This paper examines how herding behaviour (HB) affected investment decisions (ID) of retail investors with respect to mediation by investor sentiment (IS) and risk perception (RP). Traditional finance theories presume that investors make decisions rationally based on available information. However, behavioural finance (BF) refutes this concept by citing the effects that psychology and emotions have when it comes to making ID.

“Partial Least Squares Structural Equation Modeling (PLS-SEM)” was employed to analyse data of 307 retail investors.

The results show that HB plays a significant role in both IS and RP that in turn have a significant role in ID. The mediation analysis confirms that IS and RP mediate the relationship between HB and ID, with evidence of a serial mediation effect where HB shapes IS which then influences RP and ultimately drives ID.

Findings have practical implications for financial advisors and policymakers in designing strategies to lessen the effects of HB and enhance market stability.

This study advances BF by empirically establishing a serial mediation framework. Study findings show that the herding → IS → RP → ID pathway is the most influential, with RP emerging as the strongest driver.

1. Introduction

Investment decisions (ID) have traditionally been examined through classical finance theories such as Markowitz's Portfolio Theory (1952), “Expected Utility Theory” (Bernoulli, 1738) and the “Efficient Market Hypothesis” (Fama, 1965, 1970). These frameworks presume that investors act rationally and fully process available information to maximise returns. However, empirical evidence suggests that investment behaviour is frequently shaped by emotions, cognitive biases and psychological factors which lead to deviations from rational decision-making (Bihari et al., 2022; Kapoor and Prosad, 2017).

Behavioural finance (BF) opposed the assumptions of traditional finance by arguing that markets are often driven by sentiment, biases and social influences rather than objective information alone (Baker and Wurgler, 2007). Investors frequently rely on others' actions instead of independent analysis which results in herding behaviour (HB) (Baddeley, 2010). Herding amplifies speculative bubbles and market volatility and is observed among both retail and institutional investors thus influencing overall market dynamics (Baker et al., 2017; Kengatharan and Kengatharan, 2014). Such behaviour is often driven by psychological comfort, social validation and less decision stress (Nofsinger, 2005).

Investor sentiment (IS) is also a key component in the movements of a stock market as it influences price volatility and trading behaviour (De Long et al., 1990; Schmeling, 2009). Positive sentiment strengthens market reactions to favourable news and negative sentiment induces risk aversion and market downturns (Brown and Cliff, 2004; Guo et al., 2017). IS also leads to inefficiency in the market and noise trading (Qiang and Shu-e, 2009).

Risk perception (RP) can be described as the subjective assessment of financial uncertainty by investors. It includes both cognitive and emotional factors and has a major contribution in ID (Ricciardi, 2008). Higher RP can usually deter market participation and lower RP can even strengthen herding by making group decisions seem safer (Madaan and Singh, 2019).

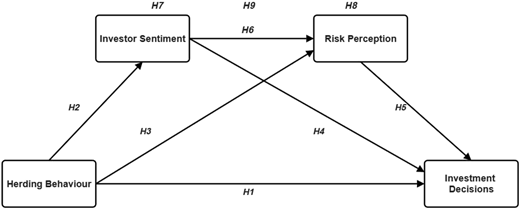

This paper will consider the effect of HB on ID plus including IS and RP as serial mediators. The research provides novel empirical evidence and advances BF literature by addressing an underexplored mediation framework in the retail investment context. Although the separate explanations and simple mediation models have been effectively used in previous BF studies but the processual mechanism by which HB, IS and RP interactively influence ID has not been fully explored. Prior studies mainly take either (1) parallel or single-mediator SEM models that rely on the direct or indirect effects (Ahmed et al., 2022a, b; Almansour et al., 2023) or (2) behavioural prioritisation approaches such as Fuzzy-AHP and hybrid multi-criteria frameworks that rank biases and contextual factors based on perceived importance rather than causal sequencing (Sachdeva et al., 2021; Sood et al., 2023). Though these approaches present great insights into what matters most but little explanation of the unfolding behavioural effects cognitively and emotionally in response to the ID process.

This study advances BF theory by conceptualising ID-making as a sequential psychological pathway which uniquely positions social influence (herding) as the exogenous trigger initiating a sentiment-risk transmission mechanism. Earlier serial mediation studies mainly emphasise internal traits (e.g. financial knowledge, optimism bias or overconfidence) (Chen et al., 2022; Lim et al., 2018). The PLS-SEM-serial mediation framework is methodologically advantageous as it empirically induces the causal prioritisation instead of perceptual ranking thus addresses a significant methodological gap in BF research. This research fills a critical theoretical gap within emerging market contexts related to the dynamic interplay of the emotional and cognitive processes in the decision-making of the retail investor by explicitly modeling sentiment and RP as interdependent mediators.

2. Literature review, hypotheses development and proposed model

2.1 HB→ID

HB within financial markets is characterised by investors imitating the actions taken by others as opposed to doing their own analysis. Such behaviour is usually compelled by the necessity to feel secure under unpredictable circumstances and the risk of losing possible profits. Prior studies indicate that herding can cause a problem of distorted stock-price representation which causes market inefficiency and speculative bubbles (Waweru et al., 2008; Xing et al., 2025).

Research suggests that retail traders have a higher likelihood of herding since they are likely to rely on their peers to make ID because of a lack of financial education and an increased level of risk aversion (Banerji et al., 2020). This behaviour is evident in both bull and bear markets but it is intensified when the market is going-down (Poshakwale and Mandal, 2014). These tendencies can bring about overtrading, low returns and poor diversification relative to rational investment behaviour (Agrawal et al., 2016).

Empirical evidence on the impact of herding presents mixed outcomes. Some studies report a positive influence on ID through information aggregation (Madaan and Singh, 2019; Qasim et al., 2019), while others emphasise adverse effects such as irrational trading and market inefficiency (Ahmad and Wu, 2022; Bikhchandani and Sharma, 2000; Zahera and Bansal, 2018). Following hypothesis is put forth based on the evidence.

HB has a significant influence on ID.

2.2 HB→IS

Research findings indicate that investors often go with the flow rather than making independent decisions and highlighting a significant influence of HB on IS (Waweru et al., 2008). Although limited research has examined this relationship, Haritha and Uchil (2020) empirically confirmed its impact. Studies also suggest that herding shapes market perceptions and investment behaviour (Qadri and Shabbir, 2014). Generally, herd mentality arises when investors follow others instead of conducting their own due diligence (Baddeley, 2010). This tendency is usually triggered by prior market profits/losses (Blasco et al., 2012). Evidence further shows that herding leads to irrational ID, as investors trade in the same set of assets regardless of private information (Kamil and Abidin, 2017).

Both institutional and individual investors contribute to herding-driven sentiment shifts. Institutional herding may destabilise prices but can also accelerate price corrections when new information emerges (Clarke et al., 2014). Individual investors are influenced by speculative bubbles and often react emotionally to market trends (Kengatharan and Kengatharan, 2014). Herding further affects market sentiment by driving stock price movements in response to news (Guo et al., 2024; Mian and Sankaraguruswamy, 2012) and influencing reactions to earnings announcements (Jiang et al., 2011). Shiller (2005) emphasised that herding is reinforced through social interactions and plays a key role in asset pricing bubbles.

This relationship was further supported by Wang and Nuangjamnong (2022), who identified a statistically significant association between HB and IS. They have found out that traders who engage in herding develop more emotional highs and lows. This is why informed and independent decision-making is essential.

Following hypotheses based on the above discussion.

HB significantly influences IS.

2.3 HB→RP

HB plays a crucial role in determining the RP of investors since traders often make decisions using collective judgment instead of individual analysis to make ID (Gavrilakis and Floros, 2021). This tendency is especially apparent in times of market instability when investors want to reduce the perceived risk by simply going along with the crowd (Dickason and Ferreira, 2018). Empirical evidence indicates that HB is common in financial markets especially during crises or uncertain conditions (Varshney et al., 2025). In developing markets, herding has been shown to influence investors' choices by reducing perceived risk (Ahmad and Shah, 2020). These findings align with evidence that investors often exhibit irrational decision-making under heightened RP, prioritising social conformity over independent evaluation (Kumar and Goyal, 2015).

It is hypothesised based on overall empirical evidence that.

HB significantly influences RP.

2.4 IS→ID

IS is an important factor in explaining ID. IS reflects investors' market perceptions and expectations of future returns. Sentiment determines how investors respond to financial information and make portfolio choices (Kengatharan and Kengatharan, 2014; Nofsinger and Varma, 2013). High levels of optimism/pessimism often drive trading behaviour at times deviating from fundamental analysis (Baker and Wurgler, 2006). Empirical studies confirm that IS directly affects ID. Metawa et al. (2018) reported a strong favourable effect of sentiment on investment choices. Similarly, Mian and Sankaraguruswamy (2012) observed that stock price reactions to earnings announcements align with prevailing sentiment with stronger responses to favourable news during high-sentiment periods. This indicates that IS shapes decision-making strategies in financial markets. Evidence from the Indian stock market shows that ID are influenced by sentiment-driven factors such as news coverage, interpersonal interactions and referral-based recommendations (Haritha and Uchil, 2020; Annapurna and Basri, 2024).

It is hypothesised based on the above that:

IS significantly influences ID.

2.5 RP→ID

RP is pivotal in ID. RP defines how investors evaluate losses and uncertainty in financial markets. Prior studies indicate that people who have a higher perceived risk will be more conservative and cautious in making ID by thoroughly examining the available options (Wattanasan et al., 2020). This cautious behaviour aligns with broader evidence showing that RP significantly influences decision-making which leads investors to adopt either risk-averse strategies or seek higher returns based on their risk tolerance (Lim et al., 2020).

RP is considered one of the determinants of investment behaviour in BF (Bhatia et al., 2020). Empirical studies indicate that traders that expect to face higher risks tend to make better informed and computationally-calculated decisions that can result in better financial performance (Kengatharan and Kengatharan, 2014). Conversely, the high degree of risk aversion can lead to inefficient ID and reduced returns (Almansour et al., 2023). Samsuri et al. (2019) found that there is a positive association between risk tolerance and ID. This finding supports the importance of risk assessment in the process of financial strategies. The fact that RP affects ID is also proved by evidence of the Pakistan Stock Exchange (Ahmad and Shah, 2020). Literature also reveals that the increased perceived risk usually discourages participation in the stock market (Awais et al., 2016; Hamid et al., 2013). There are some researches that indicates high RP can also promote risk-seeking behaviour. This behaviour observe especially in situations when investors think that they can handle uncertainty (Ishfaq et al., 2017; Kahneman and Tversky, 1979). This two-sidedness implies that the impact of RP on ID is not simple and depends on personal psychology and the conditions of the market (Lim et al., 2018).

It is postulated according to the empirical evidence that.

RP has a significant influence on ID.

2.6 IS→RP

IS strongly affects people's perception of financial risks. Investors likely to underestimate risks when sentiment is high which leads to more aggressive trading. Whereas negative sentiment increases RP and makes investors more cautious. Essentially emotional investors tend to estimate risks by considering the market sentiments. There is ample empirical evidence corroborating this notion. Dickason and Ferreira (2018) found that IS affects RP with optimistic investors perceiving lower risks. Rashid et al. (2019) also affirmed the fact that high sentiment minimises RP and promotes speculative behaviour. Similarly, Gai and Vause (2005) pointed out that sentiment change modifies the way investors assess financial risks. Qadan (2019) found a direct relationship between IS and risk appetite. Jiang et al. (2021) noted that IS causes fluctuations in RP especially in unstable markets.

Such a robust empirical base urges us to uphold the following hypothesis.

IS significantly affects RP.

2.7 Mediating role of IS and RP

Herding affects IS because individuals are likely to stick to market trends instead of conducting an independent analysis (Bekiros et al., 2017). The level of optimism/pessimism of other people can influence the general mood of the individual (Metawa et al., 2019). It often leads to emotional trading where decisions are guided by prevailing market trends instead of structural fundamentals (Kengatharan and Kengatharan, 2014). This type of emotional contagion causes speculation instead of rational decision-making (Haritha and Uchil, 2020). Research also shows that herding may cause irrational behaviour in the market driven by emotions instead of rationalism (Zhang et al., 2022). Risk-taking is affected by optimistic sentiment and pessimism motivates one to be cautious (Lim et al., 2018). This implies that IS is the mediating factor of herding on ID.

Herding also affects RP especially in the circumstances of market uncertainty (Balcilar et al., 2014). Investors often perceive lower risk when following the crowd by assuming that collective decisions reduce potential losses (Halim and Pamungkas, 2023). However, herding can also increase the perceived risk in volatile environments and cause bubbles and crashes (Ahmed et al., 2022a, b). This is in line with the results that herding causes risk misjudgements since investors are interested in social validation rather than a rational evaluation (Dickason and Ferreira, 2018). Conversely, RP has a great influence on investing behaviour since it defines the risk-seeking or risk-averse behaviour of individuals (Gupta and Kohli, 2021). Its mediating role is further supported by studies identifying perceived risk as a significant determinant of ID in herd-driven markets (Kasoga, 2021; Ng et al., 2022).

Thus, we propose.

IS performs the mediating function on the relationship between HB and ID.

RP performs the mediating function on the relationship between HB and ID.

IS and RP perform serial mediation on the relationship between HB and ID.

Accordingly, the proposed model is illustrated in Figure 1.

3. Research methodology

3.1 Data collection

Responses were assembled through a self-administered questionnaire from active stock market investors during February–March 2025 in eastern India using convenience sampling (Etikan, 2016). A total of 307 valid responses remained after removing nine outliers. G*Power confirmed adequacy with minimal sample size required (power 0.80; significance level 5%) of 77 (Faul et al., 2009). Participation was voluntary with informed consent and no sensitive data (i.e. no medical, psychological or high-risk concerns). As the institution does not have an ethics review board, formal ethical approval was not required; however, the study followed standard ethical guidelines for research involving human participants.

3.2 Measure

The questionnaire began with a study description and a screening question “Are you investing in a stock market?”. Only “Yes” responses proceeded. Constructs were measured using a “seven-point Likert scale” (1 = strongly disagree; 7 = strongly agree).

Previously established scales were adopted and modified for this study (see Appendix).

3.3 Data analysis

“PLS-SEM” is thought to be appropriate for prediction orientation in a theoretical structure in the social and behavioural sciences (Hair et al., 2022). The paper applied non-parametric “variance-based partial least squares structural equation modeling (PLS-SEM)” with “SmartPLS software version 3.2.9” for statistical application and hypothesis testing (Ringle et al., 2015). The “PLS-SEM” approach achieves adequate statistical strength and yields reliable findings, even for relatively small samples and asymmetric data (Hair et al., 2017).This study used SPSS software to perform the “Kolmogorov–Smirnov test” to assess multivariate normality. The statistically significant value of the test results is below 0.05, which indicates that the data were not normally distributed. “PLS-SEM” is an appropriate multivariate data analysis technique because the study employs a complex model (Hair et al., 2019, 2022) and a forecast perspective of investing actions towards stocks (Cheah et al., 2019; Sarstedt et al., 2019). Furthermore, “PLS-SEM” is appropriate for the present endeavour that seeks to build theory since complicated models with many components and the indicators which confirm them rapidly reach constraints (Saari et al., 2021). “PLS-SEM” is believed to be a superior technique to “CB-SEM” for assessing complex models without extensive theoretical support or reasoning (Rigdon et al., 2017). Therefore, “PLS-SEM” is seen as a more suitable and appropriate strategy for us to utilise instead of “CB-SEM”.

Concerns about common method variance (CMV) are widespread when a survey is only collected once. There are several prevention strategies implemented in line with past research to prevent CMV. The single-factor method developed by Harman was used and calculated to address the CMV issue (Teng et al., 2020). At 45.225%, Harman's single-factor measurement value met the conventional standards and fell short of the 50% explanatory value that is advised (Mishra and Dutta, 2026; Podsakoff et al., 2003). Second, a substantial correlation between the variables in the study was discovered. In order to shed light on the potential problem of strong correlation, the “variation inflation factor (VIF)” was calculated. The inner value of VIF in the structural model for all of the latent components in the study varied between 1 and 1.905 illustrating that there are no problems with multicollinearity that were detected because the calculated values fell below the 3.3 threshold level (Kock, 2015).Third, the researchers told participants before data collection that there was no correct or incorrect response on the measure and that they should select the level of agreement depending on their impression of the experience. Finally, personal information will not be revealed because the study's main objective is research only, and responses will stay anonymous.

4. Results

4.1 Measurement model

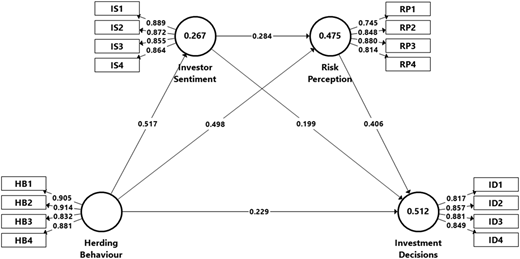

Measurement model was first assessed for reliability and validity under the “PLS-SEM” approach (Hair et al., 2017). Table 1 reports “composite reliability (CR), Cronbach's alpha, average variance extracted (AVE) and factor loadings” for all constructs. Indicator loadings (0.745–0.914) exceeding the 0.708 threshold confirm measurement's consistency or reliability (Hair et al., 2017). “Internal consistency” was confirmed as alpha values were above 0.70 (Hair et al., 2011) and CR values (0.893–0.935) fell within the recommended 0.70–0.95 range (Sarstedt et al., 2021). “Convergent validity” was established because AVE values exceeded 0.50 (Hair et al., 2017). “Discriminant validity” was examined using the HTMT criterion (Henseler et al., 2015). All “HTMT ratios” were below the 0.85 threshold (Table 2) which confirms adequate discriminant validity. Thus, the study's factors supported the validity and reliability standards.

Values of reliability and convergent validity

| Factor | Item | Factor loading | CR | rho_A | AVE | Cronbach's α |

|---|---|---|---|---|---|---|

| Herding behaviour | HB1 | 0.905 | 0.935 | 0.911 | 0.781 | 0.906 |

| HB2 | 0.914 | |||||

| HB3 | 0.832 | |||||

| HB4 | 0.881 | |||||

| Investment decisions | ID1 | 0.817 | 0.913 | 0.879 | 0.725 | 0.874 |

| ID2 | 0.857 | |||||

| ID3 | 0.881 | |||||

| ID4 | 0.849 | |||||

| Investor sentiment | IS1 | 0.889 | 0.926 | 0.904 | 0.757 | 0.893 |

| IS2 | 0.872 | |||||

| IS3 | 0.855 | |||||

| IS4 | 0.864 | |||||

| Risk perception | RP1 | 0.745 | 0.893 | 0.854 | 0.677 | 0.841 |

| RP2 | 0.848 | |||||

| RP3 | 0.880 | |||||

| RP4 | 0.814 |

4.2 Structural model

The relationship between the explained and explanatory constructs is determined by estimating the “coefficient of determination (R2)” after the validity and reliability of the measurement model have been verified. R2 values quantify “the variance in each endogenous construct that can be explained by the explanatory variables and are a measure of the model's explanatory power, sometimes referred to as in-sample predictive power” (Hair et al., 2017). The PLS-SEM analysis considers low R2 levels to be appropriate; however, the scenario determines the lowest acceptable value of R2 (Bhatt and Shiva, 2020). The R2 values in the research varied between 26.7% and 51.2%. The amount of explanation is adequate, based on the R2 results (Table 3).

Values of (R2) and (f2)

| Constructs | R2 | f2 | |

|---|---|---|---|

| Value | Effect | ||

| Herding behaviour | - | 0.059 | Weak to moderate |

| Investment decisions | 0.512 | – | – |

| Investor sentiment | 0.267 | 0.054 | Weak to moderate |

| Risk perception | 0.475 | 0.178 | Moderate |

The significance of independent factors in the model was examined using the effect size (f2) on the dependent factor as a result of R-squared variation (Cohen, 1988).The impact of f2 is 0.02 for low impacts, 0.15 for moderate impacts and 0.35 for substantial impacts, as per (Cohen, 1988). For every index, the effect's magnitude is weak to moderate (Table 3).

4.3 Model's predictive relevance (Q2 predict)

PLSpredict was used to evaluate out-of-sample predictive relevance in order to bolster the out-of-sample predictive power. Since the prediction errors were found to be normally distributed, we distinguished between the RMSE (“Root-Mean-Squared-Error”) values of PLS and LM (“Linear Regression Model”) (Shmueli et al., 2019). To ascertain the RMSE and predictive significance, Q2 predict was applied to the crucial dependent variable. Table 4 demonstrates that the criteria were satisfied because the Q2 predict values exceeded zero. Additionally, it was discovered that only one RMSE-PLS value was lower than the RMSE-LM value. This suggests that any measure of the decision to invest has a low predictive value, according to Hair et al. (2019).

PLS predict values

| Construct | Indicators | PLS | LM | PLS-LM RMSE | ||

|---|---|---|---|---|---|---|

| RMSE | Q2 predict | RMSE | Q2 predict | |||

| Investment decisions | ID1 | 1.181 | 0.177 | 1.169 | 0.194 | 0.012 |

| ID2 | 1.135 | 0.308 | 1.101 | 0.349 | 0.034 | |

| ID3 | 1.085 | 0.268 | 1.094 | 0.256 | −0.009 | |

| ID4 | 1.171 | 0.24 | 1.159 | 0.256 | 0.012 | |

Note(s): RMSE = Root Mean Squared Error, PLS- Model = Partial Least Square Model, LM = Linear Regression Model

The fitness of the model was assessed using the “Standardized-Root-Mean-Square-Residuals (SRMR)” approach (Hu and Bentler, 1999). The model's fitness was confirmed by a calculated SRMR score of 0.062, which was less than the most critical limit of 0.08 (Sarstedt et al., 2021).

4.4 Research hypotheses testing

In the structural model, the path coefficient and related t-score for the direct and mediated association were found by applying a bootstrapping approach with 5000 subsamples in smart PLS 3. A significant path coefficient is one that passes the test at the 5% and 1% levels of significance, respectively, when the path coefficient t-score is greater than 1.96 and 2.58 (Hair et al., 2011). Figure 2 and Table 5 provide path coefficients, which further illustrate the testing of the proposed relationships.

Hypothesis testing

| Direct relationships | Path coefficients | Lower CI (2.5%) | Upper CI (97.5%) | T-statistics | Decision |

|---|---|---|---|---|---|

| Herding behaviour → Investment decisions | 0.229 | 0.109 | 0.362 | 3.543** | Supported |

| Herding behaviour → Investor sentiment | 0.517 | 0.417 | 0.614 | 10.296** | Supported |

| Herding Behaviour → Risk perception | 0.498 | 0.385 | 0.610 | 8.628** | Supported |

| Investor sentiment → Investment decisions | 0.199 | 0.100 | 0.301 | 3.868** | Supported |

| Investor sentiment → Risk perception | 0.284 | 0.179 | 0.393 | 5.099** | Supported |

| Risk perception → Investment decisions | 0.406 | 0.266 | 0.537 | 5.869** | Supported |

| Mediation effect | |||||

| Herding behaviour → Investor sentiment → Investment decisions | 0.103 | 0.050 | 0.165 | 3.464** | Supported |

| Herding behaviour → Risk perception → Investment decisions | 0.202 | 0.126 | 0.287 | 4.904** | Supported |

| Herding behaviour → Investor sentiment → Risk perception → Investment decisions | 0.060 | 0.030 | 0.097 | 3.461** | Supported |

Note(s): Critical t-values; * 1.96 (p < 0.05); **2.58 (p < 0.01)

In support of H1, H4 and H5 the results (Table 5) demonstrated that HB (Beta score = 0.229, t-score = 3.543, p-score <0.01), IS (Beta score = 0.199, t-score = 3.868, p-score <0.01), RP (Beta score = 0.406, t-score = 5.869, p-score <0.01) had a positive and substantial effect on ID.

The outcomes indicated that HB has a direct, positive and substantial impact on IS (Beta score = 0.517, t-score = 10.296, p-score <0.01) and HB (Beta score = 0.498, t-score = 8.628, p-score <0.01) and IS (Beta score = 0.284, t-score = 5.099, p-score <0.01) had a positive significant influence on RP. Consequently, the hypotheses H2, H3 and H6 were supported.

A mediation study was conducted to investigate the mediating function of IS and RP in the association between HB and ID and the serial mediation of IS and RP in the association between HB and ID. The H7, H8 and H9 were validated by the evidence of a mediating effect of IS between HB and ID (Beta score = 0.103, t-score = 3.464, p-score <0.01), RP between HB and ID (Beta score = 0.202, t-score = 4.904, p-score <0.01) and IS and RP (Beta score = 0.060, t-score = 3.461, p-score <0.01).

5. Discussion

The outcomes of the research constitute a valuable contribution to the question of the impact of HB on ID of retail investors. The structural model analysis very well underscores that HB has a significant influence on ID in line with the earlier researches which also outline the function of behavioural biases in shaping investor behaviour (Shunmugasundaram and Sinha, 2024). The results indicate that HB directly influences the sentiment of investors and the way they perceive risks which influences the decisions regarding investments. These findings align well with earlier research works claiming that IS and RP are also important components of shaping ID (Ph and Uchil, 2020; Wang and Nuangjamnong, 2022).

The study confirms that HB positively and significantly impacts IS and RP. The strong link between HB and IS resonates with the findings of Ph and Uchil (2020). They identified social interaction, media influence and advocate recommendations as key drivers of IS. Moreover, the findings that HB positively affects RP are in line with the work of Almansour et al. (2025). They suggest that behavioural biases such as herding and overconfidence influence RP and ID significantly.

The effect of the IS on the ID was also seen as direct plus significant. This supports previous studies' findings that emotional variables and sentiment perform a vital function in transforming investment behaviour (Metawa et al., 2018). Similarly the significant effect of RP on ID reflects the findings of Hayat et al. (2024). They demonstrated that RP plays a mediator role in the link between behavioural biases and ID. This means that any change in the investors' perception of risk will affect their willingness to invest.

The mediation analysis highlights the complex relationship between HB, IS and RP. The study revealed that IS significantly mediates the relationship among HB and ID. This finding is consistent with Wang and Nuangjamnong (2022). They found that herding influences sentiment and thus subsequently shapes ID. RP also emerged as a significant mediator and this aligns with the outcomes from Almansour et al. (2023). They reporting that RP translates behavioural biases into ID.

The serial mediation analysis also indicates that the IS and the RP mediate the influence of the HB on the ID simultaneously. Serial mediation effect suggests that HB initially affects IS that in turn affect RP and finally ID. This multi-step process represents the psychological complexity of the investor behaviour where emotional and cognitive elements interact to direct the financial decisions.

Interestingly, these results align with broader patterns in BF. Gupta and Shrivastava (2021) emphasised that HB play a big role in the choice of retail investors. Ahmad and Wu (2022) also observed that HB had the negative effect of affecting the efficiency of the market yet it has the positive effect of influencing individuals to get decisions. This two-fold impact reveals the subtle role of herding in investment behaviour although it can be misleading market indicators but it can also offer psychological comfort to the investor.

6. Theoretical implications

The current research examines the intricate link between HB and ID among retail investors making significant theoretical advancements. This research is unlike the earlier studies which concentrated on direct effects of this relationship but instead examines the mediating role of IS and RP in this relationship. Therefore, the current study can be used to gain a better insight into the psychological mechanics that influence investment behaviour. The confirmation of serial mediation suggests that HB first shapes IS which then influences RP and ultimately driving ID. This multi-step process reflects the intricate nature of BF where emotional and cognitive factors interact to shape market behaviour. The findings are consistent with the previous literature on behavioural biases influencing the ID and go a step further to provide the theoretical framework by placing the IS and RP as key mediators.

7. Practical implications

The results are valuable to various stakeholders. Results indicate that the herding→IS→RP→ID pathway is the most influential and RP emerging as the strongest proximal driver of final decisions. This suggests that while herding initiates behavioural responses then it is the way sentiment reshapes perceived risk that ultimately guides ID. This means that herding does not influence ID in isolation rather its impact unfolds through a sequential psychological process. Specifically, exposure to collective market behaviour first shapes investors' emotional outlook (sentiment) which subsequently reframes how they subjectively evaluate financial risk and it is this altered RP that most strongly drives the final ID. The RP turns out to be the most powerful proximal predictor is an indication that investors end up acting on the perception of riskiness of an investment despite the fact that the initial trigger was social imitation. The paper therefore finds that contagion in financial markets due to behavioural factors functions in an emotion-cognition pathway where social influence drives sentiment then sentiment drives perceived risk and perceived risk drives action. This insight refines BF understanding by demonstrating that managing IS and correcting distorted RP may be more effective than addressing HB alone in promoting more rational ID. These findings help financial advisors and policymakers design interventions that address sentiment-driven risk misjudgements rather than focusing solely on HB. By recognising RP as the strongest driver, stakeholders can promote more stable and rational investment behaviour through improved risk communication and investor education.

These findings provide actionable guidance for market institutions, brokerage firms and portfolio managers. Since herding influences decisions indirectly through sentiment and perceived risk, advisory platforms can incorporate sentiment-tracking dashboards, risk alerts and structured decision checklists to discourage impulsive imitation. Brokerage houses may integrate behavioural analytics to identify periods of elevated sentiment-driven risk distortion and proactively communicate balanced market outlooks. From a research perspective, the results emphasise that interventions targeting only HB may be insufficient; instead, policies should address the sequential sentiment-risk transmission mechanism identified in this study. This highlights the importance of integrating emotional and cognitive components into BF models and encourages future empirical work to develop predictive tools that monitor sentiment-driven RP as an early indicator of unstable ID.

8. Conclusion

This paper points out the significant effect of HB on retail investors' ID with mediating factors IS and RP. The results affirm the fact that HB has a direct influence on IS and RP that consequently influences ID significantly. The mediation analysis supports the fact that HB influences ID through both IS and RP. This serial mediation effect underscores the complex psychological process involved in investment behaviour. As this serial mediation was not taken by any study as per our best knowledge. These observations form part of the information on BF as they help in explaining the interaction between emotional and cognitive influences that shape ID. This study can help financial advisers and market analysts in the sense that the knowledge on IS and RP can be applied to predict the market trends and enhance the advisory services to investors.

The present study however is based on cross-sectional data of retail investors and thus there is a limitation to make a causal inference and to observe changes in behaviour over a period. Future studies can use longitudinal/experimental designs to investigate the development of herding-based sentiment and RP at different stages in the market. Further expanding the model with the use of moderators like financial literacy, market volatility or demographic heterogeneity may shed more light on the boundary conditions of a serial mediation process. Comparative studies across markets would further enhance generalisability.

The supplementary material for this article can be found online