This study aims to dispense a concrete and coherent picture on the role of digitalization of accounting information (DOAI) among the small and medium-sized enterprises (SMEs) through a statistically reliable and parsimonious paradigm for procuring the impact of DOAI on sustainable innovation ecosystem (SIE) and public value (PV) generation. With this cue, the geographical scope of this tentative manuscript was framed in SMEs of developing countries.

A three-pronged methodology was disposed in this research, namely, literature review, expert interviews and self-administered survey. Qualitative data was procured from a series of semi-structured in-depth interviews. The quantitative data was drawn on a self-administered survey in which the closed-ended questionnaires were conveniently circulated to a cross-sectional sample of 583 respondents. The data captured from quantitative approach was processed and analyzed via covariance-based structural equation modeling with AMOS 26.0.

The outcomes analysis highlighted that there were significant positive associations between the hypothesized constructs regarding significance and effect size. These interlinks were also partially mediated through the mediation of quality of information on financial reports and SIE.

This research was bounded by geographical provenance emphasis on one country and relative smallness of the data set procured through anonymous survey-based approach drawn from a convenient sample of digitally savvy respondents working in one sub-sector resulted in the reduction in the robustness and generalizability of the observations. Nevertheless, these above-mentioned limitations could thus offer the starting points for novel avenues creation for the future research.

The practitioners would definitely have valuable benefits from in-depth insights on the obtained findings. Concretely, as lifting the degree of understandings on the magnitude of long-term cooperation and superior coordination within the SIE would enable practitioners to enlarge their business viewpoints to better cope with the challenges of complicated business settings, facilitating them to co-create PV for all their key stakeholders through giving priority to implementing DOAI.

Society could benefit from this study if policymakers and the influencers of government focus on innovative features and assure the possible environment for innovation deployment through embarking on introducing policies that would facilitate the digitalization as well as stimulate and incentivize establishing the SIE for PV generation. It would be good for both the SMEs and society when SMEs could thrive in community settings as well as this togetherness.

Unpacking the potential of DOAI has been considered as the promising research avenues that are outlined not only to redress the shortfall in the research stream in relation to the digitalization among SMEs but also provide the right directions for sustainable development among SMEs.

1. Introduction

The advent of digital technologies has had a profound impact on the innovation practices of enterprises (Teece, 2018; Nambisan et al., 2019). In particular, the increasing permeation of digital technologies has recently revolutionized how organizations have conducted business, formed connections with customers and other stakeholders (Bresciani et al., 2017; Scuotto et al., 2020) and boosted customers’ value creation (Matarazzo et al., 2021). Simultaneously, convergent globalized characteristics, namely, digital transformation, universal interaction and sustainability, have offered momentum to an exponential evolution in innovation (Costa and Matias, 2020). Therefore, small- and medium-sized enterprises (SMEs) have needed to engage in organizational changes to find an effective answer to the changing technological landscape to ensure their survival (Bos-Brouwers, 2009), sustainability and public value (PV) creation.

From the perspective of the sustainability systems paradigm (Williams et al., 2017), sustainable innovation has been considered a difficult goal to handle and reach in isolation, and hence, collaboration with other relevant entities has been demanded so as to constantly generate valuable offerings for consumers (Desouza et al., 2008; Anttonen et al., 2013; Cappa et al., 2016). The coherent emergence of innovations also raised an urgent call for a dynamic and sustainable ecosystem (Reynolds and Uygun, 2017; Gan et al., 2019; Granstrand and Holgersson, 2019; Boyer, 2020) in which innovations would be formed and operationalized as a consequence of the collaboration and cocreation among various actors (Costa and Matias, 2020).

In this regard, a sustainable innovation ecosystem (SIE) has been deliberated as an ecosystem in which the collaborations between the internal departments of organizations and external organizations have been assumed to play a strategic role. In the framework of an SIE, these actors commonly target tackling social and environmental sustainability matters through their innovative operations (Stubbs and Cocklin, 2008; Evans et al., 2017). This rests upon sustainable development comprising ethical, social, economic and environmental rules to support endurance, locality, locality, property and dynamic effectiveness and environmental hardships decline. SIEs have thus promoted productivity, as well as organizational efficiency and effectiveness (Smorodinskaya et al., 2017).

Multistakeholder collaboration has resulted in the recommendation of formal and informal exchanges of information to carry out joint practices, facilitating the coordination of actions (Oliveira-Duarte et al., 2021). As information is considered as a basis for taking actions to handle conflicts, reducing uncertainty and making decisions (Hall, 2011; Meiryani et al., 2019), information systems have been widely acknowledged as one of the most relevant components in the current environment. Of these, the accounting information system (AIS) is a subsystem of an organizational information system that allows an organization to supply useful information (Saeidi, 2014; Patel, 2015). As an integrator of the organizational information system, the AIS has grown with information technology in a technical, structural and developmental sense. The remarkable contribution of the AIS lies in supporting organizations to address short-term matters in terms of expenses, inflows and outflows by providing information (Ismail and King, 2005; Meiryani et al., 2019) in financial reports (FRs). From a longer-term standpoint, the AIS has been valuable in acquiring the effective functionality of firms in dynamic and aggressive environments to integrate operational strategies. This was because an improved quality and quantity of information was obtained, and users could make more effective decisions (Romney and Steinbart, 2009). As the AIS has played a paramount role in facilitating and composing organizations’ operations, and supporting them to reach their organizational goals with a great level of control (Kanakriyah, 2020), an urgent demand has been raised on how to set up, arrange, sustain and protect the AIS (Susanto, 2013a). In this regard, digitalization implementation in the AIS could be considered the best solution for the sustainable development of SMEs.

As the complicated interplays between digitalization of accounting information (DOAI), quality of information on financial reports (QIFR), SIE and PV have been predicted to become a novel topic that has entered the sights of innovation research, the comprehensive understanding of this multidimensional interconnection will become paramount. It will enable academics and practitioners to illuminate how enterprises can adapt and integrate digital technologies into their operations, understand how they can manage to succeed in sustainable innovation through implementing digital-based innovations and evaluate the extent to which digitalization could become a greater driving force of PV generation. Therefore, the prime objective of the present study was to delve into the SIE establishment and PV creation of SMEs through DOAI.

To this end, the observations of this study generate a myriad of salient contributions in both academic and practical aspects. From a theoretical viewpoint, this integrative theoretical model could act as a new category that is worth adding to earlier models to reenergize the attention on digitalization of SMEs in developing economies. As proposed by Kraus et al. (2019), the relevance of the subject and related works in terms of digitalization have been documented in several publications in recent years. While the recent flood of academic research on digitalization and digital transformation have offered much necessary clarity, they have been predominantly directed toward large-firm settings (Eller et al., 2020), large corporations (Cenamor et al., 2019) or digital startups and high-tech giants in the context of innovative businesses (Ghezzi and Cavallo, 2018), while particular research concentrating on SMEs operating in traditional industries have been relatively sparse (Matarazzo et al., 2021) regardless of their important roles in economic growth (Priyono et al., 2020; Ardito et al., 2021; Wengler et al., 2021).

Moving to the central contribution of this study, as has often been highlighted, the assimilation of the goals of accounting with the use of modern information technology initiated the creation of the AIS (Chidoko, 2014; Ekpung, 2014; Danbaba et al., 2016; Marshal, 2017; Mušić, 2017; Al-Fatlawi, 2018; Chen et al., 2018). This work initiates a starting point for a conceptualization of DOAI in SMEs by yielding a deeper understanding of its originality and utility and advancing the understanding of the focal concepts and the interrelationships between DOAI and other components. DOAI is considered the advanced form of the AIS that reengineered processes to allow the implementation of the AIS to become more tailorable, malleable, flexible and responsive. DOAI could, therefore, boost the efficiency and effectiveness of the AIS, and thus offers opportunities for SMEs to modernize management and engagement with their stakeholders.

QIFR has drawn concerns from the academic and practitioner communities, as the efficiency and effectiveness of numerous economic decisions of various groups in the market rest heavily on it (Assad and Alshurideh, 2020). High-quality information would enable managers to comprehend an organization and realize the shifts emerging both inside and outside the organization so that they could respond rapidly and accurately to those shifts (Susanto, 2013b).

Based on the work of Wongsim and Gao (2011), the application of the AIS has positively impacted QIFR. Building on extant digitalization literature and a cumulative body of knowledge related to the AIS and QIFR in SMEs, this research adds value to the constrained literature available on emerging trends related to the intersection of enterprise reporting and digital technologies (Lombardi and Secundo, 2020) by illuminating the potential impact of DOAI on QIFR. In doing so, the present study contributes to the knowledge on the integration between advances in digital technologies and demonstrates that AISs could generate efficient and effective measures to enhance the QIFR of SMEs in several aspects, namely, relevance, faithful representation and enhancing qualitative characteristics. Indeed, digitalization has opened innovation opportunities for innovators, creators and organizations (Yoo et al., 2010; Nambisan, 2017; Ramaswamy and Ozcan, 2018) to broadly adopt smart and digital technologies (Nambisan, 2017; Nambisan et al., 2017). Data procurement and processing of enterprise information have become simplified and enabled organizations to fulfil their reporting requirements (Lombardi and Secundo, 2020).

Despite the existing literature drawing growing concerns about digitalization and innovation ecosystems, there has been little light shed on how digitalization could drive enterprises to develop an SIE. Simultaneously, a lack of effort has been devoted to an in-depth investigation of the interplay between information systems and sustainable innovation practices in business environments (Cillo et al., 2019), although information systems have played an important role in sustainable business processes and practices through minimizing logistics expenses, enabling virtual collaboration between distributed groups, revamping cooperative understandings management and conditioning organizational processes (Watson et al., 2010). The present study’s integrative theoretical model could be used to motivate future exploration of how digitalized internal processes could result in SIE achievement. The present paper broadens extant research by being more perspicuous about the impact of DOAI on SIE achievement by deriving a lean and concrete prototype, particularly for SMEs, differing from other works on digitalization in SMEs. Multistakeholder collaboration has resulted in the recommendation of formal and informal exchanges of information so as to carry out joint practices, facilitating the coordination of actions (Oliveira-Duarte et al., 2021). DOAI has enabled SMEs to share useful information throughout the operational phase to intensify efficiency for all actors involved (Bagale et al., 2021) within the ecosystem. DOAI could result in the formulation of communities and community interaction and broader stakeholder integration to offer new perspectives on SIEs.

Moving beyond the perspective that PV creation stemmed from public sector organizations only, this research considered a pioneer’s view of PV that is generated by SMEs in developing countries. Indeed, digitalization could gain convenience and efficiency while also lowering costs, in concert with more sustainable ways of living, ultimately providing more balanced value propositions (Patrick and Patrick, 2020). Digitalization in SMEs would support this type of enterprise to achieve sustainability, resource and energy preservation and ameliorate productivity (Kagermann et al., 2013). By doing so, DOAI also assists in enacting the connectivity of stakeholders across geographical boundaries and enables integrative PV creation. Coming back to the PV point of view, so far, little has been illuminated regarding how SIE achievement could empower PV creation. With this in mind, this research further advances knowledge by offering an empirical investigation of how an SIE could facilitate SMEs’ capacities to address the challenges of PV creation in the context of digitalization.

The outcomes of AIS are FRs, which are used to supply information for paramount economic decision-making (Assad and Alshurideh, 2020; Mohamed et al., 2020). This study’s observations broaden existing frontiers of knowledge by offering a new stream of multidisciplinary work at the interconnection of QIFR, SIE and PV among SMEs. In particular, this research can broaden scholars’ horizons in terms of QIFR and SIE. The high QIFR this research could enable could thus enhance productivity, encourage innovation (Kieso et al., 2018) and lead to a change in relations between suppliers, producers and customers. As the high QIFR would become helpful for the transformation of information among a wide range of groups in the market (Jerry and Saidu, 2018), it thus could act as a paramount component that impacts providers’ and stakeholders’ decision-making (Beest et al., 2009). This, in turn, could significantly affect in-depth collaboration for co-value creation in an SIE. Although PV has attracted attention from numerous scholars, there have been no promising studies investigating whether a high QIFR in SMEs would impact PV creation in a significant and positive manner. As such, this work is unique among the related literature because it highlights the association between QIFR and PV. A high QIFR would enable managers to sense the changes emerging both inside and outside the organization so that they could tackle those changes efficiently and effectively (Susanto, 2013b) to generate PV.

Coming back to the PV point of view, so far, little has been illuminated about how SIE achievement could empower PV creation. Keeping this in mind, this research advances knowledge by offering an empirical investigation into how an SIE could facilitate SMEs’ capacities to address challenges of PV creation in the context of digitalization. Sustainability-driven innovation comprises developing products or services that boost current welfare while efficiently and effectively distributing resources for both present and future generations (Maier et al., 2020; Boons and Lüdeke-Freund, 2013). Sustainable innovations would serve as catalysts for cleaner manufacturing, addressing societal challenges in both the short and long run that comprise economic and environmental goals in local and global facets (Costa and Matias, 2020). Nevertheless, sustainable innovation has been hard to reach within an individual organization; therefore, complementary collaboration with others to generate valuable offerings for consumers has been requested (Zeng et al., 2017). In this context, SIE has fortified productivity and organizational efficiency and effectiveness (Smorodinskaya et al., 2017).

Given that the extant literature has documented the failure of several past research in reaching their destination (Saldanha, 2019) due to a lack of guidelines, the role of digitalization, especially DOAI, could not be systematically presented and further empirical efforts have been hindered. The ambition of this paper, from a practical viewpoint, is to offer guidelines on how to manage and reach SIE establishment and PV creation through DOAI implementation. By doing so, the findings of this study could provide actionable practical insights and indispensable additional techniques for SME leaders to manage and implement these complicated interlinks and handle profound AIS changes, regardless of the barriers and challenges they face during operation, namely, a shortage of (financial) resources, technical skills and information (Rizos et al., 2016). The results of this research also have implications that could allow policymakers to promulgate stringent guidelines in terms of digitalization in accounting. Simultaneously, these obtained observations can also serve as a reference for policymakers and standard setters in promulgating instructions pertaining to management policies toward establishing and operationalizing an SIE in an efficient and effective manner, which, in turn, can enhance PV creation. Finally, the findings of this manuscript hint at helpful measures for information technology or software providers in launching modern techniques that best suit the growing demands of potential customers.

The remainder of this study is structured as follows. Section 2 takes a closer look at the main issues of this research by setting out the relevant theoretical principles and several base concepts. The hypotheses and research model are formulated in Section 3. Section 4 explains the methodology pertaining to the data procuring process, the measures establishment and the analytical technique. The empirical findings and key outcomes of this research are outlined in Section 5. Section 6 concludes with noteworthy implications and limitations and offers an agenda for future work.

2. Domain background

Based on the suggestion of a demand for a robust theory underlying the proposed measurement model prior to data analysis made by Bryant and Yarnold (1995), information processing theory (IPT) and stakeholder theory (ST) are demonstrated in this section. Subsequently, the conceptual framework is presented.

2.1 Theoretical backdrop

IPT. IPT has been extensively used in information systems (Wong et al., 2015) and technology integration (Stock and Tatikonda, 2008). This type of technology was considered to elucidate how information was collected, stored and retrieved (Çeliköz et al., 2019). Grounded in the assumptions of IPT, information-processing requirements and competencies should be demonstrated in a manner fit to achieve the highest productivity (Premkumar et al., 2005). Information-processing demands can be identified by a variety of environmental settings in which the entities are located, while information-processing competencies refer to the alignments of resources, technology architecture and other works that enable information gathering, processing and allocation (Tushman and Nadler, 1978). The deep insights on information processing could help an organization to comprehend customers’ demands, task commoditization and collective technologies (Chen and Lin, 2016). Prior works have also tended to identify digital technologies as the main facet of organizational information-processing capabilities (Li et al., 2020).

ST. Stakeholders could be identified as individuals, groups, organizations, institutions or societies (Mitchell et al., 1997) that could impact or could be impacted by the implementation of organizational goals (Freeman et al., 2010). ST served as a strategic management theory originating in the 1980s (Freeman, 2010) and has continued to evolve as a management model ever since (Mitchell et al., 1997; Freeman et al., 2010), and it was considered a gold standard for theorizing and administering complicated business and society associations. It has infiltrated mainstream management theory (Jones, 1995) and has acted as the cornerstone of numerous conceptual and empirical contributions to understanding the intersection of business and society (Parmar et al., 2010). ST’s key postulation is that enterprises target shaping functioning links with their stakeholders to operate legitimately and efficaciously (Parmar et al., 2010). The prime objectives of Freeman et al. (2010) were to provide managerial principles and instruments that could be used by enterprises with regard to their stakeholder links (Flak and Rose, 2005). These principles require open and thoughtful solutions from managers when handling organizational goals and undertaking the responsibilities of managers to definite stakeholders (Freeman et al., 2010). ST was the preeminent point of view in theorizing corporate sustainable development (Chan and Oppong, 2017), as there would be a myriad of paramount information captured from stakeholders for enterprises’ sustainable development achievements (Jones and Wynn, 2021). As such, ST has transformed from a simple and static theory focusing on stakeholder groups and their roles into a more dynamic and complicated associations-focused paradigm that combines interdependencies, conflicts and intergroup standpoints (Lock and Seele, 2016).

Nevertheless, in consonance with the explanatory tradition, these theories were used purely as sensitive devices in a flexible manner (Klein and Myers, 1999) rather than a rigid instrument for theoretical investigation (Effah and Nuhu, 2017).

2.2 Conceptual framework

DOAI. The AIS has been defined as an internal subsystem of an organization (Patel, 2015) that deals with gathering, delivering, analyzing, processing and classifying material and quantitative information (Laudon and Laudon, 2015; Nguyen and Nguyen, 2020) sourced from the financial transactions of enterprises’ businesses (Grande et al., 2011) so as to offer helpful information in terms of designing, supervising and operating a business. In light of the growing demands of stakeholders regarding their direct financial interests, high-quality financial information for making investment decisions has become increasingly crucial (Mancini et al., 2013). As a result, the current AIS has further incorporated approaches through which enterprises could prepare reports on environmental, social and governance activities for stakeholders (Kerr et al., 2015).

Digitalization revolves around the notions of connectedness, interfaces, openness, availability, variability and generality (Nambisan et al., 2019). Digitalization has been well recognized as a common term covering numerous technological developments, such as robotics, artificial intelligence, the internet and big data (Mezghani and Aloulou, 2019). Attributable to these modern information technologies, digitalization has become an enabler for creating, gathering and analyzing data for value generation (Björkdahl and Holmén, 2018). This approach drove the definition of DOAI as the way in which online and digital information adoption was implemented in a firm’s AIS for efficient and effective decision-making (Alnajjar, 2017).

QIFR. FRs have been considered historical and state-of-the-art financial information (Fabozzi and Drake, 2011) demonstrating how organizational operations are composed (Drake and Dingler, 2001). As such, FRs should feature high-quality information (Suharsono et al., 2020). The notion of FR quality is broad and comprises financial information, disclosures and non-financial information that is effective for decision-making (Tasios and Bekiaris, 2012). The concept of quality depends largely on the field and object of research (Ge, 2009). Accordingly, quality has been regarded as the fulfilment of customers’ expectations and the demands for generating satisfaction with a product or service (Sahney et al., 2004). Information quality in the accounting field is determined by the aptitude to meet the demands of managers to enhance understanding of the operational situation of the organization, support them in making decisions and monitor and implement strategic goals. Building on the proposal of Jonas and Blanchet (2000), QIFR hinted at the complete and clear financial information presented in FRs, and the purpose of offering information was not intended to confuse or change users’ decisions. QIFR considers the capacity of FRs to provide faithful representation and realistic information related to operational performance and organizational financial status (Tang et al., 2008). Grounded in the point of view of harmony between the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB), the overall objective of FR preparation is to offer useful financial information to present and potential investors, lenders and other creditors in decision-making in terms of the provision of resources to an organization (IASB, 2010).

SIE. An innovation ecosystem has been considered a deliberate community of economic factors co-developed for value configuration and competency leverage via collaborative innovation (Koenig, 2012). Innovation ecosystems energize the collective compromises that expedite enterprise to integrate separate supplies into customer-oriented operations to achieve a positive response of innovation value and productivity that no organization could have reached on its own (Adner, 2006). The fundamental focus of an innovation ecosystem is placed on the concurrent collaborative, competitive and coordinative network of a nucleus entity and its partners (Adner and Kapoor, 2010); the interconnections from the interenterprise understanding of hierarchical or collective associations (Dyer and Singh, 1998); the conversations on contextual determinants (Jacobides et al., 2006); value seizure through two-sided alliances (Teece, 1986); interenterprise vertical and horizontal collective relationships (Tomlinson, 2010); integration of upstream elements and downstream counterparts (Adner and Kapoor, 2010); and organizational exterior associations and networks (Love et al., 2013). However, due to the robust connection between innovation and solutions to problems, challenges remain in terms of complicated matters requesting structural alterations and cooperative subsistence, such as sustainable development. Sustainable development was defined as an energetic process of transformation, supporting current resource usage, investment accomplishment, the direction of technological and institutional modification and the welfare maximization of current and future generations [World commission on environment and development (WCED),1987]. In this regard, sustainable innovations would underpin sustainable development by performing as catalysts for enterprises to overcome societal challenges pertaining to economic and environmental goals in local and global scopes. Consequently, there is an urgent call for SIEs that includes higher institutions, research bodies, financial resources, expert knowledge and an inclination to cooperate on global issues. An SIE is an ecosystem that possesses numerous characteristics of conventional innovations. An SIE has been deliberated as an ecosystem in which the collaborations between the internal departments of organizations and external organizations have assumed a strategic role. In the context of a SIE, these actors commonly target tackling social and environmental sustainability matters through their innovative operations (Evans et al., 2017; Stubbs and Cocklin, 2008). Specifically, it rests on sustainable development comprising ethical, social, economic and environmental rules to support the achievement of endurance, locality, and locality, property and dynamic effectiveness and environmental hardship decline.

PV. The definition of PV is relatively broad (Chatelain-Ponroy et al., 2017), and PV is a multifaceted notion that has been reached by numerous methods (Rutgers, 2015). Concretely, the idea of PV was encouraged to stress public services delivery (Moore, 1994) and focused on society as a whole rather than a single client (Moore, 2000). PV can be identified through 72 values based on the suggestion of Jørgensen and Bozeman (2007). These values could be regarded as ideal perspectives when offering public services (Andersen et al., 2012). PV could also be broadly specified as a thorough way to contemplate public management and gain advancement in public services (Constable et al., 2008; Moore, 1995). Nonetheless, PV has been associated with, but something has been different with previous studies on PV (Van der Wal et al., 2013). The present research focuses on the notion of PV provided by Moore (1995, 2013) in light of a well-defined framework for identifying PV as the advanced management philosophy for all value in public entities (Douglas and Meijer, 2016). In this regard, the PV model comprises numerous dimensions, such as the operational competency dimension focused on the administrative, financial and technological capacities of an entity; the authorizing environment dimension concentrated on the democratic reinforcement and accountability of an entity; and value proposition placing an emphasis on intended social performance (Douglas and Meijer, 2016).

3. Hypothesized model construction and hypothesis establishment

3.1 Hypothesized model construction

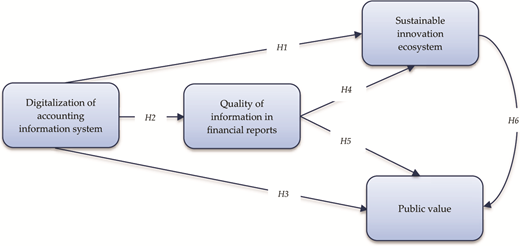

The interlinks between the four components of DOAI, QIFR, SIE and PV are presented in Figure 1.

3.2 Hypotheses establishment

Sustainable innovation has been broadly considered to be difficult to achieve within an individual entity, and hence, its attainment requires complementary collaboration with other related entities to continually bring out valuable offerings for consumers (Zeng et al., 2017; Anttonen et al., 2013; Cappa et al., 2016; Desouza et al., 2008). Such endeavors drive incumbent enterprises to become involved in establishing and operationalizing an SIE where collaboration mechanisms have become a key factor in sustainable innovation and system-wide value creation.

Multistakeholder collaboration has resulted in the recommendation of formal and informal exchanges of information to carry out joint practices, facilitating the coordination of actions (Oliveira-Duarte et al., 2021). As information has been considered a basis for taking actions to handle conflicts, reduce uncertainty and make decisions (Hall, 2011; Meiryani et al., 2019), information systems have been acknowledged as one of the most relevant components in the current environment. Of these, the AIS is a subsystem of organizational information systems that allows an organization to supply useful information (Saeidi, 2014; Patel, 2015).

The AIS has long been widely acknowledged to generate significant contributions to timely financial information for financial policy establishment and decision-making (Al-Kassawna, 2012). The effectiveness of the AIS lies in allowing an organization to achieve sustainable development during its operation (Huy and Phuc, 2020). Digital technologies have also been argued to contribute substantially to the achievement of organizational sustainable development goals (Seele and Lock, 2017) by unlocking the potential of environmentally sustainable processes (De Sousa Jabbour et al., 2018). As such, almost all enterprises have been encouraged to extend their digital technologies adoption to embed them into organizational processes for sustainable benefit accomplishment, especially in the AIS. By doing so, the AIS was believed to be more efficient and effective in assisting an organization in ameliorating work quality; developing associations between organizations, customers and stakeholders; addressing complicated matters; supporting the integration of all departments; and favorably competing in the market environment. Given that digitalization has been well regarded to cause a profound impact on organizations, upstream and downstream operations, networks and ecosystems (Iansiti and Lakhani, 2014; Jacobides et al., 2018), DOAI could play a paramount role in managing the interconnections and structures embedded in an ecosystem. DOAI also composes the internal information architecture to strengthen organizational information processing competencies and enables the exchange of information between SMEs and their members in an SIE to become efficient and effective. In doing so, DOAI could facilitate the efficient and effective allocation of resources, which, in turn, improve and enhance the potential advantages of SIE. Thus, the first hypothesis of the study is as follows:

DOAI has instigated a substantial positive effect on SIEs.

The information in FRs has been the most prominent component in organizational operations. This was because this type of information was wielded for organizational financial analysis, long- and short-term strategy determination and planning implementation (Slyozko and Zahorodnya, 2016). The application of the AIS has significantly increased the computing capacities and standardization of organizational practices and, hence, has resulted in the delivery of more accurate and timely information (Sánchez‐Rodríguez and Spraakman, 2012) and prompt FRs (Astrawan et al., 2016). In other words, the AIS has demonstrated a high impact on QIFR (Tawakal and Suparno, 2017). Notably, production planning and control decisions can be reinforced by digital technologies with efficient and effective information processing (Nguyen et al., 2018). It is evident that these technologies not only enable gains in efficiency and quality of accounting information, but also facilitate enlarging the scope of traditional accounting functions. Furthermore, these devices could determine abnormalities, autocorrect errors (Kogan et al., 2014), and drive auditor practices (Issa, 2013). Digitalization also offers traceability and visibility through real-time data gathering (Kane et al., 2015) and conducting data analysis in real time to supply advantages such as more rapid decision-making, loss-of-time prevention, and organizational performance enhancement (Hart, 2017). Based on these analyses, QIFR should increase when DOAI is implemented in an organization. Hence, the second hypothesis of the study is as follows:

DOAI has instigated a substantial positive effect on QIFR.

The success in generating benefits for economic operations and employment, social capital and cohesion, environmental performance (Benington, 2009) and access to knowledge (Bozeman et al., 2015) could be regarded as features of PV generation. Digitalization and technology-based resolutions have been considered a facilitator of service quality, arising from better resource allocation and more accurate information sharing for external and internal purposes (Abou-foul et al., 2020). Notably, increased information processing competency is the chief facilitator in revamping operational performance (Cao et al., 2018). DOAI could become an enabler to shape communities, directing numerous personal contributions and a multitude of other factors toward a common target and thus leveraging PV generation through spillover impacts on co-creation practices.

Whereas trust and legitimacy have been treated as symbols of PV creation (Talbot and Wiggan, 2010), quality-of-service delivery has been determined by advantages such as being responsive to requirements, accessible and favorable, and incorporating adequate stakeholder engagement (Al-Hujran et al., 2015; Benington, 2009; Spano, 2014). Information technology infrastructure has been argued to result in improved customer service performance (Wong et al., 2014). Digitalization has been converting ecosystems and value chains in numerous enterprises by altering the way in which these organizations interact across organizational boundaries upstream or downstream; improving supplier and consumer interactions; and gaining data acquisition, warehousing, big data analytics and data application capabilities (Porter and Heppelmann, 2015). These modern digital technologies could offer sufficient and timely information, enabling product or service optimization and requirement prediction to quickly respond to customers’ demands. Moreover, using DOAI for information processing, organizations can reconfigure resources and make financial decisions effectively for the production of customized products or services in a more flexible and effective manner.

Efficiency has been specified as the benefits offered by an entity that were assessed to be higher than the expenses of an organization (Talbot and Wiggan, 2010). Digitalization involves digital technology application to supply novel value- and revenue-creation opportunities. Digitalization also generates shared value and sustainable growth, and allows an organization to transform from maximizing short-term financial performance to prioritizing long-term economic and social responsibility (Porter and Kramer, 2011). The outcomes of DOAI could give rise to support for an organization to make decisions on requirement prediction, price optimization and product or service development, which could be helpful in meeting the growing demands of customers and thus increase market share and sales. Thus, the third hypothesis of the study is as follows:

DOAI has instigated a substantial positive effect on PV.

Insufficient information has been acknowledged as a serious matter (Bailey and Francis, 2008). This is because it could have a negative impact on organizational decision-making capacities (Boyle et al., 2009). All operations in terms of the environmental, social and economic aspects of an organization are determined as information-intensive actions. Thus, firms are considered to leverage both internal and external information to conduct operations. Of these, accounting information has been suggested to be used to assist users and stakeholders in making effective decisions (Gelinas and Dull, 2012). FRs are specified as a process of communicating organizational financial accounting information to external parties. In other words, suitable decision-making is affected by QIFR (Reginato et al., 2011). Any financial information is required to achieve such features as having faithfulness, being comparable, having verifiable timeliness and being understandable. These characteristics enable organizations to offer transparent financial information to their users and stakeholders, which allows them to make decisions and to reduce misleading or incorrect information (Gajevszky, 2015). Undoubtedly, information exchange based on high QIFR for stakeholders could allow an organization to succeed in all aspects pertaining to sustainable development in its ecosystem. Therefore, the fourth hypothesis of the study is as follows:

QIFR has instigated a substantial positive effect on SIE.

The success in generating benefits for economic operations (Benington, 2009) and quality-of-service delivery (Al-Hujran et al., 2015; Benington, 2009; Spano, 2014) could be regarded as features of PV generation. Undeniably, FRs are considered as advantageous instruments for all stakeholders to obtain true and objective information in the case that daily internal information and organizational reactions of operations are unreachable. Investing activities could not take place unless the financial information was accessible, as the available financial data would be used for planning, analyzing, evaluating and decision-making. Given that trust and legitimacy are treated as symbols of PV creation (Talbot and Wiggan, 2010), the information in FRs accompany a culture of great influence on government policies, which are assumed to be the practical accomplishment of reliable and trustworthy FR information (Hashim, 2012). More importantly, a high QIFR could help both users and stakeholders save agency costs to acquire highly accurate and reliable information. To put it simply, efficiency can be reached from a high QIFR. Therefore, the fifth hypothesis of the study is as follows:

QIFR has instigated a substantial positive effect on PV.

An organization that values operation in the area of sustainable development would shape close connections with its main stakeholders, namely, the government and financial community, which would help ameliorate the organizational operating environment in numerous ways due to the paramount resources provided by these groups of stakeholders (Alchian and Demsetz, 1972; Cornell and Shapiro,1987). This would result in reaching tangible advantages for sustainable organizations in terms of protocols for encouraging stakeholders to devote inputs to the organization (Funk, 2003; Peloza and Papania, 2008). An organization that places an emphasis on SIE creation might acquire ameliorated staff productivity by attracting and retaining better-skilled and more-dedicated employees. Appropriate performance in the field of SIE would enable an organization to revamp its organizational performance and enhance its ability to reach sources of capital. This type of organization could be considered less risky for investment because of its extraordinary management skills and decreased information risk in light of exact environmental and social disclosures. This could also lead to more loan contracts with lower average costs of capital (Nandy and Lodh, 2012). Notably, an SIE could allow an organization to reduce economic expenses and increase the economic value of their product or service. Building on these analyses, intensified SIE could lead to PV creation. Thus, the sixth hypothesis of the study is as follows:

The SIE has instigated a substantial positive effect on PV.

4. Material and methodological attributes

A survey research design was conducted to capture data from SMEs in Southern Vietnam. The sampling procedure, data collection, ethical considerations and the constructs measurement are depicted in detail in the following subsections.

4.1 Item generation and content validity

Item generation and measurement. A literature survey was initially performed with the aim of determining the measurement scales that have been used in previous works with the same focus. Back-and-forth translation processes were conducted as a starting point for the Vietnamese survey. Accordingly, original English items were translated to Vietnamese after a procedure of translation and back-translation (Brislin, 1970).

Based on the literature review, a variety of items for each construct were determined to set up the draft questionnaire. The five-point Likert scale with anchors ranging from strongly disagree (1) to strongly agree (5) (Malhotra, 2004) was applied for all items in the questionnaire to evaluate the participants’ points of view (Burns and Grove, 2009).

DOAI. In the present research, the AIS was defined to comprise four elements: a data input system, data processing system, data storage system and financial statement system. Accordingly, DOAI could be equated with these four elements being integrated with digital technology. In line with a prior study using a DOAI measurement scale (Mutoharoh and Buyong, 2020), the measurement scales for DOAI were adopted from the work of Lim (2013) and Taskinsoy (2019) that were applied in the research of Mutoharoh and Buyong (2020) and combined with the contribution of Uyar et al. (2017) for the data input system items, Romney and Steinbart (2006) and Sori (2009) for the data processing system, Sajady et al. (2008) for the data storage system and Sori (2009) and Uyar et al. (2017) for the financial statement system.

QIFR. The measurement scales of QIFR were based on the extensive approach of the FASB and IASB (2010) framework, which concentrated on the three components of relevance, faithful representation and enhancing qualitative characteristics. Relevance was evaluated on the two subscales of predictive value and confirmatory value; faithful representation was assessed on the three subscales of complete depiction, neutral depiction and free from error; and enhancing qualitative characteristics was gauged by the four subscales of comparability, verifiability, timeliness and understandability.

SIE. According to Costa and Matias (2020), sustainable innovation largely rests on sustainable development, comprising social, economic and environmental principles. In sustainability-oriented innovation ecosystems, innovative activities are carried out by actors to tackle social and environmental sustainability issues (Evans et al., 2017; Stubbs and Cocklin, 2008), as well as economic sustainability matters. Keeping these analyses in mind, the criteria applied to measure SIE were based on three primary aspects: the economic aspect, environmental aspect and societal aspect. The criteria applied to evaluate the economic aspect were referenced from the works of Wagner (2010), Chen (2008), Markatou (2012), Messeni Petruzzelli et al. (2011), Berrone et al. (2013), Ketata et al. (2014), Shuaib et al. (2014), Basso et al. (2013), Aguilera-Caracuel and Ortiz-de-Mandojana (2013), De Marchi (2012), Dong et al. (2014), Li (2014) and Lin and Ho (2008). The items for measuring the environmental aspect in this study were formulated from Chen (2008), Antonioli et al. (2013), Cheng et al. (2014), Ketata et al. (2014), Shuaib et al. (2014), De Marchi (2012), Dong et al. (2014), Li (2014) and Lin and Ho (2008). The criteria that were used to evaluate the social aspect were based on those of Chen (2008), Cheng et al. (2014), Shuaib et al. (2014) and Li (2014).

PV. The scales for assessing PV were built on the summary of the proposed PV measurement dimensions in Faulkner and Kaufman (2017). As such, the criteria used to measure PV comprised outcome achievement, trust and legitimacy, service delivery quality and efficiency (Faulkner and Kaufman, 2017).

Prior to beginning the main survey, several steps were carried out to ensure content validity and construct reliability.

Content validity. For assurance of the validity of the construct assessment and quality of questionnaire improvement, a pilot study and pre-test were implemented prior to the mass distribution of the main survey (Cao et al., 2011). The questionnaire was piloted with the involvement of several experts in reviewing the questionnaire for structure, readability, ambiguity and completeness (Dubey et al., 2019). Subsequently, a pre-test consisting of 30 respondents was conducted to corroborate the questionnaire and assessment instruments as recommended (Kothari, 2004). The reliability of the instrument was measured by calculating Cronbach’s α value (Kim and Feldt, 2008; Hernaus et al., 2012). The results analysis revealed that Cronbach’s α values were greater than common suggestions for exploratory research, demonstrating a satisfactory degree of reliability (Nunnally, 1978; Hair et al., 1998). Hence, the final form was adopted for the main survey.

4.2 Sampling strategy

Target population. Data were captured with two sampling units. The fundamental sampling unit was organizations, and organizational employees was the secondary sampling unit. The selected organizations in this research were SMEs in Southern Vietnam. These enterprises were commonly selected in several previous studies on innovation implementation (i.e. Nguyen and Wongsurawat, 2012; Hoang and Otake, 2014), as the southern areas have been considered the most dynamic areas in Vietnam. More instrumentally, from the standpoint of Ha et al. (2021), innovation implementation tended to be adopted within SMEs located in Southern Vietnam more rapidly and effectively than other areas of Vietnam. This was because the formation and development of SMEs in Vietnam originated in the late 19th century in Southern Vietnam when these regions were under French colonial rule (1884–1945). Against this backdrop, the growth of SMEs became more pronounced between 1954 and 1975; however, this was primarily in South Vietnam, as private enterprises could not be established and operationalized in the North, in which the economy was centrally planned. Nonetheless, the reunification of North and South Vietnam in 1975 resulted in the application of the North’s system and the prompt nationalization of all private firms. As such, each region still possesses different idiosyncrasies, particularly in innovation deployment (Doi, 2020), even though economic development throughout Vietnam has been nearly the same (Ha et al., 2021). This has induced discrepancies in motivation, perceived success determinants and business matters for entrepreneurs in disparate areas (Benzing et al., 2005). Accountants in SMEs were determined as the target informants of this study because they were well regarded to directly take part in the creation, assurance, publication and analysis of FRs. Adequate understanding and awareness of digitalization in terms of accounting was set as another basis for participant selection. In other words, the respondents were required to answer all of the questions in relation to this subject. As such, respondents who could not meet the demands were excluded from the dataset. This approach has been broadly used in numerous previous works (Abbasi et al., 2016; Akter et al., 2016; Ghasemaghaei and Calic, 2019).

Sampling adequacy. The quantitative approach, which has been acknowledged as a deductive research instrument for applying measurement and sampling techniques (Hair et al., 2010) to procure data, was considered the most suitable to examine the proposed model. A survey was also applied in this research due to its advantages (Bryman and Bell, 2011). Additionally, cross-sectional data were captured with non-probability convenience and snowball sampling approaches. The questionnaires were circulated in person to respondents (Lee, 2013) by the researchers, as this would provide the chance to inform the anonymity and confidentiality of the outcomes of the research, as well as minimize common method variance (Podsakoff et al., 2003). Building on the sample size criterion of an a priori sample size calculator for structural equation modeling (SEM) (Soper, 2015), a recommended sample size of 569 was obtained from the inputs of 90% desired statistical power degree, 53 observed variables, seven latent variables, 0.05 probability degrees and an expected medium effect size of 0.3. A vital sample size of 200 has been commonly proposed by numerous scholars (Sivo et al., 2006; Hoelter, 1983; Loehlin, 1992). The questionnaire distribution process took place over a five-month period from January 2021 to May 2021. Ultimately, 583 completed responses were acquired, achieving a response rate of 89.69%. Thus, the sample was considered representative of the general population in the target region.

Tests for potential bias in survey data. As this study relies on individuals to conduct the final analysis, the potential for common method bias (CMB) impacting the results needs to be addressed (Podsakoff et al., 2003). Building on the assumption that the viewpoints of late respondents bear a resemblance to non-respondents without follow-up attempts (Brusset and Teller, 2017), non-response bias was evaluated by completing a t-test on the scores of the early and late waves of the returned questionnaires. As such, respondents were split up into two subgroups of 291 responses at the beginning of the data collection period and the remaining 292 responses at the end of the data collection period. The t-test results revealed that there were no significant differences between the two groups, suggesting that non-response bias is unlikely to be a major issue.

4.3 Ethical consideration

Accountants from SMEs in Southern Vietnam were recruited from January 2021 to May 2021 after obtaining approval from their organizational leaders. Participation was established on a voluntary basis, and no financial incentive was provided. Building on the ethical issues proposed by Bryman and Bell (2007) and Saunders et al. (2012), a requirement of complete understanding of the content of the questionnaire cover letter illustrating the main aim of this research was set for participation. The participants were assured that their feedback would be anonymous, confidential and voluntary. Consequently, the collected data were processed confidentially and anonymously and will never be used for any purpose other than this study.

4.4 Statistical analytics technique

IBM SPSS 26.0 software was used to summarize the participants’ sociodemographic backgrounds, and AMOS was used to assess the fitness of the hypothesized model with the data and parameter estimates. Maximum likelihood estimation was also used for the research model’s parameter estimation, wherein all analyses were performed on variance–covariance matrices (Hair et al., 2010) due to their property of preventing violation of the normal distribution assumption, at least for large samples (Golob, 2003). A two-stage procedure was used in the measurement and structural model (Hair et al., 2010; Leong et al., 2013). Specifically, the measurement model was examined in the first stage, while the structural model was assessed in the second phase to assure that the measurements of all components were valid and reliable before drawing conclusions on the characteristics of the interconnections between the constructs of the proposed model (Okyireh et al., 2018).

5. Presentation of research analysis

The results analysis of the two-step approaches recommended by Anderson and Gerbing (1988) by applying SEM to investigate the model and hypothesized interlinks proposed in this study are depicted in detail in the following subsections.

5.1 Demographic profile of respondents

Sample characteristics demonstrated that the sample had a relatively broad coverage of businesses. Particularly, the sample had enterprises from a wide range of industries, such as apparel, leather and footwear (4.29%); machinery and equipment (6.00%); chemicals, rubber and plastics (16.47%); and food, beverages and tobacco (73.24%). The sample enterprises were local organizations with more than 20 years of operation and were privately owned. Of these, the food and beverages industry dominated the sample, as this type of industry has played an important role in meeting consumers’ requirements in the domestic market and abroad (Nguyen et al., 2020), (Ma, 2022). The food manufacturing in agriculture and organic products have not been the offerings of unique technology. They have used numerous applied technologies, namely, artificial intelligence, robotics and data analytics for getting investigation of their impacts on this type of SMEs (Ma, 2022).

It can be clearly seen from the demographic profile of respondents that a dominance of female accountants was reported in the sample’s gender composition (70.33% female and 29.67% male), which is a popular trend in accounting in developing regions like Southern Vietnam. The age group of 25–35 years constituted over half of the age distribution, and 22.30% belonged to the category of 36–46 years, with the remainder virtually split between the under-25 and over-46 groups. Regarding the length of experience, the 10–15 years group represented 33.96% of participants, compared with 50.60 and 15.44% of participants who had over 15 years and less than 15 years of experience, respectively. Regarding qualifications, 87.99% had obtained a bachelor’s degree, and 12.01% had acquired a postgraduate degree.

5.2 Outer model assessment

Building on the recommendation of Chandra and Kumar (2020), the two main tests of content and construct validity were conducted. Content validity describes the extent to which a measure illustrates all parts of a given concept (Nunnally, 1978). Construct validity can be evaluated with two approaches: convergent validity and discriminant validity (Hair et al., 2013; Chandra and Kumar, 2020). Regarding convergent validity, four elements were assessed: standardized factor loading, Cronbach‘s α, composite reliability (CR) values and average variance extracted (AVE) (Hiranpong et al., 2016). The value of standardized factor loading should be over 0.6 (Bouwman et al., 2019). Cronbach’s α test is a popular test for reliability of latent variables (Bryman and Bell, 2011) with a desired value of 0.70 or larger (Hair et al., 2011) to determine reliability of the used concept (Nunnally and Bernstein, 1994). Additionally, convergent validity is only reached when the AVE and CR values meet the widely accepted threshold (Fornell and Larcker, 1981). The CR and AVE values for each construct were recommended to be greater than 0.7 and 0.5, respectively (Hair et al., 2011). Based on the results shown in Table 1, the constructs could be used to examine the hypothesized model due to the achievement of construct reliability, convergent validity and indicator reliability.

Results summary of convergent validity

| Latent variable | Observation items acronyms | Convergent validity | Construct reliability | Discriminant validity | ||

|---|---|---|---|---|---|---|

| Standardized factor loadings ranges | AVE | Cronbach’s α | CR | |||

| Digitalization of accounting information system | DOAI | |||||

| Data input system | DIS | 0.623–0.760 | 0.603 | 0.803 | 0.808 | Yes |

| Data processing system | DPS | 0.716–0.822 | 0.664 | 0.860 | 0.862 | Yes |

| Data storage system | DSS | 0.652–0.729 | 0.617 | 0.858 | 0.859 | Yes |

| Financial statement system | FSS | 0.644–0.757 | 0.648 | 0.836 | 0.840 | Yes |

| Quality of information on financial reports | QIFR | |||||

| Relevance | REL | |||||

| Predictive value | PRV | 0.622–0.782 | 0.605 | 0.829 | 0.830 | Yes |

| Confirmatory value | CV | 0.780–0.801 | 0.618 | 0.798 | 0.802 | Yes |

| Faithful representation | FRE | |||||

| Complete depiction | CD | 0.688–0.787 | 0.664 | 0.839 | 0.840 | Yes |

| Neutral depiction | ND | 0.707–0.802 | 0.710 | 0.870 | 0.883 | Yes |

| Free from error | FFE | 0.728–0.821 | 0.717 | 0.866 | 0.870 | Yes |

| Enhancing qualitative characteristics | EQC | |||||

| Comparability | CO | 0.610–0.775 | 0.629 | 0.833 | 0.835 | Yes |

| Verifiability | VE | 0.711–0.848 | 0.671 | 0.896 | 0.910 | Yes |

| Timeliness | TI | 0.732–0.811 | 0.718 | 0.869 | 0.870 | Yes |

| Understandability | UN | 0.701–0.822 | 0.652 | 0.891 | 0.895 | Yes |

| Sustainable innovation ecosystem | SIE | |||||

| Economic innovation | EI | 0.765–0.833 | 0.604 | 0.845 | 0.847 | Yes |

| Environmental innovation | ENI | 0.666–0.795 | 0.648 | 0.873 | 0.876 | Yes |

| Societal innovation | SI | 0.712–0.834 | 0.701 | 0.872 | 0.874 | Yes |

| Public value | PV | |||||

| Outcome achievement | OA | 0.738–0.801 | 0.722 | 0.831 | 0.833 | Yes |

| Trust and legitimacy | TAL | 0.759–0.812 | 0.725 | 0.810 | 0.813 | Yes |

| Service delivery quality | SDQ | 0.662–0.796 | 0.678 | 0.807 | 0.809 | Yes |

| Efficiency | EFF | 0.773–0.815 | 0.692 | 0.897 | 0.899 | Yes |

Discriminant validity measurement. Discriminant validity affirms the distinctiveness of a measurement construct from other constructs in the model (Hair et al., 2017). The Fornell–Larcker criterion and cross-loadings are the two main approaches to evaluate discriminant validity in the traditional manner (Hair et al., 2011). The criterion of Fornell and Larcker (1981) was measured by comparing the square root of AVE and the correlation within the constructs. The value of the square root of AVE should be larger than the pairwise correlation among constructs (Afthanorhan, 2013). Additionally, cross-loadings corroborated that each indicator obtained its greatest loading value with the construct to which it was designated. Given that all of the variables presented in Table 2 are distinguished from each other, discriminant validity was reached in this research.

Results summary of discriminant validity

| DIS | DSS | DPS | FSS | CV | PRV | ND | CD | FFE | CO | VE | TI | UN | ENI | EI | SI | OA | EFF | SDQ | TAL | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DIS | 1 | |||||||||||||||||||

| DSS | 0.027 | 1 | ||||||||||||||||||

| DPS | 0.039 | 0.535 | 1 | |||||||||||||||||

| FSS | 0.030 | 0.571 | 0.537 | 1 | ||||||||||||||||

| CV | 0.061 | 0.492 | 0.474 | 0.465 | 1 | |||||||||||||||

| PRV | −0.058 | 0.508 | 0.493 | 0.497 | 0.530 | 1 | ||||||||||||||

| ND | 0.032 | 0.136 | 0.116 | 0.078 | 0.188 | 0.103 | 1 | |||||||||||||

| CD | −0.011 | −0.001 | 0.045 | 0.040 | 0.037 | −0.016 | 0.056 | 1 | ||||||||||||

| FFE | −0.010 | 0.001 | 0.018 | 0.058 | −0.008 | −0.018 | 0.066 | 0.583 | 1 | |||||||||||

| CO | −0.013 | −0.007 | 0.015 | 0.064 | 0.021 | 0.019 | 0.095 | 0.645 | 0.611 | 1 | ||||||||||

| VE | −0.055 | 0.026 | 0.043 | 0.051 | 0.186 | 0.010 | 0.079 | 0.659 | 0.559 | 0.652 | 1 | |||||||||

| TI | −0.003 | 0.098 | 0.148 | 0.091 | 0.088 | 0.086 | 0.203 | 0.037 | 0.049 | 0.043 | 0.058 | 1 | ||||||||

| UN | −0.020 | 0.052 | 0.094 | 0.077 | 0.053 | −0.008 | 0.148 | 0.036 | 0.056 | 0.024 | 0.105 | 0.645 | 1 | |||||||

| ENI | 0.070 | 0.048 | 0.093 | 0.033 | 0.133 | 0.002 | 0.458 | 0.013 | 0.006 | 0.076 | 0.063 | 0.179 | 0.127 | 1 | ||||||

| EI | 0.041 | 0.090 | 0.128 | 0.090 | 0.207 | 0.070 | 0.132 | 0.019 | −0.005 | 0.048 | 0.085 | 0.694 | 0.665 | 0.085 | 1 | |||||

| SI | 0.074 | 0.140 | 0.152 | 0.109 | 0.193 | 0.145 | 0.150 | 0.141 | 0.058 | 0.050 | 0.065 | 0.067 | 0.026 | 0.014 | 0.091 | 1 | ||||

| OA | 0.054 | 0.116 | 0.107 | 0.078 | 0.129 | 0.092 | 0.155 | 0.139 | 0.075 | 0.109 | 0.078 | 0.108 | 0.020 | 0.029 | 0.036 | 0.597 | 1 | |||

| EFF | 0.017 | 0.091 | 0.110 | 0.075 | 0.121 | 0.061 | 0.174 | 0.172 | 0.086 | 0.108 | 0.082 | 0.012 | −0.030 | 0.023 | −0.012 | 0.579 | 0.590 | 1 | ||

| SDQ | −0.018 | 0.109 | 0.104 | 0.036 | 0.178 | 0.064 | 0.496 | 0.089 | 0.115 | 0.118 | 0.101 | 0.148 | 0.105 | 0.452 | 0.054 | 0.149 | 0.124 | 0.156 | 1 | |

| TAL | −0.035 | 0.107 | 0.194 | 0.076 | 0.051 | 0.116 | 0.120 | 0.135 | 0.109 | 0.099 | 0.087 | 0.097 | 0.034 | 0.028 | 0.045 | 0.614 | 0.584 | 0.671 | 0.127 | 1 |

To ascertain the fitness of the model, the goodness of fit indices (GIFs), the Tucker–Lewis index (TLI) and the comparative fit index (CFI) were determined, as these indices have been among the most commonly used and are less influenced by sample size (Hair, 2011). Building on the proposals of Bentler (1990), a value of 0.9 should be obtained for each of the indices, and the root-mean-square error of approximation (RMSEA) values should be less than 0.06 to demonstrate a closely fitting model (Senol-Durak and Durak, 2010). In addition, the ratio of χ2 to the degrees of freedom (df) is recommended to be below 3 (Senol-Durak and Durak, 2010). The outcomes shown in Table 3 demonstrate that the GIFs achieved compatibility with the empirical data.

Results of measurement and structural model analysis

| Recommended evaluation index for model fit | Recommended criteria for evaluation | Value of index | Results of evaluation |

|---|---|---|---|

| Measurement model | |||

| χ2/df | ≤3 | 1.844 | Assented |

| TLI | ≥0.9 | 0.944 | Assented |

| CFI | ≥0.9 | 0.951 | Assented |

| GFI | ≥0.9 | 0.899 | Assented |

| RMSEA | ≤0.06 | 0.034 | Assented |

| Structural model | |||

| χ2/df | ≤3 | 1.984 | Assented |

| TLI | ≥0.9 | 0.935 | Assented |

| CFI | ≥0.9 | 0.938 | Assented |

| GFI | ≥0.9 | 0.884 | Assented |

| RMSEA | ≤0.06 | 0.037 | Assented |

5.3 Inner model evaluation

Direct effect. Building on the standardized path coefficients of the structural model demonstrated in Table 4, the empirical results indicate a significantly positive association between DOAI and SIE (H1: β = 0.417, p < 0.001) (H1: β = 0.417***). DOAI also composed the internal information architecture to strengthen the organizational information processing competencies and facilitate the efficient and effective allocation of resources, and thus conducted the complete potential of sustainability in terms of social, economic and environmental aspects. The second hypothesis of this research was also reinforced by the obtained outcomes (H2: β = 0.519***); therefore, DOAI was proved to determine QIFR. Looking at the third hypothesis, it was found that DOAI demonstrated a positive effect on the PV (H3: β = 0.430**). The impact of QIFR on SIE was investigated using the fourth hypothesis. The findings revealed that QIFR could play an important role in the generation of SIE (H4: β = 0.677***). The interconnection between QIFR and PV was also corroborated for the fifth hypothesis, and the observations revealed that the QIFR–PV link was a positive one (H5: β = 0.492**). The outcomes of H6 authenticated the association between SIE and PV creation (H6: β = 0.528**). Consequently, H1–H6 were supported.

Structural coefficients (β) of the proffered model

| Hypothesis no. | Hypothesized route of path | Estimate | SE | CR | Assessment of hypothesis |

|---|---|---|---|---|---|

| H1 | DOAI → SIE | 0.417*** | 0.126 | 3.639 | Undergirded |

| H2 | DOAI → QIFR | 0.519*** | 0.218 | 3.455 | Undergirded |

| H3 | DOAI → PV | 0.430** | 0.142 | 3.025 | Undergirded |

| H4 | QIFR → SIE | 0.677*** | 0.189 | 3.708 | Undergirded |

| H5 | QIFR → PV | 0.492** | 0.157 | 3.130 | Undergirded |

| H6 | SIE → PV | 0.528** | 0.168 | 3.532 | Undergirded |

Notes:*p < 0.05; **p < 0.01; ***p < 0.001; NS: not significant

Indirect effect. A mediating effect occurs when a third mediating variable intervenes between two interrelated concepts (Errassafi et al., 2019). The mediation effects can be categorized as partial and full mediation effects (Shankar and Jebarajakirthy, 2019). Partial mediation is achieved when both direct and indirect effects are substantial; when the indirect effect is significant and direct effect is insignificant, full mediation occurs (Cheung and Lau, 2008). Conversely, when the indirect effect is not substantial, there is no mediating effect (Hair et al., 2017). The mediation effect outcomes presented in Table 5 demonstrate the partially mediating role of QIFR on the causal relationships in the hypothesized model. SIE was found to serve as a partial mediator of the links between DOAI and PV and between QIFR and PV.

Results of indirect effect analysis

| Route of paths | Direct effect | Indirect effect | Mediation |

|---|---|---|---|

| DOAI → QIFR → SIE | 0.438*** | 0.391** | Partial |

| DOAI → QIFR → PV | 0.483** | 0.296** | Partial |

| DOAI → SIE → PV | 0.483** | 0.235** | Partial |

| QIFR → SIE → PV | 0.515** | 0.366** | Partial |

Notes:

*p < 0.05; **p < 0.01; ***p < 0.001; NS: not significant

Robust analysis. The bootstrapping technique was first introduced by Bollen and Stine (1992). As this technique can be used to address the number of determinants and estimate structure coefficients and invariance of outcomes across samples (Thompson, 1988), it has become commonly integrated into SEM procedures (Nevitt and Hancock, 2001). It can enable academics to concentrate on statistics rather than on those whose the distribution of sample were theoretically derived (Diaconis and Efron, 1983). One benefit of this approach lies in its capacity to generate an empirically estimated sampling distribution that could subsequently be used for descriptive or inferential targets, or both (Zientek and Thompson, 2007). As the outcomes offered by the bootstrapping technique create less variation, its use results in a much more faultless and reliable model (Razak et al., 2018). In the current research, the bootstrapping technique with a total of 1,500 random observations was implemented to produce a selection bias-corrected bootstrapping approach with 95% confidence intervals in the estimation of the hypothesized model. The stability of parameter estimates was identified by checking standard errors (SEs), comparing the sample statistics to mean bootstrap outcomes and determining the ratio of the mean bootstrap outcomes to SEs (Zientek and Thompson, 2007). Based on the results analyses in Table 6, the hypothesized model proposed in this research achieved incisiveness, veracity and reliability.

Results of bootstrapping estimation

| Hypothesis no. | Hypothesized route of path | Bootstrap estimation | Discrepancy | |||||

|---|---|---|---|---|---|---|---|---|

| Estimate | Mean | SE | SE (SE) | Bias | SE (bias) | CR | ||

| H1 | DOAI → SIE | 0.316 | 0.311 | 0.091 | 0.002 | −0.001 | 0.002 | −0.5 |

| H2 | DOAI → QIFR | 0.507 | 0.504 | 0.217 | 0.001 | 0.002 | 0.002 | 1.0 |

| H3 | DOAI → PV | 0.426 | 0.424 | 0.141 | 0.001 | 0.000 | 0.002 | 0.0 |

| H4 | QIFR → SIE | 0.624 | 0.622 | 0.156 | 0.001 | −0.002 | 0.002 | −1.0 |

| H5 | QIFR → PV | 0.481 | 0.481 | 0.151 | 0.001 | −0.004 | 0.002 | −2.0 |

| H6 | SIE → PV | 0.525 | 0.523 | 0.165 | 0.001 | 0.003 | 0.002 | 1.5 |

6. Final deliberations

This section focuses on the implications of the empirical investigation, the application of the present study’s observations to theory and practice and suggests routes for future research by considering the inherent limitations.

6.1 Implications

Academic implications. Regarding the impact of digitalization on SMEs’ business operations, the magnitude of DOAI was found to make a difference to SMEs’ effectiveness in terms of SIE generation, QIFR achievement and PV creation. More instrumentally, the empirical results displayed a significantly positive association between DOAI and SIE. Given that digitalization has been regarded to cause a profound impact on organizations, upstream and downstream operations, networks and ecosystems (Iansiti and Lakhani, 2014; Jacobides et al., 2018; Porter and Heppelmann, 2015), DOAI could play a paramount role in managing the interconnections and structures embedded in an ecosystem. The observations of this research offer sound evidence that DOAI is overall positively associated with QIFR. Digitalization also offers traceability and visibility through real-time data gathering (Kane et al., 2015) and conducting data analysis in real time to supply advantages such as more rapid decision-making, loss-of-time prevention and organizational performance enhancement (Hart, 2017). Digitalization and technology-based resolutions have been considered facilitators of service quality due to better resource allocation and more accurate information sharing for external and internal purposes (Abou-foul et al., 2020). As such, the AIS with the support of digital technologies, i.e. DOAI, could become a promising instrument for SMEs to achieve QIFR. Alternatively, DOAI could become an enabler to shape communities, directing numerous personal contributions and a multitude of other factors toward a common target and thus leveraging PV generation through spillover impacts on co-creation practices. The outcomes of this research recommend that a high QIFR could lead to the formulation of an SIE and create PV. Based on criteria of QIFR, such as relevance, faithful representation and enhancing qualitative characteristics, SMEs could give rise to wider interactions with internal and external stakeholders so as to collaborate on setting up an SIE and creating PV. Moreover, the research highlights the far-reaching influence of an SIE on generating PV. This is because through shaping close connections with main stakeholders, namely, government and the financial community, which would help ameliorate an organizational operating environment in numerous ways (Alchian and Demsetz, 1972; Cornell and Shapiro,1987), especially contributing inputs to an organization (Funk, 2003; Peloza and Papania, 2008), an SIE could allow an organization to reduce economic expenses and increase the economic value of their product or service, and thus lead to PV creation.

Digging deeper into the mediating components of the proposed model, these results become even more accentuated through providing evidence on the mediating role of QIFR. In this regard, QIFR was confirmed to play a pivotal role, mediating the interconnections between DOAI and SIE and between DOAI and PV. SMEs could generate an SIE and PV when appropriate attention is given to QIFR rather than focusing solely on DOAI. Undoubtedly, FRs have played a prerequisite role in the process of ascertaining organizational performance and value (Chandra and Wijaya, 2021), as well as increasing productivity and encouraging innovation (Kieso et al., 2018). QIFR would condition organizations to offer transparent financial information to their users and stakeholders, which would allow them to make decisions and reduce misleading or incorrect information (Gajevszky, 2015) and thus would facilitate attracting investment from stakeholders, thereby keeping managers in check, and realize effective decision-making for providing high-quality products or services. Likewise, an SIE was substantiated to depict mediating impacts on both the relationship between DOAI and PV and the link between QIFR and PV, which puts an emphasis on increasing the formulation and development of an SIE. The more solid an SIE becomes, the likelier that SMEs will be successful in implementing organizational digitalized processes and information disclosure to achieve PV creation. SIE achievement was corroborated to allow the formation of communities, space creation for co-creation activities and stakeholder integration to provide new points of view on PV creation.

Practical implications. Based on the proposed and empirically examined model, numerous recommendations can be drawn for practitioners, policymakers and modern technology providers.

Implications for SME managers. First, a clear DOAI strategy to achieve the desired outcomes of SIE establishment, and PV creation was considered a prerequisite. As such, SME managers should have practical insights into the essential competencies and organizational resources particular to each pathway. Given that digitalization relies heavily on human and technological resources (Sousa and Rocha, 2018; Sousa and Wilks, 2018), technology infrastructure is compulsory for enterprises to succeed in SIE establishment and PV creation.

Advanced digital technologies application typically requires well-educated staff, and the extant literature has proposed that skilled workers are indispensable for disruptive digitalization (Sousa and Rocha, 2018), especially DOAI, and all relevant staff should be reached, receive training and be encouraged to adopt DOAI, apart from essential infrastructure investments. SME managers are thus encouraged to shape positive employee attitudes toward digitalization (Baggia et al., 2019; Hernandez, 2018) in general and DOAI in particular. Managers should also direct their attention to equipping their accounting staff with skill sets relevant to accounting work, as well as information technology application capacities, through training programs that were relevant to AISs and modern information technology application.

As information quality has been widely considered the basis of organizational survival, all enterprises are encouraged to assure the authenticity of information to revamp content quality and boost timely information updates (Jiang et al., 2021), and almost all enterprises are encouraged to make a considerable investment in digitalization to enable the decrease in data processing expenses by automatizing data collection, warehousing and diagnostics (Wamba et al., 2017) for the achievement of high-quality FRs. This leads to the third implication for SME managers: equipping accounting staff with skill sets and mindsets for analyzing and communicating useful data to both interior and exterior stakeholders when DOAI is implemented.

Fourth, managers should make sense of an ever-changing SIE landscape to obtain a better management orientation for PV creation. This is because DOAI has been empirically substantiated to allow organizational staff to capture and interact with their external stakeholders in terms of the organizational ecosystem, as well as enabling the exchange of internal information between their interior stakeholders.

Strikingly, managers in SMEs have been inspired to cultivate their managerial competencies through formal mentoring programs (Amagoh, 2009) rather than solely concentrating on digital proficiency enhancement, as exceeding digital proficiency was deemed obligatory but not sufficient alone, and bolstering managerial capabilities should not be undervalued.