This study empirically attempts to uncover the connection between digital financial inclusion (DFI), accounting information quality (AIQ) and supply chain resilience (SCR).

To achieve the objectives, panel data on manufacturing registered corporations in China from 2015 to 2024 are used. Panel ordinary least squares with fixed and random effects uncover the relationship between variables.

The study observes that DFI and AIQ significantly improve SCR. Several tests are employed to signify the robustness of such findings. Mediating mechanics show that DFI and AIQ improve SCR by enhancing value co-creation and goodwill of the firms. Moreover, financial regulation positively moderated the relationship between DFI and SCR and AIQ and SCR. The supportive business environment and maturity of enterprises pronounced the impact of DFI and AIQ on SCR.

The governments and institutions should enhance cloud computing technologies, stability, network coverage, mobile payments and digital accounting information systems to improve SCR. Moreover, the laws and regulations of supply chain financing should be refined by governments so that all parties in the supply chain have sound legal protection.

The findings deliver some valuable practical implications.

1. Introduction

Supply chains have become crucial for businesses pursuing competitive advantage in the rapidly evolving global economy. Nevertheless, many uncertainties within the supply chain industry give rise to considerable economic risks. Digital financial inclusion (DFI) is an emerging field in financial technology that is increasingly penetrating and transforming traditional financial systems and actual economic models. Specifically, digital finance has promoted financial inclusion while increasing household financial risk (Yue, Korkmaz, Yin, & Zhou, 2022; Zhou, Shi, Bao, Gao, & Ma, 2023) and harming banks’ liquidity (Hao, Peng, & He, 2023). Moreover, DFI impact reaches every facet of supply chain management (SCM) and brings new approaches to mitigate the challenges of supply chain resilience (SCR). The quality of corporate accounting information quality (AIQ) further enhances the company’s reputation and aids in the negotiation of corporate debt agreements (Li, Li, Hu, & Gan, 2024; Wang, 2024). China has also developed regulatory frameworks to help businesses transition to green and sustainable practices. This includes setting environmental standards, monitoring and enforcing penalties in case of failure to comply. The greater the capability to expand the transparency of accounting information, the less the information asymmetry between external stakeholders and management (Kharouf, Lund, Krallman, & Pullig, 2020). The institutional theory suggests that business organisations must abide by these standards to gain legitimacy regarding business affairs (Risi, Vigneau, Bohn, & Wickert, 2023). Besides, studies have shown that firms responsive to policy measures tend to have solid ethics and, therefore, can encompass corporate behaviour, preventing principal-agent problems (Pacces, 2021). Furthermore, the more a firm attends to its corporate social responsibility, the more believable and transparent accounting data shall be, thus improving the quality of accounting information (Khuong et al., 2022) and SCR. SCR and quick recovery of risks are key concerns of academic research. Past studies have recognised that digitalisation brings new avenues for improved supply chain flexibility and security; thus, reinforcing SCR has been identified (Gupta, Yadav, Kusi-Sarpong, Khan, & Sharma, 2022; Reza-Gharehbagh, Arisian, Hafezalkotob, & Makui, 2023; Qi, Ma, Liu, Zhang, & Wang, 2024). Similarly, AIQ aids corporate financing decisions and information symmetry (Wang, 2024; Kharouf et al., 2020) and thus brings positive outcomes for SCR.

Bai, Huang, and Wang (2024) discussed the impacts of DFI on SCR from a different standpoint. Despite many earlier studies focusing individually on DFI, AIQ and SCR, there is a scarcity of research that integrates these three fields. Moreover, fewer studies have focused on quantitative perspectives while studying DFI, AIQ and SCR from a Chinese perspective. Therefore, the current study fills this gap by investigating the impact of DFI and AIQ on SCR. The study further contributes by exploring the mediating role of value co-creation (VCC) and goodwill (GW) because both perspectives emphasise the importance of inter-organisational collaboration (Al-Omoush, de Lucas, & del Val, 2023; Wang, Dong, & Zhai, 2023), thus strengthening SCR through DFI and AIQ. Moreover, the study adds to the existing literature by uncovering the moderating impact of financial regulation (FR) between the association of DFI, AIQ and SCR, because the FR channels such mechanisms through which DFI and AIQ foster operational resilience among supply chain companies. This gap is particularly significant in China’s industrial segment, a vital component of the global supply chain. Understanding how DFI and AIQ pillars can enhance information sharing, financial support and risk distribution is important and will eventually improve SCR. DFI facilitates small and medium-sized enterprises (SMEs) by providing digital financial services (such as mobile payments, online financing and digital insurance), focusing on lower-tier suppliers. On the other hand, AIQ guarantees that financial and operational reporting is trustworthy, transparent and timely, facilitating decision-making and building confidence across the chain. DFIs enable players to engage in financial and trade networks, but their efficacy depends on accurate and trustworthy accounting information to assess creditworthiness, manage risk and maintain compliance. High AIQ increases the effectiveness of DFI technologies by allowing for more accurate credit scoring, fraud detection and contract enforcement in digital contexts. When both DFI and AIQ are robust, organisations may better analyse suppliers’ financial health and reliability, boosting resilience through improved partner selection and risk management. Small suppliers with access to DFI and who can create high-quality accounting data are more likely to obtain financial assistance swiftly during interruptions, making the entire supply chain more robust. Therefore, the current study jointly investigates DFI and AIQ in the context of SCR.

2. Review of literature

2.1 Nexus of DFI and AIQ with SCR

Resource-based theory emphasises that it is only through unique internal resources and capabilities that a business can achieve its competitive advantages (Kozlenkova, Samaha, & Palmatier, 2014; Shan, Luo, Zhou, & Wei, 2019). This theory assists the firms in strengthening their resource base and core competencies for resilience. As a result, the manufacturing firms increase their ability to recover from potential disturbances in the supply chains. Firstly, using big data analytics and artificial intelligence, DFI empowers companies with exceptional abilities to process information and manage risk. This will allow firms to anticipate market trends better and identify supply chain vulnerabilities, thus making the supply chain more responsive and flexible (Gupta, Modgil, Choi, Kumar, & Antony, 2023). Secondly, DFI platforms enhance effective resource complementarity and aggregation among the various supply chain firms by integrating financial services and information flow. Such cooperation enhances collective risk resistance and coordination efficiency (Zaman, Khan, Qabool, & Gupta, 2023). Finally, DFI facilitates the quick processing of information and dynamic allocation of resources and allows firms to rapidly switch strategic priorities as well as models of operations based on changing conditions. In the same way, AIQ facilitates better corporate financing decisions (Wang, 2024) and aids information symmetry (Kharouf et al., 2020), thus bringing optimistic consequences for SCR. Finally, by creating value, DFI and AIQ ensure supply chain stability, consistency and robustness. In that respect, we offer the following hypotheses:

DFI improves SCR in manufacturing firms.

AIQ improves SCR in manufacturing firms.

2.2 Nexus of value co-creation and goodwill between DFI, AIQ and SCR

The value co-creation theory puts the joint activities of companies and stakeholders that seek to pool their resources, information and expertise in generating and distributing value to mutual competitive advantages and enhance market adaptability (Al-Omoush et al., 2023). According to Blaschke, Riss, Haki, and Aier (2019) and Alqayed, Foroudi, Kooli, Foroudi, and Dennis (2022), VCC points out the role of cooperation and interaction in increasing aggregate value in SCM. DFI, supply chains, blockchain and big data technologies support a more transparent data structure for value co-creation (Akhavan & Philsoophian, 2023). It enhances the responsiveness of the supply chain partners toward changing markets with increased transparency and real-time information. Consequently, it decreases the information asymmetry risk that supports SCR. Thus, we propose the H3:

Value co-creation (VCC) mediates the impact of DFI on SCR.

The greater the capability to expand accounting information transparency, the less information asymmetry between external stakeholders and management (Kharouf et al., 2020). When profit-generating pressure from sources such as green finance exists in an open channel for information communication, managerial opportunism can drop significantly. The institutional theory suggests that business organisations must abide by these standards to gain legitimacy regarding the business’s operational affairs (Risi et al., 2023). Besides, studies have shown that responsive firms to policy measures tend to have solid ethics and, therefore, can exhibit corporate behaviour, preventing principal-agent problems (Pacces, 2021). Furthermore, the higher a firm attends to its corporate social responsibility, the more believable and transparent accounting data will be; thus, the quality of accounting information will improve (Khuong et al., 2022). The value of co-creation aspects and risk management in financial services that AIQ will offer would best serve the needs of the supply chain members. Thus, we propose the H4:

Value co-creation (VCC) mediates the impact of AIQ on SCR.

GW is the company’s expected profit levels, and current literature is focused chiefly on GW creation and the associated effect on the economy (Kay & Skarlicki, 2020; Wang et al., 2023; Ferramosca & Allegrini, 2021). While talking about the impact of GW, most research studies examined the economic effects of GW via the perspective of the risk from stock price collapse, corporate behaviour and firm performance (Cheng, Susan, Lin, & Luo, 2024). However, the impact of GW on SCR has not been extensively investigated. The DFI tools, including smart contracts, ensure automatic contract fulfilment. This reduces default risks and enhances GW while raising the members’ trust in the supply chain. Trust (GW) fuels deeper engagement in value-creation projects, increasing the robustness and resilience of supply chains (Utami, Alamanos, & Kuznesof, 2021). DFI enhances GW, values cooperation and financial risk management abilities while coping with supply chain risks for efficient resource allocation. Such optimisation enables the supply chain to react flexibly when it is interrupted by external sources (Zhang, Yang, Yang, & Gao, 2022). Thus, we propose the H5:

Goodwill (GW) mediates the impact of DFI on SCR.

GW has further affected a firm’s profitability level since an empirical result indicated positive proportionality with profitability for listing companies, whereby a higher value proportion translates into increased strengths in the profit generation streams (Chelba, Melega, & Grosu, 2023; Kim, Fujiyama, & Koga, 2024). An important phenomenon concerning a firm is that GW will also impact the quality of corporate accounting information, further augmenting the company’s repute and aiding in the negotiation of corporate debt agreements (Thakur, Noordin, Matemilola, Alam, & Setiawan, 2022; Li et al., 2024; Wang, 2024), thus aiding positive outcomes for SCR. China has promoted the AIQ in the manufacturing industry to help businesses transition to green and sustainable practices. Such AIQ comprises setting climate ethics, monitoring and enforcing penalties for noncompliance. Thus, we propose the H6:

Goodwill (GW) mediates the impact of AIQ on SCR.

2.3 Impact of financial regulations on the nexus of DFI and AIQ with SCR

The market failure theory states that the market system fails to achieve efficient resource allocation because of many problems, such as market monopolies, information asymmetry and other external factors. As an innovative financial business model, DFI and AIQ encourage the need for financial regularities (Feng, Zhang, & Li, 2022; Thakur et al., 2022; Li et al., 2024), which are vital measures to preserve the financial system’s safe and stable condition, therefore boosting trust among businesses and the public. This, in turn, enhances commercial SCR (Iftikhar, Purvis, Giannoccaro, & Wang, 2023). Strong rules promote the capability of financial institutions to manage financial hazards and recover the performance of financial facilities that are advantageous to the real economy in endorsing SCR. However, the complexity, dependence and volatility associated with DFI and AIQ exacerbate more risks from under-regulation than traditional financial models. The supply chain uncertainty may also increase during external shocks due to DFI (Cao, Nie, Sun, Sun, & Taghizadeh-Hesary, 2021; Silva & Ruel, 2022). Thus, regulatory action should be stricter on DFI. Strong and supportive FR may boost the effect of DFI by assuring safe, inclusive and well-regulated digital financial systems. It increases confidence in digital transactions and protects vulnerable supply chain participants, improving financial access amid interruptions. However, too tight or outmoded laws may hinder innovation and access, undermining DFIs’ beneficial impact on resilience. Effective regulation improves the quality and consistency of accounting methods, highlighting AIQ’s role in enhancing transparency, risk management and financial forecasting. Robust regulatory standards guarantee that accounting data are reliable and similar across organisations, allowing for better informed, robust supply chain choices. In contrast, lax regulation may allow for data tampering or inconsistency, reducing AIQ’s benefits for SCR. Therefore, it is important to investigate how financial regulations moderate the association of DFI and AIQ with SCR. Thus, we propose H7 and H8:

Financial regulation (FR) moderates the relationship between DFI and SCR.

Financial regulation (FR) moderates the relationship between AIQ and SCR.

3. Methodology and data description

3.1 Data and sample

Firms from the manufacturing sector were used as the sample in this study to examine the impressions of DFI and AIQ on SCR based on the following filtering criteria: (1) firms with fewer than three consecutive years of observation are excluded from the data, (2) samples not containing key variables were ignored and (3) all data was trimmed to 1% to help reduce outliers. Subsequent empirical analyses were carried out utilising EViews 12.0 econometric software. Data were obtained from the Peking University Digital Inclusive Finance Index, China Statistical Yearbook, China Securities Market & Accounting Research and Wind databases from 2015 to 2024. The data are collected for 1,100 companies and comprise 11,000 observations.

3.2 Variable specifications

According to contemporary academic research, SCR reflects the resilience and recoverability of an entity against external shocks (Negri, Cagno, Colicchia, & Sarkis, 2021). Hence, the study categorises SCR into two major streams – the defensive and recoverability capacities of the supply chain. Major indicators were then derived from the two areas, and a composite index approach was used to evaluate SCR. Specifically, (1) SCR denotes the supply chain’s stability against disruption from the external side. Following the guidelines given by Nejati, Rabiei, and Jabbour (2017), the ratio of the interactive relationships that a firm enjoyed with its top five customers during consecutive years was used to define SCR (as suggested by Chen & Yu, 2024). A higher ratio means a stronger supply chain partnership, and (2) recovery represents how the supply chain recovers after deviating from its standard patterns. Adopting Shan, Yang, Yang, and Zhang (2014), the measure of “deviation” between variations in production and demand was utilised to measure supply chain recovery. Hence, the current study utilises SCR as the dependent variable.

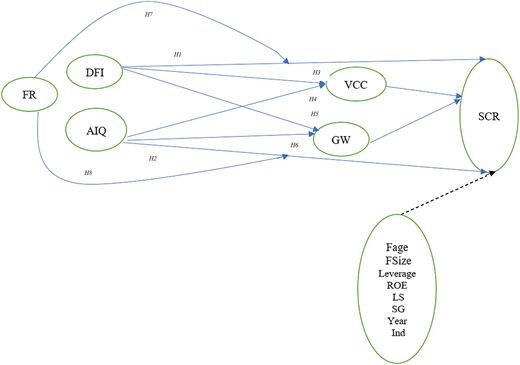

The Beijing University Digital Inclusive Finance Index is considered the best measure of DFI. Many studies applied provincial panel data; however, for this study, index data were taken related to the city where the firm is headquartered. AIQ directly impacts a company’s operational risk, influencing resource allocation and operational decision-making. This work refers to current literature and uses an enhanced Jones model for measurement (Dechow, Sloan, & Sweeney, 1995). Absolute values are counted for relevant items; a lower absolute value indicates a better accounting information standard (AIQ). Therefore, DFI and AIQ are used as primary independent variables. Following the study of Jiang, Wang, and Sam (2024), FR is used as a moderating variable in the current study. We added value from the local financial sector and the financial regulatory expenditure ratio as a measure for FR. Figure 1 depicts the association among the variables.

According to Kumar et al. (2010), value co-creation (VCC) depicts firms’ customer engagement values among their users. Customer concentration and/or engagement in the financial reports of listed companies in China is the total business volume contributed by the five biggest customers. Based on Peiyao and Benrui (2024), we used the degree of customer dispersal as our proxy variable to gauge VCC. On the other hand, GW shows a company’s future profit potential and is a valuable asset for business owners. Based on the study of Danni and Zejiang (2021), the ratio of the net value of GW and total assets allows for comparisons between companies. Hence, VCC and GW are mediating variables in the current study. Several factors, such as firm age, size, debt-to-asset ratio, return on assets, the largest shareholder’s shareholding ratio and revenue growth rate, were controlled to reduce estimation bias and focus on the impact of DFI and AIQ on SCR. The definitions and calculation methods of the main variables are reported in Table 1.

3.3 Econometric models

To experimentally test the effect of DFI and AIQ on SCR, this study develops a regression model in Equation (1) as follows:

Where SCRi,t is the outcome variable indicating SCR. DFIi,t is the independent variable signifying DFI. Similarly, AIQi, indicates AIQ. ∑Controli,t represents the set of control variables and εi,t is the stochastic error term. To further examine the mechanism where DFI and AIQ influence SCR from the VCC perspective in conjunction with Equation (1), we presented regressions (2), (3) and (4) as follows:

Where VCCi,t is the mediating variable, ζ1 gives the effect of DFI and AIQ on VCC and η1 denotes the coefficient of the mediator. Similarly, to further uncover the mechanism where DFI and AIQ influence SCR from the GW perspective in conjunction with Equation (1), we presented regressions (5), (6) and (7) as follows:

Where GWi,t is the mediating variable, ζ1 gives the effect of DFI and AIQ on GW and η1 denotes the coefficient of the mediator. Furthermore, to inspect the role of FR in the connection between DFI and SCR and AIQ and SCR, Models (8) and (9) are proposed:

Where κ2DFIi,t × FRi,t and κ2AIQi,t × FRi,t show the interaction terms between dependent and independent variables.

4. Empirical outcomes

Table 2 illustrates descriptive statistics for all the variables under study. SCR has a mean value of 0.924 with a 0.382 least value, a 0.978 extreme value and a 0.211 value for standard deviation. In the sample, the mean value of SCR is close to 1 (generally high), and most of the estimations are close to the mean value, which indicates that SCR is equally distributed in the sample. The maximum and minimum values show the volatility of SCR. DFI has a mean value of 6.374, with a least value of 4.733, a maximum value of 7.99 and a standard deviation value of 0.780. Table 2 shows that other variables are within ordinary and/or normal ranges. A test choice for a panel data model is conducted to analyse the practical association between DFI, AIQ and SCR. To verify the effect of DFI and AIQ on SCR, model 1 shows aggregated ordinary least squares (OLS) regression. To uncover the association between DFI, AIQ and SCR, Model 2 demonstrates panel fixed effects (FE). To find the impact of DFI and AIQ on SCR, Model 3 calculates panel random effect (RE); see Table 3. This study also employs a Hausman test, which shows that the outcomes of panel fixed effects are best for the baseline regression. Thus, we chose the panel FE model as the regression model for practical testing. In Model 2, the regression outcomes indicate that DFI and AIQ positively influence the SCR at 1%, with an effect coefficient of 0.065 and 0.392, respectively. Thus, H1 and H2 are accepted, as DFI and AIQ positively influence and enhance SCR. As the literature suggests, the DFI and AIQ considerably positively affect SCR. To verify the claim, the current study employs the following reliability tests. Firstly, for analysis, the mixed OLS and RE models are utilised to substitute the FE model in standard regression. Secondly, a lagged-effect test was conducted, and the regression outcomes are displayed in Table 4. After the replacement of the model, Table 3 presents that the regression outcomes of Models 1 and 3 show that DFI and AIQ positively influence SCR at 1%, supporting the reliability of outcomes of baseline regression.

To analyse whether the lagged terms influence the SCR, the study selects lags of 1 and 2 periods. The outcomes after lagging the independent variables are presented in Models 1 to 4 (Table 4), where Models 1 and 2 show the outcomes after lagging the DFI at lag 1 and 2 periods. Model 1 shows that lagged 1-period DFI positively influences SCR at a 1% significance level with a coefficient value of 0.046. The outcomes of Model 2 show that the lagged 2-period DFI also positively influences SCR at 1%, with a 0.055 coefficient. Similarly, Model 3 shows that lagged 1-period AIQ positively influences SCR with a 1% significance level, with a coefficient value of 0.168. The outcomes of Model 4 show that the lagged 2-period AIQ also positively influences SCR at 1%, with a 0.172 coefficient. The regression outcomes pass the reliability checks, verifying the reliability of the baseline regression outcomes.

As the literature review section mentions, VCC and GW are the most prominent conduction pathways through which DFI and AIQ influence the SCR. To test empirically whether VCC and GW mediate the DFI-SCR and AIQ–SCR relationships, we include them as mediators in Equations (2)–(7). Table 5 presents the outcomes of mediating variables. Column 2 reports the result of the baseline regression. Model 2 in column 3 represents the effect of DFI on the VCC (mediator). Meanwhile, Model 3 in column 4 represents the effect of AIQ on the VCC (mediator). Column 5 reports the impact of VCC on SCR. The results clearly show that the coefficients of DFI and AIQ are highly significant. Hence, DFI and AIQ have now become enhancers of VCC, and VCC positively impacts SCR, thus supporting H2 and H4. We found similar results for GW; hence, H5 and H6 were also accepted.

We add financial regularities and their interactive terms with DFI and AIQ to the regression models (Equations 8 and 9). Diagnostic outcomes related to the moderating effect of financial regularities on the DFI and SCR are as exposed in Table 6. The interactive coefficient of DFI and FR is remarkably positive, meaning financial regulations enhance SCR through DFI. Building up financial regularities effectively encouraged the positive impact of DFI on SCR, thereby supporting H7. The H8 is also accepted because we found similar results of moderating the influence of FR on the effects of AIQ on SCR.

The study first estimates the heterogeneity of the firm’s lifecycle to uncover the effects of heterogeneity. Grounded on the undertaking “life cycle theory,” we segmented the undertaking into three stages: start-up, growth and maturity. Regression results for all three stages in models 1 through 3 in Table 7. Both DFI and AIQ have a more substantial promotional impact on SCR at the maturity levels. Secondly, the study estimates the heterogeneity of the regional business environment. This study employs the marketisation index to categorise the business settings into beneficial and non-beneficial categories. The regression findings for both categories are presented in Table 8. Table 8 shows that DFI and AIQ have more significant promotional effects on corporate supply chains in attractive business environment locations.

5. Conclusions, implications and recommendations

This paper has analytically uncovered the influence of mechanisms of DFI and AIQ on SCR. The internal mechanisms that affect SCR are determined through theoretical analysis. The panel data are used from 2015 to 2024 of registered manufacturing corporations in China. We find that DFI and AIQ significantly improved SCR. Several robustness tests are applied to support such conclusions. The mechanism test showed that DFI and AIQ improve SCR by enhancing VCC and GW; moreover, FR completely moderated the association between DFI and SCR, as well as AIQ and SCR. The effect of DFI and AIQ on SCR is more pronounced in mature firms and regions with a supportive business environment. The conclusions deliver practical implications for assessing DFI and AIQ’s impact on businesses, corporate governance and government policymaking. Hence, we propose the following: First, the government and related institutes must invest more in DFIs and accounting information infrastructures. It includes increasing cloud computing technologies, stability, network coverage, mobile payments and digital accounting information systems. Second, AIQ should be innovative, with financial products and services adapted to supply chain features and needs, personalised offerings and specific financial and risk management solutions for financial organisations. Firms should also advance the quality of accounting information to improve SCR. Third, the laws and regulations of supply chain financing should be refined by governments so that all parties in the supply chain have sound legal protection. The government should enhance collaboration with global financial regulatory organisations according to leading global practices to improve supply chain financing regulatory levels in China. This can improve the transparency of supply chains, the efficiency of collaboration and the capacity for risk management, therefore strengthening SCR. Fourth, mature-stage enterprises should use their resources and knowledge by increasing investments in and applications of DFI technology and improving AIQ. This may bolster risk management ability, collaboration efficiency and supply chain transparency, thus fortifying SCR.

The paper presents a groundbreaking approach to the theoretical integration of management science, finance, accounting and supply chain management by mixing the notions of DFI, AIQ, VCC, GW, FR and SCR. The results in a changing and dynamic market landscape demonstrate how AIQ and DFI can enable alliances and VCC among enterprises across supply chains, improving their compliance and understanding of their environment. The study also has a few limitations. The study provides a broad data source and relevant context by focusing on publicly listed manufacturing companies in China. However, the results might not apply to SMEs in other countries due to differences in the legal system, market maturity and digital advancement. Upcoming researchers could explore the subtle interaction between fintech, value co-creation and accounting reporting quality to enhance SCR. For instance, future research might emphasise the scalability of digital financial and accounting solutions. Future studies may investigate the same phenomenon in different countries. The researchers are recommended to explore the exact model under different market conditions (see Shahid, 2022; Shahid & Sattar, 2017, for various market conditions).