This study aims to develop a psychometrically validated scale to measure iGen's trust in FinTech, addressing the lack of such a scale in the Indian context.

The study involved a brief literature analysis, discussion with subject experts, panel discussion and industry professionals to improve the scale. The scale includes the following key dimensions: Security, Privacy & Risk, Financial Transparency, User Experience, Customer Support, Brand Recognition, Awareness Campaign, Social Influence and Attitude. Exploratory Factor Analysis and Confirmatory Factor Analysis have been conducted to ensure the model's validity and 35-items have been chosen that exhibit the reliability, construct validity and content validity.

The findings of this paper provide valuable insights toward the factors that shape iGen's trust on financial technology. The final scale comprises 28 items across seven dimensions: security, transparency, usability, credibility, personalization, reliability and user control. In addition, it also provides guidance to the FinTech firms in building trust-enhancing features such as clear transparency policies, better security measures and user experience (UX) improvement to enhance smooth operation and trust among individuals.

The scale would enable companies to detect trust gaps, enhance UX design and develop effective communication plans. It would also serve as a diagnostic tool for policymakers and educators in assessing the success of financial literacy programs.

The present study is a novel contribution that develops the scale to measure iGens trust on FinTech.

1. Introduction

In a world where digital transformation is reshaping every industry, the financial sector stands at the forefront, driven by the disruptive force of FinTech that is not only transforming financial behavior but also challenging traditional models of consumer trust. Globally, FinTech has emerged as the key driver for achieving financial inclusion among digitally native consumers such as Generation Z (iGen), who are fast adopting digital financial services in preference to traditional banking channels (Dauda & Lee, 2015). In India also, the growth in the adoption of FinTech has been exponential where over 87% consumers have been using digital wallets, UPI-based payments and app-based banking by the year 2023 (Agarwal, 2024) Nevertheless, the successful penetration of FinTech among this segment also largely rests not only on functionality and accessibility but also significantly on the level of faith that consumers have in these digital platforms.

Though growing in adoption, no well-established and tested scale in academic research was available to particularly measure trust in FinTech among India's iGen population – a lacuna this study attempts to fill. Trust is essential in the digital money system, most significantly among iGen consumers who are early adopters and critical reviewers of technology (Phuong et al., 2022a, b). Unlike earlier generations, iGen consumers have grown up in a completely digital setting and hence are more discerning and vigilant. They are driven by peer networks, online reviews, data protection legislation and the overall user experience (Daqar, Arqawi, & Karsh, 2020; Phuong et al., 2022a, b). Although FinTech companies have created new services such as biometric identification, fraud detection by means of AI-based systems and real-time money tracking, concerns about the misuse of data, transparency in money management and customer services remain significant hindrances toward trust (Aldboush and Ferdous, 2023a, b, c). Trust is not a unidimensional construct but is affected by several dimensions, such as security, transparency, social influence and perceived service quality.

FinTech has moved from a specialist innovation to a generalist financial product, with China, the USA and the UK, leading the way in digital adoption. Trust remains the concern at the international level, with data breaches and algorithmic biases threatening the confidence of consumers (Zarifis & Cheng, 2023) In India, while the adoption of FinTech is significantly driven by UPI and mobile banking, financial illiteracy, regulatory ambiguities and low digital resilience among specific user segments inhibit large-scale adoption (Kishor, Bansal, & Kumar, 2024). This research specifically targets South India, which is undergoing one of the quickest digital makeovers, particularly among its students and young professionals. But they are one of the underrepresented groups in FinTech trust research. South India's peculiar sociocultural and technological context, with high smartphone penetration, multilingual language adoption and urban-rural digital divides, provides a rich source to analyze regional trust patterns.

Past work has analyzed the determinants of the adoption of FinTech, such as perceived usefulness, ease of use and financial literacy (Singh, Sahni, & Kovid, 2020). Trust has been studied as one concept without understanding that there are several forms. Some have emphasized individual determinants like data security (Stewart and Jürjens, 2018a, 2018b), peer influence (Phuong et al., 2022a, b) or user experience (Ali & Marisetty, 2023), but few have developed a scale that synthesizes these dimensions within a theoretical framework pertaining to iGen. Work has also been geographically siloed, and there is no psychometrically tested instrument that currently captures trust specifically for the Indian iGen context.

This study integrates the Unified Theory of Acceptance and Use of Technology (UTAUT) (Venkatesh, Morris, Davis, & Davis, 2003) and the Stimulus–Organism–Response theory (Mehrabian & Russell, 1974) in order to examine the technological, social and psychological determinants that result in the formation of trust in the use of FinTech. UTAUT explains the adoption behavior based on performance expectancy, effort expectancy, social influence and facilitating conditions, while S-O-R explains the manner in which external stimuli such as cybersecurity, fraud protection and user education affect the psychological state of trust that triggers behavioral responses (Phuong et al., 2022a, b). By merging these two models, this study develops the concept of trust further by integrating both emotional response and behavioral intention. This paper goes beyond simply categorizing statements by creating and testing a theory-based scale with EFA and CFA, providing both statistical rigor as well as practical utility.

There are seven constructs within the conceptual model that identify iGen consumers' trust in FinTech services. Focusing on trust as the prime driver for FinTech adoption highlights the critical need to understand how users build confidence in digital financial services. While the technological viability of the services being provided by FinTech in India does exist, the lack of sustained trust would limit user retention and long-term adoption. Having a tested scale for the measurement of iGen user trust would have significant practical and theoretical implications.

Innovative in several ways, the study introduces a multidimensional approach to understanding and measuring trust in FinTech services. First, the study provides the first empirically validated, multi-dimensional scale tailored to Indian iGen users. Second, the study combines theoretical constructs from both UTAUT and S-O-R models into one scale that yields a strong explanation for the development of trust in the digital environment. Third, the scale is tested by employing robust psychometric methods such as Exploratory Factor Analysis (EFA) and Confirmatory Factor Analysis (CFA) for ensuring statistical reliability and construct validity. Fourth, while most previous research has focused on adoption intention, the present study focuses on the area of trust as a long-term behavioral outcome that has relatively less research yet remains highly important.

The primary aim of this study is to develop and validate a standardized instrument that would assess the degree to which iGen trusts FinTech services along various dimensions such as security, transparency, user experience and social dynamics. The instrument would be academically rigorous and yet feasible for FinTech businesses and digital planners to administer.

The study contributes to the knowledge base in digital trust, behavioral finance and the adoption of FinTech by presenting a widely applicable measure that accords with the dominant behavioral theory. It fills the method gap by offering an empirical scale that brings together psychological and structural components of trust. In practice, it aids in the development of better products, policy compliance and customer communication by identifying key areas that establish trust. It also aids in the pursuit of the cause of financial inclusion by enabling institutions to measure and establish trust among young digital consumers in underserved markets.

2. Theoretical underpinnings

The (UTAUT and the S-O-R framework are integrated to provide a strong foundation for trust analysis in iGen and FinTech because they view iGen's trust in FinTech as an interaction of technological, psychological and social parts that shape their adoption behaviors. The UTAUT theory establishes that the user's acceptance of technology is based on different qualities of the product. The four positive attributes of technology are called “performance expectancy,” “effort expectancy,” “social influence” and “facilitating conditions,” and the authors feel that these four attributes can be used with today's younger generation (“iGen”), when evaluating fintech (financial technology) products. As the previous article stated, the UTAUT model emphasizes the functional aspect of a product as the main reason for its adoption. However, when talking about the financial sector or anything related to finances, there are so many additional factors that contribute to trust, including, but not limited to, security, privacy, transparency and ethics. In order to include these additional elements of trust, the authors have used a framework called the S-O-R model to define the correlation between external stimulus (security features, transparency, user experience, brand credibility and social cues) and how the external stimulus influences internal tissue states (including trust, perceived risk, confidence and attitude) that ultimately lead to continued use of fintech products. Most current research in fintech has only explored the relationship between these attributes of trust in separation or in a descriptive format, resulting in unstructured theoretical insights. However, this is a perfect time to examine how the previous research can be brought together to create a cohesive, theoretical framework on how to measure trust as a multidimensional construct in India's fintech ecosystem, particularly as it relates to iGen. The four key determinants of technology adoption as defined by UTAUT are essential to the development of trust in FinTech given the previously mentioned characteristics (Al-Okaily, 2025). iGen's trust leverage is due to the belief that FinTech increases financial efficiency (performance expectancy), and iGen prioritize security and real-time payments (Smith, Dhillon, & Otoo, 2022).

The S-O-R framework also explains how external stimuli contribute to the formation of trust, which ultimately determines adoption; iGen users are very sensitive to security signals, and trust levels improve with transparent data policy and biometric authentication (Phuong et al., 2022a, b). Low risk and high transparency are directly associated with stronger trust-based adoption (Chan, Troshani, Rao Hill, & Hoffmann, 2022), and peer influence and online reviews also affect trust.

Technostress and digital fatigue decrease trust, but a simple interface and ease of use help against these (Dawood, Liew, & Lau, 2022). UTAUT and S-O-R thereby provides a complete framework for the iGen's FinTech trust in that it discusses usability, security and peer influence (Kee et al., 2024a, b). FinTech companies need to instil transparency, security and usability in order to build trust (Aldboush and Ferdous, 2023a, b, c).

3. Review of literature

FinTech's ability to earn the trust of iGen is influenced by a combination of connected factors, such as security, privacy, transparency, risk perception, user experience, customer service, awareness campaigns and group opinion (or what is known as “word of mouth”). Sign in is crucial because Gen Z consumers require the strong sign in mechanisms of biometric verification, end-to-end encryption and fraud detection to use digital financial services safely (Kee et al., 2024a, b). Building multi-layer security infrastructure is what helps companies raise consumer trust, as given that FinTech adoption is higher on the side of Gen Z when reinforced by security (Al-Okaily, 2025). Privacy is equally important, as Gen Z consumers are very aware of how their financial data is managed. Trust is formed through transparency in data collection, regulatory compliance and encryption practices (Aldboush and Ferdous, 2023a, b, c). According to research, FinTech services help user in selecting data-sharing (Phuong et al., 2022a, b), increasing users' confidence that they can manage their personal financial information relatively well.

iGen's trust depends on risk perception, most likely due to iGen's concerns about financial fraud, cybersecurity vulnerabilities, unauthorized transactions, among others, that prevent it from adopting (Nugroho & Novitasari, 2023). According to research, the more real-time fraud detection, the more transparent financial policies and the more robust the authentication mechanisms, the more trust grows in FinTech services (Singh et al., 2020). FinTech platforms with real-time transaction trackable, thorough billing and easily accessible terms and conditions are demonstrated to earn more trust (Al-Okaily, 2025). On the other hand, transparency enhances skepticism since a lack of transparency discourages adoption (Kee et al., 2024a, b).

User experience, which has been revealed to be yet another big determinant of trust, is another key major determinant of trust and iGen values faster, user-friendly, and efficient and financial platform (Tan et al., 2023). In its research, FinTech companies that prioritize real-time processing, have an easier-to-navigate platform and can provide AI-driven personalization tend to be perceived as more reliable (Nurjaman, Saputra, Puspitasari, & Bazen, 2023). On the other hand, complex interfaces and slow response time give rise to loss of trust, which discourages repeat usage (Widiharlina, Saputra, Wegman, & Puspitasari, 2023). Awareness campaigns are also a tool for creating trust with consumers because they teach consumers about FinTech security, the mitigation of fraud and their financial rights (Nadyatama, Saputra, & Panduwiyasa, 2024).

The current literature indicates that the level of trust placed in FinTech services by the iGen or Gen Z population is an essential criterion when adopting these services due to the rapid digitization of financial services and the data-based nature of the global financial ecosystem. Evidence across multiple settings indicates that the elements that form the basis of trust are data security, data privacy and perceived risk (Kee et al., 2024b; Stewart & Jürjens, 2018b). Even though members of Generation Z feel that the speed and convenience of FinTech platforms meet their needs better than traditional bank platforms, they do not yet fully trust FinTech platforms and still tend to have a higher level of trust in traditional banks. This may be due to the greater likelihood that they experience various types of cyber threats, the existence of automation bias within FinTech services and the opaqueness of underlying algorithms used to power AI-based FinTech platforms (Sundararajan, 2020; Yang, 2025). Social influences and networks of peers further strengthen adoption behaviors, particularly in the areas of digital payments and investment platforms, wherein trust is socially constructed and mediated via these social connections (Alam, Tao, Lahuerta-Otero, & Feifei, 2022; Dwi Fortuna & Sutrisno, 2024). While various studies support the idea that there are a variety of factors and characteristics of FinTech companies that would enhance consumer confidence and usage over time and lead to higher satisfaction, the ongoing challenge of building long-term adoption of FinTech platforms remains fairly consistent. In particular, despite the increased digital fluency within Generation Z, low financial literacy and limited awareness will continue to restrict opportunities for continued use of FinTech platforms (Memon, Nair, & Jakhiya, 2021; Anand & Sharma, 2023). In addition to these conceptual issues, the existing body of work on financial technology continues to highlight the importance of ethical conduct and corporate social responsibility; transparency; and regulatory compliance, particularly in terms of being applicable to the trust component of FinTech and potential influences on continued usage and overall satisfaction of consumers using FinTech platforms (Syakinah, 2024).

Although much research has discussed the FinTech adoption among Gen Z, there is a gap in further developing a valid scale of measuring iGen's trust in FinTech. Most of what exists in the existing studies are the studies that deal with individual determinants of trust, lacking an integrated framework for systematically quantifying trust as a multi-dimensional construct. To bridge this gap, a rigorously developed scale is necessary to enhance theoretical and practical insights.

4. Methods

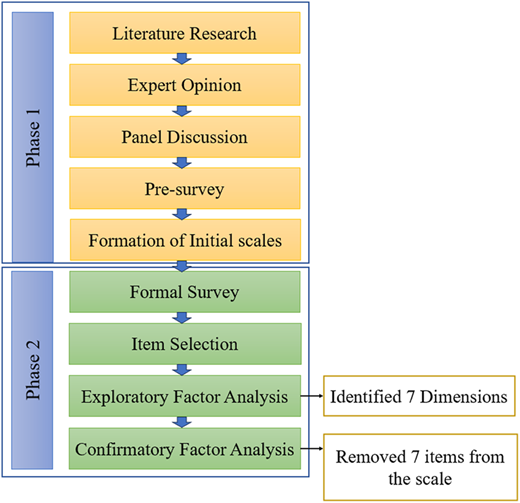

A standardized scale for assessing iGen's trust in fintech was possible through a comprehensive review of the literature and experts' insights (Quaranta & Salvia, 2014; Udjo, Simelane, & Booysen, 2000). In this study, the procedure was split into two phases: A literature review, expert opinion, panel discussions, a pre-survey, as well as preliminary item generations encompassed Phase 1 (see Figure 1); Phase 2 consisted of a formal survey, item selection, EFA and CFA. The initial goal of this study was to develop measures to assess iGen's trust in fintech.

5. Phase 1: generating items for the scale

5.1 Literature research

Initially, to generate items for measuring iGen's trust in fintech services, the study incorporated literature analysis. Keywords such as “Fintech,” “digital finance,” “user experience,” “privacy,” “trust,” “risk,” “security,” “social impact,” “transparency,” “customer service,” “awareness campaign,” “attitude,” “questionnaire” and “measurement tool” were included. Databases like Scopus and Web of Science were considered for review of articles published between 2011 and 2024. A total of 54 articles were selected following the elimination of duplicates as well as incomplete content.

5.2 Expert consultation

In order to facilitate content validity and conceptual alignment of the FinTech Trust Scale, a panel of experts was consulted. Experts were selected based on three criteria: (1) completion of a minimum of a master's degree; (2) more than ten years of professional experience; and (3) voluntary participation with informed consent. All participants were associated with a reputed organization and had relevant expertise concerning FinTech services, digital trust, behavior of consumers, cybersecurity and social influence, in which they understood the implications of the task and issues surrounding the conceptual framework. This pedigree of knowledge informed the panel's ability to provide insights on the instrument and to review the content of items both in terms of their relevance and clarity.

The expert review was structured through a questionnaire. The questionnaire contained three sections. The first provided instructions, including the purpose of the review, directions for completing it and acknowledgements of their contribution. The second part of the questionnaire was to collect demographic and professional background information to validate the expert's credibility and include basic demographic information, including age, gender, qualifications, name, organization, professional experience and contact information of the expert.

The third and final stage was the item evaluation phase. Experts were asked to evaluate the importance of each item in measuring trust in FinTech services for iGen users on a 5-point Importance scale of “very unimportant” to “very important.” They were also requested to evaluate (1) whether the items accurately aligned with content of iGen's trust in fintech services, (2) dimensions were associated with the items, (3) if there were redundancies, (4) whether the wording was simple and concise, (5) any vagueness was present and (6) the requirements of combining items. Experts were also asked to suggest any new items to enhance the scale. Experts were provided with an opportunity to provide feedback during a 12-day timeframe, at which time the responses were used to analyze items for the next revision.

Furthermore, during the subsequent meeting, experts enhanced their existing responses to improve the items. This repeated approach improved the items' clarity, as well as the fit of the items with their objective. In order to precisely measure the agreement, a consensus approach (Wang, Liao, Huang, & Xu, 2021) was considered by analyzing the expert's response as “important” or “very important”. Items with an agreement rate of 80% or above were retained, whereas those below the threshold were removed or revised. However, most of the experts approved of the item's extensive aspects. Using the scale-level content validity index and average item-level content validity index (I-CVI), the expert responses for each question were examined for content validity, which led to the elimination of “TR5.”

5.3 Panel discussion

To guarantee accuracy, clarity and comprehension, a group encompassing two professors specialized in Fintech, two digital marketing and customer experience specialists and one Master of Commerce (MCom) and Master of Business Administration (MBA) students from each investigated the language of the scale items dealing with all the items for 120 minutes before approving the items and during this stage most of the items were revised.

6. Phase 2: evaluation of the Scale's psychometric properties

6.1 Tools

Further, 41 iGen fintech users were approached with the help of a convenience sampling method based on the following criteria: (a) fintech users aged between 18 and 27 years; (b) interested or experienced with the services of fintech; and (c) voluntary involvement. Unfamiliarity with fintech services and participants unable to complete the survey due to personal or technological barriers were excluded from the study. In total, 39 participants filled out the survey and subsequently provided feedback on clarity as well as experiences on filling out the questionnaire. Seven dimensions made up the questionnaire: Security, Privacy and Risk (8 items), Social Influence (3 items), Awareness Campaign (3 items), Customer Support (3 items), User Experience (4 items), Financial Transparency (3 items) and Attitude (4 items), assessing through a 5-point Likert scale ranging from “Strongly Disagree” to “Strongly Agree.” Furthermore, we obtained approval from the Scientific Review Board of YIASCM, Yenepoya (Deemed to be University) with No. YIASCM/SRB-02/MGT/02/2024 on 18th November 2024.

6.2 Participants

Employing a stratified sampling technique, 892 iGen fintech customers were chosen from the South Indian states of Karnataka and Kerala between October 21, 2024, and February 21, 2025. The states were chosen because of their growing digital infrastructure, higher levels of FinTech adoption by youth, and a fairly government-supported population of iGen users. The residents in urban and semi-urban districts of these states provided a contextually appropriate demographic for studying youth trust in FinTech services. Two subgroups were created randomly from the total sample through SPSS Amos, distributing one for CFA and another for item screening as well as EFA, keeping in account the same criteria mentioned for the pre-survey stage.

6.3 Statistical methods

The critical ratio technique, correlation analysis, as well as homogeneity tests were employed to initially screen the items. The dimensions of the scale were further examined utilizing EFA and the model fit was assessed using CFA. Measures of content validity, construct validity, convergent validity, discriminant validity and internal consistency reliability were also applied to investigate the scale's psychometric properties.

7. Results

7.1 Characteristics of the study participants

Although a substantial body of research has examined FinTech adoption among Generation Z, a significant gap remains in developing a validated scale to measure iGen’s trust in FinTech. Existing studies primarily focus on individual determinants of trust, rather than offering a comprehensive and integrated framework for systematically quantifying trust as a multidimensional construct. As summarized in Table 1, prior literature largely emphasizes fragmented aspects of trust, highlighting the absence of a unified measurement approach. To bridge this gap, the development of a rigorously validated scale is essential to enhance both theoretical understanding and practical applications in this domain.

The sample was randomly split into two groups: one for confirmatory analysis (n = 447) and one for exploratory factor analysis (n = 445). Chi-square tests showed no significant demographic differences between them (see Table 2).

7.2 Discrimination analysis

Every subject received a rating ranging from highest to lowest based on their overall scores on the scale. The top 30% of the scores are in the high-score group, and bottom 30% of the scores are in the low-score group. Additionally, an independent sample t-test has been used to identify the significant differences of all the items between the groups and as per the findings, the scales showed strong discrimination power, and none of the scales were eliminated.

7.3 Homogeneity test

The scale has achieved the overall Cronbach's α coefficient of 0.778 in the homogeneity test, which indicates that the scale has outstanding internal consistency. This result ensures the scales' resilience and reliability by confirming that no further improvement could be made by removing any items.

7.4 Exploratory factor analysis

KMO and Bartlett test of Sphericity: Kaiser–Meyer–Olkin (KMO) and Bartlett test of Sphericity measure the inter-correlation between the variables and confirm that there are enough samples. The KMO value differs in the range of 0 to 1. According to Hair, Black, Babin, and Anderson (2010), the KMO value must be higher than 0.50, and the Bartlett test of sphericity needs to be greater than 0.000 in order to be significant.

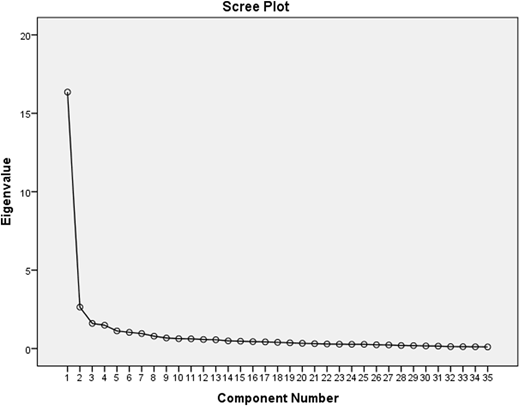

As per the result of KMO Measure (Table 3), the test value is 0.931. Moreover, Bartlett's test of sphericity value was 0.000, therefore the data is validated for the factor analysis. All communalities exceeded 0.4, indicating shared variance among items. Thus, factor analysis was conducted on all 35 items.

The EFA has been conducted with all items, and the study has yielded seven distinct factors with an Eigenvalue above 1. To look into the differences between the data gathered from the questionnaire, a Maximum Likelihood with Varimax rotation has been conducted. From the factor analysis, seven factors were extracted, which collectively explains 71.989 % of the total variance (see Table 4 and Figure 2).

Factor 1: Factor 1 is named “Security, Privacy & Risk” because all the items in Factor 1 reflect the same dimensions. The items included in this mainly focus on iGen's safety while using the financial technology services, where they prefer a high level of safety, granting access before making a transaction, having advanced biometric security features to ensure the safety online transactions. All the items were loaded above 0.5, and items with poor factor loading are removed from the study (see Table 5).

Factor 2: Factor 2 is named “Social Influence” because all the items in Factor 2 reflect the same dimensions. The items included in it highlight the importance of social interaction. Where the iGen's are greatly influenced by the peer group, they depend on family member's, and they also consider the opinions of their community. All the items were loaded above 0.5, and items with poor factor loading are removed from the study (see Table 5).

Factor 3: Factor 3 is named “Awareness Campaign” because all the items in Factor 3 reflect the same dimensions. The items included in it involves awareness of iGen's on Fintech services. Generation Z is greatly influenced by the educational programmes, which increases their knowledge & trust. All the items were loaded above 0.5, and items with poor factor loading are removed from the study (see Table 5).

Factor 4: Factor 4 is named “Customer Support” because all the items in Factor 4 reflect the same dimensions. The items included in it highlight regular service quality offered and addressing and solving the problems. All 4 items were loaded above 0.5, reflecting customer support (see Table 5).

Factor 5: Factor 5 is named “User Experience” because all the items reflect the same dimensions. The items included in the study highlight the experience of iGen's on fintech services. Where iGen's use fintech services due to its convenience, speed at which the transactions are processed, keeping up with the digital age and helps in making good financial decisions. All the items were loaded above 0.5 and items with poor factor loading are removed from the study (See Table 5).

Factor 6: Factor 6 is named “Financial Transparency” because all the items in Factor 6 reflect the same dimensions. The items included in it involve clearness in financial transactions, clarity on how fees are calculated, details of Interest rates and terms and conditions. All 4 items were loaded above 0.5, reflecting financial transparency (see Table 5).

Factor 7: Factor 7 is named “Attitude” because all the items in Factor 7 reflect the same dimensions. The items included in the study spotlight the attitude of iGen's towards fintech services. All the items were loaded above 0.5, and items with poor factor loading are removed from the study (see Table 5).

7.5 Descriptive statistics:

iGen's have shown positive opinion about the security, privacy and risk (see Table 4) which was measured using 12 items coded from SPR1 to SPR12. Respondents believe that granting access before making a transaction makes them feel secure (M = 3.9058). As far as social influence is concerned, they agreed that they depend on family member's experience while choosing FinTech services (M = 3.8520). Moreover, in the awareness campaign, iGen's approved that awareness on cybersecurity, educated them to be more alert from spammers and fraudsters (M = 3.9417). In customer support, iGen's are satisfied with the customization provided by the fintech companies (M = 3.8341).

Furthermore, Generation Z is satisfied with the speed at which the transactions are completed using FinTech services (M = 3.8700). Moving to the next factor, i.e., financial transparency, FinTech services give clarity on how fees are calculated (3.9776). Finally, the factor attitude, which is coded as A1 to A4, iGen's have a positive attitude to use the fintech services due to its advanced security and safety (M = 3.8341).

7.6 Confirmatory factor analysis (initial model)

Table 6 shows the measurement model containing seven factors. All the factors are calculated by the minimum of 1 to the maximum of 7 observed variables. The random measurement error affects reliability, every variable gets regressed into the corresponding factor. In the end, all 7 factors are correlated.

The factors are equally treated without the presence of exogenous or endogenous variables in the measurement model. As there were no proper fit indices in the current model, a modification has been made for a better fit (see Table 6). The result of the initial run model has been shown in Table 7, where the model lacks the fit in the initial stage, and the model seems to be unacceptable due to which modification was made to the model. In the first model few items were eliminated as it reduces the measurement fitness. The items whose factors loadings were below 0.5 were dropped. In the first model, SPR4, SPR10, SPR11 and SPR12 were removed, AC4 has been eliminated from the Awareness campaign, CS3 has been removed from Customer support, and TR1 has been removed. The model's fit indices exhibited better acceptance (see Table 6).

The satisfactory level of acceptance has been attained in the revised model. But, due to the validity issue and model fit, which again showed better fit indices but were not fit, so the Modifications Indices (MI) were made. The high MI values between SPR8 and SPR9; CS1 and CS4 showed the covariances between these pairings, which enhanced the model's fit. Moreover, it was found to be a covariant of the elements listed above. Following all the changes, a second CFA was performed to evaluate the model fit.

The proposed model in the present study was discovered to be an over-identified model with positive degrees of freedom. 0.909 GFI was achieved. Furthermore, 0.911 AGFI was obtained. In addition to these, the CFI and NFI values obtained were 0.907 and 0.917. The RMSEA value obtained in the study was 0.039, while the SRMR value was 0.038.

These values suggest that the model appears to have an over-identified model and an acceptable fit. While the theocratized model appears to have a good match with the observed data, the CFA results show that the model fitness is satisfactory. So, the author concludes that the hypothesized seven-factor CFA model perfectly fits the sample data.

8. Confirmatory factor analysis (modified model)

8.1 Construct validity

In 1959, Campbell and Fiske established two aspects – convergent validity and discriminant validity – for analyzing a test's concept validity.

8.1.1 Convergent validity

The measurement model's convergent validity can be assessed using both Composite Reliability (CR) and Average Variance Extracted (AVE). According to the findings, each construct's CR value is over 0.8, suggesting good dependability, which is quite satisfactory. Additionally, each construct's AVE is above 0.5, meeting the requirement that it be above 0.5 in order to be deemed acceptable for stating the constructs' convergent validity (see Table 8).

8.1.2 Discriminant validity

The correlation coefficients between the dimensions were all less than the principal square root value of AVE, and there was a significant association between all of the dimensions (p < 0.001). The aforementioned findings suggest that this scale's latent variables have excellent discriminant validity because they are both modestly linked with and distinct from one another (see Table 8).

9. Discussion and conclusion

This research aims to create a validated and scale-comprehensive measure of iGen's trust in Fintech in order to fill a significant literature gap. Trust in the contemporary digital financial environment is not just an aftermath of technology use, it is a strategic driver of long-term loyalty and engagement. For fintech businesses, building trust among digitally native users such as iGen is critical, not only in acquiring users but also in securing persistent use and word-of-mouth. Based on empirical analysis, the research established nine fundamental dimensions that guide iGen's trust in fintech platforms: Security, Privacy and Risk, Financial Transparency, User Experience, Customer Support, Brand Recognition, Awareness Campaigns, Social Influence and Attitude. Every dimension has a unique function in determining trust, and collectively they offer an integrated model for interpreting trust-building processes within the fintech sector.

The findings extend existing FinTech literature by empirically demonstrating how trust is structured among iGen users within the Indian digital financial ecosystem. While prior studies often treat trust as a single antecedent of adoption, the validated scale shows that trust emerges from multiple, empirically distinct dimensions reflecting technological, informational and experiential evaluations. By grounding the results in the integrated UTAUT and S–O–R framework, the study explains why certain trust cues translate into adoption-related responses. This addresses a key gap in prior research, which has largely relied on descriptive or adoption-focused models without validating trust as an independent construct.

10. Security, privacy and risk

Security is considered as a prominent measure to build trust among the people towards technologies; it is a practice of protecting the sensitive financial information of users. Various factors of securities have been studied by previous researchers, which contribute to the trust (Stewart and Jürjens, 2018a, b). Personal data is widely used by companies to provide better service to users, but the privacy of personal information creates risk for users (Bhatia & Breaux, 2018). This can be minimized by implementing better data security, data confidentiality and data protecting regulation, which will lead to trust building in the users (Aldboush and Ferdous, 2023a, b, c). Transparency in data utilization and adherence to laws such as GDPR enhances credibility. This is a reflection of the S-O-R model, in which good security presents as an external stimulus, influencing the perception (organism) of the user, consequently impacting trust and action intention (response).

11. Transparency

The second identified dimension of this scale is transparency, which is an openness and clear sharing of the information about the rules and the policies of company's financial practices and procedures. Transparency regarding fees, interest and terms is an important trust-enhancing factor. Fintechs that reveal their financial terms clearly and do not charge any hidden fees are preferred by users. Transparency lowers the level of uncertainty and raises confidence, particularly in digitally savvy iGen users (Addula, 2025a). Previous studies have highlighted that young individuals have a better knowledge of the usage of technologies and the smooth running of these technologies works when transaction aspects, fees of the technologies, interest rates and terms and conditions are properly mentioned on the websites (Hartono, Holsapple, Kim, Na, & Simpson, 2014).

12. User experience

In addition, the experience of the users play a significant role in building trust, which includes convenience, faster transactions, better functionality and real-time data. A smooth user experience (UX) with intuitive design, speed and personalization goes far to induce trust. Sites providing seamless real-time performance tend to win user loyalty (Meesad & Mingkhwan, 2024). Difficult or buggy interfaces discourage users and decrease trust. Studies have also argued that individuals with less experience will have less trust in financial technology compared to individuals with high experience (Zhao, Khaliq, Li, Rehman, & Popp, 2024). This is indicative of the UTAUT construct of “effort expectancy,” that simpler-to-use sites bring greater trust, particularly in areas where digital literacy may be uneven among young users.

13. Customer support

Likewise, companies will have a better future when they have strong support from the customers. Trust is supported by prompt, caring and effective customer service. When fintechs offer multi-channel support, fix issues efficiently and actively include feedback, they convey reliability. In contrast, neglect or communication breakdowns cause user dissatisfaction and loss of trust (Aldboush and Ferdous, 2023a, b, c). Contrarily, Best and Andreasen (1977) said that most of the companies shut down due to their negligence and improper communication with the customers. For young digital users facing a fast-changing fintech environment, customer support serves as a proxy for institutional trust, consistent with the “facilitating conditions” concept of UTAUT.

14. Awareness campaign

On the other hand, Serdarušić, Pancić, and Zavišić (2024) highlighted the importance of digital awareness that significantly leads to the adaptation of technologies. Customers will build trust if they are aware of the technologies they use, so the companies need to provide some basic awareness campaigns, such as awareness on global cyber-attacks and their mitigation, awareness on information security, the importance of privacy concerns and awareness on consumers right and measures. Such learning triggers fall under the S-O-R model, with trust being influenced by knowledgeable user feedback to external stimuli such as awareness campaigns.

15. Social influence

Furthermore, the scale explored social influence. According to Al Rubaiai and Pria (2022), customers will have a strong social influence in the form of societal pressure on adaptation technologies. Social influence plays a large role in influencing iGen users' trust in FinTech, as they tend to depend on peer views, online ratings and social media when considering new platforms. Studies establish that peer suggestions and social endorsement increase perceived credibility and adoption intentions (Addula, 2025a, b). Social norms minimize uncertainty, particularly when institutional trust is weak (Roh, Yang, Xiao, & Park, 2024). Positive sentiment and engagement in online communities also increase trust, consistent with previous findings that subjective norms are dominant predictors of trust in online finance (Yousafzai et al., 2009a, b).

16. Attitude

Additionally, attitude of the customers will have a greater influence on building trust (Yousafzai et al., 2009a, b). The study highlighted the importance of behavioral intentions towards the adaptation of technology by taking perceived trustworthiness as a main construct. Consumers' positive perception, decision-making, willingness to adopt and preference explores the influence factors and behavioral outcomes. This is consistent with the S-O-R model, where internal attitude (organism) acts as the mediator of external stimuli (e.g., UX, transparency) to result in trust-driven behaviors.

This research suggests a tested, multi-dimensional measure of iGen's trust in FinTech that meaningfully contributes to practice and theory. Theoretically, it is an extension of the UTAUT and the S-O-R model by the inclusion of trust-related constructs like security, transparency, privacy and social influence variables, which are increasingly important in digital financial environments. In practice, the scale offers FinTech firms, regulators and educators a strategic instrument to plan trust-building features, enhance customer service and conduct awareness campaigns aimed at youthful users. It also facilitates the development of financial literacy programs and digital inclusion programs. For future studies, this scale will be a point of departure for comparative studies between populations, technologies or geographies, providing ongoing insights into the dynamic shifts of financial technology trust.

17. Practical implication

Theoretically, this study takes an innovative approach by extending UTAUT and S-O-R framework, which provides a detailed grasp on how iGen's develop its trust in financial technology services. This research contributes to theory by applying the UTAUT to include trust-specific factors like security, privacy and financial transparency that are especially salient to iGen users in emerging markets. By incorporating these factors, the study enhances theoretical knowledge regarding digital natives' assessment and formation of trust in digital money technologies that have been less explored in previous models. Inclusion of social influence, performance expectancy and effort expectancy has extended the UTAUT theory in shaping the trust level of the customers. Moreover, recommendations from peers, family and the influence from the community have strengthened the trust in Fintech services. Strong cybersecurity and prevention of fraud had also mitigated the risk and enhanced confidence in the usage of financial technology. The S-O-R framework highlights how external environmental factors, such as fraud protection, cybersecurity, user experience and customer support, contribute to the formation of trust. The findings of this paper offer empirical evidence towards social and psychological elements that play an important role in enhancing consumer trust. Furthermore, the results of this paper support digital consumer research by offering several factors that will impact the trust on the usage of financial technology (Fintech) services.

Managerially, the scale provides a diagnostic tool for FinTech developers, marketers and digital strategists to assess and enhance trust-related issues in their platforms. It allows firms to create user-centric digital services that emphasize safe experiences, clear operations and timely customer support, all of which are essential in winning and maintaining trust among iGen users. In addition, policymakers and regulators can utilize this scale to gauge digital natives' trust readiness and develop evidence-based policies that seek to improve cybersecurity standards, data privacy safeguards and digital literacy. These interventions can assist in bridging trust gaps, enhancing safe financial habits and facilitating deeper digital financial inclusion in fast-changing markets.

At the societal level, this scale paper enhances financial inclusion and digital empowerment. Various Initiatives can be designed by the Fintech Companies to promote responsible and safe financial behaviors by identifying trust barriers such as security, lack of awareness and transparency in digital transitions. Moreover, trust in financial technology will empower the underrated communities, young people and students towards investment and digital banking, which promotes a modern technology system over the traditional financial system and encourages economic independence.

The core contribution of this study lies in developing a psychometrically validated, context-specific scale for measuring iGen's trust in FinTech in India. Methodologically, it advances scale development research by empirically establishing trust dimensions rather than assuming them a priori. Substantively, it provides FinTech firms, policymakers and educators with a diagnostic tool to identify trust gaps, design targeted interventions and evaluate financial literacy and transparency initiatives. Thus, the study moves beyond descriptive analysis to offer a theoretically grounded and practically actionable contribution.

18. Limitations and future perspective

Despite having its significant implications, this study has some drawbacks. The study fully focuses on iGen's (Generation Z) users, by giving less importance to the users who belong to Baby Boomers, Generation X and Millennials. Further, the study considered the iGen's of Dakshina Kannada, India. Expanding the study to other geographical regions could enhance the generalizability of the findings.

Looking ahead, further researchers could explore financial decision-making and perception towards the security of financial technologies to develop the adoptive trust model by considering blockchain technologies, Robo advisory and decentralized Finance (DeFi). Finally, combining big data and ML (Machine Learning) to measure the trust of customers will magnify the accuracy and transparency, which allows Fintech providers to address the concerns related to trust. This research serves as a foundation for understanding the trust of iGen's on financial technology (Fintech) services. It is anticipated to inspire further studies that address these limitations in the field of Financial Technology (Fintech).