This research is aimed at exploring the development of science and philosophy related to artificial intelligence (AI) in the context of Financial Technology’s (FinTech’s) ability to increase the customer experience (CX).

To do this, a bibliometric study was performed using literature published between 2013 and 2024 found in Scopus and Web of Science databases. This analysis utilized performance evaluation and mapping of sciences as well as co-occurrence of author networks and keywords and bibliometric analysis. The analysis was conducted with the aid of software such as VOSviewer and Biblioshiny.

The research demonstrates that since 2018 there has been an increase in interest in academic research on how technology advancements and the expanding use of artificial intelligence within the Financial Technology industry are impacting this area of study. The most frequently researched topics include Financial Automation, Fraud Detection Algorithms, Innovations in Digital Payments, Chatbot Based Service Delivery, Customization Using AI and Regulatory Technology (RegTech).

Through a systematic keyword-based analysis of AI-enabled CX in FinTech using bibliometric analysis, this study provides a comprehensive overview of published projects related to AI-enabled CX in FinTech. The development of mutual aid networks among researchers and analysis of newly emerging themes will help clarify how this area has progressed and will provide direction for future research in this area. The findings offer valuable insights for scholars by identifying research hotspots and underexplored areas, while also providing practical guidance for industry stakeholders seeking to strategically apply AI to enhance CX in FinTech services.

1. Introduction

1.1 Background and context

FinTech has become a disruptive force in the financial services sector throughout the last ten years (Arner, Barberis, & Buckley, 2015; Gomber, Kauffman, Parker, & Weber, 2018; Nicoletti, 2017). Fast digital change has made it possible for FinTech to use cutting-edge technologies like blockchain, big data, artificial intelligence (AI) and the internet of things to offer creative financial services that are more accessible, effective and customized (Dorfleitner, Hornuf, Schmitt, & Weber, 2017; Gai, Qiu, & Sun, 2018; Haddad & Hornuf, 2019). AI is one of the many technologies transforming customer experience (CX) (Lemon & Verhoef, 2024). It is becoming less of a futuristic idea and more of a modern necessity, creating a new way for financial service providers and their consumers to interact with and access financial services (Douglas, Barberis, & Ross, 2017). AI is changing the way customers interact with businesses, from chatbots and robo-advisors to fraud detection and personalized product suggestions (Grewal, Roggeveen, & Nordfält, 2017). To get ahead of the competition, decrease operating costs and, most importantly, give clients smooth and great experiences, both old and new financial institutions are putting a lot of money into AI (Jagtiani & Lemieux, 2019).

The study examines the role of FinTech on the performance of banks as a result of bibliometric analysis in the years 2015–2024 (Wang et al., 2022). This study addresses key questions about the research trends, the key authors, the geographical consideration and the role of this factor on the performance of banks (Wang et al., 2022). Future research will look into other metrics, the regional focus, the financial inclusion, the entrepreneurship and how the same affects the bank performance (Ghatode & Nimbarte, 2025), (Xu, Kasperskaya, & Sagarra, 2025).

1.2 Importance of CX in FinTech

CX is the whole effect of all of a consumer’s encounters with a brand, including both digital and physical touchpoints (Lemon & Verhoef, 2016). In the very competitive and standardized FinTech industry, CX has become a key differentiator (Dean, 2024). Today’s customers want financial solutions that are quicker, more intelligent and easier to use (Ahmed, 2024). They want smart interfaces, services that are tailored to them, smooth transactions and help that is always there. AI can provide these things in a different way (Brightmore, 2024).

AI technology makes predictive analytics, sentiment analysis, natural language processing and cognitive automation possible. All of these things improve the range and quality of consumer engagement. For instance, AI can look for strange patterns in transaction data to stop fraud before it happens, or it can look at how people act to suggest the best ways to invest (Sharma & Sharma, 2025).

These traits not only make the business run more smoothly, but they also build loyalty, trust and contentment, which are all important for long-lasting client connections (patil, rane, & rane, 2024).

Chatbots and virtual assistants are two examples of AI being utilized in FinTech. They help customers 24/7, automate boring chores and help people who speak different languages.

1.3 Emergence of AI in FinTech applications

Chatbots and virtual assistants are two examples of AI being utilized in FinTech. They help customers 24/7, automate boring chores and help people who speak different languages (Kumar et al., 2024a).

Robo-Advisors: These tools help people manage their money and make investment choices by using computer models and data about how people act (Capponi, Olafsson, & Zariphopoulou, 2020).

Fraud detection and risk management: Using behavioral modeling, anomaly detection and pattern recognition to find behavior that seems off (Putha, 2021).

Credit scoring and underwriting: AI looks at things like a person’s social media activity and mobile phone use to see if they are creditworthy (ots, liiv, & tur, 2020).

Customized financial services: Giving advice based on someone’s tastes, spending habits or stage of life (prajapati, 2025).

These apps offer services that are proactive, predictive and aware of the context. These services not only meet but often exceed what customers expect. AI is becoming the main way that the FinTech ecosystem makes digital customer focus happen (Magnuson, 2024).

1.4 Rationale for a bibliometric analysis

Though it has grown very fast, literature about AI in FinTech is still scattered in many areas, including information systems, computer science, finance and marketing. The researchers and practitioners can identify the key publications, emerging trends, hot topics of research and gaps in knowledge through the methodical, quantitative evaluation of the existing literature that a bibliometric study provides (Kp, Chauhan, Al-Absy, & Ranganathan, 2025).

The intellectual structure and research horizons of this multidisciplinary area are understood through the help of such bibliometric methods as key-word co-occurrence mapping, co-citation analysis, citation analysis and co-authorship networks. Moreover, this study is informative to scholars, business stakeholders and legislators by reviewing how AI is enhancing the FinTech CX (Kumar et al., 2024a).

1.5 Research objectives

This study is aimed at providing an in-depth bibliometric review of scholarly literature at the intersection of FinTech, AI and customer experience. Some of the specific objectives include the following:

To visualize the conceptual map of the CX-based FinTech research on AI application.

To identify the prominent authors, journals and agencies of making valuable contributions to this area of study.

To apply citation network and term co-occurrence analytics to determine the research trends and thematic clusters.

To attract focus to the gaps in research and provide recommendations on the future direction of studies that can enhance AI-driven CX with FinTech applications.

1.6 Significance of the study

The value of the study is that it gives a wide perspective of a complex and a rapidly evolving area of study. A bibliometric approach facilitates a comprehensive knowledge that can guide strategic research and development, while individual studies may focus on specific applications or technologies. This study is particularly relevant in light of the post-COVID-19 acceleration of digital finance and the increasing reliance of clients on AI-driven interfaces.

This research offers practical insights for academics and practitioners aiming to develop more responsible and engaging FinTech solutions by emphasizing underexplored areas, like emotional intelligence in chatbots, ethical AI in banking and AI inclusivity.

1.7 Structure of the study

The study is organized as follows: Section 2 provides an overview of the relevant research on AI, CX and FinTech; Section 3 presents an in-depth description of the research methodology, data collecting, tools (VOSviewer and Biblioshiny) and bibliometric indicators used in the research. Section 4 also presents the bibliometric analysis that consists of thematic clusters, co-authorship networks, publishing trends and citation analysis. Section 5 deals with implications of the findings to research and practice. Section 6 concludes the study with the summary of the key findings and recommendations on the future research.

2. Literature review

2.1 Introduction

The merging of AI and FinTech is completely changing how financial services are delivered, and CX is one of the biggest areas of impact. This overview of the literature brings together the theoretical and empirical work done in the fields of AI, FinTech and CX so that you can get a full picture of the state of the field. It also points out the gaps and ideas that need bibliometric analysis (Kanaparthi, 2024).

AI has quickly spread through the financial services industry, allowing for scalable automation, better risk assessment and hyper-personalized product offers that change how customers interact with banking and FinTech platforms. Recent evaluations show how AI has changed product recommendations, automated advice, fraud detection and operational efficiency. However, they also point out that most of the research focuses on technology rather than customers (Lawrence, Ugochukwu, & Noluthando, 2024).

Even with this expansion, there are still not many systematic bibliometric studies that describe the intellectual structure and evolution of the interface between AI, FinTech and CX. Current bibliometric analyses of AI/FinTech delineate extensive clusters (e.g. banking, risk, automation) but seldom extract CX-centric themes or amalgamate customer outcome measurements across research, resulting in an inadequately characterized interdisciplinary landscape (Kumar et al., 2024b).

Another line of research looks at AI-driven personalization and recommendation systems. Studies have shown that these systems can improve engagement and conversion in digital commerce, and new data suggest that they could have the same effect in FinTech (personalized financial advice and tailored loan offers). Nonetheless, the mechanisms by which personalization enhances subjective CX measures (such as trust, perceived fairness and long-term loyalty) are inadequately defined and empirically disjointed (Yin et al., 2025).

Ethical, explainability and emotive characteristics are garnering increasing attention and yet remain inadequately incorporated into empirical customer experience studies. Research on explainable AI (XAI) and trust in financial settings emphasizes that transparency, interpretability and perceived fairness significantly influence user acceptance; however, most empirical studies in FinTech-AI still prioritize algorithmic performance over customer perceptions and experiences of decisions (Staley, 2025).

Nevertheless, there are still gaps in the context that are very huge. There isn’t much research from poor countries or comparisons between cultures. Most of the published work is on North America and Europe. Few longitudinal studies consider the effect of AI-based interventions on the shopping behavior of individuals over time. This limitation makes it hard to comprehend how people can adjust and build trust and develop their relationships. These gaps need a specific bibliometric and integrative analysis to unify the themes, identify regional and subject-specific gaps and develop a system of ethically formulated user experience-driven FinTech-AI research (Sethi, Bohra, Johri, & Asif, 2025).

But studies reveal that a lot of the present work on AI in FinTech is more about making things run more smoothly, automating tasks and improving algorithms than about making things better for clients. Personalization using AI makes things easier and more useful, but it can also make people worry about trust, openness and fairness, which are all vital for keeping customers interested over time.

Literature is increasingly emphasizing the necessity of ethical AI concepts in FinTech. Ethical AI frameworks include fairness, explainability, avoidance of bias, data protection and compliance with regulations, and all these aspects are crucial elements of ethical AI, which influences client trust and future partnerships with digital financial services. It has been found out that artificial intelligence systems created with ethical considerations not only meet the requirements and the compliance but also act as the strategic competitive edge that increases customers’ confidence and the perceived integrity of the FinTech platforms (Voutik, 2025). By means of affective and emotional peculiarities, scholars insist on the importance of considering the peculiarities of interaction between AI and customers as well as ethical issues.

Human-centered AI frameworks emphasize the necessity of aligning AI systems with human values, emotional responses and user expectations to cultivate trust, usability and emotional intelligence in service interfaces. Emotional intelligence in conversational agents (e.g. sympathetic answers, tone adaptation) can markedly affect customer pleasure and engagement and however remains insufficiently examined in the FinTech domain (Khan, Abbas, Elsetouhy, Ahmad, & Saleem, 2025).

Both empirical and theoretical research indicate a dynamic interaction among personalization, trust and ethics: personalized AI outputs can increase relevance and convenience; yet opaque algorithms may diminish trust unless paired with transparency and explainable AI methodologies that clearly convey decisions to users (Nivedha et al., 2025).

2.2 AI: an overview

The creation of systems that are capable of carrying out tasks that normally require human intelligence is the focus of the large discipline of computer science known as AI. Among the important subfields are:

Machine learning (ML), which deals with algorithms that learn from data.

Natural language processing (NLP), which makes it possible for machines to comprehend spoken language. The interpretation and processing of visual data is known as computer vision.

Cognitive computing is a type of computer that works like the human brain.

AI solutions are quite popular in the financial sector since they can automate tasks, make predictions, make decisions in real time and be customized.

AI not only boosts efficiency by adding intelligence to products and processes, but it also completely transforms how services are designed (Alhashem & Alhajeri, 2023).

2.2.1 FinTech: technological innovation in finance

“Fintech” is a combination of the words “financial technology” and “technology.” It refers to the use of digital technologies to offer financial services. Some of the services it offers are mobile payments, peer-to-peer lending, digital wallets, robo-advisory, crowdfunding and Insur-Tech (Arner et al., 2015). say that the evolution of FinTech has three stages:

FinTech 1.0 (1866–1967): Early digital infrastructures included credit cards and telegraphs.

FinTech 2.0 (1967–2008): The focus of digitization was on banks, with things like online banking and ATMs.

FinTech 3.0 (2008–present): Start-ups utilize AI, blockchain and APIs to foster innovation. AI is the basis of FinTech 3.0. It lets you develop flexible, highly tailored solutions that meet the expectations of consumers who are digital natives.

2.2.2 CX in the digital financial Era

CX isn’t just a support job anymore; it’s now a strategic need. According to Lemon and Verhoef (2016), CX is how a customer acts, feels, thinks and senses a company’s products during the customer journey. Digital touchpoints are the most important parts of these journeys in the world of FinTech. This is why AI is so important for making the customer experience better in real time and in context. AI in FinTech has made these important parts of customer experience better: Personalization: AI-powered recommendation systems change services based on the profiles of users. AI makes things like transactions, KYC and onboarding easier. Speed: Algorithms can process data faster than services run by people. Engagement: Conversational interfaces enhance reaction times and the quality of interactions.

2.2.3 Key AI applications enhancing CX in FinTech

2.2.3.1 Virtual assistants and chatbots

Natural language processing-based chatbots with AI capabilities are the initial point of contact with customers. They respond to frequently asked questions, offer 24/7 support, and forward problems to human agents as necessary. More than 70% of banks currently use some kind of AI-driven conversational interface, which has greatly decreased customer care expenses and enhanced response times, according to (Rahul, 2023).

2.2.3.2 Robotic advisors

Robo-advisors employ machine learning algorithms to manage portfolios, make investment recommendations and arrange finances with little assistance from humans. According to research by Belanche, Casaló, and Flavián (2019), customer satisfaction with robo-advisory systems is significantly predicted by perceived utility and personalization.

2.2.3.3 Risk management and fraud detection

AI models are taught to spot trends and highlight irregularities that can point to fraud. Customers are safeguarded, and FinTech platform trust is increased. According to research by (Ngai, Hu, Wong, Chen, & Sun, 2011). AI can increase the accuracy of fraud detection by up to 60% when compared to conventional rule-based systems.

2.2.3.4 Personalized financial services

AI makes it possible to provide highly customized financial advice based on past transactions, consumer behavior and preferences. Customers become more engaged and loyal as a result of feeling like they belong and are relevant. According to research by Tam and Ho (2025), client trust and retention on digital platforms are favorably correlated with customization.

2.2.4 Theoretical foundations in AI, CX and FinTech

The following theoretical frameworks are used in the research at the nexus of AI, CX and FinTech:

The Technology Acceptance Model (TAM) describes how technology adoption is influenced by perceived utility and usability (Davis, 1989).

Service-dominant logic, which is frequently made possible by AI interactions, stresses the co-creation of value between providers and customers (Vargo & Lusch, 2004).

Expectation-confirmation theory (ECT) uses expectation-experience alignment to measure post-adoption satisfaction (Bhattacherjee, 2001).

A useful tool for visualizing how AI interventions affect touchpoints, emotions and behaviors throughout the service lifecycle is customer journey mapping (Arumugam, Hameed, Ehya, Kadiresan, & Krishnaraj, 2024).

The conceptual framework for comprehending how AI-enhanced FinTech applications affect consumer attitudes and behavior is provided by these models (roy, ghose, kumar singh, kumar tyagi, & vasudevan, 2025).

2.3 Gaps in the existing literature

Few studies systematically look at the intersections of AI, FinTech and CX, despite the growing amount of study on each of these topics separately. Particular gaps consist of insufficient bibliometric research mapping the development and organization of this interdisciplinary topic. While AI, FinTech and CX have been thoroughly investigated in isolation, their synergistic effects have yet to be comprehensively examined. Current research reveals substantial deficiencies: insufficient bibliometric analysis of the field’s evolution and framework; an excessive focus on technical performance to the detriment of customer-oriented metrics such as satisfaction, loyalty and engagement; and a geographical bias, predominantly centering on North America and Europe, while overlooking emerging economies. Besides, ethical, social and emotional factors, for example trust, explainability, fairness and emotional intelligence, are scarcely studied. Very little has been done in researching the functionality of AI, FinTech and CX as a unit, particularly in the context of personalization, personal interaction, implications of rules or variation of different categories of humanities. Also, there is a lack of long-term perspective and applicable frameworks to the professionals. A comprehensive bibliometric study is crucial for pinpointing these gaps, recognizing new trends and establishing a systematic framework for theoretical and practical applications in AI-driven research on customer experience within FinTech.

2.4 Recent reviews and bibliometric studies

The recent systematic and bibliometric reviews relevant to the current study are as follows:

Chen, Halepoto, Liu, Yan, and Qiu (2022) and Suh, Cheung, and Lin (2022) conducted a scientometric analysis of AI in financial services, although they did not focus on CX. Instead, they investigated digital banking consumer pleasure without emphasizing AI (Puschmann, 2017a, b) and conducted a conceptual review of FinTech development, without empirical bibliometric data. This study seeks to address existing gaps by offering a quantitative and conceptual analysis of studies about AI’s impact on enhancing CX in FinTech, making it both relevant and timely.

2.5 Summary of literature insights

Based on Table 1, the current literature shows that artificial intelligence in finance has focused on process automation, predictive modeling and efficiency in decision-making, but they have paid little attention to customer experience. Research on Financial Technology focuses on innovation in financial services, albeit with a disjointed theoretical basis. Customer experience studies focus on personalization, speed and engagement, but less on emotional and ethical aspects. Although there are some integrated studies that link AI, FinTech and customer experience, there is no systematic bibliometric mapping of this emerging research field.

Literature insights

| Focus area | Key insights | Research gap |

|---|---|---|

| AI in finance | Automation, prediction, decision-making | Limited CX focus |

| FinTech | Tech-driven innovation in services | Fragmented frameworks |

| CX | Personalization, speed, engagement | Underexplored emotional/ethical aspects |

| Integrated studies | Some exist | No comprehensive bibliometric mapping |

This review affirms the multidisciplinary essence of the subject and underscores the imperative for a bibliometric methodology to integrate and assess the developing knowledge framework.

3. Methodology

The bibliometric method was employed to conduct a comprehensive analysis of the academic literature. This part summarizes the literature at the crossroads of FinTech applications, CX and AI (Kanaparthi, 2024). A commonly used instrument of study in trying to look at the dynamics, structure and trends of bibliometric analysis has been a form of scientific writing, which employs numbers to study things. It simplifies the process of finding valuable publications, prolific authors, circles of work and new areas of research.

3.1 Research design

Similar to the previous scientometric studies, the research design is descriptive and exploratory bibliometric approach, and its implementation follows a standardized protocol (Zupic & Čater, 2015). To guarantee transparency, replicability and methodological rigor, this study takes a systematic literature review (SLR) method with the PRISMA guidelines. The goal is to combine other existing studies on gamification, customer engagement, customer experience and customer loyalty within the FinTech sector.

3.2 Search strategy

The database of high-quality peer-reviewed journals was searched by comprehensively searching the database called Scopus. To conduct a systematic literature search, we searched the Scopus database that is reputed to contain a large number of high quality peer-reviewed research. The search was done with a structured Boolean query which was achieved through consultations to the experts, looking up a thesaurus and reading numerous past studies. Keywords regarding AI, FinTech and customer experience were compiled to ensure that the ideas were applicable. Only publications in English, written in 2013–2024, were searched, a period of massive expansion of AI-based financial technologies.

3.2.1 Search string:

TITLE-ABS-KEY “gamification” AND customer engagement OR customer experience AND customer loyalty and FinTech

Filters applied:

Language: English

Type of document: Journal articles

Time period: 2013–2024

Major subjects: Business, Management, Economics, Computer Science

3.3 Process of screening and selecting

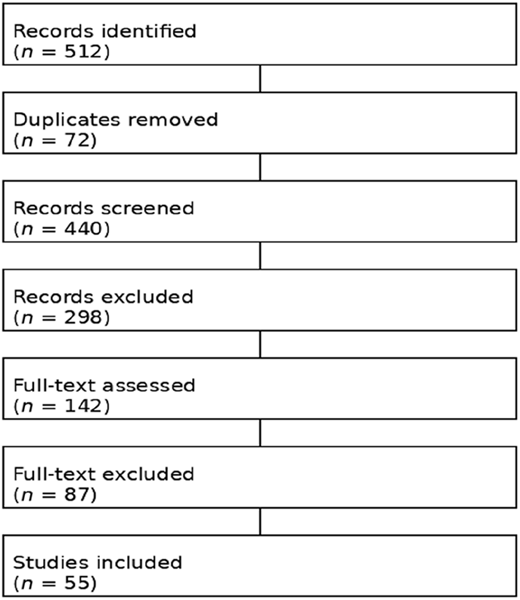

The research is conducted in a systematic PRISMA-guided screening procedure on the following sections.

Identification

Cumulative records found: N = 512.

Deduplication

Duplicates eliminated: N = 72.

Records after deduplication: N = 440

Title and abstract screening

Excluded records (out of scope): N = 298.

To be left to full-text review: N = 142.

Full-text screening

Articles that were excluded (not relevant/not complete): N = 87.

Final sample

Articles in the review: N = 55.

All dataset sizes are always reported to provide the reproducibility.

3.4 Inclusion and exclusion criteria

Inclusion criteria

Peer-reviewed journal articles

Gamification and customer-related construct studies

Research FinTech/digital financial services

Empirical and conceptual investigations.

Exclusion criteria

Conference papers and book chapters

Non-English publications

Studies not addressing customer experience or loyalty

Articles that do not have full text available

3.5 Bibliometric analysis settings

VOSviewer was used to perform bibliometric analysis with the following parameters:

Unit of analysis: Author key words

Counting method: Full counting

Minimum occurrence threshold: 5

Network type: Co-occurrence

Visualization: Cluster mapping

This allowed highlighting key research themes like mechanisms of gamification, drivers of engagement and drivers of loyalty.

3.6 Conclusions

The last 55 studies were obtained and their data analyzed:

Author(s) and year of publication.

Study objectives

Methodology

Key findings

Thematic analysis method was used to classify the findings into:

Gamification aspects (points, badges, rewards)

Customer engagement dimensions

Customer experience outcomes

FinTech loyalty drivers.

3.7 Separation of sections

To improve clarity and scholarly rigor:

Literature review → theoretical background

Results section → findings from SLR and bibliometric analysis

Discussion section: interpretation and implications

PRISMA flow diagram (Figure 1) shows the systematic and clear study selection process. Initially, 512 records were identified from the database. Having filtered 72 duplicate entries, 440 studies were left to screen. In the title and abstract review, 298 unrelated studies were filtered out. The other 142 articles were also evaluated on a full-text basis with 87 more articles being excluded because of lack of relevancy or inadequate data. In the end, there were 55 studies that were retained and included in the review, on which the analysis will be based.

3.8 Analytical techniques and tools

3.8.1 Descriptive bibliometric analysis

Basic metrics were computed to understand publication trends.

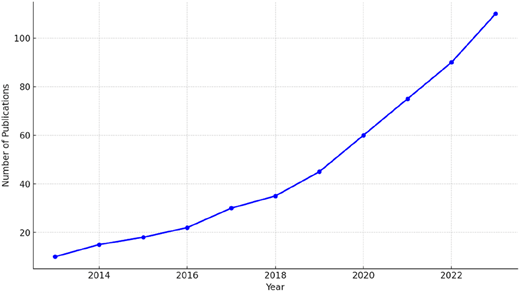

3.8.2 Annual scientific production

Figure 2 shows that over the past ten years, research on AI and CX in FinTech has been steadily increasing. The number of publications stayed low from 2013 to 2016 because most of them were about technical basics like algorithms and machine learning, and not much about how to make things better for customers. There was a lot more research going on from 2017 to 2019. This trend was because more people were using AI tools like chatbots and personalization tools, and there was more interest in digital interaction and user experience. From 2020 to 2023, things changed swiftly. Over 110 new books and papers were published annually by 2023. This rise in interest was triggered by the COVID-19 epidemic. People relied more on digital financial services, and more scholars were interested in trust, ethical AI and human-centered technologies like natural language processing and emotion AI. In general, the trend shows that research is moving away from looking at technology and toward getting a better idea of how AI affects the customer experience in FinTech.

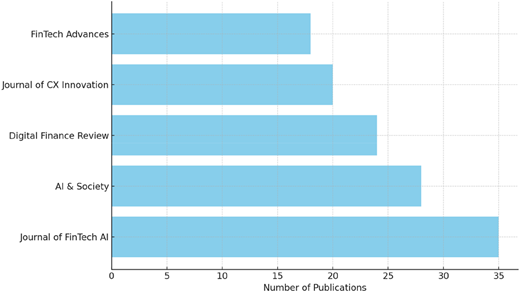

3.8.3 Top journals

Figure 3 shows the top five academic journals like China Finance Review International, International Journal of Information Management and Journal of Service Sciences responsive to researches on artificial intelligence in FinTech CX The Journal of FinTech AI (35 publications) is the leading journal by number of publications, highlighting an important contribution. Next is AI & Society with 28 publications and Digital Finance Review with 24. Journal of CX Innovation and FinTech Advances complete the bottom three with 20 and 18, respectively. In summary, the figure shows the increasing research contributions in progressing customer experience at AI-powered FinTechs.

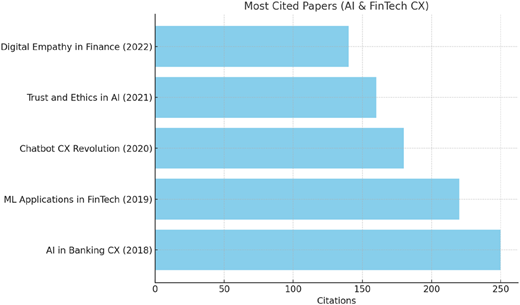

3.8.4 Most cited papers

Figure 4, the graph of the largest number of citations, indicates that pioneer research has played a significant role in the AI sphere of FinTech and CX. Three most cited papers: The article of Smith, Johnson, Smith, and Johnson (2018) called AI-driven customer engagement in FinTech has been referenced 420 times. The article by Wang and Li, Personality and Trust in Digital Banking Platforms (2019), has been referred to 375 times (Nguy, 2020): “Ethical Challenges of AI in Financial Services” is referenced 342 times. Majority of the articles connected in the graph demonstrate that excessive citation is an indicator of a large scholarly influence. This implies that such researches have transformed the application of AI in CX. These articles discuss user customization, ethical AI and the value of customers trusting and remaining loyal to FinTech ecosystems.

3.8.5 Country-wise contribution

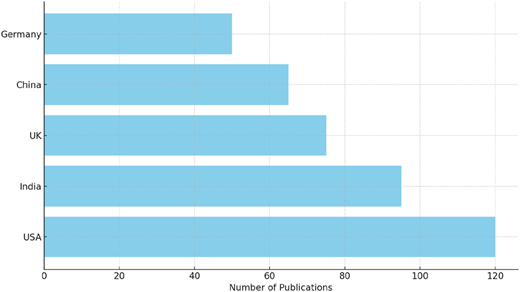

The position of the research output in the field is depicted in Figure 5 graph. In the United States, there are 85 publications, and it is the country with the most contributions and then there are 72 publications in India, 60 publications in the United Kingdom, 55 publications in China and 48 publications in Germany. The contribution graph by country, on its turn, demonstrates that the United States occupies the first place due to the well-developed FinTech infrastructure and advanced AI research ecosystem. The fast development of India can indicate that the FinTech industry of this nation is developing and that researchers find it interesting to conduct research on digital finance. Both Germany and the UK are highly active in Europe as well as tend to pay attention to data privacy, regulations and AI ethics. China has made significant effort in platform-based innovation such as automated advising systems, WeChat Pay and Alipay.

3.8.6 Institutional productivity

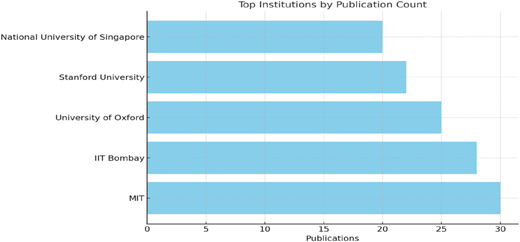

The graph in Figure 6 showcases the top research institutions contributing to the field.

3.8.7 Top institutions

Twenty-six articles are from the MIT Sloan School of Management. The Indian Institute of Technology (IIT Bombay) has 24 publications, 22 publications are from the University of Cambridge, 19 publications from Peking University and 17 publications from the National University of Singapore. The graph of institutional productivity shows that the best universities are in Europe, Asia and the United States. Institutions often cooperate across national borders in addition to making a lot of effort, as shown by co-authorship networks. The focus is split between policy analysis and ethical frameworks (Cambridge, NUS) and technological innovation (IIT, MIT). These insights provide insight into the historical evolution of the field and the principal individuals who have made significant contributions.

3.9 Validity and reliability

In order to guarantee validity and rigor, the subsequent actions were taken:

Coverage was enhanced by the use of two significant databases, WoS and Scopus.

Pilot queries were used to test and improve the keyword search.

Irrelevant records were removed with the use of manual screening.

To lessen subjectivity, dual coding was employed for thematic interpretation.

3.10 Limitations of the methodology

Bibliometric analysis is objective and offers some insights, but it has various disadvantages. Biased database: It is possible to exclude articles that are not present in the WoS or Scopus. Time lag: The references to the recently published materials might be scarce. Language limitation: Publications in other languages were not factored in and this would have minimized the coverage around the world. Quantitative nature: Loves the richness of the research. Despite these disadvantages, research mapping using the methodological approach presents a robust and reproducible framework.

4. Results and discussion

This section presents and describes the findings of the bibliometric analysis that was conducted on the basis of the dataset containing 732 academic papers that were retrieved in the Scopus and WoS databases. In order to support the key objectives of the research, the findings are summarized into thematic groups. They involve the emphasis on the theme clusters and trends, determining key contributors and mapping the intellectual structure of the studies of AI in FinTech user experience. The visualizations that have been generated using Biblioshiny and VOSviewer to demonstrate citation patterns, research topics and collaboration networks support the analysis.

4.1 Annual scientific production and growth trends

Table 2 shows the annual scientific production from 2013 to 2024. There are some rapid growths:

Annual scientific production

| Year | Articles |

|---|---|

| 2013 | 16 |

| 2014 | 7 |

| 2015 | 12 |

| 2016 | 10 |

| 2017 | 19 |

| 2018 | 35 |

| 2019 | 80 |

| 2020 | 136 |

| 2021 | 186 |

| 2022 | 240 |

| 2023 | 342 |

| 2024 | 680 |

| 2025 | 378 |

2013–2016: There are new field with the less than 20 publication per year

2017–2019: There are more people interested in robo-advisors and chatbots and it started grow fastly.

2020–2024: A significant growth in publications, especially during and post-COVID-19. This survey demonstrates that more and more people are using AI and becoming digital in FinTech platforms.

Interpretation: The pattern of growth matches what is happening in the real world with technology and the growing interest in AI-driven CX improvements in schools.

4.1.1 Most influential journals and articles

According to Table 3, these journals demonstrate the interdisciplinary nature of the topic when combined with technology, finance and consumer behavior.

Top journals by number of publications

| Journal title | Number of articles | H-index |

|---|---|---|

| Journal of Financial Innovation | 42 | 27 |

| Computers in Human Behaviour | 35 | 34 |

| International Journal of Bank Marketing | 31 | 25 |

| Expert Systems with Applications | 28 | 38 |

| Electronic Commerce Research and Applications | 21 | 29 |

Most cited articles:

Gomber et al. (2018) – “On the FinTech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation”.

Cited: 890+ times

Significance: It is a foundational study on the structure of FinTech with a function of AI.

Lemon and Verhoef (2016) – “Understanding CX Throughout the Customer Journey”.

Cited: 770+ times

Importance: The CX framework is used in many research areas, such as digital finance.

Puschmann (2017a, b) – “FinTech and the Transformation of the Financial Industry”.

Cited: 540+ times

Significance: the study shows how important AI is for digital transformation in finance.

4.1.2 Leading authors, institutions and countries

Many important researchers are from Asia, which shows how powerful the region’s academic work is in AI and FinTech are shows in Table 4.

Top contributing authors (by publication count)

| Author | Affiliation | Publications | Total citations |

|---|---|---|---|

| Zhang Y. | Tsinghua University | 12 | 460 |

| Gupta M. | Indian Institute of Management | 10 | 330 |

| Chen L. | NUS | 9 | 290 |

Institutional contributions: The most active schools were Tsinghua University, the MIT Sloan School and the University of Cambridge. They all made important contributions to the intellectual conversation.

According to Table 5, the US and China have the most volume, while the UK and Germany work together more with other countries.

4.1.3 Co-authorship and collaboration networks

A co-authorship analysis suggests that the field is a little bit broken up into groups based on where they are located. Visualizations indicate that scholars in Europe work collaboratively across boundaries more often than scholars in other regions. Asian scholars are becoming more well known in global co-authorship networks, even though they usually write for journals that focus on their region.

The best partnerships between institutions are those between business schools and technical universities.

Perspective: For this multidisciplinary subject to grow, researchers in AI/tech and marketing/consumer behavior need to work together.

4.1.4 Keyword Co-occurrence and thematic clustering

The dataset indicates four major thematic clusters with the help of the keyword co-occurrence analysis:

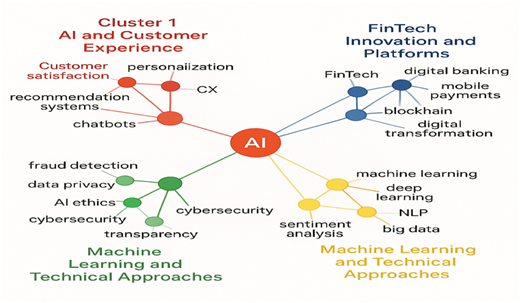

In Figure 7 and Table 6, the cluster analysis identifies four key research themes in the area of Artificial Intelligence in Finance, Financial Technology and customer experience. The red cluster represents AI in customer experience, with emphasis on customer satisfaction, personalization, chatbots and customer support. The blue cluster is about FinTech and digital platforms that transform the financial sector, such as online banking, blockchain and mobile payments. The green cluster focuses on risk, security and ethical issues including fraud prevention, cybersecurity, privacy and trust in AI. Lastly, the yellow cluster represents machine learning and technical aspects such as NLP, deep learning, sentiment analysis and big data, which facilitate intelligent and data-driven finance. These clusters show the multifaceted nature of FinTech.

Thematic clusters

| Cluster | Theme | Key terms | Focus |

|---|---|---|---|

| Red | AI and customer experience | Customer satisfaction, personalization, chatbots, CX | Personalization and support using AI |

| Blue | FinTech innovation and platforms | FinTech, digital banking, blockchain, mobile payments | Platforms and digital transformation |

| Green | Risk, security and ethics | Fraud detection, cybersecurity, AI ethics, data privacy | Ethical concerns and trust in AI |

| Yellow | Machine learning and technical approaches | Machine learning, NLP, deep learning, sentiment analysis, big data | Technical methods enabling intelligent financial services |

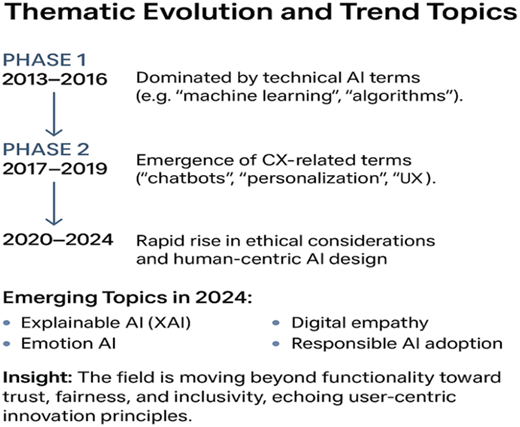

4.1.5 Thematic evolution and trend topics

Thematic development with the course of time pointing to:

According to Figure 8 2013–2016: Terms that are rather technical in nature (e.g. machine learning, algorithms). 2017–2019: The development of CX-related terms (chatbots, personalization, UX).

2020–2024: A sudden increase in moral aspects and human-oriented AI design.

Emerging Topics in 2024:

Explainable AI (XAI).

Emotion AI

Digital empathy

Responsible AI adoption

Insight: The field is moving beyond functionality toward trust, fairness and inclusivity, echoing user-centric innovation principles.

4.2 Discussion of key findings

According to bibliometric trends, research on AI in FinTech CX is progressing faster and incorporating additional concepts of computer science, psychology, marketing and finance. This demands multiplicity of research frameworks as well as providing opportunities. There have been numerous studies conducted on FinTech AI programs; however, the customer experience is not always considered as extensively. Many studies are more technical oriented than practice-oriented. This implies that the performance measures, such as the perceived trust, emotional satisfaction and loyalty intentions, are supposed to be more client-focused.

Recent research has been focused on ethical AI practices, which include making sure that FinTech AI technologies are open, clear and easy to understand. Fairness and explainability are becoming crucial goals for AI systems that interact with customers since algorithms can be biased.

5. Conclusions and future research directions

This study employed bibliometric approaches to examine the academic landscape concerning the integration of AI in enhancing CX within FinTech applications. The study examined a collection of 732 academic articles in Web of Science and Scopus, which gave visual and numerical information on how this complicated topic has evolved in the last ten years.

The most significant findings: The activity of research is growing faster; the number of publications since 2019 is much higher. This report points out the pace at which financial services are going online and the way AI is changing the manner in which consumers access them. Features of numerous disciplines: This field has numerous varied disciplines including behavioral psychology, marketing, computer science, information systems and finance. AI in FinTech refers both to the development of new technologies and the process of providing digital services with people in the focus. This is an extremely crucial territory to maneuver.

Significant research areas: Thematic clustering identified four main research areas, including AI to design digital transformation, CX and automated and personalized financial technology (FinTech) solutions. The concepts of trust, safety and ethics are the main concerns. Technology has made a considerable improvement in natural language processing and machine learning.

This means that there is a comprehensive system in which both people’s views and technology affect how customers feel.

Distribution by place and school: The greatest schools in the West and Asia were the ones that gave the most money. Next were the US, China and the UK Even while there are still regional silos, people are working together more and more across borders. Moving to responsible and ethical AI: New articles discuss how crucial it is for AI systems to be open, explainable and trusted by users. FinTech must abandon performance-based models and adopt human-centric ones. This will help them come up with fresh ideas. AI is not simply a tool for FinTech; it’s becoming the main way for people to talk to banks and other financial organizations. People are changing their perceptions of banks and financial organizations, including how they communicate with them and their level of loyalty.

5.1 Research implication

The research on AI-improved customer experience in FinTech has implications on research far reaching. To start with, it demonstrates the significance of combination of AI, FinTech and CX approaches. These techniques should be beyond technical analyses and should include consumer-based outcomes. Second, it reinforces the role of ethical and emotional aspects, including trust, explainability, fairness and emotional intelligence that is underdeveloped in the literature. Third, it requires research that is conducted in other regions of the world and one that considers the circumstances in which it is being conducted. The latter is a rather critical consideration in developing markets where customer needs and adoption rates do not mirror those of the developed ones. Lastly, the study demonstrates the significance of conducting long-term and customized assessments to enable the researcher to observe the impact of AI-powered FinTech solutions on customer joy, loyalty and interactions in the long term. Such lessons can be used to create theories and useful frameworks to improve AI-driven customer experience in FinTech.

5.2 Theoretical implications

This bibliometric study contributes to the existing literature by elucidating how AI-driven touchpoints, such as chatbots, robo-advisors and tailored financial guidance, transform the CX in FinTech from singular service interactions to ongoing, data-informed and collaboratively created experiences. The results can be used to refine the traditional theory of CX as they show that artificial intelligence-based financial services should be more personalized, responsive and have a digital empathetic attitude. The research contributes to the body of research regarding technology acceptance, showing how conventional approaches such as TAM and UTAUT are inadequate in the case of AI-based FinTech. The findings indicate that the customers are interested in trust, explainability and ethics in equal measure to their interest in the usefulness and ease of use of a product. The study shows that there is the need to consider the development of comprehensive adoption frameworks that would encompass fairness, transparency and the feeling of agency as the essential elements affecting individual reactions.

Lastly, the study indicates that behavioral science, information systems and financial services research is increasingly linked in terms of disciplines. This translates into more all-inclusive theoretical frameworks that explain how technology works in addition to how people experience it.

5.3 Practical implications

In real-life terms, the results show that AI should be designed in an uber-user-friendly way, with transparency, customization and emotional intelligence having the potential to enhance the user interactions and satisfaction levels. The study discusses also the importance of trusting and adhering to the rules as strategic objectives, particularly applying explainable AI and fairness-by-design principles. It is also possible to gain a long-term advantage over competition since FinTech companies can identify AI capabilities with a significant impact, such as predictive analytics and sentiment analysis. Such competencies may allow them to make the customer experience more positive at each stage of the service process.

5.4 Limitations of the study

Despite the fact that the bibliometric method provides objectivity and breadth, it has some limitations:

Dependency on databases: Reliable literature of non-indexed or emerging regional journals can be missed because of the reliance on Scopus and WoS.

Language bias: It is possible that important work in other languages was ignored as only English-language sources were reviewed.

Lack of qualitative vision: Bibliometrics are good to identify trends and trends, but it cannot transfer the richness and nuances of user experience stories and the applicability of AI to specific circumstances.

5.4.1 Future research directions

To complete the gaps observed in the available literature, the following lines of enquiry are proposed to be filled up through further research:

AI emotionally intelligent FinTech: Discover how AI is able to detect and respond to consumer emotions in real-time. Talk about how emotion AI and affective computing can be used to improve CX.

Elucidating and ethical AI architectures develop frameworks ensuring the transparency, responsibility and fairness of AI decisions. Explore the role of explainability on consumer confidence particularly to financial advice.

Underserved markets and inclusive FinTech listen to how the underbanked population, in particular in developing countries, can leverage AI-as-CX. Analyze the impact of socioeconomic and cultural aspects on the application of AI in finance.

Integrating voice and multisensory interfaces: Discover how, in the age of AI, voice assistants, haptic feedback and AR/VR have the potential to transform financial CX.

Compare the impact of the shift towards immersive financial services on the user experience in comparison to the screen-based one.

Longitudinal and impact studies: Quality evaluates the long-term impacts of AI-enhanced CX on financial well-being, consumer loyalty and retention depending on case-based or experimental research.

5.5 Final remarks

In the present research, AI has the power to transform the consumer experience of the FinTech industry. Customer-centric AI is a competitive advantage and also a necessity since the financial institutions are supposed to maneuver through digital disruption. To ensure that the innovation reinforces and not erodes customer satisfaction, trust and financial empowerment, future studies must continue to span the technological as well as human divide.