Acknowledging the complexity of property investment decision-making under heightened uncertainty, this study examined the dynamic relationship between market fundamentals, investors’ behavioural biases, and the moderating effects of uncertainty.

This study explored these dynamics through the perspectives of 412 commercial property investors in Australia. Using partial least squares structural equation modelling, a PROCESS macro model was developed to represent the interaction between fundamentals, behaviour, uncertainty and investment allocation decisions.

The effects of fundamentals and certain behavioural biases on investment decisions diverge in response to uncertainty. Fundamentals exhibit an inverse effect, while biases such as anchoring, overconfidence and intuition positively impact investment intention. These relationships are more pronounced as uncertainty rises, indicating that decision-making norms are dynamically responsive to external market conditions.

By representing market fundamentals, behaviour, and uncertainty in one system that explores decision-making, this study provides insights into how investors navigate different economic climates. Leveraging these insights could facilitate adaptive investment strategies that integrate fundamentals and the nuance of human behaviour.

The growing literature on adaptive markets recognises the pervasive role of emotions and market imperfections, both of which impact decision-making. Uncertainty introduces an additional layer complexity which could alter existing relationships and introduce new norms under which decisions are made, and outcomes are determined. This study modelled these complex relationships in one system to explore how property investors approach allocation decisions amid uncertainty.

1. Introduction

Recent developments in the field of behavioural economics recognise the role of the human element in decision-making, even for complex investment decisions (Gallimore and Gray, 2002; Kumar and Goyal, 2015; Waweru et al., 2014). While the prevalence of behavioural biases is generally considered suboptimal in the finance sector, property investors are often compelled to augment incomplete information with their intuition, rules of thumb and experience (Jackson and Orr, 2019; Pandey and Jessica, 2019). These relationships persist under normal conditions, but uncertainty introduces additional complexities that exacerbate investors’ reliance on behavioural biases (Ahiadu et al., 2024a; Jackson and Orr, 2019). In response to declining performance and diminishing confidence in market fundamentals, property investors increasingly rely on their cognitive biases to make irreversible decisions (Jackson and Orr, 2019; Maitland and Sammartino, 2015). These two dimensions – market fundamentals and behavioural biases – often intersect, creating complex decision-making processes that are further complicated by external uncertainties (Sharmila et al., 2024).

Much of the existing research has examined these factors in isolation, leaving notable gaps in the interaction between fundamentals and investor behaviour. Traditional models often assume investor rationality and efficient markets, but burgeoning evidence suggests that real-world decisions deviate significantly from these assumptions, especially in volatile environments. Recent market disruptions such as COVID-19, geopolitical tensions, and the Russia-Ukraine war have raised global uncertainty to historically high levels, as shown by the Economic Policy Uncertainty (EPU) index (Ahir et al., 2022; Bloom et al., 2022). These novel disruptions heavily impacted prices, transaction volumes, vacancy rates and returns (Ahiadu et al., 2024b; Allan et al., 2021; Gholipour et al., 2021; Milcheva, 2022). Although these findings provide evidence of how external factors impact performance, there is little indication of how investors navigate heightened uncertainty. The consensus reflects increased caution among investors and reduced willingness to invest, but the interaction of these variables for the different investor profiles remains underexplored.

The Adaptive Market Hypothesis (AMH) underscores the growing acknowledgement that investors are imperfect actors making decisions based on imperfect information in imperfect markets (Lo, 2004). Subsequent research has identified which biases impact decision-making and how best to suppress their effect, but this conceptualisation of fundamental human behaviour as a limitation remains problematic (Kumar and Goyal, 2016; Pandey and Jessica, 2019; Tan et al., 2017; Waweru et al., 2014). Despite complex models and seemingly limitless access to information, behavioural biases and cognitive shortcuts remain pertinent to investment decisions in normal and uncertain conditions (Gallimore and Gray, 2002; Jackson and Orr, 2019; Kumar and Goyal, 2016; Pandey and Jessica, 2019). Although risk is a ubiquitous consideration for property investors due to market imperfections and complexity, Knightian uncertainty is distinct because it represents a situation where the probabilities of future outcomes are unknown and unquantifiable (Knight, 1921).

To address these gaps, this study hypothesised investment allocation decisions as a complex system involving market fundamentals and behaviour, moderated by uncertainty and investors’ profiles. By exploring the dynamic relationship between market fundamentals and behavioural biases while introducing uncertainty as an external moderator, these findings provide a more comprehensive understanding of how investors respond to varying economic climates to make allocation decisions. Additionally, unexpected market disruptions and recent monetary policy decisions by the Reserve Bank of Australia (RBA) created the perfect testing grounds for the hypothesised relationships amid rising uncertainty levels. Practically, the modelled system of investment decisions provides actionable insights for investors, policymakers, and industry stakeholders to enhance decision-making frameworks and adapt to challenges posed by economic volatility.

2. Literature review

2.1 Property market inefficiencies, imperfect investors and decision-making complexities

Despite prevailing and longstanding theories of perfect markets and rational investors, the field of behavioural economics continues to present substantiated effects of the human element in all decision-making (Gallimore and Gray, 2002; Roberts and Henneberry, 2007). The crux of these findings suggests that the property market diverges from assumptions of markets characterised by participants who are only motivated to maximise returns (Gallimore et al., 2000; Kumar and Goyal, 2016; Waweru et al., 2014). Particularly in the absence of perfect access to information, investors may augment their decision-making with experience, specialised knowledge or intuition (Maitland and Sammartino, 2015; Newell, 2016; Sah et al., 2010). High transaction costs, limited information transparency, and illiquidity all complicate decision-making and require nuance beyond the numbers as property investors navigate different economic climates (Baum, 2009). Roberts and Henneberry (2007) perfectly summarised property investment decision-making as interactions involving imperfect investors making decisions in imperfect markets using imperfect information.

Although “imperfect” has negative connotations, it remains an apt description of human investors making decisions impacted by a litany of factors. Due to the well-documented inefficiencies of the property market, sentiment-driven decision-making is prevalent and, in some cases, ideal (Gallimore and Gray, 2002). Several behavioural tendencies impact decisions because investors are humans with emotions, who are prone to overconfidence, herd mentality, loss aversion, and recency bias (Zahera and Bansal, 2018). Although inexhaustive, this list highlights the human element in all decisions, even complicated ones such as capital allocation. Kahneman and Tversky’s (1979) seminal work identified several dimensions of decision-making under risk, including heuristics, cognitive biases, and prospect theory. Lo’s (2004) theories on AMH also suggest that investors’ bounded rationality results in decisions best described as evolving, rather than rational.

Decision-making for property investors is thus more of an evolutionary process and less of a statistical sequence (Lo, 2004). Given the wealth of options and the detrimental cost of suboptimal decisions, augmenting available information with behaviour and intuition is only human. Essentially, these complexities reduce decisions to a trade-off between economic considerations and risk, real or perceived (Nguyen et al., 2019; Nur Ainia and Lutfi, 2019; Pandey and Jessica, 2019). The state of the economy is an ever-present consideration as investors strive to navigate different climates, perceptions of which form their investment intention and ultimately define their allocation preferences (Jackson and Orr, 2019; Pandey and Jessica, 2019). Under different conditions, decisions may differ substantially from established norms – investors may anchor their expectations to previous performance, they may grow overconfident and ignore fundamentals in favour of an overperforming asset, or display gamblers’ fallacy by backing their intuition on a trend reversal (Kumar and Goyal, 2016; Pandey and Jessica, 2019; Zahera and Bansal, 2018).

2.2 Integrating market fundamentals and behavioural biases for property investment decisions

Given the limitations of purely rational or irrational approaches to decision-making, investment decisions are conceptualised as a function of both. Neither can fully explain investment decisions, but the integration of both provides a more comprehensive lens to assess the process (Clayton et al., 2009; Lowies et al., 2015; Wang and Hui, 2017). Waweru et al. (2014) reported property prices and location as critical considerations, further noting that cognitive biases such as anchoring and representativeness also influence decision-making. Similarly, Lowies et al. (2015) noted that property investors augment market fundamentals with market sentiment and personal judgment to compensate for information asymmetry. Extending these arguments to the broader population of investors suggests that market fundamentals offer objective metrics for assessing alternative options, while behavioural biases introduce a subjective of nuance for investors to navigate the complex investment landscape.

Market fundamentals remain at the core of rational property investment decisions because they determine profitability (Baum, 2009). Factors such as interest rates, prices, rental yields, and demand-supply dynamics are pivotal for estimating asset performance and identifying opportunities. Based on different investment strategies, some investors may prioritise strong location attributes and cashflow stability, and others may adopt more opportunistic or value-add strategies (Baum, 2009; Farragher and Savage, 2008; Roberts and Henneberry, 2007; Sharmila et al., 2024). However, relying solely on fundamentals often overlooks the human element, where perception, emotion, and cognitive limitations influence decision-making. In volatile markets, the predictive power of fundamentals may be undermined, creating opportunities for biases to exert greater influence (Jackson and Orr, 2019; Lowies et al., 2015). Even investors with access to the same information may reach wholly different decisions because of varying perceptions and cognitive biases. An experienced investor may reach decisions faster by leveraging a superior understanding of market dynamics (Sah et al., 2010), a cautious investor may delay decisions due to an inherent fear of losses (Maitland and Sammartino, 2015), and other investors may gravitate towards the wisdom of the crowd (Kumar and Goyal, 2016).

2.3 Property investment decisions, allocation, and intention under conditions of heightened uncertainty

Uncertainty in the aftermath of unexpected market disruptions such as COVID-19 and recent cash rate bikes by the RBA noticeably altered investment allocation decisions. Traditional frameworks that prioritise stable cash flows, predictable returns, and risk mitigation are often challenged under volatile conditions (Ahiadu et al., 2024a; Jackson and Orr, 2019). Investors may become excessively cautious, avoid high-risk opportunities, or adopt speculative strategies in search of outsized gains (Bird and Yeung, 2012; Jackson and Orr, 2019). This dichotomy reflects the dual pressures of preserving capital while attempting to capitalise on market dislocations, a decision that investors perceive differently.

The additional complexity introduced by high uncertainty levels is understandable, particularly because several performance indicators are impacted by market disruptions. A wide range of effects have been reported following significant market disruptions and the subsequent uncertainty. Uncertainty negatively impacts commercial property prices and returns (Ahiadu et al., 2024b; Gholipour et al., 2021), while vacancy rates rise in response to cautious allocation decisions (Gholipour et al., 2022). In the first six months of COVID-related uncertainty, Allan et al. (2021) reported declines of up to 32% in transaction volumes across the Asia-Pacific region. Similarly, rents also display an inverse relationship with uncertainty that persists for up to three years following the first-moment shock of a market disruption (Ahiadu et al., 2024b).

These significant impacts are transmitted to investment allocation decisions, as investors balance increased risk with potential returns (Allan et al., 2021; Jackson and Orr, 2019). Investment intentions are equally shaped by uncertainty, reflecting both rational and emotional responses to evolving market conditions. In times of heightened uncertainty, investors may delay or reduce commitments to new projects, opting instead to wait for clearer signals (Ahiadu et al., 2024a; Jackson and Orr, 2019; Pandey and Jessica, 2019). This behaviour is often influenced by psychological factors, such as fear of loss, which discourage risk-taking, or optimism bias, which fosters overconfidence in an eventual market recovery. Such responses underscore the importance of understanding the interplay between market conditions and investor psychology.

The extant literature indicates that fundamentals and behaviour interact in a complex system for investment decisions, a relationship that is impacted by externalities such as uncertainty. However, this dynamic relationship remains largely unexplored despite the growing acceptance that investment decision-making is not a static process. Understanding the moderating role of uncertainty could offer valuable insights into how market participants react to external pressures, providing a better framework to assess and predict investment intentions and outcomes. The prominence of uncertainty, as shown by trends in the EPU index, also underscores the need for more adaptive strategies that integrate rational analysis, behavioural insights, and market conditions. By examining these relationships, this study emphasised the evolving dynamics of property investment decision-making in a volatile environment.

3. Data and methodology

3.1 Data description

Motivated by growing concerns over rising uncertainty in response to a series of market disruptions to the global economy (Ahir et al., 2022; Bloom et al., 2022), this study explored the relationship between market fundamentals and behavioural biases for decision-making from the perspective of commercial property investors in Australia. This sample provided an interesting testing ground for the hypothesised dynamic relationship because, in addition to global uncertainty, uncertainty in the Australian property space was further heightened by the RBA’s aggressive monetary policy decisions to address inflation (RBA, 2023).

Due to the lack of a publicly accessible database of investors, the online questionnaire survey was designed in Qualtrics and disseminated to prospective respondents through private firms and public institutes that retain a database of client emails. According to Groves et al. (2004), this is an effective approach to identifying an obscure target population. The choice of an online survey was also a cost-effective approach for gathering timely perspectives on property investors’ decision-making considerations in uncertain conditions (Couper, 2000).

Despite limited estimates on the total number of private commercial property investors in Australia, the largest single database accessed for this study contained approximately 12,000 subscribers (residential and commercial). The questionnaire was live for the last two months of 2023, a period specifically targeted to coincide with peaking inflation levels and heightened uncertainty as investors hedged all future decisions on unpredictable rate cuts (RBA, 2023). Four hundred and twelve of the 2,012 responses received were deemed valid and complete, providing information on investors’ demographic profiles, risk attitudes, perceived uncertainty levels, and factors underpinning their decision-making on a 5-point Likert scale. The role of market fundamentals was proxied by how much these factors influence investment decisions: demand, prices, returns and vacancy rates. Based on the existing literature on the topic, anchoring, herding, intuition, loss aversion, and overconfidence represented investor behaviour in subsequent analyses.

In consideration of the level of detail required in the survey, 10 respondents were subsequently awarded gift cards in a random prize draw. These token financial incentives were intended to enhance participation and encourage completion, while still ensuring no declines in response quality (Hsu et al., 2017). The profile of respondents is presented in Table 1.

Profile of commercial property investors (questionnaire survey)

| Variable | Frequency (n = 412) | Percentage (%) | |

|---|---|---|---|

| Age | 18–24 | 16 | 3.9% |

| 25–34 | 215 | 52.4% | |

| 35–44 | 151 | 36.8% | |

| 45–54 | 21 | 5.1% | |

| 55–64 | 6 | 1.5% | |

| Above 65 | 1 | 0.2% | |

| Gender | Male | 253 | 61.9% |

| Female | 146 | 35.7% | |

| Non-binary | 3 | 0.7% | |

| Undisclosed | 7 | 1.7% | |

| Education | No formal qualifications | 5 | 1.2% |

| High school/diploma | 103 | 25.2% | |

| Bachelor’s | 178 | 43.6% | |

| Master’s/postgraduate | 122 | 29.9% | |

| Annual salary | $1–$50,000 | 3 | 0.7% |

| $50,001–$100,000 | 73 | 17.7% | |

| $100,001–$200,000 | 84 | 20.4% | |

| $200,001–$350,000 | 110 | 26.7% | |

| $350,001–$500,00 | 112 | 27.2% | |

| Above $500,000 | 25 | 6.1% | |

| Undisclosed | 5 | 1.2% | |

| Experience | 0–5 years | 144 | 35.0% |

| 6–10 years | 214 | 51.9% | |

| 11–15 years | 37 | 9.0% | |

| 16–20 years | 8 | 1.9% | |

| Above 20 years | 5 | 1.2% | |

| Undisclosed | 4 | 1.0% | |

| Sectors* | Office | 157 | 34.80% |

| Retail | 172 | 38.10% | |

| Industrial | 122 | 27.10% | |

| States* | NSW | 81 | 15.90% |

| QLD | 110 | 21.70% | |

| SA | 54 | 10.60% | |

| VIC | 73 | 14.40% | |

| WA | 66 | 13.00% | |

| TAS | 46 | 9.10% | |

| ACT | 47 | 9.30% | |

| NT | 31 | 6.10% | |

Note(s): *Denotes multiple-response questions. Respondents were allowed to choose multiple options, so the total number of responses was more than 412 for those variables

Source(s): Table created by authors

3.2 Methodology

A quantitative exploratory research design was adopted to model the hypothesised relationship between market fundamentals, behavioural biases, uncertainty, and investment decisions. Due to the complexity of these relationships and the restrictive assumption that variables can be measured without error (Sharma, 1996), first-generation multivariate techniques such as regressions were deemed inadequate. Hair et al. (2021) further noted that these limitations impact the quality of results in dynamic systems because complex causal chains cannot be observed simultaneously. Especially in social sciences where most research attempts to draw meaningful insights based on perceptions, attitudes, and behaviour, these limitations reduce the applicability of first-generation techniques (Ghasemy et al., 2020; Sharma, 1996).

To overcome these limitations and model the conceptual relationships, this study adopted the Partial Least Squares-Structural Equation Modelling (PLS-SEM) approach. According to Hair et al. (2010), this statistical method is ideal for developing a theory or exploring emerging relationships in a complex system. Latent constructs were defined for market fundamentals, behavioural biases, uncertainty, and investment decisions. Subsequently, the linear and moderating relationships were modelled using PROCESS macros in the SmartPLS4 software. This approach extends simple regression analysis to path analysis to test conceptual relationships in a multivariate system (Hair et al., 2010; Sharma, 1996). Additionally, by making no distinction between endogenous and exogenous variables, PROCESS macros account for potential measurement errors and facilitate the construction of unobservable indicators through proxies and constructs (Chen et al., 2022; Hayes, 2013).

In the context of this study, the property investment decision is the predicted construct, while behavioural traits and the perceived importance of property fundamentals are the predictor constructs, a relationship hypothesised to be moderated by uncertainty levels. The adopted approach is a staple in previous research exploring the role of behaviour and external factors of investment decisions, a burgeoning research area as the adaptive market hypothesis proposed by Lo (2004) becomes more prominent amid heightened uncertainty (Kumar and Goyal, 2016; Pandey and Jessica, 2019).

3.2.1 Conceptual model of property investment decisions amid uncertainties

Property investment decisions are generally complex processes involving market fundamentals, the investor’s behaviour and market conditions (Gallimore and Gray, 2002; Hargitay and Yu, 1993; Lowies et al., 2015). While market conditions include indicators such as information availability and transparency, uncertainty has also emerged as a prominent factor in decision-making (Ahiadu et al., 2024a; Jackson and Orr, 2019). These emerging relationships further complicate investment decisions and impact performance (Ahiadu et al., 2024b; Allan et al., 2021; Gholipour et al., 2022). Recent inflationary pressures have only exacerbated the effects of uncertainty (Bloom et al., 2022), necessitating a rethink of how investment decisions are made under volatile conditions.

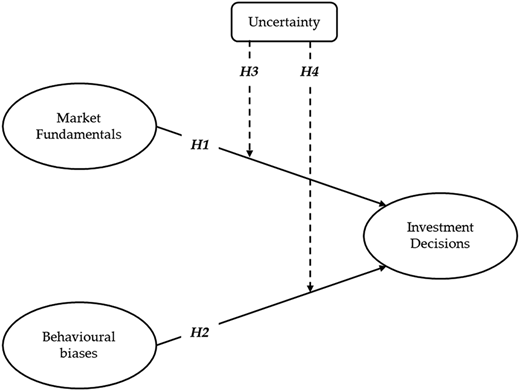

In this study, the relationship between market fundamentals and investors was conceptualised as a dynamic system moderated by economic, monetary policy, and political uncertainty. The following conceptual model, presented in Figure 1, shows the hypothesised effects of market fundamentals and behaviour on investment decisions and the moderating role of uncertainty as perceived by commercial property investors.

Market fundamentals have a negative and significant effect on investment intention and allocation decisions.

Behavioural biases have a positive and significant effect on investment intention and allocation decisions.

Uncertainty moderates the effect of market fundamentals on investment intention and allocation decisions.

Uncertainty moderates the effect of behavioural biases on investment intention and allocation decisions.

Conceptual model (property investment decision-making amid uncertainty). Source: Figure created by authors

Conceptual model (property investment decision-making amid uncertainty). Source: Figure created by authors

3.2.2 PROCESS macro model specification

The burgeoning field of behavioural economics has made it increasingly apparent that normative models of efficient markets are insufficient to explain decision-making processes and considerations (Gallimore et al., 2000; Lowies et al., 2015). As Jackson and Orr (2019) described it, investors are more likely to leverage their own perceptions and preferences when they are uncertain about future market movements. Essentially, investment decisions are made considering more than just the fundamentals, particularly under conditions of uncertainty.

To explore this complex system, this study modelled the hypothesised relationship between market fundamentals, behavioural biases, uncertainty, and investment decisions through PLS-SEM, using PROCESS macros. These constructs are not directly observable, so latent variables representing them were adopted based on the extant literature. For market fundamentals, performance indicators which are notably responsive to short-term volatility were preferred (Ahiadu et al., 2024b; Cypher et al., 2018; Gholipour et al., 2022). Prices, returns, demand, and vacancy rates were adopted as latent variables for market fundamentals. The existing literature on behavioural biases has grown extensive, and this study focused on some biases that have emerged as significant factors for investment decisions – anchoring, herding, intuition, loss aversion, and overconfidence.

Owing to recent global market disruptions and local inflationary pressures impacting property investors, the statistical model defined a variable for uncertainty, represented by perceived levels of economic, monetary policy and political uncertainty. These aspects of uncertainty are ideal latent variables because they reflect the focus of other popular indicators such as the EPU index, which tracks the prevalence of uncertainty in news outlets (Ahir et al., 2022). Lastly, investment decisions were proxied by investors’ allocation, intentions, and willingness to recommend commercial property in the current economic climate based on extensive reviews of the literature exploring the influence of behaviour on investment decisions (Kumar and Goyal, 2015; Pandey and Jessica, 2019; Zahera and Bansal, 2018). Table 2 details how all the adopted constructs and variables were defined in this study.

PROCESS macro modelling (constructs and items)

| Constructs | Items (description) |

|---|---|

| Market fundamentals | Demand (perceived investor interest in property) |

| Prices (growth trends in property prices) | |

| Returns (rental income and capital growth) | |

| Vacancy rates (rate of unoccupied properties) | |

| Behavioural biases | Anchoring (use of previous prices as a point of reference) |

| Herding (other investors’ actions impact mine) | |

| Intuition (gut feeling about future economic movements) | |

| Loss aversion (increased risk aversion after a prior loss) | |

| Overconfidence (my skills can outperform the market average) | |

| Uncertainty | Economic (lack of predictability in economic indicators) |

| Monetary policy (lack of predictability in interest rates) | |

| Political (lack of predictability about government policy) | |

| Investment decision | Allocation (intention to allocate funds into property investment) |

| Intention (desirability to invest in property) | |

| Recommend (likely to recommend others to invest in property) |

Source(s): Table created by authors

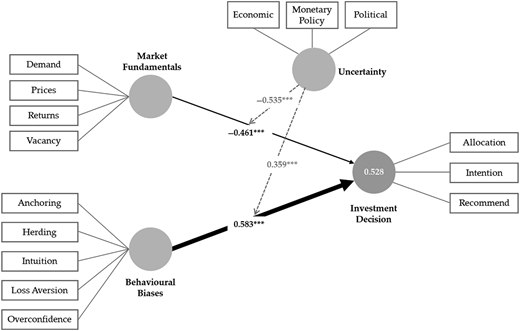

Data for these constructs were collected through close-ended questions measured on a 5-point Likert scale, encompassing the perceived importance of market fundamentals, how prominent behavioural biases are to decisions, the perceived levels of uncertainty, and investment decisions. As shown in Figure 2, these dimensions were conceptualised to influence the decision-making of commercial property investors under normal and uncertain economic conditions.

PROCESS macro model (property investment decision-making amid uncertainty). Note: This model represents the PROCESS macro model developed in SmartPLS4 to explore the dynamic relationship between market fundamentals and behavioural biases, moderated by uncertainty. The direction of these effects is shown with solid arrows, while dashed arrows show the moderating effects of uncertainty. All path coefficients are presented on the respective arrows, significant at 1% (***). The explanatory power of the model is highlighted in the “investment decision” construct (R2 = 0.528). Source: Figure created by authors

PROCESS macro model (property investment decision-making amid uncertainty). Note: This model represents the PROCESS macro model developed in SmartPLS4 to explore the dynamic relationship between market fundamentals and behavioural biases, moderated by uncertainty. The direction of these effects is shown with solid arrows, while dashed arrows show the moderating effects of uncertainty. All path coefficients are presented on the respective arrows, significant at 1% (***). The explanatory power of the model is highlighted in the “investment decision” construct (R2 = 0.528). Source: Figure created by authors

3.2.3 PROCESS macro model: quality criteria and reliability validity tests

Several tests were conducted to verify the model’s quality, as well as the reliability and validity of the implied relationships and effects. Hair et al. (2013) established the ideal sample size of PLS-SEM, based on the number of indicators – a minimum of 10 respondents for each item. Fifteen latent variables were adopted to represent the constructs in this study, setting a minimum acceptable sample size of 150 for the statistical model. Thus, the final sample size of 412 was deemed adequate for the analyses. The model’s coefficient of determination (R2) returned a value of 0.528, which indicated that the defined relationships explain approximately 52.8% of the variability in investment intention and allocation decisions amid uncertainty (Hair et al., 2013). The constructs are also reliable, based on Cronbach’s alpha and a minimum threshold of 0.70, as detailed in Table 3 (Sharma, 1996).

Construct reliability and validity

| Constructs | Cronbach’s α | Number of items |

|---|---|---|

| Market fundamentals | 0.883 | 4 |

| Behavioural biases | 0.871 | 5 |

| Investment decision | 0.767 | 3 |

| Uncertainty | 0.910 | 3 |

Source(s): Table created by authors

Goodness of fit indexes were also assessed based on established thresholds and decision rules (Hair et al., 2013; Hayes, 2013; Sharma, 1996). These model fit tests included absolute, incremental, and parsimonious indexes, as detailed in Table 4. The estimated model was also bootstrapped to establish the statistical significance of all the path coefficients (Hayes, 2013).

PROCESS macro model fit tests

| Category | Indexes | Value | Threshold level |

|---|---|---|---|

| Absolute fit | Root Mean Square Error of Approximation (RMSEA) | 0.048 | <0.06 |

| Minimum Discrepancy for Confirmatory Factor Analysis/Degree of Freedom (CMIN/DF) | 1.783 | <3.0 | |

| Goodness of Fit (GFI) | 0.920 | >0.90 | |

| Incremental fit | Comparative Fit Index (CFI) | 0.955 | >0.90 |

| Tucker–Lewis index (TLI) | 0.919 | >0.90 | |

| Normed Fit Index (NFI) | 0.944 | >0.90 | |

| Parsimonious fit | Parsimony Comparative Fit Index (PCFI) | 0.810 | >0.50 |

| Parsimonious Normed Fit Index (PNFI) | 0.847 | >0.50 |

Note(s): These tests represent the statistical tests conducted to confirm model fit for the hypothesised relationships. The values of all indexes were considered against the established threshold values to ensure model fit

Source(s): Table created by authors

4. Results and discussion

4.1 Heightened uncertainty levels and implications for property investment decisions

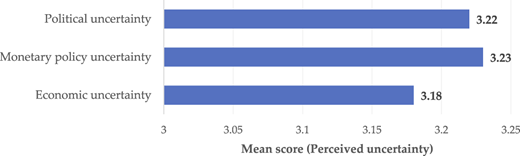

Hargitay and Yu (1993) asserted that all investment decisions are made under some level of uncertainty because access to information is always imperfect, which exposes property performance to exogenous market conditions (Jackson and Orr, 2019; Ling et al., 2010). Recent market disruptions, notably COVID-19, inflationary pressures, and the RBA’s monetary have significantly amplified uncertainty levels over the past few years (Ahir et al., 2022; Bloom et al., 2022; RBA, 2023). In the immediate aftermath of these disruptions, the extant literature reported declines in transaction volumes, capital allocation, prices, and overall performance (Ahiadu et al., 2024b; Allan et al., 2021; Gholipour et al., 2021; Milcheva, 2022). Due to this extended period of underperformance, investors’ risk perceptions shifted as they were compelled to reassess established norms, adopting cautious strategies or adapting to leverage emerging opportunities (Ahiadu et al., 2024a; Jackson and Orr, 2019). This study explored perceived uncertainty levels among commercial property investors to highlight the conditions under which decisions were made, and the underlying reasons for some reported shifts in perspective. As shown in Figure 3, investors’ perceived uncertainty was above normal (on a scale of 1–5), considering the economy, monetary policy and political climate.

Perceived uncertainty levels among property investors. Source: Figure created by authors

Perceived uncertainty levels among property investors. Source: Figure created by authors

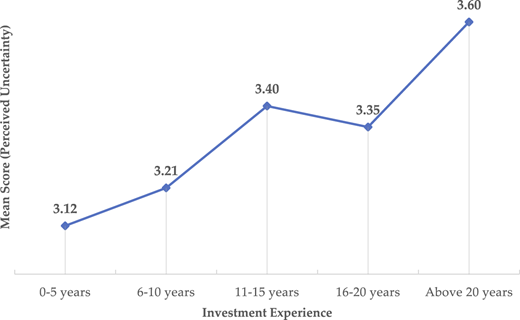

Subsequent analyses explored how heightened uncertainty influences investors’ perceptions and impacts decision-making. Although the overall response of investors to rising uncertainty is negative (Jackson and Orr, 2019), Ahiadu et al. (2024a) established significant differences based on risk profiles, experience and wealth. Established theories on adaptive markets suggest that investors are constantly evolving their decision-making considerations based on previous experiences (Lo, 2004).

Figure 4 drew on these relationships to link investment experience to perceived uncertainty levels, which was hypothesised to impact investment intention and allocation decisions. Despite persistent arguments in favour of wholly rational investors, experience remains a significant differentiator due to the property market’s inefficiencies (Maitland and Sammartino, 2015; Newell, 2016; Sah et al., 2010). Experienced investors demonstrate a nuanced understanding of market conditions, often leveraging their knowledge of historical trends and market movements to inform decisions. As such, their perceptions of risk are more acute and aligned with economic indicators, which explains why perceived uncertainty is notably higher with more experience. Practically, these varied perspectives emphasise how investors view the market through different lenses shaped by their profile, attitudes to risk, and perceptions. With a better understanding of these decision-making dimensions, investors could limit their overreactions to short-term volatility and manage their reliance on certain cognitive biases (Ahiadu et al., 2024a; Jackson and Orr, 2019). Similar lessons could improve the decisions of more experienced investors who may become overly reliant on proven rules of thumb (Maitland and Sammartino, 2015), which can occasionally lead to misjudgment in rapidly changing environments.

Variations in perceived uncertainty based on experience. Source: Figure created by authors

Variations in perceived uncertainty based on experience. Source: Figure created by authors

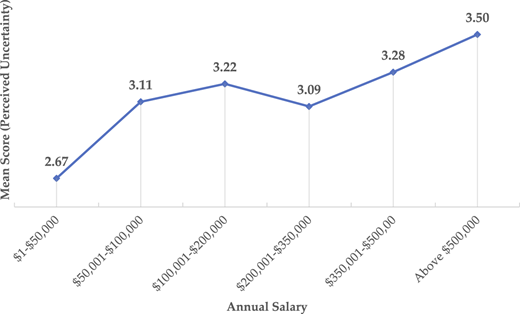

For wealthier investors, the scale of their portfolios introduces heightened sensitivity to economic movements during periods of uncertainty. The amount of capital required and the irreversibility of investment decisions underscore some of the property market’s inefficiencies, which encourage investors to rely on cognitive biases (Gallimore and Gray, 2002; Miles, 2009; Sah et al., 2010). Larger portfolio sizes require greater capital commitments, making these investors more vulnerable to perceived risks in volatile markets. Empirical results suggest that wealthier investors are more measured in their decision-making amid uncertainties, as shown in Figure 5. The relationship between wealth and risk perception may also be influenced by the higher stakes involved in wealthier investors’ decisions. Significant financial exposure amplifies the psychological pressure to preserve capital, considerations that could explain reduced capital allocations and investors’ wait-and-see attitudes in these conditions (Ahiadu et al., 2024a). By introducing unique challenges that amplify risk sensitivity, investors’ wealth emerges as a significant factor to account for in attempts to explain decision-making considerations following unexpected market disruptions.

Variations in perceived uncertainty based on wealth. Source: Figure created by authors

Variations in perceived uncertainty based on wealth. Source: Figure created by authors

Access to finance is another foundational consideration in property investment, often serving as the initial screen through which opportunities are assessed (Baum, 2009; Hargitay and Yu, 1993). During periods of heightened uncertainty, lenders tend to tighten credit conditions, thereby limiting the ability of investors to act, regardless of their appetite for risk or strategic preferences. This dynamic introduces a critical behavioural dimension: while some equity investors may remain optimistic or even opportunistic during uncertain times, their decisions are often curtailed by the more conservative stance of lenders. However, wealthier investors may experience this tension differently. With greater access to capital or better financing terms, they may be less constrained by shifting lending conditions and more able to deploy capital flexibly (Ahiadu et al., 2024a). As such, investor behaviour in response to uncertainty is not only shaped by individual risk tolerance or strategic outlook but also by structural factors like financing access, which vary significantly for different investors.

4.2 The relationship between market fundamentals and behaviour for property investment decisions

Property investment decisions are influenced by a complex interplay of rational analysis and behavioural tendencies (Clayton et al., 2009; Lowies et al., 2015; Sharmila et al., 2024; Wang and Hui, 2017). In response to volatile conditions after significant market disruptions, Jackson and Orr (2019) evinced that this relationship evolves as confidence in the fundamentals declines and cognitive biases become more prominent. Similarly, Ahiadu and Abidoye (2024) reported significant effects of rising uncertainty on performance indicators, transaction volumes, risk perceptions, and willingness to invest. To test these emerging norms under conditions of uncertainty, Table 5 details the hypotheses testing results from the conceptual model designed for this study. In response to rising prices, vacancies, and demand, the negative path coefficients show that investors become less willing to invest in commercial property.

Hypotheses testing results

| Hypothesis | Relationship | Path coefficient | Std. dev. | T-stat. | Decision |

|---|---|---|---|---|---|

| H1 | Fundamentals → Decision | −0.461*** | 0.072 | −6.403 | Accepted |

| H2 | Behaviour → Decision | 0.583*** | 0.088 | 8.898 | Accepted |

| H3 | Uncertainty × Fundamentals → Decision | −0.535*** | 0.059 | −11.203 | Accepted |

| H4 | Uncertainty × Behaviour → Decision | 0.359*** | 0.052 | 10.75 | Accepted |

Note(s): This table presents the test results of the hypothesised dynamic relationship between market fundamentals, behavioural biases and uncertainty. The arrow (→) in the ‘relationship’ column highlights the direction of effect. Hypotheses 3 and 4 denote the moderating effects of uncertainty. *** represents p-values at 1% significance, which justified the decision to accept the hypotheses

Source(s): Table created by authors

Although market fundamentals underpin most investment decisions (Baum, 2009), recent literature has highlighted how uncertainty can reduce performance through several transmission channels (Allan et al., 2021; Gholipour et al., 2021; Milcheva, 2022). The inverse relationship between fundamentals and investment allocation decisions were prominent topics in the aftermath of the COVID-19 pandemic. Allan et al. (2021) reported significant declines in transaction volumes, Gholipour (2019) linked uncertainty to declining economic activities, and Ahiadu et al. (2024b) indicated persistent effects on rents and capital values. Theoretical perspectives on this phenomenon align with the role of fundamentals as proxies for market stability (Baum, 2009; Hargitay and Yu, 1993). When these indicators reflect volatility, investors perceive higher potential for loss, prompting reduced capital allocation (Jackson and Orr, 2019).

In contrast, the relationship between some behavioural biases and investment activity is positive during uncertain periods. Despite the overall cautious attitudes of investors amid conditions of heightened uncertainty, certain profiles adopt more aggressive strategies to capitalise on underpriced assets and declining demand (Ahiadu et al., 2024a; Jackson and Orr, 2019; Zhang et al., 2022). Overconfident investors, in particular, may back themselves to outperform the market even amid declining performance indicators and increased risk (Kumar and Goyal, 2016; Pandey and Jessica, 2019). This underscores the adaptive, albeit imperfect, nature of behavioural biases in filling the gap left by disrupted market fundamentals. While these biases can encourage investment during uncertainty, they also risk perpetuating inefficient or speculative behaviour, such as the tendency for anchoring on past prices or trends irrespective of changing market realities.

The contrasting impacts of market fundamentals and behavioural biases highlight the dual forces shaping investment allocation decisions under uncertainty. While fundamentals serve as rational signals of market health, their negative influence during volatility underscores the challenges investors face in interpreting and acting upon them. Conversely, the positive role of certain biases demonstrates the psychological mechanisms investors employ to navigate uncertainty. Practically, the balance between these two dimensions of decision-making is crucial for investors attempting to navigate periods of uncertainty. Strategies incorporating sensitivity analysis into portfolio decisions or leveraging behavioural nudges to counteract suboptimal tendencies can enhance decision-making during uncertainty. Improving transparency and information availability could also go a long way to mitigate negative risk perceptions, even when fundamentals underperform in response to uncertainty.

4.3 Decision-making in the aftermath of market disruptions: exploring the moderating effects of uncertainty

By exploring how uncertainty moderates decision-making considerations amid heightened uncertainty, this study provides further insights into the complex dynamics at play when property investors must make potentially irreversible decisions in a volatile climate. These effects were analysed through simple slope analyses based on the PROCESS macro model developed to represent the conceptualised decision-making system. These charts represent how fundamentals and behaviour impact investment intentions and allocation decisions as uncertainty fluctuates. Moderating effects modelled through PLS-SEM need to be tested at mean, +1 and −1 standard deviation for results to be deemed significant (Hayes, 2013).

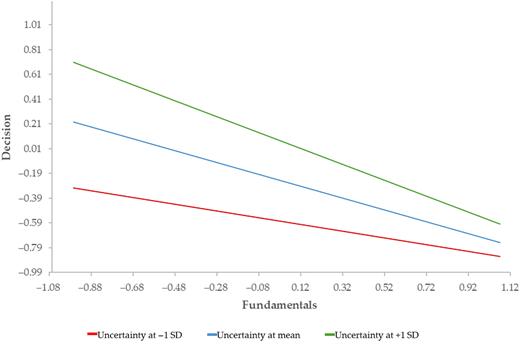

Figure 6 illustrates the effects of market fundamentals on investment intention and allocation decisions at different levels of perceived uncertainty. The negative moderating effects highlighted suggest that uncertainty further weakens this relationship, making investors less willing to invest and allocate capital. With uncertainty at mean (normal levels), this relationship is moderate and reflects a typical investor’s response to signals from fundamentals. As uncertainty decreases, this relationship becomes even less pronounced, and investors’ allocation decisions become more stable and less reactive to changes in prices, returns, vacancies, and demand. During periods of heightened uncertainty, core market fundamentals such as rents, prices, and transaction volumes often decline, reflecting broader shifts in market sentiment and performance (Ahiadu et al., 2024b; Allan et al., 2021; Milcheva, 2022). However, the impact of uncertainty extends beyond measurable indicators. Investor confidence in the future trajectory of these fundamentals also diminishes, introducing an additional psychological layer to decision-making. In such contexts, the perceived instability of market signals prompts investors to augment traditional analysis with behavioural heuristics, experiential knowledge, and intuitive judgement, further reinforcing the adaptive nature of investment behaviour under uncertain conditions (Lo, 2004; Mushinada, 2020).

Simple slope analysis (moderating effects of uncertainty on the relationship between market fundamentals and investment decisions). Source: Figure created by authors

Simple slope analysis (moderating effects of uncertainty on the relationship between market fundamentals and investment decisions). Source: Figure created by authors

The overall implication of these results implies that even minor deviations in market fundamentals can exacerbate investors’ reluctance to invest during volatile periods, further indications of risk-averse behaviour as uncertainty peaks (Ahiadu et al., 2024a; Jackson and Orr, 2019). Higher risk and uncertainty premiums could also diminish interest in underperforming assets as concerns over future economic movements erode investor confidence and capital allocation (Chau, 1997). Additionally, investors may opt to delay decisions and wait for clearer signals due to the fear of losses (Jackson and Orr, 2019; Kumar and Goyal, 2016; Pandey and Jessica, 2019). The pronounced negative relationship under heightened uncertainty underscores the need for property investors to adopt more robust risk assessment frameworks. By incorporating stress testing and scenario analysis, investors can better anticipate how fluctuations in fundamentals might affect their portfolios during volatile periods.

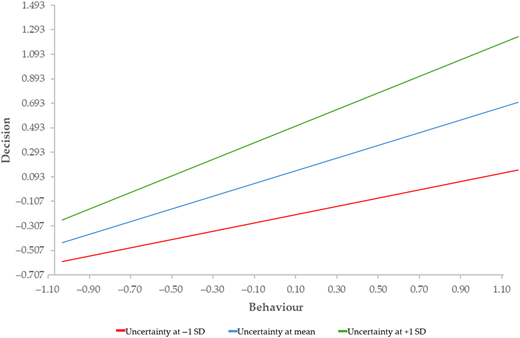

Conversely, uncertainty amplifies the positive effects of behavioural biases such as overconfidence, anchoring, and intuition on allocation decisions. As shown in Figure 7, behavioural biases are less likely to impact investment allocation decisions when uncertainty is low, but much more prominent when conditions are more volatile. Behavioural biases exhibit a positive relationship with investment decisions across all levels of uncertainty. However, this relationship is less pronounced when uncertainty is low, suggesting that in stable markets, biases are less prominent in shaping investment behaviour (Jackson and Orr, 2019; Newell, 2016; Pandey and Jessica, 2019). However, amid heightened uncertainty, the influence of biases becomes more pronounced, exacerbating the effects of herding, intuition, and overconfidence on decision-making.

Simple slope analysis (moderating effects of uncertainty on the relationship between behaviour and investment decisions). Source: Figure created by authors

Simple slope analysis (moderating effects of uncertainty on the relationship between behaviour and investment decisions). Source: Figure created by authors

There are several transmission channels through which the property market’s inefficiencies limit rational decision-making, but information asymmetry is ubiquitous and encourages investors to augment fundamentals with biases such as intuition and experience (Gallimore et al., 2000; Kumar and Goyal, 2016; Waweru et al., 2014). Given these universal challenges, the persistent role of behavioural biases on investment decisions is unsurprising. Uncertainty introduces an additional layer of complexity that amplifies this relationship by reducing confidence in market fundamentals, thus shifting tendencies towards loss aversion and cautious attitudes (Brundin and Gustafsson, 2013; Jackson and Orr, 2019). In an attempt to navigate what they perceive as more volatile economic conditions, investors may leverage intuition built on experience and overconfident investors may back themselves to outperform the market by going against economic indicators (Ahiadu et al., 2024a; Sah et al., 2010). Even as overall investment activity dips, these investors could allocate more capital to capitalise on emerging opportunities created by underperformance and shifting consumer attitudes (Ahiadu et al., 2024a). The heightened impact of behavioural biases under uncertainty calls for strategies to mitigate their influence on decision-making. For investors, awareness and management of biases through tools like decision-making frameworks or behavioural finance training can reduce the risks associated with over-reliance on intuition or herd behaviour.

The findings further accentuate the intricate interplay between market fundamentals, behaviour, and uncertainty in shaping property investment decisions. Investors respond differently to signals from market fundamentals and behavioural tendencies based on the level of uncertainty, highlighting the dynamic nature of decision-making across varying economic climates. During stable periods, these effects are less pronounced, the diminished impact of fundamentals and the amplified influence of biases suggest a shift toward reactive, emotionally driven decision-making. To leverage these insights, stakeholders must integrate context-sensitive strategies. Adaptive frameworks that consider both rational and behavioural dimensions could become essential as decision-making becomes more complicated in the digital age, noting that investors’ key considerations shift in response to uncertainty and other externalities (Ahiadu et al., 2024a).

5. Conclusions

The nature of the property market, the cost of assets, and the complex frameworks influencing performance complicate investment decisions. In the aftermath of unexpected market disruptions, the extant literature suggests that decision-making is further complicated due to heightened uncertainty and reduced confidence in market fundamentals. Although these fundamentals remain core to investment decisions, uncertainty and information asymmetry often compels property investors to augment their decisions with cognitive biases, such as intuition, experience and other heuristics. A few significant market disruptions have, over the past few years, increased uncertainty and complicated investment decisions. In response to the COVID-19 pandemic and geopolitical tensions, rising uncertainty impacted prices, returns, vacancy rates, and capital allocation. Building on the existing literature of adaptive markets and investors’ tendency to rely on mental shortcuts for complicated decisions, this study integrated both market fundamentals and behavioural biases in a single framework to assess how they influence property investment decisions under varying levels of economic, monetary policy, and political uncertainty.

These relationships were investigated based on the perspectives of 412 commercial property investors in Australia gathered over the last two months of 2023, a period marked by heightened uncertainty in response to a series of aggressive monetary policy decisions by the RBA and inflationary pressures. Subsequently, the hypothesised dynamic system of market fundamentals, behaviour, uncertainty and investment decisions was modelled through PLS-SEM, using the PROCESS macro approach. Constructs representing the focus variables in this study were developed based on existing literature in this domain – market fundamentals (demand, prices, returns, and vacancy rates) and behavioural biases (anchoring, herding, intuition, loss aversion, overconfidence). Investment decisions were represented by investors’ intention and willingness to allocate capital to or recommend property investment. The developed model was extensively tested to establish model fit and the statistical significance of all relationships represented in the system.

Perceived economic, monetary policy and political uncertainty among investors was rated above normal, reflecting other indicators tracking market stability in response to a series of exogenous shocks. Different investors appear more sensitive to uncertainty fluctuations, notably based on their experience and wealth. The existing literature highlights how investors leverage their experience and specialised knowledge to navigate uncertainty and information asymmetry. For wealthier investors, the higher capital requirements could make their decisions more susceptible to external factors due to the fear of losses as fundamentals weaken in response to uncertainty.

The relationship between market fundamentals and behavioural biases is also dynamic, moderated by perceived uncertainty levels. There is a significant negative impact of fundamentals on investment allocation and intention decisions, underscored by recent findings that reflect investors’ reluctance to allocate capital in the aftermath of market disruptions and weakening performance indicators. Conversely, behavioural biases such as herding, intuition, and overconfidence become more pronounced under these conditions, driving investment activity despite volatile market signals. These results underscore the adaptive yet imperfect nature of investor behaviour, where fundamentals dominate decision-making in stable climates, and biases play a larger role during uncertainty.

The findings of this study offer several actionable insights for property professionals and investors operating in the commercial property space. For agents, understanding that investors respond differently to uncertainty based on their wealth and experience can guide how they tailor advice, marketing strategies, and investment recommendations. Particularly during periods of heightened uncertainty in response to market disruptions, agents can frame investment opportunities in ways that align with how investors perceive risk during uncertainty, highlighting stability, comparative market performance, or long-term value rather than short-term volatility. For investors, this dynamic relationship highlights the importance of adaptive strategies that emphasise core fundamentals during stable periods, while being consciously aware of and managing the influence of cognitive biases during volatile times. In addition, the findings encourage the use of experience-based heuristics as a tool, not a substitute, for data-driven investment evaluation. This adaptive approach was particularly evident in the aftermath of the pandemic, as more experienced and agile investors reallocated capital away from underperforming office and retail assets toward industrial property despite historical data classifying it as a riskier asset class.

By modelling these relationships in one system, this study provides a nuanced understanding of how investors navigate varying economic climates and the implications for capital allocation tendencies. The findings also support the AMH by integrating the rational and human elements of decision-making. The fluid interaction of this complex system of decision-making also challenges traditional, longstanding views on efficient property markets and rational investors. Because property markets exhibit several inefficiencies, including imperfect access to information, behavioural tendencies can encourage investment intentions and allocation decisions under certain conditions. Investors can leverage these results through adaptive strategies that prioritise fundamentals during stable conditions while mitigating the influence of biases under uncertainty.

Much like the complexities and emerging norms that motivated this study, the intricacies of property investment decisions are challenging to model statistically. A key limitation of this study is its focus exclusively on private commercial investors, which may limit the generalisability of the findings to institutional and residential investors. The modelled behaviour was also based on self-reported data on investors’ perceptions and intentions, which may not always translate to investment behaviour. By employing process-tracing techniques, future extensions could observe investors’ decision-making considerations in real time and under varying economic conditions. Access to finance is also a crucial consideration in property investors’ capital allocation decisions, and future research could explore how the availability and nature of financing impact decisions, particularly the interaction between lenders’ response to uncertainty and investors’ debt appetites. Lastly, some questions about how fundamentals, behaviour, and uncertainty impact investment outcomes remain unanswered and could provide further insights into ideal strategies as investors navigate an increasingly complex landscape.

The continued integration of artificial intelligence (AI) in property investment decisions and systems will undoubtedly introduce novel challenges, but is unlikely to completely invalidate the role of the human element in complex decision-making. Although the integration of AI is set to enhance property investment decision-making by improving the analysis of large datasets and forecasting trends, questions remain over how well human behaviour can be represented in these systems. Therefore, as AI becomes increasingly embedded in investment strategies, understanding the interaction between AI-driven insights and human biases will be crucial. The behavioural factors identified in this study remain central to investment decision-making, and thus, the insights derived from this research will continue to be relevant as investors navigate the complexities of real estate markets in an era of technological advancement. Leveraging AI to track and debias behavioural biases remains a promising application of the emerging technologies to improve decision-making under varying levels of information asymmetry and uncertainty.

This paper is part of an ongoing PhD study on commercial property investment decision-making amid conditions of heightened economic uncertainty. As part of this broader study, other papers of different scopes will be published. The authors are grateful to the anonymous property experts who were interviewed and investors who responded to the online questionnaire survey.