– This paper aims to examines whether Chinese firms’ signals of green governance, including environmental management, green innovation, and greenhouse gas (GHG) and pollution emission, vary significantly with their ownership structure and aim of being environmentally sensitive.

– From corporate social responsibility (CSR)-China website and CNINFO, a total of 781 CSR reports released during 2008-2010 were collected. The collected data were coded and analyzed using content analysis.

– In overall disclosure of environmental protection information (TotalEP), no significant difference existed between state-owned enterprises (SOEs) and privately owned enterprises (POEs). Chinese environmentally sensitive industries (ESIs) have a tendency to disclose significantly more information about their actions of environmental protection than their counterparts. Moreover, SOEs and ESIs scored higher than their counterparts on energy saving and carbon reduction and development of circular economy. A steady increase was also observed in the disclosure ratio for CO2 emission. During 2008-2010, SOEs and ESIs were relatively more committed to the disclosure of SO2 emission as compared to other emission items.

– Managers should disclose signals of green governance actively to avoid adverse selection caused by information asymmetry which further lower their financing cost.

– There is still a lack of evidence as to whether Chinese firms are implementing actions to slow down climate change. This paper endeavours to provide an insight into Chinese firms’ compliance with the green governance requirements of the Eleventh Five-Year Plan. The study hopes to fill the current gap in understanding the environmental behaviours of Chinese firms under pressure to alleviate climate change.

1. Introduction

In recent years, abnormal climate phenomena have increased in frequency and severity across the globe. It has been widely reported that CO2 emission is the major cause of these abnormal phenomena (Solomon et al., 2007). Many nations have therefore viewed carbon reduction as a global issue and a factor that has a serious impact on their economic development. Lu et al. (2006) estimated that the pollution costs to the Chinese economy is 7-10 per cent of gross domestic product. So, it is not surprising that the Chinese Government has set ambitious targets for environmental protection, reduced national energy intensity and the greater use of clean energy (Minas, 2012).

Low-carbon economy is an economic system where corporate social responsibilities extend to cover conservation, recycling and reuse of resources, emission reduction and environmental protection. China understands that development toward low-carbon economy is a must for retention of their current economic growth. Unfortunately, they are faced with drastic changes and challenges in energy saving and carbon reduction. To create a sustainable economy, these two issues must first be tackled.

One the one hand, it is an internal problem by nature. China’s rapid economic growth over the years was the result of an extensive production model characterized by “high input, high energy consumption, and high emission”. This Chinese model has generated enormous economic benefits, yet it also caused serious environmental and social problems. On the other hand, it is also viewed as an external problem. In 2009, China overtook USA to become the world’s largest CO2 emitter. China’s economic activities have already drawn international attention. For instance, it was announced in the 2009 United Nations Framework Convention on Climate Change – COP15 and CMP5 that China, India and other developing nations with large emissions shall implement strategies to develop a low-carbon economy.

These two issues have put China under domestic and international pressure. In the Eleventh Five-Year National Plan on National Economic and Social Development during 2006-2010 (Eleventh Five-Year Plan, 2006) and the Twelfth Five-Year Plan on National Economic and Social Development during 2011-2015 (Twelfth Five-Year Plan, 2011), China has set a goal to progressively achieve sustainable economic and environmental development, as well as social harmony through energy saving and carbon reduction.

In fact, the energy-saving and carbon reduction policy in the Eleventh and Twelfth Five-Year Plans is considered to be green governance. What is green governance? Green Governance is a systematic life cycle to help an organization drive towards environmental sustainability. Green governance promotes global sustainability through the devolution of both governmental and non-governmental entrepreneurism, as well as through partnerships and collaborations to promote energy and environmental sustainability (Bae, 2012). Furthermore, Paddock (2008) suggests that an organization should build the necessary competencies for effective environmental management to attain green governance by integrating economics- and values-based tools.

Klassen and McLaughlin (1996) argue that environmental management is an enterprise trying to make products to minimize impact on the environment. Environmental management is also a management mechanism through internal and external monitoring power to achieve environmental protection and economic development (USA Environmental Protection Agency, 2003).

Chen et al. (2006, p. 332) define “green innovation” as hardware or software innovation that is related to green products or processes, including the innovation in technologies that are involved in energy-saving, pollution-prevention, waste recycling, green product designs or corporate environmental management. Green innovation is used to boost the performance of environmental management in order to satisfy the requirement of environmental protection (Lai et al., 2003).

The environmental information disclosure is expected to speed up the transition from conventional government-dominated environmental regulation to a more transparent and “modern” environmental governance system in China, though there is a huge gap between the expectation and reality of transparency in environmental reporting by the government (He et al., 2011).

Thus, this paper attempts to examine if Chinese firms’ green governance varies with their ownership or aim of environmental sensitivity under the low carbon economy policy prescribed in the Eleventh and Twelfth Five-Year Plans. Zeng et al. (2012) pointed out that when driven by external coercive pressures, firms are indeed more likely to disclose environmental information but they may not necessarily be concerned about the content of disclosure. This paper will conduct a more comprehensive (covering three dimensions) and more in-depth (based on 11 measures and GHG and pollution emission) assessment of Chinese firms’ disclosure on environmental management, green innovation, GHG and pollution emission. The objective of this paper is to examine and compare how varying ownership structure and environmental sensitivity of Chinese firms affect their decision to disclose environmental information.

This paper shall adopt statistical analysis approach. In China, state-owned enterprises (SOEs) are usually pioneers in implementing government policies. As different industries have different environmental impacts, the type and level of control imposed on them also vary by industry (Halme and Huse, 1997). Therefore, this paper will examine whether Chinese firms with different ownership structure and environmental sensitivity have significantly different disclosure levels for environmental governance, green innovation and GHG and pollution emission to meet political expectations.

So far, there is a lack of evidence whether Chinese firms attempt to alleviate environmental issues. This paper will provide an insight into Chinese firms’ compliance with the green governance requirements of the Eleventh Five-Year Plan. This paper will evaluate green governance of Chinese firms through a review of related literature and a thorough analysis of their environmental information disclosure. The study aims to provide a better understanding of the green behaviour of Chinese firms under adaptation of climate change.

2. Study background and literature review

2.1 China’s energy-saving and carbon reduction plan

Since its implementation, China’s extensive production model has brought not only rapid economic growth but also resource and environmental problems which pose a serious threat to the balance of its economic, environmental and social development. To overcome these environmental problems, China has set up a two-phase plan, namely, “The Eleventh Five-Year Plan” and “The Twelfth Five-Year Plan”, in hopes of using energy-saving and carbon reduction as a means to achieve economic and environmental sustainability.

It can be seen in the Eleventh Five-Year Plan that China began to prototype a low-carbon economy in 2006. The Twelfth Five-Year Plan details the major industries promoting energy-saving and carbon reduction (e.g. steel, coal mining, power and chemical engineering) and how to develop a sustainable economy through resource development, energy conservation, clean production and circular economy.

China plans to strengthen its green development (i.e. low-carbon economy) through the Twelfth Five-Year Plan. It attempts to progressively transform its industrial structure to create a low-carbon economy, and energy-saving and carbon reduction is the means China is using to achieve this goal.

2.2 The disclosure of corporate green governance

Many businesses view environmental management as unnecessary and even obstructive to corporate development and growth because of the trade-off between environmental laws and business performance (Porter and van der Linde, 1995). However, businesses can use green innovation as a means to increase their efficiency and offset the cost of environmental management. For instance, Porter and van der Linde (1995) pointed out that pioneers of green innovation have a first-mover advantage. They can also improve their corporate image, create a new market and gain competitive advantage (Chen et al., 2006; Porter and van der Linde, 1995). According to the win–win hypothesis introduced by Porter and van der Linde (1995), while using environmental management and green innovation to reduce production waste and improve production efficiency, businesses are also delivering positive information about their firms to investors. Therefore, corporate commitment to environmental management and green innovation is beneficial to both businesses and investors.

Environmental information disclosure allows stakeholders to know the impact of their company on the society and the environment (Deegan, 2007). If they can obtain more information about the company (i.e. higher information transparency), they can have lower adverse selection risk, and this goes towards benefitting the company. The company can also enjoy lower financing cost and higher competitive advantage. In other words, higher information disclosure quality is contributive to the relationship between businesses and stakeholders (Pellegrino and Lodhia, 2012). It will motivate business to invest more in green management and voluntarily disclose green management information (Sullivan and Gouldson, 2012).

In fact, most businesses disclose their actions and the results of green management, such as GHG emission, in their reports. They improve their reputation by reporting their compliance with government policies and how they have achieved related goals through emission reduction and energy saving. In the future, green management is likely to be one of the main drivers of business performance growth (Sullivan, 2008).

To sum up, both environmental management and green innovation are part of green governance. Simply put, having a low-carbon economy is the way to achieve sustainable development. Previous studies have pointed out that the low-carbon economy could reduce pollution costs (Engels, 2009) and create profits (García-Sánchez and Prado-Lorenzo, 2012).

2.3 International Organization for Standardization environmental certification as the start of green innovation in China

Jaffe et al. (2005) pointed out that emission reduction is the most direct goal of all environmental policies and also the most cost-efficient strategy. Nowadays, many enterprises have realized the importance of compliance with environmental regulations in China (Noronha et al., 2013). Noronha et al. (2013) point out that the Chinese Government and China’s stock exchanges are pushing the idea of environmental management to become more acknowledged by Chinese enterprises. Porter and van der Linde (1995) also pointed out that the relevant environmental protection laws and regulations may be an effective tool for promoting enterprises’ technological innovation and competitiveness. In China, government and capital market have prompted enterprises to adopt aggressive measures to save energy, reduce carbon emission and develop a circular economy.

International Organization for Standardization (ISO) 14001 is a standard for environmental management systems (EMS) that can help businesses address environmental management problems. ISO 14001 is one of the most popular voluntary environmental standards in the world. In 2002, China ranked fifth globally and second among Asian nations on the number of domestic businesses with ISO 14001 certification (International Organization for Standardization, 2002). According to China National Accreditation Board (2004), the number of domestic businesses with ISO 14001 increased by 134 per cent in June 2004. So far, the number has exceeded 35,400 (Dietmar et al., 2011). The large numbers of Chinese firms applying for ISO 14001 certification is resultant from:

the incentives of international trade (Prakash and Potoski, 2006); and

the high export orientation of most Chinese businesses (Christmann and Taylor, 2001).

Businesses will be motivated by business needs to introduce more advanced environmental management systems. Their introduction of the systems can also help improve the overall environmental performance of their nation.

McGuire (2011) indicated that ISO 14001 adoption for Chinese enterprises increases compliance with environmental regulations in China. Based on previous studies, businesses acquire ISO environmental certification as the start of green innovation in China.

2.4 Signalling theory

The purpose of signalling is to acquire information from the capital market to resolve the extensive information asymmetry in economic and social areas (Spence, 2002). In other words, the signalling theory focusses on signals and feedbacks, that is, the receiver’s response to the signals. Besides, signal quality (i.e. quality of information disclosed) implies reputation or prestige (Certo, 2003), which is positive for enterprises (Mishra and Suar, 2010).

The purpose of signalling is also to reduce information asymmetry and avoid adverse selection. The validity of signals, called signal observability, is the extent to which a firm’s disclosure of environmental management or green governance information can affect its business performance. Previous research (Al-Tuwaijri et al., 2004) has shown a positive relationship between environmental management and firm performance. Signal observability refers to the degree to which a signal is easy to capture and interpret for the receivers. For instance, if the disclosed environmental information or green governance information is not easy to understand or compare, it cannot fully reflect the effort made by the firm and therefore cannot positively affect the firm’s performance as much as expected. Therefore, higher signal observability means higher information transparency, which is helpful for firms to effectively reduce their financing cost. With a lower financing cost, they can operate at a lower cost and achieve higher business performance more easily.

In recent years, China’s regulations for firms on environmental information disclosure have great changes. The first legal document for environmental disclosure was issued by China State Environmental Protection Administration (SEPA) in 2007, requiring enterprises to disclose the information of environment pollution, and report executed and planned operations for appropriate environmental protection in annual reports. Based on the rules of SEPA, Shanghai Stock Exchange issued a regulation in 2008, requiring all Chinese listed companies to mandatorily disclose information related to environmental protection (Meng et al., 2013). Firms with poor environmental performance face more political and social pressures that threaten their legitimacy. Hence, they would be expected to communicate more extensive off-setting or positive environmental disclosures in their corporate social responsibility (CSR) reports to external stakeholders (Cho and Patten, 2007). Environmental disclosure under the mandatory regulation setting is mostly a legitimacy device and not an accountability mechanism (Patten, 2005), as more environmental disclosure is to meet with the increasing demand for stakeholders to legitimate their existence to match the increasing focus on environmental issues (Fallan and Fallan, 2009). Thus, some researchers recently tend to use the legitimacy theory as an explanatory theory of environmental disclosure reporting (Cho and Patten, 2007; de Villiers and van Staden, 2010; Fallan and Fallan, 2009; Kuo and Chen, 2013). The environmental behaviours of Chinese firms have been studied by some researchers (Liu and Anbumozhi, 2009; Zeng et al., 2012; Kuo et al., 2012). The present condition is that the strategy of environmental information disclosure on Chinese listed companies is oriented to fill up the government’s environmental concerns (Liu and Anbumozhi, 2009). The strategic perspective views legitimacy as somewhat controllable. It argues that “organizations are able to make strategic choices to change their legitimacy situations and to accumulate the resources through corporate actions, by adapting their activities and altering perceptions” (Aerts and Cormier, 2009). Recently, Kuo and Chen (2013) investigate the relationship between level of environmental disclosure by CSR reporting and establishment of a legitimacy image of operation among firms. The findings from this study suggest that disclosure (signal) of substantive environmental actions using CSR reporting may help the firms in environmentally sensitive industries to bridge the legitimacy gap.

2.5 Stakeholder theory perspective

Stakeholder theory explains the relationship between stakeholders and the information they receive (Sun et al., 2010). In other words, a firm’s environmental information disclosure plays an important role in its communication with stakeholders. Gray et al. (1995) stated that disclosure of information to stakeholders is likely to be taken as a firm’s legitimate contribution to the society. Stakeholders usually use environmental information disclosed by a firm as one of the measures of the firm’s reliability and legitimacy.

From the perspective of the legitimacy theory (Ullmann, 1985), managers have to consider all the factors and stakeholders that affect the firm’s policy, decision-making process and implementation plans (Freeman, 1984). For instance, the pressure imposed by supervisory agencies within the government affects a firm’s decision and implementation of environmental innovation (Qi et al., 2010). To reduce government intervention, the firm is likely to increase its environmental activities. Therefore, the government is virtually the most critical stakeholder in most businesses (Liu and Anbumozhi, 2009). According to Zhang et al. (2008), community pressure also has a significant and positive effect on a firm’s environmental management performance. It can be inferred that a firm’s action or inaction in environmental management and green innovation is an important deciding factor for its operations. The firm will be seriously affected if any of its principal stakeholder groups withdraws their support (Clarkson, 1995).

3. Methodology

3.1 Sample

The sample comprised 971 CSR reported released during 2008-2010. These reports were obtained from CSR-China (www.csr-china.net) and CNINFO (www.cninfo.com.cn). We excluded reports released by foreign firms or firms in the banking and insurance industry for two reasons: first, this paper focusses on indigenous firms in China. For foreign firms in China, compliance with their mother companies’ CSR goals is their primary concern, and compliance with local laws is only their secondary concern. There are essentially some differences in CSR policies between indigenous firms and foreign firms. Moreover, the “Expert Assessment System for CSR China Honor Roll” was designed exclusively for indigenous firms in China and may not be applicable to foreign ones. Second, the banking and insurance industry has some specific industry characteristics (Leuz et al., 2003). As this industry is a service-oriented industry, it causes significantly less environmental impacts and has relatively fewer environmental problems (Brammer and Pavelin, 2008). According to aforementioned reasons, this study deleted 38 firms belong to banking and insurance industry. Moreover, this study deleted 152 firms without complete CSR reporting during 2008-2010. Last, but not least, only 781 CSR reports were used for analysis.

Environmentally sensitive industries include mining and energy, utilities, chemical and pharmaceutical and paper-making industries (Cho and Patten, 2007); non-environmentally sensitive industries include manufacturing, information technology and architecture industries.

3.2 Coding

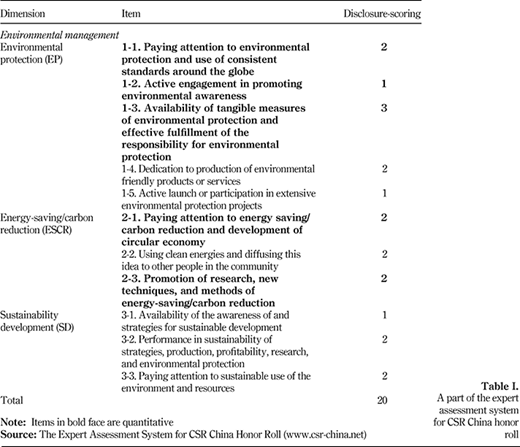

This paper is concerned with environmental information disclosure of Chinese firms and the tendency of their green governance during 2008-2010. We adopted content analysis to evaluate the sample firms’ disclosure of green governance signals. Content analysis is a systematic and objective analytic technique (Berelson, 1952; Krippendorff, 1980). It can be used to examine both quantitative (e.g. to find tendency of change of a frequency over time) and qualitative data (e.g. to support a hypothesis). Content analysis can increase the reliability of findings and the power of explanations (Laplume et al., 2008). To explore Chinese firms’ disclosure of information about environmental protection and green innovation, we used the environmental management section of the rating table for Expert Assessment System for CSR China Honor Roll introduced by Kuo et al. (2012) (see Table I). Following the framework of Kuo et al.’s (2012) disclosure-scoring, this study consists of 11 grid items with three dimensions, including environmental protection (9 scores), energy saving and carbon reduction (6 scores) and sustainable development (5 scores). The best scores of overall items are 20 for each company. In this study, the coding information will be presented as a table rather than as a text description. Of the 11 grid items, 5 are quantitative measures and 6 are qualitative measures. Quantitative measures evaluate items depending on statistical figures. “0” is given to items for which no figure is available. Qualitative measures evaluate items depending on availability of text descriptions. “0” is given to items for which no text description is available. The above rating method is similar to the methods used by Aerts and Cormier (2009), Wiseman (1982), and Al-Tuwaijri et al. (2004).

We also examined the reliability of the coding results (Kuo et al., 2012 for details on the coding procedure). The Cronbach’s alpha was 0.852. Nunnally (1978) has indicated 0.7 to be an acceptable reliability coefficient.

4. Results and findings

Table II presents the basic statistics of the sample. In the environmental management dimension, the maximum and minimum values were 0 and 18 respectively, with a mean of 4.68. In the energy saving and carbon reduction dimension, the maximum and minimum values were 0 and 6 respectively, with a mean of 1.466. Overall, the statistics suggest that Chinese firms have not made enough effort to disclose their environmental management system or green innovation.

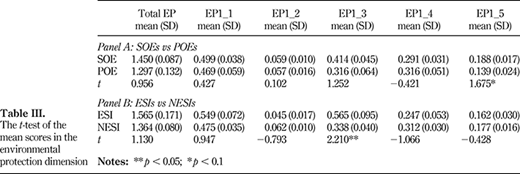

The differences between SOEs and POEs in the environmental protection dimension are shown in Table III. Panel A (SOEs vs POEs) reveals that the difference in Total EP was not significant, but the difference in EP1_5 was. In other words, SOEs significantly outperformed POEs in disclosing information about “Active launch or participation in extensive environmental protection projects”.

This result, from the compliance of government policies, one of the goals of SOEs is to be the pioneer in executing Chinese Government policies. In nature, there is a large difference in matching government policies and regulations between SOEs and POEs. Besides, Halme and Huse (1997) have pointed out that the type and level of control interventions for each industry vary depending on the environmental impact of the industry.

The differences between ESIs and NESIs (Panel B) are slightly different from that shown in the above figure. For instance, ESIs scored higher than NESIs on EP1_3; their difference in EP1_5 was, however, not significant. This result suggests that SOEs, POEs, ESIs and NESIs have inconsistencies in their disclosure of information in the environmental protection dimension. Besides, no significant difference in environmental management (EP1_1) was found between SOEs and POEs or between ESIs and NESIs.

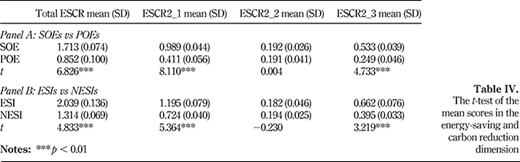

Table IV compares the disclosure ratings between SOEs and POEs (Panel A) and between ESIs and NESIs (Panel B) in the energy-saving and carbon reduction dimension. In terms of TotalESCR, both SOEs and ESIs scored higher than their respective counterparts, suggesting that SOEs and ESIs have been more active in showing their dedication to energy-saving and carbon reduction to stakeholders under the policy of the Eleventh Five-Year Plan. For instance, SOEs and ESIs scored significantly higher than POEs and NESIs, respectively, on ESCR2_1 and ESCR2_3 (p < 0.01). This result also conforms to the key items (i.e. develop circular economy, pay attention to energy consumption and saving and invest in new innovations) and industries (i.e. environmentally sensitive industries) that are given special concern in the Eleventh and the Twelfth Five-Year Plans.

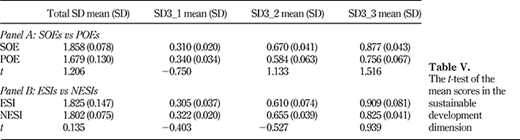

The comparison in the sustainable development dimension is presented in Table V. It can be seen that the overall difference between SOEs and POEs (Panel A) or between ESIs and NESIs (Panel B) was not statistically significant. Moreover, the difference between SOEs and POEs or between ESIs and NESIs was not significant across all the three items (i.e. SD3_1, SD3_2 and SD3_3). It can be inferred that the Chinese firms’ disclosure of information regarding sustainable development issues was not affected by their ownership structure or status of being environmentally sensitive to a significant level.

The environmental management section of the rating scale for the Expert Assessment System for CSR China Honor Roll does not evaluate a firm’s GHG and pollution emission. Therefore, we further examined these firms’ emission of items specifically listed in the Eleventh and the Twelfth Five-Year Plans. These items include carbon dioxide (CO2), sulfur dioxide (SO2), chemical oxygen demand (COD) and nitrogen oxide (NOX). As shown in Table VI, all the disclosure ratios were not high, but the ratio for CO2 was on the increase. This tendency shows the People's Republic of China (PRC) Government’s effort to promote carbon reduction policy and concepts has gradually paid off. However, Table VI also revealed that there was insufficient action taken by Chinese firms to disclose their GHG and pollution emission.

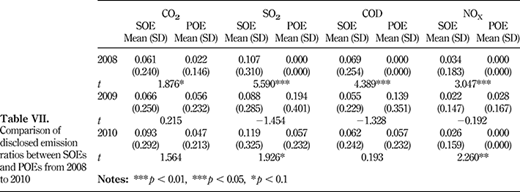

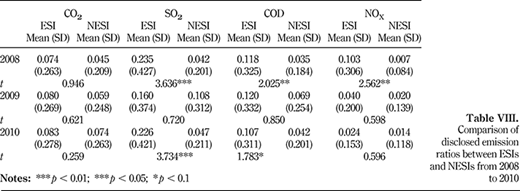

We further analyzed the comparisons between SOEs and POEs and between ESIs and NESIs (Table VI) separately. Table VII shows the comparison on GHG and pollution emission ratios between SOEs and POEs. In 2008, SOEs had significantly higher disclosure ratio for each item than POEs. Besides, SOEs tended to be more active in disclosing SOE emission during 2008-2010. This tendency coincided with the period of time where a strict control on total SO2 emission was imposed according to the Eleventh Five-Year Plan. As to disclosure of CO2 emission, we found a steady growth of the disclosure ratio for CO2 emission. The ratio grew 0.41 (0.027/0.066 = 0.41) from 2009 to 2010. This growth was much greater than the growth from 2008 to 2009 (0.005/0.061 = 0.08). This tendency revealed that SOEs increased their disclosure of CO2 in the last year of the Eleventh Five-Year Plan in preparation for the Twelfth Five-Year Plan where CO2 is listed as the primary pollution to be reduced. Table VIII presents the comparison between ESIs and NESIs. It can be seen that ESIs had a significantly higher disclosure ratio for SO2 than NESIs. During 2008-2010, ESIs were also relatively more active in disclosing their SO2 emission. This finding implies that SOEs and ESIs were more active in complying with and responding to national policies. Besides, the disclosure ratio for CO2 among ESIs increased year by year.

5. Discussion

This finding supported the argument that SOEs are pioneers in the implementation of national policies (Zu and Song, 2009). ESIs are companies that should be given special attention according to the Eleventh and the Twelfth Five-Year Plans. To reduce or avoid penalties, they would certainly be more motivated to comply with government policies (Cho and Patten, 2007; Aerts and Cormier, 2009). In other words, external coercive pressures have encouraged the act of disclosure (Zeng et al., 2012).

Another notable finding was that the difference in SD3_1 was insignificant across the two panels (SOEs vs POEs and ESIs vs. NESIs). However, despite the importance of sustainable development for all of them, POEs and NESIs paid more attention to disclosure of their sustainable development strategies. A plausible explanation is that POEs were under greater competitive pressures than SOEs or had higher administrative efficiency than SOEs (Zu and Song, 2009). In addition, SOEs are usually pioneers in the implementation of government policies, and ESIs are more likely to draw public attention if they fail to address any environmental pollution problem properly. Our analysis of emission information disclosed by the sample firms showed that ESIs and SOEs had higher emission disclosure ratios for SO2. This result matched with the strict limitation on the total SO2 emission set in the Eleventh Five-Year Plan. The gradual increase in the disclosure ratio of CO2 emission suggested that the Chinese firms were preparing to meet the requirements of the CO2 reduction policy stressed in the upcoming Twelfth Five-Year Plan.

5.1 Managerial implications

From the analysis of green governance of Chinese firms, we derived some important managerial implications. First of all, the PRC Government has clearly outlined the goal of developing toward low-carbon economy in the Eleventh and the Twelfth Five-Year Plans and set up related laws to support these plans. However, as found in this study, Chinese firms have not put in sufficient effort into green governance. Therefore, managers of Chinese firms should be more active in disclosure of their green governance to reduce information asymmetry. Through disclosure of green governance, they can further minimize the risk of adverse selection for investors and also lower their financing cost. Besides, in a globally competitive environment, the sustainable development of a business or an economy relies heavily on environmental management techniques. According to Kuznets’ (1995) hypothesis, environmental management techniques can help reduce pollution emissions and are thus essential for steady economic growth. Therefore, to maintain competitive advantages, business managers in China should pay more attention to research and development of environmental management techniques or seek cooperation with foreign firms on environmental management. In their planning of green/environmental management strategies, they should prioritize research and development of environmental management techniques. With advanced management techniques, they can accelerate their development into the third phase of Kuznets’ hypothesis – low environment pollution and steady economic growth – and achieve the goal of sustainable development. Business owners or managers can easily achieve compliance with national policies and laws if they address problems at the end of their production process or purchase some waste processing facilities. Chinese environmental management is a government-oriented mode, and its environmental policies continue to be executed in a top–down fashion. The style of environmental management became gradually more open, with increasing flexibility, more decentralization, further transparency and more involvement of the public (He et al., 2012). More recently, conceptions of what is economically and technologically practical, ecologically necessary and politically feasible are changing. With the large diversity of actors involved in environmental governance, various instruments for environmental management (e.g. green credit, green insurance, green trade and green taxation) have been developed and applied at different levels (Mol and Carter, 2006).

6. Conclusion

In this paper, we examined Chinese firms’ disclosure of environmental management, green innovation and GHG and pollution emission from a wider view (including three dimensions) by using a greater number of measures (11 items and GHG and pollution emission). The results showed that no significant difference in disclosure of EMS (EP1_1) exist between SOEs and POEs or between ESIs and NESIs. The sample firms seemed to be more dedicated to the disclosure of EMS as compared to other environmental protection items, in hopes of signalling stakeholders that they have obtained international certifications. This finding is consistent with the statistics provided by ISO (2002) and China National Accreditation Board (2004). Besides, SOEs and ESIs scored higher than their respective counterparts in disclosure of green innovation (ESCR2_1 and ESCR2_3). This tendency can be attributed to the fact that most SOEs were larger than POEs and had more resources for green innovation. Moreover, ESIs were under greater governmental pressure than NESIs. They would invest more in green innovation to reduce stakeholder attention. Finally, our analysis of GHG and pollution emission showed that SOEs and ESIs tend to be more dedicated to the disclosure of SO2 emission among other emissions during 2008-2010. This tendency coincided with the period of time when a strict control on total SO2 emission was imposed according to the Eleventh Five-Year Plan. Besides, the disclosure ratio for CO2 emission was on the increase during these three years. The increase was a positive signal suggesting that Chinese firms were making more effort to address the abnormal climate changes. Moreover, this tendency also showed that Chinese firms were already preparing themselves for the CO2 reduction policy stressed in the next five-year plan.

Through an evaluation of some Chinese firms’ disclosure of information on environmental management, green innovation, GHGs and pollution emissions, this paper obtained an insight into Chinese firms’ compliance with the green governance requirements under the Eleventh Five-Year Plan. The results are proof the effectiveness of the low-carbon economy policy that has been promoted by the PRC Government but also offer firms some directions on how to improve their green governance during the Twelfth Five-Year Plan.

The-test of the mean scores in the energy-saving and carbon reduction dimension

The-test of the mean scores in the energy-saving and carbon reduction dimension

Comparison of disclosed emission ratios between SOEs and POEs from 2008 to 2010

Comparison of disclosed emission ratios between SOEs and POEs from 2008 to 2010

Comparison of disclosed emission ratios between ESIs and NESIs from 2008 to 2010

Comparison of disclosed emission ratios between ESIs and NESIs from 2008 to 2010

References

About the authors

Lopin Kuo (PhD, National Central University) is a Professor of accounting at Tamkang University in Taiwan. Kuo’s current research involves activity-based costing (ABC), corporate governance (CG), environmental disclosure and carbon management in Japan, corporate social responsibility (CSR) in China and education for sustainability. She has published papers in Journal of Air Transport Management (JATM), Family Business Review (FBR), International Journal of Production Research (IJPR), Academy of Management Learning & Education (AMLE), Management Decision (MD), Corporate Social Responsibility and Environmental Management (CSR&EM), Transnational Corporations Review (TNCR), Journal of Cleaner Production (JCR) and Asian Journal of Finance & Accounting. Lopin Kuo is the corresponding author and can be contacted at: lopinkuo@gmail.com

Hui-Cheng Yu is an Assistant Professor of Department of Accounting and Taxation at Shih Chien University Kaohsiung Campus in Taiwan. He has published papers in Corporate Social Responsibility and Environmental Management (CSR&EM), Transnational Corporations Review (TNCR), his research involves corporate social responsibility in China and corporate governance.

Bao-Guang Chang is a Professor of Department of Accounting at Tamkang University in Taiwan and teaches Managerial Accounting and Financial Statement Analysis. He completed his PhD at the Department of Accounting, National Chengchi University, Taiwan. His research areas include managerial accounting, ethics and behaviour and efficiency analysis. His research papers have been published at Journal of Business Ethics (JBE), Mainland China Studies (MCS), Journal of Contemporary Accounting (JCA), The International Journal of Human Resource Management (IJHRM), International Journal of Revenue Management (IJRM), The Indian Journal of Economics (IJE), International Journal of Management (IJM), Academia Economic Papers (AEP), Taiwanese Journal of Applied Economics (TJAE), Asia Pacific Management Review (APMR), Sun Yat-Sen Management Review (SYSMR), Journal of Management & Systems (JMS), Contemporary Management Research (CMR), The Journal of Human Resource and Adult Learning (JHRAL), Soochow Journal of Economics and Business (SJEB).