The objective of this paper is to propose a taxonomy of sustainability communication (SC) topics that provide digital content managers with a guide for setting a sustainability content agenda and for fostering stakeholder engagement mechanisms on environmental, social and economic issues that increasingly characterize conversations on social media of all stakeholder groups.

Taxonomy is a conceptual and qualitative way used to classify and represent the corporate sustainability (CS) domain of knowledge. The taxonomy categories of SC topics are both theoretically and empirically derived, combining an in-depth literature review with a thematic content analysis of 300 web pages of the corporate websites of the top ten sustainable brands selected in “The 2019 GlobeScan-SustainAbility Leaders Survey.”

The analysis of the results led to the construction of a hierarchical dictionary of tags that categorizes all sustainability topics based on a new, four-dimensional conceptual structure: planet, people, profit and governance. Each dimension is organized in four groups of sustainability themes, which, in turn, group multiple topics, considered the smallest communication unit to develop the SC content.

The taxonomy provides a concise and immediate conceptual framework on all those topics of broader interest, which, suitably modulated, can act as touch points with several groups of stakeholders. Drawn upon the best practices of thematic organization of SCs via the web, the taxonomy represents a guide for programming an editorial plan based on environmental, social, economic and governance issues from a sustainability content marketing perspective. The taxonomy of sustainability topics also finds application as a framework for a content intelligent system, providing a dictionary of tags that can be used for the indexing and retrieval of SC web content.

The study represents the first attempt at reaching a taxonomic organization of the sustainability aspects from a communicational perspective, supporting a new way of thinking and managing SC in the digital realm. Moreover, the results highlight, for the first time, that the Triple Bottom Line (TBL) theory, applied to corporate communications, lacks the governance aspect, which is essential to pursue sustainability consistently and effectively.

Introduction

Principles and concerns related to environmental sustainability, ethical and social impact and the critical future of the planet, in the last few years, are guiding the choices of businesses, consumers and other stakeholders. It is of increasing importance to adopt responsible behavioral models with a consequent propensity to sustainable consumption (Lim, 2017; Luchs and Miller, 2015). A new sustainability mindset is emerging (Nielsen, 2018; Piligrimienė et al., 2020) together with the so-called “mindful consumer” (Bahl et al., 2016; Shet et al., 2011), who actively uses the Internet and social media to obtain information on the sustainable characteristics of products and services (Onete et al., 2013).

Starting from this assumption, it is essential that companies adopt a strategic approach to sustainability, showing a consistent commitment in the dissemination of practices and content aimed at creating “shared value” between company and stakeholders—consumers in particular— taking advantage of the discussion on sustainability to trigger inclusive and participatory processes of stakeholder engagement. This, therefore, implies not only promoting a responsible approach to raw material consumption in favor of sustainable development but also starting a public discourse that leads to concrete social and civil actions (Reinermann et al., 2014).

The communication for sustainability that acts as a true agent of change needs to go beyond the reporting of sustainability performances, drawing on forms of content marketing (Conrad and Thompson, 2016; Leinaweaver, 2015; Villarino and Font, 2015) to promote a “new possible world” (Sarkar, 2012). For social media managers and content creators, the challenge arises due to the increase of opportunities for discussion on environmental, social and economic issues according to consumers' expectations (Cortado and Chalmeta, 2016). Moreover, highlighting the emotional essence of messages could help in establishing an empathic relationship with users and pushes them to be more inclined to share among them such content online (Araujo and Kollat, 2018).

However, sustainability and sustainable development represents a rather recent and articulated domain of knowledge, which, impacting many aspects of a company's work, requires an in-depth understanding of dimensions and aspects that can describe it. Thus, the objective of this paper is to explore and systematize the wide range of topics that corporate sustainability (CS) intercepts, proposing a taxonomy of sustainability communication (SC) topics. It must incorporate and categorize all aspects related to the characterizing dimensions of CS, that is, those relating to environmental, social and economic responsibility, into an organized structure.

The paper is structured as follows: First of all, the conceptual background is presented. Then, research methodologies are explained, followed by findings of the taxonomy construction procedures. Subsequently, the structure, originality and implications of taxonomy are highlighted, and, finally, limits and proposals for future research are presented.

Conceptual background

The sustainability mindset and its impact on corporate communication

Due to the democratization of information, and therefore of knowledge, greater awareness has been acquired about the consequences that individuals' actions have on the future of our planet (Gallagher, 2020). In fact, a collective awareness gradually emerged that led people to ask questions about the work of governments, institutions and companies in favor of sustainable development. From the consumer perspective, this new sensitivity to sustainability has translated into the desire to act and have a positive impact on the world, increasing the demand for sustainable products and services (Allen and Spialek, 2018). This proactive attitude characterizes, in particular, the new generations of consumers: millennials and, above all, Gen Z'ers. The Generation Z cohort includes young people born after 1995 and up to 2010: the first generation composed exclusively of digital natives (therefore also called “NetGen” or “IGen”) (Borg et al., 2020; Twenge, 2017). Gen Z'ers are highly educated, tech-savvy and community-oriented (Su et al., 2019). Because they are born and raised in a high-speed and connected world, they are ready to express themselves publicly on the work of organizations that can affect their well-being, with the potential to affect businesses that fail to adapt their working behavior to sustainable standards (Borg et al., 2020).

Considering these new trends, for organizations, being sustainable means defining a new corporate philosophy, turning the traditional marketing concept toward sustainability marketing (Kumar et al., 2012), contextually establishing sustainable relationships with customers, society and the environment (Peattie and Belz, 2010).

The integration of sustainability principles and practices in marketing strategies inevitably impacts, primarily, communication and branding. Branding sustainability means interacting with the public (Kuchinka et al., 2018; Grubor and Milovanov, 2017), conveying socially relevant values externally, in an appealing and effective way, and highlighting how deeply they overlap with those of the brand (Kumar and Christodoulopoulou, 2014; Newig et al., 2013).

Sustainability communication: issues, approaches and the use of the web

The importance of companies' communicating their sustainability initiatives has always been a subject of strong interest in academic research. In fact, many studies have focused on various aspects of the SC: on what, to whom, how to and where to communicate sustainability messages (Gruber et al., 2017).

SC concerns the future development of society, which, trying to understand the relationship between human beings and their environment, aims to develop a critical awareness of problems of this relationship and thus relate them to social values and norms (Godemann and Michelsen, 2011). The discussion on SC involves arguments that derive from economic, ecological, social and cultural perspectives and is located in an area that includes all social systems. Among these, companies have always played a fundamental role (Waddock, 2004). Their intervention in the sustainability discourse is historically linked to their economic, legal, ethical and philanthropic responsibilities (Carroll, 1979). For some authors, SC implies communicating the social role of business (i.e. “corporate citizenship”) (Hartman et al., 2007); for others, reasoning on ecological development of the planet should not be excluded (Ott et al., 2011). In this sense, SC is generally regarding corporate social responsibility (CSR), corporate citizenship and sustainable development (Capriotti and Moreno, 2007). Communication on sustainability, therefore, encompasses issues such as climate, biodiversity, human rights, public health, consumption and so forth.

As for to whom to communicate, the SC has changed from a mere instrumental process of accounting toward institutional decision-makers to include shareholders and internal stakeholders up to the wider public of consumers and public opinion (Lodhia, 2014). Particular attention still needs to be paid toward more demanding members of Generation Z that expect interactivity (Southgate, 2017) and value quick and easy online information (Priporas et al., 2017). Consequently, the way in which sustainability has to be communicated must evolve, both in terms of approach (from one way and static to multi-directional and dynamic) and the vehicles used (from the paper report, to its online transposition, to the web and social media) (Manetti and Bellucci, 2016).

In general, SC can follow two approaches: (1) the mono-directional diffusion of information and (2) the creation of symmetrical relationships with key stakeholders (Khan et al., 2019). The first approach entails the main goal of spreading data to affect the public's image of the organization. It primarily serves the institutional accounting needs: SC has to be measurable and has to facilitate comparability and objective evaluation (Özdemir et al., 2011). In that sense, SC has its roots in analysis, data and real results, collected following harmonized procedures also at an international level that are verifiable, replicable and, possibly, certified by third independent entities. For this reason, the adoption of global disclosures standards based on the ESG (environmental, social and governance) paradigm has emerged in this area of communication. Information is expressed as a periodic report according to metrics and indicators that make it immediately interpretable and comparable with a good standard (such as the dominant one of the Global Reporting Initiative [GRI]). The reports clearly have the intent of involving a specific segment of stakeholders, interested in carefully monitoring corporate performance in certain areas (governments, investors, suppliers, etc.) (Garcia-Torea et al., 2020). However, many audiences do not tend to proactively seek information on corporate responsibility, especially when it requires understanding key performance indicators. It is, therefore, advisable to incorporate sustainability messages into the mainstream of web communications with a clear explanation of the relevance of the problem to the stakeholder concerned (Dawkins, 2005). Isaksson and Steimle (2009), for example, argue that GRI guidelines for reporting do not consider the needs of customers and are hence inadequate in answering their concerns.

When supported by the information and communications technologies (ICTs), reporting could evolve from a monologue controlled by the company to a symmetrical and interactive approach, which allows reaching a wider audience, building dialogs and obtaining feedback and suggestions from all groups of stakeholders (Fulgoni, 2016; Isenmann et al., 2007).

This second approach needs to actively use the Internet and its tools (i.e. web and social media). However, the sustainability digital report is a communication tool that has several limits in terms of effective engagement (Stocker et al., 2020). People ask for data because these allow them to verify the truthfulness of performance statements. But the social and political role that organizations are called to play today (Miklian, 2019) goes far beyond reporting (Henisz, 2017). It includes, in fact, education for a new, sustainable lifestyle, through the dissemination of values, inspiration through case studies and sharing good examples, following a “walk the talk” perspective (Schons and Steinmeier, 2016) and setting the basis for brand activism (Kotler and Sarkar, 2018). The web and social media offer companies concrete opportunities in that sense to connect and interact with stakeholders in innovative and engaging ways (Saxton et al., 2019). The dialogic and symmetrical communication of the web makes it possible to respond to both the information-seeking needs and the search for entertainment (de Vries et al., 2012). As stated by Khan et al. (2019), leverage on the web-atmospheric cues (i.e. visual, information, social, ethics and security) on social media is fundamental to contribute to the development of positive behavior of people in sustainability terms. Social media, in fact, show the potential of impacting attitude formation and change (Fortin and Dholakia, 2005); they favor the emotional engagement and connection of individuals with messages, amplifying their persuasive effect (Fulgoni, 2016) and conveying the idea that companies are willing to commit themselves for boosting their customers' sustainable growth (Kang and Park, 2018). By intercepting new concerns and public inputs, initiating discussions on different daily topics and encouraging consumers to pose questions and share experiences (Heinonen, 2011), SC promoted on the web could reach a higher degree of differentiation of core themes that define the most central characteristics, values and philosophy the organization wishes to express (Gilpin, 2010). This helps in capitalizing on the potential reputational benefits of SC, reaching differentiation and competitive advantage, especially in the context ruled by the younger generation of users (Reinikainen et al., 2020; Francis and Hoefel, 2018; Duffett, 2017).

Toward a taxonomy of SC topics

Considering the limits of engagement of sustainability reports (both as a communication vehicle and for the type of content) and the need to relate with a more interactive audience, the real challenge in communicating sustainability becomes finding customer-centered ways of involvement (Chomvilailuk and Butcher, 2018; Lim and Greenwood, 2017), making easier and more attractive complex, technical and specialist information (Rossi, 2017). This requires converting metrics into relevant and emotionally engaging content from a content-marketing perspective focused on those sustainability-related topics that attract people's attention. The aim is to move away from reporting to embrace forms of argumentative (and even narrative) communication about all those aspects of life and business that impact the sustainability of the planet and that can contribute for promoting it.

While the reporting of sustainability goals and results is guided by frameworks based on metrics and performance indicators, a model that can be considered a guide for creating content typical of a SC agenda is missing. Thus, there is the need to map aspects of CS—and, more generally, of sustainable development—about which companies should discuss with their audience.

However, the domain of knowledge relating to the concept of CS is a multi-dimensional issue involving huge amounts of sub-issues (i.e. pollution, climate change, social development, supply chain management, etc.). The main aim of the paper is, therefore, to define a taxonomy of SC topics, each of which can represent a touch point between the expectations of stakeholders and the interests of companies.

The usefulness of a taxonomy generally lies in the fact that it can be used as a way to set a guide able to hierarchically organize concepts in a particular domain (Centelles, 2005). In fact, it can even help to define aspects that define a complex construct, such as that of CS. In the academic literature, it is possible to trace studies that have attempted to trace the fundamental aspects of CS (or of the correlated construct of CSR), which fulfill different objectives. Some of these are built on the basis of a stakeholder approach; that is, they categorize activities and practices by grouping them with respect to the interests of the various stakeholder groups. Among the most important taxonomies constructed in this way, we must mention that of Spiller (2000), used as a starting point in numerous studies (including Jamali, 2008; Lamberti and Lettieri, 2009; Schipper and Silvius, 2017). Other taxonomies are, instead, structured on the basis of other approaches, which range from the content analysis of theoretical definitions to the identification of themes in a specific industrial sector (Haberberg et al., 2010). Among these, Dahlsrud (2008) and Lindgreen et al. (2009) studies have to be remembered.

The construction of a sustainability taxonomy in the context of CS has never been tackled before. Considering the research objective of this paper, none of the above-mentioned approaches is functional. Attempting to categorize sustainability issues by grouping them on the basis of stakeholders' interests, for example, is anachronistic in a historical moment, in which concerns and interests about sustainability are shared between different groups. Furthermore, it is not the purpose of this paper to focus the attention on a single industrial sector. Rather, we want to develop a taxonomy of sustainability topics aimed at systematizing the domain of this broad theme, placing itself at the top of any business activity. It is therefore necessary to (re)define CS dimensions in a framework adaptable to multiple realities.

Research methods

SC topics taxonomy: definition and construction

A taxonomy is a classification of items into separate groups, so that there is intragroup similarity and intergroup difference (Rich, 1992). The groups are organized in a tree structure, where each set is nested in larger category and, at the same time, includes the lower-level group. How the hierarchy of a taxonomy is determined depends mainly on the generic relationship. Hierarchical relationships are based on levels of superordination and subordination, where a (broader) superordinate or parent term represents a class or a whole, and a (narrower) subordinate or child term represents a subclass or a part of the whole.

In the taxonomy of sustainability topics, the definition of hierarchical relationships is traced in the so-called logic of “whole–part relationship” (Fraunhofer, 2009). The whole–part relationship “refers to the relation between a concept/entity and its constituent parts” (Khoo and Na, 2006). This relationship can be characterized by an “is part of” relationship between the narrower term and the broader term, such that existing between a complex construct (i.e. “sustainability”) and its components (sustainability issues). The fundamentum divisionis (literally, “the basis of division”) (Marradi, 1990) is, thus, that of “family resemblance” (Wittgenstein, 1953), so that, through a deductive process linked to the semantics of terms, the high-level concepts can accommodate the semantics of their children's concepts (Yao et al., 2012).

Defining a taxonomy is a conceptual and qualitative way of classifying and representing information (Tsui et al., 2010); then, the SC topics’ taxonomy has to be intended as a hierarchical dictionary of tags, both theoretically (in order to delimit conceptual boundaries of sustainability aspects) and empirically (in order to define the nomenclature of categories) derived.

The construction of a taxonomy can take place following two different procedures (Sujatha et al., 2011): (1) the top–down procedure, which provides the definition of a few more general concepts such as superordinate categories and the subsequent identification of sub-categories referred to each category; (2) the bottom–up procedure, which implies the definition of more specific categories, with the subsequent collection of these into general groups. This study started by implementing a top–down approach, subsequently integrated with the results of the bottom–up approach in order to refine the labeling system of taxonomy categories.

For the identification of the superordinate categories of sustainability, a systematic literature review was conducted. In a second phase, the declination of superordinate categories into sub-categories required a thematic content analysis according to methods that will be indicated later on.

Furthermore, a taxonomy can be built through a manual or automatic approach (Meng et al., 2015). Although several tools are available to automatically generate a taxonomic structure, manual construction provides a greater control over the disambiguation of topics and the choice of labels to be assigned to thematic categories (Sujatha et al., 2011).

The superordinate categories of sustainability topics taxonomy: a literature review

The superordinate categories of the taxonomy have to be found in the definition of the CS construct. This construct has been, previously, defined as a “business contribution to sustainable development” (van Marrewijk, 2003) in those business operations with the ultimate goal of “meeting the needs of the present without compromising the ability of future generations to meet their own needs” (WCED, 1987). A multiple-step systematic literature review was therefore carried out to understand what aspects concern (or are affected by) these operations. The first step of review was conducted on CS- (and CSR-) related academic contributions, published in the years between 2000 and 2020. The authors located papers by searching for the keywords “corporate sustainability,” “corporate social responsibility” and “CSR,” each combined with the keywords “dimensions,” “aspects” and “pillars.” The review focused on journal articles, volume contributions and conference proceedings that were found searching on the Google Scholar and Web of Science databases. For each search string, the first 50 resulting records were collected and sorted according to the number of citations for a total of 900 records. We therefore proceeded to exclude duplicate documents and those not relevant to the research (i.e. the off-topic file). The documents in which the concepts of “dimensions,” “aspects” and “pillars” actually referred to the concept of CS were kept. The final sample consisted of 500 documents.

What has emerged with great evidence from the review of these documents is that most of them (81.8%) consider CS as the product of the balance between three dimensions: environmental, social and economic issues. These studies, thus, openly recall the Triple Bottom Line (TBL) construct, introduced in 1987 by the Brundtland Commission and then theorized by John Elkington in 1994. This theory is also known as the “3P”; it states that all kinds of companies should be responsible for profit, people and planet (Elkington, 1994, 2013). To confirm the scientific interest in investigating CS with reference to the TBL pillars, a second phase of review was conducted on the literature that resulted from the specific key phrases such as “environmental sustainability,” “social sustainability” and “economic sustainability.” The tables in Appendix 1 are intended to offer a summary of the academic contributions of the last 20 years that have had as their subject the planet, people or profit dimension of sustainability. Furthermore, if it is considered that TBL has been used for the development of frameworks designed to measure sustainability performance (Hubbard, 2009; Mitchell et al., 2008), the relevance of this theory is strengthened. Therefore, it can be argued that there are three fundamental dimensions for the creation of the taxonomy of SC topics: the environment (planet), the society (people) and the economy (profit). The last step of the literature review was therefore focused on verifying the possible preexistence of a sustainability taxonomy built on the TBL. It turned out that the GRI standards (Hedberg and von Malmborg, 2003) already offer a taxonomic structure of the economic, environmental and social issues significant for the organization.

The profit dimension of sustainability in the academic literature

| Author(s) | Headline | Theme | Year |

|---|---|---|---|

| Col, B., and Patel, S | Going to haven? Corporate social responsibility and tax avoidance | This study examines the endogenous relation between CSR and tax avoidance by focusing on a common strategy of corporate tax avoidance, i.e. establishing entities in offshore tax havens | 2019 |

| Hammer, J., and Pivo, G | The Triple Bottom Line and sustainable economic development theory and practice | This research regarding whether and how practitioners prioritize and engage in triple bottom line economic development. It aims at defining TBL in the sustainable economic development perspective | 2017 |

| Gonzalez-Rodrıguez, R., Dıaz-Fernandez, C., Simonetti, B | The social, economic and environmental dimensions of corporate social responsibility: the role played by consumers and potential entrepreneurs | In this paper, a research model is developed to examine the drivers which influence consumers and entrepreneurs' perceptions of CSR | 2015 |

| Reverte, C., Gomez-Melero, E., Cegarra-NavarroJ.G. | The influence of corporate social responsibility practices on organizational performance: evidence from eco-responsible Spanish firms | This study fills in an important gap by analyzing the impact of CSR practices on a measure of organizational performance encompassing both financial and nonfinancial indicators and by studying the potential mediating role of innovation in the CSR performance relationship | 2015 |

| Saeidi, S.P., Sofian, S., Saeidi, P., Saeidi, S.P., SaaeidiS.A. | How does corporate social responsibility contribute to firm financial performance? The mediating role of competitive advantage, reputation and customer satisfaction | This study considers sustainable competitive advantage, reputation and customer satisfaction as three probable mediators in the relationship between CSR and firm performance | 2015 |

| Rusmanto, T., Williams, C | Compliance evaluation on CSR activities disclosure in Indonesian publicly listed companies | The objective of this research is to evaluate disclosure compliance of CSR activities, including policies, programs and cost for sustainable development of the companies | 2015 |

| Fifka, M., Pobizhan, M | An institutional approach to corporate social responsibility in Russia | The objective of the study is to analyze to what degree the national political and socioeconomic institutions determine CSR practice, and how it is influenced by international factors, such as CSR standards, frameworks and foreign stakeholder expectations | 2014 |

| Waworuntu, S.R., Wantah, M.D., Rusmanto, T | CSR and financial performance analysis: evidence from top, ASEAN listed companies | The purpose of this research is to investigate whether the commitment of companies to their stakeholders has a relationship with better financial results and also to establish the extent and pattern of corporate disclosure in the top listed companies in the ASEAN region | 2014 |

| GoeringG.E. | The profit-maximizing case for corporate social responsibility in a bilateral monopoly | The paper provides a novel theoretical profit-maximizing rationale for the strategic use of CSR, demonstrating that a CSR contract can be used in place of the traditional two-part tariff scheme (wholesale price and fixed franchise fee) to optimally coordinate the marketing channel | 2013 |

| Wagner, M | The role of corporate sustainability performance for economic performance: a firm-level analysis of moderation effects | This paper analyses the link between sustainability management and economic performance using panel estimation techniques | 2010 |

| Guenster, N., Bauer, R., Derwall, J., and Koedijk, K | The economic value of corporate eco-efficiency | This empirical study reports that eco-efficiency relates positively to operating performance and market value | 2007 |

| Heal, G | Corporate social responsibility: an economic and financial framework | The study analyses CSR from economic and financial perspectives and suggest how it is reflected in financial markets | 2005 |

| Doane, D., and MacGillivray, A | Economic sustainability: the business of staying in business | This report finds that economic sustainability is the most elusive component of the TBL approach | 2001 |

The people dimension of sustainability in the academic literature

| Author(s) | Headline | Theme | Year |

|---|---|---|---|

| Crane, A., Matten, D., Glozer, S., and Spence, L | Business ethics: managing corporate citizenship and sustainability in the age of globalization | This book aims to explore the foundations of business ethics, including the nature of business ethics, the social role of the corporation, ethical theory, ethical decision-making and business ethics management | 2019 |

| Eizenberg, E., and Jabareen, Y | Social sustainability: a new conceptual framework | The study proposes that social sustainability strives to confront risk while addressing social concerns. Authors propose a comprehensive conceptual framework of social sustainability, which is composed of four interrelated concepts of socially oriented practices | 2017 |

| Xia, Y., Zu, X., and Shi, C | A profit-driven approach to building a “people-responsible” supply chain | This research develops a stylized analytic framework that links a firm's supply chain social performance in people with its economic performance in profit | 2015 |

| Duff, A | Corporate social responsibility reporting on professional accounting firms | This paper examines the CSR reporting undertaken by the 20 largest professional accounting firms in the United Kingdom. These social evaluations (prestige) allow them to enhance their intellectual capital and consequently charge premium fees and effectively increasing partner wealth | 2014 |

| Vifell, Å. C., and Soneryd, L | Organizing matters: how 'the social dimension' gets lost in sustainability projects | On the basis of relevant organizational dimensions and case analyses, the paper shows how the organization of sustainability shapes the ways in which the projects articulate the social dimension | 2012 |

| Dillard, J., Dujon, V., and King, M. C | Understanding the social dimension of sustainability | This book employs a multidisciplinary perspective to explore a diverse range of topics along different geographical scales within varying locations to better understand the social aspect of sustainability | 2008 |

| Newell, P., and Frynas, J. G | Beyond CSR? Business, poverty and social justice: an introduction | This special issue aims to analyze how far CSR initiatives help to address poverty, social exclusion and other development challenges | 2007 |

| Utting, P | CSR and equality | This paper attempts to contribute to the discussion on CSR impacts by focusing on the contribution of CSR to equality and equity, understood here in terms of minimizing deprivation; enhancing equality of opportunity; correcting gross imbalances in the distribution of income, wealth and power and social justice | 2007 |

| Sharma, S., and Ruud, A | On the path to sustainability: integrating social dimensions into the research and practice of environmental management | This paper is focused on the social principles of justice and inclusiveness embedded in the concept of sustainable development. It states that promoting sustainable development requires that governments incorporate these principles into designing holistic policies that motivate and enable firms to develop more sustainable strategies | 2003 |

| Ferris, J., Norman, C., and Sempik, J | People, land and sustainability: community gardens and the social dimension of sustainable development | In this study, emphasis is given for exploring the social dimension of sustainable development policies by linking issues of health, education, community development and food security with the use of green space in towns and cities | 2001 |

The planet dimension of sustainability in the academic literature

| Author(s) | Headline | Theme | Year |

|---|---|---|---|

| Zeng, S., Qin, Y., and Zeng, G | Impact of corporate environmental responsibility on investment efficiency: the moderating roles of the institutional environment and consumer environmental awareness | From the perspective of investment efficiency, this paper discusses the impact of corporate environmental responsibility on investment efficiency and the moderating role of the institutional environment and consumer environmental awareness | 2019 |

| Doluca, H., Holzner, B., and Wagner, M | Corporate sustainability and environmental innovations: practical implications from a cross-country analysis over 15 years | This paper underlines the importance of environmental-related innovation activities for the present and for the future | 2019 |

| Graafland, J., Smid, H | Reconsidering the relevance of social license pressure and government regulation for environmental performance of European SMEs | Whereas social license pressure is held as a strong motive for the corporate social performance (CSP) of large enterprises, it is argued in the literature that it will not sufficiently motivate small and medium-sized enterprises (SMEs). In this view, government’s regulation is the most effective way to improve the environmental performance of SMEs | 2017 |

| Dangelico, R. M., and Pontrandolfo, P | Being “Green and Competitive”: the impact of environmental actions and collaborations on firm performance | In this paper, the authors seek to enhance the understanding of the link between environmental management and firm performance, so contributing to the debate of being “green and competitive” | 2015 |

| Searcy, C., Dixon, S.M., NeumannW.P. | The use of work environment performance indicators in corporate social responsibility reporting | Work environment issues refer to all aspects of the design and management of the work system that affect employees' interactions with the workplace | 2015 |

| Khojastehpour, M., and Johns, R | The effect of environmental CSR issues on corporate/brand reputation and corporate profitability | The purpose of this paper is to investigate the effect of environmental CSR (climate responsibility and natural resource utilization) on corporate/brand reputation and corporate profitability | 2014 |

| Cho, C.H., PattenD.M. | Green accounting: reflections from a CSR and environmental disclosure perspective | The paper attempts to illustrate the problems that voluntary environmental disclosure creates with respect to reduced incentives for companies to improve environmental performance | 2013 |

| Bönte, W., Dienes, C | Environmental innovations and strategies for the development of new production technologies: empirical evidence from Europe | This study empirically investigates whether firms' improvements in energy and material efficiency are related to the extent to which external partners are involved in the development of process innovations, covering 14 European countries | 2013 |

| Flammer, C | Corporate social responsibility and shareholder reaction: the environmental awareness of investors | This study examines whether shareholders are sensitive to corporations' environmental footprint | 2013 |

| Babiak, K., Trendafilova, S | CSR and environmental responsibility: motives and pressures to adopt green management practices | This paper examines the diffusion of environmental management initiatives in business and the motives and pressures reported by senior executives to adopt these practices in one industry | 2011 |

| Wahba, H | Does the market value corporate environmental responsibility? An empirical examination | The aim of this research was to present empirical evidence regarding the influence of engaging in environmental responsibility on the corporate market value | 2008 |

| Simpson, M., Taylor, N., and Barker, K | Environmental responsibility in SMEs: does it deliver competitive advantage? | The study aimed to assess the ability of SMEs to create a competitive advantage by adopting environmental good practice and making environmental improvements to their business | 2004 |

| Gray, R., and Bebbington, J | Environmental accounting, managerialism and sustainability: Is the planet safe in the hands of business and accounting? In Advances in environmental accounting and management | This chapter seeks to provide a review of the current state of the art in environmental accounting research through a “managerialist” lens and then goes on to illustrate the essence of the problem through the reporting of a new analysis of data from an international study of accounting, sustainability and transnational corporations | 2000 |

The GRI emerged and established itself as an international model for sustainability reporting (Brown et al., 2009), as it provides a suitable basis for (both traditional and digital) reporting sustainable performances of organizations of any size, belonging to any sector and country (Milne and Gray, 2013). The three pillars of sustainability are expressed, through the GRI 200, 300 and 400 series [1], in multiple measurable aspects of business activities. They are therefore designed to be expressed numerically in the form of key performance indicators. However, previous studies have shown that when individuals talk about sustainability, they conceive dimensions other than those foreseen by the GRI framework, thus suggesting a disconnection between reports on CS and real interests of stakeholders (Bradford et al., 2017). Thus, some GRI categories are difficult to interpret as being topics of SC. The need to modify the GRI's scheme to adapt it to the research objective immediately was emerged. However, having the TBL pillars as main references, the GRI 200, 300 and 400 series can be considered a useful and consistent starting point for developing the taxonomy of sustainability topics. Thus, they are the interpretative guidelines used to identify the topic tags in the following bottom–up procedure of thematic content analysis.

The sub-categories of sustainability topic taxonomy: a thematic content analysis

Starting from the categories identified by GRI, to better understand how to organize and label new categories, a thematic content analysis was applied in a multiple-case research context. Thematic content analysis is “a method for identifying, analyzing and reporting patterns (themes) within data” (Braun and Clarke, 2006, p. 79). Case studies were selected from the top ten list of corporate brands included in “The 2019 GlobeScan-SustainAbility Leaders Survey” [2]. These are brands that have best integrated values and principles of sustainability into the business strategy. Since communication was one of the factors considered in assessing leadership, we proceeded to verify in which topics the digital communication of sustainability was declined by these brands. After preliminarily ascertaining the intensive use of social networks (Facebook and Twitter) to post website-native SC content, it was decided to explore the corporate website, considered to be the reference channel. The website is in fact the most comprehensive and exhaustive source of information on a company's activities (Du et al., 2010; Moreno and Capriotti, 2009), with sections specifically dedicated to the declaration of the company's strategic orientation and initiatives undertaken in terms of sustainability (Siano and Conte, 2018).

In analyzing corporate websites of sustainable brands, therefore, reference was made to the section dedicated to sustainability (or CSR), together with the page dedicated to the presentation of the company (e.g. “About us”). It, in fact, generally includes information on corporate strategy and, therefore, also on sustainable orientation (Siano and Conte, 2018) [3]. The data were retrieved in September 2019 from a publicly available site-map or, in the absence of this, from the navigation menus. The sustainability topics that have at least one dedicated website page were identified. In the presence of a single menu item, thematic sub-sections were found within the main web page that was focused on sustainability. Websites that did not have a section of the site dedicated to sustainability, but only a sustainability report was excluded (i.e. tesla.com).

Text analysis was used as an inductive method for data analysis, while emerging coding was selected as a technique for defining taxonomic category labels (Schipper and Silvius, 2017). First, two independent researchers analyzed the corpus of 300 web pages collected as described above and associated a list of descriptive labels of the main topic to each piece of content (each one was in charge of coding a checklist of labels). Some of the labels have been selected among those of the GRI series, where they were considered sufficiently descriptive; others were borrowed from the nomenclature commonly used on websites or were proposed from scratch. The lists have been compared, checking the reliability of the coding. If the level of reliability was not acceptable, researchers repeated the previous steps. Once reliability was established, the coding was used to define the taxonomy.

Appendix 2 summarizes the content analysis of corporate websites, reporting for each website section the number of web pages analyzed. The third and final column assigned a label, on which both researchers agreed, to define the detected sustainability issues. Some labels were more generic than others. Therefore, starting from the third column and considering the aforementioned principle of “family resemblance” (Wittgenstein, 1953), we proceeded to group the narrower subjects—which we define topics—into more general themes and to classify them, in turn, according to the broader dimensions of sustainability.

Findings

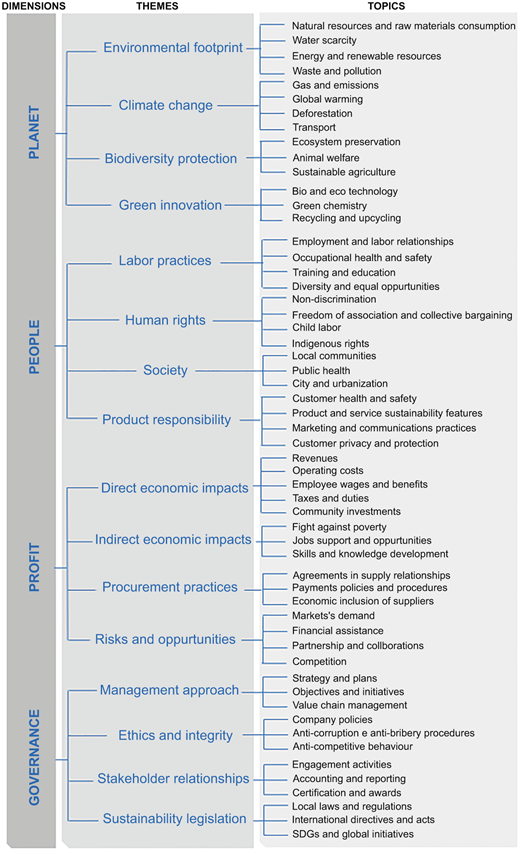

The final taxonomic structure is shown in Figure 1 and is divided into four sustainability dimensions—planet, people, profit and governance—each organized into four themes. Each theme, in turn, could group multiple topics of SC.

In the context of the planet dimension, the topics of discussion are linked to the consumption of natural resources and raw materials, the scarcity of water, energy expenditure and renewable resources, initiatives to reduce pollution and the production and disposal of waste. All refer to the issue of environmental impact, which, being often intended in terms of “ecological footprint,” is labeled as “environmental footprint.”

The topics relating to the impact of CO2 emissions, global warming and consequences of deforestation or transport on the health of the air all refer to the general theme of climate change, seen as a consequence of these factors. This theme has been labeled “Climate change.” On the other hand, all topics that refer to the impact on biodiversity are labeled “Biodiversity,” that is, the management of an ecosystem for business purposes, with particular emphasis on animals and agricultural land use. A different theme is content related to environmental technologies or green technologies, therefore labeled as “Green innovation.” This refers to content focused on innovation of processes and tools from an eco-friendly perspective.

All topics related to person or group of people are identified as part of the people dimension. People are intended in their different relationships with the company (i.e. employees and supply chain partners, local communities and society, in general, and consumers). With the label “Labor practices,” we grouped all subjects concerning the management policies for work conditions and supply chain relationships, safety and health in the workplace, training and education of employees, respect for diversity and equal opportunities (in terms of career chances and remuneration). The “Human rights” label includes all the topics relating to nondiscrimination initiatives (seen in all its forms: gender, race, age, etc.), freedom of association and collective bargaining, child labor, rights of natives and promotion of education in developing countries. Instead, subjects that can be grouped together in the “Society” theme refer to initiatives promoted by the company in favor of local communities, public health and well-being, city sustainability and urban development. Finally, the “Product responsibility” theme refers to consumers, bringing together all those topics that focus on the sustainability of products/services and respect for consumers (i.e. health and safety, transparency of communications and interactions and privacy issues).

As part of the profit dimension, all content that indicates costs and revenues, wages and benefits of employees, payments to investors and governments or the promotion of investments, fall under the theme “Direct economic impacts.” Decisions and activities promoted against poverty (such as economic investments in highly poor areas) and the development of skills and career opportunities are instead considered topics that refer to the “Indirect economic impacts.” Within the “Procurement practices,” content regarding policies, practices, procedures and agreements for procurement can be grouped. Finally, under the label “Risks and opportunities” are all those topics related to economic risks and opportunities for a company, which are therefore connected to changes in market demand, financial assistance (i.e. contributions, incentives and royalties), partnerships with other companies and competition.

An interesting result of the content analysis, which represents the added value of this work, was that many sustainability issues were not attributable to any of the three dimensions of the TBL. Rather, they were referable to a set of principles, rules and procedures concerning the management of a company oriented toward sustainability. The creation of a fourth dimension of taxonomy, called governance, has therefore become necessary. This dimension can be divided into the themes of “Management approach” and “Ethics and integrity” of the business; initiatives and activities to enhance “Stakeholder relationships” and everything related to “Sustainability legislation,” which governs business activities (laws, acts, international agreements, etc.).

Discussion and implications

The development of the taxonomy of SC topics is distinguished from taxonomies already existing in CSR or the sustainability literature from multiple points of view: (1) in terms of the basic theoretical approach, (2) in the structure's development and (3) regarding the purpose of use in practice.

First, the design of the taxonomy is detached from the traditional stakeholder approach (Jamali, 2008), typically used as a basis for studies aimed at defining sustainability accounting practices and procedures (Hörisch et al., 2020). This study starts from the consideration that the web should be understood as a primary and ideal environment for the development of stakeholder engagement mechanisms through SC. The modern world is submerged by concerns of collective interests. For instance, impacts on climate and biodiversity, peaceful struggles for the enhancement of diversity and the achievement of equality are all issues that affect everyone and cannot have a preferential audience. In planning communications on environmental, social and economic issues, no audience cohort or topic for engagement should be excluded. The approach to SC requires a vision of the “big picture” (Hemingway, 2019). The taxonomy provides a concise and immediate conceptual framework on all those topics of broader interest, which, suitably modulated, can act as touch points with several groups of stakeholders.

About the structure, this study opted for a development approach that combines the theoretical foundations about sustainability pillars with the empirical evidence drawn from the communication practices already in place by those who are considered leaders in managing sustainability issues. In this way, the taxonomic framework of the topics is already in line with the best practices of thematic organization of SCs via the web. It is thus functional to the content marketing objectives in the context of SC because it represents a “platform” for programming an editorial plan based on environmental, social, economic and governance issues. The aim of the content marketing practices in this area is twofold (Villarino and Font, 2015): first, to make the target audience aware of how the products offered will meet their sustainable consumption needs and second, to establish a deeper and more complex dialog with stakeholders, exploiting the capillarity of web communications in order to find new possible world realities and to explore how business can do well by doing good, engaging all involved players (Senge et al., 2008).

Both aspects can have a potential effect, especially on the younger generation of consumers, as they highly value environmental/ethical commitments, diversity and inclusiveness, truth and ethics (Francis and Hoefel, 2018); show a strong sense of social responsibility and state to be socially and health conscious (Koulopoulos and Keldsen, 2014). More than all others, this particular category of stakeholders (of consumers and future decision-makers) is influenced by web cues and expects a simplified language of sustainability messages, with a high degree of interactivity, interconnectivity and signals of trust (Thomas et al., 2018).

In this perspective, the work, carried out starting from the GRI, was aimed at moving away from the strictly parametric definition of aspects of sustainability in order to reach a system of labels that express the argumentative nature of sustainability issues [4].

The thematic content analysis showed that the content about principles, values and policies that guides and regulates corporate management—topics that are organized under the Governance dimension—is commonly disclosed within websites, as much as those of the other dimensions of sustainability. This means that, in planning SC, companies tend to opt for a content agenda that correctly balances not three but four items: planet, people, profit and governance. It is therefore believed that from a sustainability content marketing perspective, governance is to be recognized as a fourth pillar of CS (Alibašić, 2017). In the corporate context, the TBL lacks an essential aspect to pursue sustainability consistently and effectively. The inclusion of governance is necessary, as it strengthens all parts of sustainability planning, ensuring that efforts in terms of environmental, social and economic responsibilities are implemented in an efficient and ethical way. This principle also applies to corporate communication: it is necessary to disclose commitments and initiatives in favor of the planet or of society as they tell how and why these actions are carried out.

Regarding the practical use of the taxonomy, it must be first considered that the taxonomy was born as the evolution of the GRI framework. Thus, it helps to overcome the disconnection, currently still existing, between the reports and branding content in the direction of “integrated reporting” (IR). The taxonomy of sustainability topics allows, in fact, the sustainability elements to be framed in a semantically wider discourse in which the information on performance can (and must) constitute only the starting point of a narrative continuum through which a user can explore and be involved in the business reality from every point of view.

The set of taxonomy labels can also find value in a so-called content intelligence system. Used as tags to describe the topic of digital content, the labels allow to connect, in a sort of hypertext, all content that belongs to the same category, whether it is conveyed in digital reports, on a website or on another channel. In this way, content is automatically classified in an ordered archive, which can be consulted at any time. This offers, thus, a huge simplification of the work of web editors. This is also an advantage in terms of user experience: for a user, it is possible to “navigate” the topic of interest in a sort of continuum not tied to the medium. A content intelligence system does not just sort the content. Through tagging, the system “activates” it; the system is able to return data about which content creates more leads and which is the most interesting content for each user, and, based on this, automatically customizes the user experience. In brief, tagging content allows content managers to have continuous insights, which are useful not only for content management but also for the redefinition of content strategies.

As a framework for a content intelligent system, the taxonomy of sustainability topics serves several purposes: (1) provides a dictionary of tags that can be used for indexing and retrieval of SC web content; (2) promotes uniformity in categories' groups format and in the assignment of labels; (3) indicates semantic relationships among items; (4) provides consistent hierarchies to improve web content navigation to help users locating desired content objects and (5) serves as a search aid in locating content objects.

Conclusions and further research

The paper contributes for enriching the academic literature relating to CS and SC, strengthening the prolific link that exists between the latter and digital content marketing practices. In this perspective, the objective of the paper was to respond to the need to equip the communication managers of sustainable organizations with a framework useful for conceptually ordering and categorizing sustainability issues in the context of corporate communications. The taxonomy of SC topics guides the elaboration and organization of content aimed at triggering stakeholder engagement mechanisms on environmental, social and economic issues. First of all, the categorization of CS aspects into an organized structure supplies parameter around what pertains to sustainable development and to sustainable business. The general understanding of the 3Ps defined by the TBL is in fact contextualized to the corporate area, divided here into a multitude of narrow environmental, social and economic corporate aspects. It also includes the fourth dimension of governance, showing the need to highlight to the wider audience the decisive role of the organizational structure. The governance must not only guide and control processes and activities by managing the risk of noncompliance with laws and regulations but also ensure that the company acts in an ethical way that is in favor of the well-being of the environmental and social context in which it operates.

Future research can be put into practice to overcome some limitations of this study. The taxonomy can be advanced by examining the communications of a larger sample of companies or using automatic content analysis procedures on a vast body of sustainability content, with the aim of reducing the subjectivity of manual content analysis and, at the same time, identifying new topics. Appropriate and relevant social media in the SC context should be identified and incorporated in further studies. The survey needs to be extended to social media natives' sustainability content and also consider user-generated content (i.e. comments), not only to eventually intercept new topics but also to enrich the taxonomy with folksonomy entries. An important aspect of the study entails evolving the sustainability-oriented corporate communications in the direction of the jargon of younger web users. This kind of communication appears to, in fact, have a positive impact on the awareness of the sustainable-sensitive Gen Z's audience group, which should be better analyzed with further research in this field.

Considering the current taxonomy as a digital content tagging system, future research can be conducted to evolve the current taxonomy into an ontological language for the semantic web. This taxonomy, in fact, represents the first step toward the semantic organization of information on sustainability into a web-friendly format, which can improve the responsiveness to online users' searches on the specific subject of sustainability. Finally, the implementation of the taxonomy as a database structure of content analysis tools can find application in studies aimed at investigating the most discussed sustainability topics in business communications from both intrasectoral and intersectoral perspectives.

Thematic content analysis of corporate websites of brands listed in “The 2019 GlobeScan-SustainAbility Leaders Survey”

| Company (website URL) | Website section | # Of web pages | Sustainability issues |

|---|---|---|---|

| Unilever (unilever.com) | /about/take-action/topics | 9 | Water; climate; partnerships; management approach; human rights; public health; planet; society and value chain |

| /sustainable-living | 32 | Customer health and safety; green innovation; natural resources; biodiversity; human rights; waste; direct economic impact; ethics and integrity; governance; stakeholder engagement; public health; emissions; water; raw materials; value chain and labor management | |

| Patagonia (eu.patagonia.com) | /activism | 34 | Management approach; economic opportunities; recycling; certification and awards; natural resources; value chain; customer health and safety; training and education; objectives and initiatives; labor management; equal opportunities; raw materials; stakeholder engagement; waste; society; climate and recycling |

| Ikea (ikea.com) | /sustainability | 12 | Green innovation; waste; recycling; climate; customer health and safety; decent work; value chain; diversity and equal opportunities |

| /who-we-are | 4 | Customer health and safety; partnerships and Stakeholder relationships | |

| /organisation/ikea-in-the-world | 4 | Market's demand; local communities and value chain | |

| Interface (interface.com) | /sustainability | 10 | Recycling; partnerships; accountability practices; certifications; raw materials and city and urbanization |

| /campaign/climate-take-back | 3 | Climate and emissions | |

| Natura (natura.com.br) | /susteintabilidade | 13 | Strategy and plans; objectives and initiatives; natural resources and raw materials; customer health and safety; climate and biodiversity |

| /iniciativas | 4 | Stakeholder relationships; marketing initiatives and objectives and initiatives | |

| Danone (danone.com) | /impact | 17 | Customer health and safety; public health; management approach; emissions; agriculture; water; recycling; stakeholder engagement; diversity; public health; management policies; initiatives and investments |

| Nestlé (nestle.com) | /csv/global-initiatives | 3 | Public health; stakeholder engagement and environmental footprint |

| /csv/impact | 43 | Customer health; value chain; human rights; labor management; water; climate; environmental footprint; waste and recycling | |

| /csv/raw-materials | 14 | Raw materials; natural resources and customer health | |

| /csv/performance | 5 | Accounting | |

| /csv/what-is-csv | 10 | Ethical business; direct economic impact; management approach; stakeholder engagement and partnerships | |

| Marks and Spencer (corporate.marksandspencer.com) | /sustainability | 25 | Strategy and plans; partnerships and collaboration; certifications; climate; waste; recycling: natural resources; health and safety; human rights; marketing; value chain; initiatives; public health; city and urbanization; policies; employment relationships; diversity and equality; bribery and corruption; ethical business and stakeholder engagement |

| Tesla (tesla.com) | – | – | – |

| BASF (basf.com) | /who-we-are/sustainability | 10 | Environment; carbon management; employment relationships; society; value chain; partnerships; management; sustainable development goals; circular economy and local community |

| /we-source-responsibly | 4 | Raw materials; renewable resources and initiatives | |

| /we-produce-safely-and-efficiently | 20 | Customer health and safety; management policies; energy; climate; natural resources; emissions; value chain; water; ecosystem protection; pollution; waste; biotechnology and product responsibility | |

| /we-drive-sustainable-solutions | 3 | Accountability standards; strategy and plans; recycling; green chemistry and product responsibility | |

| /we-value-people-and-treat-them-with-respect | 18 | Labor relationships; work conditions; employment policies; safety; privacy; citizenship; education; public health; partnerships and human rights | |

| /management-goals-and-dialog | 3 | Management approach; partnerships and stakeholder engagement |

Notes

The “GlobeScan-SustainAbility” surveys are the result of a collaborative platform that sees the two institutes (GlobeScan Incorporated and Sustainability Ltd) combining their research-driven insights into surveys such as the one mentioned, which involved over 800 experts from 78 countries around the world, with the aim of identifying most influential thought leaders in the sustainability arena and intercepting the big challenges for a sustainable development agenda.

For companies that have distinct web sites by geographic region, we considered the US website to promote the analysis in the language from which much of the sustainability terminology is adopted internationally.

For this reason, for example, the GRI “market presence” label in the profit dimension disappears, and a broader but semantically prolific wording, “revenues,” is favored.