This paper aims to systematically review the existing studies on the relationship of Sharī'ah governance (SG), as represented by the Sharī'ah supervisory board (SSB), with firm performance of Islamic banks (IBs), to suggest opportunities for future research in this field.

By adopting a systematic literature review, 21 empirical and theoretical papers published in Scopus concerning the relationship between SSB and performance of IBs were selected for review and analysis.

In light of the existing research studies' limitations, this paper suggests that the effect of SSB on IBs' performance still requires more empirical analyses using alternative analytical methods, alternative measures, and different periods (during crisis and non-crisis). Besides that, these studies should take into account the differences across jurisdictions in their SG models, the degree of agencies' intervention in SG practices, the control over cross-memberships of scholars, and the differences across IBs in the position of SSB in the organization structure.

The analysis undertaken in this paper would address the literature gaps on the effect of SSB on IBs' performance as this study serves as a guide for the researchers, academicians, and interested researchers from Islamic international autonomous non-for-profit organizations, e.g. AAOIFI and IFSB in research related to this important area. Importantly, the findings of this study would support regulators and related authorities across jurisdictions with suggestions on improving the current SG practices.

This paper presents a critical review of the existing research on SSB and IB performance and suggests new variables, measurements, analytical methods, and new issues for researchers in this area. Thus, it identifies the literature gap that still needs further empirical investigation and a suitable way to close it.

1. Introduction

The Islamic banking industry has grown rapidly since the early 2000s (Safiullah and Shamsuddin, 2018). Islamic banks (IBs) differ from their conventional counterparts in their functions, structure, and objectives (Mohammed and Muhammed, 2017a). The main difference distinguishing the IBs from conventional banks (CBs) is the absolute prohibition of interest (riba) (Ghayad, 2008) and business relating to alcohol, gambling, and excessive speculation (Zirek et al., 2016). Basically, IBs must guarantee that all of their products and operations are compliant with the Sharī'ah rules and principles (Grais and Pellegrini, 2006a). Thus, the governance structure of IBs requires them to establish Sharī'ah supervisory boards (SSBs) besides the usual boards of directors (BoDs) (Alnasser and Muhammed, 2012; Nomran et al., 2018). This extra layer of governance, as represented by the SSB, aims to monitor, approve, and report on IBs' compliance with moral values (Abdelsalam et al., 2016; Shibani and De Fuentes, 2017).

It is the main responsibility of the SSB to closely supervise the implementation of the Sharī'ah principles throughout the operations of IBs (Nomran et al., 2017). As a result of non-compliance with Sharī'ah rules, depositors may withdraw their deposits and investors may cancel their investment agreements, which would decrease the IBs' profitability and increase bank risk[1] (Hamza, 2013; Grassa, 2015). In brief, if the IBs become non-Sharī'ah compliant, their position in the market will be negatively affected due to lack of customers' confidence (Alnasser and Muhammed, 2012; Hamza, 2013; Grassa, 2015) and consequently decreasing these banks' profitability and increasing their risks (Hamza, 2013; Grassa, 2015). Given that SSB supervises bank investment, banks cannot invest beyond the SSB-approved investments even if they can earn a higher rate of returns (Ullah and Khanam, 2018).

Generally speaking, the importance of corporate governance (CG) implementations has increased in the business environment especially after the financial crises, i.e. the Asian financial crisis of 1997 and the global financial crisis of 2008. There is no doubt that good CG has a positive impact on performance, where most of the studies confirm that good governance improves firms' profitability, productivity, and competitiveness and decreases risk (Claessens, 2006; Todorovic, 2013; Riwayati et al., 2016; Ciftci et al., 2019).

In the Islamic banking context, IBs have “multi-layer” governance[2], i.e. SSBs besides the BoDs, which acts as dual internal governance mechanisms affecting IB performance[3]. As the BoD is a powerful internal governance mechanism affecting IB performance, the SSB is also an important stakeholder that affects their performance (Mohammed and Muhammed, 2017a). The decision-making of management in the IBs is indeed constrained by an SSB that rejects any proposals in light of the Sharī'ah principles (Ghayad, 2008); therefore, BoD is obliged to obey the SSB decision (Alnasser and Muhammed, 2012). The nature of the SSB decision may influence the acceptance of one product over another, hence; the SSB certification of approval could increase or decrease the volume of banking business, especially when no rights are given for the management to involve in the SSB decision (Mohammed and Muhammed, 2017a). In addition, the SSB role means that products are likely to be Sharī'ah compliant and less risky, and then, it ameliorates the negative effects of excessive risk-taking, thus contributing to better performance of IBs (Mollah and Zaman, 2015; Nomran and Haron, 2020).

However, as most studies on Islamic banking are normative and/or theoretical in nature, thus the need for more empirical studies, especially on the CG of IBs, is imperative (Mollah and Zaman, 2015; Ajili and Bouri, 2018). More precisely, there is a lack of studies on the impact of Sharī'ah governance (SG), as represented by SSB, on IB performance across jurisdictions (Hasan, 2011; Musibah and Alfattani, 2014; Grassa, 2016). The majority of these studies are theoretical, and they have been carried out to examine the function of SSB and the issues surrounding its function. In contrast, the empirical studies on the SG issues are limited in general and focus on the relationship between SSB and performance of IBs in particular. Therefore, the main objective of this paper is to review the existing studies on the relationship of SG mechanism, as represented by SSB, with firm performance of IBs, to suggest opportunities for future research in this field. A systematic literature review is used to achieve this objective.

The paper is organized into eight sections. The second section deals with the theoretical background of this paper. The third section explains the methodology employed, followed by the fourth section which presents the main findings from the systematic literature review. The fifth section suggests some recommendations for future research developments, while the sixth one concludes the paper. Lastly, the seventh section discusses implications for research and practice.

2. Theoretical background

This section summarizes the theoretical predictions on the effects of SSB on IB performance. Agency theory (AGT) and stakeholder theory (SKT) are the two popular CG-related theories of boards and governance mechanisms that can justify the impact of SSB on IB performance. From the AGT perspective, governance mechanisms aim to guarantee agent–principal benefits alignment, safeguard shareholder benefits, mitigate agency costs (Davis et al., 1997), and hence improve the companies' performance (Demsetz and Lehn, 1985).

As mentioned above, IBs are subject to two internal mechanisms of CG, the BoD and the SSB, as a necessary alteration has been made by adding into another layer to the governance from “single layer” as in the conventional ones into “multi-layer” governance (Mollah and Zaman, 2015; Abdelsalam et al., 2016; Almutairi and Quttainah, 2017; Shibani and De Fuentes, 2017; Safiullah and Shamsuddin, 2018). While BoD represents the first layer of governance mechanism that provides legal oversight, SSB represents the second layer of governance mechanism that provides moral oversight (see, e.g., Abdelsalam et al., 2016; Shibani and De Fuentes, 2017). Indeed, BoD gives more attention to the conventional legal liability compared to the moral liability[4]. It has been found that SSBs of IBs affect and shape managerial behavior and mitigate agency problems (Quttainah and Almutairi, 2017). SSB plays an important role in mitigating agency problems by acting as an additional monitoring mechanism (see, e.g., Abdelsalam et al., 2016; Shibani and De Fuentes, 2017; Quttainah and Almutairi, 2017).

From the SKT perspective, Mohammed and Muhammed (2017b) argue that the SSB plays an important role in influencing the performance of IBs as it has been selected among the four key stakeholders that affect the financial performance of IBs besides the management (BoD and CEO), the ownership, and the external auditor based on the Islamic stakeholder model. SSB is an important stakeholder in Islamic banking due to its role of ensuring that the operations of IBs are Sharī'ah compliant through approving their transactions and activities (Mohammed and Muhammed, 2017b). However, it is important to mention that the stakeholders of IBs are not restricted to these key groups. As Dusuki (2008) indicates, the stakeholders' groups for IBs involve clients, depositors, employees, IB managers, Sharī'ah scholars, local communities, as well as the regulatory authorities.

3. Methodology

Given the objective of this paper, the matter that has been taken into consideration for the subsequent systematic literature review is the relationship between SG mechanism, SSB, and performance of IBs. The adopted methodology in this paper, i.e. a systematic literature review, is inspired by the previous studies (see, e.g., E-Vahdati et al., 2019; Le et al., 2019).

3.1 Information sources and period

The systematic literature review was conducted for the relevant papers on Scopus published during the period 1999–2018 in English. The rationale for the year 1999 selection to start the review is to ensure reviewing most of the related literature. This is due to the increased importance of CG implementations, in general, in the business environment, especially after the Asian financial crisis of 1997.

3.2 Search strategy

To conduct the search, related key terms were used as shown in Appendix 1. The authors combined each of the two keywords representing dependent (performance) and independent (SG mechanism) variables in the search field using Boolean search AND, and then they selected papers with these keywords in at least one of the following fields, namely, title, abstract, and keywords.

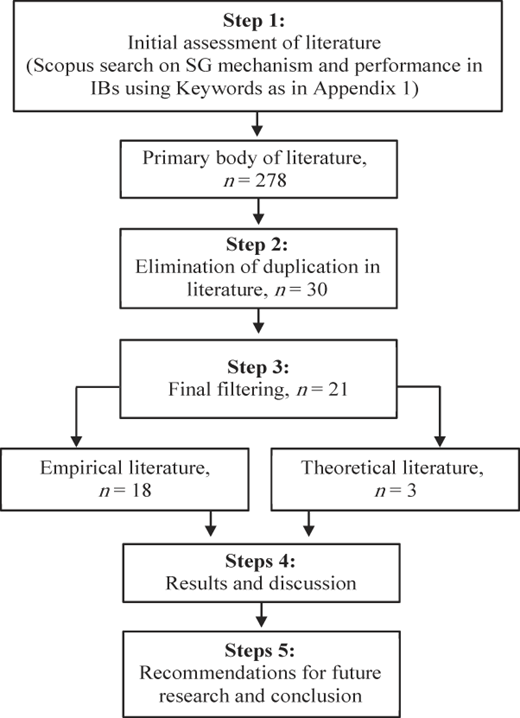

However, the data collection and analysis process is made up of five steps as implemented by E-Vahdati et al. (2019). Following E-Vahdati et al., (2019) first, 278 papers on Scopus were selected after filtering the results via a Boolean search AND based on the basis of their relevance to the purpose of this work using the related keywords[5]. Second, the duplicates were eliminated and store literature as per their respective keywords (see Appendix 1) in titles and abstracts besides introducing restrictions that would limit the search to only the relevant fields such as years and language, and this resulted in a total of 30 papers. Third, the collected papers' contents also were fully reviewed, and only the papers that highlighted the relationship between SG mechanism and performance of IBs were selected for the final analysis. Based on the additional filtering in this step, 21 papers were selected. Step four is related to the results as will be shown later, while the final step is related to the recommendations for future research and conclusion. Figure 1 provides a summary of the five steps mentioned that explain data collection and analysis process.

4. Results

Table I summarized the final collection of papers based on authors, date of publication, nature of studies, and journals' names. As Table I shows, there are 17 refereed journals that published 21 papers on the relationship between SG mechanism, as represented by the SSB, and IB performance. Out of the 21 papers, 18 papers are empirical while three are theoretical and/or qualitative studies. These studies were published during the period (2014–2018) with the exception of one study which was published in 2008.

4.1 Empirical studies on the impact of SSBs on IBs' performance

Research on SG in Islamic banking is not only limited, but there is a lack of studies that investigate the impact of SSB on the performance of IBs (Nathan, 2010; Mollah and Zaman, 2015; Hakimi et al., 2018). Most of the empirical studies on SG examined the impact of SSB characteristics on disclosure (see, e.g., Farook and Lanis, 2007; Farook et al., 2011; Rahman and Bukair, 2013; Abdullah et al., 2014), on earnings management (see, e.g., Quttainah et al., 2013; Quttainah and Almutairi, 2017) and on credit ratings of IBs (Grassa, 2016). Nevertheless, literature shows that some empirical studies have been conducted to examine the impact of SSB characteristics on financial performance as presented in Table I. In order to provide a wide view regarding the impact of SSB on the IBs' performance, this section discusses these studies in the following part.

Abdel-Baki and Leone Sciabolazza (2014) examined CG on performance of IBs using CG index which was built based on a cross-country survey of 72 IBs in 14 Middle East and Asian countries while the financial data were collected from the website of the Thomson Reuters Eikon. The CG index consists of six core CG themes and 40 sub-themes. Among these 40 sub-themes, there are six sub-themes items related to SSB which are whether remuneration of SSB members solely decided by a BoD and approved by shareholders, and SSB size, SSB cross-membership, disclosure about the decisions of SSB, and whether Sharī'ah auditors countercheck decisions of SSB.

A study was conducted by Grassa and Matoussi (2014a) examining the impact of CG characteristics of IBs, including SSB characteristics, on the financial performance of 77 IBs and 85 CBs in GCC countries and Southeast Asian countries for the period 2000–2009. After controlling for bank age and size, the study examined many explanatory variables which can be divided into three groups. The first and second groups are related to the characteristics of the BoD and CEO. The third group shows the SSB characteristics which are SSB size, SSB cross-membership, SSB scholars with accounting/finance knowledge and the number of women on SSB. They found that BoD' fees and CEO duality and age positively affect the performance of IBs. SSB with accounting/finance knowledge have a positive and significant impact on the performance of IBs. Results indicated that SSB size and cross-membership negatively affect the performance of IBs in Southeast Asian countries. It has been found that there is no impact for SSB gender (women) on IBs performance. The study concluded that CG characteristics of IBs in GCC countries and Southeast Asian countries are different.

Musibah and Alfattani (2014) examined the impact of SSB effectiveness and intellectual capital on corporate social responsibility (CSR) of 36 IBs from GCC countries for the period 2007–2011. They also investigated the mediating impact of IB performance in the above relationship. The education level of SSB scholars (shaikh, doctor, doctor shaikh) was used as a measurement for SSB effectiveness, while ROA and ROE were employed as measurements for IB performance. The study found a positive impact for SSB effectiveness, capital employee, and structure capital on the CSR of IBs. It was found that the SSB education level affects IB performance positively. The study concluded that IB performance mediates the relationship between SSB effectiveness, capital employee, structure capital, and the CSR of IBs.

Another study on the same context is conducted by Mollah and Zaman (2015). This study investigated the impact of SSB size, BoD structure, and CEO power on financial performance of 86 IBs and 86 CBs across 25 countries for the period of 2005–2011 including the 2008 crisis. The study aims to investigate if Sharī'ah supervisory functions, as measured by SSB size, improves IB performance and then enhances shareholders' value. The regression was conducted by employing random-effect GLS method based on secondary data collected from Bankscope and annual report of the banks. The researchers supported the results of Sharī'ah supervision from the regression tests by using a survey with response rate of almost 15% from 11 responses across six countries. The performance was measured by using five measurements, namely, ROIAE (operating profit divided by average equity), ROIAA (operating profit divided by total assets), ROAE (net income divided by average total equity), ROAA, and Tobin's Q. The study concluded that IB performance is affected by SSB, BoD, and CEO power. It is found that the impact of SSB on IB performance is positive, especially when SSBs have a supervisory role. The findings also revealed that SSB size influences IB performance positively during the crisis period. The study concluded that the “multi-layer” CG approach, as applied in IBs, helps them to have a better performance compared to the CBs.

Rahim and Mahat (2015) investigated the effects of risk management (RM) and CG on IB performance. Then they investigated the mediating effects of risk governance (RG) on the relationship between RG and CG and IB performance. They employed cross-sectional sample of 200 IBs across 21 countries for the year 2014. To measure RM, CG, and RG, they used many variables, namely, RM: loan loss provision (LLP), capital adequacy ratio (CAR), total deposit ratio (TDP), GDP, central bank lending rate (CBLR), and inflation (INF); CG: CEO, BoD size, remuneration meeting (REM), external audit (EA), accounting standard (AS), and credit rating agency (CRA); and RG: chief risk officer (CRO), risk committee member (RCM), and SSB member. They found that RM and RG affect performance, and RG has a mediating effect as expected.

Kusuma and Ayumardani (2016) analyzed the efficiency of the CG and its impacts on Indonesian IBs using quarterly data for the period between 2010 and 2014. They used a measurement of CG efficiency consisting of three variables, namely, BoD size, board commissioner size, and SSB size. The Data Envelopment Analysis (DEA) was employed to measure CG efficiency, while regression analysis was used to analyze the relationship between CG and IB performance. The study found that the efficiency level of CG of Indonesian IBs improved significantly during the study period. Additionally, it was found that CG efficiency significantly affects IB performance.

Almutairi and Quttainah (2017) conducted a study to investigate the effects of SSB characteristics on IB performance based on a sample of 82 banks from 15 countries over the period 1993–2014. They found that IBs with SSBs outperform IBs without SSBs and performed better in monitoring management behavior. It was also found that integrating SSBs into IB governance structures improves strategic design and implementation and offers more guidance to directors, managers, and employees. Furthermore, SSB characteristics (size, membership of AAOIFI, cross-membership, and education) are associated with better financial performance.

Mollah et al. (2017) conducted a study to examine whether the differences in CG structures of IBs and CBs have any impact on the risk-taking and performance of the banks by selecting 52 IBs and 104 CBs from 14 countries for the period between 2005 and 2013. Given that an SG system does not exist in the CBs, therefore, the authors developed CG index by combining the BoD and CEO characteristics that exist in the IBs and CBs. They assumed that IBs reflect the Sharī'ah-supervised governance structure as these banks have an SG system. The study found that CG structure in IBs enables them to take higher risks and have better performance compared to the CBs. The authors justified this result by arguing that IBs have different financial contracts than the SSBs and also a different CG structure which influences the risk-taking and performance of IBs. The study suggested that researchers should give more attention on the role of the SSB.

Nawaz (2017a) examined the impact of investments in human capital (HCI) and investments in structural capital (SCI) and CG attributes on market-based performance of 67 IBs during the period 2006–2009. Four CG attributes were investigated, namely, BoD size, BoD composition, the role of duality (CEO power), and SSB size. The findings indicated that HCI have a significantly positive impact on the market value of IBs. The results further reveal that IBs' strategy to rely on long-term human capital accumulation can be seen as idiosyncratic problem-solving knowledge capital. The paper found that both BoD size and role duality have significant positive impact on bank performance. In contrast, it is found that SSB has a negative impact on market value, indicating that the market does not favour larger SSB in the presence of a large-sized governing board.

Nawaz (2017b) also examined the effect of intellectual coefficient of IC (VAIC), human capital efficiency (HCE), structural capital efficiency (SCE), capital employed efficiency (CEE), and SG, as measured by SSB size, on performance of 47 IBs in the GCC region over the period 2006–2010. The study took into consideration the pre-crisis period (2006–2007) and post-crisis period (2009–2010). The findings indicated that higher IC efficiency helps IBs to improve their performance (ROA and Tobin's Q) both before- and after-crisis periods. The study concluded that knowledge resource, i.e. IC, is the main line of defense for IBs against negative shocks. Finally, the study asserted that SG alone may fall short in explaining the growth trends in the Islamic finance industry.

Similarly, Nawaz (2017c) examined the effect of HCI and CG features on the market performance of 47 IBs during the period 2005–2010. Five CG attributes were investigated, namely, BoD size, BoD independence, SSB size, CEO power, and audit committee size. The study found that HCI has a positive effect on the market performance in the pre- and post-financial crisis period. Further, it was found that BoD size and CEO power have a significant positive impact, while the SSB size has the opposite effect on market performance. Overall, the analysis suggested that the financial crisis may have further spurred the impact of investments in human capital on the market performance.

Quttainah et al. (2017) investigated the impact of CG on the financial performance of 34 IBs and 607 IB-year observations across 15 countries, with a specific focus on their SSB. They found that IBs with SSBs embedded into their governance structures outperform those without such integrated boards. Additionally, it was found that SSB characteristics, including size, interlocks, and education affect the financial performance of IBs with such boards. The study concluded that SSBs provide tighter monitoring and control, as well as more advising and counselling, compared with IBs without dedicated SSBs. In short, the study confirmed that SSBs benefit IBs' shareholders by complementing corporate boards and thus mitigating agency problems and agency costs.

Recently, Ajili and Bouri (2018) examined the impact of CG on the performance of 44 IBs from GCC countries for the period 2010–2014. The findings indicated that IBs in GCC countries give more attention to the effectiveness of SSB as compared to the other CG mechanisms. The study shows that there is no significant impact of CG on IB performance in GCC countries. As the authors argue, the potential reason is that good CG of IBs in the GCC countries was not oriented to maximize the performance of shareholders. Furthermore, they concluded that the role of most SSBs in GCC IBs is advisory as compared to those boards that have a supervisory role. However, the study suggested that regulatory authorities in the GCC countries should improve CG practices.

Farag et al. (2018) examined the impact of dual board structure (BoD and SSB) on the performance of 90 IBs from 13 countries. They also examined how BoD size and SSB size are determined. The authors employed a fixed effects model and GMM estimation to analyze the data. The findings indicated that SSB size is related positively to the performance of IBs. In addition, a weak positive impact for the BoD size on performance is recorded. On the other hand, the study concluded that IBs' size and age affect boards' size (BoD and SSB) positively.

Hakimi et al. (2018) examined the effects of BoD and SSB on the performance of 13 IBs from Bahrain for the period of 2005–2011. Based on panel data analysis and the GMM technique, they found that BoD duality, BoD size, and SSB size are the corporate boards' characteristics affecting the performance of Bahrain IBs positively. In contrast, the BoD independence and SSB expertise in finance and accounting do not have any significant impact on the performance.

Mezzi (2018) examined the impact of CG mechanisms on the performance of IBs by employing efficiency as the performance measurement. The study found a positive and significant impact of BoD size, BoD independence, and the existence of centralized SG model (CSGM) on the efficiency of IBs. A positive and significant relationship was also found between concentration of ownership and the efficiency of IBs although it is a weak relationship.

Nomran et al. (2018) examined the effects of SSB characteristics on IBs' performance in Malaysia being a country that applies the most extreme intervention of regulatory agencies (pro-active model). The study employed a sample of 15 Malaysian IBs for the period 2008–2015 using the GMM as estimator. The results revealed strong support for a significant association between SSB size, doctoral qualification, change in the SSB composition and performance. In addition, the study supports the view that SSB with cross-membership and reputation are crucial in improving the performance of IBs.

Lastly, Zeineb and Mensi (2018) examined the effect of CG on efficiency and risk of 56 GCC IBs during the period 2004–2013. They included five CG variables, namely, SSB size, CEO duality, institutional, private, and foreign ownership. The findings indicated that implementing rigorous CG structures correlate with higher efficiency levels. Moreover, it was found that the governance structure of IBs allows them to take higher risk to achieve a high efficiency level. Furthermore, the findings show that IB efficiency and risk are positively related.

4.1.1 Critical analysis of the above empirical studies

Table II provides a summary for the above-mentioned empirical studies that investigated the impact of SSB on IBs' performance. As Table II presents, most of these studies suffer from some limitations that suggest a need for more empirical analysis. Empirical studies in the field of SSB and performance of IBs is important as it would support regulators and related authorities across jurisdictions with suggestions on improving the current SG practices.

4.2 Theoretical studies on the impact of SSBs on IBs' performance

There are, however, at least two theoretical studies that provide a theoretical justification for the relationship between the SSB and IB performance (see, Ghayad, 2008; Mohammed and Muhammed, 2017b), while the third study is conducted based on qualitative method (see, Ullah and Khanam, 2018).

Ghayad (2008) conducted a study to explore how CG can influence IB performance based on case studies from one country only (Bahrain) without providing any empirical evidence. The results revealed that managerial factors play an important role in affecting the performance of IBs besides internal factor such as the financial ratios. Moreover, IB directors are subjected to the governance of the BoD and additional crucial governance of the SSB. The study confirmed that it is necessary for the SSB members to be qualified in finance and economic fields. The study suggested that Investment Account Holder (IAH) should be given seats in the board of IBs in order to enhance the CG. The main limitation of the study is the absence of empirical evidence to support the argument.

Mohammed and Muhammed (2017b) also conducted a study to examine the AGT and the SKT from the perspective of the Islamic principles. To do so, they adopted a critical review method which takes into consideration presenting important theories and comparing those theories with an Islamic perspective. The paper highlighted the important discussion on the difference between ordinary theories to explaining CG and Islamic perspective. The paper browsed into whether the SSB fits with the AGT by explaining the AGT and how it differs from the Islamic banking concepts. The paper involved an analytical review on SKT and presented a critique and the rationale as to why there is ample room for the SSB to be considered fit with the SKT, as the SSB is an independent body influencing the IBs.

Finally, the study of Ullah and Khanam (2018) linked the SSB to the performance of IBs but based on qualitative method. They investigated the impact of Sharī'ah compliance on the financial performance of a bank, i.e. Islamic Bank Bangladesh Limited, as a case study. To address this question, the authors conducted interviews with related parties such as financial analysts and executives of regulatory bodies. The findings of the study asserted that the Sharī'ah compliance processing in the banks positively related to the outstanding financial performance as the level of Sharī'ah compliance is the dominant instinct in acquiring a leading position. However, the limitation of the study is that it focused only on one bank coupled with the absence of quantitative evidence.

However, the main limitation of the above theoretical studies is the absence of empirical evidence to support the argument.

4.3 General studies of Sharī'ah supervisory function, issues, and practices

The above section discussed the existing empirical and theoretical studies that linked SSB to IB performance based on the study objective. As explained above, the majority of these studies have some limitations that suggest a need for more empirical analysis and then can be recommended for future research. However, before suggesting the research areas for future studies in light of the above-mentioned critical review, it seems important to explore any other important related issues on SSB by reviewing the existing theoretical studies of Sharī'ah supervision in IBs as a whole. This would help in identifying important issues that require more empirical support for future research besides the weaknesses that have been discovered in the above-reviewed literature as explained in Table II. These studies are related to the Sharī'ah supervisory function, issues, and practices.

Several studies have discussed the CG from an Islamic perspective, current SG practices and issues, challenges of good SG, different SG models and systems across jurisdictions (see, e.g., Grais and Pellegrini, 2006a; Grais and Pellegrini, 2006b; Hasan, 2009; Nathan Garas and Pierce, 2010; Nathan, 2010; Hasan, 2011; Abdullah Saif Alnasser and Muhammed, 2012; Nathan Garas, 2012a, 2012b; Grassa, 2013; Hamza, 2013; Grassa and Matoussi, 2014b; Ayedh and Echchabi, 2015; Sulaiman et al., 2015; Grassa, 2015).

However, some of these studies are descriptive (see, e.g., Hasan, 2011; Grassa and Matoussi, 2014b), while some other studies are empirical (see, e.g., Nathan, 2010; Nathan Garas, 2012a). Despite the last two studies being empirical, they only focused on the SSB performance and function, and they did not link the SSB to the bank performance. The following part discusses some of these studies, highlighting the most important issues on the SG practices.

Grais and Pellegrini (2006a) examined the challenges facing SG regulations in ensuring Sharī'ah compliance activities in IFIs across 11 countries. Particularly, the study focused on the challenges facing SSBs at institutional and national levels in conducting their roles. The findings revealed that SSBs are the most important CG instruments in ensuring Sharī'ah compliance in IFIs and enhance their stakeholders' confidence. In addition, SSBs suffer from many challenges that affect their performance such as the members' independence and the confidentiality of banks' information. Furthermore, there is a lack of qualified scholars who have enough knowledge in finance besides the Sharī'ah. The study suggested that it is better for the SSBs in IFIs to have consistent opinions.

Moreover, Grais and Pellegrini (2006b) provided another analytical study on the CG practices for 13 IFIs in 16 countries. By comparing the SSB disclosure score across the IFIs, the study concluded that IFIs have weak disclosure pertaining to SSB background, SSB fatwas, and responsibilities. The study also found that there is a need for more competent and independent SSBs in IFIs.

In an attempt to explore the differences in the SG regulatory systems across jurisdictions, Hasan (2009) examined the SG systems in Malaysia, GCC countries, and the UK as these countries reflect different legal environments (mixed, Islamic, and the Western). By comparing the different frameworks of SG in different environments, Hasan (2009) found that countries can be classified from SG regulatory perspective into regulated and unregulated. More specifically, countries can be classified based on the degree of intervention of regulatory agencies into five groups, namely, reactive, passive, minimalist, pro-active, and interventionist. The findings of the study revealed that the regulatory SG of Malaysia is very strong as compared to the other systems in the UK and GCC countries. It was recommended that countries should have a clear legal framework and a sound SG system.

Another study on SSB function of IFIs is by Nathan Garas and Pierce (2010). This study investigated the significance, objectives, and roles of SSB in IFIs by reviewing many theoretical studies. The findings revealed that SSB is the most important instrument to ensure Sharī'ah compliance in IFIs. The study provided some suggestions which could improve the performance of Sharī'ah supervision. These suggestions include the issuance of specific regulations about the selection of SSB scholars and controlling the SSB cross-memberships by the regulatory authorities. Adding to that, the IFIs should apply the AAOIFI standards in their practice and operation. To ensure a more independent SSB, the authors suggested that the position of SSB should be located under the shareholders and not under the BoD. They confirmed that SSB should have more knowledge in financial, economic, and commercial fields.

Nathan (2010) empirically evaluated the function and performance of SSB in IFIs of the GCC countries. In undertaking his study, data were collected from 219 IFIs in 2009 through a questionnaire as his research tool. The study examined the impact of five explanatory variables on SSB performance. These five factors are the number of SSB meetings, the SSB qualification, the evaluation of SSB scholars, the performance of the Sharī'ah control department, and the position of SSB in the institution. The findings indicated that the first three variables affect the SSB performance positively, while the fourth variable affects it negatively. For the last variable, the study did not find any significant impact.

By using a survey as his research instrument, Hasan (2011) conducted a descriptive study in 2009 to investigate SG practices in the UK, Malaysia, and the GCC countries by taking into consideration the features of good CG that consist of independence, competency, transparency, disclosure, and consistency. The survey findings indicated that there are many differences in the SG practices across the countries such as only few IFIs adopt the AAOIFI standards. Most IFIs have male scholars in their SSBs. The findings revealed that Malaysia has a strong SG framework compared to the UK and the GCC countries. The study concluded that the current SG practices should be enhanced and improved in terms of the regulatory framework, independence, and competence of SSBs and disclosure practices.

Another empirical study on SSB function in IFIs is conducted by Nathan Garas (2012a). This study examined the relationship between six explanatory variables and the conflicts of interest inside the SSB. These variables are the SSB executive position, the SSB reward, the relationship between the BoD and the SSB, and the SSB membership in Islamic funds, in issuers of Sukuk, and in capital markets. The researcher used a mail questionnaire which was distributed to 219 IFIs in the GCC countries in 2009. The study found that there is no significant impact of reward and SSB membership in capital markets on the conflicts of interest while the other variables have significant impact.

Grassa (2013) examined the SG systems in IFIs and attempted to explore the challenges affecting the implementation of sound SG practices. The study found many differences in the SG practices and models across jurisdictions. Furthermore, the degree of regulatory authorities' intervention differs from one jurisdiction to another. The study revealed that the current SG practices should be improved for a sound SG is important to enhance the credibility of the IFIs. The author concluded that the growth of the Islamic finance industry can be negatively affected if IFIs fail to apply strong SG.

By conducting qualitative analyses, Hamza (2013) examined how the differences in the SG models [Centralized (CSGM) and Decentralized (DSGM)] in Malaysia and the GCC countries can influence the effectiveness of SG. After comparing the CSGM and DSGM models, the study revealed that the CSGM is better for the IBs compared to the DSGM. The CSGM provides uniformity, consistency, and harmonization of the Sharī'ah opinions (fatwas) across IBs; therefore, it can enhance the independence of SSB and decrease the potential conflicts between scholars. In contrast, the study revealed that obtaining consensus in the Sharī'ah opinions and then controlling the conflict of interest is difficult with the DSGM for IBs. However, the study does not provide any empirical evidence to support the discussion.

Grassa and Matoussi (2014b) compared the CG characteristics and governance structure of IBs in the GCC and Southeast Asia countries by using descriptive analysis for 83 IBs for the period 2002–2011. They found several differences in the CG structure between the IBs in the GCC and the Southeast Asian countries. For example, blockholders dominate IBs in the GCC countries, and their number seems to be higher in the IBs of the GCC compared to those in Southeast Asia. IBs in Southeast Asian countries have higher SSB size and SSB women members as compared with the IBs in GCC countries. On the other hand, IBs in the GCC countries have higher SSB cross-membership and SSB members with experience in finance and economic fields than that of the IBs in Southeast Asia. The study concluded that such differences belong to the differences between the GCC and the Southeast Asian countries in their economies, cultures, legal, and regulatory frameworks. The findings of the study indicated that the current CG of IBs still needs more development and standardization.

More recently, Grassa (2015) conducted a critical analysis to examine the SG systems of IFIs across 25 Organization of Islamic Cooperation (OIC) countries. The study found that the majority of the OIC countries still have weak SG systems and regulatory frameworks. These weaknesses lie in the functions and the responsibilities of the SSBs at the national and institutional levels. To enhance the SG practices, the author suggested that it is very necessary for the central authorities to play a more important role in providing good SG practices.

The above section has thoroughly highlighted previous studies on the current SG practices, challenges of good SG, different SG models and systems across jurisdictions. Table III depicts the essence of each study and highlights the important issues on SG and the limitations of the studies. Since the most common and prominent setbacks of the studies reviewed is the absence of empirical investigations, future research should provide empirical evidence to examine the aforementioned issues.

5. Recommendations for future research

In light of the above discussion, there are some important points that can be recommended for future research on SSB and IB performance studies. These points are related to the SSB characteristics' variables, issues, analytical methods, and measurements of variables.

5.1 SSB characteristics' variables

The body of knowledge is in dire need for empirical evidence on how SSB independence can affect the performance of IBs. Adding to that, the question of how SSB remuneration[6] can affect the performance of IBs needs to be addressed together with its effect on that of the BoD (see Bakar, 2016).

5.2 Issues

There is a need for more empirical studies to examine whether the effect of SSB and its characteristics on IB performance vary between IBs that operate:

Under the two different SG models (CSGM and DSGM).

In regulated and unregulated jurisdictions.

In jurisdictions that adopt extreme or slight degree of agencies intervention in SG practices.

In jurisdictions that control the cross-memberships for Sharī'ah scholars versus those that do not control it.

When the SSB position in the organization structure of a bank is located under the shareholders as compared to its position under the BoD or executive management.

There is also a need for more empirical studies to examine whether the effect of SSB and its characteristics on IB performance differ during crisis and non-crisis periods, especially the financial crisis of 2008. This would help IBs to adopt an appropriate SSB structure that will enhance their performance. Furthermore, there is a need for more empirical studies to examine the relationship between the BoD and the SSB in IBs and how such a relationship can affect the performance, risk-taking, and disclosure practices of the IBs. Highlighting this issue is very important as the relationship between the BoD and the SSB is still ambiguous[7], requiring an in-depth analysis.

5.3 Analytical methods

Future studies should control for endogeneity issue. One of the recommended methods to solve this issue is using GMM estimator (see, e.g., Nomran et al., 2018).

Future studies may employ Structural Equation Modeling (SEM) in the governance and performance studies in general. This method allows the inclusion of unobserved influence in the model through latent/unobservable variables which can be measured using many observed variables. In the SSB context, it would help in measuring the SSB influence, as unobserved variable, using the SSB characteristics that may determine how effective the SSB conducts its task, as observed variables. Roemer (2016) highlighted in details why SEM can be suitable for panel data studies.

5.4 Measurements of variables

The performance of IBs should be measured using the Sharī'ah approach, and Zakat ratios have been suggested as alternative measurements of performance, e.g. Zakat on assets and Zakat on equity (see, e.g., Mohammed and Muhammed, 2017a; Nomran and Haron, 2019).

There is a need to create a suitable measurement for SSB independence as there is a lack of studies that have provided such measurement besides ignoring the impact of this variable on performance, risk, and CSR of IBs as a whole. Recently, however, Musleh Alsartawi (2019) measured SSB independence using a single proxy as binary variable: “zero” if the SSB member has direct or indirect relationship with the IB; “one” indicates otherwise. Despite this, it is believed that such measurement alone is not enough to measure the SSB independence, therefore this study suggests using a new score to measure SSB independence involving some important items that may reflect the independence of SSB[8].

SSB total effect should be measured using an SSB measurement that can reflect the total effect of SSB based on the most important characteristics that affect SSB performance. This measure can be either a score/proxy[9] that can be used for studies which employ GMM and other panel data methods. Otherwise, a construct (latent variable) for studies which employ SEM model as discussed above can be employed. In both cases, the validity and consistency of the measurements have to be examined.

6. Conclusion

The purpose of this paper is to identify the literature gap in the study of SG, as represented by the SSB, and its impact on IB performance. Through a systematic literature review, 21 papers were selected and analyzed. It was found that although many studies have been conducted on the SG in IFIs, a majority of these studies are theoretical, and they have been carried out to examine the function of SSB. In contrast, the empirical studies on the SG are limited in general as well as on the relationship between the SSB and the performance of IBs in particular.

However, the existing research studies suffer from some limitations, suggesting an urgent need for more empirical analyses. Because of these limitations, the literature cannot provide meaningful and relevant suggestions to the related parties for the development of the SG practices.

Hence, this paper suggests that future research should empirically examine how the SSB independence and remuneration can affect the performance of IBs. There is a need for more empirical studies to examine whether the effect of SSB and its characteristics on IB performance can be moderated by the differences across jurisdiction in their SG models (CSGM and DSGM), the degree of agencies intervention in SG practices, controlling the cross-memberships of scholars, and SSB position in the organizational structure of IBs. Further, future research should examine whether the effect of SSB and its characteristics on IB performance differ during crisis and non-crisis periods, especially the financial crisis of 2008. This would help IBs to adopt the appropriate SSB structure that help in enhancing their performance, hence value creation.

In terms of the analytical methods, future studies should control for endogeneity issue by using a GMM estimator. In addition, they may employ SEM in the governance and performance studies in general due to its advantages. Finally, the performance of IBs should be measured by using a Sharī'ah approach such as Zakat ratios. SSB total effect should also be measured using SSB measurement that can reflect the total effect of SSB based on the most important characteristics affecting the SSB performance either using a score or proxy for studies that employ panel data methods or a construct (latent variable) for studies that employ the SEM model. Regarding the available databases, there are at least two important databases that can be used by researchers in this research area, i.e. Orbis Bank Focus (Orbis) database and Zawya database. Orbis database provides data about banking activities, while Zawya database provides data about firms including governance and Sharī'ah scholars in IFIs.

This study, however, has its limitation. First, it was restricted in the common features of Scopus search, e.g. the choice of number and type of keywords and the resulting selection of studies. Second, the review was limited to the peer-reviewed papers, meaning other materials such as books, magazines and working papers were excluded.

7. Implications for research and practice

The study has some implications for research and practice as the following.

Although many studies exist on CG in IBs, research on Sharī'ah supervision is still very limited, especially in investigating the impact of SG mechanism on IB performance. Thus, the analysis undertaken in this paper aims to address the literature gaps on the effect of SSB on IBs' performance and the important practical issues on SG practices. This study therefore serves as a guide for researchers and academicians in research related to this important area besides other research and regulatory authorities, e.g. Central banks and Islamic international autonomous non-for-profit organizations, e.g. AAOIFI and the Islamic Financial Services Board (IFSB).

Researchers and academicians may benefit from the attempt to prove that AGT can be used in analyzing how SG mechanism (SSB) mitigates agency problems through moral monitoring and then enhance IBs' performance. Additionally, they may benefit from the attempt to prove that many CG theories, e.g. AGT and SKT, can be used in analyzing how SSB characteristics can improve SSB effectiveness and then enhance IBs' performance.

This study reviews the existing literature on the relationship between SSB and IB performance. The authors suggested the important literature gap that still needs to be empirically examined in different themes of the topic. Thus, it is expected for academic research to benefit from the attempt to explore new related variables to SSB and its characteristics, e.g. SSB independence and remuneration which can enhance IBs' performance besides taking into account the differences in regulatory environments across countries. This would help in developing a SG framework based on the fact that SG practices differ across countries, and then, the strength of SSB performance relationship is affected by such differences.

Regarding the methodology, this study also encourages researchers to adopt more appropriate and robust analytical methods in analyzing the relationship between SSB and IBs' performance, e.g. controlling for endogeneity issue using GMM and employing SEM to construct latent variables. Furthermore, the study suggests using suitable measurements to measure the related variables such as Sharī'ah approach to measure IBs' performance and using score/proxy to measure the total effect of SSB, rather than the selective SSB variables as currently practice in SSB research. In addition, this study suggests a new score to measure SSB independence. Finally, the study suggests employing a new measurement for SSB remuneration which takes into account consumer price index (CPI) to reflect the differences in prices across countries.

In terms of practical implication, this study provides an important summary for shareholders of IBs, policy makers, regulators, and related authorities across countries, to understand how to enhance the performance of IBs with enhancement on SG. In addition, reviewing empirical studies in the field of SSB and performance of IBs are very important to these parties as it would provide them with suggestions on improving the current SG practices for the betterment of the IB industry worldwide.

Notes

Risk means a probability or threat of loss.

The duality of governance of firms is common in some countries, e.g. non-executive directors in Germany, the Netherlands, China, and Indonesia supervise executive directors in two-tier boards as mentioned by Bezemer et al. (2014). However, there are different views regarding the effectiveness of this model. While some believe that such a model is good, some others such as Bezemer et al. (2014) argue that under this board model, challenges might be particularly difficult to address due to the formal separation of management boards' decision management from supervisory boards' decision control roles.

Performance of banks means a capacity to generate sustainable profit (Ishtiaq, 2015).

According to Abdelsalam et al. (2016), religiously oriented organizations apply strict moral constraints. They assert that the opportunistic behavior of managers may be suppressed within an environment that incorporates organizational moral values; hence the religious adherence of IBs implies a possible reduction in agency costs through organizational moral accountability constraints. As they mentioned, the concept of Islamic accountability extends the moral responsibility of the managers and board members of IBs beyond conventional legal liability.

Most papers were excluded in this stage as they are irrelevant.

It can be measured as log of annual SSB remuneration (see, e.g., Grassa and Matoussi, 2014b). For robust check, especially if the study covers IBs across countries, SSB remuneration can be adjusted to reflect the differences across countries in prices and amenities by dividing total remuneration by the consumer price index in each country following literature (see, e.g., Winters, 2009).

To the best of our knowledge, to date, there are still no studies attempted to address this empirically.

In light of the related literature, the suggested SSB independence score sums the value of the dichotomous characteristics of four items, which takes a score bounded by 0–1 as the following:

“1” if the shareholders only appoint SSB scholars; “0” otherwise.

“1” if remuneration of SSB scholars is solely decided by shareholders; “0” otherwise.

“1” if the SSB position in the organization structure of a bank is located under the shareholders; “0” otherwise.

“1” if the SSB attends the BoD meetings to discuss the religious aspects of their decisions; “0” otherwise.

For example, the SSB score was used by many studies (Farook et al., 2011; Rahman and Bukair, 2013; Nomran and Haron, 2019). This score sums the value of the dichotomous characteristics of the SSB, which takes a score bounded by 0–1 (SSB size: “1” for banks with 5 or more members and “0” otherwise), (SSB cross-membership: “1” if at least one SSB scholar with cross-membership and “0” otherwise), (SSB educational qualification: “1” if at least one SSB scholar with PhD and “0” otherwise), (SSB reputation: “1” if at least one SSB scholar sits on the SSB of AAOIFI and at least two Sharī'ah board memberships and “0” otherwise) and (SSB expertise: “1” if at least one SSB scholar with experience and knowledge in the field of accounting/economic/finance and “0” otherwise).