This paper examines how the integration of Artificial Intelligence (AI) within accounting information systems (AIS) influences organizational performance and decision-making capacity in Saudi Arabia. It further investigates the mediating role of decision-making capacity in the relationship between AI-enabled AIS and organizational performance.

A quantitative research design was employed using data collected from 340 accounting and finance professionals in Saudi Arabia. The proposed relationships were tested using covariance-based structural equation modeling (CB-SEM) to assess both direct and indirect effects.

The results reveal that AI integration within AIS has a significant positive impact on both financial and non-financial performance, with a stronger effect observed on financial performance. Additionally, AI-enhanced AIS improves decision-making capacity. The findings also indicate that decision-making capacity partially mediates the relationship between AI integration and organizational performance, suggesting that AI creates value both directly and indirectly through enhanced analytical and informational support.

The study is limited by its reliance on cross-sectional, self-reported data, which restricts causal inference. Future research is encouraged to adopt longitudinal designs and incorporate objective performance measures.

The findings highlight the importance for organizations to integrate AI technologies such as machine learning, robotic process automation, and predictive analytics into AIS. Enhancing decision-support capabilities through AI can lead to improved organizational performance and more effective strategic decision-making.

This study contributes to the literature by conceptualizing AI as a strategic capability embedded within AIS and providing empirical evidence from the Saudi Arabian context. It extends prior research by offering a more nuanced understanding of how AI integration influences organizational performance through decision-making mechanisms.

1. Introduction

Accounting Information Systems (AIS) are being transformed by Artificial Intelligence (AI) to become more automated, to process data more efficiently, and to conduct analyses. Machine learning, robotic process automation (RPA), and natural language processing (NLP) technologies allow organizations to produce more relevant, current, and error-free financial data, and to aid in making better managerial decisions (O'Leary, 2024; Schreyer et al., 2019). With the expansion of AI use, the question of its influence on organizational outcomes has become a critical research topic in accounting and information systems literature.

However, the available research mostly focuses on the direct impact of AI on performance, which does not provide sufficient information about the mechanisms through which AI can be used to generate organizational value. Specifically, the mediating role of decision-making between AI integration and performance outcomes is not adequately studied (Schreyer et al., 2022; Parker et al., 2022). Moreover, existing studies often lack a clear theoretical connection between the adoption of AI and organizational capabilities, particularly in the context of emerging economies like Saudi Arabia (Zayed et al., 2024).

To address this gap, this research paper explores the impact of AI implementation in AIS on both financial and non-financial performance, along with the mediating role of decision-making capacity. Based on the capability-based approach, AI is viewed as a strategic asset that can enhance organizational performance by improving the quality of information and analytical support (Yoshikuni et al., 2023).

The study tests the proposed relationships using Covariance-Based Structural Equation Modeling (CB-SEM) with data from a survey of 340 Saudi Arabian accounting and finance professionals. The results contribute to the literature by offering a mechanism-centered explanation of AI value creation, demonstrating how decision-making mediates the relationship between AI integration and performance outcomes, and providing empirical evidence in the context of a developing economy.

2. Artificial intelligence and its impact on AIS

Accounting Information Systems (AIS) are gradually being transformed by Artificial Intelligence (AI), which makes them increasingly automated, capable of processing more data, and analytically robust. Technologies such as machine learning (ML), robotic process automation (RPA), and natural language processing (NLP) can automate routine accounting processes, enhance the quality of classifications, and produce more accurate financial statements (Richins et al., 2018; Abdullah and Almaqtari, 2024). Additionally, predictive analytics and anomaly detection are enhanced by AI, enabling AIS to identify irregular transactions and forecast financial risks more efficiently than conventional systems (Haenlein and Kaplan, 2019; Schreyer et al., 2019). This development shifts AIS toward being a more advanced analytical system as opposed to a transaction-processing system.

Beyond operational advancements, the application of AI enhances decision-making processes by offering real-time insights, predictive data, and data-driven recommendations (Parker et al., 2022).This change facilitates more informed managerial decision-making and shifts accounting professionals toward a more strategic role (Baldwin et al., 2006). Nevertheless, the impact of AI on organizational performance is not uniformly positive. While some studies report improvements in efficiency, reporting accuracy, and compliance (O'Leary, 2024; Kokina and Davenport, 2017), others emphasize that outcomes are dependent on organizational readiness, digital infrastructure, and organizational culture (Badghish and Soomro, 2024; Qatawneh and Al-Okaily, 2024). These findings indicate that AI is a technological component whose performance depends on enabling conditions.

Additionally, AI usage raises concerns regarding transparency and accountability. Deep learning systems often employ complex algorithms that operate as “black boxes”, which may lack explainability and raise concerns in the context of financial decision-making (Leocádio et al., 2024). Excessive dependence on automated output can also undermine professional judgment unless supported by appropriate governance.

Overall, previous studies suggest that AI can enhance organizational performance and decision-making in AIS, yet the effectiveness of translating AI-generated information into action must be examined. This positions decision-making as a critical process connecting AI integration and performance outcomes, which supports the need to address both direct and indirect impacts.

3. Literature review

This section reviews the theoretical and empirical literature on the relationship between Artificial Intelligence (AI) and Accounting Information Systems (AIS). It is divided into two parts. Section 3.1 presents the theoretical foundations explaining AI adoption and its implications, while Section 3.2 examines empirical evidence on performance and decision-making outcomes. Together, these perspectives provide a structured understanding of how AI contributes to organizational value.

3.1 Theoretical literature

Theories that can be used to explain AI integration in AIS include the Theory of Technology Dominance (TTD), Decision Support Systems (DSS) theory, Resource-Based View (RBV), and Technology Acceptance Model (TAM). This study does not examine them in isolation; rather, it combines these perspectives to explain adoption and outcomes.

TAM has been used to explain the behavioral determinants of AI adoption, with a focus on perceived usefulness and perceived ease of use (Davis, 1989). Research indicates that professionals embrace AI when it enhances efficiency, is strategically oriented, and is perceived as trustworthy (Vărzaru et al., 2022; Bakarich and O'Brien, 2021). However, TAM does not explain performance outcomes, but mainly focuses on adoption.

RBV extends this by conceptualizing AI as a strategic resource that improves performance when integrated with organizational capabilities such as data infrastructure, human capital, and governance systems (Yoshikuni et al., 2023). Studies indicate that AI generates value when it is effectively integrated into organizational processes, not merely as standalone technology (Yoshikuni et al., 2023).

DSS theory explains how AI enhances decision-making processes by enabling real-time analytics, predictions, and anomaly detection (Duan et al., 2019).These capabilities enhance decision quality, responsiveness, and strategic planning, especially in complex environments which underscores decision-making as a key mediating mechanism linking AI to performance.

Conversely, TTD highlights the risks of excessive reliance on AI and the potential erosion of professional judgment (Arnold and Sutton, 1998; Zeiser, 2024). Nevertheless, governance and explainable AI approaches can help mitigate these risks (Crowston and Bolici, 2025; Adadi and Berrada, 2018).Overall, these perspectives imply that AI can affect performance both directly and indirectly, with decision-making as a significant mediating process.

3.2 Empirical literature

This section reviews empirical evidence on how AI integration in AIS affects organizational performance and decision-making.

3.2.1 Adoption of AI and organizational performance in AIS

Empirical research generally indicates that the use of AI in AIS can positively impact organizational performance through improvements in accuracy, efficiency, and reporting compliance (2023; Kokina and Davenport, 2017; Haenlein and Kaplan, 2019). Studies by Bin-Nashwan et al. (2025) demonstrates enhancements in reporting reliability and audit effectiveness, particularly when supported by robust internal controls. Evidence from the MENA region also suggests improved compliance and reduced reporting errors (Shiyyab et al., 2023). Nevertheless, results are not entirely uniform. Research indicates that outcomes are determined by organizational readiness, infrastructure, and cultural alignment (Badghish and Soomro, 2024). Excessive reliance on AI without human oversight can result in inconsistent results (Lodhi and Kassem, 2024), and some studies show no improvement in performance due to external factors like market conditions and management practices (Bin-Nashwan et al., 2025).

The integration of AI in AIS leads to improved organizational performance.

3.2.1.1 Financial performance

Research finds that AI-based AIS enhances profitability, reporting timeliness, and cost-efficiency, particularly when supported by strong governance and data management (Al-Mekhlafi, 2024; Almaqtari, 2024). Nevertheless, AI can present budget risks or yield limited returns, and may not have significant effects, especially in complex environments (Moll and Yigitbasioglu, 2019; Bin-Nashwan et al., 2025). Some researchers do not find a significant association between AI and financial outcomes (Shiyyab et al., 2023; Bin-Nashwan et al., 2025).

The integration of AI in AIS has a significant positive impact on the financial performance of organizations.

3.2.1.2 Non-financial performance

AI integration has been linked to improvements in decision quality, operational efficiency, and stakeholder trust (Moll and Yigitbasioglu, 2019; Abdullah and Almaqtari, 2024). It is also associated with innovation and sustainability (Moll and Yigitbasioglu, 2019). Nonetheless, automation bias and reduced professional judgment remain risks, and some studies report no significant effects in cases of weak organizational conditions (Adadi and Berrada, 2018).

The integration of AI in AIS has a significant positive impact on the non-financial performance of organizations.

3.2.2 AI and decision-making capacity in AIS

The use of AI enhances decision-making by improving forecasting capabilities, anomaly detection, and real-time response (Almaqtari, 2024). Nevertheless, over-reliance on AI can reduce critical thinking and lead to misguided priorities without appropriate oversight (Adadi and Berrada, 2018). Some studies show no significant effects due to low AI Overall, AI enhances decision-making capacity; however, its effectiveness is determined by governance, organizational readiness, and human-AI collaboration. Decision-making is thus one of the key mechanisms through which AI integration is linked to performance.

The integration of AI in AIS significantly improves strategic decision-making capacity.

Decision-making capacity mediates the relationship between AI integration and organizational performance.

4. Methodology

4.1 Research design and data collection

The research adopts a quantitative research design that examines the relationship between Artificial Intelligence (AI) implementation in Accounting Information Systems (AIS), organizational performance, and decision-making capabilities in Saudi Arabia. To gather primary data, a survey-based method was utilized because it is appropriate for testing hypothesized relationships and examining the links among variables in an organizational context. A structured questionnaire was employed to gather data from accounting and finance professionals in organizations that utilize digital accounting systems. Target respondents were identified based on their direct involvement in accounting processes and their experience with AI-based tools in AIS. A total of 340 valid responses were received from organizations of different sizes and degrees of digital maturity. The sample is primarily concentrated in large economic centers like Jeddah and Riyadh, reflecting the concentration of accounting activities and digitization initiatives in Saudi Arabia. The sample size exceeds the minimum requirements for Structural Equation Modeling (SEM), which ensures the robustness of the analysis.

4.2 Measurement of variables

The research employs multi-item scales to measure the key constructs. AI integration in AIS was assessed through items that reflected automation, machine learning, natural language processing, and analytical capabilities embedded in accounting systems. Organizational performance was measured using two dimensions: financial performance and non-financial performance. Decision-making capacity was assessed using items related to information quality, decision support, and timeliness. All items were measured using a five-point Likert scale ranging from 1 = strongly disagree to 5 = strongly agree. The measurement items were adopted from previously validated instruments in the accounting and information systems literature and slightly modified to align with the context of AI integration in AIS (e.g. Issa et al., 2024; Kokina and Davenport, 2017; Parker et al., 2022). The use of perceptual measures was justified by their wide acceptance in accounting and information systems research where objective organizational data are not readily available.

4.3 Data analysis techniques

Data were analyzed using SPSS (v26) and STATA (v16). Equal-weight averaging was used to construct composite indicators. Reliability was assessed using Cronbach's Alpha and Composite Reliability (CR), both exceeding the recommended thresholds. Construct validity was assessed using Confirmatory Factor Analysis (CFA), with all factor loadings above acceptable levels and Average Variance Extracted (AVE) exceeding 0.50. The Fornell-Larcker criterion was used to assess discriminant validity. The KMO test and Bartlett's Test of Sphericity were used to assess sampling adequacy. Pearson correlation was used to examine the relationships between variables. Given the large sample size (n = 340), parametric statistics were deemed robust despite slight deviations from normality. Hypothesized direct and indirect relationships were tested using Structural Equation Modeling (SEM), and model fit was evaluated using standard indices (CFI, TLI, RMSEA). For robustness checks, multiple regression analysis was also performed.

5. Empirical findings and analysis

This section presents the empirical findings using a final sample of 340 responses. The analysis is conducted in a structured sequence. First, the measurement model is tested for reliability and validity. Second, descriptive statistics of the key constructs are presented. Third, correlations among variables are examined. Finally, the study hypotheses are tested using regression analysis and Structural Equation Modeling, followed by mediation analysis.

5.1 Reliability and validity analysis

The measurement model was evaluated using Cronbach's Alpha, Composite Reliability (CR), Kaiser-Meyer-Olkin (KMO), AVE, and factor loadings to assess the reliability and validity of the measurement model. Table 1 indicates that all constructs exhibited strong internal consistency with Cronbach's alpha values ranging from 0.863 to 0.928, which exceed the recommended threshold of 0.70. These findings reveal that the measurement items are consistent in capturing their underlying constructs.

Composite Reliability values ranged from 0.557 to 0.711. While some CR values are slightly below the traditional threshold of 0.70, values above 0.50 are acceptable in exploratory research, especially when accompanied by high factor loadings and strong Cronbach's Alpha values (Nunnally, 1978; Byrne, 2010). Thus, construct reliability is considered sufficient for this study.

KMO values ranged from 0.808 to 0.918, indicating high sampling adequacy and the suitability of the data for factor analysis. Convergent validity was established as AVE values ranged from 0.652 to 0.769, which exceed the recommended threshold of 0.50. Factor loadings ranged from 0.763 to 0.929, indicating that all items made significant contributions to their respective constructs.

The Fornell-Larcker criterion was used to assess discriminant validity by comparing the square root of AVE for each construct with its correlations with other constructs. The results confirm that the constructs are empirically distinct. Overall, the findings provide strong support for the reliability and validity of the measurement model.

5.2 Descriptive analysis

This section presents the demographic profile of respondents and the descriptive statistics of the study constructs.

5.2.1 Demographic characteristics

The demographic characteristics of the respondents in terms of job title, years of experience, organization size, and location are summarized in Table 2. The majority of respondents held accounting and finance positions, particularly as auditors, accountants, and financial analysts. The sample consisted of both early-career and seasoned professionals, with the largest proportion having over 10 years of experience. Most organizations were located in Jeddah and Riyadh and were classified as large or very large. Overall, the sample is appropriate for investigating AI integration into AIS in the Saudi context.

5.2.2 Descriptive statistics of constructs

Table 3 presents descriptive statistics based on responses from 340 respondents using a five-point Likert scale. The overall mean score for AI use in AIS is 3.045 (SD = 0.861), indicating moderate AI adoption levels with some variations across organizations.

At the item level, the highest mean was observed for AI usage in daily work processes (M = 3.11, SD = 1.065), followed by machine learning for data analysis (M = 3.07, SD = 1.017). Robotic process automation also showed moderate use (M = 3.05, SD = 0.983). In contrast, natural language processing had the lowest mean (M = 2.98, SD = 1.007), indicating that more advanced AI applications are less common. Overall, the standard deviations reveal moderate variability, reflecting differences in the extent of AI integration across organizations.

Table 4 presents descriptive statistics for the financial performance construct based on responses from 340 respondents using a five-point Likert scale. The overall mean is 3.322 (SD = 0.739), indicating a moderately positive perception of the relationship between AI integration and financial outcomes, with relatively consistent responses.

At the item level, the highest mean was for improved financial reporting accuracy (M = 3.52, SD = 0.822), followed by cost reduction (M = 3.47, SD = 0.991). AI's contribution to financial forecasting was also positively perceived (M = 3.28, SD = 0.904), though perceptions were lower for AI's role in regulatory compliance (M = 3.22, SD = 0.789). Profitability had the lowest mean (M = 3.12, SD = 1.047), suggesting that its impact is less immediate than other financial benefits.

Table 5 presents descriptive statistics for non-financial performance based on responses from 340 respondents using a five-point Likert scale. The overall mean is 3.419 (SD = 0.805), indicating a moderately positive perception of non-financial benefits from AI integration, with relatively consistent responses.

The highest mean was observed for system usability (M = 3.52, SD = 0.836), followed by improved workflow transparency (M = 3.44, SD = 0.927). Respondents also rated system reliability (M = 3.41, SD = 0.951) and user satisfaction (M = 3.39, SD = 0.936). System adaptability had the lowest mean (M = 3.34, SD = 0.916), suggesting potential areas for improvement.

The standard deviations overall indicate moderate variation, reflecting differences in system maturity and implementation quality across organizations.

Table 6 presents descriptive statistics for decision-making support based on responses from 340 respondents using a five-point Likert scale. The overall mean is 3.553 (SD = 0.769), indicating a moderately positive perception of AI's role in enhancing decision-making, with relatively consistent responses.

The highest mean was for faster decision making (M = 3.68, SD = 0.899), followed by error detection (M = 3.64, SD = 0.880), and the provision of timely and accurate data (M = 3.61, SD = 0.870). Bias reduction (M = 3.56, SD = 1.013) and support for long-term planning (M = 3.52, SD = 0.850) were also perceived positively.

Strategic decision support (M = 3.42, SD = 0.927) and confidence in AI-assisted decisions (M = 3.44, SD = 0.965) had slightly lower means, suggesting areas for further development. Overall, the standard deviations indicate moderate variation in the extent of AI-assisted decision-making across organizations.

6. Correlation analysis

Table 7 presents the Pearson correlation coefficients among the study variables. All correlations were positive and statistically significant at the 0.01 level, indicating meaningful relationships between the constructs. AI integration in AIS was positively correlated with financial performance, non-financial performance, and decision-making support. The strongest correlation was observed between non-financial performance and decision-making support, suggesting a strong relationship between system quality and improved managerial decision-making.

7. Regression analysis and hypothesis testing

Table 8 presents the results of the regression analysis examining the effect of AI use in AIS on financial performance, non-financial performance, and decision-making support. The results indicate that AI use has a positive and statistically significant effect on all three dependent variables.

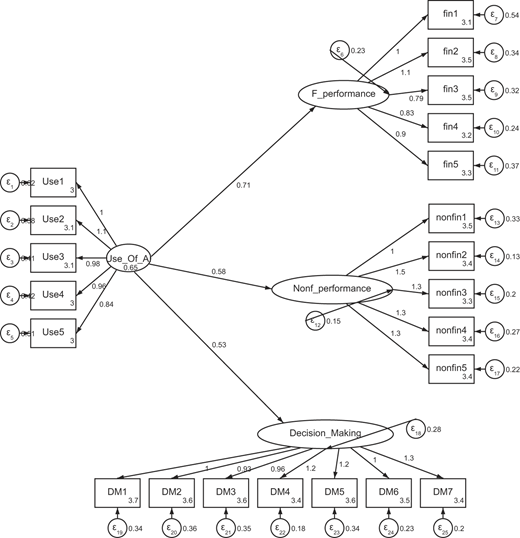

For financial performance, the AI use coefficient is positive and highly significant (β = 0.707, z = 10.17, p < 0.001). This finding suggests that greater AI adoption in AIS is associated with significant improvements in financial outcomes, such as profitability, cost reduction, and reporting accuracy. The 95% confidence interval [0.571, 0.843], which does not include zero, further confirms the robustness of this relationship. These results provide strong empirical support for Hypothesis H1a, which proposes a positive relationship between AI integration in AIS and financial performance.

Similarly, AI use demonstrates a significant positive effect on non-financial performance (β = 0.580, z = 10.67, p < 0.001). The confidence interval [0.473, 0.686] confirms the stability and significance of this effect, suggesting that AI adoption improves system usability, reliability, adaptability, and transparency. This finding supports Hypothesis H1b, confirming the positive contribution of AI integration to non-financial performance dimensions.

Regarding decision-making support, the results reveal a positive and statistically significant relationship with AI use (β = 0.530, z = 9.24, p < 0.001). The confidence interval [0.418, 0.643] confirms the consistency of this effect. This indicates that AI-enabled AIS enhances organizational decision-making capability in terms of decision speed, accuracy, bias reduction, and strategic insight. These findings provide strong support for Hypothesis H2.

Comparing coefficient magnitudes, AI use has the greatest impact on financial performance, followed by non-financial performance, and then decision-making support. Overall, the results demonstrate the critical role of AI integration in AIS in enhancing performance outcomes and managerial decision-making, thereby supporting the core theoretical propositions of the study.

Figure 1 presents the path diagram of the structural model. The goodness-of-fit indices indicate that the structural model achieves good fit with the data. While the chi-square statistic is significant ( = 229.116, p < 0.001), this is expected in large samples and does not necessarily indicate poor fit. The normed chi-square ratio is within the acceptable range ( = 1.123), supporting model adequacy. The Root Mean Square Error of Approximation (RMSEA) value of 0.028 demonstrates excellent fit, well below the thresholds for acceptable (0.08) and good (0.05) fit. Furthermore, all incremental fit indices exceed the recommended threshold of 0.90: Normed Fit Index (NFI) (0.998), Relative Fit Index (RFI) (0.984), Incremental Fit Index (IFI) (0.954), Tucker-Lewis Index (TLI) (0.952) and Comparative Fit Index (CFI) (0.904). These values collectively verify that both the measurement and structural components of the model demonstrate good fit, confirming the adequacy of the proposed model (Table 9).

8. Mediation analysis

Table 10 presents the results of the mediation analysis, examining both the direct and indirect effects of AI use in AIS on financial and non-financial performance, with decision-making capacity serving as the mediating variable. The analysis reports standardized coefficients, z-values, and confidence intervals to ensure the reliability and robustness of the results.

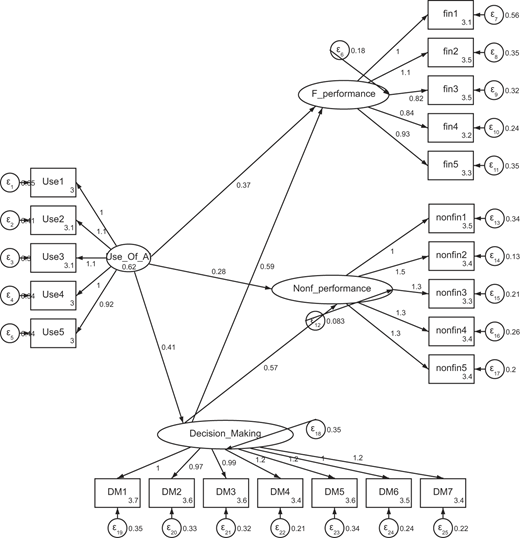

The results reveal that decision-making support has a strong and positive effect on financial performance (β = 0.589, z = 8.82, p < 0.001).The confidence interval [0.458, 0.720] further confirms the significance and robustness of this relationship, suggesting that enhanced decision-making capabilities are strongly associated with improved financial outcomes. Critically, even after accounting for the mediating effect, AI use retains a significant direct effect on financial performance (β = 0.371, z = 6.78, p < 0.001). This indicates that AI adoption contributes to financial outcomes both through improved decision-making and through other direct operational pathways.

A similar pattern emerges for non-financial performance. Decision-making capacity demonstrates a significant and positive effect (β = 0.568, z = 10.82, p < 0.001), with a confidence interval of [0.465, 0.671]. AI use also maintains a significant direct effect on non-financial performance (β = 0.281, z = 7.64, p < 0.001), indicating that AI integration is associated with improvements in system usability, transparency, and reliability that are independent of its effect on decision-making processes. Consistent with the mediation model, AI use is a significant predictor of decision-making capacity (β = 0.406, z = 7.42, p < 0.001), confirming a robust pathway through which AI adoption influences organizational performance.

The indirect effects demonstrate significant mediation. AI use has a positive and statistically significant indirect effect on financial performance through decision-making capacity (β = 0.239, z = 6.29, p < 0.001), with the confidence interval [0.165, 0.314] reinforcing the robustness of this relationship. Similarly, the indirect effect of AI use on non-financial performance is significant (β = 0.231, z = 6.81, p < 0.001), as evidenced by the confidence interval [0.164, 0.297]. The presence of both significant direct and indirect effects suggests partial mediation, i.e., decision-making capacity is a crucial but not exclusive mechanism linking AI adoption to performance outcomes. In other words, AI enhances performance both directly through automation, enhanced data processing, and improved system capabilities, and indirectly through improvements in decision-making quality and effectiveness.

The consistency of coefficients, sustained statistical significance across all pathways (p < 0.001), and narrow confidence intervals collectively demonstrate the robustness of the mediation analysis. These results confirm the validity of the theoretical model and the proposed relationships among AI use, decision-making capacity, and organizational performance, demonstrating strong empirical support.

In summary, the mediation results provide strong empirical evidence supporting the study's conceptual framework. They demonstrate that AI adoption in AIS enhances organizational performance both directly by improving financial and operational processes, and indirectly by enhancing decision-making quality. Decision-making capacity thus emerges as a key mechanism through which AI generates value, underscoring the importance of translating technological capabilities into meaningful organizational outcomes.

Figure 2 presents the path diagram for the mediation model. Table 11 presents the goodness-of-fit indices used to evaluate the overall fit of the mediation structural equation model. Multiple measures of absolute, incremental, and parsimonious fit were examined to provide a comprehensive evaluation of model adequacy.

The chi-square statistic (χ2 = 419.23, df = 204, p < 0.001) is statistically significant, which is typical for models with relatively large sample sizes, since the chi-square test is highly sensitive to sample size. Therefore, model fit evaluation relies more heavily on alternative fit indices rather than the chi-square statistic alone.

The normed chi-square ratio (χ2/df = 2.055) is well within the recommended range of 1–5, indicating acceptable and parsimonious model fit. This suggests that the discrepancy between the observed and model-implied covariance matrices is within acceptable limits relative to model complexity.

The RMSEA value of 0.035 is well below the stringent threshold of 0.05, indicating excellent model fit. This low RMSEA value indicates minimal approximation error, reflecting close fit of the model to the population covariance matrix.

Regarding incremental fit indices, all reported values far exceed the recommended threshold of 0.90. Specifically, NFI (0.976), RFI (0.912), IFI (0.982), TLI (0.998), and CFI (0.992) all demonstrate excellent fit. The exceptionally high values of TLI and CFI indicate that the proposed model represents a substantial improvement over the null model, providing strong evidence of good fit.

Overall, the combination of a satisfactory normed chi-square, a low RMSEA, and consistently high incremental fit indices provides compelling evidence that both the measurement and structural model fit the data exceptionally well.

These results confirm the adequacy of the proposed model and the validity of the hypothesized relationships among AI use in AIS, decision-making support, and organizational performance. Consequently, the model is deemed suitable for hypothesis testing and structural path interpretation.

9. Conclusion

This study explored the role of Artificial Intelligence (AI) integration in Accounting Information Systems (AIS) and its implications for organizational performance and decision-making capacity in the Saudi Arabian context. Motivated by the rapid pace of digital transformation in the accounting profession and the growing strategic importance of AI, the research aimed to provide empirical evidence on how AI-enabled accounting systems contribute to both financial and non-financial organizational outcomes.

Using a quantitative research design and data collected from 340 accounting and finance professionals, the study employed a comprehensive analytical framework that included reliability and validity analysis, correlation analysis, regression modeling, and Structural Equation Modeling (SEM). The empirical findings demonstrate that AI integration in AIS significantly enhances organizational performance both directly and indirectly. AI integration is positively associated with improved financial outcomes through increased efficiency, accuracy, and analytical capability, as well as enhanced non-financial outcomes such as system reliability, transparency, and user satisfaction. Moreover, decision-making capacity emerged as a crucial mechanism through which AI capabilities are translated into organizational value, thereby reinforcing the strategic role of AIS beyond routine automation.

From a theoretical perspective, this study contributes to the Accounting Information Systems literature by empirically validating the performance-enhancing effects of AI in the context of an emerging economy. By examining financial performance, non-financial performance, and decision-making capacity simultaneously, the research extends previous studies that have tended to focus on isolated AIS outcomes. The identification of decision-making capacity as a partial mediator provides additional theoretical richness by demonstrating how technological capabilities translate into organizational performance through managerial processes.

From a practical standpoint, the findings have important implications for organizations, policymakers, and accountants. The results indicate that successful AI adoption in AIS requires more than technological investment alone. Organizations must also focus on enhancing decision-making processes, developing analytical capabilities, and fostering effective human-AI collaboration. Organizations should prioritize AI tools such as robotic process automation (RPA), machine learning, and predictive analytics, while strengthening governance and explainability mechanisms to ensure reliable and transparent outcomes. For Saudi organizations in particular, the findings align with the goals of Saudi Vision (2030), (2016) by highlighting AI-enabled accounting systems as strategically important instruments for enhancing efficiency, governance, and long-term competitiveness.

Despite its contributions, this study has several limitations. The analysis is based on cross-sectional survey data, which limits the ability to draw causal inferences or examine changes over time. In addition, the sample is concentrated in major economic centers, which may restrict the generalizability of the results to smaller organizations or regions with lower digital maturity. Future research could address these limitations by employing longitudinal designs, qualitative methods, or cross-regional comparisons to gain deeper insights into the evolving role of AI in accounting systems.

In conclusion, this research provides strong empirical evidence that AI integration in AIS is a powerful driver of organizational performance and decision-making effectiveness. By demonstrating how AI enhances performance both directly and through decision-making capacity, the study underscores the strategic importance of AI-enabled AIS in the digital era and provides a robust foundation for both researchers and practitioners to advance understanding and practice of accounting transformation through AI.