The purpose of this paper is to present a systematic review of the literature on financing channels for innovation in small and medium-sized enterprises (SMEs). The review aims to provide a comprehensive understanding of these channels, examining their characteristics, relationships and, most importantly, identifying which channels effectively drive innovation and which may not be as relevant. By doing so, the study seeks to highlight the key factors that contribute to the successful financing of innovation in SMEs and to identify potential gaps and opportunities for future research.

A systematic literature review was conducted following Preferred Reporting Items for Systematic Reviews and Meta-Analysis guidelines, analyzing studies published up to August 2024 in both English and Spanish. This approach ensures a thorough examination of both traditional and emerging financing channels, their interplay and their influence on innovation within SMEs.

The review uncovers the diverse roles that different financing channels play in supporting innovation in SMEs. While traditional channels like bank credits are critical, their effectiveness is influenced by factors such as technological capacity and market competition. Emerging channels, including crowdfunding and technology bonds, show potential but require further research to understand their full impact. In addition, the study reveals significant geographic and sectoral disparities, with certain regions and sectors being underrepresented in the existing literature.

The review is limited to articles published until August 2024 and primarily focuses on sources in English and Spanish. Future research should explore more diverse linguistic and regional contexts, particularly in underexplored regions such as Latin America and Africa, to gain a fuller understanding of global financing practices.

To maximize innovation, SMEs should strategically manage a mix of financing channels based on their specific characteristics and needs. Policymakers and financial institutions are encouraged to develop tailored financial products that cater to the unique requirements of SMEs, considering both traditional and emerging financing options.

This review contributes to the literature by not only mapping out the various financing channels for SMEs but also critically assessing their effectiveness in driving innovation. It highlights which channels are most beneficial and under what circumstances, offering actionable insights for SMEs, policymakers and financial institutions.

1. Introduction

This article presents a systematic review of the literature on financing channels for innovation in small and medium-sized enterprises (SMEs), with the aim of evaluating their impact and providing researchers with new tools and practices that can optimize innovation financing. The study specifically addresses a critical gap in the current literature by focusing on how different financing channels – both traditional and emerging – affect innovation outcomes in SMEs. This is particularly important given the unique challenges SMEs face in accessing finance compared to larger firms, especially in the context of innovation, which requires sustained investment and risk management. Over time, the role of innovation in the economic development of productive systems and, consequently, in the economy of countries has become increasingly significant. The advancement in science, technology and innovation is crucial for bringing about structural and economic transformation in nations (Bakhouche, 2021; Grilli et al., 2018; King and Levine, 1993). As noted by Schumpeter in his 1911 Theory of Economic Development, innovation serves as the impetus for economic change by facilitating the introduction of novel goods and production methods that disturb the existing economic balance and engender new prospects for sustained economic expansion (Schumpeter, 1934).

Despite the recognized importance of innovation, the existing literature highlights that SMEs often struggle to secure the necessary financing to support their innovative activities. These challenges include limited access to financial markets, higher perceived risks by lenders and a lack of tailored financial products. The absence of comprehensive studies that evaluate how different financing channels interact with the unique characteristics of SMEs to influence innovation represents a significant gap that this review aims to address. From a Schumpeterian perspective, the materialization of innovation in SMEs hinges on the availability of accessible and adequate sources of financing (Bakhouche, 2021; Cruz, 2020; Udimal et al., 2019). The extant evidence indicates that SMEs that are not integrated into financial markets encounter impediments to both growth and innovation (Bakhouche, 2021; Civelek et al., 2021; Aiello et al., 2020). It is therefore imperative to analyze the relationships between innovation financing in SMEs and the available financial solutions to foster support for innovation in these businesses. This approach has the potential to not only increase the intensity of their innovative activities but also enhance their competitiveness in the market.

This review also seeks to identify the specific characteristics and interactions of different financing channels, assessing which are most effective in driving innovation in SMEs. First, such an analysis can help overcome the barriers faced by innovative SMEs, such as lack of government support, quality of human resources, lack of managerial skills, availability of equipment and technology, intellectual capital, economic conditions and business partners and risk aversion (Civelek et al., 2021; García-Pérez-de-Lema et al., 2021; Hall and Lerner, 2010; Indrawati et al., 2020). Moreover, the issue of financing is not only focused on access barriers but also on identifying the most appropriate type of financing to achieve innovation goals (Mazzucato and Semieniuk, 2017). As highlighted by Al Wali et al. (2022), other internal organizational factors such as creative self-efficacy and leadership are also crucial.

Second, the analysis of innovation financing in SMEs can contribute to the economic growth of these firms. According to Gómez et al. (2009), the evolution of the financial structure behavior of SMEs can be framed within several financial theories: the pecking order theory (Myers and Majluf, 1984), the life cycle theory (Weston and Brigham, 1981), the agency theory (Jensen and Meckling, 1976) and the credit rationing theory (Stiglitz and Weiss, 1981). Given the importance of SMEs for economic growth, it is crucial to identify the most commonly used financing channels internationally and their impact on innovation outcomes, thereby supporting the aforementioned economic theories.

Finally, the study of the relationships between R&D investment, innovation outcomes and financing channels can provide guidelines for the implementation of public policies by highlighting relevant findings to be considered.

The available literature on the link between finance and innovation is scarce, with four relevant reviews: first, Hall and Lerner (2010) discussed the theoretical background of R&D investment, the determinants of R&D financing and the impact of financial considerations on the investment decision. Second, Bergemann and Hege (2011) discussed the funding of research projects and the agency conflicts that arise due to uncertainty about the time and capital required for completion. Third, Kerr and Nanda (2014) highlighted the growing role of innovation-related debt financing. Finally, Hahn et al. (2019) examined the impact of innovation on corporate finance and the ways in which investors can benefit from these emerging opportunities.

Unlike prior research, this systematic review aims to objectively assess the effects of various financing sources on innovation. By doing so, it seeks to uncover novel techniques and practices, such as the rise of alternative actors like crowdfunding platforms (Stefani et al., 2020), that can enhance innovation funding for SMEs. In addition, this study fills a critical void in the literature by focusing specifically on the financing of innovation in SMEs – an area often overshadowed by studies on larger firms. This entails identifying the most researched sources, examining their essential features and understanding their relationships with innovation outcomes. Furthermore, the study showcases the most often referenced authors regarding the subject.

The following is a description of the organization of the article: Section 2 outlines the systematic review method used, including the Preferred Reporting Items for Systematic Reviews and Meta-Analysis (PRISMA) and the population, intervention, comparison, and outcome (PICO) framework, used for the selection and filtering of pertinent articles, as well as the research questions addressed. Section 3 provides a comprehensive account of the most notable studies, classified according to the number of citations, geographical location, databases used and models used by the authors. In Section 4, the primary findings are presented, and the research questions are answered, emphasizing the financing channels with the greatest impact on SME innovation and their complementary relationships and impact on innovation. Section 5 presents potential avenues for future research, based on the identified gaps, as well as practical implications for SMEs, policymakers and researchers. Finally, the conclusions underscore the significance of specific financing channels for SME innovation, including credit, public resources and self-financing. This highlights the necessity for more efficient and selective management of public aid and proposes novel guarantees, such as patents.

2. Research methodology

The objective of this article is to conduct a systematic review of the literature on financing channels for innovation in SMEs. The PRISMA method guidelines were used to minimize bias in the selection and exclusion of articles (Barrios Serna et al., 2021; Contreras-Barraza et al., 2021; De Dios et al., 2011; Moher et al., 2014; Sánchez-Serrano et al., 2022). To determine eligibility and focus the study on the established objectives, the PICO tool was employed: P (patient, problem or population), I (intervention), C (comparison, control or comparator) and O (outcomes). Introduced by the National Institute for Health and Care Excellence in 1995 (Thabane et al., 2009), PICO is a strategy used to formulate various types of research questions arising from clinical practice, the management of human and material resources or the use of assessment instruments (Aguiar et al., 2015; Carrión Pérez et al., 2020). Table 1 illustrates its application in the context of this review.

Table 1 outlines the specific criteria used to guide the selection and evaluation of articles. Specifically:

Population: Focused exclusively on studies involving SMEs.

Interventions: Required that articles present a clear model or methodology for analysis or measurement.

Comparator: Concentrated on various financing channels.

Outcomes: Needed to demonstrate results related to innovation intensity in SMEs, such as R&D expenditure or an increase in patents.

Time Frame: No restrictions were applied.

To gain comprehensive insight into the current state of literature pertaining to the influence of financing channels on SME innovation, their outcomes and limitations, the following research questions have been formulated:

Which financing sources have been studied the most by researchers?

What is the impact of different financing sources on SMEs’ innovation intensity?

What is the future research scope in innovation finance for each financing source?

2.1 Data search

The research is based on an extensive search of the Scopus and WOS databases to ensure the inclusion of only peer-reviewed studies and high-quality sources on the Web (Cañedo et al., 2010). The keywords were selected by the authors after a comprehensive review of previous research and review articles related to the specific topic (Aiello et al., 2020; Barona-Zuluaga et al., 2015; Guercio et al., 2020a; Hall and Lerner, 2010; Kerr and Nanda, 2014). The primary search terms included “sources of financing,” “innovation” and “small and medium-sized enterprises.” As the term “innovation” is used interchangeably in the context of financing, related keywords for research and development (R&D) were also included in the search.

The final search equations, shown in Table 2, were prepared using Boolean operators and field codes. The search was restricted to English and Spanish, and the fields of study were limited to business, management and accounting and economics, econometrics and finance.

The search was carried out until August 2024. The screening was carried out by the authors following the criteria of the PICO table:

Accessibility criterion: Articles available in the Scopus and WOS databases;

Document type criterion: Scientific and review articles;

Time period criterion: All publication years to analyze the evolution over time;

Thematic inclusion criterion: Articles focused on financing channels, innovation, R&D and models;

Thematic exclusion criterion: Excluded topics include Fintech, Digital Finance, Financial Innovation, Eco-innovation, Circular Economy, Financial Performance of Innovation and Financial Education;

Subarea criterion: Articles from the areas of Business, Management and Accounting, Economics, Econometrics and Finance and Social Sciences;

Language criterion: Spanish and English, according to the authors’ language proficiency;

Methodological criterion 1: Articles specifically studying financing channels for innovation in SMEs; and

Methodological criterion 2: Articles with clear and coherent methodologies and models.

Inclusion criteria:

Citations identified in the documents.

Citations identified in the search of different databases.

Records or citations from organization websites.

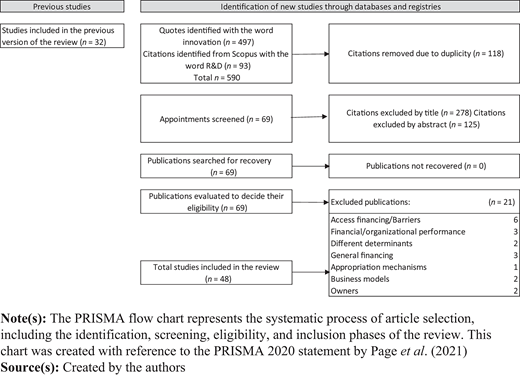

To minimize biases, the research followed the bias assessment protocol outlined in the PRISMA checklist (Moher et al., 2014). The complete inclusion and exclusion process resulted in the identification of 631 articles. The flow diagram illustrating the literature review process according to the PRISMA 2020 model is presented in Figure 1, with the full procedure detailed in Appendix 1 and 2.

After completing the screening process and searching for additional references, the study was consolidated with a total of 48 articles. This analysis allowed for the classification of information to effectively address the research questions.

2.2 Most cited studies

Table 3 presents the twenty most frequently cited articles from the comprehensive review of both the Scopus and WOS databases. This review highlights that the most frequently cited study is titled “Government Support for SME Innovations in Regional Industries: The Case of Government Financial Support Program in South Korea,” authored by Soogwan Doh and Byungkyu Kim and published in 2014. The study examines the impact of government support policies on SME innovation within the regional industries of South Korea, with a particular focus on Gyeongbuk Province. The authors aim to contribute to the existing literature by analyzing the effects of government support on SME innovation and providing implications for other developing countries.

2.3 Geographical location and availability of information

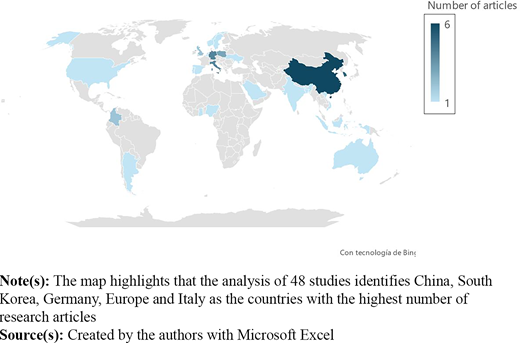

Figure 2 presents a choropleth map that highlights the countries or regions where studies have examined the impact of financing on innovation. A review of 48 studies indicates that the countries with the highest number of investigations are China (6 articles), South Korea (5), Germany (4), Europe (4) and Italy (4).

This concentration of studies can be attributed to the availability of data linking the intensity of innovation in SMEs with the financing channels used for R&D expenditure. As shown in Table 4, there is a positive correlation between the number of available databases for each country (excluding studies conducted with proprietary questionnaires) and the countries with the highest number of investigations.

2.4 Sectors of small and medium-sized enterprises represented in the studies

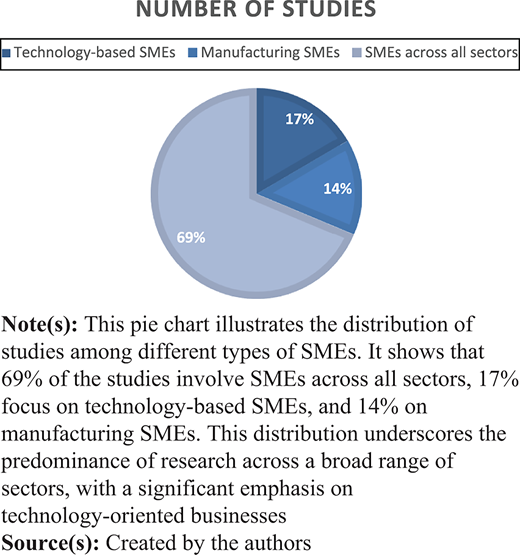

Figure 3 illustrates that the prevalence of studies in this review focuses on SMEs across all sectors (69%), technology-based SMEs (17%) and manufacturing SMEs (14%). The significant representation of technology-based SMEs, particularly in countries like China and South Korea, indicates a strategic emphasis on consolidating high-tech sectors as fundamental pillars of economic growth and industrial development. This trend is supported by various government initiatives and research efforts specifically targeting these companies.

For instance, the Korea Science and Engineering Foundation (KOSEF) provides substantial support through the Science and Technology Promotion Fund (Ju and Sohn, 2014), while technological development assistance funds in South Korea serve as substitutes for broader government support policies aimed at SMEs in regional industries (Doh and Kim, 2014). Similarly, the Chinese government has implemented tax incentives for research and development (R&D) to foster innovation within the technology sector (Shao and Wang, 2023). These initiatives create a favorable environment for sustained technological advancement in these regions, reinforcing the importance of technology-based SMEs in their economic strategies.

2.5 Models used in studies

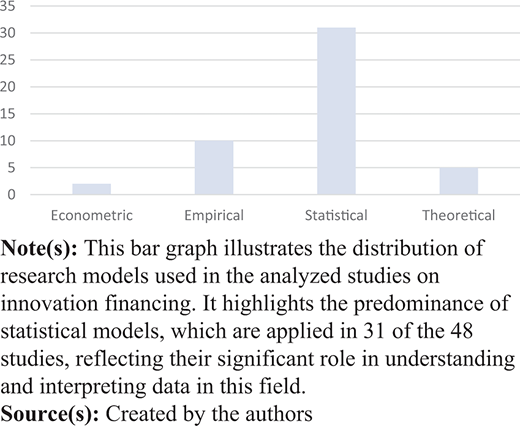

The literature reviewed employs a variety of models to analyze data using statistical and econometric approaches across different disciplines. Table 5 classifies these models into four categories: econometric, empirical, statistical and theoretical. Among these, statistical models are the most frequently used, with 31 out of the 48 studies applying this methodology.

According to Table 5, it has been observed that statistical models predominate among the methodologies applied in the reviewed literature, with 31 out of the 48 studies using this approach. This significant reliance on statistical methods underscores their importance in analyzing and interpreting data within the field of innovation financing. Figure 4 presents a bar graph that visually illustrates these findings, further highlighting the predominant use of statistical models in the studies reviewed.

3. Findings and discussion

This section presents a comprehensive review of the literature on various innovation financing channels for SMEs across different countries. It provides a detailed account of the number of studies conducted on each channel, their defining characteristics and the primary findings regarding innovation expenditure and outcomes, including radical, incremental, product and process innovation. This comprehensive analysis addresses the three research questions initially posed.

The first part of this section addresses the initial research question:

Which financing channels have been most studied by researchers?

It explores the motivations behind these findings and the focus on certain channels.

The second part tackles the question:

What is the impact of different financing channels on the innovation intensity of SMEs?

This analysis distinguishes between “traditional” and “emerging” financing channels, facilitating a nuanced understanding of the descriptive theory of each channel, particularly given that information on traditional channels is more prevalent than on emerging ones.

Finally, the third research question:

What is the future scope of research in the field of innovation financing related to each financing channel?

Is addressed by identifying gaps highlighted by the authors of the articles included in this review. This section examines the literature on how SMEs in various countries finance innovation, covering different financing sources, preferences, characteristics and findings regarding spending and results in radical, incremental, product and process innovation. It also discusses potential future research directions arising from the gaps identified in the reviewed articles.

3.1 The most examined channels of innovation financing

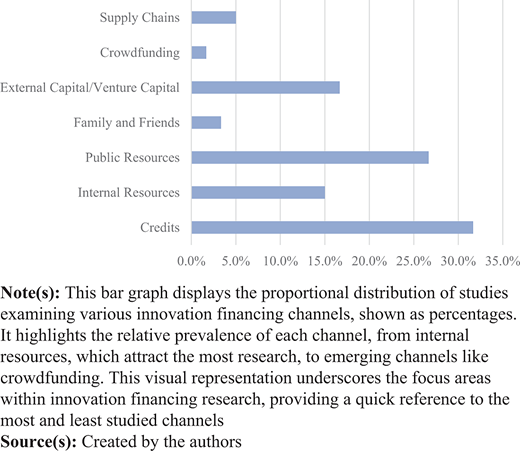

To address the initial research question, the study examined the most investigated financing channels, as presented in Figure 5. Researchers like Aiello et al. (2020) and Padilla-Ospina et al. (2021) have compared various channels to evaluate their impact on innovation and to facilitate a comparative analysis of results. Consequently, the total number of studies included in this section is higher. The channels most extensively studied in terms of innovation include bank credits (31.7%), government support (26.7%), external capital or venture capital (16.7%) and internal resources (15%). These are designated as “traditional” financing channels, while the remaining channels are classified as “emerging” financing channels. The most studied among the latter category are external capital/venture capital (16.7%), supply chains (5%), loans from family and friends (3.3%) and crowdfunding (1.7%).

3.1.1 Reasons for the prevalence of traditional channels.

Substitution of self-financing: SMEs often lack sufficient internal resources to fund innovation projects, making access to credit essential to cover the high costs typically associated with these endeavors (Kokot-Stepien, 2022; Scellato and Ughetto, 2010). Access to credit not only increases the capacity of SMEs to undertake innovations but also enhances the scale of their innovative activities (Padilla-Ospina et al., 2021), enabling them to compete with larger firms that have easier access to financial markets.

Data and information accessibility: Bank credits are one of the most accessible and widely available forms of financing for businesses and individuals. Due to their prevalence, they constitute a crucial area of interest for academic studies aiming to understand financing dynamics across various sectors and regions. The abundance of data, such as that available in Europe from the Survey on the Access to Finance of Enterprises (SAFE) administered by the European Central Bank (Guercio et al., 2020b), provides detailed and relevant information about the financing sources used by companies (Aiello et al., 2020). This data set enables robust and detailed analysis of the links between the decision to innovate and different financing sources. The systematic regulation and documentation of bank credits facilitate access to detailed information for empirical and comparative analyses.

Economic impact: Banks play a vital role in the economy by facilitating the flow of capital toward productive sectors. Minimizing the need for collateral to obtain external financing can boost the innovative activity of small businesses and, in turn, trigger economic growth (Kaur et al., 2022). Adequate financing through credits allows companies to invest in research and development activities, enhancing their capacity to innovate and compete in the market (Li and Zhang, 2023). Proper financing through credits enables these companies to expand, increase their service offerings and hire more staff, thereby contributing to overall economic development (Spatareanu et al., 2019).

Policy relevance: Governments and regulators are interested in how banks can support or inhibit innovation through their lending policies. If credit constraints are found to hinder innovation, policymakers might need to consider interventions to improve access to financing for SMEs (Guercio et al., 2020b; Mohammed, 2022). Similarly, SMEs might adjust their strategies on how they finance their R&D activities based on the findings of such research (Ali et al., 2024; Czajkowska, 2019). Studies in this area can influence policy formulation to enhance the efficacy of bank financing in innovation.

Comparability with other sources: Bank credits offer an interesting point of comparison with other financing sources, such as venture capital or crowdfunding (Aiello et al., 2020). Analyzing these contrasts may reveal the strengths and weaknesses of bank credits in different contexts.

Risks vs outcomes: R&D activities are typically high-risk and require long-term investment, making them less attractive for traditional credit financing, which often demands quicker returns and lower risks. Studying this area allows researchers to explore the complex dynamics between risk, financing structure and innovation outcomes (Ali et al., 2024).

Geographical differentiation: The role of bank credits in financing innovation varies significantly depending on the geographical and economic context, with substantial differences even between regions within the same country (Feng et al., 2021). This variability provides a fertile ground for research on the global and local dynamics of innovation financing.

3.2 Characteristics of financing channels

3.2.1 Traditional channels.

3.2.1.1 Credits.

According to the review conducted, credits are the most studied financing channel, representing 31.7% of the analyzed studies. These credits can originate from banks (Grilli et al., 2018; Scellato and Ughetto, 2010) or other entities, such as financial SMEs (Qamruzzaman and Jianguo, 2019). However, despite their prevalence, this channel is not necessarily the most influential on innovation (Aiello et al., 2020; Bougheas et al., 2003; Brown et al., 2012).

Financing innovation through this channel becomes a paradox for SMEs. On one hand, innovative companies face obstacles when accessing bank loans (Aiello et al., 2020; Roche et al., 2022). On the other hand, other authors such as Ayyagari et al. (2011), Archer et al. (2020) and Kaur et al. (2022) argue that external bank financing is positively and significantly related to the degree of business innovation, especially in the introduction of new products, enhancements of existing lines, opening of new plants and the establishment of companies abroad (Gregori et al., 2022). However, this type of financing is also negatively and significantly associated with the financial performance of these companies (Ali et al., 2024).

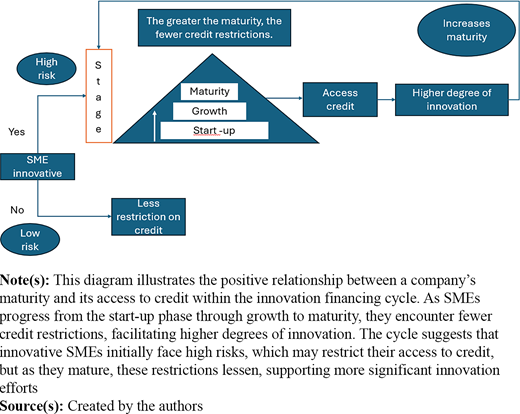

This paradox can be partly explained by the maturity of the innovation within companies and/or the specific stages of the innovation process (Feng et al., 2022). According to Nguyen et al. (2020), a positive relationship with access to bank loans is observed only when an SME has already implemented production processes or new technologies, especially in the case of short-term loans (Nunes et al., 2013). Conversely, this positive relationship does not exist when the company has not yet engaged in R&D activities. In fact, Guercio et al. (2020b) conclude that while innovation drives applications for external financing, it simultaneously hinders actual access to such funding. Figure 6 provides a graphical explanation of the innovation cycle, showing how innovation intensity increases as the company reaches a higher degree of maturity and gains greater access to credit financing.

A significant feature associated with financing through bank credits is their positive correlation with patents, a key measure of innovation in companies (Doh and Kim, 2014). Li et al. (2020) observed that companies in regions with greater banking diversity tend to have a higher number of patent applications and grants compared to those in regions with less diversity (Scellato and Ughetto, 2010). Authors such as Eldridge et al. (2021), Udimal et al. (2019) and Pederzoli et al. (2013) emphasize the importance of patents in fostering innovation and competition in markets. Patents provide valuable information for banks when assessing the risk of these companies, potentially alleviating the financial restrictions they face in the credit market.

In terms of financial innovation, which is distinct from innovation financing, this aspect is emerging as a developing dimension within SME innovation finance. It encompasses areas such as digital finance and microfinance with innovative support models (Qamruzzaman and Jianguo, 2019). These approaches are pivotal for business development as they facilitate access to credit for innovation at any stage of the business cycle.

3.2.1.2 Public resources.

Investments in research and development (R&D) are widely recognized as fundamental drivers of competitiveness and economic growth, particularly through the development of process and product innovations during periods of economic downturn (Aiello et al., 2020b; Shao and Wang, 2023; Wang and Kesan, 2022). This impact is observable at both the microeconomic level (Czarnitzki, 2002) and the macroeconomic level (Brautzsch et al., 2015).

Public funding for innovation can be classified into direct, indirect or combined mechanisms (EC/OECD, 2016). Direct funding allows governments to focus their efforts on activities that generate social benefits, even if they are not necessarily economic, while indirect funding reduces the marginal cost of spending on R&D and innovation, without discriminating between companies of different sizes. International examples of programs that facilitate innovation include the Small Business Innovation Research (SBIR) program in the USA (Mina et al., 2021), the Innterconecta program in Spain, which supports cooperative experimental development projects, the Torch Program in China, focused on the commercialization of advanced technologies and Horizon Europe, which funds innovation projects across Europe.

Public funding instruments, which vary by country, include subsidies, grants, tax credits, consulting services, tax incentives and innovation vouchers, among others (EC/OECD, 2016). These resources, representing 26.7% of the reviewed literature on innovation financing, are crucial for understanding how different nations approach support for innovation, with direct implications for the ability of companies to compete and grow in a global environment. The cases identified in the reviewed literature are detailed below.

3.2.1.2.1 Subsidies and grants

Subsidies, grants, tax credits and government support programs account for 29% of all analyzed aspects of financing innovation. These subsidies are often designed to stimulate innovation and business growth, particularly in emerging economies (Edeh and Acedo, 2021). They provide significant incentives for increased investment in R&D, thereby enhancing the innovative capabilities of firms (Al Wali et al., 2023). This support has been shown to result in the development of marketable product innovations (Aiello et al., 2020; Hottenrott and Peters, 2012; Huergo et al., 2016) and improvements in the productivity of innovation efforts (Aiello et al., 2020; Al Wali et al., 2023). The effect of subsidies on innovation varies between the manufacturing and service sectors. In manufacturing, subsidies tend to have a more significant impact on product innovation, whereas in the service sector, the focus appears to be more on process efficiency (Oh and Hwang, 2022).

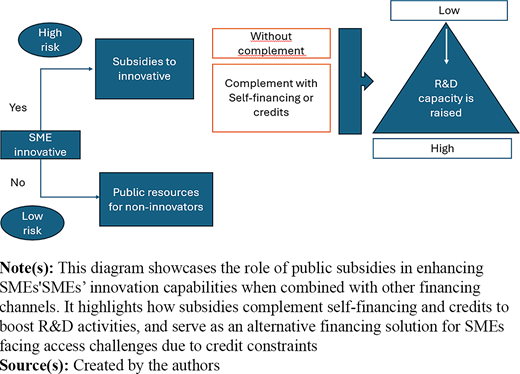

Public subsidies do not typically crowd out private investment in R&D (Czarnitzki, 2002; Møen, 2019). On the contrary, when complemented by other sources of financing, such as credit or self-financing, they can enhance the R&D capacity of smaller firms (Engel et al., 2019), as illustrated in Figure 7. For SMEs that face difficulties accessing financing due to issues like lack of transparency in their credit records or inability to provide collateral, subsidies and grants serve as alternative sources of innovation financing, making them effective tools for fostering innovation (Aiello et al., 2020).

3.2.1.2.2 Tax credits

Møen (2019) observed that tax credits are more effective than other instruments or channels in generating productive knowledge for firms and providing a higher private return. However, according to Brautzsch et al. (2015), the impact of R&D tax credits on stimulating innovative and patenting activities can be limited, depending on the specific characteristics of the country and industry.

3.2.1.2.3 Aid funds

In South Korea, Technology Development Assistance Funds (TDAF) have been provided by the government to promote technological innovation in SMEs, particularly in strategic regional industries. These funds have been positively correlated with the acquisition of patents and the registration of new designs by regional SMEs (Doh and Kim, 2014). The study by Edeh and Acedo (2021) found that the impact of financial support on innovation varies significantly based on the source of the funds – state, federal or foreign. Federal and foreign funds had a significantly positive impact on the intensity of R&D investment, whereas state funds did not show a significant effect on R&D expenditure. However, state funds contributed to the implementation of product and process innovations, although they did not significantly impact marketing innovations.

3.2.1.2.3 State regulations

Governmental support aimed at removing obstacles hindering SME growth can take the form of supply-side improvements, institutional modifications or demand-side interventions (Møen, 2019). State subsidies are particularly beneficial as they support investment in intangible assets, which are crucial for innovation in SMEs (Aiello et al., 2020). These subsidies tend to yield better technological returns compared to those aimed solely at new product development (Sohn et al., 2007). However, the effective management of these resources often requires efficient internal management or additional technological support from both central and local governments (Doh and Kim, 2014).

One of the main reasons for the extensive examination of state subsidies is their role in addressing market failures, as explained by Spence (1984) in the work of Bronzini and Piselli (2016). When public support is lacking, private investment in R&D may fall below socially optimal levels due to challenges such as the inability to appropriate the benefits of innovation, resource indivisibility and uncertainty. These obstacles can prevent firms from fully realizing the potential benefits of their innovations.

However, some researchers, like Mina et al. (2021), argue that many government programs designed to support SMEs may not always be effective, as they often fail to account for the fact that not all SMEs are inherently innovative. This oversight can expose these entities to high risks of irrecoverable losses, necessitating more targeted assessments to address the financial needs of companies with genuine growth potential. Moreover, while financial regulation can enhance the effectiveness of innovation during the financing and R&D phases, it might also introduce constraints that could hinder innovation during the operational stages (Feng et al., 2022).

3.2.1.3 Self-funding.

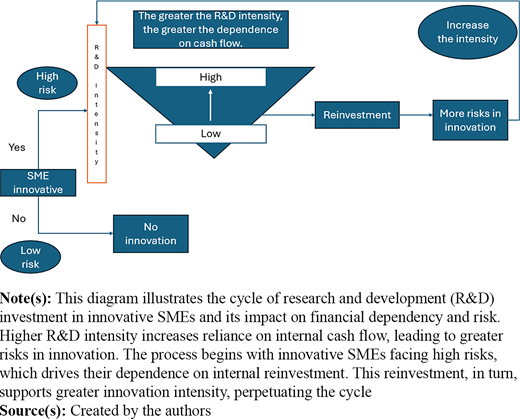

Self-funding, or the use of internal resources, is the third most used innovation financing channel, accounting for 13% of the cases studied. According to analyses by Kwak (2021) and Padilla-Ospina et al. (2022) based on the 2017 World Bank Enterprise Survey, SMEs often follow the pecking order theory, prioritizing self-funding for research and development (R&D) over external financing sources like bank loans. Self-funding operates as a self-sustaining cycle that fosters intrinsic innovation, as depicted in Figure 8. This cycle begins with the retention of profits, which are then reinvested into R&D activities, driving innovation within the company. Hall and Lerner (2010) emphasize that while these R&D investments may not always have a clear forecast of future profitability, they are crucial for developing new technologies and products.

SMEs with high R&D intensity tend to rely heavily on internal cash flow due to significant uncertainties and risks associated with innovation, making external capital both difficult and expensive to obtain (Nunes et al., 2013). As the risk of investment increases, external capital becomes costlier, leading to a disparity between the costs of external and internal funds. This scenario makes certain projects feasible only through internal financing (Berger and Udell, 1998).

The cycle of internal reinvestment not only fosters sustained innovation capacity but also allows companies to take calculated risks, enabling the continuous development of new technologies and products. By reinvesting retained earnings, companies can perpetuate a cycle of innovation, leading to the generation of additional profits that are subsequently reinvested.

In the context of complementarity between financing channels, Guercio et al. (2019) observed that companies managing internal funds tend to have a higher propensity to incur debt, thereby increasing their likelihood of loan approval. This suggests that financial institutions positively perceive the use of internal funds, interpreting them as a sign of prudent financial management. In addition, companies with high social capital are more likely to secure equity financing, which further promotes innovation and growth (Strom et al., 2023). Therefore, internal funds are increasingly recognized not only as substitutes but also as complementary resources that enhance the effectiveness of other financing channels.

3.2.1.4 External capital/venture capital.

When SMEs lack sufficient internal resources, they often turn to external financing options rather than issuing shares (Kwak, 2021). The use of external capital significantly increases the likelihood of undertaking innovative activities, as evidenced by Aiello et al. (2020). Multiple studies suggest that companies with foreign capital participation tend to be more engaged in innovative activities compared to those relying primarily on domestic capital (Guadalupe et al., 2012; Thangavelu and Findlay, 2018; Wellalage and Fernandez, 2019).

In this study, external capital is often referred to as risk capital when it comes from investors outside the company, although not all types of external capital are considered risk capital. Venture capital, specifically, is a form of external capital that is independently managed and focuses on equity or equity-related investments in private companies with high growth potential. Countries like the USA, Israel and Canada have well-established private venture capital sectors that aim to overcome the funding challenges faced by innovative startups (Hall and Lerner, 2010).

Venture capitalists offer SMEs more than just financial support; they provide management expertise, access to networks and contacts, performance monitoring, incentives for achieving high returns and enhanced portfolio credibility, all of which can stimulate innovation more effectively than direct financing alone (Rossi, 2015; Avnimelech and Teubal, 2008). However, it is important to note that venture capital is not solely invested in SMEs for innovation. The majority of venture capital funds are allocated to sectors that are not necessarily technologically advanced or to large and mature companies. Only a small proportion of funds are dedicated to select high-tech sectors through specialized small funds (Rossi, 2015).

The study by Hnoievyi et al. (2022) further underscores the role of venture capital as a catalyst for innovation and economic growth in SMEs. It highlights the importance of a supportive regulatory and financial environment that encourages such investments. In addition, it emphasizes the state’s role in fostering the adoption of innovative business models through public policies and public-private partnerships.

3.2.2 Emerging channels.

3.2.2.1 Crowdfunding.

Equity crowdfunding has emerged as a significant financing tool for SMEs, allowing them to enhance their innovation levels and better capitalize on growth opportunities (Eldridge et al., 2021). This financing model is particularly effective when investors exchange capital for an ownership stake in the company. Research shows that foreign equity participation through crowdfunding can substantially boost a firm’s innovation capacity by facilitating the transfer of advanced technologies and innovative practices from foreign markets to the domestic economy (Guadalupe et al., 2012). This process often necessitates concurrent investments in advanced fixed assets, human capital development and new organizational practices (Bakhouche, 2021). In essence, foreign capital, introduced through equity crowdfunding, plays a pivotal role in driving innovation by bringing in critical knowledge and technologies from abroad.

3.2.2.2 Supply chain.

Supply chain financing remains an underexplored area in the context of SME innovation, yet it offers a viable solution for overcoming resource constraints. Partnerships within the supply chain, particularly in R&D, have been shown to positively impact SME performance (Rezaei et al., 2015). However, partnerships in other functional areas have not demonstrated the same level of impact. The adoption of various supply-chain financing schemes, combined with the use of information technology, can significantly enhance SMEs’ financial performance, innovation capacity and market responsiveness, ultimately providing them with a competitive edge (Lu et al., 2020). Despite its potential, supply chain financing is an area that warrants further research to fully understand its implications for SME innovation.

3.2.2.3 Family y friends.

Funding from family and friends represents a unique and often underappreciated source of capital for SMEs. This type of financing can be particularly advantageous due to the “information advantage” stemming from the close relationships and trust inherent in these ties (Allen et al., 2019). Such informal funding sources can help SMEs overcome financial barriers, especially in situations where information asymmetry makes access to formal credit markets difficult (Aiello et al., 2020). However, research by Padilla-Ospina et al. (2021) indicates that in certain contexts, such as in Colombia, SMEs engaged in innovation do not rely heavily on informal loans or financial support from family and friends. This finding suggests a potential gap in the literature and raises questions about the applicability of traditional economic theories across different geographic and cultural contexts.

3.3 Interactions of financing channels and their impact on innovation

This section presents a detailed analysis of how each financing channel complements or substitutes others and its impact on innovation. Table 6 serves as a valuable tool for understanding the complex interactions that shape the financing ecosystem for innovation in SMEs.

This analysis highlights the nuanced roles of these channels in enhancing or inhibiting innovation depending on their application and the specific contexts in which they operate. The table also highlights the complexity of interactions between financing channels and different actors in supporting SME innovation efforts, revealing the strategic considerations that firms need to address to optimize their innovation potential and financial performance. This insight is crucial for policymakers, financial analysts and business leaders in structuring effective support frameworks for innovation-driven growth.

3.4 Future research

The comprehensive analysis of different financing channels for innovation has revealed a complex interplay of factors that influence their effectiveness and impact on SMEs. While significant insights have been gained, several areas require further exploration to address the third research question: What is the future scope of research in the field of innovation financing related to each of the financing channels? This review has identified key gaps and opportunities for future research that could provide deeper understandings of how these financing mechanisms support or hinder innovation. The following sections outline potential research directions based on the identified gaps, focusing on the roles of traditional and emerging financing channels, the influence of geographic and sectoral contexts and the interaction of these factors with company lifecycle stages. These directions are essential for refining strategies that enhance the efficacy of financial support to foster innovation in SMEs across various environments.

3.4.1 Bank credits.

Despite being the most studied financing channel according to this review, the field of future research remains broad. Key areas for further exploration include:

Research should investigate the interaction of financial factors with technological capacity and market competition and how these interactions impact the development of innovation activities in SMEs (Ayyagari et al., 2011; Padilla-Ospina et al., 2021);

The role of patents in banks’ credit risk assessments should be explored to understand how intellectual property can serve as collateral (Pederzoli et al., 2013; Spatareanu et al., 2019);

Future research should assess how government interventions can reduce financing barriers for innovative companies and how market fragmentation influences financial constraints for SMEs (Guercio et al., 2020b; Scellato and Ughetto, 2010); and

The way financing options vary across the lifecycle of a company, particularly for smaller and younger firms compared to larger and more established ones, is another crucial area for study (Guercio et al., 2020b).

3.4.2 Public resources.

Research on public resources could benefit from assessing the effectiveness of national fund evaluation programs in promoting science and technology, as well as their impact on innovation outcomes. In addition, there is a need to analyze how public resources influence commercialization strategies and the management of R&D projects, particularly in SMEs (Sohn et al., 2007).

3.4.3 Supply chains.

The supply chain channel offers several promising avenues for future research. To gain a more comprehensive understanding of the applicability of supply chain financing, it is essential to extend the analysis to other industries and types of companies, including low-technology firms. It would be beneficial for future studies to examine the discrepancies in how SMEs engage in supply chain partnerships and their performance in both developed and developing countries. The application of these methods could facilitate the measurement of the effectiveness of supply chain partnerships in different functional areas and the analysis of their relationship with SME performance (Lu et al., 2020; Rezaei et al., 2015).

3.4.4 Emerging innovation financing methods.

As technology continues to advance, it is imperative that research consider the emergence of new forms of financing for innovation. Credit guarantees, technology bonds and leasing represent emerging methods that may offer potential avenues for supporting innovation. However, further in-depth study is required to fully ascertain their viability (Kokot-Stepien, 2022; Li and Zhang, 2023).

3.4.5 Geographic and sectoral contexts.

Moreover, research should examine the disparate impacts of innovation financing on SMEs in emerging economies, with a specific emphasis on the service sector.

While studies have often focused on countries like China and South Korea, which offer robust support for technology-based companies (Doh and Kim, 2014; Feng et al., 2022; Kwak, 2021; Shao and Wang, 2023; Sohn et al., 2007), there is a need to expand research to less explored contexts.

In addition, future research should assess how service sector SMEs in emerging economies can transition to high-tech business models, considering the regional challenges and opportunities that exist.

3.4.6 Geographic gaps.

There is a notable lack of research in understudied regions, which demands attention. Areas like Latin America and Africa are still under-researched, indicating that findings from developed economies may not be directly applicable in these contexts. There is a necessity for a comprehensive utilization of available databases to bolster and stimulate innovation in SMEs within these under-researched regions.

3.4.7 Company maturity cycle.

Finally, the relationship between financing sources and the maturity cycle of companies is a crucial topic. Research has shown that SMEs only exhibit a positive relationship with access to bank loans, particularly short-term loans, once they have implemented production processes or new technologies (Nguyen et al., 2020). Understanding how other financing sources, particularly emerging ones like venture capital, crowdfunding, supply chains and loans from family and friends, influence innovation intensity according to the company’s maturity cycle presents an open avenue for future research.

These proposed directions aim to fill the gaps identified in this review, offering a comprehensive roadmap for future research in the field of innovation financing for SMEs.

3.5 Practical and policy implications

3.5.1 For small and medium-sized enterprises.

This study underscores the critical importance of using a combination of diverse financing sources to maximize innovation in SMEs. The reviewed literature highlights successful cases, such as the POIR 2014–2020 program in Poland, which facilitated innovation and access to capital through incentives for the amortization of technological investment loans (Czajkowska, 2019). Based on these findings, it is recommended that SMEs actively participate in public programs, leveraging government initiatives that provide incentives for innovation, such as the Central Innovation Program for SMEs (ZIM) in Germany, which strengthened R&D capabilities in response to economic crises (Brautzsch et al., 2015). In addition, SMEs should foster R&D collaboration networks by establishing strategic partnerships with other companies and academic institutions, emulating the success of the LECC program in Germany, which increased R&D spending and strengthened cooperation networks (Engel et al., 2019). Furthermore, SMEs should actively explore diverse financing sources such as venture capital, crowdfunding, credit guarantees and technology bonds as mechanisms to access new capital and validate business ideas more broadly and efficiently, ensuring they tailor these strategies to their specific industry and market context.

3.5.2 For policymakers.

Public resource support has proven to be an essential complement to other financing sources, enhancing SMEs’ ability to innovate and grow. Programs such as the SBIR in the USA and the SME Instrument of the European Union have been successful in supporting the financing of young and innovative companies (Mina et al., 2021). From these examples, key recommendations for policymakers can be drawn. First, policymakers should focus on creating an environment that encourages SMEs to diversify their funding sources by integrating public and private resources. This includes promoting public-private partnerships that facilitate access to financing for SMEs and encouraging collaboration in R&D projects. In addition, implementing tax incentives for private investors can increase investment in strategic sectors, complementing public sector efforts (Doh and Kim, 2014; Shao and Wang, 2023).

Simplifying access procedures by reducing bureaucracy and administrative barriers is essential to making financing programs more accessible and efficient for SMEs. Policymakers should work to create a more favorable regulatory environment that facilitates access to financing and promotes transparency and efficiency in resource allocation (Guercio et al., 2020b). This includes simplifying application processes, reducing documentation requirements and promoting digital platforms that allow faster and more efficient access to financing.

Furthermore, implementing favorable regulations is necessary to enhance the effectiveness of innovation, especially during the financing and R&D phases. A well-structured regulatory environment can reduce the risk associated with innovation investments, thus increasing the willingness of financial institutions to grant credit to SMEs (Feng et al., 2022). In addition, reviewing credit policies to include mechanisms that consider the use of patents as collateral could expand the financing options available to innovative companies (Pederzoli et al., 2013; Spatareanu et al., 2019).

Promoting sustainable innovation is also essential, ensuring that economic growth does not compromise the environment. This includes creating incentives for the development and adoption of clean technologies, as well as promoting sustainable business practices. Moreover, financing programs should align with sustainable development goals, prioritizing projects that have a positive impact on the community and the environment (Oh and Hwang, 2022).

Finally, improving policy evaluation and monitoring systems is key to measuring the impact of financing policies on SME innovation. This allows for the identification of areas for improvement and the adjustment of policies to maximize their effectiveness (Brautzsch et al., 2015). Policymakers should promote data collection and analysis of the results of financing programs, thereby facilitating a better understanding of the factors contributing to the success of SME innovation.

3.5.3 For researchers.

This study identifies several areas for future research, including the need to understand how SMEs in emerging economies and less technologically advanced sectors can adopt high-tech business models. Based on these observations, researchers are encouraged to implement multimethod methodologies that combine quantitative and qualitative approaches to gain a more comprehensive understanding of financing and innovation dynamics. It is also important to explore regional differences by investigating variations in financing practices between developed and emerging economies, with particular emphasis on Latin America and Africa, where significant knowledge gaps exist. In addition, evaluating the impact of new financing forms, such as credit guarantees, technology bonds and leasing, is essential to determine their effectiveness as tools for promoting innovation in SMEs (Kokot-Stepien, 2022; Li and Zhang, 2023).

These recommendations are fundamental for fostering innovation in SMEs, facilitating broader and more equitable access to the financial resources necessary for their innovative development.

4. Conclusions

The financing of innovation in SMEs is characterized by its diversity, reflected in the coexistence of multiple theories that address different aspects of financing. This study on financing channels has revealed significant findings and provided insights that can guide future research and policy.

First, credits obtained through banks or other financial entities emerge as the most studied financing channel, representing 31.7% of the studies. However, it has been found that SMEs, both innovative and non-innovative, face difficulties in accessing bank loans, especially those that have not engaged in R&D activities. Credits can have a significant impact on the ability of SMEs to innovate, but this impact is conditioned by factors such as the company’s capital structure, the availability of internal financing and the presence of information asymmetries. Although bank credits are the second preferred source of financing after internal resources, the pecking order theory suggests that this preference may vary depending on the specific circumstances of each company (Martinez et al., 2019). In addition, other factors such as patents and financial innovation that affect the development of innovation activities were identified and require further study (Eldridge et al., 2021; Padilla-Ospina et al., 2021; Pederzoli et al., 2013; Qamruzzaman and Jianguo, 2019).

Second, public resources, which include grants, subsidies, tax credits and government support programs, constitute the second most important source studied in innovation financing, representing 26.7% of the studies. These aids have demonstrated their ability to promote growth and business competitiveness through product and process innovations. The effectiveness of public financing mechanisms and instruments, whether direct or indirect, varies by context, with tax credits being especially effective in generating productive knowledge and providing higher private returns.

Third, internal resources represent 15.0% of the studies. Retained earnings play a crucial role in R&D investment decisions, and companies that use internal funds tend to show a greater propensity to undertake innovation activities. However, companies that rely on self-financing often find that internal funds are not sufficient to cover all their innovation financing needs, highlighting the need to explore new forms of financing.

External capital/venture capital is also a significant source of innovation financing, representing 16.7% of the studies. It plays a critical role in high-tech sectors and startups, providing not only capital but also management assistance, access to networks and monitoring of innovation performance. However, the focus of venture capital often extends beyond innovation to include sectors that are not technologically advanced or larger and more mature companies.

Family and friends financing accounts for 3.3% of the studies. This channel often provides an essential initial funding source for SMEs, particularly in the early stages of business development, but its impact on innovation is less explored and understood.

Crowdfunding is represented in 1.7% of the studies. Although it is a relatively new financing channel, it has shown promise in enabling SMEs to raise capital for innovative projects by tapping into a broad base of small investors.

Finally, supply chains represent 5.0% of the studies. This channel, though less frequently discussed, plays a vital role in providing resources and fostering collaboration between firms, which can lead to enhanced innovation and market responsiveness.

This study opens new directions for future research that could deepen our understanding of financing mechanisms and their influence on the success and sustainability of innovative SMEs. In the case of bank credits, it is suggested to explore how financial factors interact with technological capacity and market competition, as well as to evaluate the use of patents as collateral for loans (Ayyagari et al., 2011; Padilla-Ospina et al., 2021; Pederzoli et al., 2013). In addition, it is recommended to investigate how government policies can mitigate financial barriers and how credit market fragmentation affects SMEs (Guercio et al., 2020b; Scellato and Ughetto, 2010).

Regarding public resources, it is essential to assess the effectiveness of national fund evaluation programs and R&D project commercialization strategies (Sohn et al., 2007). In the area of supply chains, it is proposed to extend the analysis to other industries and types of companies, applying multi-criteria decision-making methods to measure partnerships and their impact on the performance of SMEs (Lu et al., 2020; Rezaei et al., 2015).

Future research should also focus on new forms of financing, such as credit guarantees, technology bonds and leasing, for which information is still scarce (Kokot-Stepien, 2022; Li and Zhang, 2023). In addition, there is a need to explore the impact of financing on SMEs located in emerging economies, especially in the service sector, to understand how they can transition to high-tech business models (Doh and Kim, 2014; Feng et al., 2022; Kwak, 2021).

Finally, the importance of studying the relationship between financing sources and the maturity cycle of companies is highlighted, especially with emerging sources such as venture capital and crowdfunding. Understanding how these sources influence the intensity of innovation according to the company’s maturity cycle represents an open gap for future research (Nguyen et al., 2020).

These future investigations will enrich our understanding of innovation financing and provide valuable insights for public policy formulation and business strategies. By addressing these challenges and opportunities, we can develop more effective strategies for supporting innovation-driven growth in SMEs.

This research was supported by the Ministry of Science, Technology, and Innovation of Colombia, Universidad de la Costa, and Universidad de Sucre.

Funding: Open access funding was provided by Universidad Cooperativa de Colombia.

References

Further reading

Appendix 1

Appendix 2. Glossary of acronyms

- AR

= Analysis of Requirements;

- AIFI

= Associazione Italiana del Private Equity e Venture Capital (Italian Private Equity and Venture Capital Association);

- BCS

= Business Characteristics Survey;

- BVD

= Bureau Van Dijk;

- CDTI

= Centro para el Desarrollo Tecnológico Industrial (Center for the Development of Industrial Technology);

- CIEM

= Central Institute for Economic Management;

- CIS

= Community Innovation Survey;

- CSM

= China Securities Market;

- CSO

= Central Statistical Office;

- DPMA

= Deutsches Patent- und Markenamt (German Patent and Trademark Office);

- EIT

= European Institute for Innovation and Technology;

- IDS

= Institute for Development Studies;

- KOSEF

= Korea Science and Engineering Foundation;

- LECC

= List of Enterprise Clusters and Companies;

- MIP

= Mannheim Innovation Panel;

- MRA

= Microcredit Regulatory Authority;

- NEEQ

= National Equities Exchange and Quotations;

- NICE

= National Information and Credit Evaluation;

- NIS

= Nigeria Innovation Survey;

- NTIS

= National Science and Technology Information Service;

- PITEC

= Panel de Innovación Tecnológica (Technological Innovation Panel);

- POIR

= Programa Operativo Inteligente y Responsable (Smart and Responsible Operational Program);

- R&D

= Research and Development;

- SABI

= Sistema de Análisis de Balances Ibéricos (Iberian Balance Analysis System);

- SAFE

= Survey on the Access to Finance of Enterprises;

- SBIR

= Small Business Innovation Research;

- SCOPUS

= No specific acronym; it is the name of the database.;

- SMEs

= Small and Medium Enterprises;

- TDAF

= Technology Development Assistance Fund;

- WOS

= Web of Science; and

- EC/OECD

= European Commission/Organisation for Economic Co-operation and Development.