This study investigates the influence of female board inclusion (FBI) on the intellectual capital (IC)-financial performance (FP) nexus of commercial state interest entities (CSIEs).

The analysis draws on panel data from Ghanaian CSIEs covering the period from 2012 to 2021. A two-step system generalized method of moments estimator is used to assess the dynamic relationships.

IC generally enhances FP across CSIEs. Notably, FBI strengthens the IC-FP link in fully-owned CSIEs but shows no significant effect in partially-owned CSIEs. The resource-based, resource dependency and agency theories provide a suitable theoretical lens for understanding FBI’s role in this context.

The findings offer useful insights for policymakers in designing governance frameworks that promote FBI as a strategic complement to IC, potentially improving FP in CSIEs.

This study contributes to public sector literature by exploring FBI’s role in the IC-FP nexus within CSIEs. It also uniquely integrates both VAIC and MVAIC models to measure IC in this setting.

1. Introduction

Commercial state interest entities (CSIEs), also referred to as state-owned enterprises (SOEs) with commercial objectives or government business enterprises (International Public Sector Accounting Standards Board, 2022). They are hybrid organizations that combine public sector and private sector operational models. These entities play a critical role in supporting national development, with no exception to emerging and developing economies, where they complement private sector activities and contribute significantly to GDP (Bruton, Peng, Ahlstrom, Stan, & Xu, 2015; Kim, 2019; Argento, Grossi, Persson, & Vingren, 2019; Lin, Lu, Zhang, & Zheng, 2020; Abang’a, Tauringana, Wang’ombe, & Achiro, 2022; Boateng, Aboagye-Otchere, & Asare, 2025). Structurally, CSIEs can be fully-owned (100% government equity) or partially-owned (less than 100% government equity) (Grøgaard, Rygh, & Benito, 2019; Kaunda & Pelser, 2023; Boateng et al., 2025), designed to operate with private sector efficiency while fulfilling public mandates.

Despite their strategic importance, the performance of certain CSIEs (especially in developing countries such as Ghana) has often been underwhelming. Concerns raised in the State Ownership Report (SOR, 2020, 2021) and regulatory oversight mechanisms such as the State Interests and Governance Authority (SIGA), aim to ensure CSIEs’ efficient and profitable operations (SIGA Act, 2019). This context underscores the need to investigate factors that drive financial performance (FP) in CSIEs. Among such factors, intellectual capital (IC) and female board inclusion (FBI) are increasingly recognized as strategic resources.

Existing studies have shown that IC is essential for organizations (including CSIEs) ability to perform. IC system is considered a value creation mechanism that maximizes the advantage of one entity as opposed to the other or enables entities to be competitive in their own merit. Owners and managers need to be circumspect with IC in order to draw the appropriate benefits from such resources. Impactful IC assures the public or citizens of the prudent usage of public financial resources. According to Akgün and Türkoglu (2024), deciding on a good organizational strategy emanates mostly from IC and is significant for achieving a sustainable competitive edge for financial performance (FP). ICs are intangibles that cannot be decoupled from physical resources necessary for an entity’s performance (Jordão & Novas, 2017; Xu & Li, 2022). IC functions more efficiently if a robust governance framework is in place to continuously monitor it (Appuhami & Bhuyan, 2015; Van der Zahn, 2022). Importantly, while considering strong governance forms inside organizations, it will not be judicious to overlook the involvement of women on boards.

Similarly, FBI has been viewed by researchers (e.g. Ntim, 2015; Shahzad, Baig, Rehman, Latif, & Sergi, 2020; Luh & Kusi, 2023; Kabir, Ikra, Saona, & Azad, 2023; Mensah & Onumah, 2023) as having implications and mostly being an enhancer of organizational performance. Critically, one of the key indicators of Sustainable Development Goal-SDG 5 (gender equality) is to ensure female opportunities in organizational governance and decision-making (UN, 2015). Referring to Ain, Yuan, Javaid, Usman and Haris (2021), who revealed that in state-owned enterprises (SOEs), agency glitches seem to be more serious and gender-diverse boards perform better. There have been debates for and against the inclusion of females on the boards of entities. Proponents suggest that the synthesis of varying competences appropriate for organizational success and the achievement of the gender equality agenda (such as Chandler, 2016; De Vita & Magliocco, 2018; Hamplova, Janecek, & Lefley, 2022). The opponents allude to the decision challenge and the incorporation of tokenism with the inclusion of women (see Meier, 2013; Piscopo & Muntean, 2018). However, previous empirical evidence concurs with the representation of females on boards compared to those not in favour. Hence, the FBI on which this study relies consists of female board representation (FBR) and the Blau index for board gender diversity (BI).

In relation to FP, this study employed return on assets (ROA). Again, the study’s selected performance metric (ROA) is mainly related to Ghana SIGA’s primary responsibility of ensuring profitable and efficient commercial entities in which the government has an equity stake (SIGA Act, 2019). Additionally, the 2021 State Ownership Report (SOR) was consulted for the choice of the performance indicator (SOR, 2021). Notwithstanding, the choice of the performance measure was based on prior research works (e.g. Nguyen, Ntim, & Malagila, 2020; Xu, Haris, & Feng Liu, 2023; Luh & Kusi, 2023).

While prior studies have explored the relationships among IC, FBI and FP, the existing literature remains limited in several key areas. Research has primarily focused on the direct impact of IC on FP (e.g. Asare, Aboagye-Otchere, & Muah, 2022; Faruq, Akter, & Rahman, 2023; Habib & Dalwai, 2023; Majumder, Ruma, & Akter, 2023; Akgün & Türkoglu, 2024), as well as the influence of FBI on FP (e.g. Shahzad et al., 2020; Issa, Yousef, Bakry, Hanaysha, & Sahyouni, 2021; Andoh, Abugri, & Anarfo, 2023; Luh & Kusi, 2023; Mensah & Onumah, 2023). However, most of these studies concentrate on the banking sector and non-CSIEs, impeding the generalizability of their findings. Notably, there is a gap in the literature regarding the moderating role of FBI in the IC-FP relationship, particularly in the African context. For example, while Isola, Adeleye and Olohunlana (2020) investigated the effect of female board participation on IC and performance, their study was confined to Nigerian commercial banks. Similarly, other recent studies (e.g. Tiwari & Arora, 2024; Farooq & Ahmad, 2023) have focused on specific sectors, such as non-banking firms in India or non-financial firms in Pakistan. This highlights the need for a more comprehensive investigation that goes beyond homogenous sample scopes (e.g. solely banking or non-banking firms) and instead adopts a heterogeneous approach to improve the generalizability of findings. As emphasized by Barak and Sharma (2024) and Tiwari and Arora (2024), broader, more inclusive studies (heterogeneous samples) are necessary to better augment generalization when examining IC, FBI and FP. Moreover, studies around IC, FBI and FP phenomena within the CSIEs arena are underrepresented, especially from a developing country such as Ghana. To address this gap, this study examines whether FBI moderates the association between IC and FP in CSIEs in Ghana. Specifically, it investigates: the direct effects of IC and FBI on FP and the moderating effect of FBI on the IC-FP relationship. This leads to the key question: does FBI matter in the link between IC and FP of CSIEs?

The study suggests various contributions. First, the study extends public sector IC literature by integrating resource-based theory (RBT), resource dependence theory (RDT) and agency theory (AT) to explain how FBI influences the IC-FP relationship in CSIEs. Again, the Ghanaian CSIEs’ context-specific investigations of IC and FBI effects on FP benefit from the study. The study provides some evidence to support that IC is an essential driver of FP in the CSIEs when FBI is considered. Moreover, the study offers actionable insights for CSIEs’ managers, practitioners and oversight institutions (such as SIGA in Ghana) on how suitable FBI can enhance the value derived from IC. The findings can inform board composition guidelines and strategic planning across the CSIEs sector.

This is how the remainder of the paper is structured. The literature review, including theories, development of hypotheses from empirical review and conceptual framework, are presented in Section 2. Section 3 discusses the study’s data and methods and Section 4 details the results and discussion. Section 5 presents conclusion and implications.

2. Literature review

2.1 Theories

2.1.1 Resource-based theory (RBT)

Wernerfelt (1984) was the first to suggest this theory, which was later enhanced by Barney (1991). According to RBT, companies require both tangible and intangible resources in order to function well and remain competitive. Resources are thought to be special, suitable for certain businesses and difficult to duplicate (Helfat & Peteraf, 2003). Moreover, relevant resources for corporate organizations should be endogenous, which means they should be uncommon, unique and difficult to transfer (Xu et al., 2023). Furthermore, distinctive IC resources, including its capabilities, directly guarantee organizations' long-term competitiveness and success (Faruq et al., 2023; Mansour, Shubita, Lutfi, Saleh, & Saad, 2024; Saleh & Maigoshi, 2024; Khalaf, Ismail, Haat, Zakaria, & Saleh, 2024; Saleh, Alshdaifat, Shubita, Mansour, & Lutfi, 2025). Thus, the traits found in RBT are portrayed by IC resources, which provide competitiveness and appropriate value addition that will aid in meeting performance goals. RBT has been embraced by scholars (such as Isola et al., 2020; Faruq et al., 2023; Majumder et al., 2023; Boateng et al., 2025) to assert connections with performance.

2.1.2 Resource dependency theory (RDT)

This theory is associated with Pfeffer and Salancik (1978), who emphasized the importance of resources possessed by outside forces pertinent to the sustainability of entities. Additionally, the theory recognizes the board’s dependent role in cultivating connections with the stakeholders who manage the company’s essential resources (Smriti & Das, 2022). Furthermore, RDT demonstrates that having gender-diverse boards benefits companies by guaranteeing favourable relationships with the outside operating environment, which is essential for obtaining relevant and useful resources for expansion (Ain et al., 2021; Faruq et al., 2023; Majumder et al., 2023). According to RDT, having more women in the boardroom raises the possibility that they will make wise strategic decisions that enhance the performance and competitive gain of the company (Mardini & Lahyani, 2024). Existing authors (see Issa et al., 2021; Andoh et al., 2023; Luh & Kusi, 2023; Faruq et al., 2023) utilized this theory when looking at suitable links with performance.

2.1.3 Agency theory (AT)

Jensen and Meckling (1976), who proposed this theory, stated that managers (agents) are mandated by owners (principals) to handle the entities’ affairs on their behalf. In entities where the government has an ownership stake, the agents are representing the government and the people and should consider both interests. Because of these dynamics, entity boards’ monitoring function is important to enhance oversight and aid in curbing competing interests between managers and owners (Saleh et al., 2025). So, the composition of a diverse board, coupled with effectiveness and where female participation is not passive, is more capable of addressing agency issues (Nadeem, De Silva, Gan, & Zaman, 2017; Ain et al., 2021). Researchers (e.g. Issa et al., 2021; Andoh et al., 2023; Luh & Kusi, 2023) have employed this theory to posit associations with performance.

2.2 Empirical review and hypotheses development

2.2.1 Intellectual capital, female board inclusion and financial performance

Intellectual capital (IC) function more efficiently when a strong governance framework is in place to continuously monitor it (Appuhami & Bhuyan, 2015; Van der Zahn, 2022). In the current corporate governance literature, female board inclusion (FBI) has come to be acknowledged and accepted as having an impact on the performance of organizations (see Post & Byron, 2015; Mensah & Onumah, 2023; Prencipe, Boffa, Papa, Corsi, & Mueller, 2023). Essentially, it would be imprudent to ignore the participation of women on boards when contemplating robust governance structures within entities, with no exception to commercial state interest entities (CSIEs).

Prior to FBI serving as a moderating factor, as long as there is a link between the key independent variable (IC) and the dependent variable (FP), it is important to establish an association between FBI and FP from the perspective of CSIEs. According to Namazi and Namazi (2016), the moderating factor is an alternative independent variable and should be related to the dependent variable. Studies have been conducted on the interplay between IC, FBI and FP with varying findings. From the existing literature, both IC and FBI influence organizational performance (FP). For example, Asare et al. (2022) suggested a positive link between IC and FP using banks in Africa. In addition, Akgün and Türkoglu (2024) employed listed firms from 13 selected European countries to predict a positive association between IC and FP (measured as ROA). Isola et al. (2020) applied listed commercial banks in Nigeria to support the positive effect of IC on performance (measured by ROA). Moreover, Mollah and Rouf (2022) sourced listed commercial banks’ data in Bangladesh to establish a positive association between IC (i.e. VAIC) and performance (i.e. insignificant with ROA). However, authors like Mohammad and Bujang (2019) posited an adverse relationship between IC and FP of listed plantation firms in Malaysia. Regarding the connection between FBI and FP, scholars (e.g. Luh & Kusi, 2023) indicate a positive link between female participation on boards and FP (measured as ROA) of 15 listed non-financial companies in Ghana. Also, Andoh et al. (2023) asserted mixed outcomes in the link between board gender diversity (BGD) and performance (measured by ROA) using listed banks and non-financial entities in Ghana. With the banks, Andoh et al. (2023) aver an insignificant relationship between BGD and ROA. On the side of non-financial entities, Andoh et al. (2023) suggested a significant positive effect of BDG on ROA. Nevertheless, Issa et al. (2021) sourced data from banks listed in countries within the Middle East and North Africa region to reveal an insignificant positive link between gender diversity (measured via Blau index-BI) and FP (measured via ROA). Nonetheless, the association between FBI (FBR and BI) and FP (ROA) is favourable within the European countries’ context (Kabir et al., 2023). On the contrary, Fariha, Hossain, and Ghosh (2022) utilized publicly listed commercial banks in Bangladesh to allude to the significant negative effect of BGD on performance (measured as ROA). Notwithstanding, Kotte and Reddy (2023) employed listed commercial banks in India to suggest an adverse relationship between BGD and FP (measured as ROA). An insignificant effect was emphasized among the listed commercial banks in Nigeria when Isola et al. (2020) compared FBR and performance (measured as ROA). There is exiguous literature on the influence of FBI in the IC-FP nexus, especially among CSIEs. Tiwari and Arora (2024) found that BGD did not significantly influence the IC-performance relationship in Indian listed non-banking firms. In contrast, Isola et al. (2020) found that female board participation strengthened the relationship between IC components and FP in Nigerian selected listed commercial banks. These findings suggest that FBI may conditionally enhance the value derived from IC, but the effect appears to vary by context and firm type.

In CSIEs, where the dual imperatives of public interest and commercial efficiency coexist, integrating internal and external resource capabilities (resource-based and resource dependency) in advancing the performance course could be especially critical and, by extension, curtails agency glitches. As Baron and Kenny (1986) and Namazi and Namazi (2016) recommend, moderation analysis is appropriate when theoretical rationale and empirical ambiguity both exist, as in this case. Consequently, we propose the following hypotheses:

There is a positive effect of IC and FBI on FP.

FBI moderates the link between IC and FP.

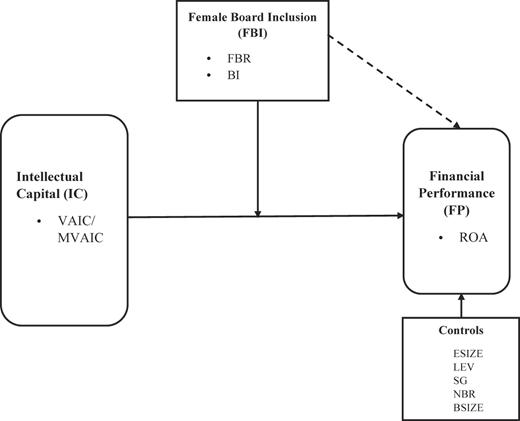

2.3 Conceptual framework

From Figure 1, the conceptual framework diagrammatically explains the relationship between IC and FP of CSIEs being moderated by FBI while controlling for other variables that are more likely to affect FP. The framework further considers FBI influence on FP, which is essential to establish prior to moderation. When looking at a moderation relationship, the connection between the moderating variable and the dependent variable should be established (Namazi & Namazi, 2016).

3. Data and methods

3.1 Data

The data were secondary and sourced from various databases, including State Interests and Governance Authority (SIGA), State Ownership Report (SOR) from the Ministry of Finance (MOF), Ghana, Ghana Stock Exchange (GSE)-Osiris and the chosen firms’ websites through annual reports (mostly audited annual financial statements). The study covers 71 CSIEs (35 fully-owned CSIEs and 36 partially-owned CSIEs). The chosen entities and the set period coverage (2012–2021) were based on data availability, which agrees with existing literature (Aboagye-Otchere & Boateng, 2023; Boateng et al., 2025). In addition, the motivation for the 10-year span (2012–2021) was drawn from Rashid (2020) and Boateng et al. (2025), who alluded to the fact that a time scope above five years within datasets may enhance the generalizability of the study. Moreover, with the aid of SIGA-2020-SOR, the sectoral categories of the selected CSIEs consisted of infrastructure (4), energy (10), financial and allied (13), transport (7), manufacturing (8), communications (5), agriculture (11) and mining (13).

3.2 Methods

3.2.1 Variables description

The variables description, which gives the measurement of the variables, are shown in Table 1.

3.2.2 Model specification

In addressing the objective of this study, the dynamic model was employed through a two-equation approach, which was assisted by prior literature (Isola et al., 2020; Ofoeda, Agbloyor, & Abor, 2022; Aboagye-Otchere & Boateng, 2023; Habib & Dalwai, 2023).

where

= financial performance, = lag factor of financial performance, = intellectual capital, = female board inclusion, = interaction influence, = control variables, , = intercept/constant, = error terms, = cross-sectional against time series dimensions and = cross-section of sectors.

3.2.3 Estimation technique

The role of FBI in the link between IC and FP of CSIEs in Ghana was discovered by the application of dynamic panel regression analysis. The generalized method of moments (GMM) estimation approach, which was initially put forth by Arellano and Bover (1995) and later enhanced by authors (such as Blundell & Bond, 1998; Roodman, 2009), is ideal for linear dynamic panel models. This estimator is capable of dealing with probable endogeneity problems, heteroscedasticity and serial correlation, including unobserved individual heterogeneity, which are somehow popular in panel datasets (Saleh & Maigoshi, 2024; Saleh et al., 2025; Boateng et al., 2025). This study specifically benefits from the two-step system generalized method of moments (SGMM) due to its strong efficiency and consistency, as well as the feature that permits more data points to be used during estimation (Majumder et al., 2023; Mansour et al., 2024; Boateng et al., 2025). Using the two-step SGMM estimator, both levels and differences can incorporate lagged dependent variables and lagged endogenous variables (Majumder et al., 2023; Mansour et al., 2024). Furthermore, it allows for the measurement of only exogenous components at levels and in differences (Kalash, 2023; Mansour et al., 2024; Boateng et al., 2025). Existing studies (e.g. Dalwai & Sewpersadh, 2023; Majumder et al., 2023; Assfaw & Sharma, 2024; Boateng et al., 2025) utilized this estimator when establishing connections.

3.2.4 Pre-estimation diagnostics

Prior to estimation, endogeneity, multicollinearity, heteroscedasticity and serial correlation were all assessed to provide assurance for the study’s outcome. The diagnostic test for endogeneity using the Durbin-Wu-Hausman test for endogeneity (see Appendix A) has shown the existence of endogeneity with reference to the p-value (0.0001). Again, to assess whether any of the independent variables are highly correlated, a test for multicollinearity was performed. From Pearson’s pairwise correlation matrix (refer to Table 3), it generally indicates low degrees of association among the independent variables. Moreover, checks from the result reveal the presence of heteroscedasticity. The modified Wald test for groupwise heteroskedasticity (see Appendix A) was performed using the independent variables. The null hypothesis (constant variance) was rejected, as evidenced by the incredibly significant p-value (0.0000). Furthermore, a serial correlation test was conducted by employing the Wooldridge test for autocorrelation (see Appendix A). The serial correlation p-value of 0.0918 thinly suggests the presence of autocorrelation, which contradicts the null hypothesis (no first-order autocorrelation). Consequently, the two-step system GMM estimator becomes the preferred choice in this study.

4. Results and discussion

4.1 Descriptive analysis

The descriptive results of the entire, fully-owned and partially-owned samples ascertained in this study are summarized in Table 2. The average performance (ROA) from the different samples is reported as −0.87%, −2.14% and −0.63%. Profit (ROA) generation is a challenge for CSIEs, but this is more evident with fully-owned firms. Additionally, the mean values of the key IC variable (VAIC) for the study are 3.3857, 2.6031 and 4.0493 for ES, FOS and POS, accordingly. This signifies that for every unit of money employed, the entities create an average addition of 3.3857, 2.6031 and 4.0493. The MVAIC, which represents the confirmation of the VAIC approach, reported average values of 3.4101, 2.6252 and 4.0752 for ES, FOS and POS, respectively. On the side of the moderating variables (FBR and BI), the mean values of FBR for ES, FOS and POS are approximately 20%, 25% and 15%, respectively. Although there are broadly few women represented on entities’ boards, it is more pronounced in POS compared to FOS. Moreover, BI indicates the balance in gender difference or gender equality on the entities’ boards and shows average values of approximately 26%, 32% and 20% for ES, FOS and POS, respectively.

4.2 Correlation analysis

Table 3 depicts the results of the Pearson’s correlation and variance inflation factor (VIF). To ascertain whether a high correlation between the explanatory variables would result in multicollinearity and a skewed estimation outcome, Pearson’s pairwise correlation was run. The low correlation coefficient in the correlation results suggests that almost all of the independent variables are not highly correlated, indicating that multicollinearity is not a major problem and allowing for the regression estimation. Although the strongest correlation coefficient of 0.876 is between two control variables (NBR and BSIZE), it is below the prior literature (see Tabachnick & Fidell, 1996; Haniffa & Cooke, 2002) stated criteria of 0.90 or above. Notwithstanding, the VIF of the variables falls within the acceptable threshold (that is, less than 10).

4.3 Regression analysis

Using regression analysis, the forecasted connection of the role of FBI in the IC-FP nexus was investigated across the selected CSIEs. The findings for the three (3) primary CSIE samples (entire, fully-owned and partially-owned) are displayed in Tables 4 and 5 by applying the baseline estimator, the system generalized method of moments (SGMM) and, particularly, the two-step method. The p-values were statistically significant at the 1% (0.000) level with regard to the overall fitness of the regression models, as determined by the Wald Chi-squared statistic (Tables 4 and 5). This demonstrates that the regression models are reliable and stable.

Table 4 discloses the empirical results of intellectual capital (IC, measured via VAIC), female board inclusion (FBI, operationalized through female board representation–FBR–and Blau index for board gender diversity–BI) and financial performance (FP, measured as ROA) across the sampled entities category: entire sample (ES), fully-owned sample (FOS) and partially-owned sample (POS).

The findings consistently indicate a positive and statistically significant relationship between IC and FP across all samples (ES, FOS, POS), aligning with previous studies (such as Isola et al., 2020; Asare et al., 2022; Faruq et al., 2023; Akgün & Türkoglu, 2024; Boateng et al., 2025). This supports the resource-based theory (RBT), which posits that unique internal capabilities (such as intellectual capital) can provide a sustainable competitive advantage. In the context of CSIEs, this suggests that strategic management of intellectual assets is instrumental in improving firm-level efficiency and returns.

However, the association between FBI and FP yields heterogeneous outcomes across the sampled entities. In the ES and POS, FBI has a negative (ES: insignificant; POS: significant) effect on FP, which contrasts with the positive and significant effect observed in FOS. These mixed results are consistent with some prior findings (e.g. Isola et al., 2020; Fariha et al., 2022; Andoh et al., 2023), but they call for deeper contextual interpretation. The adverse outcomes in POS may reflect structural challenges in integrating female directors meaningfully into governance processes. Cultural norms, some tokenism or entrenched patriarchal board dynamics could probably undermine the potential benefits of board gender diversity. This limits the efficacy of resource dependency theory (RDT) and agency theory (AT) in such settings, as these frameworks assume that diverse boards can effectively leverage external resources and monitor managerial decisions. In contrast, the positive FBI–FP link in FOS may reflect more institutionalized diversity practices, such as stronger compliance with board gender encouragement policies or better alignment between female directors’ qualifications and strategic board roles. This aligns with studies such as Shahzad et al. (2020) and Luh and Kusi (2023), which emphasize the importance of context and capacity in determining the effectiveness of board diversity.

Substantially, the study examined the moderating effect of FBI on the IC-FP connection. Results reveal an insignificant positive effect when FBI moderates the IC-FP nexus (similar to Tiwari & Arora, 2024) for ES and POS. This result posits the non-existence of an effect on FP when IC interacts with FBI, implying a net effect of zero. Also, the moderation or conditional effect of FBI on the association between IC and FP is positive and statistically significant for FOS. This finding is in tandem with that reported by Isola et al. (2020). The result implies that in FOS, female board presence enhances the positive effect of IC on FP–suggesting a synergistic interaction between internal and external resources and governance mechanisms. This supports an integrated view of RBT, RDT and AT, indicating that when the quality and depth of board diversity are substantive (such as in FOS with qualified and empowered female board members), external and internal resources are better mobilized, managerial oversight is stronger and performance outcomes improve. This further highlights that the RBT, RDT and AT become relevant in this context because internal and external resources can be leveraged and by extension, curtail agency glitches (including the probable public confidence emanating from the judicious investment of public funds). These findings also lend support to quota-based interventions emphasized in Hamplova et al. (2022), suggesting that institutional mechanisms can enhance the functional impact of diversity. Notably, while earlier studies like Isola et al. (2020) and Tiwari and Arora (2024) adopted single-theory perspectives (RBT and RDT, respectively), this study applies a triangulated theoretical framework (RBT, RDT and AT). This approach strengthens the explanatory power of the results by recognizing the interplay between internal capabilities, governance structures and access to external resources (Jacobs, 2012). Thus, rather than seeing RBT, RDT and AT in isolation, this finding demonstrates how their combined explanatory capacity is essential for understanding the complex dynamics of IC, board diversity and FP in public-sector contexts (specifically, CSIEs).

Finally, Table 5, which reports robustness checks using Modified VAIC (MVAIC), confirms the consistency of the findings. The similar results between VAIC and MVAIC estimations validate the reliability of the conclusions drawn and reinforce the theoretical insights offered by this study.

5. Conclusion and implications

This study examined the moderating role of female board inclusion (FBI) in the connection between intellectual capital (IC) and financial performance (FP) among 71 commercial state interest entities (CSIEs) in Ghana, comprising 35 fully-owned and 36 partially-owned, over the period 2012–2021. Using a dynamic panel model with a two-step system GMM estimator, the findings confirm that IC positively influences FP across all entities. However, FBI enhances FP in fully-owned CSIEs but shows a declining effect in partially-owned CSIEs. Crucially, FBI strengthens the IC-FP relationship, especially in fully-owned CSIEs, indicating its differential effect based on ownership structure. The findings underscore the significance of ownership context in leveraging board gender dynamic for performance gains.

Certain implications (research-theoretical, practice and policy) become substantial from the study. First, this study advances the literature on IC and FP by applying a triangulated theoretical framework (resource-based theory-RBT, resource dependence theory-RDT and agency theory-AT) to investigate the moderating role of FBI within CSIEs. By leveraging these complementary theories, the study offers a more holistic understanding of how board gender dynamic influences the IC-FP nexus, particularly in the under-researched public sector. Importantly, the study addresses a key gap in the literature by examining both fully-owned and partially-owned CSIEs. The findings reveal that the impact of FBI on the IC-FP linkage varies by ownership structure, with evidence indicating that an average FBI level of approximately 25% to 32% is apt for enhancing FP through IC, especially in fully-owned CSIEs. This finding not only extends the theoretical relevance of the applied frameworks but also identifies ownership structure as a critical variable warranting deeper exploration in governance-performance models. Second, for practitioners, owners (like the government) and managers within CSIEs (particularly, fully-owned), the findings suggest evidence-based guidance on how gender-diverse boards can be strategically leveraged to enhance the impact of IC on financial outcomes. Specifically, maintaining approximately an average minimum of 25% to 32% female board participation appears suitable for enhancing the performance returns from IC investments. This awareness can inform board recruitment practices and broader human capital development strategies. Interested parties (e.g. the owners and managers) are encouraged to foster synergies between diverse board compositions and IC initiatives to maximize organizational performance. Emphasis should also be placed on developing IC in a manner that complements the governance capacities of a gender-diverse board. Third, the study provides actionable insights for policymakers (like regulators or oversight institutions) responsible for CSIEs. The findings underscore the importance of promoting meaningful FBI as a lever for improving FP through more effective IC utilization. To this end, policymakers might consider implementing incentivized frameworks that support gender diversity on boards (without compromising qualifications). Such frameworks could align with the content of SDG 5 (gender equality) by ensuring that women are adequately represented in organizational governance and decision-making roles. By doing so, policy initiatives can foster a governance environment where IC is more effectively utilized, contributing not only to better FP but also to more inclusive and equitable organizational practices.

Notwithstanding, there are some limitations to this study that create the chance for further investigation. To begin, the study relied on data from one jurisdiction and the same can be replicated elsewhere. Again, conducting cross-national research will add to the existing suggestions. Moreover, an identical study can be done, and the attention will be on the individual sectors within the CSIEs in order to complement this one. Lastly, the dynamics of the periods of the quota and non-quota systems of FBI can be interlinked with IC and FP in future studies.

The supplementary material for this article can be found online.