Evolving financial issues in the sporting industry

Introduction

In recent years, the landscape of sport finance has changed rapidly and in often unpredictable directions. The explosion of fantasy sports, liberalization of sports betting laws in the United States and introduction of non-fungible tokens (NFTs) related to such assets as sports-related tweets and match highlights have each created derivative sources of value within the industry. Much of this value has been created through innovations, such as those listed previously, that allow fans and investors to “get in the game” as never before. At the same time, sports broadcasting rights, sponsorships and naming rights are routinely selling for record amounts (see, e.g. Kariyawasam and Tsai, 2017; Keating, 2018), and North American sport franchise valuations have also maintained a high growth rate (DeSantis, 2018).

The rise and shift of top sport franchise valuations

In 2020, Forbes Magazine estimated the average value of an NFL team to be $2.86bn, and NBA teams averaged $2.123bn. Over the past decade, we have observed aggressive annual growth in the world’s highest valuation sports franchise.

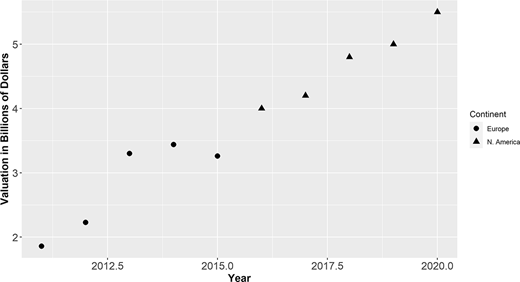

Table 1 shows steady growth in the world’s highest valuation sports franchise during the past decade. During that period, the top franchise valuation rose by approximately 196% cumulatively. That is, this valuation rose to almost three times its 2011 value by the year 2020. This implies an annualized valuation growth rate of approximately 12%, as demonstrated in the following growth accounting equations. In these equations, the annualized growth rate in proportion terms is represented as g.

World’s highest valuation sports franchise by year 2011–2020

| Year | Team | Sport | Value ($) | Nominal % increase | Continent |

|---|---|---|---|---|---|

| 2011 | Manchester United | Football/Soccer | 1.86b | – | Europe |

| 2012 | Manchester United | Football/Soccer | 2.23b | 0.20 | Europe |

| 2013 | Real Madrid | Football/Soccer | 3.30b | 0.48 | Europe |

| 2014 | Real Madrid | Football/Soccer | 3.44b | 0.04 | Europe |

| 2015 | Real Madrid | Football/Soccer | 3.26b | −0.05 | Europe |

| 2016 | Dallas Cowboys | American football | 4.00b | 0.23 | North America |

| 2017 | Dallas Cowboys | American football | 4.20b | 0.05 | North America |

| 2018 | Dallas Cowboys | American football | 4.80b | 0.14 | North America |

| 2019 | Dallas Cowboys | American football | 5.00b | 0.04 | North America |

| 2020 | Dallas Cowboys | American football | 5.50b | 0.10 | North America |

Source(s): Forbes data

This exercise demonstrates the steep rise in top sport valuation growth rates from 2011–2020, a trend visualized in Figure 1.

Figure 1 illustrates both the steep and fairly consistent rise in top sport franchise valuation and also the changing geographic landscape of the sport industry. Whereas European soccer/football clubs once dominated the world franchise valuation list, this list is now increasingly dominated by National Football League teams. The valuation of NFL teams has been buoyed by increasingly lucrative broadcasting deals, merchandising deals, sponsorships, naming rights, as well as a continued high demand for game attendance. Throughout its revenue rise, moreover, the NFL has maintained single, dominant league status in its sport on a global level. It has leveraged that status in recent years to build a greater international fan base via internationally located games and an increasingly global broadcasting footprint. Despite challenges to its single dominant league status throughout the NFL’s history (e.g. four incarnations of the American Football League, 1926, 1936–37, 1940–41 and 1960–69; the All-America Football Conference, 1946–49; the World Football League, 1974–75; the United States Football League, 1983–85, two incarnations of the XFL, 2001, 2020 and the Alliance of American football, 2019). Through all of these challenges, the NFL has maintained its status via a large league size that leaves few major U.S. markets without a franchise, a modern league revenue sharing policy that allows smaller market teams to remain viable and happy in the NFL, and a de facto, partial anti-trust exemption that allows teams to revenue share and collectively sell national broadcasting rights.

Effects of the COVID-19 pandemic upon sport and sport finance

As with anything else, the pandemic has changed the nature and role of finance in sport. In-person game attendance, the lifeblood of many sports teams and leagues, went completely away for the 2020 season for many sports, and severe limits were in place for leagues that did host fans. Leagues without major television deals, such as minor league sports in the United States, were decimated by the pandemic, with some leagues and teams choosing simply not to play rather than incurring losses. This led to a major restructuring of the minor league baseball system and has created innovative player development changes in sports such as hockey.

As the world adapts and hopefully moves beyond the COVID-19 pandemic, the financing of the sports world has been changed, seemingly for good. Direct relationships between sports teams and leagues and betting/daily fantasy markets, once unheard of in the United States, now dominate the landscape and continue to grow. This segment of the market provides considerable upside growth in revenue for these businesses, in addition to the leagues, teams and players as well. Technology allows for more options for fans to interact with teams and players, attend virtual events and connect with their favorite teams and sports in ways that no one would have considered in years past.

The pandemic has also emphasized aspects of the sports industry in ways that few foresaw. Trading cards and collectibles, whose marketplace seemed to be dwindling, met with a resurgence in 2020 and 2021. Investors have paved the way for high-end products to be delivered to the marketplace with resounding success for the companies and parties involved. This outcome has led to a trickle-down effect to the old sports staple of trading cards as companies such as Topps, Upper Deck and Panini find their products selling out and secondary market prices skyrocketing as parents stuck at home with their children have passed along their hobby passion to a new audience.

As we look to the future, however, there remains the need to be able to understand the past. Although the actual details may change, sports are still driven by consumers and their wants can only be addressed through product innovation and satisfaction. Research on costs and benefits, attendance analysis, game viewership online or on television, stadium finance and other issues provide information that will be useful to those taking sports in whatever direction it goes post-pandemic, and we are proud to present research on this topic in this special issue.

Special issue articles

The purpose of this special issue is to better understand contemporary sport finance trends and their underlying factors in the sport industry. To this end, we present 10 articles in the special issue. Several of these papers tackle issues related to performance elements of sport finance given specific characteristics of a player, match or event. Others consider firm or league performance more generally, including the regional economic effects of sport events. We first consider studies in the former group. Paul et al. (2021) find that not only precipitation but also cloud cover and barometric pressure negatively affect attendance in NFL games. Ehrlich et al. (2021a) examine the marginal salary returns to offensive win production and defensive win production in Major League Baseball. They find that offense is valued significantly and substantially more than defense in MLB free agency player markets. Walia and Boudreaux (2021) estimate and classify the costs of sport injuries across a number of sports and injury types. Garcia-del-Barrio and Pujol (2021) assesses the relationship between player on-field value and media presence upon transfer fee valuations in professional soccer/football. Di Simone and Zanardi (2021) studies the relationship between on-field and financial performance among professional European soccer/football clubs.

Among papers studying more general characteristics of firm or league performance, Kahane (2021) considers the economic impact of the 34th American Cup upon taxable sales in San Francisco. Khraiche and Alakshendra (2021) study cost under-estimation in the Olympic bidding and hosting process. Aftab and Naveed (2021) analyze financial performance of cricket teams in the Pakistan Super League. Omondi-Ochieng (2021) finds a positive relationship between financial performance, financial effectiveness and financial efficiency among not-for-profit sports federations in the United Kingdom. Ehrlich et al. (2021b) study the adverse financial impact of the pandemic upon North American professional sports leagues, as well as league counter-measures to mitigate this impact.

In their totality, these studies provide a global and far-reaching analysis of contemporary sport finance issues, challenges and future directions.