This study aims to examine how auditors’ attitudes towards responsibility shape the possibilities for using artificial intelligence (AI) within the auditor risk assessment process (ARAP).

Using an affordance lens and abductive approach, the authors deconstruct human actions into avoidance and arrangement, applying these frameworks to structured interviews with auditors.

Possibilities are filtered through responsibility. Moreover, the authors identify a non-linear relationship between the attitudes towards responsibility and algorithms.

The study focuses solely on the auditor’s perspective, while further research should include other stakeholders. The findings highlight a potential systemic policy risk should AI adoption challenges remain unaddressed.

By linking algorithm aversion to distributed responsibility, this study offers fresh insights into human–AI interactions and contributes to the understanding of barriers to AI adoption in professional services.

1. Introduction

Artificial intelligence (AI) is rapidly permeating various aspects of modern life, echoing the transformative impact of the internet in the early 1990s. As human interaction with AI expands, our understanding of these interactions remains limited, with this knowledge gap creating uncertainty, which hinders both social and economic progress. Given AI’s growing role in auditing practices, a comprehensive examination of the Audit Risk Assessment Process (ARAP) and its intersection with AI is crucial for research and practice.

The ARAP involves identifying and evaluating the risk of material misstatement in financial statements, requires the professional judgement and expertise of a responsible auditor and their team and is subject to scrutiny by supervisors, self-regulatory bodies and other stakeholders.

Auditors’ actions are shaped by a range of possibilities understood through an affordance perspective. These possibilities are, however, bounded by auditors’ attitudes towards algorithms and perhaps their perceptions of responsibilities.

We define responsibility as the duty or obligation to complete a task or perform a role. The human responsibility is solely assigned to humans, while the distributed responsibility cannot be directly exhaustively or unambiguously attributed to a human being, and might relate to humans and AI systems, or solely to AI systems. Attitudes towards responsibility and algorithms can vary significantly. Individuals may assume full responsibility for AI actions, delineate boundaries between human and AI responsibility or distribute responsibility among multiple human actors. Similarly, individuals may exhibit algorithm aversion or appreciation, influencing their decisions to avoid or engage with AI. While algorithm attitude provides insights into how auditors emotionally and cognitively respond to AI, the central focus of this study is on the responsibility–possibility link.

Existing accounting and auditing literature suggests a prevalence of algorithm aversion in AI adoption (Commerford et al., 2022; Lombardi et al., 2021), although it demonstrates reduced attention to the interrelation between possibilities and responsibilities.

Consequently, this study aims to examine auditors’ attitudes towards responsibility and the possibilities for applying AI in ARAP. Drawing on prior research (Califf et al., 2020; Faraj and Azad, 2012; Fayard and Weeks, 2014; Gibson, 1977; Salijeni et al., 2021), we use the affordance that incorporates a motivational dimension (Steffen et al., 2019). Thus, we define affordances as the possibilities for action available to actors, constrained by auditor motivations.

We map auditor arguments for and against AI applications in the ARAP, decomposing the action into two concepts: avoidance (lack of application) and arrangement (application). We used qualitative research methods. We conducted structured interviews with auditors, identified their perspectives on AI utilisation and coded their arguments. Focusing on Polish auditors, we aimed to broaden the scope of existing studies, which predominantly focus on the Anglo-Saxon perspective.

This study contributes to the ongoing discussion regarding the advantages and disadvantages of AI in auditing (Commerford et al., 2022; Dyball and Seethamraju, 2022; Eilifsen et al., 2020; Landers and Behrend, 2022; Lehner et al., 2022; Salijeni et al., 2021) by demonstrating that possibilities are framed by the attitudes towards responsibility (Agostino, Bracci, et al., 2022; Lombardi et al., 2021) that interplay with algorithmic attitude. Specifically, human responsibility is linked to algorithm aversion, while algorithm appreciation is a key factor differentiating AI adoption.

The remainder of the paper is structured as follows. Section 2 reviews the literature. Section 3 explores the theoretical approaches. Section 4 outlines the research design, while Section 5 presents the findings. The last section provides a discussion and conclusions.

2. Literature review

Studies have examined human–technology relations in accounting and auditing (e.g. Moura and Bispo, 2020; Bracci, 2022; Dyball and Seethamraju, 2022). In auditing, AI influences both how audits are conducted and how auditors assess clients’ AI systems (Commerford et al., 2022; Ding et al., 2020). Prior research highlights AI’s benefits and risks (Lombardi et al., 2021; Zhang, 2019), as firms face fee pressure, quality demands and resource constraints (Fedyk et al., 2022; Gepp et al., 2018).

AI enhances accuracy and efficiency – for instance, through drone-assisted stocktakes (Christ et al., 2021) and automation that enables more advisory work (Kokina and Davenport, 2017). The application of AI into the ARAP touches on various areas, from human–machine interaction to the interpretation of data, with AI acting in ways that emulate humans (Huang and Rust, 2021; Noor et al., 2022; Park et al., 2021), affect human decisions (Arnaboldi et al., 2017), outperform humans in complex information processing (Liu, 2022) and redefine the human response to technology, calling for reshaping the ethics framework (Almufadda and Almezeini, 2022; Munoko et al., 2020; Vitali and Giuliani, 2024). Yet, persistent AI-related risks, including algorithm aversion and unclear responsibility boundaries, constrain auditors’ ability to fully explore and realise the possibilities offered by AI in audit practice.

Responsibility is traditionally understood as reflecting an individual’s connection to an event (DeZoort and Harrison, 2018, p. 861), often highly personalised to what is termed “individual responsibility” (Nikidehaghani et al., 2023, p. 698). Both perspectives centre responsibility around human actors, which we refer to as “human responsibility”. However, with the advent of AI systems – capable of making decisions and executing tasks without human supervision – this traditional concept of responsibility is increasingly challenged. AI’s autonomy introduces complexity in assigning responsibility, as actions and outcomes may no longer be directly attributed to a single human. To address this tension, we propose the concept of “distributed responsibility”, where responsibility is either shared between humans and AI systems or attributed to the AI systems’ autonomy.

The rise of complex AI creates “responsibility gaps”. For example, developers could face a gap due to discrepancies between their intended purpose and the algorithm’s actual behaviour and outcomes (Mittelstadt et al., 2016), which can be seen as a transfer of ethical responsibility to the technology itself (Lehner et al., 2022).

Responsibility is linked to the governance framework, and the emergence of AI as an autonomous decision-making system strains the concept of responsibility. The literature generally agrees that responsibility lies with humans (Bracci, 2022; Vesa and Tienari, 2022), but acknowledges that treating AI merely as a tool creates a disjunction between performing a task, explaining its execution and attributing responsibility (Agostino, Saliterer et al., 2022; Bracci, 2022). Given AI’s complexity and development by many specialists, actions and errors cannot be clearly linked to a single individual, especially when systems self-configure or modify their own code (Birchall, 2015).

Auditors thus adopt two positions: viewing AI as a tool with full human responsibility, or seeing it as partially responsible due to its autonomy, leading to distributed responsibility. Their attitudes towards algorithms further shape AI adoption, showing algorithm aversion or appreciation.

Some research reveals algorithm aversion, where individuals underuse algorithms even when they are superior to humans (Dietvorst and Bharti, 2020). Others document the opposite: algorithm appreciation, where humans over-rely on AI (Logg et al., 2019). Factors contributing to aversion include ethical concerns (Bigman and Gray, 2018), perceived limitations in understanding human nuances (Longoni et al., 2019), lack of transparency (Lebovitz et al., 2022) and the level of understanding of the input data (Commerford et al., 2022).

Commerford et al. (2022) demonstrated that algorithm aversion in auditors’ judgements is linked to credibility concerns and moderated by the characteristics of information sources. If auditors consider information sources to be more objective, algorithm aversion is moderated. The authors therefore find that auditor susceptibility to AI algorithm aversion could prove costly for the profession and financial statement users.

Although research confirms both the existence of algorithm and responsibility attitude effects, the precise causal relationship between them in the context of AI–human interaction remains unclear.

The relationship between audits, responsibility and algorithms creates a hidden layer requiring a conceptual framework that integrates observable and hidden dimensions. The affordance theory supports this, suggesting that actions depend on material configurations that reveal possible options. Thus, auditors’ decisions to use AI depend on how risks are recognised (e.g. inclusion of AI risks in audit models), while responsibility and algorithmic attitudes form interacting layers within these affordances.

Consequently, we put this relationship in the ARAP context to explore both motives, and frame it through affordances. This abductive framing guides the conceptual approach outlined in the next section.

3. Theoretical approach

Gibson (1950, p. 198) introduced the concept of affordance, defining it as what an environment offers, provides or furnishes for either benefit or harm (Gibson, 1979), a concept that has been applied to understand how technology transforms business practices (Bérard, 2014; Fayard and Weeks, 2014; Hultin and Mähring, 2014), including within institutional settings (Pollock and D'Adderio, 2012).

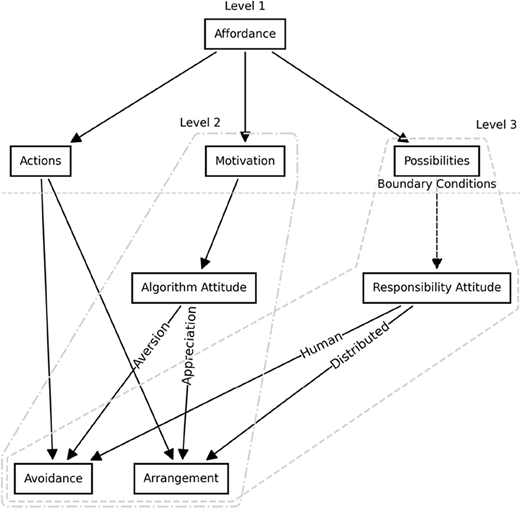

This study adopts and modifies the affordance framework proposed by Steffen et al. (2019) which emphasises the importance of framing affordances in terms of human motivations. Affordances are defined as the action possibilities available to actors within their environment (Heras-Escribano, 2019, p. 3), conditioned by human motivation (Steffen et al., 2019), and therefore the core relationship explored here is the interplay between possibilities, motivations and actions that constitute an affordance – the first level of analysis in this study (see Figure 1).

Actions are categorised into avoidance (lack of action) and arrangement (engagement with AI and attempts to apply it to the ARAP[1]).

Figure 1 shows the basic affordance framework possibilities-action, which we extend after Steffen et al. (2019), introducing motivation as a conceptual moderator. At Level 1, affordances enable actions; at Level 2, motivation operationalised through the algorithmic attitude – mediates this link. Level 3 adds the responsibility attitude, which constrains or expands the set of possible actions. Thus, possibilities define the boundary of both attitudes. Figure 1 illustrates this decomposition and highlights the key potential responsibility → possibility relationship.

We position this study within an abductive approach. While the first and second-level structure was theoretically given in the literature, the responsibility attitude emerged. It was only through recurrent comparison between empirical findings and the evolving conceptual model that the interdependent structures forming the third levels were identified. Finally, the relative strength of these interdependencies was inferred from the data, constituting the central theoretical contribution of this study.

Drawing on the discussion in Section 2, we suspect that algorithm aversion and the desire for human responsibility stimulate avoidance behaviours, while appreciation for algorithms and a sense of distributed responsibility encourage arrangement behaviours. Furthermore, this structure suggests a potential link between attitudes towards responsibility and algorithms, possibly reducible to a single factor.

As the virtual reality context is too far from AI, we excluded the predefined possibilities as reported by Steffen et al. (2019); instead, we reconstructed possibilities from the arguments used by the auditors to support their actions.

4. Research design

4.1 Structured interviews

Moura and Bispo (2020) identified interviews, observations (including shadowing, zooming in and out), films, photos and archives as potential methodologies in sociomaterial-based studies, while we opted for interviews, as other techniques were inaccessible due to confidentiality restrictions on audit/supervisor file documentation. We developed the interview template based on prior research, professional literature, discussions with practitioners, a pilot test and the practical experience of one of the researchers, although the interview’s focus on human agency limited the exploration of non-human agency.

We mitigated non-human agency limitation by incorporating a visual aid. Following Hultin (2019), who used a photo elicitation technique, we concretised the intangible ARAP process into a visual “equation’” (compare Appendix online Panel B supplementary online material). Capturing auditors’ initial attitudes towards the algorithms we investigate their views on AI responsibility, yielding on responses focused on AI use in ARAP and revealing underlying attitudes towards algorithmic responsibility. At the same time, we do not examine how auditors audit the AIs used by the auditee, as this goes beyond the purpose of this study.

During the pilot phase, respondents expressed discomfort with the interview format when combined with doubling (a coaching presentation technique) or AR process mapping, as suggested by Moura and Bispo (2020). Consequently, we were unable to fully address the potential role of materiality in the discourse.

We considered unstructured (questions not prepared in advance), structured (all questions predefined) and semi-structured (some questions predefined) interviews, with the pilot phase revealing that respondents in unstructured interviews tended to focus on the most recent or impactful experience, often drifting outside the specific context of ARAP and AI. This study therefore used a structured interview instrument with closed- and open-ended questions to ensure consistency, reliability and generalisability.

Closed-ended questions provided a mechanism for controlling the internal consistency of interviewee responses, while open-ended questions formed the core of the data collection. We presented the extended AR model to respondents, posing questions that avoided direct references to specific concepts under investigation, with two additional questions included for snowball sample participants to cross-check consistency across samples. The interview instrument was designed to avoid direct questions about auditors’ algorithms and responsibility attitudes in the ARAP process to minimise confirmation bias. An hourglass questioning strategy was used, progressing from broad inquiries to specific questions and concluding with open-ended prompts, with the protocol applied to all interviews. The study received ethical approval from the Ethics Committee of the SGH Warsaw School of Economics. Initially, invitations with basic information about the purpose, method and timing of the study were distributed to a random cohort of Polish registered auditors, who confirmed their participation and signed consent forms before each interview, with assurances of anonymity, voluntary participation and the right to withdraw at any stage. Structured interviews were conducted online, averaging 35 min in duration. Participants were invited via e-mail or telephone, with one follow-up reminder; non-respondents were not contacted further. In a few cases, interviews were rescheduled due to technological or personal constraints, primarily vacation-related, and some participants provided written explanations for unavailability, most often citing prior AI experience or vacation commitments. Interviews began with general questions about AI approaches and then focused on the risk assessment process, and each transcript was reviewed multiple times, with finalised versions sent to the interviewees for approval.

4.2 Interviewee data

The study’s sampling population differs from prior research (Eilifsen et al., 2020; Fedyk et al., 2022;Salijeni et al., 2021), which interviewed the Big Four and middle-tier audit firms. To mitigate technological and operational bias, we sampled auditors [2] from diverse roles (including quality control, supervisory and research) within organisations of varying sizes.

This study uses data from a larger project, “Friction perception of the application of artificial intelligence to auditors’ risk assessment processes”. We analysed data from 41 interviews conducted with auditors, with a structured interview instrument (Cerbone and Maroun, 2020; Malmi et al., 2020) used for all respondents, which was pre-tested, cross-validated and finalised with the agreement of all authors. Interviews were conducted between August 2021 and August 2022. Structured interviews and participant-verified transcripts ensured the reliability of the data.

A hybrid sampling approach combined stratified sampling (August to October 2021) for balanced auditor representation and snowball sampling to mitigate self-selection bias among AI audit experts (Russano et al., 2014). Data saturation emerged progressively during the data collection process, becoming apparent after around 33 interviews. We therefore stopped recruiting new respondents. The study concluded with 41 interviews in total, including 23 follow-up interviews conducted in July to August 2022 to complete thematic coverage (Lodhia, 2019; Malsch and Salterio, 2016; de Villiers et al., 2019).

Video-recorded interviews via MS Teams were conducted in Polish, with informed consent obtained beforehand and the transcripts independently analysed by multiple researchers, ensuring data quality through clarifications of ambiguities, response probing and participant verification. Even brief interviews (less than twenty minutes) provided targeted, meaningful responses, allowing us to infer consistent patterns across participants and supporting the development of grounded insights. We cross-checked findings for diversity in work experience, organisational size and gender. Data were stored securely, and identifiers were removed to protect confidentiality.

4.3 Coding and pattern extraction

Interview data were coded following established qualitative research methodologies (Mihas, 2023; Vaismoradi et al., 2013). In the first stage, interview transcripts were read, with initial codes assigned to three action constructs – avoidance, substitution and arrangement (Figure 1), focusing on responses to questions 8–9 (Appendix online, supplementary material). Respondents lacking prior or current AI experience were coded as “avoidance”, while those with both types of experience were coded as “arrangement”. In mixed responses, a judgement between “arrangement” and “substitution” was made based on the overall context of the free-text explanation, with inter-author reconciliation of the interview context.

Algorithm and responsibility attitudes were coded using four codes: algorithm appreciation, algorithm aversion, human responsibility and distributed responsibility, an approach that facilitated direct coding for level two decomposition.

For level three decomposition, an open coding strategy was used, with an initial set of codes developed and applied to the data after thoroughly reading the interviews. However, open coding was also incorporated, allowing for the emergence of new codes as needed, with sub-codes created when the direction of the argumentation was relevant. For example, “Alternative High” indicated that the respondent argued for the existence of an alternative solution to AI application, while “Alternative Low” stated the absence of such a consideration. Maxqda software was used for coding and statistical analysis.

Coding was initially conducted by a single researcher using a structured codebook developed through iterative pilot testing. To enhance rigour, segments of the coded data were reviewed in pairs by a second coder, and two additional authors independently verified the coding framework, achieving 89% agreement; discrepancies were resolved through collaborative discussion. Following reviewer feedback, a post hoc reliability assessment was conducted: a separate team of researchers independently coded 20% of the interviews (randomly selected). Inter-coder reliability was calculated using Krippendorff’s Alpha (α) between the original coder and the independent team, yielding a score of α = 0.91, indicating substantial agreement.

The entire team reconciled findings to mitigate personal bias (Gothberg and Sterenberg Mahon, 2023; Mihas, 2023), ensuring that naturally occurring arguments were captured comprehensively (Lune and Berg, 2017, p. 90), with a latent perspective adopted, focusing on the interviewee’s most plausible meaning rather than specific terms. Coding in Maxqda was recursive, allowing for merging, splitting and the reassignment of codes until consensus was achieved. For instance, a statement like R25, “I took part in the EU in the implementation of robotisation in systems or combining non-integrated financial and accounting systems”, was coded, either exclusively or collectively, as “Expertise”, “Awareness” and/or “Experience”, based on the context (in this case, “Expertise” and “Awareness”). After cross-checking, the final set of detailed codes was agreed upon (Guthrie et al., 2004). The final code list and definitions are presented in Appendix.

The relationships between motivation and actions, as well as among motivation and possibilities, were investigated, while patterns emerging from the coded argumentation and auditors’ motives were analysed, and qualitative observations were cross-checked against the code correlation structure [3].

The results were reviewed in relation to existing literature, and the intermediate findings were shared with colleagues and at seminars (Steccolini, 2022). Potential limitations related to cross-sectional or temporal biases were addressed through non-statistical resampling and recoding, with a rigorous analysis including multiple readings, cross-checking and code aggregation. It is acknowledged that the interpretation and selection of illustrative quotes remain subject to researchers’ judgement.

5. Results

The auditors in our sample have an average of 18.4 years of professional experience (Table 1, Panel A). They are all highly educated; 73% have prior experience with AI, 37% currently use AI and approximately half have experience with AI in audits (Table 1, Panel B).

The majority of respondents work for small- and medium-sized firms, representing a gender-balanced sample, and all respondents answered all the questions except one. The auditors remain confident in excluding AI from the ARAP, as AI-related factors receive less attention than inherent detection and control risk – despite acknowledging AI’s impact on AR (compare Tables IA and IIC in Appendix online, supplementary material). This potential inconsistency aligns with narrative-based empirical findings.

We present our findings further by referencing the decomposition level (Figure 1).

5.1 Level one

At level one, the basic answer to our research question “How does the attitude towards responsibility impact possibilities in the AR assessment process?” is twofold. First, possibilities are constrained by responsibility. Second, motivation, shaped by attitudes towards algorithms, interplays with responsibility attitudes. It influences actions primarily through algorithm appreciation. To uncover this relationship and support our findings, we must examine the second-level disaggregation interplay.

5.2 Level two

We identified two major channels through which attitudes influence action. The first is the interrelation between human responsibility and algorithm aversion; the second is the transfer of algorithm appreciation into action, namely, into the arrangement.

5.2.1 Human responsibility and algorithm aversion.

Auditors primarily frame their arguments about human responsibility in contrast to algorithm aversion, expressing scepticism about the diffusion of responsibility. When asked directly about the possibility, they generally deny such a feature (R19, R21, R40, R41), with one auditor stating, “It is science fiction. At this point, there is no such option, a human being must answer” (R40-Q14). This scepticism is linked to concerns about potential algorithm manipulation: “If someone can use the results, they can manipulate the batch data” (R40-Q9). In some instances, auditors personify the algorithm, as in the comment, “It has a saving on research time or people, but it runs the risk of that stupid computer going crazy” (R32-Q12a). At the same time, they highlight the risk of diminished human oversight: “Yes, because it frees a person from thinking” (R32-9). Human responsibility is often justified from ethical and purposive perspectives: “In general, the problem is who will create artificial intelligence and for what purposes. The intentions of the creator are important, with regard to how ethical and honest (the creator) is” (R13-9). This concern is further reinforced by the risk of humans losing control over the algorithm’s execution: “AI is dangerous – for the reason that if we make a mistake, we can lose control over it” (R13-Q16). Others also share this argumentation (R3-12, R15, R19-R36, R39-41).

5.2.2 Algorithm appreciation and arrangements.

A higher level of algorithm appreciation among auditors drives the arrangement of AI within audit processes, with this appreciation often expressed in relation to hardware capabilities: “A computer can replace a human being to some extent and in an instant analyse millions of data sets that a human being would spend several weeks, several months on…” (R28-Q16). This view is similar in others (R1-10, R13, R17-18, R20-21, R23, R25-26, R37-39, R41). Less frequently, it is directed towards software: “It seems to me that artificial intelligence will be used in accounting programmes, and auditor support programmes. For sure it will be, I don’t know how fast, but it is a natural process, just like the transition from paper ledger documents to electronic ledgers in computers” (R37-Q10).

We observed a consistent positive cross-motive pattern between algorithm aversion and human responsibility, as well as a consistent relationship between algorithm appreciation and distributed responsibility, suggesting that algorithm and human responsibility attitudes are non-linearly related.

5.3 Level three

We instrumented possibilities with the respondents’ arguments for and against applying AI in the ARAP. Possibilities that drive the attitudes towards algorithms include Oversight, Regulation, Control, Predicted Adjustment, Interaction, Reaction, Replicability, Amorphism, Complexity, Judgemental Alternative, Awareness and Self-adjustment. Responsibility is affected by Judgement, Answerability, Awareness, Self-Adjustment and Correction, although they impact algorithm aversion, appreciation and human and distributed responsibility differently.

5.3.1 Algorithm appreciation and aversion.

The perception of a robust regulatory framework (Regulation [4]), combined with the lower effort to execute control over AI (Control Low), stimulates algorithm appreciation, with auditors acknowledging the need for regulatory and supervisory institution involvement. “So for sure the main role I see here is with the PIBR[5] as an institution that takes care of us – auditors” (R23-Q15). However, they often admit lacking control skills – “not sure how it works” (R23-Q9), similarly to the others (R1, R6, R13, R19, R25, R29).

The existence of the authorities’ attitude to AI applications (Awareness High or Low) moderates algorithm appreciation, as the auditors account for uncertainty generated by the institution involvement: “Perhaps the proposal to expand the scope of audit risk to include auditor and client risks will meet with the approval of the PIBR and auditors, but we should not rule out that artificial intelligence risk will be an element of inherent risk that will increase” (R16-Q12a).

Auditors report that AI’s existence drives them to adjust their behaviour, resulting in enhanced algorithm appreciation (Predicted Adjustments): “Without AI, I cannot deal with AI at the customer’s site” (R13-Q10) as well as (R5-R6).

While AI exhibits internal interactions (Interaction), recognises the auditor (Reaction) and demonstrates explainability (Replicability), auditors may still fail to grasp the full spectrum of AI possibilities (Amorphism) or struggle to understand its judgements (Judgement). Nevertheless, simply acknowledging AI’s complexity (Complexity) contributes to algorithm appreciation.

Conversely, a high level of internal decision-making by AI (Judgmental High) and its actual implementation in the ARAP (Awareness) can limit appreciation. This stems from the mystification of AI autonomy, reducing it to an emerging technology requiring significant human supervision. As one auditor summarises: “Musk makes cars, but we don’t quite know if it’s transparent – the car drives, the computer controls, but what does he do, who manages it?” (R7-Q16).

Uncertainty in interpretation primarily drives algorithm aversion: “I’m supposed to trust some artificial intelligence programme for all its intents and purposes, which, as an auditor, I don’t fully understand and probably the business environment doesn’t have a full understanding of either” (R19-Q14). It manifests with limited imagination about AI’s potential applications in the ARAP (Awareness) and the fear that AI might adapt its features through interactions with humans or other forms of AI (self-adjustment). Aversion is further reinforced when auditors cannot identify alternative solutions to replace AI in the ARAP.

5.3.2 Human and distributed responsibility.

Auditors based human responsibility primarily on two factors: the limited explainability of AI’s conduct (Judgmental Responsibility) and the difficulty of enforcing human-designed responsibility frameworks (Answerability), an enforcement challenge that arises from the perception of AI as merely a tool. As one auditor stated, “it [AI] is a tool, right?” (R31-Q12a). Some auditors expressed concern about ceding control to algorithms, with one stating, “Well, it would be a tragedy. It would be the end of freedom, and it would turn humans into slaves of machines” (R32-Q14), just as (R8-10, R13, R15, R19-20, R22, R26, R41).

Conversely, distributed responsibility appears to be driven by awareness, particularly concerning AI’s ethical implications in the ARAP. Auditors highly aware of AI’s applications in this context accept AI’s capacity to adapt its behaviour based on auditor input, even when this adaptation involves complex, opaque system-to-system interactions.

6. Discussion and conclusion

Our central argument is that possibilities are shaped by auditors’ sense of responsibility. We extend the existing affordance framework, which links action, possibilities and motivation, by introducing responsibility as a key factor that influences how possibilities are turned into action. This new perspective helps us understand why the affordance lens, while useful, does not fully capture the complexities of how auditors interact with AI in ARAP.

Auditors with greater familiarity and experience with AI tend to embrace distributed responsibility and appreciate AI more, whereas those with less AI knowledge focus more on human responsibility and are more averse to AI. These results show that the relationship between technology and auditors’ behaviour is not straightforward – it is influenced by deeply held views about responsibility.

This research contributes to the literature on AI adoption in auditing by confirming previous findings that auditors perceive limited utility for emerging technologies such as AI (Eilifsen et al., 2020). The affordance lens enables us to disentangle the auditor’s response to the reconfiguration of AI risks in the ARAP and look beyond the surface of action-possible frames towards responsibility through algorithmic attitudes. Even when auditors are faced with enablers of AI risk, they approach the application of AI to the risk assessment with reluctance, with the “limited use” being attributed to a lack of algorithm appreciation among auditors. Building on existing research (Commerford et al., 2022), our findings demonstrate that algorithm appreciation is crucial in driving auditors’ actions towards AI adoption.

More specifically, our investigation into the impact of attitudes towards responsibility and algorithms on AI applications in the ARAP yielded unexpected results, with both attitudes exhibiting non-linear relationships and varying degrees of influence. Algorithm aversion interplays with human responsibility, while algorithm appreciation is the primary driver of action.

Extending prior discussions (Commerford et al., 2022; Dyball and Seethamraju, 2022; Eilifsen, Kinserdal, Messier, et al., 2020; Landers and Behrend, 2022; Lehner et al., 2022; Salijeni et al., 2021), we found that distributed responsibility (Agostino, Bracci, et al., 2022; Lombardi et al., 2021) has a limited impact on algorithm aversion in AI applications within the ARAP, while human responsibility bridges algorithm aversion, although algorithm appreciation determines the course of action.

We further investigate the process behind algorithm aversion, echoing concerns raised in earlier studies (Dietvorst and Bharti, 2020). Besides ethical concerns (Bigman and Gray, 2018), mutual logic (Longoni et al., 2019), transparency (Lebovitz et al., 2022) and input quality (Commerford et al., 2022), our results show that a lack of viable alternatives and limited awareness of AI within the ARAP contribute significantly to algorithm aversion. This is further intensified by fears that AI may exhibit unintended behaviour due to interactions with humans or other AI systems, which raises concerns about responsibility. As auditors become more familiar with the construction and functionality of AI, the aversion diminishes, leading to increased adoption of distributed responsibility. These findings align with previous work (Gepp et al., 2018; Kend and Nguyen, 2020; Persellin et al., 2019).

The auditors with less AI experience and knowledge tend to prioritise human responsibility, while those with greater experience are more likely to support distributed responsibility. This supports the “diluted” perspective identified in other research (Agostino, Saliterer, et al., 2022; Bracci, 2022), but adds a nuance – responsibility perceptions shift with increased knowledge and experience. As auditors acquire knowledge and expertise, they are more likely to base their actions on the ability to determine responsibility for AI decisions (Birchall, 2015).

Taken together, these insights reinforce prior findings of limited AI adoption in auditing (Bakarich and O'Brien, 2021; Eilifsen et al., 2020). While some see AI as beneficial for automating tasks (Salijeni et al., 2021), concerns about AI autonomy persist in human-centric processes (Tiron-Tudor and Deliu, 2021), particularly as these concerns crystallise around defining the boundaries of responsibility.

This study is not without limitations. The interview-based research design inherently focuses on human agency, which may overshadow nuances in the actual execution of ARAP, while observational methods could provide deeper empirical insights. Future cohorts of auditors are likely to possess more accounting and algorithmic skills, suggesting that algorithm appreciation may naturally develop as new generations of auditors enter the profession. Moreover, the study focuses on audit processes (Grabski et al., 2011; Issa et al., 2016; Moll and Yigitbasioglu, 2019), leaving other contexts unexplored. Finally, potential overlaps between auditors’ and lawyers’ responsibility regimes (Staszkiewicz et al., 2024; Čerka et al., 2017; Fleming, 2019) point to the need for cross-professional dialogue on shared responsibility in AI-mediated decision contexts.

In conclusion, this research investigated affordances – actions and possibilities moderated with motivation – by examining attitudes towards responsibility. We showed that responsibility filters possibilities.

For policymakers and professional bodies, this suggests that auditors’ continuing professional development agendas should be revised to expand the scope of AI-related topics within audit training programmes. An alternative approach would involve clearly defining the division of responsibilities between auditors and AI systems.

Future research might examine how evolving forms of expertise – particularly among more algorithmically skilled auditor cohorts and in relation to auditees’ expectations – reconfigure the boundaries of professional responsibility in AI-mediated auditing.

The authors thank Warren Maroun, the editor, and the reviewers for their insightful and constructive feedback. The authors are also grateful to Igor Staszkiewicz for significant support during the review process, including recoding, simplification, formal notation, mathematical corrections and results replication. An earlier version of this paper was presented at AOM 2023, the EARNet 2023 Symposium and the Meditari Accountancy Research Conference 2023; the authors thank participants for their valuable comments. AI-assisted proofreading (GPT and Gemini), followed by human revision, was supported by SGH Warsaw School of Economics (ADOP/RID24/25:Z6.P3). Agnieszka received funding from Koszalin University of Technology (CRU-3098/2021) for a research internship at SGH. Piotr acknowledges support for the focus group pilot (ADOP/RIDTEAM25/06; RID/SP/0049/2024/01).

Appendix

Notes

For simplicity, we skipped the substitution (search for alternative emerging technologies without autonomy properties) in the main analysis, as it preconditioned prior arrangement. However, we mapped our data with “substitution” as the mean for the internal validity check.

Chartered accountants, seniors and equivalent experienced professionals eligible for registration.

One-tailed Pearson’s correlations were calculated for the possibility, algorithm attitude and responsibility attitude codes to re-examine the level-three decomposition structure. These results should be interpreted qualitatively rather than purely quantitatively. While the sample size is sufficient for assessing code-pair correlations, the use of purposive sampling may introduce bias towards actors who have engaged with AI. Nevertheless, the consistency in direction and structure between the qualitative and quantitative findings supports confidence in addressing the research question at an exploratory level. A more detailed examination of the relationships between possibilities and motivation is beyond the scope of this study and is recommended for future research.

In parentheses, the possibilities’ names; Suffix: Low – de-stimulant, High – stimulant. For the definitions, refer to Appendix.

¹Author’s note: PIBR – Polish Chamber of Public Auditors.

References

Further reading

Supplementary material

The supplementary material for this article can be found online.