This study examines the determinants affecting the adoption of blockchain technology in Jordanian audit businesses, emphasizing age disparities among auditors. This study significantly contributes by analyzing generational differences in blockchain technology (BCT) uptake, offering valuable insights into how age-related factors influence individuals' attitudes, perceptions and intentions toward adopting innovative technologies. By examining how different generations respond to BCT.

This research integrates the diffusion of innovation theory with the unified theory of acceptance and use of technology, utilizing structural equation modeling through AMOS to examine data gathered from 139 auditors in both Big 4 and non-Big 4 organizations in Jordan.

Observability, compatibility and relative advantages strongly affect adoption intention, emphasizing the need for explicit benefits and smooth integration. However, trialability negatively correlates with adoption, suggesting practical trials may slow adoption. The research shows that middle-aged and senior auditors (Generations X and Y) prioritize specific benefits, whereas younger professionals (Generations Y and Z) stress comparative benefits.

The study provides essential insights for audit firms and policymakers aiming to utilize blockchain technology, highlighting the importance of tangible utility and organizational alignment in adoption choices.

In addition to examining the determinants affecting the adoption of blockchain technology, this paper examines the generational differences that could influence technology usage and adoption.

1. Introduction

Blockchain technology (BCT), regarded as a fundamental innovation, stands as one of the most popular technologies, gaining significant attention from both academic and practitioner communities (Toufaily et al., 2021). Even though blockchain is a recent innovation, it is already revolutionizing the digital world by giving a new perspective on corporate processes' security, resilience and efficiency (Sciarelli et al., 2022). Blockchain is a technology that operates as a decentralized and distributed digital ledger. It is employed for recording transactions across multiple computers to prevent any past record from being altered without impacting all subsequent blocks (Han et al., 2023). BCT stands out as one of the most significant technological advancements due to its ability to ensure data privacy and integrity, facilitate rapid information sharing and enable the design and automation of process controls (Ferri et al., 2021).

The adoption of BCT has the potential to simplify the responsibilities of auditors (Alshurafat et al., 2023). While blockchain implementation is still in its early stages, acquiring knowledge about it can improve auditors' comprehension of its functionalities and potential applications and enable them to make more informed decisions regarding its integration (Handoko et al., 2020).

Generational differences significantly influence technology usage and adoption. Generation X and Generation Y exhibit a high level of engagement and frequent usage of technology (Vogels, 2019). Millennials, also known as Millennials, are defined as individuals born between 1980 and 1994, are followed closely by Generation X, individuals born between 1965 and 1979 (Ludwig et al., 2020). Moreover, Generation Z, born between 1995 and 2010, demonstrates an even higher receptivity towards technological advancements, especially in financial transactions (Hysa et al., 2021). Researchers suggest that Generation Z, as digital natives, are quickly becoming proficient information consumers and providers, equipped with advanced technological competencies (Sagheer et al., 2022). Although there are some overlapping features, Generation Z possesses distinct characteristics that set them apart from Millennials (Hysa et al., 2021). This study targets these generational cohorts due to their significant potential and distinct behaviors in technology adoption.

This study has more relevance when considering generational disparities among auditors, which might impact the way these aspects are perceived and addressed, potentially resulting in diverse reactions to the deployment of technology. This study addresses a significant gap in understanding the extent to which certain elements impact the inclination of auditors in Jordan to embrace BCT. In terms of this study's motivation, Jordanian audit businesses are currently at a critical point where the use of BCT could greatly transform audit processes (Alshurafat et al., 2023).

This study investigates the determinants influencing the adoption intentions of BCT in Jordanian audit firms, emphasizing five elements of the diffusion of innovation (DOI) theory–compatibility, complexity, relative advantage, observability and trialability–alongside the facilitating conditions factor from the unified theory of acceptance and use of technology (UTAUT). Furthermore, it examines how generational disparities among auditors affect these adoption processes.

2. Literature review

2.1 Blockchain technology background

BCT signifies a substantial progression in guaranteeing data integrity, facilitating real-time information interchange and automating process controls (Ferri et al., 2021). The decentralized and irreversible, time-stamped ledger prevents illegal alterations, presenting the potential to revolutionize company operations (Juma’h and Li, 2023). BCT provides essential advantages like privacy, transparency, immutability and efficiency (Sciarelli et al., 2022), enhancing confidence via traceability while decreasing expenses and optimizing record-keeping (AlShamsi et al., 2022). By removing intermediaries, it improves stakeholder engagement and facilitates secure global peer-to-peer transactions, including Bitcoin transfers. BCT offers strategic, organizational, economic, informational and technological benefits (Bag et al., 2023).

Recent research highlights a growing interest in understanding the adoption of BCT across various sectors in developing countries. Alkhwaldi (2024) extended the UTAUT model to explore how blockchain is being adopted in the accounting and auditing profession in Jordan. Their findings reveal that performance expectancy, social influence, blockchain transparency and efficiency significantly influence behavioral intention, while effort expectancy does not. This suggests that professionals in this field are more influenced by the practical benefits and transparency of blockchain rather than the ease of its use. Similarly, Dbesan et al. (2025) adopted an extended UTAUT2 framework to examine blockchain in the healthcare sector in Iraq. By introducing trust and knowledge sharing as key variables, they found that trust directly influences behavioral intention and is mediated by knowledge sharing, highlighting the importance of organizational culture and trust in sensitive environments like healthcare.

In contrast, Bhat et al. (2025) employed the technology–organization–environment (TOE) framework to study blockchain adoption in Omani small and medium entities (SMEs). Their research identified factors such as relative advantage, technological readiness and top management support as key drivers, while external factors like government policy and vendor support were found to be insignificant. This underscores the role of internal organizational dynamics over external influences in SME adoption decisions. Complementing these studies, Alkhwaldi and Aldhmour (2021) focused on the public sector in Jordan and identified key implementation barriers, including technological infrastructure gaps, institutional resistance and regulatory uncertainty. Together, these studies demonstrate that while blockchain holds significant promise across sectors, its successful adoption is heavily influenced by contextual factors such as trust, organizational support, regulatory readiness and sector-specific needs.

2.2 BCT impact on the auditing and accounting profession

Research underscores blockchain’s capacity to revolutionize auditing by improving efficiency, facilitating comprehensive and ongoing audits and redirecting emphasis towards control testing; nonetheless, revised standards are requisite (Elommal and Manita, 2021). Adoption is affected by performance expectations, societal pressure and implementation effort (Ferri et al., 2021).

BCT’s accounting reform potential has drawn attention. Juma’h and Li (2023) polled 118 US auditors and found that blockchain knowledge increases adoption intent, while faith in present standards decreases it, indicating resistance despite benefits. Desplebin et al. (2021) evaluate BCT’s future effects on accounting methodology, auditing procedures and auditor responsibilities and skills. These studies provide important insights into BCT adoption in various contexts, but a large information gap remains regarding the determinants of adoption in emerging countries like Jordan, especially among auditing professionals facing institutional and cultural constraints.

Therefore, this study seeks to fill a crucial gap in the current literature by examining how specific elements, as articulated through relevant theoretical frameworks, influence the willingness of auditors in Jordan to adopt BCT. The motivation for this research stems from the recognition that Jordanian auditing firms are at a pivotal juncture, where the integration of BCT holds the potential to significantly revolutionize traditional audit methodologies. As highlighted by Alshurafat et al. (2023), the adoption of BCT can lead to substantial enhancements in audit processes by increasing transparency, improving accuracy and fortifying the security of financial audits. Furthermore, previous studies such as Alzahrane (2024) emphasize that these technological advancements not only streamline operations but also foster greater trust among stakeholders by ensuring the integrity of financial data. By investigating these dynamics, this study aims to provide deeper insights into the factors that motivate or hinder auditors in Jordan from embracing BCT, ultimately contributing to the evolution of audit practices in the region.

3. Theoretical framework

The basic principles of the DOI theory, as described by Rogers et al. (2014) and Rogers and Williams (1983), provide a crucial perspective for analyzing the adoption of new technology. The reasons behind relying on the DOI theory in this study are as follows. This theory describes the psychological and sociological factors that affect how new technologies are adopted in social systems. It classifies adopters based on their willingness to try new things and emphasizes the importance of communication in spreading new technologies. Rogers' influential research lays the foundation for comprehending the adoption of technology on a broad scale. However, more recent studies, such as Skafi et al. (2020), build upon these ideas and adapt them to modern technological situations. The utilization of the DOI framework in this study provides a compelling method to investigate the detailed factors that either promote or hinder the acceptance of blockchain as a cutting-edge technology within organizations. This sheds light on the factors that facilitate or obstruct this transformative process.

Rogers et al. (2014) grouped adopters by innovativeness, firm size, resources and information and communication technology (ICT) management practices, and noted that technological attributes affect adoption decisions. These parameters prioritize objective technological factors over decision-makers' subjective opinions, according to Skafi et al. (2020). Rogers' DOI theory identifies five adoption factors: complexity (user-friendliness), relative advantage (perceived benefits), compatibility (congruence with current practises), trialability (experimentation) and observability (evident outcomes). Alternatively, enabling settings indicate a person’s perceived technology use control (Venkatesh et al., 2008).

4. Hypothesis development

4.1 Complexity and the intention to adopt blockchain technology

Rogers et al. (2014) outline complexity in innovation as the difficulty of understanding and using new technologies. This complexity includes both technological use and execution issues. Complexity in technological adoption often causes doubt among potential users, hindering their ability to understand and use the novelty (Choi et al., 2020). According to Wong et al. (2020), increased complexity reduces the likelihood of speedy implementation, which may reduce their willingness to adopt the technology.

How various generations use technology may affect their perceptions and adoption of blockchain in auditing. Millennials' ease with technology, inclination for social and interactive platforms and active engagement with digital content creation may make them early blockchain auditing adopters. Older generations' practicality and complexity concerns may first hinder adoption (Calvo-Porral and Pesqueira-Sanchez, 2020). The following non-directional hypothesis addresses generational gaps in technology adoption, even though past research has generally found a negative association between complexity and technology adoption:

There is a significant relationship between complexity and the intention to adopt blockchain technology in Jordanian audit firms.

There is a significant relationship between complexity and the intention to adopt blockchain technology among different generations of auditors in Jordanian audit firms.

4.2 Relative advantages and the intention to adopt blockchain technology

The concept of relative advantage in innovation, as described by Rogers et al. (2014), refers to the benefits that innovation can offer an organization. These benefits motivate companies to gain new knowledge, enhancing their absorptive capacity for adopting new technology. These advantages are employed to elucidate the acceptance of technologies by end users. The DOI theory suggests that the likelihood and speed of technology adoption are positively linked to its perceived relative advantage (Wang et al., 2022).

According to Culp-Roche et al. (2020), faculty development activities can assist faculty in learning, troubleshooting and integrating technology into online courses, making it less daunting, especially for those with less experience. Reverse mentorship, particularly beneficial for Generation X faculty, involves learning from Generation Y members to integrate new technologies. These relationships demonstrate the value of technology in teaching and reducing workload. Using available resources eases anxiety related to technology integration. Considering the diverse student population, younger students expect technological integration, while older students benefit from a blend of low and high-tech activities. Based on these factors, it is hypothesized that:

There is a significant positive relationship between relative advantage and the intention to adopt blockchain technology in Jordanian audit firms.

There is a significant positive relationship between relative advantage the intention to adopt blockchain technology among different generations of auditors in Jordanian audit firms.

4.3 Compatibility and the intention to adopt blockchain technology

Technology’s compatibility with an organization’s legacy systems, practices, information technology (IT) infrastructure and other networks is called compatibility (Choi et al., 2020). The congruence of innovation, management and business culture and practices is key to technological adoption. Li et al. (2022) found that construction businesses are more likely to embrace and use BCT when they believe it fits their corporate culture and business practices.

Referring to the research conducted by Agárdi and Alt (2022), it is evident that the acceptance of mobile payment technologies is greatly influenced by the perceived compatibility with modern lifestyles and payment habits, especially among Digital Natives (Generation Z). This parallel can also be observed in the field of auditing when considering the adoption of BCT. Therefore, it can be argued that there is a positive link between how compatible BCT is perceived to be and its adoption among different generations in the auditing profession in Jordan. Accordingly, the following hypothesis is proposed:

There is a significant positive relationship between compatibility and the intention to adopt blockchain technology in Jordanian audit firms.

There is a significant positive relationship between compatibility and the intention to adopt blockchain technology among different generations of auditors in Jordanian audit firms.

4.4 Trialability and the intention to adopt blockchain technology

Trialability is the extent to which an innovation can be tried before adoption (Rogers et al., 2014). Users try out technology or services to decide whether they want to acquire them (Rogers et al., 2014). Research shows that trialability influences technological adoption (Badi et al., 2021). Ullah et al. (2021) also found that trialability affects IS use intentions. Badi et al. (2021) found that respondents highly support trialability, meaning to test smart contracts on a small scale before adopting them to avoid perceived risks.

Trialability may assist organizations in comprehending BCT benefits and appropriately measure its worth (Li et al., 2022). Adding to Nakagawa and Yellowlees (2020), younger physicians, who are digital natives, are more likely to use new technology in their clinical practices. Auditors may follow this pattern. Being willing to experiment emphasizes the need to quickly test and integrate novel solutions into established systems. Younger generations' tech comfort and eagerness to experiment can help audit businesses implement user-focused solutions. The following hypothesis follows:

There is a significant positive relationship between trialability and the intention to adopt blockchain technology in Jordanian audit firms.

There is a significant positive relationship between trialability and the intention to adopt blockchain technology among different generations of auditors in Jordanian audit firms.

4.5 Observability and the intention to adopt blockchain technology

Observability is defined by Rogers et al. (2014, p. 244) as “the degree to which the results of an innovation are visible to others”. It is a general belief that organizations are more likely to adopt new technology when they witness the benefits experienced by other organizations adopting the same technology.

Blockchain innovation’s youth and lack of scale make it difficult to analyze empirical outcomes, signaling a need for further research and practical implementation before concluding. Some innovations are easy to define and observe, whereas others are too complex (Rogers et al., 2014). Thus, potential adopters' capacity to demonstrate an innovation’s utility boosts its adoption rate (Ajouz et al., 2020).

Based on the findings of Szymkowiak et al. (2021) regarding the effectiveness of observable and interactive learning aids for Generation Z, it is clear that these immersive educational experiences greatly improve engagement and understanding. Applying this idea to the professional field, namely in audit firms, emphasizes the significance of offering auditors tangible and engaging encounters with BCT. The advantages of BCT, such as improved efficiency, transparency, data quality and security in audit procedures, become evident when auditors can directly see and participate in environments that showcase these benefits. Thus, the following hypothesis is proposed:

There is a significant positive relationship between observability and the intention to adopt blockchain technology in Jordanian audit firms.

There is a significant positive relationship between observability and the intention to adopt blockchain technology among different generations of auditors in Jordanian audit firms.

4.6 Facilitating conditions and the intention to adopt blockchain technology

According to Venkatesh et al. (2012), facilitating conditions are one of UTAUT’s key constructs that determine technology use. Facilitating conditions refer to an individual’s belief in the existence of organizational and technical support systems for using a particular system (Venkatesh et al., 2003). This concept reflects an individual’s perception of their control over behavior. Generally, facilitating conditions entail an individual’s perceptions of access to technological and/or organizational resources, such as knowledge, resources and opportunities that can eliminate obstacles to using a system (Venkatesh et al., 2003).

These conditions may consist of customized technical assistance, intuitive interfaces and company policies that promote technology involvement. By catering to the distinct requirements of elderly auditors and offering supplementary assistance, audit firms can establish an all-encompassing atmosphere that encourages the extensive implementation of BCT among individuals of all age brackets, hence resulting in the following hypothesis:

There is a significant positive relationship between facilitating conditions and the intention to adopt blockchain technology in Jordanian audit firms.

There is a significant positive relationship between facilitating conditions and the intention to adopt blockchain technology among different generations of auditors in Jordanian audit firms.

5. Methodology

This study examines generational differences in the intentions of Jordanian auditors to use blockchain through a quantitative survey methodology, which provides cost-effectiveness, time efficiency and diminished bias (Malik et al., 2021; AlKubaisy and Al-Somali, 2023). It incorporates the DOI and UTAUT frameworks to merge innovative characteristics with behavioral motivators, facilitating an exhaustive examination of adoption trends (Alkhwaldi, 2024).

5.1 Population and sampling procedure

This study explores Jordanian auditors from Big 4 and non-Big 4 firms' generational views, experiences and decision-making processes to determine how they affect audit quality in diverse regulatory, cultural and economic situations. A random sample approach was used to ensure equal selection probability, using Microsoft Forms to distribute an online survey. LinkedIn surveys were sent to 200 randomly selected Jordanian audit firm auditors, yielding 139 completed replies and a 69.5% response rate.

5.2 Measurements and operationalizations

The questionnaire consisted of three sections: an introduction, demographic inquiries and adoption metrics utilizing a 5-point Likert scale. It comprised nominal data regarding auditors' qualifications, gender and age. Adoption was evaluated using elements from the DOI framework (Rogers et al., 2014), encompassing complexity (6 items) and advantages, trialability, observability and facilitation (5 items each). The adoption of blockchain was assessed through seven metrics.

6. Data analysis and findings

Table 1 indicates that all observable variables exhibited substantial loadings (0.416–0.838), surpassing the 0.4 criterion (Tamsah et al., 2020), hence affirming robust item-construct linkages. Reliability was evaluated using Cronbach’s alpha (α = 0.86–0.913) and composite reliability (C.R. = 4.678–9.651), both exceeding the 0.70 threshold (Ali et al., 2023). Average variance extracted (AVE) values (0.554–0.658) exceeded 0.5, signifying robust convergent validity. The measuring model exhibits exceptional construct validity, and discriminant validity is currently under evaluation.

6.1 Discriminate validity

The Fornell-Larcker criterion was used to assess discriminant validity by comparing the square root of each component’s AVE to construct correlations. The squared AVE exceeds the greatest correlation in Table 2, proving discriminant validity. Constructions are more strongly related to their indicators than others. All heterotrait-monotrait ratio of correlations values (Table 2) were below 0.9 (Gold et al., 2001), confirming discriminant validity. These findings confirm each latent construct’s uniqueness, improving the measurement model’s reliability and validity.

6.2 Descriptive analysis

Jordanian auditors' intentions to adopt BCT reflect a mixed yet positive perspective. They find blockchain somewhat complicated, with an average score of 2.398. However, they recognize its advantages, rating it at 3.601. Auditors view BCT as trainable, visible and compatible with their systems, with scores ranging from 3.410 to 3.597, suggesting ease of integration. As shown in Table 3, a mean score of 3.540 indicates that organizational support is seen as encouraging for deployment. Despite a moderate preparedness score of 3.520 for implementation, there is optimism about blockchain’s promise. More research is needed to address constraints and enhance acceptance in the auditing sector.

6.3 Correlation analysis

Table 4 demonstrates significant positive correlations between blockchain adoption and relative advantage (r = 0.746***), compatibility (r = 0.723***) and observability (r = 0.740***), suggesting that auditors who recognize BCT as beneficial, congruent with current practices and evident in its advantages are more inclined to adopt it. Trialability exhibits a somewhat positive association (r = 0.624***), indicating that the simplicity of experimentation promotes adoption.

Conversely, Complexity exhibits a slight negative association (r = −0.102), indicating it may impede adoption, albeit insignificantly. Facilitating conditions have a more robust positive correlation (r = 0.629***), underscoring the significance of supportive environments. The results highlight the significance of relative advantage, compatibility, observability, trialability and facilitating aspects in auditors' intentions to adopt BCT. No correlation surpasses 0.9, signifying the absence of collinearity concerns. The variance inflation factor (VIF) study corroborated this, revealing all values below 10 and an average of 2.41 (Buallay, 2022).

6.4 Structural equation modelling (SEM)

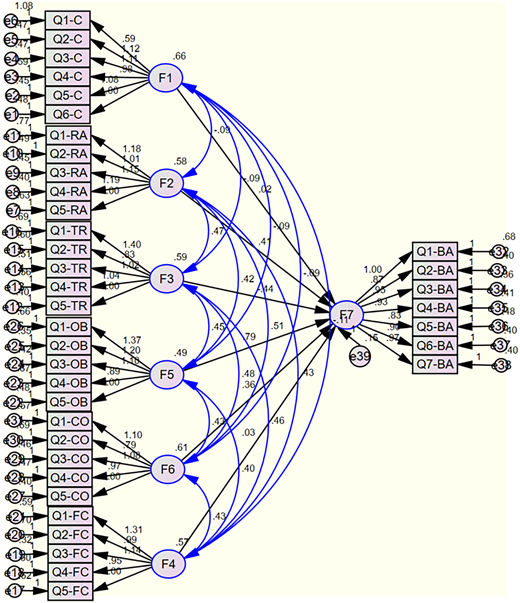

Structural equation modeling (SEM) technique has been using AMOS to study hypotheses. Figure 1 shows the relationship between the latent variables with the observed variables. Where F1 stands for complexity, F2 stands for relative advantage, F3 stands for trialability, F5 stands for observability, F6 stands for compatibility, F4= stands for facilitating conditions, F7= stands for blockchain adoption, Q represent observed variable.

6.4.1 Model fit criteria

A satisfactory match was found in the AMOS analysis, with a χ2 of 1629.308 (degrees of freedom (DF) = 644) and a CMIN/DF ratio of 2.529 (Marsh and Hocevar, 1985). Despite most indicators being good, sample size restrictions caused noticeable differences. The comparative fit index (CFI) (0.747) was below the 0.80–0.90 range (Adawi et al., 2019), although the root mean square residual (RMR) (0.086) barely exceeded 0.08 (Güzel, 2023). Root mean square error of approximation (RMSEA) (0.105) exceeded the ideal threshold of 0.08 but stayed within the permitted range of ≤0.10 (Aydin and Kabukçuoğlu, 2020). Smaller samples with sensitive fit indices have many minor variations. The model fits well, with variances indicating statistical noise rather than misconfiguration.

6.4.2 SEM results

As shown in Table 5, Path analysis identifies Jordanian auditors' main blockchain adoption factors. Observability has the greatest impact (β = 0.788, p < 0.001), followed by relative advantage (β = 0.405, p < 0.05) and compatibility (β = 0.361, p < 0.10). Trialability negatively impacts adoption (β = −0.441, p < 0.05), suggesting experimentation choices may inhibit adoption. Both complexity (β = 0.017) and enabling conditions (β = 0.029) are not significant (p > 0.05). These data support observability, relative advantages, compatibility, but not trialability, complexity, or facilitation.

The notably strong coefficient for observability (CR = 3.654) highlights the significance of visible blockchain advantages in adoption choices, whilst the adverse trialability effect (CR = −2.157) indicates unforeseen behavioral dynamics. All approved positive correlations exhibit critical ratios beyond 1.9, thereby affirming their statistical reliability regardless of differing significance levels.

6.4.3 Multiple Group Analysis

Multiple Group Analysis (MGA) determines hypothetical group relationship differences (Muharam et al., 2024). This study uses multi-generational methods to analyze auditor blockchain usage by age groups. Participants were divided into three cohorts: Generation X (born 1965–1979, ages 45–59 in 2024), Generation Y (1980–1994, ages 30–44) and Generation Z (1995–2010, ages 14–29) (Ludwig et al., 2020; Hysa et al., 2021). To improve data reliability and reduce bias, participants reported their age in defined intervals (<30, 30–39, 40–49 and 50–59 years) instead of self-identifying generational affiliations (Silva et al., 2015).

Table 6 demonstrates two adoption factors that varied significantly by generation. Benefits of BCT are more noticeable to senior auditors (Generations X/Y) than mid-career (β = 0.415, p = 0.077) or digital-native cohorts (β = 0.359, p = 0.08). This implies that experienced techies prioritize results when implementing new technology. Younger auditors (Generations Y/Z) view BCT use as more beneficial than older auditors (β = −0.452, p = 0.07). Young professionals are more like transitional adopters than established professionals, since digital natives, mid-careers and senior auditors share similar views.

Other adoption factors–compatibility, trialability, complexity and facilitating conditions–are generationally neutral. This consistency suggests that BCT adoption factors like perceived system compatibility and trial opportunities are equally important across age groupings. Consistency may reflect industry-wide technology adoption or professional norms that cross generational lines.

7. Discussion

We reject H1 because Jordanian auditors' complexity and blockchain adoption goals are adversely associated. Complex BCT may reduce auditor adoption, but this is minor. Similar resistance was identified among Australian firms by Malik et al. (2021). Because complexity did not vary by generation (Y, X, Z), H1a was rejected. Although small, Generation Z was more sensitive to complexity. This implies that generational IT familiarity does not affect complexity’s impact on BCT adoption in Jordan’s audit industry.

The strong positive link between relative advantage and Jordanian audit firms' BCT adoption supports H2. Research suggests adoption for transparency, efficiency and security (Hashimy et al., 2023). Mid-career auditors (Gen Y/Z) perceive more competitive advantages than senior accountants (β = −0.452, p = 0.07), indicating enthusiasm among younger professionals. Digital natives' blockchain assessments are more like transitional adopters' than either category, showing that career stage and professional experience matter more than age.

H3 was confirmed by a positive connection (p < 0.10) between compatibility and uptake in Jordanian audit businesses. Auditor acceptance increases when BCT meets systems and procedures, according to Malik et al. (2021). Implementing this alignment requires process and infrastructure changes. H3a was rejected because generational modifications did not affect compatibility. Although Generations Y and X exhibited higher compatibility sensitivity (Δ = 0.267 and Δ = 0.179), Generation Z had a little preference for Generations Y and Z (Δ = −0.088). Non-significant differences existed. Organizational and infrastructural alignment is more important than age targeting since compatibility affects adoption across generations.

The study rejects H4 because Jordanian audit firms' propensity to adopt blockchain is negatively correlated with trialability. Ironically, additional opportunities to test BCT may reduce uptake because of auditors' risk aversion, decreased self-efficacy, or doubt about its benefits.

Trialability and adoption intent were not significantly different across generations (H4a rejected). While not statistically significant, Generation Z had higher sensitivity than Y&X (Δ = −0.361) and Y&Z (Δ = −0.15), but surpassed Y&X (Δ = −0.211). Trialability makes Jordanian auditors' blockchain adoption unaffected by demographics. The lack of significant replies across age groups suggests that institutional preparedness or perceived use may exceed trialability’s benefits regardless of career level.

The unexpected negative correlation between trialability and adoption may reflect Jordanian auditing. Initial BCT experiments may show their complexity, technological restrictions and integration challenges, raising doubts. Trial environments in highly regulated and risk-averse professions like auditing may focus on short-term disruptions or compliance issues rather than blockchain’s long-term benefits. Professionals may view trialability as risky, preventing adoption.

A substantial positive correlation (p < 0.01) exists between observability and intention to use BCT in Jordanian audit firms, supporting H5. Alam et al. (2021) suggest that observability affects user decisions and technology adoption. The study shows that mid-career auditors value observable advantages more than younger generations (Δ: 0.415, p < 0.10) and Generation Z alone (Δ: 0.359, p < 0.10). The vulnerability of Generation Z is slightly higher than Y&Z (Δ: −0.056). Senior auditors (Y&X) may prefer observable risk management reliability, whereas digital natives (Z) may consider it inherent. Blockchain adoption must emphasize its benefits, especially for mid-career auditors using traditional and creative methods.

Rejecting H6, the analysis demonstrates a positive but statistically negligible relationship between facilitating conditions and Jordanian audit firms' blockchain commitment. While organizational assistance and resources should help adopt, their insufficient efficacy shows inadequate infrastructure or persistent hurdles, including legislative constraints, cultural opposition, technological complexity, or perceived hazards that may exceed current support systems. According to Chowdhury et al. (2023), institutional and geographical inequalities affect blockchain adoption patterns. Also, generational differences were modest (H6a rejected). Minor changes were observed, with Generation Z responding better to enabling conditions than Y and X (Δ: −0.213) and Y and Z (Δ: −0.148), while Y and Z slightly surpassed Y and X (Δ: −0.065). None were statistically significant. Systemic barriers (e.g. resource shortages or regulatory issues) are greater than generational constraints, as auditors at any career stage face insufficient support. Blockchain deployment in Jordan’s audit business may involve regulatory changes, talent development, or technical partnerships.

8. Conclusion

This study addressed Jordanian audit firms' blockchain BCT adoption drivers theoretically and practically. Compatibility and observability strongly influence adoption intent, suggesting auditors favor technologies that integrate with current procedures and provide measurable benefits. The high association between observability and trust indicates how utility visibility increases tech confidence. Trialability exhibited an unanticipated negative (although minor) effect on adoption, suggesting that early BCT exposure may increase perceived complexity rather than decrease it, indicating psychological hurdles to adoption.

The study’s findings on generational disparities offer profound insights into auditors' responses to adoption variables, indicating that mid-career professionals are more swayed by concrete benefits, whilst younger auditors concentrate on prospective advantages. These patterns indicate the necessity for adoption techniques that consider generational viewpoints, thereby enhancing current technology adoption models by integrating demographic factors pertinent to professional services. Practically, the findings suggest that audit companies must exhibit the tangible advantages of blockchain via pilot projects and case studies, while assuring integration with current systems. Training methodologies must be customized for different generations, prioritizing reliability and transparency for senior auditors and underscoring strategic importance for younger professionals.

The Jordan-centric focus may limit generalizability and more qualitative research is needed to improve comprehension. Future research should examine these dynamics in various situations, evaluate how changing regulations affect acceptance and track technical advances to improve auditing implementation strategies.