions, hazardous waste and water use – areas where CE provides direct operational solutions.

In parallel, the corporate social responsibility (CSR) literature has emphasised the role of ethical responsibility, stakeholder engagement and transparency in enhancing firm legitimacy and minimising reputational risk (Carroll and Shabana, 2010; Jo and Harjoto, 2011). However, CSR is often conceptualised separately from the operational strategies embedded in CE, resulting in a theoretical and empirical disconnect. Few studies have integrated CSR and CE within a unified framework that explains how concrete environmental actions translate into improved stakeholder perceptions and reduced exposure to controversy (Todaro and Torelli, 2024). This fragmentation has been noted by Montabon et al. (2016), who call for integrated models that bridge symbolic and substantive aspects of sustainability, especially in addressing reputational vulnerabilities.

Further, although the natural resource-based view (NRBV) has been widely used to theorise the competitive advantages of environmental capabilities – such as pollution prevention and product stewardship (Hart, 1995; Hart and Dowell, 2011) – its application in explaining how CE capabilities mitigate ESG-related controversies remains limited. Recent work by Sehnem et al. (2022) and Alkaraan et al. (2024) explores how CE contributes to firm performance through dynamic capabilities. Yet, the link between these capabilities and their role in defusing stakeholder conflict or reputational crises remains empirically underexplored. This lack of integration between NRBV and the reputational literature further limits the theoretical tools available to explain how CE investments function not only as ecological strategies, but also as mechanisms of risk mitigation and stakeholder alignment.

Taken together, these observations reveal a significant blind spot in the literature: while CE practices are widely promoted as environmental best practices, their role in reducing ESG controversies and enhancing stakeholder legitimacy has not been systematically theorised or empirically validated. The few studies that do mention reputational benefits tend to rely on broad ESG ratings as proxies, rather than examining controversy-specific metrics or disaggregated environmental actions (Dorfleitner et al., 2021; Li et al., 2019). As a result, the literature fails to clarify whether and under what conditions, investments in circular practices shield firms from reputational harm or stakeholder backlash.

This study aims to fill this gap by developing and testing a conceptual framework that integrates NRBV, CE and CSR perspectives to explain how circular environmental practices mitigate ESG controversies. Unlike previous research that aggregates sustainability performance into composite scores, this study disaggregates CE actions into three critical domains – energy, waste and water – and analyses their distinct effects on controversy exposure. In doing so, it answers recent calls for more granular and theoretically integrated sustainability research (Montabon et al., 2016; Nirino et al., 2021) while contributing empirical evidence on how CE practices operate not only as environmental strategies but also as instruments of reputational resilience.

The remainder of this paper is structured as follows. The next section reviews the relevant literature and elaborates on the theoretical framework. This is followed by the development of the research hypotheses and the proposed conceptual model. The methodology section outlines the data set, variables and analytical strategy. Results are then presented and discussed in light of both theory and practice. The final section concludes by highlighting key implications for sustainability scholars, corporate managers and policymakers and outlines avenues for future research.

2. Literature review

2.1 Natural resource–based view as a key to CE and environmental, social and governance controversy mitigation

The Natural Resource–Based View (NRBV) offers a foundational lens for understanding how firms can turn environmental pressures into strategic opportunities, particularly when addressing ESG controversies through CE practices. Rooted in Hart (1995) premise that environmental capabilities constitute sources of competitive advantage, the NRBV has been extended by scholars who recognise the importance of valuing natural capital (Cairncross, 1992) and adopting systemic sustainability principles such as those in “The Natural Step” (Robert, 1995). These early frameworks anticipated the logic of industrial symbiosis later popularised by Frosch and Gallopoulos (1989), whose vision underpins CE’s emphasis on resource efficiency and waste minimisation (Schulte, 2013; Acerbi and Taisch, 2020). The NRBV’s Pollution Prevention pillar supports CE strategies to eliminate waste at the source through reverse logistics, safe material substitution (Willig, 1994) and closed-loop industrial platforms (Coppola et al., 2023; Sehnem et al., 2022). These practices help firms respond to regulatory and market pressures, thus lowering stakeholder controversies (Aragón-Correa and Sharma, 2003). Empirical studies confirm that CE implementation enhances resilience and transparency in manufacturing and supply chains (Mathiyazhagan et al., 2013; Dey et al., 2022; Mitra and Datta, 2014; Saha et al., 2022). Product stewardship extends NRBV principles across the lifecycle, emphasising the integration of sustainability into design, sourcing, use and end-of-life phases (Kirchherr et al., 2017; Bocken et al., 2016). Embedding stewardship practices such as modularity, recyclability and green chemistry (Clark et al., 2016) enables firms to mitigate risks linked to material scarcity and ethical sourcing while simultaneously enhancing legitimacy and trust among stakeholders (Montabon et al., 2016; Brammer and Pavelin, 2006; Alkaraan et al., 2024). Governance oversight, particularly board-level engagement in green innovation and the integration of stewardship principles into corporate performance metrics, further strengthen accountability and generate both operational and reputational benefits (Büyüközkan and Karabulut, 2018; Merli et al., 2018). The Sustainable Development pillar of NRBV, finally, emphasises balancing profit generation with ecological regeneration. CE technologies such as smart energy systems (Chan et al., 2016), advanced water-reuse schemes (Murray et al., 2017; Ruiz et al., 2020) and digital monitoring platforms (Bag et al., 2021; Kistoffersen et al., 2021) provide the means to translate this ambition into measurable results aligned with the sustainable development goals (SDGs). These efforts gain further traction through bottom-of-the-pyramid strategies (Prahalad and Hart, 2002), which expand CE’s scope into underserved markets and through collaborative value chains that accommodate both environmental and social equity goals (Ahi et al., 2016; Zhu, 2005). Integrated approaches have consistently been associated with reduced ESG controversies across sectors and regions (Yin et al., 2023; Nirino et al., 2021), confirming the strategic value of NRBV when operationalised through CE.

In addition to these theoretical foundations, recent work in the philosophy of management provides an essential normative layer to understanding sustainability and CE practices. Rendtorff (2019a) argues that the United Nations Sustainable Development Goals (SDGs) should be viewed not only as policy objectives but also as strategic and ethical drivers capable of mobilising firms, public institutions and civil society towards more just and responsible economic models. This interpretation positions sustainability as a transformative force that reshapes corporate governance and managerial decision-making. In his subsequent monograph, Rendtorff (2019b) further emphasises the centrality of ethical reasoning, stakeholder responsibility and intergenerational justice within managerial practice. By framing sustainability as a moral commitment rather than an operational add-on, his work reinforces the argument that CE practices contribute to legitimacy, trust and stable stakeholder relations. Integrating these philosophical insights into the NRBV–CE framework broadens the understanding of ESG controversy mitigation: environmental practices such as CO2 reduction, water efficiency and waste minimisation become both technical strategies and ethical obligations aligned with SDG-driven visions of sustainable development. This dual interpretation helps explain why CE initiatives grounded in ethical governance tend to strengthen reputational resilience across diverse institutional contexts.

2.2 Natural resource–based View as a strategic lens for CE implementation

While traditional sustainability programmes often remain confined to compliance checklists, NRBV repositions CE as a proactive and differentiating strategic capability. It invites firms to view environmental constraints as opportunities for resource innovation, particularly when CE practices are designed to meet the VRIN criteria (Hart and Milstein, 2003). Recent studies demonstrate how CE adoption – particularly product-service systems and circular design – yields cost savings, innovation potential and reputational gains simultaneously (Bocken et al., 2016; Geissdoerfer et al., 2020). Strategic complementarities between CE practices, such as energy optimisation and advanced recycling, yield nonlinear benefits for ESG ratings and stakeholder perceptions (Yang et al., 2019; Potting et al., 2017; Clark et al., 2016). The strategic coherence of CE–NRBV integration is particularly evident in sectors subject to public scrutiny, such as agriculture, fashion and energy-intensive manufacturing (Todaro and Torelli, 2024; Lo, 2013). Here, sustainable process design and social innovation converge, with SMEs often acting as agile testbeds for systemic circularity (Mitra and Datta, 2014; Dey et al., 2022). As Zhu et al. (2017) argue, the internalisation of environmental knowledge into business culture enables long-term adaptation and differentiation. Moreover, aligning CE practices with strategic foresight – such as scenario planning and supply risk mapping – helps firms anticipate ESG controversies before they materialise, thereby embedding resilience into their core value proposition (Montabon et al., 2016; Kamboj and Rahman, 2015).

2.3 Corporate social responsibility in controversial sectors

The full reputational impact of CE and NRBV investments becomes visible only when situated within robust CSR strategies. In controversial sectors – such as mining, fossil fuels and fast fashion – the interdependence between operational impact and societal trust is heightened, requiring a blend of transparency, co-governance and ethical commitment (Lindgreen et al., 2009; Barnett and Hoffman, 2008). CSR provides the relational infrastructure that links technical sustainability with legitimacy, particularly when CE initiatives are co-designed with affected stakeholders (Jo and Harjoto, 2011; Minor and Morgan, 2011).

Studies in green operations and supply chain management (Choi and Hwang, 2015; Wong et al., 2012; Zailani et al., 2012) show that CSR commitments – when backed by operational credibility diminish stakeholder scepticism and create buffers against ESG-washing accusations (Brammer and Pavelin, 2006; Dorfleitner et al., 2021). This is further supported in niche and emerging markets (EM), such as eco-fashion (Lee et al., 2012) and sustainable mobility (Lo, 2013), where consumer scrutiny is exceptionally high and trust must be actively built through executive accountability and incentives (Cai et al., 2011). Quality systems and social auditing frameworks (Kuei and Lu, 2013; Rost and Ehrmann, 2017) institutionalise these values, making CSR less about signalling and more about measurable impact.

Moreover, historical perspectives (Wilson and West, 1981; MacArthur, 2013) remind us that the evolution of CSR has always been intertwined with innovation in business models and governance. Contemporary frameworks – such as integrated reporting and multi-stakeholder accountability platforms (Prieto-Sandoval et al., 2018) – demonstrate how CSR can embed CE and NRBV into firms’ everyday decision-making. When this triadic integration is achieved, it not only mitigates controversies but also actively redefines the firm’s societal role and secures its social licence to operate.

3. Hypothesis development and conceptual model

While the NRBV, CSR and CE frameworks have each contributed significantly to our understanding of how sustainability practices influence firm performance and stakeholder legitimacy, existing research remains fragmented in its examination of how these perspectives intersect to explain the mitigation of ESG controversies. Prior studies tend to focus either on strategic environmental capabilities (Hart and Dowell, 2011), on stakeholder engagement and transparency mechanisms (Barnett and Salomon, 2012) or operational transitions towards circular resource flows (Kirchherr et al., 2017), often in isolation. However, the growing complexity of environmental and reputational risks necessitates integrative models that transcend single-theory approaches and provide a comprehensive understanding of how firms prevent controversies through coordinated strategic, operational and relational actions.

Recent contributions have emphasised the need for cross-framework syntheses that explain how concrete environmental initiatives – such as reductions in emissions, waste or water consumption – translate into reduced stakeholder conflict and reputational vulnerability (Dorfleitner et al., 2021; Nirino et al., 2021). Yet, there remains a limited empirical investigation into how NRBV-informed capabilities are operationalised through CE practices and socially legitimised through CSR engagement, particularly concerning a firm’s exposure to ESG-related controversies. While ESG scores are frequently used as proxies for sustainability performance, they aggregate disparate dimensions without sufficiently disentangling the specific levers through which firms avoid incidents such as pollution scandals, regulatory non-compliance or public backlash (Friede et al., 2015; Li et al., 2019).

Moreover, few studies have examined how resource-specific interventions – namely, in the energy, waste and water domains – act as distinct yet interconnected mechanisms for controversy mitigation. Although energy efficiency, waste reduction and water stewardship have individually been linked to improved environmental outcomes (Münch et al., 2022; Waniak-Michalak and Michalak, 2024), their role as integrated operational manifestations of a broader strategic-responsible-circular model remains underexplored. This theoretical gap is especially salient in high-impact industries, where controversies often originate from failures in precisely these areas.

To address this shortcoming, the present study develops and empirically tests a conceptual model that integrates NRBV, CE and CSR into a coherent framework of ESG controversy mitigation. By investigating the distinct effects of energy efficiency, waste management and water governance – both individually and as components of a systemic sustainability strategy – we aim to clarify the mechanisms through which environmental practices reduce reputational risk. In doing so, we respond to calls in the literature for greater theoretical integration and analytical granularity in ESG research (Montabon et al., 2016; Suchman, 1995), offering a multidimensional model that links sustainability capabilities, operational redesign and stakeholder alignment to reduced firm exposure to ESG controversies.

3.1 Energy efficiency and environmental, social and governance controversies

The integration of NRBV, CE and CSR underscores energy efficiency as a crucial domain where firms can develop capabilities to mitigate ESG controversies. However, most studies continue to subsume energy performance under broader ESG or environmental scores, limiting the analytical resolution required to understand its specific reputational implications (Friede et al., 2015; Dorfleitner et al., 2021). Although NRBV highlights the importance of pollution prevention (Hart and Milstein, 2003; Hart and Dowell, 2011), most research does not explicitly address energy efficiency as a direct lever for controversy mitigation. CE theory further supports the strategic importance of minimising energy throughput and fossil fuel reliance through systemic redesign (Kirchherr et al., 2017; Ghisellini et al., 2016), yet the reputational outcomes associated with these operational shifts remain underexplored. From a CSR standpoint, transparent communication of climate commitments and progress in energy management enhances perceived authenticity and reduces scepticism (Barnett and Salomon, 2012; Minor and Morgan, 2011), but studies rarely test how such disclosures interact with controversy dynamics.

The emerging literature indicates that firms lacking robust energy practices face heightened scrutiny and sanctions, particularly in sectors sensitive to emissions and air pollution (Li et al., 2019; Waniak-Michalak and Michalak, 2024). However, there is limited disaggregation of which energy interventions, such as CO2 management systems or greenhouse gas (GHG) reduction strategies, most effectively insulate firms from reputational harm (Nirino et al., 2021). This empirical gap motivates the following hypotheses:

Companies that adopt higher levels of energy efficiency are associated with fewer ESG controversies.

Companies with more substantial CO2 management initiatives report lower levels of ESG controversy.

Companies engaged in robust greenhouse gas mitigation efforts experience fewer incidents of controversy.

3.2 Waste reduction as an imperative of the CE– corporate social responsibility interface

Waste reduction occupies a central position within CE frameworks, which view waste not as inevitable but as a design flaw to be eliminated through circular strategies (Kirchherr et al., 2017; Ghisellini et al., 2016). However, few studies examine how these practices, beyond improving environmental outcomes, translate into lower reputational risk. As also highlighted for energy optimisation in terms of pollution prevention, the specific contribution of waste management to controversy mitigation has been rarely investigated in the literature (Hart and Milstein, 2003). The CSR literature adds a moral dimension, emphasising social expectations for responsible waste governance in communities affected by toxic dumping and landfill overflows (Brammer and Pavelin, 2006; Barnett and Hoffman, 2008).

Although evidence shows that poor waste handling can lead to litigation, reputational crises and financial loss (Li et al., 2019; Münch et al., 2022), there is a lack of systematic analysis linking distinct waste-reduction initiatives to ESG controversy outcomes. This absence is particularly significant in sectors with high exposure to environmental scrutiny. The current study addresses this gap by testing the effects of targeted practices – such as recycling systems, hazardous-waste treatment and pollution prevention – on reputational conflict. Therefore, we propose:

Companies that strengthen waste reduction efforts report fewer ESG controversies.

Companies that commit to pollution prevention and recycling exhibit lower controversy levels.

Companies that improve hazardous-waste treatment experience fewer reputational conflicts.

Companies investing in advanced waste-recycling technologies reduce their exposure to controversies.

3.3 Water management and the mitigation of environmental, social and governance controversies

Water resource management is increasingly recognised as a critical sustainability priority, yet its specific role in controversy mitigation remains under-theorised. Proactive water management is another dimension of NRBV’s pollution prevention and stakeholder legitimacy (Hart and Milstein, 2003; Aragón-Correa and Sharma, 2003). CE approaches further advocate closed-loop systems that reduce water withdrawals and mitigate contamination through reuse and treatment technologies (Kirchherr et al., 2017; Murray et al., 2017). Despite growing adoption of such practices, few empirical studies explore how they contribute to reputational resilience or reduce ESG controversies.

CSR scholarship links water governance to social legitimacy, particularly in communities where water access and quality are sensitive ethical concerns (Minor and Morgan, 2011; Carroll and Shabana, 2010). Reputational crises related to overextraction, pollution or infrastructure neglect have been widely reported (Li et al., 2019; Rost and Ehrmann, 2017), yet research rarely examines which water-specific strategies are most effective in preventing such crises. This study responds to this gap by disaggregating the reputational effects of wastewater treatment, water reuse, infrastructure investments and stress mitigation, leading to the following hypotheses:

Companies that prioritise water resource management are associated with fewer ESG controversies.

Companies with higher commitments to wastewater treatment technologies encounter reduced controversy.

Companies that implement water reuse practices experience lower reputational risks.

Companies improving water infrastructure and distribution minimise stakeholder conflicts.

Companies mitigating water stress are better insulated from controversies.

3.4 A Conceptual model for mitigating environmental, social and governance controversies

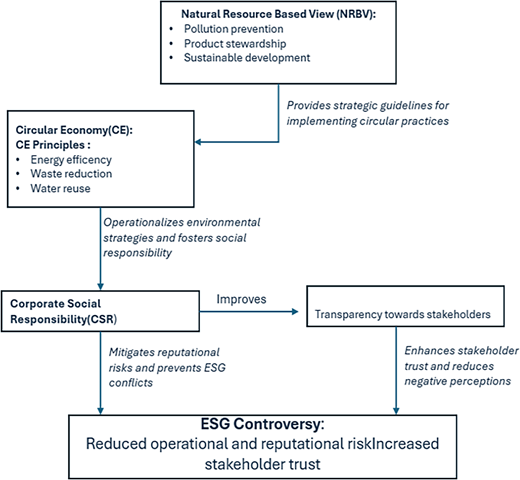

The conceptual model developed in this study proposes an integrated framework that combines the NRBV, the CE and CSR to explain how sustainability orientated practices can serve as mechanisms for mitigating ESG controversies. Rather than examining these theoretical perspectives in isolation, the model articulates a dynamic and complementary relationship among strategic intent, operational execution and stakeholder legitimacy, three pillars that jointly contribute to reputational resilience.

At the strategic level, CE practices rooted in NRBV create VRIN environmental capabilities (Hart, 1995; Hart and Milstein, 2003). The CE framework builds upon and operationalises the NRBV by transforming abstract environmental commitments into tangible practices that redesign production and consumption systems. CE emphasises circularity through energy efficiency, waste minimisation and water reuse, three domains that address the material sources of many ESG controversies (Kirchherr et al., 2017; Ghisellini et al., 2016). By closing resource loops and internalising environmental costs, firms reduce ecological harm while simultaneously demonstrating alignment with the regenerative principles increasingly demanded by policy frameworks and global sustainability agendas (Murray et al., 2017). Within the model, CSR serves as the relational axis, translating sustainability efforts into legitimacy and stakeholder trust (Carroll and Shabana, 2010; Barnett and Salomon, 2012). Within the model, CSR serves as the relational axis, translating sustainability efforts into legitimacy and stakeholder trust (Carroll and Shabana, 2010; Barnett and Salomon, 2012).

The interplay among these frameworks forms the basis of the proposed model: the NRBV establishes the strategic rationale for environmental capabilities; the CE framework implements those capabilities through systemic operational practices; and CSR legitimises these practices in the eyes of stakeholders. When integrated effectively, these dimensions reduce the firm’s exposure to ESG controversies by addressing both the root causes of environmental risk and the social perceptions that amplify reputational consequences (Suchman, 1995; Orlitzky et al., 2003).

What differentiates this model from prior literature is its emphasis on disaggregating the operational domains of energy, waste and water and linking them to specific reputational outcomes. Rather than relying on broad ESG scores or undifferentiated sustainability indicators, the model identifies these three areas as distinct, measurable levers that can independently and interactively reduce reputational vulnerability (Dorfleitner et al., 2021; Li et al., 2019). Further, it acknowledges the synergistic potential among these domains; for example, how investments in clean energy may reinforce the credibility of waste management efforts or how water stewardship can strengthen stakeholder confidence in broader sustainability initiatives.

By providing a theoretically grounded and empirically testable explanation of how firms can prevent ESG controversies, the model responds to recent calls for more integrated and granular approaches to sustainability research (Montabon et al., 2016; Nirino et al., 2021). It highlights that reputational resilience is not the by-product of generic environmental compliance but the outcome of coherent strategies, operational excellence and ethical engagement, all converging towards the same objective: building stakeholder trust and reducing exposure to controversy in complex and demanding institutional environments. Figure 1 provides a clear visual synthesis of the proposed framework, mapping the three theoretical pillars, their interactions and the pathways through which they collectively build reputational resilience.

4. Methodology

4.1 Research design

We used a cross-sectional research design using ordinary least squares (OLS) regression to examine the influence of CE practices and associated investments on firms’ controversial scores. The controversy score, defined in the Morgan Stanley Capital International (MSCI) ESG database, captures the extent and severity of negative attention a company receives regarding ESG issues. This metric is pivotal in assessing how stakeholder concerns about environmental and social performance translate into reputational risks and potential financial implications. By focusing on controversy scores, we aim to understand how CE practices can mitigate reputational risks and align firms’ operations with stakeholder expectations for sustainable development.

Our analysis encompasses 2,762 companies from the MSCI All-Country World Index (ACWI). This index is a globally recognised benchmark, encompassing large and mid-cap companies across 23 developed markets and 24 EM. These firms represent approximately 85% of the global investable equity universe, making the MSCI ACWI an ideal data set for investigating global corporate sustainability practices. The diversity of the sample enables a comprehensive analysis of how CE practices vary across industries, geographies and market maturity levels, thereby enhancing the generalisability of our findings.

The inclusion of MSCI ACWI-listed companies provides several advantages for this study. Bouslah et al. (2013) noted that firms within the MSCI ACWI are subject to heightened scrutiny from stakeholders, including media, investors and financial analysts. This level of visibility significantly reduces information asymmetry, ensuring that ESG-related disclosures and controversies are consistently monitored and reported.

We sourced data from MSCI ESG Research, a leading ESG and climate-related data provider, to measure CE practices and controversy scores. MSCI ESG Research uses rigorous methodologies to assess companies’ sustainability practices, offering detailed insights into their performance across key ESG dimensions. Using MSCI ESG data ensures that our study leverages a consistent, transparent and comprehensive data set that aligns with the reviewer’s request for methodological transparency.

Our selection of MSCI ESG data is justified by its alignment with the study’s objectives, as it offers detailed metrics closely tied to CE principles such as energy efficiency, waste management and water reuse initiatives. These metrics provide the necessary granularity to analyse the alignment of CE investments with firms’ sustainability goals. The MSCI controversy score also serves as a standardised and robust measure of a firm’s exposure to negative stakeholder attention, making it an ideal dependent variable for this analysis. The credibility of MSCI ESG data, recognised for its rigorous collection and evaluation processes, ensures high-quality and reliable inputs for empirical research. This standardised methodology minimises bias, enabling meaningful comparisons across firms and industries.

The data cleaning process was meticulously conducted to address potential concerns regarding data reliability. Firms with incomplete ESG metrics were removed and missing values for variables with less than 5% missingness were imputed using mean substitution. Further, extreme outliers, identified as values exceeding three standard deviations from the mean, were excluded to maintain the robustness and integrity of the results.

4.2 Variables

4.2.1 Dependent variable.

The study uses the MSCI ESG Controversy Score (CONTROVERSY_SCORE) as a comprehensive, standardised metric to evaluate company controversies related to ESG issues. This score assesses confirmed and alleged incidents, capturing their severity and impact on reputational and operational risks across industries and geographies. By incorporating diverse stakeholder perspectives, including input from NGOs, academic institutions, regulators and the media, the CONTROVERSY_SCORE provides a holistic view of a company’s ESG-related risks.

The score assesses the adverse impacts of environmental violations, labour rights abuses or unethical governance practices. These incidents may range from isolated events, such as oil spills or workplace accidents, to systemic issues, including repeated labour rights violations or regulatory failures. MSCI’s framework organises these controversies under ESG pillars. Each pillar addresses climate change, resource management, human rights, labour practices, consumer safety and corporate accountability.

Scored on a scale from 0 (no controversy) to 10 (severe controversies), the CONTROVERSY_SCORE quantifies reputational risks in a manner that aligns with CE principles.

It captures the impact of sustainability practices on environmental efficiency, social equity and transparency in governance, enabling a nuanced analysis of how CE strategies mitigate ESG controversies and enhance stakeholder trust.

4.2.2 Independent variables.

To evaluate companies’ efforts in supporting CE practices, we relied on standardised indicators from the MSCI ESG database. These metrics capture financial allocations and corporate initiatives in three critical areas. Carbon management is assessed through the CO2 management and GHG mitigation scores, which measure firms’ ability to reduce emissions via comprehensive policies, cleaner energy adoption, efficiency improvements and transparent disclosure (Hart, 1995; Kirchherr et al., 2017; Alkaraan et al., 2024; Sehnem et al., 2022). Waste management is evaluated using the Pollution Prevention, Hazardous Waste Treatment and Recycling Technology scores, reflecting companies’ capacity to minimise pollutants, safely treat hazardous waste and invest in advanced recycling technologies (Münch et al., 2022; Todaro and Torelli, 2024). Water management, a central component of CE, is captured through the Wastewater Treatment, Water Recycling, Water Infrastructure and Water Stress scores, which indicate firms’ ability to enhance resource stewardship, recycle and reuse water, strengthen infrastructure and mitigate scarcity through innovative technologies (Coppola et al., 2023; Bouslah et al., 2013). Detailed definitions of all metrics are provided in Appendix.

4.2.3 Control variables.

In addition to the primary variables, we incorporated control variables to account for contextual factors that may influence the relationship between CE practices and ESG controversies. These controls enhance the robustness of our analysis by isolating the effects of CE investments from other firm-specific characteristics and industry-wide dynamics.

First, we included industry classification using the Global Industry Classification Standard (GICS), represented in the study as GICS_IND. The GICS framework, introduced in 1999 by MSCI and Standard & Poor’s (S&P), categorises companies into 11 industrial sectors, ranging from energy and materials to information technology and consumer discretionary, providing a structured taxonomy to identify sector-specific CE adoption trends and ESG controversy exposure. For instance, resource-intensive sectors such as energy, materials and utilities are often subject to heightened scrutiny due to their significant environmental impacts, whereas sectors like Technology and Healthcare may face distinct challenges related to social and governance controversies (Sehnem et al., 2022; Kirchherr et al., 2017). Including GICS_IND allows us to control for such sectoral variations, ensuring that industry-specific factors do not skew our findings.

We also considered sales revenue (SALES) as a proxy for company size and resource availability. Firms with higher sales typically have more extensive financial resources, which can facilitate investments in CE initiatives and advanced sustainability practices. However, large-scale operations may also attract greater stakeholder scrutiny, potentially increasing the likelihood of ESG controversies. By including SALES as a control variable, we address the potential dual role of firm size in shaping the capacity for CE investment and exposure to ESG-related risks. Sales data were collected for the reference period to ensure consistency with other financial and ESG metrics used in the analysis (Bouslah et al., 2013; Todaro and Torelli, 2024).

Including these control variables aligns with established practices in sustainability research and directly addresses the reviewer’s concern about providing a comprehensive explanation of variable selection.

Table 1 summarises the variables used in the analytical model, highlighting their measurement type and respective data sources.

4.3 Descriptive statistics

Table 2 highlights the descriptive statistics for risk measures and explanatory and control variables. Regarding the ESG controversy score (CONTROVERSY_SCORE), the mean (median) controversy level is 6.73 (7). This highlights a significant controversy for companies in the MSCI ACWI index, suggesting the need to develop strategies and controls to manage controversial risks.

We can also capture detailed insights into the extent of CE practices across the sampled companies, highlighting the variability and scope of CE adoption within the corporate sector. The variables, such as Pollution Prevention (POLL_PREV), Waste Treatment (WASTE_TREATMENT), Preventive Recycling (PREV_RECYCLING), Water Treatment (WATER_TRTMT), Water Recycling (WATER_RECYCLING), Water Infrastructure (WATER_INFRA) and Water Stress Management (WATER_STRESS), are measured by their revenue percentage or scores, providing a quantitative snapshot of companies’ commitments to these practices.

The mean values indicate the average level of engagement in each CE aspect, with WATER_STRESS (2.41) and CO2_MGMT_SCORE (5.37) reflecting moderate engagement levels in water efficiency and CO2 management, respectively. Thus, while there is a conscious effort to incorporate CE principles, there is considerable room for improvement in adopting more profound sustainability strategies.

The median values, predominantly zero for several variables, suggest that many companies might not be engaged in specific CE practices or that such engagements must be more substantial to significantly impact their revenue streams or management scores. This discrepancy between mean and median values points to a skewed distribution, where a small number of firms with high engagement levels in CE practices may be elevating the mean. At the same time, the majority have minimal to no involvement.

Further, the standard deviations reveal a wide disparity in CE practice adoption across companies. For example, the standard deviation for WATER_STRESS (2.97) indicates diverse approaches to managing water efficiency, reflecting firms’ varying capacities and priorities in addressing water-related challenges.

The maximum values highlight outliers or best performers in each category, underscoring the potential for CE practices to boost a company’s revenue and management effectiveness. For instance, the maximum values for POLL_PREV (9.18) and WATER_RECYCLING (7.66) indicate that some companies have successfully integrated these CE practices into their business models, potentially serving as benchmarks for others in the sector.

The variability and disparities in engagement levels emphasise the need for tailored strategies that address the specific challenges and opportunities within various sectors and firms. This nuanced understanding of CE practices provides a foundation for further analysis of their impact on corporate sustainability and stakeholder perceptions.

Further, Table 3 (the correlation matrix) sheds light on the interdependencies among these CE practices. The correlations, especially those with significant levels (**), highlight how certain CE practices are more closely related than others, suggesting synergies that could be leveraged for more effective CE implementation and offering valuable perspectives for strategising more holistic, practical CE. For instance, the positive correlation between pollution prevention and the CO2 management score indicates that companies focusing on reducing emissions are likely to engage in broader pollution prevention efforts. However, the variance inflation factors (VIFs) presented, all below the threshold of 10, reassure the absence of multicollinearity and affirm the reliability of the regression models used in the study.

5. Analysis and discussion of results

5.1 Estimation procedure

To empirically test the conceptual model and the hypotheses derived from the NRBV–CE–CSR integration, we used an OLS regression approach with backward stepwise variable selection. This methodological strategy is consistent with the linear structure of our framework, which theorises direct associations between firm-level environmental practices – specifically in the domains of energy, waste and water – and ESG-related reputational controversies. OLS regression is particularly suitable given the continuous nature of the dependent variable (CONTROVERSY_SCORE), the presence of multiple independent variables and the objective of assessing the magnitude and significance of specific sustainability-related predictors across a broad sample of firms.

The decision to use backward stepwise selection was guided by the model’s multidimensional structure and the diversity of predictors from the MSCI ESG database. These predictors span distinct environmental performance categories that reflect different CE practices, alongside control variables such as industry affiliation and firm size. Rather than assuming equal importance across all variables, the backward stepwise procedure allows for a data-driven refinement of the model. Starting from a complete specification that includes all theoretically grounded variables, the method systematically removes those that do not meet statistical significance thresholds, based on p-values, until the most robust subset of predictors remains. This ensures that model parsimony does not come at the expense of theoretical coherence and that retained variables reflect both empirical relevance and conceptual justification.

The stepwise process enhances the interpretability of results by reducing the risk of multicollinearity and overfitting, which are common when working with high-dimensional, intercorrelated predictors. We used the adjusted R2 as the selection criterion throughout the procedure, following Ing and Lai (2011), to ensure that each model iteration improved explanatory power while avoiding inflation of variance due to irrelevant variables. This approach is especially appropriate for our research objective, which is not to evaluate the general influence of sustainability performance but rather to isolate which specific CE-orientated investments – such as CO2 emissions management, hazardous waste handling and water resource efficiency – most effectively mitigate ESG controversies.

Notably, the backward stepwise procedure aligns with the structure of the hypotheses, which are formulated at the level of individual CE domains. By retaining only those environmental variables that exhibit a statistically significant and consistent relationship with the outcome, the method enables a direct empirical validation of the differentiated impact theorised in the model. This represents an essential contribution to the literature, which often treats environmental performance as a composite or aggregated construct, without accounting for the heterogeneity of practices across sustainability domains.

To further ensure robustness, we assessed multicollinearity among independent variables by calculating VIF. All VIF values were below the conventional threshold of 10 (Neter et al., 1996), indicating no significant multicollinearity issues. Additionally, we applied robust standard errors to correct for potential heteroskedasticity and improve the reliability of coefficient estimates. Throughout the stepwise procedure, we monitored changes in adjusted R2 and significance levels to verify that model refinement enhanced explanatory performance without introducing specification bias.

5.2 Results and discussion

The results of the OLS regression analysis (Table 4) offer clear evidence of the relationship between CE practices and ESG controversies, as measured by the CONTROVERSY_SCORE. The findings indicate that targeted CE-related investments significantly reduce controversy levels, confirming the reputation-protective role of environmental practices. However, the adjusted R2 value of 22.6% reflects the inherent complexity of ESG controversies and the presence of additional unobserved drivers. Although this value may appear modest, it is fully aligned with expectations for socially constructed and multidimensional outcomes such as ESG controversies (Dorfleitner et al., 2021; Montabon et al., 2016). Importantly, recent empirical studies modelling ESG controversies or CE-related reputational outcomes report comparable or even lower explanatory power, reinforcing that modest R2 values are common when outcomes depend on stakeholder perceptions and contextual dynamics. For instance, Ma and Ma (2025) and Elamer et al. (2024) show that ESG controversies explain only a limited share of variance in firm value and performance due to the inherently reputational and perception-driven nature of these events, while Mazzucchelli et al. (2022) and Barbosa et al. (2025) similarly report moderate R 2 values when assessing the reputational effects of CE practices. These parallels confirm that the explanatory power observed in this study is entirely consistent with the empirical literature and appropriate for the complexity of the dependent variable.

ESG controversies arise from the interplay among organisational actions, regulatory pressures, stakeholder sensitivities and public perceptions. Accordingly, achieving high levels of variance explained is methodologically challenging, as many influential factors – including media exposure, crisis management capabilities and CSR communication intensity – are difficult to capture with quantitative indicators alone. Future research could also examine potential nonlinear relationships, such as diminishing marginal reputational returns to CE investments, by incorporating quadratic or interaction terms to determine whether additional environmental expenditures yield proportionally smaller gains in reputation.

The model was intentionally designed to be parsimonious, centreing on three core CE domains (energy, waste and water) and a limited set of control variables (industry classification and firm size). This enhances clarity and reduces construct redundancy, but it also implies that specific relevant drivers of controversies remain unaccounted for. Integrating additional organisational and communicative indicators – such as media sentiment, stakeholder discourse or exposure to public scrutiny – could substantially increase explanatory power and provide a more holistic understanding of controversy formation in future research.

Despite these limitations, the statistical significance and theoretical consistency of the main predictors demonstrate the model’s robustness. CO2 management, hazardous waste treatment and water stress mitigation all exhibit negative, significant associations with controversy scores, indicating that firms’ investments in these environmental practices contribute to reputational resilience. These findings align with the NRBV, which posits that proactive environmental strategies support the development of intangible resources such as legitimacy and stakeholder trust (Hart, 1995). The more substantial effects observed for CO2 and water practices suggest that stakeholders tend to reward highly visible efforts connected to global sustainability priorities. In contrast, less salient practices – such as hazardous waste treatment – may be undervalued unless adequately communicated.

Control variables further reinforce the interpretation of the results. Firms in resource-intensive industries face greater scrutiny and thus exhibit higher controversy scores. At the same time, larger companies tend to report fewer controversies, likely due to superior resource endowments and more advanced sustainability infrastructure. These patterns indicate that firm size enables more effective implementation and communication of CE practices, with important implications for small and medium-sized enterprises (SMEs). Given their resource constraints, SMEs may struggle to invest in high-impact CE technologies; future studies should therefore investigate modular, affordable or collaborative CE solutions that allow smaller firms to benefit from circular strategies despite limited financial and technological capacity.

In summary, the results confirm that CE practices play a significant role in reducing ESG controversies, even within the constraints of a parsimonious model and a modest adjusted R 2. The findings underscore that environmental investments in CO2 reduction, water efficiency and waste treatment not only enhance operational sustainability but also mitigate reputational risks in increasingly scrutinised institutional environments. The inclusion of longitudinal data, perception-based indicators and non-linear model specifications in future research would broaden the understanding of how circular investments translate into reputational outcomes over time.

6. Conclusions and implications

This study provides substantial empirical evidence on the relationship between CE practices and ESG controversies, shedding light on the strategic importance of sustainability initiatives in modern business environments. Specifically, the findings demonstrate a significant negative relationship between targeted CE investments in water and energy efficiency and corporate controversies. These results substantiate key theoretical frameworks, including the NRBV and extend the existing body of sustainability literature by emphasising the transformative role of CE practices in fostering corporate legitimacy and enhancing stakeholder trust (Hart, 1995; Hart and Dowell, 2011; Ghisellini et al., 2016). This study offers valuable insights into how firms can strategically position themselves as sustainability leaders by addressing a critical gap in understanding the interplay between CE practices and stakeholder perceptions.

The findings directly connect to central themes in CE literature, particularly the emphasis on resource efficiency and environmental stewardship as cornerstones of sustainable business models (Schulte, 2013; Kirchherr et al., 2017). The observed reductions in controversy levels attributable to robust CO2 management practices align with NRBV’s pollution prevention strategy, which posits that proactive measures to reduce emissions mitigate risks and create competitive advantages by addressing stakeholder concerns. This connection is especially salient in rising global awareness of climate change and regulatory pressures to reduce carbon footprints. Similarly, the significant impact of water stress management supports NRBV’s sustainable development strategy, underscoring the necessity of long-term resource stewardship as a foundational principle for achieving corporate resilience in resource-scarce environments. These findings also reinforce Yin et al. (2023) assertion that CE investments yield multidimensional benefits, enhancing environmental performance and strengthening corporate reputation.

This research also draws on CSR principles, focusing primarily on transparency and ethical governance to build stakeholder trust. The demonstrated role of CE practices in reducing controversies highlights the interplay between operational sustainability and corporate reputation, validating prior studies that emphasise the societal and environmental dimensions of CSR (Li et al., 2019). Aligning CE investments with stakeholder expectations illustrates how firms can simultaneously address reputational vulnerabilities and enhance organisational resilience. These findings validate that CE practices are instrumental in aligning corporate goals with societal demands, furthering the discourse on sustainable business strategies.

From a managerial perspective, this study emphasises integrating CE principles into strategic decision-making processes. CE investments emerge as compliance mechanisms and strategic tools for creating long-term value. The observed reductions in controversy levels demonstrate the tangible benefits of prioritising energy efficiency, water conservation and waste management. For instance, companies that excel in CO2 management by adopting renewable energy and optimising energy efficiency are firmly committed to addressing climate change and fostering stakeholder trust and loyalty. Similarly, firms that invest in advanced water recycling technologies and closed-loop systems are leaders in addressing global challenges such as water scarcity and in enhancing their market competitiveness and reputational capital.

Moreover, managers should also consider the broader operational benefits of CE investments by integrating social dimensions into their sustainability strategies. For example, initiatives such as developing equitable supply chains and engaging with local communities can further enhance a firm’s reputation and operational resilience while simultaneously contributing to social sustainability.

Managers should also consider the broader operational benefits of CE investments, including mitigating reputational risks, pre-emption of regulatory penalties and reducing operational disruptions. These strategies are particularly critical in high-impact manufacturing, energy and agriculture industries, where stakeholder scrutiny and regulatory pressures are more pronounced. By proactively addressing environmental challenges, firms can secure their positions in increasingly competitive and sustainability-conscious markets. The findings of this study serve as a clear call to action for corporate leaders to view CE practices not as peripheral initiatives but as integral components of business strategy and long-term value creation.

Importantly, firms of different sizes may face various challenges in adopting CE strategies. SMEs often lack the financial and technological resources available to large corporations. For these firms, managers could prioritise modular, low-cost CE initiatives – such as process optimisation, design for recycling, shared circular infrastructure or participation in industrial symbiosis networks – as viable entry points into circular transformation. Collaborative approaches, including partnerships with local institutions, supply chain actors or industry consortia, can help SMEs overcome resource constraints while still achieving meaningful environmental and reputational gains.

The policy implications of this research further underscore the importance of fostering an environment conducive to CE adoption. Policymakers play a crucial role in shaping the institutional framework that supports sustainable business practices. Financial incentives, such as tax credits, grants and subsidies, can significantly lower barriers to entry for firms investing in CE technologies. Regulatory frameworks that mandate or reward resource efficiency, emissions reductions and waste management can also drive widespread adoption of CE practices. For instance, policies that require mandatory reporting on CE initiatives or establish public recognition programmes for sustainability achievements can amplify the societal benefits of corporate environmental efforts. Additionally, fostering collaboration through public-private partnerships and knowledge-sharing platforms can catalyse innovation and accelerate the diffusion of CE practices across industries.

This research also sets the stage for future studies to explore the broader implications of CE practices. While this study focuses on controversy levels, subsequent enquiries could examine how reduced controversy influences long-term financial performance, innovation capacity and market valuation. For example, future research could investigate the cascading effects of CE investments on cost savings, supply chain resilience and employee engagement. Expanding the data set to include a more diverse range of industries, geographic regions and organisational contexts would provide richer insights into the generalisability of these findings. Moreover, examining the intersection of CE practices with other dimensions of corporate governance, such as diversity, equity and inclusion, could offer a more comprehensive understanding of sustainable business strategies.

Additionally, while the paper primarily focuses on the environmental aspects of CE, future research would also benefit from considering the potential role of social CE practices. This could include exploring how equitable supply chains and enhanced community engagement contribute to overall corporate sustainability, thereby broadening the appeal of the research and opening new avenues for investigation.

In conclusion, this study makes a significant contribution to the sustainability literature by demonstrating the pivotal role of CE practices in mitigating ESG controversies and enhancing corporate reputation. The findings bridge critical theoretical frameworks, including NRBV and CSR, while offering actionable insights for managers and policymakers. By aligning corporate strategies with sustainability objectives and leveraging supportive policy environments, firms can catalyse progress towards global environmental goals, foster stakeholder trust and secure long-term competitive advantages. This research underscores the dual role of CE investments as tools for ecological stewardship and drivers of corporate value, highlighting their essential contribution to a more sustainable and resilient future. Through continued efforts to integrate sustainability into core business strategies, firms and policymakers alike can advance the transition to a CE that benefits businesses, stakeholders and society.

7. Limits and future research

This study focuses on specific facets of the CE, particularly how environmental strategies impact firms at the centre of controversies. While this approach provides valuable insights, it captures only a narrow segment of the complex interactions and potential outcomes within the broader CE framework. By emphasising environmental strategies, this research overlooks the role of social-focused CE practices, which are increasingly recognised as critical in addressing controversies. Future studies should explore how socially orientated CE initiatives, such as equitable supply chain management or community-focused programmes, mitigate the negative reputational and operational impacts of controversies. These dimensions could provide a more comprehensive understanding of the CE’s potential to transform corporate sustainability and stakeholder relationships.

The data set used in this research comprises 2,762 companies representing a diverse range of global firms. While this diversity enhances the generalisability of some findings, the data set’s inherent limitations warrant attention. The selected firms are included in the MSCI ACWI, which focuses predominantly on large- and mid-cap companies. This scope excludes smaller firms and enterprises operating in niche markets or under-represented geographies, which may exhibit different dynamics regarding CE adoption and ESG controversies. Future research should expand the scope of analysis to include a more diverse set of firms, including small and emerging-market companies, to ensure that findings are truly representative of the broader business landscape. This expansion would yield findings more representative of the wider business environment, thereby enhancing the generalisability of conclusions. Moreover, comparative analyses with studies using alternative data sets could further validate the robustness of our findings and contextualise their external validity.

Another notable limitation is the study’s cross-sectional nature, which confines the analysis to a one-year observation period. While this approach provides a snapshot of CE practices and their relationship with ESG controversies, it does not capture the longitudinal dynamics of these relationships. A longer observation period or preferably a panel data approach, would allow for the examination of temporal changes in CE adoption and their long-term effects on stakeholder trust and financial performance. For instance, longitudinal studies could examine how sustained CE investments impact stakeholder trust and financial performance over time, providing deeper insights into the strategic value of sustainability practices. Moreover, while OLS regression is a robust method, its application in this study is subject to certain limitations. The assumption of linearity may not fully capture the potentially nonlinear relationship between CE investments and ESG controversies, where impacts may vary at different levels of investment. Future research should therefore explore potential nonlinear effects – such as diminishing marginal returns or threshold effects – by incorporating quadratic terms or interaction effects into regression models. Similarly, the assumption of homoscedasticity may not hold across firms of diverse sizes and sectors, suggesting the need for techniques like robust standard errors or weighted least squares in future research.

Despite acceptable VIF levels, the interrelated nature of CE metrics suggests potential multicollinearity, which can be addressed through approaches such as ridge regression or principal component analysis. The reliance on cross-sectional data limits the ability to capture temporal dynamics, warranting future exploration through panel data regression to account for changes over time and firm-specific effects. Additionally, unobserved confounders, such as governance quality or cultural factors, may introduce bias, underscoring the importance of instrumental variable techniques in enhancing causal inference. Addressing these methodological concerns through advanced econometric methods would improve the robustness of future analyses and further clarify the causal relationships between CE practices and ESG controversies.

Additionally, the reliance on MSCI ESG data, while offering consistency and reliability, introduces certain constraints. The MSCI data set prioritises large, publicly traded firms, which may skew findings towards companies with greater resources to implement and report CE practices. Smaller firms or those operating in EM may face unique challenges and opportunities that this data set does not adequately capture. Future research should consider integrating alternative data sources or combining MSCI data with other metrics to address this limitation. Incorporating data from multiple sources could also mitigate biases and provide a more nuanced understanding of how CE practices impact firms across diverse economic and regulatory contexts.

Future research should use panel data analysis to enhance the robustness of findings. This approach enables control for company-specific fixed effects and captures temporal variation. It would allow for a more detailed examination of how organisational characteristics, such as governance structures or market conditions, influence the effectiveness of CE practices in mitigating controversies. Moreover, panel data could facilitate the exploration of feedback loops, such as how improved reputations stemming from CE investments influence future strategic decisions.

Our analysis is based on a specific set of CE-related metrics, focusing on water, energy and waste. While this targeted approach has its merits, it limits the ability to consider the full spectrum of CE practices. Future analyses should incorporate additional metrics related to circular business models (e.g. product lifecycle management, reverse logistics and material innovation) to provide a more comprehensive picture of CE’s impact on corporate sustainability. Moreover, the cross-sectional nature of the data prevents us from capturing temporal dynamics and establishing robust causal relationships. This limitation is particularly significant in ESG controversies, where a longitudinal approach could reveal how CE practices evolve and influence stakeholder relationships over time. An additional critical point is the exclusion of small firms from our sample. This omission may lead to a distorted view of the business landscape, as small firms often exhibit behaviours and dynamics that differ from those of larger organisations. Consequently, the generalisability of the findings may be limited and the conclusions might not entirely reflect the situation where small firms play a significant role. Given the growing importance of SMEs in sustainability transitions, future studies should investigate modular, low-cost and collaborative CE strategies that allow resource-constrained firms to participate effectively in circular transformation.

In summary, while the study makes significant contributions to clarifying the role of CE practices in mitigating ESG controversies, we underscore the need for further research that expands the scope of analysis, adopts longitudinal designs and diversifies data sources. These methodological enhancements and broader data inclusions will be essential in constructing a more comprehensive and robust understanding of the multifaceted relationship between CE practices and corporate sustainability outcomes, thereby providing practical insights for firms and policymakers integrating sustainability into global business practices. To enhance clarity and usability, Table 5 provides a visual summary that aligns each limitation identified in the study with corresponding methodological directions for future research.