The purpose of this paper is to identify and analyze the literature related to accounting and auditing services quality.

The authors performed a systematic literature review that considered 22 papers on the topic. The authors also applied a bibliometric analysis in order to identify the main characteristics of these studies to discuss and provide research opportunities in this field.

The bibliometric results indicate that most papers were published in services and marketing journals. The accounting service quality theme has been rarely researched in accounting field. In addition, based on our review, it was possible to identify that most papers use quantitative methods, such as surveys. The papers' conclusions diverge from each other, demonstrating a still fragmented literature.

Taken together, the paper shows how accounting services quality is relevant and emerging topic that demands future research about accounting professionals' skills, their activities and how their customers perceive quality in an environment of constant change.

The analyses indicate that there are six broad areas for future research on this topic: successes and failures of accounting services providers; the role of “client centricity”; digital accounting services; services quality and accounting education; services quality when considering different types of accounting and auditing services and development of a measurement scale and a theoretical model for accounting services quality. This paper contributes for the ongoing debate about how competition, technology and innovation are changing the landscape for accounting and auditing services providers.

1. Introduction

Competition, innovation and technology are changing the prospects for accounting and auditing services providers (Arnaboldi et al., 2017; Botha and Wilkinson, 2019). The migration toward international sets of accounting standards and the provision of automated routines pose a challenge on how firms can pursue new, credible and more efficient ways to produce information for their clients (Santos-Vijande et al., 2013).

Recent studies (e.g. Groff et al., 2015) argue that the services quality and professional qualification are key aspects for client retention. Service quality is defined as customer's overall assessment of the service delivered (Zeithaml, 1988). Also, it can be defined as the difference between customers' expectations and the actual service's performance (Parasuraman et al., 1985). Consequently, accounting services providers are investing to be perceived as more empathic, reliable and responsive to individual clients demands (Aga and Safakli, 2007; Groff et al., 2015). In an environment with adverse conditions and high competitiveness, it seems increasingly the focus on services quality in order to meet customer expectations (Lee et al., 2016).

On the other hand, few studies have focused on assessing empirically the accounting services quality (examples of papers about this topic are: Aga and Safakli, 2007; Freeman and Dart, 1993; Keng and Liu, 1998; Lee et al., 2016; Phiri, 2017). As an emergent field, the knowledge about accounting service quality is fragmented and dispersed. The prior literature reaches different conclusions in order to validate (or not) certain dimensions of quality perception, such as tangibility, reliability and responsiveness. These variety of views generates disperse results and conclusions, leaving a gap in the development of a consolidated theory of accounting service quality. In addition, to the best of our knowledge, there is no systematic literature review on this topic aiming to identify and discuss the theoretical and methodological bases applied in the literature so far. Given that, an effort must be made to converge the accounting service quality knowledge, integrating future researches opportunities and providing more relevant impact about this theme on society.

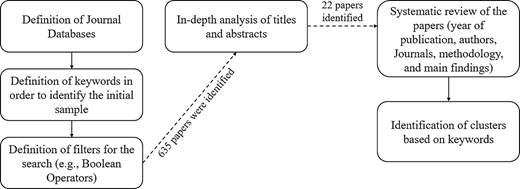

Therefore, our research questions are: What is the current state of accounting services quality literature? What are the advances possibilities in this field? To answer our research questions, we aimed to review the existing research on accounting service quality and to point out where additional studies are called for. We used Boolean operators and several keywords related to the theme. Given that, we have identified 635 papers published in journals indexed by SCOPUS and Web of Science databases from 1989 to 2018. It is important to note that the “service quality” addressed in this study does not cover earnings management, reporting quality and other subjects related to quality of accounting information. We considered the context of a service delivered and the customers' expectations and perceptions, following Parasuraman et al. (1985) definition. Thus, after analyzing and classifying each of these articles, we were able to select 22 papers related to the accounting (or auditing) services quality concept which we are using in this study.

We examined these 22 papers in detail using bibliometric methods and performing a systematic literature review. The use of bibliometric methods and a systematic literature review could allow a broader view of this specific field and may contribute to the identification of causes of phenomena related to the most significant works and the main themes in the field. As results of our bibliometric analysis, we were able to identify that although most of the papers were published in non-accounting journals (nineteen papers). However, more than half of the citations on this topic come from two papers published in accounting journals (Accounting Horizons and Accounting, Organizations and Society). Most of the papers rely on services quality and clients' perception literature and usually apply a quantitative approach.

Our detailed analyses provide three main contributions. First, to the best of our knowledge, this is the first literature review that focuses on accounting services quality, providing a framework for understanding the knowledge produced up to this date on this topic. Second, we created a cluster framework and we identified the following three streams of research: firms and competitive advantage, client perception and accounting as a Knowledge Intensive Business Service (KIBS). Third, each stream of research allowed us to suggest a research agenda that covers six main areas: (1) the success and failures of accounting services providers; (2) the customer centricity in accounting and audit services; (3) the digitalization of accounting and auditing services; (4) how services quality is related to new skills and accounting education; (5) the comparison between different types of accounting services and (6) the development of a theory and measurement model for the accounting service quality. We hope that our findings may provide a starting point for future research on this topic.

2. Theoretical framework

2.1 Service quality

Service quality is the general judgment of the customer regarding the service provided (Hussain et al., 2015). Parasuraman et al. (1985) argue that service quality could be explained as the gap between perceived and expected quality of services by customers. Quality can be interpreted in different ways, and it depends on which stakeholders and which industry and/or service are being analyzed (Garvin, 1984).

For the perception of the quality of services provided, one of the main aspects considered by consumers refers to the failures and successes made by an organization (Sivakumar et al., 2014). In an era of constant pressure for companies to cut costs and to shrink the workforce, the pursuit of error-free service becomes an arduous task (Hussain et al., 2015; Sivakumar et al., 2014). Thus, efficiency and quality are points that must be constantly analyzed by managers. Moreover, provide services with high quality can be important for companies in different ways. Previous studies argued that service quality is related to customer satisfaction (Nagel and Santos, 2017; Narteh, 2018), loyalty (Hapsari et al., 2017), willingness to pay a premium price (Bünnings, Schmitz, Tauchmann and Ziebarth, 2019) and firm reputation (Wang et al., 2003).

During the 1980s and 1990s, the academic community paid close attention to service quality theory. At that time, different models and theories emerged that sought to conceptualize and measure quality (e.g. Cronin and Taylor, 1992; Gronroos, 1984; Parasuraman et al., 1988). One of the most famous models used until today is “SERVQUAL”, developed by Parasuraman et al. (1988). The scale considers five dimensions of service quality: tangibles, reliability, responsiveness, assurance and empathy. This measurement model was created to capture service quality in different industries, and it is used in several different contexts until today.

2.2 Accounting services management

The current business environment has been changing the characteristics of management accounting practices (Albu and Albu, 2012). The development of management accountants is also determined by the need to meet stakeholder expectations for credibility, transparency in corporate reporting and their involvement with social responsibility (Zyznarska-Dworczak, 2018).

Lukka and Vinnari (2014) and Zyznarska-Dworczak (2018) address the changes in management accounting over the years. Customer orientation has become the current focus of managers. Although accountants deal with a specific type of service that is generally provided to other organizations, the management of accounting firms (or offices) needs to be performed similarly to other sectors that are also valued for information and knowledge of the service provided (Borodako et al., 2014).

This means that accounting services need to focus on customer needs and their perceptions of accounting service quality, as well as constantly investing in the good skills of the business team (Jia et al., 2016; Lee et al., 2016; Zyznarska-Dworczak, 2018). As the traditional services provided by accountants for decades are likely to be replaced by technological development, accounting firms which want to compete in this new context will potentially need to deliver high-quality services to their customers. Otherwise, they are likely to disappear.

3. Methods

The first step in our study is to identify the relevant papers that relate services quality with accounting services. To do this, it took different stages as: definitions of databases, definition of keywords, elimination of repeated articles and alignment by reading the title, abstract and main findings. As discussed by Carvalho et al. (2020), these stages are present in different frameworks used as guidelines for systematic literature review.

We start by using two major Journal Databases: SCOPUS and Web of Science. Taken together, the databases cover the most relevant scientific journals. Therefore, we do not filter our search by journals, but by databases, as done by previous studies (e.g. Castilla-Polo and Gallardo-Vázquez, 2016; Nouri and Parker, 2020). For the keywords, we used the term “service quality” with the Boolean operator “AND” providing combinations with the following terms: “account*”, “audit*”, “tax account”, tax service, “CPA”, and “Certified Public Accountant”. We considered title, abstract and keywords as the search fields and filter the results only for scientific journals.

Without restricting our sample period, we were able to identify 635 papers (this search was conducted in June 2018). We then used the software EndNote X7 in order to organize and standardize all the references and to eliminate potential duplicates since we considered two different databases. Following the approach presented and used before by other studies (Carvalho et al., 2020; Valmorbida and Ensslin, 2017), we exclude papers that are outside the scope of our research by analyzing their titles, abstracts, keywords and main findings. In order to mitigate bias, all papers were analyzed by three experienced judges.

From our initial search, 524 papers were identified as being related to service quality in other sectors, such as health, banks, transport, IT services, hospitality, etc. This could be explained because the keyword “account*” can have different meanings that are not related only to the accounting services itself. In addition, 25 papers were related to accounting information quality, but not to accounting service quality. Finally, 55 papers were neither related to service quality or accounting services. These 55 papers approached diverse themes related to marketing, such as brand equity, decision-making, post-choice experience, optimal service price and consumer satisfaction and did not specifically focused on the quality of services of accounting service providers. After the analysis, our final sample comprises 22 papers that focus on services quality and accounting or auditing services.

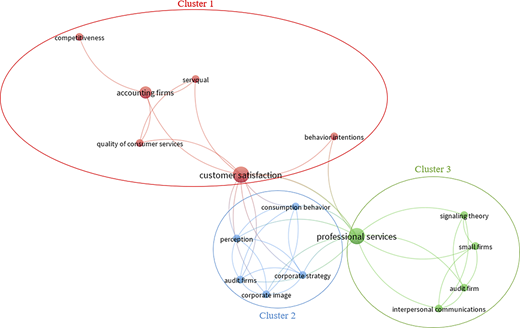

The next step was to apply a systematic literature review on the 22 papers. We extracted and analyzed the following information: year of publication, journal, methodological approach (e.g. conceptual; survey), number of citations for the paper, theories used to support their hypotheses and conclusions. We used the software VOSviewer 1.6.5 in order to identify clusters. We identify each cluster based on keywords co-occurrence, as proposed by van Eck and Waltman (2010). This technique considers the relation between different keywords. For example, if the same paper has the keywords A and B, and the same keywords were also present in another paper, the connection between keywords A and B will be greater. Thus, VOSviewer analyze two different weighting attributes. The first one is the number of links (co-occurrences) among keywords. The distance between the clusters' circles indicates the attribute of relation's strength. The closer two keywords are on the network, the higher is the number of articles in which these keywords appear associated. And the second one is the size of each circle representing the proportion of occurrence for each keyword in relation to all keywords of the sample. Figure 1 presents the methodological procedures in order to achieve our research goal.

It is noteworthy that the groupings elaborated through VOSviewer 1.6.5 are relevant to uncover links between themes, allowing to trace the development of a particular field of research. In addition, this method can help identifying specific topics of interest to the scientific community by suggesting topics with a potential association that can be explored in future research (van Eck and Waltman, 2010).

4. Results

4.1 Most relevant journals and how the discussion evolved in the literature

According to our results, the earliest identified paper that relates services quality and accounting services was the study developed by Ferguson and Higgins (1989). The paper analyses if the “Certified Public Accountant” certification and the amount of fees charged by an accounting firm may impact the expected quality and the quality perceived by the customer. The paper is aligned with other studies in the services quality literature in the 80s: to develop exploratory research to better understand what may be relevant for quality perception and how to formulate strategies in order to achieve a desired quality perception by the customers (Zeithaml et al., 1996).

Since Ferguson and Higgins (1989), other 21 papers were published relating services quality and accounting services. There is an increase in this research topic in the mid-90s (up to six per year). However, we do not identify papers between 2001 and 2005. Recently, the number of publications per year averages three. Three journals concentrate more half of the papers: Journal of Relationship Marketing (05 papers), Service Marketing Quarterly (04 papers) and Actual Problems of Economics (02 papers). Journal of Relationship Marketing and Service Marketing Quarterly are US-based journals that are focused on marketing-related topics. Actual Problems of Economics is a Ukrainian journal that focuses on Economics. Most of the journals are focused on services management and marketing. Only three papers were published in accounting journals.

4.2 Citation analysis, methodologies and theories

In order to evaluate the impact of each paper, we considered the total number of citations, according to the Google Scholar platform. Most cited papers are presented in Table 1.

Among the five papers with the highest number of citations, three of them focus on services quality for auditing services (Behn et al., 1997; Cameran et al., 2010; De Ruyter and Wetzels, 1999). Our results indicate that there are a small number of papers covering the subject of accounting services quality which have a considerable number of citations.

We also considered the main theories and concepts applied in our sample. We observed an already expected use of service quality theory as the basis for 16 papers. We find five papers that are based on customer perception, such as their evaluation and satisfaction with the service delivered. These aspects are seen in previous studies as possible antecedents and consequences of the quality of services (Cronin et al., 2000; Kasiri et al., 2017). In addition, articles were also based on KIBS-related definitions, demonstrating that previous literature discusses the development of the quality of accounting services relating them to the characteristics of high knowledge needs (Santos and Spring, 2015).

We also analyzed the methodological approaches and research design from each paper. The classification was designed by analyzing the approaches and strategies used in the studies' data collection. The methodological analysis allows us to identify a predominance in empirical studies that apply the theoretical concepts in the practical context in order to understand the reality. This type of method has congruence with studies focused on the quality of services, considering that it is an area explored in marketing that often conducts empirical studies that seek to understand the reality of organizations and consumers. In addition, the approach in most of the research was quantitative by applying surveys with consumers of accounting services. This demonstrates the predominance of studies that investigate and test the relationship between variables through the perspective of customers. Regarding quantitative studies, only one (Lee, 2013) used secondary data in their analysis.

About the papers that used questionnaires, our findings show that fifty-six percent applied the measurement scale “SERVQUAL”, developed by Parasuraman et al. (1988). Other scales, like “SERVPREF” (Cronin and Taylor, 1992) and the service quality model proposed by Gronroos (1984) are less frequent. A potential explanation for the use of “SERVQUAL” is its widespread use in the services quality arena, with more than 30 thousand references. The scale relies on more generalist dimensions that could be applied to different contexts (Roy et al., 2015). On the other hand, some authors had criticized the application of general scales such as “SERVQUAL”. They argue that these instruments do not capture the details of specific services as accounting (Fleischman et al., 2017; Ladhari, 2008).

Regarding our sample, we find different results for the papers that used the “SERVQUAL” as the measurement scale. For example, results from Freeman and Dart (1993) study validated only three factors of the scale: tangibility, assurance and empathy. In addition to these dimensions, the authors advocated for the inclusion of other variables. Results from Keng and Liu (1998) study, that also applied a modified version of the Parasuraman et al. (1988) scale, suggest that long-term relationship management and the availability to respond to any request quickly are important characteristics to maintaining a customer base. In addition, employees of accounting firms must be well-trained, and trust must be established between them and their clients.

Aga and Safakli (2007) and Lee et al. (2016) also measured the quality of accounting service using the SERVQUAL scale of Parasuraman et al. (1988). Results indicate that five dimensions are significant for the context of accounting services and indicate a positive effect between the quality of services provided and customer satisfaction. Therefore, based on this, the quality of this type of service depends on how accountants are managing the service provided, seeking the satisfaction of their customers.

Although the majority of the studies use the “SERVQUAL” scale (Parasuraman et al., 1988), this measurement instrument considers only the functional dimensions of service quality. The scale does not consider specific contexts, and thus does not consider industry-specific characteristics (Fleischman et al., 2017). It is important to highlight that none of the papers focused on developing measurement scales designed specifically for accounting services. Since accounting services are within the KIBS classification (Santos and Spring, 2015), many services are unique and there is an opportunity for future research to develop a more specific measurement scale, based on a more extensive and in-depth analysis of the factors that may contribute to the perception of quality of its unique features.

5. Cluster analysis

Our cluster analysis considered the occurrence of keywords and the ties between them using VOSviewer. We present our results in Figure 2. The circles closest to each other demonstrate the groupings of themes in analyzed studies. Thus, this cluster analysis is important to identify themes and concepts that are more discussed in accounting service quality studies.

Results from the cluster analysis, presented by Figure 1, indicate the existence of three clusters. The first one is more aligned with market competitiveness and how accounting firms can retain its customers and capture new ones. The second cluster is aligned with consumption behavior and perceptions about the company image. The third cluster is related with the professional features of accounting services and the required services providers' knowledge.

5.1 Competitiveness

The first cluster is related to how firms manage their competitive advantages. It is formed by the following keywords: competitiveness, accounting firms, SERVQUAL, quality of consumer services, customer satisfaction and behavior intentions. This cluster has a more focused discussion in understanding how customer satisfaction and perception of service quality may be managed as intangible assets in order to create competitive advantages (Armstrong and Smith, 1996). Bean et al. (1996), for example, found results indicating that one-to-one communication, pricing and customer satisfaction directly impact customers' choices, thus being a way to retain current customers and to attract new ones.

Given the great competition in accounting context, other variables were studied to understand how to reach competitive advantages in this sector. From customers' point of view, the accounting firms' market share can indicate the quality of service delivered. This statement can explain why the performance of international accounting firms is better than non-international (Lee, 2013).

In order to identify factors that impacts customers' choices, studies measure quality perception based on SERVQUAL variables. For Armstrong and Smith (1996), there are intangibles (e.g. reputation and professional quality) and external factors (e.g. word-of-mouth and employees' behaviors). For Keng and Liu (1998), to choose an accounting audit firm, it is relevant the reputation, the audit fees charged and the other services provided. In line with this last one, Lee (2013) argue that given the last years changes in customers' demands, accounting firms needs to provide more analytical and consultant services. This can be a way to increase the competitive advantages.

5.2 Image and perceived value

The second cluster considers issues related to customers' perceptions and expectations about the firms. The main keywords are consumption behavior, perception, corporate strategy and corporate image. Papers in this cluster usually focus on understanding service quality via the analysis of customers' opinions (e.g. Aga and Safakli, 2007; Cameran et al., 2010; Lee et al., 2016). Overall, our review indicates that long-term relationships between accounting firms and its customers may be relevant for service quality, indicating a relation between satisfaction and customer loyalty. Moreover, the perceived quality affects corporate image of the accounting services provider, what could be relevant to explain the willingness of the customer to recommend the firm for other potential customers (Cameran et al., 2010; Fleischman et al., 2017).

Since service quality literature was developed (Gronroos, 1984; Parasuraman et al., 1988), consumer expectations and perceptions are a key point to capture higher level of quality delivered. In accounting context, this is not different. For Bean et al. (1996), accounting consumers' expectations are linked with satisfaction and quality of the last service provided. If those expectations are met, the image of the firm is positively impacted. According Keller (1993), “image” refers to the perceptions of a company reflecting the associations presented in the consumer's memory. Corporate image may impact customer satisfaction about the service (Aga and Safakli, 2007; Cameran et al., 2010).

In literature, the relationship between service quality and firm's image can be seen as a cycle. The more quality the service has, the better the company's image will be perceived (Bean et al., 1996). On the other hand, the better image the company has, the perception of quality will be higher. To explain this second phenomenon, it is important to treat the service provider image as a mediator of the relationship between the perception of functional/technical quality and overall service quality (Fleischman et al., 2017).

5.3 Knowledge and professionalism

Finally, the third cluster considers accounting services characterized as KIBS. The relevant keywords are professional services, audit firms, small firms and interpersonal communications. Studies like Freeman and Dart (1993) and Olorunniwo and Hsu (2008) argue that the exchange of information and knowledge among the firms that provide accounting services indicate the need for better interpersonal communication between them and their customers. In addition, service coproduction and the constant need for innovation are features of the accounting services.

In professional services as accounting, the communication between services providers and customers might generate better technical and processual quality. Consumers highlight different points about communication that are linked to the accountant's knowledge and professionalism. For example, as the willingness in responding client's questions about the service, to inform about laws and regulations and the capacity to understand the customer's point of view (Sarapaivanich and Patterson, 2015). Therefore, these aspects highlight the accountants' necessity to have a good technical knowledge aligned with communication ability.

Another point about professionalism and knowledge is the level of specialization of the service provider. Companies from different industries have different regulations and specificities. Thus, there is a demand for highly specific knowledge about the client's industry. Keng and Liu (1998) argue that one of the most important reasons for choosing an audit firm is its level of industry specialization.

6. Discussion

Taken together, our results indicate that there are several research opportunities for studies that are focused on accounting services quality. Most of the papers were published in areas like services management, and the literature still lacks theoretical development about the relation between specific factors that may be relevant for the perception of quality for accounting services providers.

Although many accounting services providers exist around the globe, only 22 papers attempt to consider this type of specialized service, despite its importance (Aga and Safakli, 2007; Bean et al., 1996; Lee et al., 2016; Groff et al., 2015). Papers are usually discussed more on the “services” field, and not in accounting Journals. It may be relevant for accounting researchers to develop studies in order to better understand how accounting services are perceived and how this perception is affected by multiple factors.

Our results also indicate the presence of three main streams in accounting service quality: (1) competitiveness, (2) image and perceived value and (3) knowledge and professionalism. These three themes highlight different lens and levels to understand the perception of quality in accounting services.

First, relationships and comparisons between accounting firms can improve quality perceptions of delivered services. Market share, services' price and communication one-to-one are important to choose the service provider (Armstrong and Smith, 1996; Lee, 2013). Thus, delivering quality to market is not only important for retail sector, in accounting services this is also considered. The management of an accounting firm (or office) and competition can generate opportunities to improve our knowledge in this area. We noted that none of the 22 papers investigated considers a comparison between different accounting sub-areas. It is important to understand the different ways to manage quality in accounting, audit, non-audit or tax services. In addition, there is a lack of case studies about accounting firms' successes and failures and how digital tools implementation can impact the quality of the services. It would be useful the development of conceptual models for managers in accounting firms (or offices).

The second issue is related to the customers' perceptions and corporate image. There is a main discussion about the perception of quality and how it can improve customers' satisfaction and loyalty. Accounting firms' image is also important to generate a better perception about service quality (Aga and Safakli, 2007; Cameran et al., 2010). While client focus is widely explored in marketing- and services-related literature, there is a lack of discussion among the accounting scientific community. This can be demonstrated by the fact that accounting service quality papers are mostly published in non-accounting journals. There is an opportunity to generate a theory that explores services quality, from the initial contact with the client until after the provision of services. In addition, previous studies captured perceived service quality using general models as SERVQUAL (Parasuraman et al., 1988). With a better understanding about how clients behave, there is a possibility to create new service quality measurement models based specific accounting clients' perceptions.

Finally, the third issue is accounting firms as KIBS. We can investigate the quality of accounting services looking for professional features of these firms. There is a need for innovation and constant investments in training employees. Technical knowledge is an important characteristic of the accounting services industry (Bakre, 2006). Thus, our findings indicate the need for a greater focus on accountants' education. For example, accounting and auditing Standards change constantly. Even though it is a relevant subject for accounting firms as KIBS, accountants' education was not the central point of any of the 22 articles investigated. A better understanding about accounting education providers and their organization might contribute to a better perception about the development of professional skills in order to achieve their learning outcomes.

In addition, there is an ongoing discussion about changes in services features and how a portion of accounting services may be digitalized and automated (Lee et al., 2016). If competition increases, it may be relevant to study how clients perceive quality (Fleischman et al., 2017). There is still a lack of a theoretical base developed specifically for accounting services. Most of the literature is based on broader theories related to services quality (e.g. Aga and Safakli, 2007; Lee et al., 2016). It would be desirable that accounting services could be studied more specifically, benefiting from other areas that study KIBS.

The central issue to be explored is a better understanding about the role of the clients in relation to the provision of accounting services. According to our systematic literature review, clients have been treated secondarily, despite their relevance. It appears that there is still a myopic view of the literature about accounting services, considering only the service itself, disregarding certain external elements, like the client. Thus, the development of theories and methods for measuring accounting services quality, considering the client centricity in the process, is an important contribution to the accounting area. Accounting professionals can be best trained and prepared to delivery results expected by clients, benefiting everyone: accountants, clients, market and society. This has been the quality role of services in many areas, including accounting.

7. Conclusions

In view of a dispersed literature with different results, our study aimed to review and organize the accounting service quality theme, creating a path for the development of a main theory. We found 22 papers in scientific journals from Scopus and Web of Science databases. Our study leads to the conclusion that accounting service quality is more explored in other scientific areas such as service management and marketing. Even though there are three clear streams divided into competitiveness, image and perceived value and knowledge and professionalism, the accounting service quality theory needs to be further explored and well developed by accounting researchers.

7.1 Research agenda

Given this need for further exploration in the field, we identify several research opportunities in order to contribute with the area improvement:

Success and failures of accounting services providers: there is a need to develop more studies in order to understand the business phenomenon behind the provision of accounting services. Although some studies have focused on factors that impact client perception, we have not identified any work that explored management strategies. Research can be developed focusing on the determinants of successes and failures by accounting services providers, using primary or secondary data. For example, considering the ability for professional accountants to manage their own businesses. In this stream of research, entrepreneurship theories, such as innovation theory, may be applied.

Client centricity in accounting services: in services quality theory, clients' perceptions about the firms are important (Cronin and Taylor, 1992). One of our clusters identify “corporate image and perceived value' as a key theme for accounting service quality. Studying the relationship between clients and providers might reveal new knowledge about accounting as a business and could contribute for more discussions about client-centricity in accounting services. Qualitative research, as case studies, can help to achieve new theories about the accounting services with this marketing approach. Further, quantitative studies with primary and secondary data can validate the proposed theories or hypotheses.

Digital accounting services: it is important to understand which type of service is being digitalized/automated and how digitalization will require new skills and bring an impact on the future of the profession. There is an open question if digital accounting services will increase competition and its effects on pricing. Understanding the client of digital services is a key to study factors that are relevant for quality perception. Qualitative research may contribute to identify potentially relevant factors for clients' perceptions, leading to quantitative designs in order to confirm the new proposed theoretical understanding about accounting digital services quality. Management theories may be relevant as a starting point for this research stream.

Services quality and accounting education: as discussed before, accounting services are characterized as KIBS. Thus, the service depends on employees' technical knowledge and training. As such, we could benefit about a better understanding on how accounting education considers (or not) services quality. The perceptions from professors and students may reveal how services quality is treated in accounting education programs in order to prepare current and future professionals. Future research may be focused on identifying challenges to be discussed in accounting as a discipline or within an educational framework.

Investigation of service quality in different types of accounting services: there are a range of sub-areas in accounting such as auditing, managerial and tax services. We have identified previous studies in some of these sub-areas, but none has compared the perception of quality considering their specificities. Thus, differences among sub-areas of accounting services could be explored in order to improve services quality theory that considers the range of accounting services.

Development of an accounting services quality theory with a measurement model: overall, there is a need for a theory designed for accounting services quality. The literature, so far, indicates an initial relevant path. However, prior papers are based on general theories and exploratory studies. The first step would be to identify quality attributes for accounting services. Qualitative research, based on interviews and focus groups, may be useful for identifying the attributes for subsequent empirical testing. The attributes may lead to the development of a specific measurement scale, resulting in an applied theory to accounting services quality.

Taken together, this research agenda shows how accounting services quality is relevant and is an emerging topic that demands future research about accounting professionals' skills, their activities and how their clients perceive quality in an environment of constant change.

7.2 Implications and limitations

Our research provides several contributions and implications. In theoretical terms, our results present an overview of a theme still little explored in accounting field. The cluster framework demonstrates current approaches in order to organize the accounting service quality streams. Further, the research agenda aims to contribute with the evolution of this research field, providing some gaps still not explored by accounting researchers. Given that, it is possible to stimulate new studies in order to create a more robust discussion about service quality in accounting literature.

In practical terms, we highlighted the importance in considering the service quality management in accounting firms. Given the current changes on services because of the digitalization and the increased market competition, it is important to generate strategies in order to meet customer expectations. In addition, by generating a more organized discussion and presenting the mean themes of the accounting service quality (knowledge, professionalism, competitiveness and image), it creates a perception of what need to be taken into account by audit and accounting firms to improve their quality management.

Although the results of our research may have several contributions, we also highlight some limitations. First, despite covering many scientific journals, our choice for using Scopus and Web of Science databases may provide some level of bias. New literature reviews could be preceded using different databases in order to find papers published in journals not covered in this current review. On the other hand, it is important to highlight that Scopus and Web of Science are the currently most important databases in the field. Second, given the objective of this study, we did not make a deep comparison of accounting service quality with other types of services. Further studies could make a literature review about service quality covering different types of KIBS to compare the results presented in literature about these services. This will be useful to provide discussions about the differences and similarities of these services in quality management perspective.

In sum, the path suggested by our study is the first step toward the construction of the accounting services quality theory. New gaps may arise with the topic increasement, as well as publications in accounting journals.

This research was supported by Brazilian National Council for Scientific and Technological Development (CNPq/Brazil), project 304209/2018-0, by Foundation for Research Support of Espírito Santo (FAPES/Brazil), projects 84513772 (599/2018) and 85395650 (228/2019), by Portuguese Science Foundation (FCT/Portugal) through NECE (Núcleo de Estudos em Ciências Empresariais), project UID/GES/04630/2020 and by IFTS (Instituto Fucape de Tecnologias Sociais), project 2018-2021.