Value constitutes a key principle of asset management (AM) and decision-making processes should be oriented toward optimizing it. Value models refer to models that can measure the effects of any decision over value, supporting decision-making concerning the assets through their whole lifecycle. In this context, the objective of this work is to develop a methodology for establishing value models to support decision-making in strategic capital investments for multi-category portfolios.

An approach that integrates multi-criteria decision-making, AM principles and participatory processes is proposed.

The analytic hierarchy process and multi-attribute utility methods are used as analytical tools enabling the assignment of absolute merits to the evaluated alternatives. The application of the AM principles allows one to frame the decision problem within the context of AM. Furthermore, participatory processes enhance transparency and trust in the developed value model and empower employees.

Through the application of a case study, it has been demonstrated that the approach not only facilitates the ranking of alternatives and a better understanding of their strengths and weaknesses but also establishes a shared concept of objectives (and attributes for their assessment) within the company for the capital investment decision-making.

The AM literature often lacks systematic approaches for identifying value and making value-based decisions. While some approaches have been proposed for guiding strategic capital investments, they typically rely solely on financial and risk criteria. This work aims to bridge this gap by integrating various dimensions of value into the development of a comprehensive value model.

1. Introduction

Asset management (AM) is defined as the coordinated activity of an organization aimed at realizing value from its assets (ISO 55000, 2014). AM encompasses all the activities involved in the asset’s lifecycle, which initiates with identifying requirements or opportunities, advances to asset acquisition or creation, involves ongoing operations and maintenance, and culminates in renewal or disposal (GF- MAM, 2014).

In AM, capital investment decision-making comprises the processes for evaluating and analyzing options related to acquiring or creating new assets, enhancing asset capabilities or renewing assets when they reach the end of their useful life (IAM, 2015). These types of capital investments apply to both individual assets and multi-asset systems.

According to Petchrompo and Parlikad (2019), multi-asset systems are composed of multiple assets that share common characteristics or resources under the control of an organization and can be differentiated into

Fleet: either a group of identical assets or assets that share similar technical features and operate under the same conditions;

Portfolio: a collection of assets under an organization’s control, which can either belong to the same category but have different features “single-category portfolio” or belong to different categories “multi-category portfolio”.

This paper focuses on capital investment decision-making of multi-category portfolios.

Strategic decisions are defined as decisions that have a high impact on the future performance of the organization, involve substantial commitments of resources over an extended period, are often difficult to reverse, and entail a significant time lag between the decision and its resultant outcomes (Matheson and Matheson, 1998). Although some decisions may be relatively “operational” in nature, many capital investments exhibit a more “strategic” focus.

Financial methods are commonly employed to assess the viability of investments or to compare various alternatives (Haka, 2006). Examples of these methods include net present value (NPV), return on assets or investment (ROA or ROI), internal rate of return (IRR) and the payback period, among others. Nevertheless, over-reliance on financial appraisal tools is thought to bias decision-makers against undertaking strategic investments that are crucial to the development of business capability and innovation (Alkaraan and Northcott, 2006).

A solution to enhance decision-making in strategic capital investments may be found in the concept of value, which constitutes a key principle of AM. Value is obtained by acquiring assets that allow an organization to fulfill its strategic objectives (El-Akruti et al., 2013) and ensuring that the assets keep fulfilling those objectives throughout their lifecycle. Value includes all the dimensions necessary to achieve organizational objectives and not only financial ones.

In value-based decision-making, an organization must define what constitutes value in relation to achieving its organizational objectives (Esteves et al., 2023). This involves considering the needs and expectations of various stakeholders, including investors, customers, regulators, employees and local communities. Once the concept of value has been established, the decision-making process should be oriented toward optimizing it.

Value optimization is not a straightforward task due to the presence of multiple dimensions, both tangible and intangible (Woodhouse, 2018). Tangible dimensions include quantifiable factors like costs or revenue generation. In contrast, intangible dimensions encompass factors like enterprise reputation, customer satisfaction or employee morale, which are critical to an organization’s success but not easily quantified.

In this context, value models play a crucial role in supporting the decision-making process for value optimization. A value model refers to a model that can measure the effects of any decision over value, supporting decision-making concerning the assets through their whole lifecycle (Crespo M´arquez et al., 2020). However, the literature lacks systematic approaches for identifying value and making value-based decisions (Srinivasan and Parlikad, 2020). Therefore, the challenge of this work lies in integrating the various dimensions of value into the development of a comprehensive value model aimed at guiding decision-making in strategic capital investments for multi-category portfolios.

In value-based approaches, decision-makers often strive to achieve multiple dimensions of value, but progress in one direction can sometimes hinder progress in others. According to ISO 55000, 2014, the realization of value typically involves balancing costs, risks, opportunities and performance. In the literature, multi-criteria decision-making (MCDM) has been employed to address complex decision-making problems with multiple conflicting objectives.

Building upon the foundations of AM, MCDM and participatory processes, the novelty of this work is the introduction of a methodology for developing value models that can support decision-making in strategic capital investments for multi-category portfolios. The paper is structured as follows: Section 2 analyzes the state-of-the-art and Section 3 summarizes the main tools that are utilized in the methodology. Section 4 illustrates the proposed methodology and Section 5 applies it to a case study for its validation. Obtained results are discussed in Section 6, and finally, Section 7 presents the conclusions and sets the directions for future work.

2. State-of-the-art

In AM of multi-category portfolios, numerous studies have addressed the definition and optimization of short- and long-term investment plans for asset renewal. As assets naturally age and degrade, the critical task is to determine which ones to replace and when. Infrastructure AM, which encompasses areas such as water supplies, sewer networks, roads and electricity distribution networks, often involves the periodic renewal of a variety of geographically distributed simple components. Here, “simple” indicates that aging primarily leads to inefficiencies rather than major risks. Examples can include pipes, insulators, cables and more. Investment plans are developed to outline short- and long-term renewals of these components (Vieira et al., 2020; Ramos-Salgado et al., 2022). In this context, the decision-making process becomes operational, requiring investment optimization typically based on component degradation estimation and prediction (Hashim et al., 2019; Hawari et al., 2020).

For more complex assets, the renewal decision is more challenging and less straightforward, shifting the problem from investment optimization to prioritization. The useful life of these assets can be assessed using an economic life approach, which involves determining the optimal renewal time to minimize the combined effect of costs and risks, quantified in monetary terms. This assessment is typically expressed in terms of the total cost of ownership (TCO) (Woodward, 1997), as extensively discussed in Woodhouse (2018). However, several authors have sought to enhance the TCO concept by adopting a more holistic approach. For instance, De la Fuente et al. (2021) integrated asset condition projections over time using the Asset Health Index to improve the accuracy of TCO estimation. Additionally, Roda and Garetti (2020) extended the TCO’s cost-risk optimization by incorporating the performance dimension through the use of the reliability block diagram based on Monte Carlo simulation.

The aforementioned works quantify risks in monetary terms, while analyses of other difficult-to-quantify risk aspects, such as personnel safety, environmental damage or negative public acceptance, are often treated separately in different processes. To seamlessly combine risk and economic analyses, risk-centered approaches can be adopted. Catrinu and Nordgard (2011) propose the use of MCDM under uncertainty to integrate the assessment of safety risks and costs for supporting the evaluation of maintenance and reinvestment alternatives. A similar approach is presented in Syed and Lawryshyn (2020), where a framework and methodology are proposed for the quantitative prioritization of risk-informed AM projects using MCDM.

Both the TCO-centered and risk-centered methodologies are especially valuable for “like-for-like renewals,” where the asset is replaced without enhancing its functionality, essentially maintaining the status quo. However, different approaches are necessary for strategic capital investments. Examples of strategic capital investments can be found in various scenarios, including the acquisition or creation of new assets, the enhancement of asset capabilities, or the renewal of existing assets. For instance, a strategic capital investment might involve acquiring an asset that increases the company’s production capability or enables the manufacturing of a different product. It could also entail retrofitting existing assets with digital technologies to introduce additional functionalities (Jaspert et al., 2021; Sanchez-Londono et al., 2023) or renewing an asset with one that offers increased resilience to climate change or reduced greenhouse gas emissions. In these examples of strategic capital investments, various dimensions of value must be considered to support sound decision-making.

Research on asset selection for multi-asset systems is still very limited (Petchrompo and Parlikad, 2019), particularly in the context of approaches for strategic capital investments. However, within the field of AM for energy portfolios, Bambirra et al. (2023) introduce a methodology for evaluating the acquisition of long-term energy assets, where investment alternatives are assessed within plausible future scenarios. They employ MCDM to evaluate alternative based on financial and risk criteria, including the expected net revenue of the portfolio, revenue in the worst-case scenarios, and an insurance index. On a similar note, Latunde and Bamigbola (2018) propose an optimal control approach for modeling strategic capital investments from the perspective of an investor. Their objective is to maximize the expected present value of the utility of assets while minimizing associated risks. However, it is worth noting that even though these approaches are applied to strategic capital investments, they still rely solely on financial and risk criteria.

To the best of the authors’ knowledge, the only work proposing the development of a value model for strategic capital investments is presented in Biard et al. (2022). In this study, the authors define a hierarchy of objectives for prioritizing investment projects in the power industry based on a literature analysis. However, while this approach holds value, the objectives have not been validated with decision-makers and stakeholders involved in the decision-making process, potentially limiting its practical applicability within the organization. Additionally, the creation of the value model is left as future work.

In the context of multi-category portfolios, the novelty of this work lies in the definition of a methodology for developing value models that integrate different dimensions of value to guide decision-making in strategic capital investments.

3. Theoretical framework

This section provides a summary of the primary tools utilized in the methodology to construct value models for guiding decisions in strategic capital investments. The analytic hierarchy process (AHP) is explained in Section 3.1, the multi-attribute utility (MAU) is covered in Section 3.2, and the AM principles are illustrated in Section 3.3.

3.1 Analytic hierarchy process

The AHP is one of the most popular MCDM methods (Tavana et al., 2023). It consists in a theory of measurement through pairwise comparisons that relies on the judgments of experts to derive priority scales (Saaty, 1994). The AHP allows dealing with quantifiable and intangible criteria and is based on the principle that, to make decisions, experience and knowledge of people is at least as valuable as the data they use.

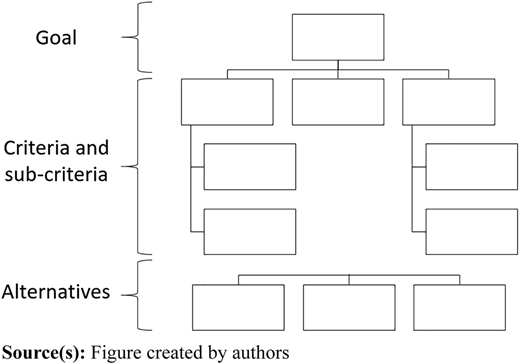

In the AHP, a decision hierarchy is first structured with the goal of the decision at the top, followed by criteria, sub-criteria and alternatives; see Figure 1.

After establishing the hierarchy, a set of pairwise comparison matrices is constructed. In these matrices, each element in an upper level is used to compare the elements in the level immediately below. Pairwise comparisons are employed to evaluate both criteria and alternatives. When comparing criteria, the objective is to determine their relative importance or relevance in relation to higher-level criteria within the hierarchy, whereas the goal of comparing alternatives is to assess whether an option is superior to another with respect to a specific criterion. Typically, a nine-point scale is employed to quantify the importance and preferences in these pairwise comparisons; see Table 1.

Local priorities for the criteria and the relative importance of the alternatives concerning each criterion are determined using weighting methods. Subsequently, the overall priority of each alternative is calculated as the sum of the products of the local priority of the alternative relative to each criterion, weighted accordingly. Finally, the alternatives are ranked based on their overall priorities.

3.2 Multi-attribute utility

Among MCDM, MAU method is an extension of conventional utility theory (Wallenius et al., 2008). In MAU, the attribute scale provides a means to measure the achievement of a specific objective, with the attribute referring to the quantity measured on the attribute scale (Clemen and Reilly, 2013). For instance, if minimizing cost is one of the objectives in a given decision, then measuring cost in dollars is an appropriate attribute scale, and the cost value represents the attribute for this objective.

Three types of attributes can be identified (Edwards et al., 2007): natural attributes, proxy attributes and constructed attributes. These attribute categories facilitate the evaluation of tangible objectives. However, when dealing with intangible objectives, a specialized form of constructed attribute can be employed. This type is characterized by constructed scales with two or more distinct qualitative levels of objective achievement, with each level accompanied by a corresponding verbal judgment (Table 2). This approach enables the conversion of an uncertain attribute into a deterministic one.

MAU involves defining a utility function for each attribute, followed by their weighting and aggregation to generate an overall utility function. In this context, the additive utility function represents an easy-to-use technique applicable for independent attributes. This function calculates an overall utility for an alternative as a weighted sum of individual utility functions for each objective. For an alternative characterized with attribute levels x1, …, xm on the m objectives, the utility of this alternative can be computed as:

where the weights are k1, …, km and the utility functions for each attribute are U1(x1), …, Um(xm). In cases where there is no uncertainty about the attributes, such as with constructed attributes, the values of xi are deterministic.

Different approaches can be utilized to assess utility functions from constructed attributes (Keeney and Raiffa, 1993). One common method is the proportional scores approach, which involves assigning a score of 0 to the lowest level on the constructed scale and a score of 1 to the highest level. All the other levels are then rated between 0 and 1, reflecting the degree of preference for each constructed level relative to the lowest and highest ranked ones.

Finally, a variety of methods can be used to assess the weights of the individual utility functions (Clemen and Reilly, 2013), such as pricing out, swing weighting, and lottery weights, among others.

3.3 Asset management principles

Decision-making is a vital and complex element underpinning successful AM. In making AM decisions, it is important to find the right compromise between competing interests, such as asset utilization/performance versus asset care (maintenance), capital investment cost versus operating expenditures, or short-term benefits versus long-term sustainability (IAM, 2015).

Roda and Macchi (2018) outline the key principles that serve as the basis for effective asset-related decision-making. These are

Lifecycle orientation: incorporates long-term objectives and performances to drive decision-making.

System orientation: emphasizes the holistic consideration of asset systems in their entirety, going beyond individual components.

Risk orientation: utilizes risk management approaches to address uncertainties associated with achieving stated objectives for assets.

Asset-centric orientation: focuses on leveraging asset data and information for making informed business decisions.

These principles serve as fundamental pillars for effective asset-related decision-making, enabling organizations to navigate the complexities and trade-offs inherent in the management of their asset portfolios.

4. Value models for strategic capital investments

This section presents the methodology proposed for establishing value models able to support decision-making in strategic capital investments. Section 4.1 outlines the requirements that the developed model must fulfill. Then, Section 4.2 demonstrates the capability of a hybrid approach that combines AHP with MAU to fulfill the identified requirements. Finally, Section 4.3 details the proposed methodology integrating AM, MCDM and participatory processes.

4.1 Requirements

The value model must be intuitive to enhance the transparency of the decision-making process during its application; i.e. the model should provide a clear explanation of how it assigns a specific merit to an alternative. Otherwise, decision-makers may struggle to trust or utilize the model effectively.

Because the value model needs to estimate the asset’s potential to generate value for the organization, its output must be independent of the analyzed alternatives. In other words, it should provide an absolute merit for each alternative rather than a relative one. This requirement serves to safeguard against the approval of suboptimal capital investments solely because weaker alternatives have been proposed.

Given that organizations need to incorporate both tangible and intangible elements of value into their decision-making processes, the developed value model must address both quantifiable and intangible dimensions. This comprehensive approach ensures that strategic capital investments are evaluated holistically.

According to Matheson and Matheson (1998), organizations that make good strategic decisions use participation in the decision-making process to achieve employee empowerment and alignment around common goals. Therefore, the value model must be co-created with the decision-makers and the involved stakeholders.

Finally, given that the value model is constructed in a participatory manner, the method used for its development must be easily comprehensible to the participants. This approach ensures that the focus during the co-creation activities remains on discussing objectives and their relative importance, rather than on understanding the method and how to precisely translate participants’ preferences into it.

In summary, the identified requirements are

Intuitive model: the resulting value model must be transparent to the decision-makers and the stakeholders involved in the decision.

Absolute merit: the value model must provide an absolute merit for each alternative.

Tangible and intangible elements: the value model must address both quantifiable and intangible dimensions of value.

Co-creation process: the value model must be co-created with the decision-makers and the stakeholders involved in the decision.

Comprehensible method: the method for constructing the value model must be easily understood by participants in the co-creation activities.

4.2 Analytical approach

Starting from the requirements identified in Section 4.1, the analytical approach adopted for the value model is next illustrated.

AHP may be a suitable candidate to fulfill the identified requirements since it is perhaps the most intuitive and widely used method in MCDM analysis. AHP is capable of incorporating both tangible and intangible aspects of value, and the resulting model is simple, constructed collaboratively through expert judgments. However, the method assigns a relative merit to each alternative, as they are compared pairwise based on defined criteria. Therefore, an alternative approach must be identified to create a model capable of determining an absolute merit to each alternative.

MAU shares similar characteristics with AHP. A straightforward model can be constructed when utilizing the additive utility function. Intangible elements can be managed in a deterministic form through constructed attributes and converted into utility functions using the proportional scores method. Weights and utility functions can be assessed collaboratively. Unlike AHP, MAU is capable of assigning absolute merits to the evaluated alternatives.

Building upon the aforementioned considerations, MAU appears to meet all the identified requirements. However, the methods used for the weighting process (e.g. pricing out, swing weighting, lottery weights, etc.) may be less intuitive compared to the pairwise comparisons utilized in AHP. Since the best approach often involves a combination of methods (Edwards et al., 2007), a hybrid approach that integrates AHP and MAU is employed. This hybrid approach involves: (1) the use of an additive utility function as the overall value model; (2) the creation of individual utility functions for intangible objectives derived from constructed attributes using the proportional scores method; (3) the assessment of weights through pairwise comparisons using the AHP method.

Finally, the defined analytical approach is demonstrated to fulfill the identified requirements:

Intuitive model → the additive utility function is a transparent model as it involves a weighted sum.

Absolute merit → MAU methods provide an absolute merit for each alternative.

Tangible and intangible elements → for intangible objectives, proportional scores enable the conversion of constructed attributes into utility functions.

Co-creation process → weights are assessed through pairwise comparisons of objectives, while a merit from 0 to 1 is assigned to each constructed level of intangible objectives. Both processes occur in a participatory manner.

Comprehensible method → participants in the co-creation process find the pairwise comparison and merit assignment to constructed scales easy to understand.

4.3 Methodology

Considering that a hybrid approach that combines AHP with MAU is utilized, the methodology for developing the value model is constructed by integrating elements from AHP (Saaty, 1994) and MAU (Keeney and Raiffa, 1993; Saaty, 1994; Edwards et al., 2007). Additionally, AM principles are incorporated to facilitate the creation of a model able to guide effective asset-related decision-making. The proposed methodology comprises the following steps:

Definition of the decision problem: since a surface problem can hide the real issue, the exact problem must first be identified. This step includes, but is not limited to, defining the decision-makers and stakeholders involved in the strategic capital investment decision-making, understanding the organizational structure and processes related to the decision, exploring past decisions and methods and identifying potential alternatives and preferences.

Identification of objectives and attributes: objectives related to strategic capital investments are identified, along with attributes capable of measuring the achievement of each objective. Constructed attributes are utilized for intangible objectives, while the principles of AM serve as a guiding framework for defining the objectives.

Assessment of the objective weights: objectives are compared pairwise using Saaty’s scale during a co-creation workshop with selected actors. After ensuring the consistency of the obtained comparisons, weights are assessed.

Assessment of the utility functions: a utility function is evaluated for each attribute. For attributes with constructed scales, the proportional scores method is applied after assigning merit to each constructed level in a co-creation workshop.

Construction of the value model: the overall additive utility function is computed using the weights assessed in step 3 and the individual utility functions formulated in step 4.

Validation of the value model: validation is essential to ensure the effectiveness of the value model. Various strategies can be employed for this purpose, including applying it to past capital investment decisions with known outcomes or engaging in discussions with decision-makers and stakeholders.

5. Case study

In accordance with the definition of strategic decision provided by Matheson and Matheson (1998) (Sec 1), the acquisition of laboratory equipment in a university constitutes a strategic capital investment within a multi-category portfolio since it involves:

High impact on future performance: the quality and availability of laboratory equipment directly influence the institution’s ability to conduct cutting-edge research and provide high-quality education, which, in turn, affects its reputation and competitiveness.

Substantial commitments of resources: budgets must be allocated for the purchase, maintenance, and operation of the equipment, making it a long-term financial commitment.

Difficulty to reverse: once laboratory equipment is acquired, it becomes an integral part of the university’s infrastructure. Reversing such decisions would require significant financial and logistical challenges, making reversibility a complex and costly process.

Time lag for resultant outcomes: it takes time to select, purchase, install, and integrate this equipment into the academic and research processes. The benefits, such as improved research capabilities and enhanced educational experiences, become evident over the long term.

In this section, the proposed methodology is applied to establish a value model for guiding the acquisition of strategic laboratory equipment in the Mechanical Engineering Department at the Universidad de los Andes.

5.1 Definition of the decision problem

At the Universidad de los Andes, the Faculty of Engineering allocates an annual budget for capital investments to each department. Within the Mechanical Engineering Department, professors are organized into research groups, and each group is tasked with submitting equipment proposals. These proposals must include the purchase cost and justifications for acquisition. Subsequently, a financial committee, comprising three professors and the department chair, reviews the submissions and selects the equipment for acquisition. However, past experiences with suboptimal investments have prompted a reevaluation of this decision-making process.

The decision quality chain proposed in Matheson and Matheson (1998) was used to identify improvement opportunities. In particular, the process exhibited deficiencies in the following areas:

Clear values and trade-offs: the criteria for measuring the value of alternatives were not established, and it was unclear how the financial committee made rational trade-offs among alternatives.

Meaningful and reliable information: the right information should support the decision-making process. However, since criteria were not established, the information provided in the proposal submissions was arbitrarily filled out within the justification section of the proposal. Consequently, the same information was not consistently presented for different alternatives, resulting in incomplete information regarding the values crucial for making the decision and the comparison of alternatives.

Suitable decision models: notably, the decision-making process of the financial committee relied on common sense rather than analytical approaches, hindering the determination of which alternatives would create the most value.

In conclusion, addressing these deficiencies was essential to enhance the decision-making process for allocating capital investments effectively. Furthermore, the developed approach had to be operational; if it were too complex, it might not be applied.

5.2 Identification of objectives and attributes

The Mechanical Engineering Department of the Universidad de los Andes comprises 15 professors organized into five research groups. To define the objectives sought by decision-makers in addressing the decision, we conducted semi-structured interviews with the directors of the five research groups and the laboratory coordinator (representing key decision stakeholders) as well as with the department chair (representing the decision-makers; i.e. the financial committee). The interview questions were formulated based on the key principles of AM outlined in Section 3.3. The primary aim was not only to identify the objectives but also to establish operational attributes capable of measuring their accomplishment. In this context, an “operational attribute” refers to an attribute for which the information necessary to describe the consequences of an alternative over the objective can be obtained, allowing for a reasonable value trade-off.

According to Edwards et al. (2007), objectives can be classified into fundamental and means objectives. Fundamental objectives are used to describe the basic reasons for being interested in the decision, whereas means objectives are important only for the influence on the achievement of the fundamental objectives. Objectives can be organized into a hierarchy in which the lower levels (i.e. means objectives) explain what is meant by the higher levels, i.e. fundamental objectives. This representation is defined as objectives hierarchies (Keeney and Raiffa, 1993), also known as a value tree (Edwards et al., 2007).

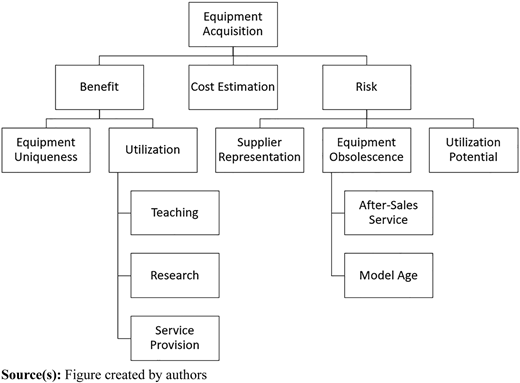

Following the outlined approach, the interviews were recorded and subsequently transcribed. All the concepts related to the reasons why the decision-makers and the stakeholders were interested in the decision were identified and converted into objectives by assigning a name and definition to each. Subsequently, a hierarchy of objectives was constructed, as illustrated in Figure 2. Additionally, each objective was provided with a definition, which can be found in Table 3.

In accordance with the AM definition of value (ISO 55000, 2014), the fundamental objectives were identified as benefit, cost estimation and risk, whereas the others were categorized as means objectives. Additionally, the purchasing cost was not included in this process since it is considered at a later stage where the final decision is made based on the merit assigned by the value model to the different alternatives and their purchasing costs. The risk assessment focused solely on the risks related to the equipment’s acquisition, since risks associated with its subsequent use, such as occupational health and safety risks, are evaluated in a separate process. Finally, the equipment uniqueness criterion assessed the strategic value of an acquisition, while the purchase of redundant equipment, because it is operationally determined that another one is needed, does not fit into this process.

After identifying the objectives, a set of constructed attributes was defined for both tangible and intangible objectives, as outlined in Table 4. Constructed attributes were employed also for tangible objectives to facilitate an operational assessment. For instance, estimating the NPV of the services that the equipment would provide to industries could be challenging due to uncertainties and a lack of readily available information within the department’s regular operation. Consequently, constructed attributes were used to evaluate intangible objectives and to operationalize the assessment of tangible objectives.

Finally, the defined objectives (Table 3), hierarchy (Figure 2), and constructed attributes (Table 4) were validated in a workshop with two research group directors and two professors from the financial committee. Subsequently, a few iterations were carried out via email to finalize the details before arriving at the objectives and attributes presented in this article.

5.3 Assessment of the objective weights

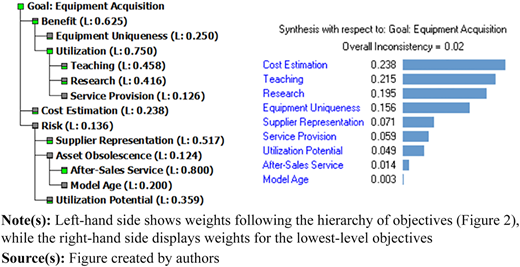

During the workshop to validate the objectives and attributes, a pairwise comparison of the objectives was also conducted. We chose synchronous discussions to ensure a consensus, rather than relying on asynchronous and individual surveys with subsequent aggregation of results using an analytical method, such as the geometric mean. This approach allowed us to better understand the professors’ preferences and facilitated high-quality results, as each pairwise comparison was defined after comprehensive discussions and critical analysis. This level of depth would not have been possible with individual surveys alone. Since a consensus was reached for each comparison, additional weighting approaches, as discussed in Tavana et al. (2023), were unnecessary.

For the pairwise comparisons, we employed the Saaty scale, as shown in Table 1, but we used numerical values ranging from 1 to 5 instead of the original 1 to 9. For instance, “weak importance” was assigned a numerical value of 2, “demonstrated importance” received a value of 4 and so on. This modification was made to simplify the scale by eliminating intermediate levels, as their inclusion was deemed unnecessary for this study. Using the original Saaty scale without the intermediate levels would have unnecessarily widened the gap between objectives.

The data collected during the workshop were processed using Expert Choice software. The resulting assessed weights are displayed in Figure 3. As suggested by Saaty (1994), an inconsistency ratio of up to 10% is considered acceptable. This threshold is based on empirical observations and practical experience with the AHP methodology. While perfect consistency (i.e. 0%) is ideal, achieving it in real-world decision-making scenarios may be impractical due to the inherent subjectivity and complexity involved. An inconsistency ratio lower than 10% indicates that the level of inconsistency in the pairwise comparisons is relatively small and does not significantly affect the overall reliability of the decision-making process. In the case study, the obtained inconsistency ratio was 2%; see Figure 3. Therefore, the results of the pairwise comparisons were deemed satisfactory, and no further review or reconsideration by the professors was necessary.

5.4 Assessment of the utility functions

To evaluate the utility functions of the constructed attributes, a workshop was organized with the participation of two professors from the financial committee and the laboratory coordinator. Details regarding the specific merits assigned to each level on the constructed scale are outlined in Table 4. The same utility function was obtained for each attribute by applying the proportional scores approach and assigning a merit of 0 to the worst level of the constructed scale and of 1 to the best level. All the other levels are then rated between 0 and 1, reflecting the degree of preference for each constructed level relative to the lowest and highest ranked ones.

5.5 Construction of the value model

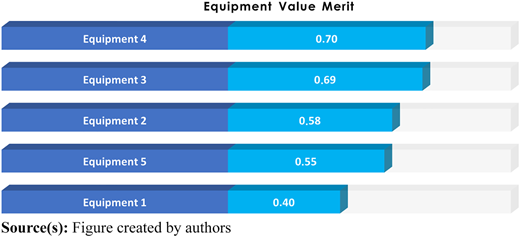

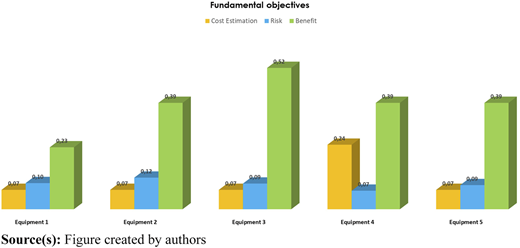

Excel was adopted to construct the value model, utilizing individual sheets for evaluating each alternative. The alternatives are assessed against the constructed attributes illustrated in Table 4, and the overall utility function is automatically computed, incorporating the weights defined in Figure 3. These assessments are then aggregated in a “Results” sheet, facilitating the comparison of the alternatives. A hierarchy of alternatives, ranked according to their respective value merit, is established (refer to Figure 4), serving as a crucial tool for assessing the most favorable choices among the options. At this stage, a “black box” decision-making approach may be adopted, incorporating the purchasing cost and considering the acquisition of equipment sets that offer the highest value merit within the available capital budget.

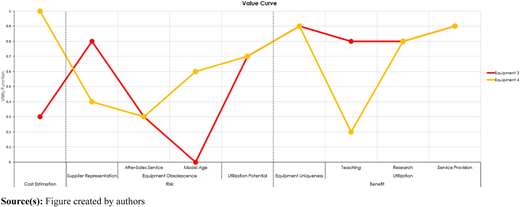

However, a “white box” decision-making approach may be preferable since the hierarchy is generated using the additive utility function. This function allows the compensation between good and bad scores across objectives while also foregoing specific information that may be important when ranking the alternatives. For this reason, two additional tools are provided. The histogram in Figure 5 illustrates the performance of the alternatives across the fundamental objectives (i.e. dimensions of value), providing decision-makers with a visual representation that aids in understanding the strengths and weaknesses of each alternative. Additionally, the value curve shown in Figure 6 offers an insightful overview of the performance of each alternative on the evaluated objectives, allowing the financial committee to assess the overall suitability of each alternative. The value curve is a graphic depiction of a company’s relative performance across its industry’s factors of competition and has been utilized as a diagnostic and an action framework for building compelling organizational strategies (Kim and Mauborgne, 2005). In this work, the value curve is adopted for a point-to-point comparison of alternatives.

While the additive utility function may have limitations, such as assuming additive independence and allowing for the compensation of objectives, the three visualizations defined serve as valuable tools for comprehending the alternatives, thereby supporting informed decision-making. By integrating the purchasing cost and available capital budget, decision-makers can assess the strengths and weaknesses of various equipment options and make strategic decisions aligned with the organizational risk appetite, required level of service, and estimated future expenses and resource availability.

5.6 Validation of the value model

The developed value model was utilized to compare three pieces of equipment of different categories, each with diverse price ranges and characteristics. The assessment process was overseen by the laboratory coordinator without imposing an extensive burden on normal operations. Additionally, the obtained visualizations were reviewed with two professors from the financial committee. The professors acknowledged that the model facilitated the ranking of alternatives and provided a better understanding of their strengths and weaknesses, thereby enabling informed value-based decisions.

6. Results and discussion

In this section, the obtained results are presented and discussed. The case study is first analyzed (Section 6.1) followed by the proposed methodology (Section 6.2). Finally, possible limitations of the approach and areas for improvement are highlighted (Section 6.3).

6.1 Case study

By applying the proposed methodology, a value model was obtained for guiding the acquisition of strategic laboratory equipment in the Mechanical Engineering Department at the Universidad de los Andes.

In light of the identified improvement opportunities in the original acquisition process (refer to Sec. 5.1), we proceed to demonstrate how the defined value model addresses these issues:

Clear values and trade-offs: a robust decision-making framework was established for guiding the equipment acquisition. Firstly, the model identifies clear objectives based on AM principles, ensuring a thorough consideration of each aspect of the decision. By categorizing the objectives into fundamental and means categories and organizing them hierarchically, the model provides a clear delineation of priorities. Additionally, to manage trade-offs effectively, the model assigns specific weights to each objective and utilizes constructed attributes in evaluating the varying levels of achievement for each objective across different alternatives.

Meaningful and reliable information: clear guidelines were established for the quantification of the achievement of the objectives through constructed attributes. These guidelines make it evident what specific information should be included in each alternative’s proposal, thus facilitating a comprehensive and standardized evaluation process.

Suitable decision models: the value model empowers the decision-makers to transcend common-sense-based approaches and make analytically sound choices by providing the robust visual representations and comprehensive insights presented in Section 5.5.

To conclude, the systematic implementation of the methodology not only effectively addressed the identified improvement opportunities but also facilitated the development of a comprehensive value model capable of guiding strategic decisions. Moreover, the implemented analysis led to a redefinition of the decision-making process within the financial committee. Initially, the model assesses the value of the alternatives, and subsequently, the final decision is made based on the computed value merit, the strengths and weaknesses of the alternatives, and the associated purchasing costs. This approach provides the financial committee with a clear understanding of the value associated with each alternative, allowing for informed budget allocation decisions. It is evident that the focus of the decision-making process has shifted to value rather than the purchasing cost.

6.2 Methodology for strategic capital investments

The proposed methodology is rooted in MCDM and AM principles, utilizing participatory processes for developing value models that guide decision-making in the context of strategic capital investments across multi-category portfolios. Next, the contribution of these elements is outlined based on the results obtained in the case study.

MCDM facilitates the formalization of strategic capital investment decision problems through the identification of objectives, the construction of objective hierarchies, and the establishment of attribute scales for their assessment. Constructed attributes, in particular, proved to be an effective approach in handling the intangible aspects of value and in operationalizing the assessment of tangible elements that would otherwise be challenging to quantify. With clear objectives and attributes in place, trade-offs are managed by integrating.

MAU and AHP, leading to the development of an intuitive model capable of assigning absolute merit to each alternative. Due to its simplicity, such a model can be built through collaborative co-creation processes.

AM principles guided the formulation of the semi-structured interview questions and the subsequent definition of objectives. The identified fundamental objectives in the case study closely resemble the value definition provided by ISO 55000 (2014). Additionally, the application of the following AM principles is evident in the constructed objective hierarchy (Figure 2):

Lifecycle orientation: the cost estimation objective encompasses considerations across the entire equipment lifecycle.

System orientation: the benefit objective quantifies the equipment’s impact on the organization’s objectives.

Risk orientation: the risk objective assesses the risks associated with the equipment’s acquisition.

Asset orientation was not directly applied, as comprehensive equipment knowledge would be obtained post purchase. Nevertheless, these principles provide a valuable framework for framing the MCDM decision problem within the context of AM.

The value model was constructed using various participatory processes, including semi-structured interviews, synchronous and asynchronous validations, and co-creation workshops. This approach fostered a shared understanding of the strategies for value creation, enhanced transparency and trust in the developed value model, and empowered employees. Given the intricate nature of AM decision-making, participation emerges as a valuable solution for incorporating the needs and expectations of the decision-makers and the various stakeholders involved in the decision.

It can be noticed that the combination of MCDM, AM principles and participatory processes proved to be effective in the development of value models able to guide decision-making in the context of strategic capital investments across multi-category portfolios. While their potential application in other AM decision-making processes appears promising, further investigation in future studies is recommended to validate their efficacy.

Finally, a significant challenge in implementing the methodology may be the perception among stakeholders that they are being singled out as guilty for past practices. This perception may hinder collaboration and impede the progress of the project. Even though the methodology introduces a value model and changes the previous decision-making process, it is crucial to avoid creating an environment where individuals feel blamed or defensive. Instead, effective communication and active involvement of all stakeholders are essential. By making stakeholders feel like creators of the new process rather than placing blame on them, we can foster collaboration and overcome obstacles to successful implementation.

6.3 Limitations and areas for improvement

Even though the methodology has proven to be effective in the case study, various areas for improvement can be identified. The primary limitations are observed in the analytical approach, which could be enhanced if more quantitative methods are needed. For instance, different approaches can be utilized to construct individual utility functions by formally modeling uncertainty and decision makers’ attitudes toward risk. Alternatively, quantitative tools can be adopted to assess the achievement of objectives within constructed attributes, such as demand analysis or simulation, among others. Therefore, the analytical approach proposed in this work may serve as a baseline that can be improved based on the complexity and importance of the decision at hand. For instance, a semi-quantitative approach, such as the one proposed in this work, may be suitable for university laboratory equipment, but a more structured approach may be necessary for critical industrial assets. In this context, the integration of MCDM techniques within AM decision-making could be beneficial and should be further investigated.

Finally, the value model was constructed based on expert judgment. Like any subjective process, some objectives may have been neglected or may not be fully aligned with the organizational strategy. Future work should introduce an approach to verify the alignment of the developed value model with the company’s strategy. In this regard, the utilization of value frameworks could be beneficial (Barbieri et al., 2024), as they describe what constitutes value for an organization in relation to achieving its organizational objectives, while also considering the needs and expectations of its stakeholders.

7. Conclusion and future work

In AM, strategic capital investments have a significant impact on the organization’s sustainability. Traditionally, financial methods were used to support decision-making. However, given the need for informed decision-making that considers multiple dimensions be-yond just financial aspects, value-based approaches have been proposed. In this context, value models capable of quantifying the impact of decisions over value become a promising approach. Nevertheless, the literature lacks value models that integrate various dimensions of value to guide decision-making in strategic capital investments.

Based on the aforementioned considerations, the aim of this study was to develop a methodology for establishing value models that can support decision-making in strategic capital investments for multi-category portfolios. To achieve this goal, an approach that integrates MCDM, AM principles and participatory processes was proposed. In particular, the AHP and MAU methods were used as analytical tools. These were complemented by the application of AM principles to frame the decision problem within the context of AM. Furthermore, participatory processes were employed to enhance transparency and trust in the developed value model and to empower employees.

For validation, the methodology was applied to a case study involving the establishment of a value model for guiding the acquisition of strategic laboratory equipment in the Mechanical Engineering Department at the Universidad de los Andes. By implementing the proposed approach, a robust value model was created, enabling the assessment of various alternatives based on the objectives significant to decision-makers and stakeholders. The approach facilitated not only the ranking of alternatives and a better understanding of their strengths and weaknesses but also the establishment of a shared concept of objectives (and attributes for their assessment) within the company for the analyzed process.

By applying the proposed methodology and developing a value model to guide strategic capital investments, companies can make more informed investment decisions that align with organizational goals, optimize returns on investment and minimize risks. This can contribute to increased profitability and long-term financial sustainability.

Given the obtained results, the following future works have been identified:

Analytical approach: the model was built in a semi-quantitative manner using constructed attributes. Consideration may be given to investigating quantitative tools for assessing the achievement of objectives within constructed attributes. Additionally, exploring different MCDM approaches could involve defining individual utility functions by formally modeling uncertainty and incorporating decision makers’ attitudes towards risk.

AM decision-making: given the effectiveness demonstrated by the integration of MCDM, AM principles and participatory processes, their potential application in other AM decision-making processes should be investigated.

Value framework: methodologies should be developed to establish value frameworks that can be utilized to ensure the alignment of the value models with the organizational strategy.