This study aims to revisit the existence of liquidity spillover effects between the US and European stock markets and investigates their dual-role structures. It examines which markets act as shock sources or absorbers or simultaneously assume both roles.

We employ entropy transfer to identify markets' roles. Additionally, a new multidimensional liquidity index is the primary variable in cross-market spillover analysis.

Evidence shows that the USA is both a source of shocks and a major absorber for the Austrian, Belgian, Swiss, Polish and Portuguese markets, alternately acting as both an absorber and a source of shocks, thereby confirming the hypothesis that the USA plays a dual role in this transmission network.

The dataset is limited to the US and 10 European countries. Expanding to include emerging markets in Asia or Latin America would improve generalizability. More critically, the divergence between Shannon and Rényi entropy suggests potential further exploration.

This study develops a multidimensional liquidity index grounded in the theory of liquidity spillover at the market level. The index holds substantial potential as a proxy for further empirical research on cross-market liquidity spillovers.

This study contributes directly to the theory of liquidity spillovers by revising the existing literature, which overemphasizes the USA as a source of shocks rather than other markets. The findings also support the efficient market hypothesis by showing that markets respond synchronously to shocks through cross-border liquidity channels.

1. Introduction

In the post-financial crisis and COVID-19 pandemic, the global financial system has increasingly demonstrated its deep interconnectedness and high sensitivity to liquidity shocks. The globalization of capital flows, the strong development of high-speed trading technology and the cross-ownership structure of assets between markets make it possible for shocks in one financial center to quickly spread to other regions, overcoming geographical and institutional boundaries (Carrieri et al., 2007; Arouri and Foulquier, 2012; Wu, 2020). In that context, identifying the nature, direction and structure of liquidity spillovers between major financial centers – especially between the USA and Europe – becomes essential. Most previous studies have approached the transmission from a one-way liquidity spillover model, in which the USA is seen as the primary source of global liquidity shocks, while European markets such as Switzerland, Portugal and Austria play a passive role as absorbers (Zhou et al., 2018; Shu and Chang, 2019; Aladesanmi, 2020; Zhang et al., 2021; Balli et al., 2021). However, this structure does not fully reflect the reality of an increasingly interconnected financial system, where financial centers can act as shock sources and absorbers (Mobarek and Mollah, 2016; Dimpfl and Peter, 2014; Choi and Yoon, 2023; Muñoz Mendoza et al., 2023). However, these studies have primarily focused on using stock market indices or macroeconomic risk aspects and have not been directly tested on the liquidity channel, except for the study by Muñoz Mendoza et al. (2023), which found that it remains unknown whether the United States can absorb liquidity shocks from other countries. The reason may be that Muñoz Mendoza et al. (2023) still analyze based on the liquidity measure variable spread, which lacks multidimensional market liquidity.

Accordingly, it is crucial to reexamine the dynamic and potential nature of liquidity spillovers across major markets. This study aims to fill this gap by testing the hypothesis that the USA can simultaneously act as both a shock source and a shock absorber of liquidity shocks affecting major stock markets in Europe.

The main novelty of this study lies in its dual perspective on liquidity spillovers, based on refined measurement approaches that construct a multidimensional liquidity index by integrating single proxies that only reflect one aspect of liquidity (Naik and Reddy, 2021; Le and Gregoriou, 2020). This index simultaneously reflects transaction costs, market depth and the ability to respond to information. In addition, the multidimensional liquidity index and entropy combination provide a new analytical framework to determine the direction and intensity of spillovers, allowing for the measurement of nonlinear and asymmetric causal relationships between markets.

The contribution of the study is not only to develop a new measurement index or apply a relatively new analytical method compared to previous studies but also to contribute to reshaping the framework of the theory of liquidity spillovers, moving from a unidirectional model to a bidirectional model in which financial centers such as the USA can both be sources and absorb liquidity shocks, which is a new approach that is closer to the reality of the system in the modern financial network.

The remainder of this paper is structured as follows. Section 2 outlines the theoretical foundation for the two core hypotheses. Section 3 introduces the construction of the multidimensional liquidity index and the use of transfer entropy (TE) as the primary analytical tool. Section 4 presents empirical results and robustness checks supporting the hypotheses. Finally, Section 5 discusses the theoretical contributions and practical implications for understanding the dual role of liquidity spillovers.

2. Literature review, theoretical framework and hypothesis development

2.1 Literature review

Over the past decade, the research stream on liquidity spillovers between the USA and Europe has been primarily dominated by the contagion framework in which the USA plays a central shock source (Table S1-Supplementary material). Typical examples include Zhou et al. (2018), Shu and Chang (2019), Aladesanmi (2020), Zhang et al. (2021), Balli et al. (2021), Anaraki (2010), Xiao and Dhesi (2010) and Attílio et al. (2024), which, although analyzed for different national scopes, have in common the USA as the center, as a major source in the global financial network. In this approach, the USA is the main source of liquidity shocks spreading to Europe, while European markets play a largely passive, receptive role. These findings reinforce the contagion framework in which the USA plays a central shock source, from which the shock spreads in one direction. However, this line of research leaves an essential gap in that there is no complete verification of the ability of the USA to also absorb or adjust to shocks from Europe, i.e. ignoring the possibility of a financial market network structure in which shocks spread and absorb feedback and markets adjust together, clearly reflected through the liquidity channel.

Notably, there is a recent study by Muñoz Mendoza et al. (2023) that also follows this line of research, somewhat opening the direction of testing the possibility of expanding the concept of the traditional one-way role and implementing another proxy for liquidity, which is spread instead of return or price volatility, as in previous studies. Muñoz Mendoza et al.'s (2023) results also identify the USA as a net transmitter, thereby maintaining the logic of one-way diffusion. However, the study of Muñoz Mendoza et al. (2023) not only asserts that the USA is a net shock source but also emphasizes the existence of multicenters when developed markets and some emerging markets also play a signaling role, i.e. extending the picture of liquidity spillover effects in a multicenter direction. From this perspective, the question can be asked: Can the USA also play the role of absorbers when facing shocks from other centers? However, the study of Muñoz Mendoza et al. (2023) does not provide an answer to this problem. Their key limitation lies in using only spread as a measure of liquidity. This unidirectional proxy reflects transaction costs but does not cover other important aspects, such as market depth, resilience or information absorption capacity.

Overall, it can be seen that the knowledge system over the past 10 years has still strongly leaned towards the thesis that the USA holds a central position, spreading shocks in a one-way contagion model, while lacking evidence and analytical frameworks that demonstrate a two-way spillover mechanism or mutual adjustment. This research gap is the basis for developing multidimensional measurement methods and expanding the theoretical framework to test the liquidity spillover effect not only as a one-way contagion phenomenon from the USA, but as a multidirectional network, where each pole can be a shock source and shock absorber, fully reflecting the reality of an increasingly complex global financial system.

Therefore, new approaches are needed to overcome the limitations of single liquidity proxies and be capable of capturing the intertwined structure. In this context, this study aims to develop a multidimensional liquidity index combined with an entropy transfer to clearly identify the dual role of the USA as well as the dynamic relationship between European markets. The expected results fill a gap in liquidity spillover theory and contribute to reshaping our understanding of the interconnected structure and synchronization of global financial centers.

2.2 Theoretical framework and hypothesis development

Liquidity spillover effects refer to the phenomenon in which changes in liquidity conditions in one financial market can affect other markets through direct or indirect transmission mechanisms (Brunnermeier and Pedersen, 2009). The degree of interconnectedness is becoming increasingly tight over time due to economic, political and institutional developments (Bekaert and Harvey, 1995) through channels such as capital flows, information and investor expectations (Daugherty and Jithendranathan, 2015; Aladesanmi, 2020). Structural reforms, financial liberalization and technological advancements in trading infrastructure significantly enhance integration by lowering barriers to international capital mobility and improving market efficiency (Arouri and Foulquier, 2012; Wu, 2020).

Liquidity spillovers can be explained through three main mechanisms: pricing linkage, capital and funding linkage and collateral linkage. Each mechanism reflects a different path through which liquidity shocks in one market can affect other markets (Anderson et al., 2015).

First and most importantly, pricing linkage is an indirect spillover mechanism through asset price movements in highly interconnected markets, explaining liquidity linkages between markets through the simultaneous variation of stock prices across regions (Sakthivel, 2012). Specifically, in cross-listed stocks or global ETFs, price movements in one market (e.g. New York Stock Exchange (NYSE)) can be quickly reflected in the linked market (e.g. Frankfurt). When a market suffers a liquidity shock leading to a rapid price drop and a surge in trading volume, other markets with pricing linkages will immediately adjust to maintain parity, creating a liquidity spillover effect (Anderson et al., 2015; Albuquerque et al., 2005; Sakthivel, 2012). Furthermore, the degree of covariation is not uniform across markets because it depends on the quality of liquidity – highly liquid markets tend to absorb information faster, reducing the covariation effect. In contrast, illiquid markets are more susceptible to spillovers from external shocks (Jafari et al., 2006).

Secondly, the capital and funding linkage mechanism plays a crucial role in transmitting liquidity shocks across markets. When global investors face a liquidity shock in a market, they often tend to restructure their portfolios, shifting capital flows to markets that are considered more liquid. This process not only further reduces liquidity in the original market but also puts pressure on the liquidity of the capital-receiving market. In particular, in the context of investment funds and multinational banks acting as intermediaries in capital allocation, a liquidity shock in a financial center like the USA can quickly trigger a wave of capital withdrawals in other markets in Europe (Anderson et al., 2015; Albuquerque et al., 2005; Sakthivel, 2012).

Third, collateral linkages represent another mechanism for the propagation of liquidity shocks across markets. In leveraged financial activities, such as derivatives or securitization, collateral plays a central role. When a stock market is under liquidity pressure and asset prices fall, the collateral value declines, increasing margin requirements or leading to forced liquidation (margin calls) in other markets. This effect is a chain reaction and can be amplified through the global leverage structure, thereby spreading liquidity risk throughout the system (Anderson et al., 2015).

Taken together, these three mechanisms indicate that liquidity spillovers are inherently multidirectional and depend on market structure, institutional integration and the relative position of markets within the global financial network. Importantly, they do not impose any a priori restrictions on the direction of liquidity transmission, implying that major financial centers may alternate between transmitting and absorbing liquidity shocks depending on the origin and nature of the disturbance.

Historically, the USA has occupied a dominant position in the global financial system due to its large and deep market, high liquidity and relatively low capital barriers. These characteristics have enabled the US market to act as a primary source of liquidity shocks, influencing other interconnected markets through pricing, capital and collateral linkages. A large body of empirical literature supports this view, documenting the central role of the US as a key transmitter of liquidity and financial information within the global financial network (Zhou et al., 2018; Shu and Chang, 2019; Aladesanmi, 2020; Zhang et al., 2021; Balli et al., 2021; Anaraki, 2010; Xiao and Dhesi, 2010; Attílio et al., 2024).

However, the deepening of bilateral trade, cross-border investment and financial integration between the USA and Europe has gradually weakened the traditional unidirectional spillover paradigm. From a theoretical perspective, the linkage mechanisms suggest that liquidity disturbances originating in European markets can also be transmitted to the USA. Through pricing adjustments, portfolio rebalancing by globally active investors and collateral-based leverage channels, the US market may internalize external liquidity shocks rather than merely propagate them outward. Existing empirical evidence in this regard remains limited but suggestive. Tilfani et al. (2020) document the transmission of macroeconomic and financial risk information from Europe to the USA, while Aladesanmi (2020) highlights the role of investor psychological factors (such as expectations, anxiety and herding) in facilitating bidirectional spillovers. Although these studies provide initial support for the possibility that the USA can act as a liquidity absorber, the evidence remains fragmented and lacks a systematic framework.

Consequently, there is still no comprehensive empirical assessment of the conditions under which the USA absorbs, adjusts to or amplifies liquidity shocks originating in Europe. This gap motivates the need for an analytical framework that conceptualizes major financial centers not only as dominant shock transmitters but also as dynamic shock absorbers or responders within an increasingly integrated global financial system.

To partly fill the above gap, this study tests the central hypothesis: “In the liquidity spillover effect between the US and European stock markets, the US is not only a shock source but also can absorb shocks from Europe.” This hypothesis is specified as a specific hypothesis testable with the entropy transfer model, presented in part 3.2.

If the central contagion hypothesis is empirically tested, the findings will advance the behavioral foundation of the liquidity contagion theory, shifting from a one-way contagion model to a two-way information flow structure. Within the framework of the theory of global liquidity contagion and modernized financial contagion in an increasingly interconnected network, major financial centers, such as the USA, simultaneously act as both transmitters and receivers of signals, alternating between these roles depending on market sentiment and risk perception.

This alternative transition reflects a shift from centralized contagion to decentralized behavioral synchronization, amplifying systemic sensitivity through feedback and expectation loops. The study thus establishes a behavioral-finance-based foundation for understanding liquidity network entropy rather than static contagion effects, capturing the reflexivity and adaptive complexity of modern financial systems.

3. Research methodology

3.1 Model specification and hypotheses

To empirically examine the liquidity spillovers between the US and European stock markets, this study adopts the entropy transfer framework, which captures the directional information flow between financial time series. Within this framework, we specify a model that evaluates the TE from the liquidity index of the USA to the liquidity index of a given European market i and vice versa. This method detects asymmetric and nonlinear causal relationships in a time series.

Formally, the TE from the USA to the European market i is defined as

Where:

X and Y are multidimensional liquidity index of the US and given European stock markets, respectively;

k is the lag order and

p (.) denotes the joint or conditional probability distribution estimated from the data.

This central hypothesis is transformed into two empirically testable sub-hypotheses within the entropy transfer framework, allowing for a formal assessment of both directions of information flow.

(Shock source hypothesis):

(no information flow from the US to country )

(the US transmits shocks to country )

(Shock absorber hypothesis):

(no information flow from country to the USA)

(country transmits shocks absorbed by the USA)

Where represents each of the 10 European markets: Austria, Belgium, France, Germany, the Netherlands, Poland, Portugal, Spain, Switzerland and the UK.

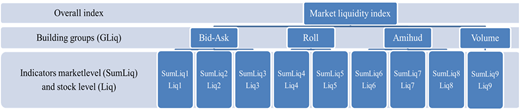

3.2 Multidimensional liquidity index

Liquidity is a multidimensional concept, with each dimension capturing different market characteristics such as transaction cost, market depth, resiliency and responsiveness to information (Le and Gregoriou, 2020; Fong et al., 2017; Aitken and Comerton-Forde, 2003; Shen and Starr, 2002). This diversity creates challenges for cross-market research due to the incompatibility and correlation among different measures (Huang and Stoll, 1997; Liu, 2006; Dong et al., 2011; Bhattacharya et al., 2019; Naik and Reddy, 2021; Chordia et al., 2000). When multiple liquidity dimensions react similarly to the same signal, they reflect market consensus; when divergent, they offer insights into investor heterogeneity. Therefore, combining various measures is necessary to fully capture market-wide liquidity.

Following the methodological foundation of Garabedian and Inghelbrecht (2020), this study adapts and simplifies their framework to construct a multidimensional liquidity index using nine daily liquidity measures, aggregated at the market level. The choice of low-frequency (daily) data over high-frequency (intraday) measures is based on coverage, accessibility and comparability across countries (Le and Gregoriou, 2020; Goyenko et al., 2009).

The construction of the multidimensional liquidity index follows a structured five-step process (Figure 1). First, the raw data (including trade volume, company capitalization, total return, enterprise value, outstanding share, open price, close price, high price, low price, turnover, bid close, ask close and company share) are collected through a process of filtering each stock according to the time it entered the market index calculation. Then, nine daily liquidity proxies are calculated at each stock level. Second, these stock-level measures are aggregated to the market level by applying market capitalization weights, ensuring that larger and more liquid firms contribute proportionally to the overall index. Third, the aggregated market-level series are normalized using the cumulative distribution function to enable comparability across countries and time. Fourth, the standardized measures are grouped into four liquidity dimensions, following the study of Garabedian and Inghelbrecht (2020), each representing a fundamental aspect of market liquidity.

Finally, these liquidity sub-indices are integrated into a single composite index by applying weight from principal component analysis (PCA) (Table S4-Supplementary material), based on reducing the dimensionality of the data to avoid duplication of information between different liquidity aspects, which incorporate signals that only some dimensions can pick up and that others might neglect, especially during times of extreme, or volatile, illiquidity pressure, capturing the co-movement among liquidity dimensions.

Additionally, the robustness of the constructed indices is validated through the eigenvalue decomposition in the PCA framework (Table S3-Supplementary material), which confirms that the first principal component captures most of the joint variation across the grouped liquidity measures. This validation affirms the internal consistency of the multidimensional liquidity index and strengthens the reliability of the subsequent spillover analysis, which relies on these indices as core inputs.

As a result, the study produces a panel of 11 standardized, market-level daily multidimensional liquidity indices, each corresponding to one of the countries in the sample. These indices are cross-country comparable and serve as the primary variables in the entropy-based modeling of liquidity spillovers.

The multidimensional liquidity time series for the US and each of the European markets be denoted as

X = : the multidimensional liquidity time series of US at day t.

Yi = :Each of the European markets at day t, where Y corresponds to one of the European countries (Austria, Belgium, France, Germany, the Netherlands, Poland, Portugal, Spain, Switzerland and the UK).

Where: symbolizes the vector of liquidity groups = (, …, ),

3.3 Data sources and sample

This study utilizes a dataset extracted from Refinitiv Eikon DataStream, covering all listed firms that are constituents of the major stock indices in eleven countries: the USA, Austria, Belgium, France, Germany, the Netherlands, Poland, Portugal, Spain, Switzerland and the UK. The dataset spans 14 years, from January 1, 2010, to December 31, 2023, encompassing various economic periods, including crisis periods and market recoveries.

The raw dataset comprises over 9,000 unique firm observations. Given the daily frequency, this equates to approximately 30 million firm-day observations across all markets. As a final output, the study constructs a daily multidimensional liquidity index for each of the 11 countries in the sample, generating 11 market-level liquidity time series that are consistent, standardized and analytically suitable for cross-market spillover analysis (Table S2-Supplementary material).

From a methodological standpoint, using daily data to construct the multidimensional liquidity index is empirically justified and sounds theoretical. Unlike high-frequency measures that require granular tick-by-tick data – often limited to mature markets and constrained by data access, privacy and processing costs – daily data offer a practical and consistent foundation for cross-country analysis (Le and Gregoriou, 2020). Moreover, daily observations are more sensitive to short-term liquidity shifts and microstructural dynamics than weekly or monthly data, allowing the index to capture better how markets absorb information shocks in near real time. Liquidity is not a static phenomenon; it fluctuates frequently due to changes in trading behavior, market sentiment and external macro-financial shocks. Therefore, daily granularity is essential to detect subtle but significant changes in market conditions – primarily when the index is intended for spillover analysis, where the timing of transmission across markets is a core concern. Finally, daily measures ensure sufficient data points for robust statistical inference, especially in PCA and entropy-based models requiring rich time-series variation. Daily frequency balances data richness, comparability, and macro-financial relevance for constructing a high-quality multidimensional liquidity measure across diverse market environments.

To summarize the disparate liquidity indicators belonging to some proxies into one composite multidimensional liquidity index, the process is presented in detail in Figure 1.

3.4 Rationale for the choice of transfer entropy

Traditional econometric models have long been used to study the interdependencies between financial markets. While these methods provide valuable insights, they are inherently limited by their reliance on linearity and parameter structure assumptions, which may not fully capture the complex and dynamic nature of financial markets (Syllignakis and Kouretas, 2010; Balli et al., 2021; Choi and Yoon, 2023; Attílio et al., 2024). Given that the central hypothesis of this study concerns the asymmetric and potentially nonlinear liquidity spillovers between the US and European stock markets, these limitations present a significant challenge to inference.

TE offers a compelling alternative. It is a non-parametric, model-free method that captures directional, nonlinear and time-varying dependencies, making it especially suitable for testing the hypothesized liquidity transmission. TE quantifies the magnitude and direction of information transfer between time series, which aligns with this study's empirical needs (Korbel et al., 2019; Bossomaier et al., 2016).

This paper's analysis incorporates both Shannon entropy and Rényi entropy as underlying information-theoretic measures for TE estimation. Shannon entropy defines uncertainty as the average information content of a probability distribution and has become a standard framework in information theory (Shannon, 1948). In contrast, Rényi entropy generalizes this concept by introducing a parameter q that adjusts the sensitivity of the entropy measure to common versus rare events (Rényi, 1961; Van Erven and Harremos, 2014). While Shannon entropy provides a fixed measure of uncertainty, Rényi entropy offers a family of measures with varying q, enabling a more flexible analysis of information dynamics.

Using both entropies in parallel is a robustness strategy: Shannon captures average-case dependencies, while Rényi helps detect structures that may emerge only during extreme market conditions – such as crisis periods – where liquidity spillovers can be most pronounced. This complementary use enhances the credibility of the entropy-based inference and allows for a more nuanced assessment of the hypothesis.

Three key advantages support the decision to adopt TE in this study. First, TE identifies the direction and magnitude of information flow between financial time series, capturing the asymmetries and long-term dependencies that traditional linear models often overlook (Junior et al., 2015; Jizba et al., 2012; Gong et al., 2019). Second, TE has demonstrated superior performance in detecting causality and quantifying intensity, offering insights into the centrality or peripherality of markets within global financial networks, especially under extreme conditions (Korbel et al., 2019; Ferreira et al., 2022). Third, the reliability of TE has been empirically validated in previous studies, including Behrendt et al. (2018), which confirmed the central role of the USA in transmitting information to European markets, and Bossomaier et al. (2016) and Gong et al. (2019), which affirmed TE's applicability to nonlinear and asymmetric financial systems.

To perform a robust test for the results from TE, the study uses an additional linear method, the vector autoregression, which is one of the most common econometric models that uses multivariate regression time-series analytic techniques to capture the linear interdependencies among multiple time series to determine interlinkages between markets (Zivot and Wang, 2006).

4. Results and discussions

The research results in Table 1 confirm the existence of a liquidity relationship between the US and European markets, as most of the transmitted entropy (TE) values in each pair show at least one direction with a positive value and reliable statistical significance. Accordingly, the hypotheses H1a and H2a were rejected, and H1b and H2b were confirmed; in other words, there is spillover of liquidity shocks across stock markets between the USA and Europe.

Firstly, using the Shannon entropy method, H1b was confirmed to be significant at the 0.05 level for 9/10 pairs (except the US-Poland pair). For Rényi's results, H1b was determined for 5/10 market pairs, including the US-Poland pair (left side of Table 1). In addition, the robust test results from the Granger causality (Table 2) coincide with the Shanon results when examining the hypothesis H1b.

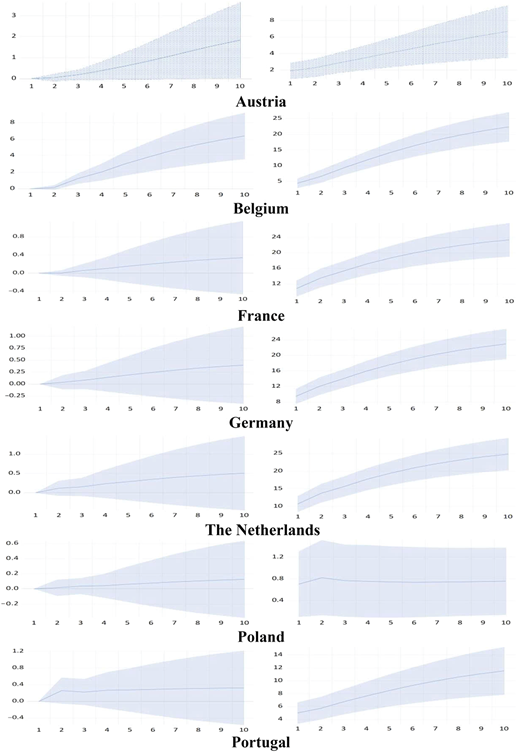

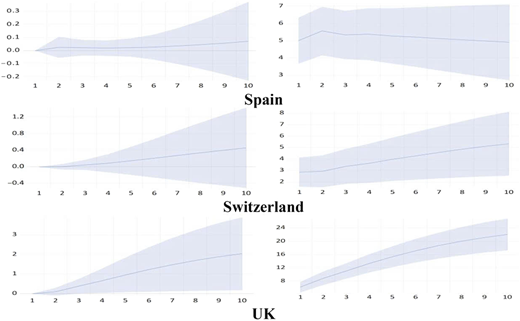

Moreover, the TE values from the USA to Europe are always larger than in the reverse direction from Europe to the USA, as the variance decomposition results (Figure 2) show, with shocks originating from the USA accounting for the majority of the forecast error variance in European markets (explanatory power ranging from about 5% to almost 25%). In contrast, the reverse impact of European markets on US volatility is significantly lower, typically in the range of 1–10%. The stability of the vector autoregressive models is confirmed when all eigenvalues lie within the unit circle, thereby ensuring robust estimates (Figure S2 – Supplementary material). The comprehensive results (traditional linear and nonlinear models), emphasizing the influence of the USA on Europe and reinforcing the central role of the USA as the primary source of liquidity information, once again confirm the results of previous studies, which show the systemic impact of the USA on global financial markets, especially Europe (Marfatia, 2020; Muñoz Mendoza et al., 2023; Li, 2021; Junior et al., 2015; Mahmoudi and Guerrero, 2016; Bastidon et al., 2023; Debata et al., 2021). The convergence of results is further strengthened by the use of multidimensional liquidity indices, which provide a more comprehensive view of liquidity across markets and a more rigorous foundation for analyzing the role of liquidity dynamics in financial market interdependencies.

Secondly, the TE results from European countries to the USA are used to test the hypothesis H2b to see if the USA is a shock absorber from European countries in addition to being a shock source and at the same time to test the existence of two-way information flow between these markets, as shown in the right part of Table 1. In detail, the results for each pair of US and European markets show that some European countries have bidirectional information flows with the USA, while others have only unidirectional relationships.

In the case of Austria and Belgium, the TE from the USA to Austria and the opposite direction shows a significantly stronger TE, a highly significant TE in both directions, and the robust test results also confirm the dual causality between the two countries. In the afternoon, Austria and Belgium receive significant information flows from the USA, as small, highly open economies are particularly vulnerable to financial shocks from larger markets like the USA (Gong et al., 2019; Mahmoudi and Guerrero, 2016; Baele, 2005; Nikolaos et al., 2009). On the contrary, Austria and Belgium exhibit a shock source to the USA; this is a new result that reflects the nonlinear interaction in liquidity transmission in small, open economies (Égert and Kočenda, 2011). Similarly, Poland and Portugal also exhibit two-way transmission with the USA. This suggests that peripheral European markets are susceptible to liquidity spillovers from the USA (Mahmoudi and Guerrero, 2016; Aladesanmi et al., 2019; Kopczewski and Bil, 2024). However, as mentioned, the reverse direction is significant only in the Rényi method, suggesting the existence of nonlinear, asymmetric and tail-dependent transmission mechanisms. These mechanisms often detect subtle information flows that linear measures cannot capture, such as strong bidirectional interactions arising from crises or extreme shocks (Aladesanmi et al., 2019; Shu and Chang, 2019; An et al., 2024). With Switzerland, the bilateral relationship with the USA is also notable, with significant information flow in both directions. As a global financial center, Switzerland often acts as an intermediary in information flows between regions, and its close connection with the US market has been noted in many previous financial studies (King and Wadhwani, 1990; Mahmoudi and Guerrero, 2016; Bastidon et al., 2023).

Thus, the H2b hypothesis is confirmed for the markets of Austria, Belgium, Switzerland, Poland and Portugal. The USA and these countries are both shock sources and absorbers. This shows that countries with less-developed markets are increasingly playing a dual role within a complex liquidity spillover network and that the world is becoming increasingly well-connected and balanced (Li, 2021; Muñoz Mendoza et al., 2023).

The remaining results for the five countries (France, Germany, the Netherlands, Spain and the UK) suggest that the US is a liquidity transmitter, as TE values from these countries to the USA are not significant in either the Shannon or Rényi methods. At the same time, the robust tests also indicated that France, Germany and Spain have only unidirectional relations with the USA. The US spillover caused a considerable shock to other markets, while the remaining countries tended to absorb rather than transmit liquidity flows to the USA (Zhou et al., 2018; Balli et al., 2021; Li, 2021; Shahzad et al., 2018; Aladesanmi, 2020). In addition, Europe is mainly influenced by large intra-bloc markets such as Germany, Switzerland or France (Guidi, 2008; Junior et al., 2015; Tilfani et al., 2020; Bastidon et al., 2023). Simultaneously, these markets are developed markets with well-established market structures, resulting in better information absorption and reduced susceptibility to external shocks, thereby reducing the effect of simultaneous variability (Jafari et al., 2006; Li, 2021).

In summary, the empirical results provide substantial evidence supporting both sub-hypotheses H1b (shock source) and H2b (shock absorber) for a subset of European countries. Specifically, information flows (i.e. both hypotheses accepted) are observed for Austria, Belgium, Switzerland, Portugal and Poland, suggesting that the USA acts simultaneously as a shock source and absorber concerning these markets. In contrast, for countries such as France, Germany, the Netherlands, Spain and the UK, only H1b is supported, confirming the USA as a liquidity transmitter.

Furthermore, the convergence across different estimation methods demonstrates a consistent directional pattern in most cases, thereby enhancing the robustness of the findings. However, a few inconsistencies between the Shannon and Rényi results (Figure S1- Supplementary material) (as in Poland and Switzerland) highlight potential nonlinear or tail-sensitive effects that warrant further investigation.

5. Conclusion

5.1 Theoretical contributions

This study makes a significant theoretical contribution by reframing the traditional unidirectional contagion paradigm into a framework of liquidity spillovers at the market level. While prior research has emphasized the dominant role of the US as a one-way source of liquidity shocks, our findings challenge this assumption (Zhou et al., 2018; Shu and Chang, 2019; Balli et al., 2021). Using entropy transfer methods, we provide robust evidence that liquidity spillovers play a dual role: the USA not only sources shocks but also absorbs them from specific European markets, especially in its interactions with Austria, Belgium, Switzerland, Poland and Portugal. These findings empirically validate the core hypothesis that the USA plays a dual role within a complex spillover network.

Also, building on Muñoz Mendoza et al. (2023), we propose a refined theoretical lens that incorporates pricing, funding, and collateral linkages as core transmission mechanisms (Anderson et al., 2015; Brunnermeier and Pedersen, 2009). Crucially, this framework repositions liquidity as an active and central conduit of systemic risk, rather than a passive outcome of price volatility. This study advances a more dynamic, interactive and realistic understanding of financial contagion in a globally interconnected system.

5.2 Practical implications

This study develops a multidimensional liquidity index grounded in the theory of liquidity spillover at the market level. Beyond its methodological contribution, the index provides regulators and policymakers with a comprehensive tool for tracking market efficiency and detecting systemic liquidity pressures at an early stage. For investors, it serves as a practical signal of overall market liquidity dynamics, helping them assess trading costs, timing of market entry or exit and potential contagion effects across assets. Moreover, the index holds substantial potential as a robust proxy for future empirical research on cross-market liquidity spillovers.

5.3 Limitations and further research

While this study offers a comprehensive analysis of liquidity spillovers across markets, several limitations remain. The dataset is limited to the USA and 10 European countries. Expanding to include emerging markets or financial hubs in Asia or Latin America would improve generalizability. More critically, divergence between Shannon and Rényi entropy – especially from Poland and Switzerland to the USA – suggests potential nonlinear, tail-sensitive or crisis-driven spillovers. Though not uniformly significant, these effects approach key thresholds and merit further exploration. Advancing this line of inquiry directly contributes to modernizing spillover theory in globally interconnected markets.

5.4 Conclusion

This study strengthens our understanding of global liquidity dynamics by analyzing information flows between the US and European stock markets. The results show a dual liquidity relationship: the USA remains the primary transmitter of financial information, while several European markets, including Belgium, Austria, Switzerland, Poland and Portugal, show strong two-way information transmission with the USA, reflecting a more complex and interdependent global financial landscape.

The supplementary material for this article can be found online.