The transition from corporate social responsibility to environmental, social and governance (ESG) has brought realised benefits to businesses, including increased investor favourability, increased financial performance and enhanced brand image. Unearthing the barriers, drivers and key interested stakeholders of ESG reporting in public–private partnership (PPP) project is crucial for improving the ESG outlook of a project. While research studies have identified a range of barriers, other works have identified how these can be addressed. This study aims to uncover the critical barriers and drivers of ESG reporting and explores how they can be turned into facilitators.

This study meta-analysed and synthesised empirical studies by undertaking a systematic review.

Seven main barriers, six drivers and interested parties of ESG reporting of PPP projects have been identified. Significant barriers to ESG reporting of PPP project includes insufficient understanding of ESG benefits, lack of standardised reporting frameworks and the cost involved in ESG reporting. Also, key drivers for ESG reporting comprise of regulatory disclosure demands and improved project performance. Addressing these barriers and leveraging the drivers is crucial for the successful integration of ESG reporting within PPP projects for enhanced sustainability performance and long-term project success. PPP projects encompass a diverse group of stakeholders each with a vested interest in the sustainability and governance outcomes of a project. These groups form a complex network of interests that drive the need for transparent and robust ESG reporting.

This study unearths significant barriers and drivers to ESG reporting in PPP projects providing the significant motivators to ESG reporting uptake and critical challenges. The findings of this study advocate for policies that factor the importance of ESG reporting, thereby enhancing PPPs commitment to sustainable practices.

1. Introduction

Global sustainability reporting indicates that 79% of N100 companies reported on sustainability, and nearly all the world’s top 250 companies (G250) now report on sustainability, with a reporting rate of 96% (KPMG, 2022). Environmental, social and governance (ESG) reporting is a comprehensive disclosure of a company’s ESG initiatives that allows stakeholders to make informed decisions about the sustainable commitment of a company’s practices (Krantz and Jonker, 2024). Reporting ESG for companies and projects is crucial for several reasons. It helps in meeting legal and regulatory requirements, ensuring transparency and accountability in operations. It is evident that ESG reporting leads to improved project performance and long-term returns, reflecting the interests of stakeholders focused on sustainability (Amalia et al., 2023; Chao and Farrier, 2021; Kharlamov, 2023). Furthermore, societal and external stakeholder pressures drive the demand for ESG reporting, accenting the need to address these pressures for long-term sustainability. ESG reporting involves a wide range of factors, including that of environmental impact assessments, social responsibility initiatives and governance practices of the project. ESG reporting for public–private partnerships (PPP) projects may have unique drivers and may be faced with specific challenges because of the peculiarities of the project. Some environmental disclosure such as energy consumption, waste reduction and carbon emissions should be reported by PPP projects (Chao and Farrier, 2021). Also, social or societal disclosures that cover aspects such as community engagement, labour practices and diversity and inclusion efforts are necessary (Amalia et al., 2023). Furthermore, governance practices of the project should also be reported, addressing issues related to defined plan for reaching commercial and financial close of the project, improved supply chain planning and due diligence with tender documents and drafted PPP contracts (Kharlamov, 2023). ESG issues are critical for public–private investors when investing in infrastructure assets and are therefore considered to be like any other investment risk. AMP Capital (2013) purports that ESG considerations in infrastructure PPPs aim to create greater wealth and better investment decisions and opportunities and therefore is critical to report ESG practices of PPP projects. By reporting on these ESG criteria, PPP projects can demonstrate transparency and accountability while addressing the expectations of stakeholders.

It is posited that the way of reporting ESG should be aligned with the regulatory and legal requirements of PPP projects. This will ensure transparency and accountability in project operations, reflecting the demands from internal, connected and external stakeholders (WBCSD, 2019). ESG reporting must be presented in a way that places emphasis on its influence on project performance, long-term returns and the overall success and longevity of PPP projects (Weber et al., 2016). Societal expectations and external stakeholder interests are crucial to strategically addressing pressures for transparency and accountability in ESG practices with infrastructure investments. Therefore, the reporting of ESG should be integrated into PPP projects in a manner that reflects its peculiarities, significance and impact on project operations (Amalia et al., 2023). It is critical that during ESG reporting, the diverse group of stakeholders, including regulatory bodies, investors, shareholders and the public, is considered. Reporting ESG practices of a project gives the public a reason for the execution of the project, and it demonstrates a commitment to sustainable and responsible business practices. Furthermore, sharing ESG practices with stakeholders is vital for addressing societal and environmental concerns, as well as for fostering transparency and trust (Alsayegh et al., 2020). Ultimately, reporting on ESG to a wide range of stakeholders is essential for promoting transparency, accountability and long-term sustainability in PPP projects. However, it is critical to identify the intended stakeholders to report ESG to within the PPP enclave. This is crucial as it affects what the project reports and considers important, thus enabling management to evaluate what is most useful for their needs and to determine the most significant information to report to its audience (WBCSD, 2019).

The transition from CSR to ESG has brought several benefits to businesses, including increased investor favourability, improved performance and enhanced brand image (Acharyya and Agarwala, 2022; Andrey, 2023; Robinson and McIntosh, 2022). These benefits are realised through mechanisms such as ESG information disclosure and improved operational efficiency. There exist barriers to ESG adoption because of the lack of clarity around regulatory and reporting standards (Parameswar et al., 2023). Also, drivers of ESG within PPP projects can be attributed to coordinating mechanisms of its stakeholders that support operational success. These mechanisms are crucial for overcoming the complexities and inefficiencies that arise from the collaboration between public and private sectors. Addressing the barriers to ESG adoption and implementing effective coordinating mechanisms that are essential drivers for the success of ESG within PPP initiatives present a practical and achievable path to sustainability performance. This study presents significant barriers and drivers that will lead to accurate ESG disclosure and success of ESG within PPP practices. This study through synthesis of literature presents barriers, drivers and key interested stakeholders associated with ESG reporting in PPP. The paper is organised into five sections: Section 1 – introduction, Section 2 – methodology, Section 3 – analysis and discussion of results, Section 4 – implications and proposition for future research and Section 5 – conclusions.

2. Research methodology

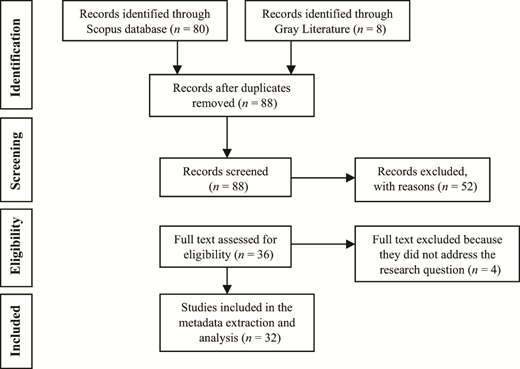

In identifying the barriers and drivers of ESG reporting, it is critical that a systematic literature review (SLR) of previous studies on sustainability reporting and ESG disclosure practices of PPP projects, construction projects and other related mega projects is done. This is to identify, select and critically appraise research studies to answer the research questions of this study. This is a scientific process followed to ensure that there are no biases with the data obtained for this investigation. The appropriateness and suitability of using SLR to understand barriers and drivers of an emerging research interest has been established in literature (Wuni, 2022). As such, this current study has used SLR guided by the preferred reporting items for systematic reviews and meta-analyses (PRISMA) for this investigation (Page et al., 2021). This was adhered to because it is identified as a protocol that minimises the risk of bias and increases scientific validity of research findings. This roadmap describes how the research was done and what was found. Towards the end of this SLR, the study formulated research questions, provided keywords that were used to select articles, database that was used, literature search and retrieval, screening, inclusion/exclusion, metadata extraction and data analysis. Figure 1 presents the PRISMA flowchart, indicating how the study meticulously followed the scientific process to select relevant papers for the study. The section below presents on the data collection and preparation process.

2.1 Data collection and preparation

This study has used the Scopus database to search for the academic literature published on the area of the study focus. The search was done in February 2024 and re-searched in March 2024 to cover materials that were published in February 2024 before the data extraction and metadata extraction were done. The study also used grey literature, which is one of the main sources used to obtain organisational reports that formed part of the selected documents ( AppendixTable A1) reviewed to identify the barriers and driver’s to ESG reporting of PPP projects. This was done to ensure that the study presents a comprehensive coverage of the research domain. Search of articles and organisational reports did not restrict the date for which articles or organisational reports were published. The field of SLR and the broader PRISMA process lack a unified and cohesive approach for identifying search terms (Beller et al., 2013; Paul et al., 2021). It is important to recognise that the selection of any set of word strings is constrained by their completeness (Polonsky et al., 2022). The study used the following search terms: “Environmental, Social, and Governance Report*” OR “Environmental, Social, and Governance Disclosure” OR “ESG Report*” OR “ESG Disclosure” OR “sustainability reporting” OR “corporate reporting” OR “sustainability disclosures” OR “corporate performance” OR “environmental performance” “barriers” OR “hindrances” “inhibitors” OR “constraints” OR “inhibiting” OR “impeding” OR “obstacles” OR “bottle-necks” OR “bottleneck” OR “deterrent” OR “challenges” OR “failure*” OR “drivers” OR “facilitators” OR “determinant” OR “develop*” OR “growth” OR “benefit” OR “success” “construction” OR “construction project” OR “infrastructure” OR “infrastructure project” OR “mega?project” OR “PPP project” OR “public?private*” OR “private investment” OR “build operate transfer” OR “build, own and operate” OR “build, own, operate and Transfer” OR “build, transfer and operate” OR “Build-Operate-Transfer” OR “Asset management”.

The integrated refined search identified 80 works in Scopus and eight documents from grey literature, a total of 88 documents. This includes organisational reports, book chapters, conferences and articles, with the recommendation by other research that suggests the inclusion of all types of studies, including those that have not been previously published (Choudhury et al., 2020). After the removal of articles that were not relevant for analysis and based on abstract search and full-text reading, the study maintained 32 documents for metadata extraction. This was followed by reviewing full text to identify related barriers and drivers of ESG reporting for PPP projects. These 32 documents were summarised and meta-analysed to identify the barriers, drivers and key stakeholders within the study.

3. Results and discussion

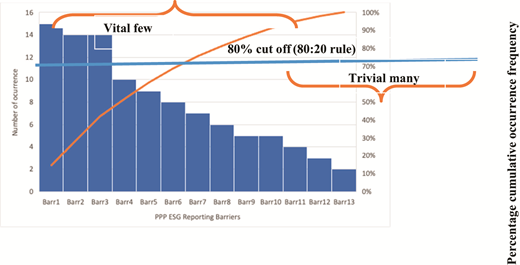

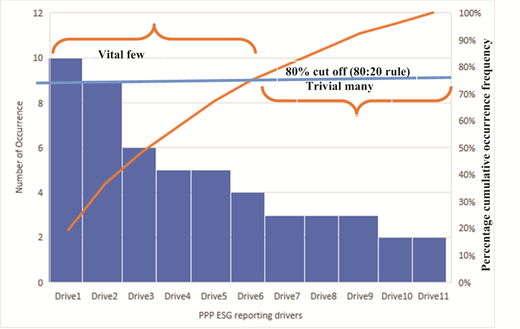

After collecting metadata from the 32 selected documents ( AppendixTable A1), the study presents quantitative investigation based on the data obtained. The study has used graphs like pie chart, bar graphs and Pareto distributional chart to make presentation of findings. The frequency of occurrence of an identified barrier or driver in documents is presented, whereas the frequency of articles and documents published in years, methodology used and countries of focus of selected studies have been presented. The Pareto distributional plot has been used to identify prioritised barriers and drivers to ESG reporting in PPP projects. The Pareto principle, also known as the 80/20 rule, posits that in many events, approximately 80% of the effects stem from just 20% of the causes (Erridge, 2006; Grosfeld-Nir et al., 2007). This heuristic highlights the unequal distribution of outcomes based on inputs. Specifically, the cumulative frequency is equivalent to 100%, with the “vital few” barriers or drivers accounting for a substantial 80% of the cumulative percentage of frequencies. By contrast, the “trivial many” barriers or drivers make up only the remaining 20% of occurrences. To identify these critical barriers and drivers, this study used Pareto charts (including histograms and curves) for the barriers and drivers of ESG reporting in PPP projects. Also, the number of occurrences of an identified barrier or driver has been used to determine the significance of the factor using relative importance index (RII). Critical barriers and drivers of PPP ESG reporting trends have been identified by calculating its relative importance using the mathematical formula below:

where is the weight assigned to each factor within a document (i.e. 0 or 1), N is the total sample size, which is 32 in this study, and a is the highest impact (1 in this case). The RII presents the evidence of existing barriers and drivers of ESG reporting for PPP projects in the literature.

3.1 Overview of selected studies

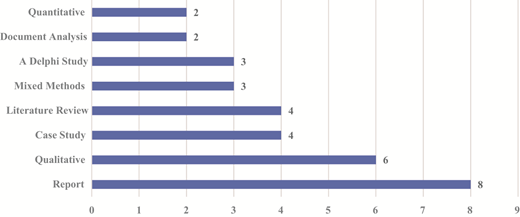

As it is depicted in the chart below (Figure 2), across the relevant works, there were six main methodological approaches: reports (eight), qualitative studies (six), case studies (four), literature review or conceptual works (four), mixed method studies (three) and Delphi studies (three), document analysis (two) and purely quantitative studies (two). It is inferred that studies related to ESG reporting of PPP projects have diverse methodological approaches used in the relevant literature, highlighting the richness of research methods used. It is evident that eight works used a report-based approach, which serves as a rich descriptive information of the phenomena of study. Deloitte (2022) in its report identified barriers associated with ESG reporting. The evidence presented illustrates that the lack of common language in ESG reporting has resulted in fragmentation, complexity and increased costs. Additionally, organisations are often ill-equipped with the necessary knowledge, skills and information to effectively engage in ESG reporting. Also, the evidence from qualitative studies confirms the extent to which prior research delved into the subjective experiences, opinions and behaviours of individuals about ESG reporting. A recent study by Izquierdo et al. (2024) explored the drivers of ESG reporting through qualitative investigation. Their findings reveal that project success factors, contractual requirements and preconstruction considerations significantly influence ESG reporting practices within the built environment.

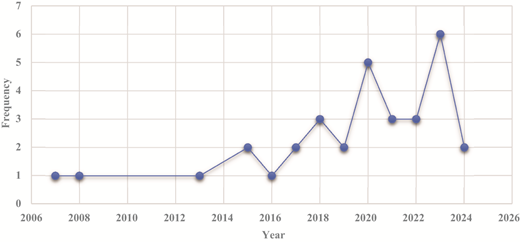

As can be seen in Figure 3, most of the 32 selected documents are relatively recent publications, and a significant proportion of the selected studies (approximately 60%) was published between 2020 and 2024. This surge in recent publications indicates a growing interest in ESG reporting within the context of PPP projects. It would therefore appear that interest in ESG reporting in PPP projects is a relatively new but growing research area. Around 30% of the selected articles fall within the time frame of 2019–2015. These mid-term publications contribute to the evolving body of knowledge ESG reporting for PPP projects. Approximately 10% of the works date back to the period between 2014 and 2007. While relatively fewer in number, these earlier studies provide valuable insights into the historical context of ESG reporting in PPP projects. This distribution suggests that interest in ESG reporting within the PPP domain is relatively new but steadily gaining momentum. Researchers and practitioners are increasingly recognising the benefits of ESG reporting for infrastructure projects, and this trend is reflected in the recent surge of scholarly contributions.

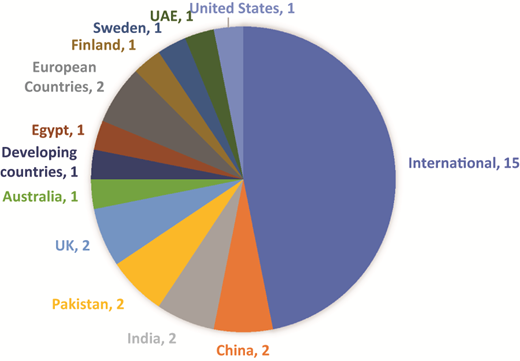

The studies assessed emanate from a wide range of countries, with 15 selected documents focusing on international investigation. It is shown that two were undertaken in China, India, Pakistan and the UK. Individual studies were undertaken in Australia, developing countries setting, Egypt, European Countries, Finland, Sweden, the UAE and the USA (Figure 4). It is evident that overall, there appeared to be higher levels of interest in ESG reporting of PPP projects in the global scene.

3.2 Identification of barriers and drivers

An analysis of the metadata of the literature selected for the purposes of this study has been used to provide thematic analysis of the various barriers and drivers identified in this study. At the first stage, factors for barriers and drivers of ESG reporting of PPP projects have been identified through the literature synthesis. Based on the ideas, terms and findings of these previous studies, 13 barriers have been identified, and 11 drivers were similarly identified, where RII computations and the Pareto have been used to identify prioritised factors. Table 1 presents the statistical results of the identified barriers and drivers. The number of occurrences, weight of a factor and RII values have been presented.

The 13 barriers of ESG reporting of PPP projects are shown to be competing project priorities, insufficient understanding of the benefit of ESG reporting, lack of investment in training and development programs for critical actors, unavailability of standardised ESG reporting standards and frameworks, complex administrative requirements and legal enforcement procedures, insufficient government incentives, cost involved in ESG reporting, difficulty measuring and tracking ESG performance, absence of comparability ESG metrices, ratings and investment approaches, lack of sound infrastructure and technology to report ESG, limited public awareness of ESG reporting, difficulty in compiling and digitising unstructured data from multiple sources and inadequate ESG expertise for PPP projects. These barriers have been arranged in order of importance based on the literature gathered. The study has identified several barriers to ESG reporting in PPP projects, with the most significant being competing project priorities, which appeared 15 times, indicating a conflict between immediate project demands and long-term ESG goals. Insufficient understanding of the benefit of ESG reporting and lack of investment in training and development programs for critical actors both occurred 14 times, highlighting a gap in knowledge and expertise. The unavailability of standardised ESG reporting standards and frameworks was mentioned ten times, reflecting the complexity of establishing consistent reporting practices.

Also the 11 drivers to ESG reporting are regulatory disclosure demands, improved project performance and expected long-term returns, society and external stakeholder pressures, desire to mitigate project risk, economic benefits, altruistic values, government and regulatory pressures, employee and activist investor pressure, establishing cross-functional teams and accountabilities, requirements imposed by banks and other lenders and supply chain concerns. The key drivers for ESG reporting include regulatory disclosure demands, with an RII of 0.31, emphasising the influence of legal and regulatory requirements. Secondly, improved project performance and expected long-term returns had an RII of 0.28, suggesting that ESG reporting can enhance project success. Society and external stakeholder pressures were also notable, with an RII of 0.19, indicating the impact of societal demands on ESG practices. These factors underscore the multifaceted nature of ESG reporting, where both barriers and drivers shape its adoption and implementation in PPP projects. Prioritised barriers and drivers to ESG reporting have been profiled based on the Pareto chart in the section below.

3.3 Critical barriers to environmental, social and governance reporting of public–private partnership projects

The Pareto distributional chart has been used to identify significant barriers to ESG reporting of PPP projects (Figure 5). This Pareto analysis presents the barriers in a decreasing order of relative frequency from the left to right. It is shown from the Pareto chart that the most important barriers to ESG reporting of PPP projects include competing project priorities (Barr1), insufficient understanding of the benefit of ESG reporting (Barr2), lack of investment in training and development programs for critical actors (Barr3), unavailability of standardised ESG reporting standards and frameworks (Barr4), complex administrative requirements and legal enforcement procedures (Barr5), insufficient government incentives (Barr6) and cost involved in ESG reporting (Barr7). It is shown that seven barriers to ESG reporting in PPP projects are identified.

3.3.1 Competing project priorities.

Competing project priorities challenge arises when the tangible demands of short-term project implementation – for instance, timely delivery, budget and quality requirements – are prioritised at the expense of long-term ESG reporting and consequent benefits that could lead to achieving sustainable goals for the project (Horry et al., 2022a, 2022b). Strategic coordination of project goals and ESG objectives can overcome this barrier to ensure that there is no conflict between meeting immediate project outcomes and long-term sustainability when implementing projects. High investment and low return on investment is yet another challenge. Often, PPP projects require a long-term upfront investment, and a return on the investment can be uncertain or low. Financial return on investment can create a prioritisation conflict, as the stakeholders require achieving the short-term financial returns despite the importance of long-term ESG goals. Chotia et al. (2023) purport that financial constraints and the uncertainty of economic benefits in PPP projects can affect ESG reporting. Such financial challenges can lead to a prioritisation of immediate fiscal stability over the integration of ESG reporting, which is essential for long-term sustainability.

3.3.2 Insufficient understanding of the benefit of environmental, social and governance reporting.

This barrier is recognised as a significant obstacle to ESG reporting within PPP projects. It is frequently mentioned across various studies, indicating a lack of awareness or knowledge about the advantages of ESG reporting. This gap in understanding can lead to underutilisation of ESG reporting, potentially affecting project sustainability and stakeholder trust. Enhancing education and communication about ESG benefits could transform this barrier into a driver for better reporting practices. Revell and Blackburn (2007) highlight that there is a compliance aspect to ESG reporting, which can be vulnerable due to insufficient understanding. This suggests that without a clear grasp of the benefits ESG reporting, PPP projects may only comply with ESG reporting requirements superficially or minimally, which can undermine the effectiveness of the reporting. Siew et al. (2015) purport that the lack of clear definitions of sustainable PPP project contributes to the insufficient understanding of ESG reporting. This implies that stakeholders may struggle to see the value of ESG reporting if they cannot define what sustainability means in the context of their project. Further, it is suggested by Shen et al. (2017) that there is little understanding and experience of green procurement and green building materials. This lack of knowledge can be a barrier to recognising the benefits of ESG reporting, as it is challenging to report on aspects of sustainability that are not well understood or implemented in the first place. These studies collectively suggest that a deeper understanding and clearer definitions in the realm of sustainability of PPP projects are crucial for recognising the full benefits of ESG reporting in PPP projects.

3.3.3 Lack of investment in training and development programs for critical actors.

Recognised as a significant barrier to ESG reporting in PPP projects. This barrier is a notable concern that leads to the insufficient understanding and implementation of ESG reporting. ESG reporting requires investment in training programs to enhance ESG expertise. The study by Montalbán-Domingo et al. (2020) highlights the importance of knowledge and experience-based training for critical actors in PPP projects for ESG reporting. It suggests that such training is essential for understanding and implementing ESG reporting effectively. Expertise deficiency as mentioned by Waqas et al. (2021) is indicative of lack of expertise as a barrier to ESG reporting. They emphasise the need for specialised training programmes to build the necessary skills for ESG reporting within PPP projects. The lack of support for staff and critical actors as Horry et al. (2022a, 2022b) identified is a hindrance to ESG reporting. Studies advocate for structured support systems to help critical actors navigate ESG reporting requirements. These studies collectively underscore the need for targeted training and development programmes to overcome the barriers related to ESG reporting in PPP projects.

3.3.4 Unavailability of standardised environmental, social and governance reporting standards and frameworks.

Another obstacle hampering the timely and accurate reporting of ESG information is the absence of widely accepted and uniform ESG reporting standards and framework. Lack of common reporting frameworks complicates the process of reporting and comparing the ESG performance of different projects. Developing targeted and universally accepted ESG reporting standards can enable better transparency and accountability regarding PPP projects. This barrier is supported by multiple sources in the literature, indicating its prominence in the field of ESG reporting of PPP projects. A study by Izquierdo et al. (2024) highlights the volatility in ESG regulation, which adds to the complexity of establishing standardised reporting frameworks. Additionally, CPA-Australia (2023) indicated that the lack of a common language in ESG reporting leads to fragmentation and complexity, making it difficult for PPP projects to adhere to a unified standard. It is evident that ESG judgement challenges, which are identified in literature, are exacerbated by the absence of standardised frameworks (CPA-Australia, 2023; Izquierdo et al., 2024). These studies mutually underscore the need for standardised ESG reporting standards to overcome the barriers and streamline the reporting process for PPP projects.

3.3.5 Complex administrative requirements and legal enforcement procedures.

The Pareto chart identifies complex administrative requirements as a significant barrier to ESG reporting in PPP projects, indicating that navigating ESG reporting requirements can be challenging. It also mentions legal enforcement procedures as a barrier, suggesting that the legal aspects of ESG reporting can be difficult to manage. This barrier contributes to the difficulties faced by PPP projects in implementing effective ESG reporting practices. The barrier implies that simplifying administrative processes and clarifying legal enforcement could improve ESG reporting. The administrative requirements for ESG reporting in PPP projects can be convoluted due to PPP peculiarities, making compliance challenging. It is inferred that strict legal enforcement procedures add to the complexity, requiring projects to navigate through various legalities to ensure ESG reporting adherence. Studies by Horry et al. (2022a, 2022b) highlight the absence of sufficient legal support from government as a barrier, suggesting a need for more proactive government involvement in ESG reporting. Chotia et al. (2023) add that the lack of government policies that clearly indicate supportive policies could hinder compliance and ESG reporting practices.

3.3.6 Insufficient government incentives.

This barrier refers to the lack of adequate government support or rewards that could encourage the adoption of ESG reporting within PPP projects. The absence of incentives can lead to reduced motivation for PPP projects to invest in ESG reporting, potentially hindering its implementation. It is identified as a significant barrier, mentioned in several documents reviewed in the study. Overcoming this barrier may involve advocating for policy changes that recognise and promote the value of ESG reporting in PPP projects. This barrier is supported by studies such as Ahmed et al. (2020) and Cortés et al. (2023), which highlight issues like insufficient policies and lack of incentive systems as challenges to ESG reporting. The absence of incentives can lead to reduced motivation for PPP projects to invest in ESG reporting, potentially hindering its implementation.

3.3.7 Cost involved in environmental, social and governance reporting.

The cost of ESG reporting is also identified as a significant barrier for PPP projects. This includes the cost of collecting ESG data, analysing it and presenting it to investors. The financial impact of ESG reporting means committing financial resources that can be used for other project activities, making the cost hard to justify. The financial burden of ESG reporting can impact the overall budget and financial planning of PPP projects. Despite the costs, ESG reporting is crucial for transparency and can drive long-term benefits and stakeholder trust. Revell and Blackburn’s (2007) study suggests that ESG reporting can be expensive to undertake, which aligns with the financial burden discussed. Cortés et al. (2023) in a recent study maintained that the lack of willingness and economic hurdles corroborate the challenges in allocating budget for ESG reporting. A study by Izquierdo et al. (2024) directly addresses the cost involved in ESG reporting, reinforcing the emphasis on the financial challenges faced by PPP projects in ESG reporting.

3.4 Critical drivers to environmental, social and governance reporting of public–private partnership projects

Considering the drivers to ESG reporting of PPP projects, the study considers what are causing the demand for ESG reporting of these projects. Figure 6 presents the Pareto distributional plot, which identifies six important drivers to ESG reporting of PPP projects. The vital few drivers to ESG reporting in PPP projects include regulatory disclosure demands (Drive1), improved project performance and expected long-term returns (Drive2), society and external stakeholder pressures (Drive3), desire to mitigate project risk (Drive4), economic benefits (Drive5) and altruistic values (Drive6).

3.4.1 Regulatory disclosure demands.

This driver refers to the legal and regulatory requirements that compel PPP projects to report ESG information. It is identified as one of the key motivators for ESG reporting, ensuring transparency and accountability in project operations. The demands from regulatory bodies can significantly influence the extent and quality of ESG reporting by PPP projects, making it a critical factor for consideration. This driver appears to be a significant factor in the literature, indicating its importance in the field of ESG reporting for PPP projects. The RII for this driver suggests that it has a considerable impact on the adoption of ESG reporting practices within PPP projects. Industry and regulatory standards compliance is identified a significant contributing factor to ESG reporting as evident in several studies. For instance, the study by Horry et al. (2022a, 2022b) emphasises the importance of adhering to industry standards and regulations in ESG reporting for PPP projects. Cortés et al. (2023) highlighted that significant pressure from stakeholders ensure transparency and accountability in ESG practices. Governmental influence and demands determines the practice of ESG reporting greatly. Gradillas et al. (2021) discuss the impact of government and regulatory pressures on the integration of ESG reporting within PPP projects. These findings collectively underscore the critical role of regulatory disclosure demands as a driver for ESG reporting in PPP projects.

3.4.2 Improved project performance and expected long-term returns.

This is identified as a key driver for ESG reporting in PPP projects. It suggests that ESG reporting can lead to better project performance and enhance the potential for long-term returns. This driver reflects the influence of stakeholders who are focused on the long-term sustainability and success of projects. The driver stresses the role of ESG reporting in overall PPP projects success and sustainability. Izquierdo et al. (2024) argue that the success of the project goes hand in hand with the project’s nature, thus ensuring strategic planning, stakeholder management and risk management. Boffo and Patalano (2020) discuss how ESG considerations drive project performance and can lead to improved long-term returns. This might be through better resource management, increased investor interest and enhanced corporate reputation. These studies collectively suggest that ESG reporting is not only beneficial for compliance and transparency but also plays a crucial role in driving project performance and securing long-term financial returns.

3.4.3 Society and external stakeholder pressures.

This driver discusses how societal and external stakeholders exert pressure on PPP projects to adopt ESG reporting. It highlights the growing demand for transparency and accountability in ESG practices within infrastructure investments. The pressures from these stakeholders are identified as key drivers for improving ESG integration in PPP projects. The driver suggests that PPP projects must strategically address these pressures to enhance their ESG outlook and ensure long-term sustainability. This reflects the importance of considering societal expectations and external stakeholder interests in the successful implementation of ESG reporting for PPP projects. A study by Francart et al. (2019) showed the importance of involving local actors, such as municipalities, in PPP projects. This engagement is crucial for addressing community-specific ESG concerns and fostering trust. Horry et al. (2022a, 2022b) emphasise that improved relationships with stakeholders result in effective ESG reporting. This can lead to enhanced cooperation and support for PPP projects. CPA-Australia (2023) discusses the impact of community pressure on PPP projects. It is shown that communities increasingly demand transparency and accountability in ESG practices, driving the need for robust reporting. Gradillas et al. (2021) also showed that focusing on the broader societal and stakeholder pressures compel PPP projects to adopt ESG reporting. These pressures reflect the growing societal expectations for sustainable and responsible project management.

3.4.4 Desire to mitigate project risk.

This driver emphasises the importance of ESG reporting in reducing potential risks associated with PPP projects. By addressing ESG concerns, projects can achieve greater stability and predictability in their outcomes. Effective risk management through ESG practices can enhance the confidence of investors and other stakeholders. It aligns with the goal of securing improved project performance and ensuring long-term returns. This driver is one of the key factors that encourage the adoption of ESG reporting within PPP projects. It reflects the proactive approach to safeguarding the project’s success by considering ESG factors. Risk mitigation is important in every business or project delivery. Using effective risk management strategy through ESG practices can enhance investor confidence and project stability. A study by Horry et al. (2022a, 2022b) indicated how green corporate image ensures project success. It highlights the role of ESG reporting in enriching the green corporate and public image, which is crucial for long-term project success and stakeholder trust. CPA-Australia (2023) discusses how ESG reporting can help in mitigating potential legal risks, ensuring compliance with regulations and avoiding legal repercussions. Boffo and Patalano (2020) describe the desire to mitigate risk as a proactive approach that drives the adoption of ESG reporting within PPP projects.

3.4.5 Economic benefits.

Financial and economic advantages can be gained from ESG reporting in PPP projects. Economic benefits of ESG reporting are shown to be a significant driver to ESG reporting, and this is why stakeholders get on board. This leads to cost savings and enhanced profitability. Demonstrating a commitment to ESG principles, PPP projects can demonstrate sustainable commitment, thereby attracting investors who are increasingly looking for sustainable and responsible investment opportunities. ESG reporting creates a competitive edge of one project company to the another. An ESG reporting PPP project will improve reputation and credibility. This driver highlights the importance of economic benefits as a key driver for ESG reporting in PPP projects, underlining its role in promoting sustainability and financial success. For instance, ESG reporting posits a mandatory assurance requirement. According to a study by Esty et al. (2020), economic advantage of the mandatory ESG reporting helps build trust among investors and stakeholders, which could lead to financial benefits of PPP projects. Another research conducted by Gradillas et al. (2021) emphasises the importance of ecosystem development in PPP projects. They suggest that a well-developed ecosystem can contribute to economic growth and attract more investment. In addition, Khan et al. (2018) found that there are economic gains from environmental benefits in PPP projects. Things like cost savings from efficient resource use and improved project sustainability can enhance the financial performance of the project.

3.4.6 Altruistic values.

Altruistic concerns actions taken for the benefit of others without expecting anything in return. These values can drive ESG reporting as organisations or project companies strive to contribute positively to the society and the environment. In PPP projects, altruistic values can lead to more transparent and comprehensive ESG reporting. Altruistic values are identified as one of the drivers for ESG reporting, encouraging ethical practices and social responsibility. Altruistic values in PPP projects are influenced by internal organisational characteristics, which include ethical practices and social responsibility initiatives. These characteristics drive transparent and comprehensive ESG reporting, as highlighted by Gradillas et al. (2021). Boffo and Patalano (2020) emphasise that altruistic values contribute to a positive brand image and reputation. By reporting on ESG factors, PPP projects can demonstrate their commitment to societal and environmental well-being. EY (2021) suggests that engaging with stakeholders to prioritise issues creates value for the project. Altruistic values drive this engagement, leading to better identification of ESG concerns and more effective reporting.

3.5 Interested parties of environmental, social and governance reporting of public–private partnership projects

The stakeholders involved in ESG reporting of PPP projects is a diverse group of people, each with a special interest in the project’s sustainability. All these interested parties directly or indirectly affect the project outcome. External stakeholders, such as regulators, NGOs, media, ecologists, unions, governmental supervisors, academia and the society and are directly involved with the project’s impact on the environment and community. These stakeholders are interested in the project outcome. The internal stakeholders include public sector project sponsor, suppliers, legal advisors, operator and construction contractor, PPP units, who are responsible for delivering the project. Lastly, connected stakeholders, which include employees, shareholders and independent reviewers, who are indirectly affected by the project (Table 2). Together, these groups form a complex network of interests that drive the need for transparent and robust ESG reporting.

3.5.1 External stakeholders.

External stakeholders of PPP projects are individuals or entities not directly involved in the execution of a project but have an interest in its outcome (Amadi et al., 2018; WBCSD, 2019; Wojewnik-Filipkowska and Węgrzyn, 2019). From the identified barriers, it can be said that unavailability of standardised ESG reporting standards, insufficient government incentives and absences of comparability ESG metrices are attributed to external stakeholders. Insufficient government incentives and the absence of standardised ESG reporting standards and frameworks make it difficult for external stakeholders to assess and compare ESG performance. Also, there is limited public awareness of ESG reporting, which can affect the pressure external stakeholders exert for transparency. It is evident that regulatory demands and societal pressures from the external stakeholders are significant factors that compel PPP projects to report their ESG. Regulatory disclosure demands from bodies like governments and financial institutions compel PPP projects to report ESG information.

3.5.2 Internal stakeholders.

Internal stakeholders are identified as actors within the project responsible for delivering the project. They are directly involved in the project’s operations and success, playing a pivotal role in ensuring the project’s objectives are met (Amadi et al., 2018; WBCSD, 2019; Wojewnik-Filipkowska and Węgrzyn, 2019). Based on the identified barriers and drivers, the significant barriers attributed to internal stakeholders for ESG reporting are competing project priorities, insufficient understanding, and lack of training investment for ESG actors. The focus on immediate project delivery demands can overshadow the long-term benefits of ESG reporting. Studies have shown that there is lack of awareness about the advantages of ESG reporting among internal stakeholders (Dolla and Laishram, 2020). Also, there is a need for investment in training programmes to enhance ESG expertise among internal stakeholders (Hendiani and Bagherpour, 2019). Drivers attributed to internal stakeholders’ pressure in reporting ESG are associated with regulatory disclosure demands, where legal and regulatory requirements compel transparent ESG reporting. Improved project performance on the promises that ESG reporting can lead to better project performance and enhance potential for long-term returns.

3.5.3 Connected stakeholders.

Connected stakeholders in PPP projects are those who are indirectly affected by the project but whose actions can influence the project progress. They are not directly involved in the project’s execution but are integral to its success (WBCSD, 2019; Wojewnik-Filipkowska and Węgrzyn, 2019). Examples include employees, shareholders and independent reviewers of the project. Inadequate ESG expertise, complexities in administrative requirements and availability of technology infrastructure are major drivers to ESG reporting of PPP projects identified for connected stakeholders. A lack of specialised knowledge in ESG reporting can hinder effective participation, whereas the absence of technology infrastructure complicates the reporting process. The lack of proper infrastructure can impede accurate ESG reporting.

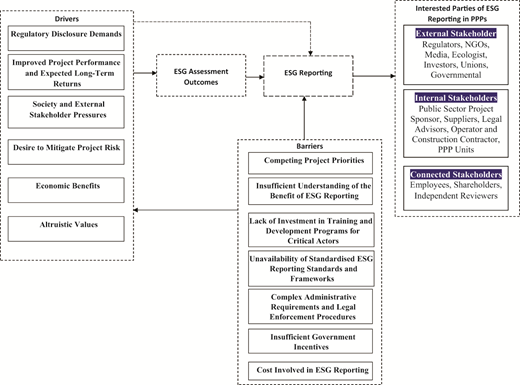

3.6 A conceptual framework of the barriers and drivers of environmental, social and governance reporting of public–private partnership projects’ stakeholders

The conceptual framework presented below (Figure 7) is an interplay between the barriers and drivers of ESG reporting in PPP projects. The framework identifies regulatory disclosure demands, project performance and societal pressures as primary drivers for ESG reporting. Regulatory bodies impose legal requirements that compel PPP projects to maintain transparency and accountability in their operations. Simultaneously, societal and external stakeholders exert pressure to ensure that PPP projects adhere to ESG standards, reflecting the growing societal expectations for sustainable and responsible project management. These influences drive the demand for ESG reporting, emphasising the need for PPP projects to strategically address these pressures to enhance their ESG outlook and ensure long-term sustainability.

Balancing priorities and knowledge gaps, the framework highlights barriers such as competing project priorities and insufficient understanding of ESG reporting benefits. Immediate project demands often overshadow the long-term benefits of ESG reporting, leading to critical sustainability initiatives being deprioritised. Moreover, a lack of awareness or knowledge about the advantages of ESG reporting can lead to its underutilisation, affecting project sustainability and stakeholder trust. Addressing these barriers requires strategic alignment of project goals with ESG objectives and enhancing education about ESG benefits to transform these barriers into drivers for better reporting practices.

Lastly, the framework presents some operational and economic considerations. The framework points out operational barriers like the unavailability of standardised ESG reporting standards and frameworks, complex administrative requirements and the cost involved in ESG reporting. These factors complicate the reporting process and can impact the overall budget and financial planning of PPP projects. Conversely, the quest to mitigate project risk and the potential economic benefits act as drivers, encouraging the adoption of ESG reporting by these projects. These drivers highlighted in this study are key motivators for stakeholders to engage in ESG reporting, which can provide a competitive edge and improve the project’s reputation and credibility.

Interested parties identified for PPP projects are realised to play significant role in the successful execution and delivery of PPP projects. Their active participation, collaboration and alignment with project goals contribute to effective project management and sustainable achievements. The factors identified shape how stakeholders engage with and prioritise ESG reporting, impacting project results. This conceptual framework underscores the complex nature of ESG reporting, where both barriers and drivers shape its adoption and implementation in PPP projects. It serves as a guide for identifying the critical factors that influence ESG reporting and provides a basis for developing strategies to enhance ESG integration in PPP initiatives.

4. Implications and proposition for future research

4.1 Implications for theory

Based on the study findings and discussion on ESG reporting for PPP projects, the following theoretical implications are made. The study highlights the need for standardised ESG reporting frameworks based on PPP project peculiarities; this will contribute to the development of a unified theory for ESG reporting in PPP projects. Also, the study places emphasis on the role of various stakeholders, suggesting an exposition of stakeholder theory in the context of ESG reporting, particularly within PPP projects. Furthermore, the identification of the barriers, drivers and interested parties to ESG reporting in this context could inform a theory of change that explains how and why ESG reporting practices evolve in PPP projects. Lastly, the study’s focus on the coordination mechanisms between public and private sectors could enhance theories related to collaborative governance and inter-organisational cooperation. These implications can also serve as a foundation for future research to build upon and refine the understanding of ESG reporting in PPP projects.

4.2 Implications for practice

Findings from this study suggest that actors of PPP projects should not only focus on the immediate project deliverables but also integrate ESG reporting into their core objectives for sustainability purposes. This will ensure that while the project meets its short-term goals, it also drives long-term sustainability targets. Interested parties should actively seek policy changes that incentivise ESG reporting. By advocating for policies that factor the importance of ESG reporting, PPP projects can enhance their commitment to sustainable practices. Incorporating ESG considerations into the decision-making process will lead to more informed and responsible project results. This approach can help overcome barriers such as competing project priorities and insufficient understanding of ESG benefits. Addressing the barrier of insufficient investment in training and development programmes for critical actors is essential. By investing in specialised training for critical actors, PPP projects can build the necessary expertise for effective ESG reporting. The lack of standardised ESG reporting standards is a significant barrier. PPP projects should work towards adopting or developing tailored frameworks that facilitate consistent and comparable ESG reporting. Lastly, understanding the cost involved in ESG reporting and conducting a thorough cost–benefit analysis can help justify the investment in ESG initiatives. Encouraging policy changes to recognise and promote the value of ESG reporting in PPP projects is critical, future studies may focus on how policy advocacy can compel ESG reporting.

5. Conclusion

This study unearths the barriers, drivers and key interested stakeholders of ESG reporting in PPP project. This study responds to research need for studies into the barriers, drivers and key stakeholders of ESG reporting of PPP projects. The study has meta-analysed and synthesised empirical studies and made this research contributions. This study realises the benefits of reporting ESG information to a diverse group of stakeholders, called interested parties of PPP project including regulatory bodies, investors and the public, to promote transparency and accountability. The study identified significant barriers to ESG reporting of PPP project including insufficient understanding of ESG benefits, lack of standardised reporting frameworks and the cost involved in ESG reporting. Also, key drivers for ESG reporting comprise of regulatory disclosure demands and improved project performance. Addressing these barriers and leveraging the drivers is crucial for the successful integration of ESG reporting within PPP projects for enhanced sustainability performance and long-term project success.

This paper is part of a PhD research project being conducted at the School of Engineering, Design and Built Environment at Western Sydney University, Australia. The authors acknowledge Western Sydney University for full funding of research.