This study aims to offer a more precise understanding of the dynamics affecting managerial performance in the sector of industry by examining the factors of participative budgeting, staff capacity, information communication technology and organizational commitment.

The research is based on a sample of 1,040 individuals working in the financial departments of industrial enterprises. The analysis resorted to a combination of partial least-squares structural equation modeling and artificial neural network to test its hypotheses.

The findings reveal the direct effects of participative budgeting on staff capacity and organizational commitment. These two variables play a mediating role in the relationship between participative budgeting and managerial performance. Furthermore, information communication technology moderates the effects of participative budgeting on managerial performance through staff capacity and organizational commitment.

The cross-sectional design limits causal inference, and the focus on a single sector within one country constrains generalizability. Future research should adopt longitudinal and comparative approaches and examine additional determinants of managerial performance.

Managers can enhance decision-making transparency, collaboration and organizational performance by implementing participative budgeting, investing in capacity-building initiatives, adopting ICT tools and fostering organizational commitment.

By employing advanced analytical techniques, this study offers valuable insights into organizational dynamics, leading to a deeper understanding of the factors influencing managerial performance.

1. Introduction

Industry plays a key role in spurring economic growth and significantly contributes to economic prosperity and development through its diverse sectors such as oil and gas, manufacture, construction and agriculture (Al-Obaidi et al., 2022). It provides employment, revenue and technological advancement while reducing dependence on oil revenues and shielding economies from oil price shock (Prabhu et al., 2024). Moreover, by encouraging investment, entrepreneurship and human capital development, the sector provides a solid foundation for achieving sustainable growth.

However, industrial sectors in certain countries face challenges, particularly due to their limited participation in decision-making and policy formulation (Huy and Phuc, 2025), the lack of transparency and accountability in their management, the inefficient use of resources fostering diminished competitiveness, and inconsistencies in the goals and orientations of their different managerial factions (Alhasnawi et al., 2023). These hurdles result in poor managerial performance, which prevents the sector from operating effectively (Prabhu et al., 2024).

The trajectory of an organization's performance is a good indicator of its success or failure in achieving its vision (Singh et al., 2025). The comprehensive functionality of the industrial sector hinges on managerial performance and its elements, including operational efficiency, resource allocation, safety protocols, environmental compliance, strategic planning and stakeholder relations (Huy and Phuc, 2025). To address the numerous challenges it faces, the industrial sector requires comprehensive reforms, strategic planning and collaborative efforts to create an environment that is conducive to growth and competitiveness (Zhang et al., 2025), improve its efficiency through novel business practices, ensure budget transparency and increase its accountability (Alhasnawi et al., 2023; Al-Obaidi et al., 2022).

Participative budgeting thus emerges as a promising solution to the aforementioned challenges (Al Jasimee and Blanco-Encomienda, 2024). This budgeting model involves all relevant stakeholders, notably senior management and employees, that take part in the planning of budgets and allocating resources (Alhasnawi et al., 2024a). Their involvement helps refine the planning and implementation of the budget and enhances efficiently applying their organizations' financial and human resources (Zhang and Liao, 2011).

Participative budgeting is conceptualized as a core organizational approach that extends beyond its traditional financial role. From an organizational process perspective, budgeting operates as a cross-functional workflow that integrates information exchange, negotiation and the coordination of activities across departments (Cuganesan, 2017).

Due to its significant role in fostering democracy and economic development, participative budgeting has attracted the attention of budget practitioners, researchers and academics (Sihotang, 2023). Investigating this model not only contributes to the modernization of administrative methods and the promotion of inclusive governance and accountability but also helps cultivate strong partnerships among employees from various sectors and encourages their further involvement in decision-making processes (Brun-Martos and Lapsley, 2017).

Participative budgeting also enables employees to influence their organizations' budget goals (Chovanecek et al., 2024). This study positions participative budgeting as a core business process that coordinates planning, communication and decision-making across organizational units. From a Business Process Management (BPM) perspective, budgeting is not only a financial tool but a structured process that integrates information flows, aligns departmental objectives and supports strategic execution. By framing budgeting as a business process, this work directly contributes to the BPM literature, where the focus lies on designing, enabling and improving organizational processes to enhance performance.

The budgeting model primarily affects managerial performance through cognitive and motivational factors (Her et al., 2019; Nguyen et al., 2019). Staff capacity, which refers to the cognitive abilities, skills and knowledge of the individuals participating in the budgeting process, represents the cognitive aspect of this type of budgeting (He and Ismail, 2023). Meanwhile, organizational commitment mediates the relationship between participative budgeting and managerial performance by amplifying the positive effects of the former on employees' motivation, effort and goal alignment, which ultimately results in improved performance (Chong et al., 2006).

Gaining a comprehensive understanding of organizational dynamics requires examining the moderating role of information and communication technology (ICT) on the relationship between participative budgeting, managerial performance and the mediating effects of staff capacity and organizational commitment (Bartocci et al., 2023). By providing communication channels, ICT not only facilitates effective contributions from employees but also allows them to engage in collaborative decision making (Zheng and Schachter, 2018). Moreover, ICT promotes managerial performance by increasing workforce engagement and facilitating the evaluation of budgeting outcomes (Bartocci et al., 2023).

ICT thus plays a pivotal role in enabling the process by enhancing transparency, supporting real-time communication and strengthening collaboration among stakeholders (Yunis et al., 2018). ICT-enabled budgeting processes reduce information asymmetry, standardize procedures and improve responsiveness through integrated data flows and digitalized monitoring mechanisms (Jiang et al., 2025; Megha and Srikantha Dath, 2024). By examining how ICT conditions the effects of participative budgeting on staff capacity, organizational commitment and managerial performance, the current study contributes to the literature on digital transformation and business process improvement by demonstrating how digital tools reshape budgeting into a more transparent, integrated and agile organizational process.

Recent work has emphasized that ICT adoption is part of a broader digital transformation that reshapes organizational processes and governance practices (Jiang et al., 2025; Susanti et al., 2023). Digital transformation initiatives enable real-time information sharing, collaborative decision-making and process integration, which are at the core of business process management (Yunis et al., 2018). Moreover, emerging evidence shows that organizations that embed ICT and digital tools in budgeting and performance monitoring achieve greater transparency, efficiency and adaptability in dynamic environments (Megha and Srikantha Dath, 2024).

However, the findings of previous analyses on the relationship between participative budgeting and managerial performance are inconsistent (Al Jasimee and Blanco-Encomienda, 2024). While certain have identified a positive correlation between participative budgeting and managerial performance (Chong and Chong, 2002; Chong et al., 2005; Her et al., 2019; Lau and Tan, 2006; Le and Nguyen, 2020; Leach-López et al., 2009; Nguyen et al., 2019), others have observed either a negative (Cheng, 2012; Etemadi et al., 2009) or an insignificant correlation between the two (Brownell and McInnes, 1986; Dunk and Nouri, 1998; Riyadh et al., 2023). It is due to these inconsistencies that the relationship between participative budgeting and managerial performance requires further research (Sicilia and Steccolini, 2017).

In addition, although certain specialists have indeed examined the role of ICT in participative budgeting and managerial performance (Mærøe et al., 2021; Rose et al., 2010; Xiao et al., 2011), they have largely ignored the importance of its effect on the relationship (Bartocci et al., 2023). Moreover, in spite of the existence of previous research resorting to partial least squares–structural equation modeling (PLS–SEM) to inspect the linear relationships between participative budgeting and managerial performance (Macinati et al., 2016; Riyadh et al., 2023), they have ignored potential nonlinear and non-compensatory relationships (Alhasnawi et al., 2023). This inconsistency may be actually ascribed to the fact that these analyses only focused on a single mechanism of participative budgeting (Her et al., 2019; Nguyen et al., 2019).

To address these gaps, the current study proposes a complex model that uncovers the nonlinear and non-compensatory relationships between participative budgeting and management participation. This integrative model not only offers a highly nuanced perspective on the dynamics of organizational decision-making processes but also takes into account the moderating effects of ICT, an aspect which has been largely ignored in the literature (Bartocci et al., 2023). This model also sheds light on the mediating role of organizational outcomes by integrating motivational and cognitive factors, specifically staff capacity and organizational commitment.

The current study proposes the following research questions as guides:

Which factors contribute to improving managerial performance within the industrial sector?

Does active participating in the budgeting process help stakeholders improve their performance in overseeing the industrial sector?

How does integrating ICT enhance and refine the operational practices within the industrial sector?

In sum, this analysis focuses on a question that has been overlooked in the literature, namely how ICT interacts with participative budgeting to influence staff capacity and organizational commitment and ultimately shape managerial performance. Previous work has yielded inconsistent findings on whether participative budgeting directly improves managerial performance (Alhasnawi et al., 2024b). These discrepancies may stem from differences in corporate contexts, firm size and macroeconomic environments, underscoring the need for a more integrated model that accounts for organizational resources and digital enablers (Gao et al., 2024).

By leveraging advanced analytical techniques, such as the two-staged SEM–artificial neural network (ANN) and the conditional moderation mediation effects analysis, the findings of this study offer more comprehensive results than those resorting to conventional models (Leong et al., 2020) as well as valuable insights into organizational dynamics (Qureshi et al., 2025).

Furthermore, this study benefits from several assets. Firstly, the survey data were collected from staff and managers who actively participate in budgeting processes and leverage their accounting expertise. Secondly, the data were assembled from various enterprises within the industrial sector, thus preventing the findings from being confined to the idiosyncrasies of any single enterprise, thus enhancing their generalizability to individuals involved in budgeting processes across different organizational settings. Thirdly, the data offer insights pertinent to staff and managers who participate in the budgeting processes of their enterprises.

The remaining sections of this paper are structured as follows. Section 2 advances the theoretical framework and hypotheses while section 3 introduces the research methodology. Section 4 then recounts the data analysis and results. Finally, section 5 presents the discussion, implications, limitations and future lines of research.

2. Theoretical framework and hypotheses development

This study relies on both the contingency theory and the resource dependency theory (RDT) not merely as background perspectives, but as complementary theoretical lenses that jointly explain the variation of the effects of participative budgeting across digitalized organizational environments. While earlier research has tended to reference these theories descriptively, this analysis has attempted to articulate a theoretical logic that integrates their core assumptions and generate new contextual propositions regarding the mechanisms linking participative budgeting to managerial performance.

The contingency theory, well established in accounting literature (Chenhall, 2003; Franco-Santos et al., 2012), emphasizes that control systems must fit contextual conditions such as technological infrastructure, decision structures and environmental complexity. The theory implies that participative budgeting is not inherently effective or ineffective; rather, its influence depends on the alignment between budgeting practices and contextual contingencies – particularly those stemming from digital transformation (Katz et al., 2002). As noted by certain analyses, ICT capabilities fundamentally reconfigure information flows, accountability structures and decision rights (Cunha et al., 2011; Gao et al., 2024). Thus, from a contingency perspective, digital maturity constitutes a salient contextual factor that alters the motivational and cognitive processes through which participative budgeting operates.

The RDT, by contrast, foregrounds power asymmetries and the strategic implications of resource control (Davis and Cobb, 2010). In budgetary contexts, participative processes shape the distribution and accessibility of informational and material resources, thereby influencing managerial autonomy, dependence relationships and the ability to secure needed support. Although the RDT has been increasingly applied in public management and organizational design (Coupet, 2013; Pilbeam, 2012), its relevance to budgetary participation remains underexplored (Alhasnawi et al., 2023). Applying it to participative budgeting suggests that organizations with stronger digital infrastructures are better positioned to reduce information dependence, enhance transparency and equalize access to critical resources – thus altering the strategic value of participation for managers.

Merging these theories has yielded theoretical tension and led to propose a more nuanced explanation. The contingency theory predicts that ICT conditions the fit between participative budgeting and organizational needs, whereas the RDT predicts that ICT alters the power and resource structures underlying budgeting interactions (Chenhall, 2003; Davis and Cobb, 2010; Katz et al., 2002; Islam, 2003). Integrating the two theories suggests that ICT is simultaneously (1) a contextual contingency shaping behavioral responses to budgeting and (2) a strategic resource that redefines information dependency, coordination and control. This duality can be extended to existing models allowing to theorize why participative budgeting yields heterogeneous effects across organizations with different levels of digital capability – another aspect largely overlooked by prior research.

Consistent with research on BPM, ICT is conceptualized as a digital infrastructure that enables real-time integration, transparency and process standardization (Jiang et al., 2025; Yunis et al., 2018). ICT likewise embeds participative budgeting within broader process-oriented transformation efforts, reducing information asymmetries and enhancing coordination. This perspective enriches the theory by demonstrating that this type of budgeting is not only a behavioral mechanism but also bears a processual capability whose effectiveness depends on the digital configuration of the organization (Megha and Srikantha Dath, 2024).

Motivational and cognitive views offer further grounds for theorizing on conditional effects. From the motivational standpoint, participative budgeting fosters commitment and ownership (Lau and Buckland, 2001; Murray, 1990). From the cognitive standpoint, it enhances information exchange and decision quality (Aranda et al., 2023). Yet empirical findings remain inconclusive as they have yielded positive (Chong and Chong, 2002; Chong et al., 2005; Her et al., 2019; Lau and Tan, 2006; Le and Nguyen, 2020; Leach-López et al., 2009; Nguyen et al., 2019), negative (Cheng, 2012; Etemadi et al., 2009)and null effects (Brownell and McInnes, 1986; Dunk and Nouri, 1998). Integration of the contingency and RDT theories provides a theoretical explanation for these inconsistencies: the value of participation depends on the digital contingency fit and the degree to which ICT alleviates resource dependency through improved information availability and coordination.

Accordingly, this study advances the theory by proposing that participative budgeting influences staff capacity, organizational commitment and managerial performance through mechanisms that are contingent upon – and strategically shaped by – the organization's ICT environment. This integrated theoretical stance positions the model within core BPM concerns, highlighting how digital resources reshape organizational behaviors and the effectiveness of key business processes.

2.1 The mediating role of staff capacity

Participative budgeting offers insights into administrative procedures, facilitates making contributions to governance policies, ensures accountability and guarantees an equitable distribution of public resources (Jayasinghe et al., 2020; Pamela, 2002). He (2011) highlighted the effectiveness of participative budgeting in managerial integration, fostering participation and reducing competition.

According to Haldma and Lääts (2002), qualified accountants play a pivotal role in shaping organizational practices. Staff capacity captures the cognitive and technical abilities necessary for managers to process budgetary information, implement participative practices and align them with organizational goals. The contingency theory allows to view staff capacity as an internal determinant of managerial performance, whereas the RDT identifies this element as a reflection of how human resources shape the activities of an organization (Otley, 2016). Implementing participative budgeting in the industrial sector is hindered by the lack of full-time accountants working in finance departments and the intricacies of their daily operations (Célérier and Cuenca Botey, 2015), both of which prevent enterprises from setting their budget goals (Yuen, 2004, 2007). Douglas (2000) and Leach-López et al. (2015) identified three key elements that drive the success of organizational reforms, namely, accounting staff, advanced knowledge training and availability of adequate resources. Conversely, Célérier and Cuenca Botey (2015) proposed that the lack of qualified internal accounting staff may impede an enterprise from adopting novel business practices.

Participative budgeting involves employees in the budgetary process so as to enhance managerial performance (Chong et al., 2006; Frucot and White, 2006; Her et al., 2019). This collaborative approach not only fosters ownership and accountability but also facilitates informed decision making and goal alignment by leveraging employee insights (Cuganesan, 2017; Her et al., 2019). The efficacy of this budgeting model depends on several organizational factors, including staff capacity, which in turn encompass the cognitive abilities, skills and knowledge of employees that are critical to their participation in drafting budgets (Haldma and Lääts, 2002). The contingency theory suggests that enterprises must align their practices with their internal capabilities and external environments (Katz et al., 2002). Having a robust staff capacity allows these enterprises to effectively implement participative budgeting and consequently enhance managerial performance.

Staff capacity in this study is conceptualized as a dynamic, process-responsive capability rather than a fixed or innate individual attribute. Drawing on capability development and organizational learning perspectives, staff capacity can evolve when employees gain access to richer information, participate in joint problem-solving and engage in routines that enable experiential learning (Haldma and Lääts, 2002; He and Ismail, 2023). Under this lens, participative budgeting functions as a structured organizational process that creates opportunities for knowledge acquisition, enhances cross-functional interaction and strengthens employees' understanding of resource allocation and performance criteria.

Participative budgeting enhances these developmental conditions by improving information flows, clarifying task expectations and involving staff in decision-making routines (Chong et al., 2006; Cuganesan, 2017). Through repeated interaction with budgetary information and collaborative planning discussions, employees can build technical, analytical and coordination-related competencies. This implies that staff capacity is partially shaped by the organizational processes in which employees are embedded. Thus, when participative budgeting is implemented systematically, it is reasonable to expect that it will contribute to strengthening staff capacity over time rather than merely relying on pre-existing qualifications.

In the presence of qualified staff, enterprises can embrace participative budgeting and consequently enhance their managerial efficiency. By contrast, entities devoid of qualified staff may face challenges when implementing this type of budgeting. Managers can positively influence managerial performance if they possess significant knowledge and experience in decision making, resource utilization and budget planning (Célérier and Cuenca Botey, 2015). These arguments lead to the following hypotheses:

Staff capacity positively mediates the relationship between participative budgeting and managerial performance.

Participative budgeting positively affects staff capacity.

Staff capacity positively affects managerial performance.

2.2 The mediating role of organizational commitment

Chen et al. (2006) defined commitment as a force that binds individuals to activities that are in line with the objectives of their enterprises. Organizational support from the top-down is particularly crucial to participative budgeting endeavors (Bartocci et al., 2023). Organizational commitment reflects the motivational mechanism that links participative budgeting to sustained engagement and improved performance (Al Jasimee, 2019; Vugec et al., 2020).

Managers who demonstrate a strong sense of duty toward their enterprises are more likely to introduce participative budgeting in a decisive and results-oriented manner. The contingency theory emphasizes the importance of maintaining the alignment between a firm's practices and its specific circumstances and goals (Otley, 2016). The successful implementation of participative budgeting greatly depends on several factors, including goals, culture and external environment (Vugec et al., 2020). For example, if a business values transparency and employee involvement, then participative budgeting may bolster organizational commitment. Meanwhile, the RDT suggests that the survival of enterprises hinges on the availability of external resources (Otley, 2016). Resource allocation also plays a crucial role in participative budgeting and influences organizational commitment. A fair allocation of resources demonstrates the commitment of a business to value the input and welfare of its employees, thus potentially enhancing organizational commitment.

Sofyani et al. (2022) argued that organizational commitment is manifested through various activities, such as goal setting, resource allocation, formulating strategies and plans, rejecting stifling resources, and providing the necessary political backing to inspire goal achievement. Tahar and Sofyani (2020) stated that organizational commitment significantly influences the capacity of an enterprise to adopt performance-enhancing policies. Moreover, organizational commitment of managers plays a crucial role in the establishment of performance-related organizational policies (Sofyani et al., 2022).

Organizational commitment is conceptualized differently depending on the commitment framework (Cunha et al., 2011). For instance, it may represent the attitudes of employees or the forces that bind employees to their enterprises. It can also be fostered through participation in decision-making processes (Bartocci et al., 2023) and managerial involvement (Nouri and Parker, 1998; Parker and Kyj, 2006). This type of commitment has likewise been positively linked to employee performance (Camilleri and Van Der Heijden, 2007). Managerial commitment to the firm can encourage employees to accept and work toward achieving their organizational goals, thus enhancing managerial performance.

According to Nouri and Parker (1998), participative budgeting influences job performance through organizational commitment. Previous work on organizational commitment has also highlighted the significance of democratic and participative processes. Participative decision making, including participative budgeting, suggests that in order to achieve success in their enterprises, employees should implement the decisions attained through participative processes. In other words, participation helps integrate employees into their businesses and build their commitment to organizational decisions. Therefore, as employees further engage in decision-making processes, they experience greater organizational commitment, which in turn improves managerial performance. Participative budgeting triggers these positive effects by exerting a strong influence on motivation variables (Frucot and White, 2006).

Participatory practices reinforce employees' sense of autonomy, competence and relatedness, three core psychological needs identified by the self-determination theory (Forner et al., 2021; Manganelli et al., 2018; Slemp et al., 2021). Satisfying these needs has been consistently linked to stronger commitment and proactive engagement in organizational initiatives. Participative budgeting provides an institutionalized opportunity for employees to express their views, influence key decisions and develop a shared understanding of organizational priorities, thereby reinforcing their intrinsic motivation to support organizational goals (Wong-On-Wing et al., 2010).

Research on collective governance also supports the idea that participation builds ownership and shared responsibility. Inclusive and deliberative processes foster trust, mutual recognition and commitment to collective outcomes (Albareda and Sison, 2020; Kim, 2016). Budgetary participation, as a structured form of collaborative governance, generates these relational and psychological conditions within organizations. Therefore, the participative nature of budgeting practices not only enhances technical decision quality, but bolsters employees' identification with the organization and their willingness to contribute to its long-term performance.

These arguments lead to the following hypotheses:

Organizational commitment positively mediates the relationship between participative budgeting and managerial performance.

Participative budgeting positively affects organizational commitment.

Organizational commitment positively affects managerial performance.

2.3 Effects of ICT

The rapid evolution of ICT in recent years and the availability of its support (Rose et al., 2010) has encouraged citizen engagement in democratic processes such as participative budgeting (Mkude et al., 2014). This involves accessing information, public deliberations, negotiations and large-scale decision making.

ICT contributes to process efficiency by reducing redundancy and streamlining workflows, ensuring that budgeting and performance monitoring are carried out with fewer delays and errors. It also reinforces joint decision-making as managers and staff can access and analyze real-time data collectively, leading to more informed and participative choices.

Moreover, ICT fosters information sharing by integrating data across units, increasing transparency, and enabling better alignment of departmental objectives. Recent studies further emphasize its role as a digital enabler of business process transformation and managerial decision making (Kraus et al., 2021; Susanti et al., 2023; Yunis et al., 2018).

Although ICT has widely served in participative budgeting to facilitate participation, other initiatives have not extensively integrated these technologies. Such discrepancy raises doubts on whether ICT usage in participative budgeting actually enhances managerial performance. This leads to varied perspectives regarding its adoption in traditional practices (Winata and Mia, 2005). Previous works reveal that optimal outcomes may not be achieved by relying on participative budgeting alone (Chong and Chong, 2002). However, integrating ICT into managerial practices allows for adaptive efforts based on new information. The effectiveness of participative budgeting in improving managerial performance depends on the use of ICT (Maiga et al., 2014).

ICT can likewise directly enhance staff capacity by increasing access to real-time information, standardizing data processing routines and supporting learning-by-doing. Digital tools expand employees' analytical capabilities and facilitate the acquisition of the technical and cognitive skills required to support budgeting processes (Lopes Gomes et al., 2025). Thus, ICT serves as an infrastructure that strengthens employees' ability to process information, coordinate tasks and apply budgeting techniques more efficiently.

Furthermore, ICT contributes to strengthening organizational commitment by improving perceptions of transparency and organizational support (Vaccaro et al., 2008). ICT-enabled communication, open data environments and collaborative platforms increase employees' sense of inclusion and trust in organizational decisions. When information is shared equitably and digital systems are perceived as supportive rather than controlling, employees tend to experience higher levels of affective and normative commitment (Aubé et al., 2007; Sartori et al., 2023).

ICT likewise improves managerial performance by boosting decision accuracy, accelerating performance feedback loops and enabling data-driven coordination. It also enhances organizational responsiveness and operational efficiency (Kazakov et al., 2021; Yunis et al., 2018). ICT-enabled performance measurement systems assist managers in identifying deviations, reallocating resources and taking corrective actions more effectively, thereby improving managerial effectiveness.

ICT, in fact, interacts positively with participative budgeting by boosting the cognitive, informational and motivational mechanisms through which budgeting participation yields its effects. Digital systems facilitate access to relevant data, improve communication channels and support collaborative problem-solving, thereby complementing the participatory aspects of budgeting. Evidence suggests that ICT also strengthens the informational and coordination-related benefits of participative management practices (Andersen, 2001; Lopez-Nicolas and Soto-Acosta, 2010). Such interactions generate conditions in which this form of budgeting can be more effectively translated into improved managerial behavior and organizational outcomes.

Winata and Mia (2005) supported the above notions after highlighting the significant moderating effect of ICT on the relationship between participative budgeting and performance in the hotel industry. However, further research on this aspect is warranted due to the significance of budgeting in manufacturing and the highly inconsistent conclusions regarding management control and ICT (Chong and Chong, 2002; Granlund and Mouritsen, 2003). These arguments lead to following hypotheses:

ICT positively affects staff capacity.

ICT positively affects organizational commitment.

ICT positively affects managerial performance.

High ICT levels strengthen the relationship between participative budgeting and managerial performance under the mediating effect of staff capacity.

High ICT levels strengthen the relationship between participative budgeting and managerial performance under the mediating effect of organizational commitment.

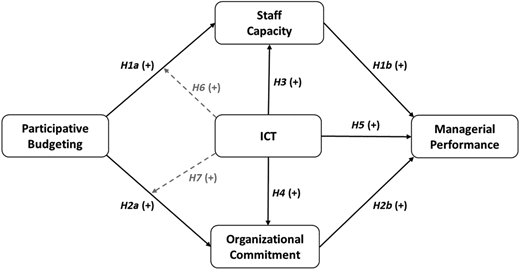

Figure 1 depicts the conceptual model guiding this study. The solid arrows highlight the predicted causal relationships among the variables while the dashed arrows indicate the conditional moderation mediating effects.

3. Research methodology

This study adopted a quantitative design to explore the interrelations among variables within the industrial sector. All the data were collected via a questionnaire.

3.1 Population and sample

The target population consisted of individuals working in the finance departments of enterprises (directors and accounting staff) from the industrial sector of Iraq.

To ensure relevant expertise, the participants were selected by means of purposive sampling. Of the 1,700 total questionnaires remitted, 1,100 were returned. The total was reduced to 1,040 after applying exclusion criteria (incomplete, inconsistent or patterned answers or submissions outside the target population).

The 1,040 stemmed from different branches of the industrial sector, notably chemical, oil, gas, construction, copper, packaging, electronics, energy, textiles, agriculture and food production.

The sample was further broken down into 714 males and 326 females with approximately 7% aged between 20 and 30, 36% between 31 and 40, 44% between 41 and 50, and 13% over 51 years. More than half (56.3%) hold a bachelor's degree, 35.2% a master's degree and only 8.5% a doctoral degree. In terms of academic achievement, the majority (69.5%) benefitted from a relevant accounting background, while the others specialized in fields closely related to accounting.

The participants chosen for the study were deemed to possess sufficient knowledge to offer well-informed insight into issues related to budgeting. In terms of work experience, 15% had less than 10, 54% between 10 and 20 and 31% over 20 years.

The sample's demographic and professional characteristics are consistent with the profiles of general management of the Iraqi industrial sector. The sample also spans multiple industries and includes individuals bearing diverse managerial levels, educational backgrounds and years of experience, minimizing the risk of bias linked to any specific segment.

3.2 Measurement instrument

All of the items of the questionnaire were adapted from the relevant literature. To ensure its clarity and comprehensibility, it was revised based on feedback of five academic specialists in accounting and research methodology and five potential participants working in the Iraqi industrial sector.

The variables applied likewise have their root in literature. The participants were asked to rate each item on a seven-point Likert scale, ranging from 1 (“strongly disagree”) to 7 (“strongly agree”), based on the extent to which their enterprises conformed to the content of each item.

Participative budgeting was assessed using a scale adapted from Chong et al. (2005), Parker and Kyj (2006) and Her et al. (2019), staff capacity was evaluated using a scale adapted from Prabhu et al. (2024) and He and Ismail (2023), organizational commitment was measured with a scale adapted from Camilleri and Van Der Heijden (2007), ICT was measured using a modified version of the scale developed by Kyj and Parker (2008) and later adapted by Lunardi et al. (2019), and managerial performance was evaluated using a scale adapted from Her et al. (2019). The measurement scales are listed in Table 1.

4. Analysis

4.1 Measurement model evaluation

A confirmatory factor analysis was carried out to analyze the measurement model. The results listed in Table 2 confirm that all indicators align with factor loadings exceeding the 0.70 threshold recommended by Hair et al. (2019). Furthermore, their Cronbach's alpha coefficients and composite reliabilities Rho_A and Rho_C were all above 0.70, thereby confirming the model's high degree of construct reliability. In terms of convergent validity, all indicators obtained average variance extracted (AVE) values exceeding 0.50, thereby suggesting that the items converge with the relevant constructs and that the model has construct validity (Hair et al., 2019).

Two methods were set upon to evaluate the discriminant validity of the model. The first consisted of calculating the heterotrait–monotrait ratio of correlations following Henseler et al. (2015) which yielded values that did not exceed the 0.85 threshold. The second, following Fornell and Larcker (1981), served to compare the correlations among the latent variables with the square root of AVE. The diagonal values in Table 3, which equate with the square roots of AVE, exceeded the values below the diagonal elements, which represent the correlations among the constructs, thereby confirming the model's discriminant validity.

4.2 Common method bias

Testing for the presence of common method bias (CMB) potentially stemming from self-reported data (Podsakoff et al., 2003) was carried out using two methods given that the predictor and outcome variables were collected by means of a single instrument. This implied, on the one hand, testing the variance inflation factor (VIF) values within the inner model. The fact that they all ranged from 1.4532 to 2.465, well below the 3.3 threshold (Kock, 2015), confirmed the absence of CMB. On the other hand, the results of Harman's single-factor test, where all key constructs were incorporated into a principal component analysis, revealed that the highest factor explained 36.83% of the covariance. The absence of CMB in this study was thus reconfirmed as this value did not exceed the 50% threshold (Podsakoff et al., 2003).

4.3 SEM assessment

A PLS–SEM was applied by means of the SmartPLS software with a bootstrapping of 100,000 random subsamples and no sign change setting to test the hypotheses. A one-tailed test was also conducted yielding a significance level of 0.05.

Several criteria were adopted to evaluate the SEM model, notably R2, Q2, fit indices and the statistical significance of the structural paths. As visible in Table 4, the R2 value for managerial performance was 0.655, confirming a strong explanatory power (Hair et al., 2019). The Q2predict value of 0.537 also exceeded zero, indicating predictive relevance (Dul, 2016). Model fit indices further supported the adequacy of the model. The SRMR value fell well below the recommended 0.08 cut-off (Hu and Bentler, 1999), while the NFI value approached the commonly accepted threshold, suggesting a good fit between the hypothesized model and the observed data (Henseler et al., 2016). Taken together, these indices confirm that the model exhibits both explanatory robustness and predictive accuracy.

4.4 Direct effects analysis

Table 5 lists the results of the direct effects analysis, which empirically supports all hypotheses. Specifically, participative budgeting has a statistically significant positive effect on staff capacity (β = 0.277, p < 0.001) and organizational commitment (β = 0.088, p < 0.01), thereby substantiating H1a and H2a.

Staff capacity (β = 0.171, p < 0.001) and organizational commitment (β = 0.101, p < 0.001) also display a statistically significant positive effect on managerial performance, thereby supporting H1b and H2b.

ICT likewise reveals a significant positive effect on staff capacity (β = 0.523, p < 0.001), organizational commitment (β = 0.454, p < 0.001) and managerial performance (β = 0.250, p < 0.001), thereby bolstering H3–H5.

The significance of participative budgeting on managerial performance requires being viewed through the lens of a process. Specifically, the statistical evidence indicates that budgeting is not only a financial mechanism but a structured business process that shapes information flows, coordinates departmental activities and guides resource allocation.

This process-based interpretation positions the empirical findings within the BPM domain by conveying how budgeting contributes to organizational process effectiveness.

4.5 Mediating effects analysis

Table 6 presents the results of the mediating effect of staff capacity and organizational commitment. On the one hand, participative budgeting and managerial performance display a complementary (partial mediation) relationship through staff capacity (β = 0.047, p < 0.001). This thereby suggests that participative budgeting positively affects staff capacity and subsequently affects managerial performance, notions that reinforce H1.

On the other hand, participative budgeting and managerial performance reveal a partially mediated correlation through organizational commitment (β = 0.009, p < 0.05). This suggests that participative budgeting influences organizational commitment and subsequently affects managerial performance, a notion supporting H2.

4.6 Conditional mediation and moderation effects analysis

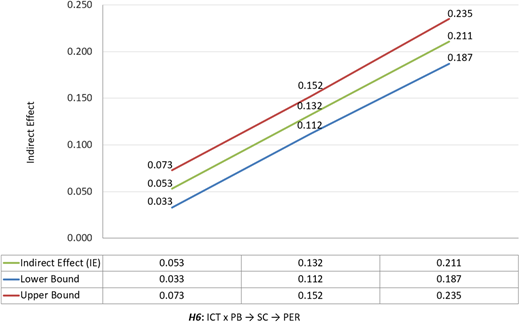

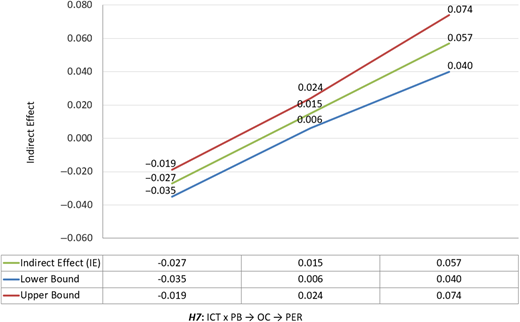

The values of Table 7 indicate that the relationship between participative budgeting and managerial performance is moderated by ICT through staff capacity (β = 0.079, p < 0.001) and organizational commitment (β = 0.042, p < 0.001). They thereby substantiate H6 and H7. In other words, higher ICT levels intensify the indirect effects of participative budgeting on managerial performance.

Figures 2 and 3 further support these findings. Following Preacher et al. (2007), a continuous moderator was applied to differentiate the various levels of the conditional mediation effect as depicted by the Johnson–Neyman plot. The results reveal that ICT does not simply enhance the relationship but also conditions its strength. As depicted in Figure 2, the effect at lower levels of ICT of participative budgeting on staff capacity and, consequently, on managerial performance, is weak and often insignificant. However, this relationship at higher ICT levels becomes stronger and statistically significant. The steeper gradient observed in Figure 3 illustrates this conditional effect, demonstrating that ICT creates thresholds beyond which participative budgeting translates more effectively into improved managerial performance through organizational commitment. In sum, ICT both moderates and conditions the budgeting–performance link, underscoring its central role in enabling participative practices to yield tangible organizational benefits.

4.7 ANN analysis

An ANN analysis was conducted to validate the PLS–SEM results and to establish the nonlinear connections among the variables (Alnoor et al., 2024). ANN learns through repetitive training and encodes knowledge as synaptic weights (Leong et al., 2020; Qureshi et al., 2025) that are regulated by activation functions that reduce the error between the actual and desired outputs via iterative adjustments. ANN techniques have been widely applied to a variety of domains, including accounting (Moussaid et al., 2023; Parot et al., 2019), management (Alnoor et al., 2024) and tourism (Huang et al., 2007).

The ANN analysis was conducted by means of SPSS software. Following Leong et al. (2019), overfitting was avoided by allocating 90% of the samples for training and the remaining 10% for testing. A 10-fold cross-validation method was subsequently employed, and the root mean square of errors (RMSE) was calculated (Ooi and Tan, 2016). This was followed by applying a multilayer perception with a feed-forward back-propagation algorithm. The significant predictors from the PLS path analysis were treated as input neurons, and a sigmoid function served to simultaneously activate the output and the hidden layer. Table 8 indicates that the RMSE values for training and testing are respectively relatively low, at 0.1025 and 0.0871. The R2 of the ANN model was then computed following Hew and Kadir (2016). The results confirm that the model predicts managerial performance with an accuracy of up to 80%.

A sensitivity analysis was also carried out to evaluate the predictive power of each input neuron (Table 9). This analysis generated normalized values expressed as percentages (Karaca et al., 2019), which confirm that participative budgeting has the highest predictive importance (96.0%) followed by ICT (81.0%), staff capacity (23.0%) and organizational commitment (21.0%).

5. Discussion

This study examines how managerial performance is concurrently influenced by the motivational and cognitive mechanisms of participative budgeting. Through an intervening approach, it reveals that staff capacity and organizational commitment mediate the relationship between participative budgeting and managerial performance. Thus, this form of budgeting affects managerial performance through its significant and positive impact on staff capacity and organizational commitment, a notion that supports the findings of previous research (Chong et al., 2005; Lau and Tan, 2006; Le and Nguyen, 2020; Nguyen et al., 2019). The findings gathered here also assist in reconciling prior inconsistencies by demonstrating that the effect of participative budgeting on performance becomes more pronounced when taking into account ICT use, staff capacity and organizational commitment. This clarifies why certain earlier analyses yielded weak or inconclusive results, particularly in contexts lacking adequate resources or digital infrastructure.

From a business process management perspective, the findings illustrate that participative budgeting functions as a structured organizational process rather than a simple accounting practice. The process integrates communication, negotiation and decision-making across multiple departments, a transformation that is further enabled by ICT by digitalizing workflows and ensuring real-time information sharing. The mediating effects of staff capacity and organizational commitment provide additional evidence that organizational resources and behaviors shape the effectiveness of such processes. Taken together, the results highlight how participative budgeting, supported by ICT and human factors, operates as a business process that enhances managerial performance.

The results of the conditional moderation mediation effects analysis underscore the moderating role of ICT on the aforementioned effects. Such effects are particularly pronounced under high ICT levels, which strengthens the indirect relationship between participative budgeting and managerial performance. This finding is consistent with the arguments of other specialists who emphasize the significance of ICT in improving managerial performance (Yunis et al., 2018).

This study also combines the PLS–SEM and ANN techniques to analyze the factors that affect managerial performance. Each of these approaches identify ICT as the most influential factor followed by staff capacity and organizational commitment. The consistency of their results confirms the robustness of the findings and draws attention to the importance of these variables for managerial effectiveness. Specifically, PLS-SEM enables the examination of mediation and moderation mechanisms, thereby uncovering the process-oriented pathways through which participative budgeting affects managerial performance. ANN, in turn, is more suitable for handling nonlinear and complex interdependencies among variables, offering stronger predictive validity (Qureshi et al., 2025). The complementarity between these methods lies in the fact that while PLS-SEM provides theory-driven causal inferences, ANN captures hidden patterns and enhances prediction. Together they yield a richer understanding of how ICT conditions the budgeting–performance relationship. These results also shed light on the complementary nature of PLS–SEM and ANN in understanding complex organizational dynamics, thus offering useful insights into the optimization of decision-making processes and operational efficiency.

These findings are likewise consistent with the growing body of research on digital transformation, which emphasizes that ICT facilitates the redesign of business processes and the adoption of more participative forms of governance. For instance, Winata and Mia (2005), Yunis et al. (2018), Kraus et al. (2021), Susanti et al. (2023) and Hasan et al. (2025) suggest that digital transformation improves managerial decision-making by integrating information flows, whereas Maiga et al. (2014) and Bartocci et al. (2023) emphasize the contribution of digital platforms to participative budgeting. This current analysis thus extends this stream of research by empirically demonstrating how ICT-enabled transformation supports the mediating effects of staff capacity and organizational commitment on managerial performance.

5.1 Theoretical implications

This investigation also offers valuable insights in several key aspects that significantly advance the literature on participative budgeting and managerial performance.

Firstly, it fills a research gap by demonstrating the combined effect of motivational and cognitive factors. Although previous work has separately examined the effects of staff capacity and organizational commitment on managerial performance, it has largely ignored their combined effects.

Secondly, this analysis contributes to the participative budgeting literature by constructing an integrative model that takes into account the moderating influence of ICT. In this way, this model reveals how ICT interacts with participative budgeting to affect various organizational outcomes, including staff capacity and organizational commitment, and ultimately impact managerial performance. It likewise contributes to the present theoretical understanding of an area that has been overlooked and offers a highly nuanced perspective on the dynamics of organizational processes.

Thirdly, unlike previous research that has primarily focused on the linear impacts of participative budgeting and intervening variables on managerial performance, this study develops a more complex model applying a two-stage SEM–ANN approach to capture nonlinear and non-compensatory relationships (Qureshi et al., 2025). In doing so, it advances the theoretical debate by revealing that participative budgeting operates through complementary cognitive (staff capacity) and motivational (organizational commitment) mechanisms, while ICT further conditions these effects as a critical digital enabler in contingency-based explanations of managerial performance.

Prior research that relied only on direct linear effects offer limited explanatory power (Chong et al., 2005; Lau and Tan, 2006; Nguyen et al., 2019). By integrating mediation, moderation and nonlinear patterns, the current analysis extends the contingency theory in both explanatory scope and predictive capacity, offering a more comprehensive understanding of how contextual factors shape managerial outcomes (Otley, 2016).

Finally, this study explores participative budgeting in a framework where the concept is relatively unknown. By focusing on the Iraqi industrial sector, it offers valuable insights into the applicability of participative budgeting practices in developing countries.

5.2 Practical implications

This study provides actionable guidance for industrial organizations seeking to enhance operational effectiveness and managerial performance. The findings indicate that participative budgeting can be operationalized as a structured managerial process that strengthens transparency, shared responsibility and decision-making quality while aligning capital allocation with workforce expertise and reducing project inefficiencies (Al Jasimee and Blanco-Encomienda, 2024; Alhasnawi et al., 2025).

The integration of ICT should be prioritized as a core component of management systems, as it enables real-time information sharing, supports data-driven decision-making, improves cross-functional coordination and facilitates continuous performance monitoring, thereby reinforcing the effectiveness of participative budgeting (Al Jasimee et al., 2025).

Investing in staff capacity through continuous professional development, targeted training and knowledge-sharing initiatives equips employees with the competencies required to contribute meaningfully to budgeting processes, ultimately strengthening managerial effectiveness and operational outcomes (Hasan et al., 2025). In parallel, fostering organizational commitment through inclusive leadership, recognition practices and supportive organizational cultures helps sustain employee alignment with strategic goals and amplifies the positive impact of participative budgeting on long-term performance (Raziq et al., 2024).

Collectively, the integration of participative budgeting, ICT adoption, human capability development and organizational commitment creates a synergistic managerial framework that enhances process efficiency, decision quality and sustainable organizational performance across industrial contexts (Al-Hazaima et al., 2025).

5.3 Limitations and directions for future research

Despite its contributions to literature, this study suffers from several limitations that provide avenues for future research. Firstly, it fails to establish causal relationships due to the cross-sectional nature of the data it collected. Future research could adopt longitudinal designs to further delve into the dynamic interactions among participative budgeting, staff capacity, organizational commitment and managerial performance over time. Secondly, this investigation only focused on the industrial sector of a specific country, which limits generalizing its findings to other industries or geographical regions. Future research can enhance their generalizability and uncover industry-specific insights by replicating the analysis in other contexts. Thirdly, managerial performance can be influenced by factors other than participative budgeting, staff capacity, ICT and organizational commitment. Future research should attempt to examine factors such as leadership styles, organizational culture and external environmental conditions to further advance the understanding of managerial effectiveness in complex organizational settings.

Finally, while this study focuses on internal organizational mechanisms, external contingencies such as leadership style, organizational culture and macroeconomic conditions deserve further inquiry as they can potentially also shape managerial performance. Comparative studies spanning industries and national contexts, as well as longitudinal designs, could yield deeper insights into how participative budgeting and ICT influence performance over time and under varying institutional settings.

6. Conclusion

This study provides robust empirical evidence on how participative budgeting influences managerial performance through the mediating roles of staff capacity and organizational commitment, while ICT serves as a critical moderating mechanism that strengthens these relationships.

The findings highlight that effective budgeting is not merely a structural process but a multidimensional mechanism that integrates human, motivational and technological resources to enhance decision-making quality, operational efficiency and overall organizational performance. By applying a combined SEM–ANN approach, the study captures both linear and nonlinear relationships, addressing limitations of prior research that relied predominantly on linear models and deepening understanding of the complex dynamics underlying managerial performance (Al-Hazaima et al., 2025).

From a theoretical perspective, this research advances contingency theory by demonstrating how contextual factors, cognitive mechanisms, motivational mechanisms and digital enablers interact to shape managerial outcomes, particularly in industrial settings within developing countries (Alhasnawi et al., 2023, 2025).

From a practical perspective, the results provide managers and industrial organizations with a framework for implementing participative budgeting, investing in capacity building, integrating ICT and fostering organizational commitment, thereby enabling more informed, agile and effective decision-making processes (Raziq et al., 2024).

Thus, this study not only deepens theoretical understanding of the mechanisms driving managerial performance but also offers a practical roadmap for industrial organizations seeking to leverage participative budgeting, staff development, ICT integration and organizational commitment to achieve operational excellence and sustainable performance outcomes.