This study systematically reviews sustainability measurement frameworks (SMFs) using the TCCM (Theory, Context, Characteristics and Methodology) approach to evaluate their theoretical foundations, contextual relevance, core constructs and methodological robustness across different types of enterprises, including commercial, non-profit and hybrid organisations.

A systematic quantitative literature review was conducted following the SPAR-4-SLR protocol. In total, 161 peer-reviewed journal articles published between 1994 and 2024 were analysed. The TCCM framework structured the analysis to synthesise theoretical, contextual and methodological patterns in SMF research.

The review found that existing SMFs predominantly rely on traditional theories like Corporate Social Responsibility and Stakeholder Theory and are mainly designed for commercial enterprises. Most SMFs inadequately address the needs of non-profits and hybrid organisations. Research remains heavily concentrated in high-income regions, and there is limited multidimensionality and contextual adaptability in existing frameworks.

This study uniquely applies the TCCM framework to the SMF literature, highlighting critical theoretical, contextual and methodological gaps. It calls for the development of inclusive, multidimensional and context-sensitive SMFs tailored to diverse enterprise types.

The findings suggest that policymakers, practitioners and enterprises must critically assess and adapt SMFs to better align with diverse organisational missions, particularly for social enterprises and non-profits, to enhance sustainability measurement effectiveness.

Developing more inclusive and contextually sensitive SMFs can better capture and support the sustainability efforts of mission-driven organisations, promoting broader social equity, environmental stewardship and community well-being.

This study uniquely applies the TCCM framework to the SMF literature, highlighting critical theoretical, contextual and methodological gaps. It calls for the development of inclusive, multidimensional and context-sensitive SMFs tailored to diverse enterprise types.

1. Introduction

The integration of sustainability into organisational strategy and performance evaluation has become central for scholars, practitioners and policy-makers. Sustainability, defined as the ability to preserve specific systems in a state of equilibrium or to bring intergenerational equality (Osorio et al., 2005), incorporates economic and social well-being alongside environmental protection. The 2015 adoption of the United Nations Sustainable Development Goals (UN SDGs) gained global momentum, linking sustainability to the intertwined challenges of poverty, inequality, climate action and responsible consumption (Scheyvens et al., 2016; Wonglimpiyarat, 2025).

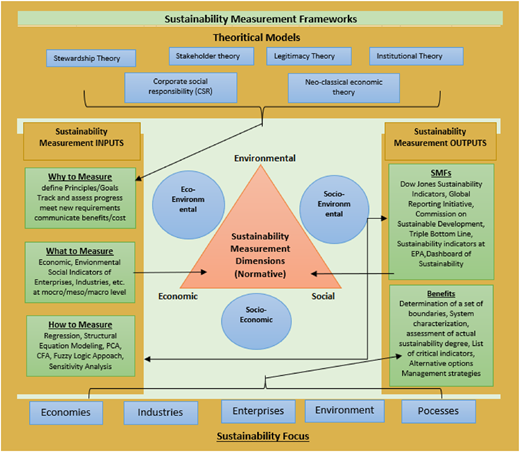

Governments, commercial enterprises (CEs) and social enterprises (SEs) are, therefore, expected to embed sustainability principles in governance, strategy and reporting (Al-Shaer and Hussainey, 2022; Initiative, 2002; Keeble et al., 2003; Picciotti, 2017). A wide variety of enterprises with different missions and objectives acknowledged the importance of sustainability measurement (Gandhi and Raina, 2018; Scheyvens et al., 2016) and, as a result, sustainability measurement frameworks (SMFs) have emerged as essential tools that provide structured methodologies to convert sustainability-related objectives into measurable indicators, performance benchmarks and informed decision-making processes (Ebenezer et al., 2020). These frameworks help align enterprise practices with stakeholder expectations, regulatory requirements and global sustainability standards (Scheyvens et al., 2016) and enable comparisons across enterprises by quantifying sustainability performance differences (Kamaludin et al., 2021; Ngwakwe and Ambe, 2016). In so doing, SMFs provide foundational indicators to measure sustainability based on measurable goals and attainable objectives, offering consistent benchmarking for enterprises to balance sustainability and their primary objective (Jayal et al., 2010; Mihalič et al., 2012; Qiu et al., 2018).

Three core frameworks shape contemporary sustainability measurement. Firstly, the Global Reporting Initiative (GRI) standards (revised in 2021) provide an integrated, double-materiality disclosure system aligned with emerging mandates such as the European Union's (EU) Corporate Sustainability Reporting Directive (CSRD) and IFRS-S2. Secondly, the Triple Bottom Line (TBL) reframes performance around “people, planet and profit”, serving as a normative lens rather than a prescriptive metric set. Finally, the International Organisation for Standardisation (ISO) 26,000 offers voluntary guidance across seven social-responsibility domains but lacks certifiable management system rigour, unlike other ISO standards. Although all three frameworks are nominally “open to any organization”, their uptake remains firmly corporate. For instance, KPMG's 2024 survey shows that 71% of the world's 5,800 largest companies and 77% of G250 multinationals use GRI, while practitioners flag ISO 26000's non-certifiable status and resource demands as obstacles, especially for SMEs. This corporate centrism clashes with the needs of SEs, whose goal is mission fulfilment rather than capital-market signalling. A recent UNCTAD survey found that, although more than 80% of SMEs view sustainability as material, only 7.7% publish reports, citing cost, complexity and fragmented standards as key deterrents (Pillai et al., 2024; Salavou and Manolopoulos, 2021).

The scholarship recognises the need for tailor-made frameworks that reflect these enterprises' hybrid logics and diversified impact metrics (Gandhi and Raina, 2018). Nevertheless, the literature remains fragmented regarding what should be measured and how, particularly for hybrid forms (Ali et al., 2023). SEs, for example, prioritise community engagement, social innovation and equitable outcomes, which are not typically accounted for in commercially focused frameworks (Pillai et al., 2024). SEs, non-profits and hybrid entities operate under different motives than CEs (Salavou and Manolopoulos, 2021), as their objectives extend beyond financial returns to social impact, inclusivity and environmental stewardship. An SE operates in the same market as a CE but with different objectives to cater for long-standing problems. However, sustainability measurement is less standard in SEs than in CEs due to the distinctive characteristics of SEs, such as objectives that aim to combine economic with social sustainability (Picciotti, 2017).

Fundamentally, prevailing SMFs lack the nuance required to achieve the sustainability performance of diverse organisational models (Gandhi and Raina, 2018). Current research offers limited guidance on which frameworks best serve specific enterprise forms or how foundational theoretical and methodological choices shape SMF design. Critically, no comprehensive synthesis evaluates available frameworks' contextual adaptability, construct validity and methodological rigour, and to address this gap, the present study conducts a Systematic Quantitative Literature Review (SQLR) guided by the Theory–Characteristics–Context–Methodology (TCCM) framework. This structured approach allows the study to answer the following:

What are the theoretical foundations that guide the development of SMFs in enterprise contexts?

To what extent are existing SMFs contextually relevant and adaptable to different enterprise types?

How are the core constructs and sustainability dimensions embedded in SMFs?

What methodological approaches have been utilised in designing, validating and applying SMFs?

This study endeavours to answer these questions using the TCCM framework (Paul et al., 2024; Paul et al., 2021b). It first investigates the predominant theoretical foundations that inform the construction of SMFs, which helps reveal how theory shapes the structure, metrics and priorities embedded in them. Next, the contextual relevance and adaptability of SMFs to various enterprise types are assessed then the core constructs and dimensions that reflect evolving paradigms in sustainability research are considered. Finally, the study reviews the methodological approaches employed in designing, validating and implementing SMFs in various enterprise types. It evaluates how methodological rigour influences the robustness and applicability of SMFs across different contexts (Paul and Menzies, 2023; Paul et al., 2021b).

This SQLR is organised as follows: Section 2 describes the research design by discussing the techniques used in synthesising the literature, reporting on the approach used in this study, followed by a descriptive analysis of the sample research articles. Section 3 presents a discussion and conclusion of the findings concerning the existence and applicability of SMFs among various enterprise types, while Section 4 discusses the limitations of this research and concludes the SQLR.

2. Methodology: scientific procedures and rationales for systematic literature reviews (SPAR-4-SLR) with TCCM framework

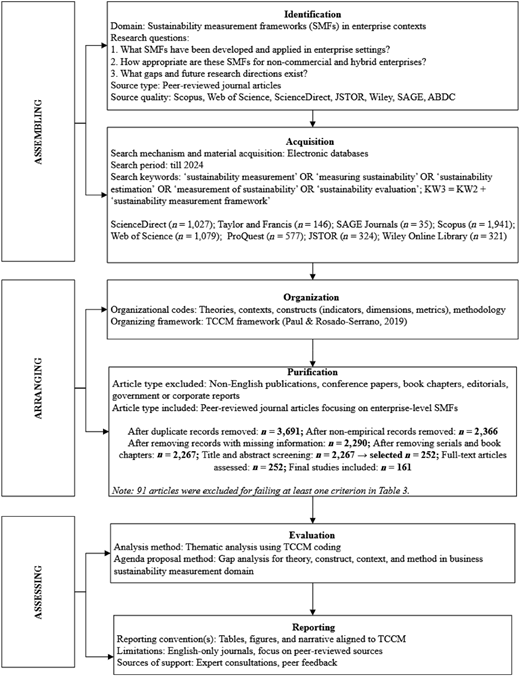

This study follows the SPAR-4-SLR protocol (Paul et al., 2021b) presented in Table 1, comprising the Assembling, Arranging and Assessing stages to ensure rigour, replicability and transparency in the SQLR. To further enrich the analytical process, the TCCM framework was applied to categorise and interpret the findings.

2.1 Assembling stage

This step focused on identifying and acquiring relevant literature that had not been previously synthesised following the SPAR-4-SLR guidelines (Paul et al., 2021a, b). Eight well-established academic databases were selected for the search—ScienceDirect, Taylor and Francis, SAGE Journals, Web of Science, Scopus, ProQuest, JSTOR and Wiley Online Library—based on their reputability and alignment with prior systematic review protocols (Paul and Dhiman, 2021; Paul et al., 2021b). These sources were deemed the most reliable for extracting bibliographic data on SMFs from diverse enterprise contexts.

The search strategy was informed by the core research objective: to deepen understanding of SMFs within the enterprise sustainability literature. To this end, a comprehensive keyword query was developed to capture relevant studies. The Boolean search string included the terms: “sustainability measurement” OR “measuring sustainability” OR “sustainability estimation” OR “measurement of sustainability” OR “sustainability evaluation” OR “sustainability measurement framework”. These keywords were applied across article titles, abstracts and author-defined keywords. Initial test searches confirmed that the first two keyword [1] sets captured the threshold of relevant literature and helped refine the query's sensitivity. No publication year or regional filters were applied during the search to allow for the broadest possible inclusion of studies. The keyword query returned 5,450 documents, as summarised in Table 2.

Under sub-stage 2 (acquisition) (Paul et al., 2021b), selected publications were validated based on the field of study and publication type. This SQLR used several selection criteria (Table 3) to refine the results and receive a more targeted selection of academic literature on the phenomenon under research (Klarin, 2024). Hence, the records were scrutinised using the following criteria.

The inclusion criteria demonstrate that selected studies articulate the theoretical foundations of SMFs using the TCCM framework. However, studies are excluded if they lack a coherent theoretical basis, focus solely on non-enterprise settings and validate isolated metrics outside a structured framework or context-irrelevant methods.

2.2 Arranging stage

The second stage of the systematic review, arranging publications, involved the structured organisation and careful purification of the literature to ensure relevance and methodological integrity. Initially, articles were systematically coded according to the TCCM framework during the organisation substage. Each study was classified based on its theoretical foundations “T”, research context “C”, sustainability constructs/characteristics “C” and methodological approach “M” (Grover and Garima, 2025; Prasanna and Kushwaha, 2025). This rigorous coding process enabled a coherent synthesis of diverse research contributions and facilitated comparative analysis across various dimensions of sustainability measurement.

Two domain experts jointly conducted the screening and coding processes in the purification sub-stage (Pomerlyan and Belitski, 2023), with the lead reviewer responsible for the preliminary identification, screening and coding of potentially relevant studies retrieved during the initial phases of the systematic review of methodological rigour and consistency. In the subsequent stage, all records were independently evaluated against the predefined eligibility criteria explained in Table 3 by both reviewers. Inclusion and exclusion decisions were carefully documented, each supported by a clear justification based on standard criteria. When discrepancies arose, the reviewers engaged in collaborative discussions to reach a consensus. This multi-stage review process was designed to uphold the integrity and reliability of the study selection procedure (Paul and Menzies, 2023).

The screening process systematically removed duplicate records, non-empirical publications, non-English articles and materials outside of the peer-reviewed journal literature. Subsequent title- and abstract-level screenings identified 252 articles for full-text review, and of these 161 met all inclusion criteria and were retained for synthesis. The remaining 91 were excluded because they: (1) did not directly examine SMFs; discussed sustainability in general; (2) lacked a coherent theoretical foundation, offering only descriptive or normative commentary; (3) focused on macro-level or policy issues rather than enterprise contexts; or (4) employed highly technical or sector-specific methods with limited relevance to organisational SMF development. For example, full-text screening eliminated studies that did not meet our enterprise-level focus (Table 3) and macro-scale resource assessments lacking an organisational context were excluded, such as Bronner and See's (2024) meta-frontier analysis of European water-use efficiency, Gao et al. (2023) and Zhao et al.'s (2023) appraisal of Yanbian's urban water resources, and Zhao et al.'s (2024) emergy As in the amount of energy consumed in transformations? Study of coupled water–soil systems. Sector-specific case studies without a recognised SMF were also removed, including Ceccato et al.'s (2023) life cycle estimate of MaaS environmental impacts in a medium-sized city and Briamonte et al.'s (2024) Key Performance Indicator (KPI) proposal for Italy's agri-food chain. Finally, city-scale planning and adoption research lacking enterprise-level SMFs, exemplified by Cvejic et al.'s (2023) ecological audit of urban forests and Ibrahim et al.'s (2024) fuzzy-set evaluation of autonomous-vehicle mobility, failed the “SMFs applied in enterprises” inclusion criterion. This rigorous filtering ensured that the final articles were theoretically sound, contextually pertinent and methodologically robust, providing a solid foundation for the systematic review (see Figure 1).

2.3 Assessing stage

The systematic review's third and final stage involved a thorough review of 161 peer-reviewed articles and focused on quantitatively and qualitatively evaluating the selected literature (Bhardwaj and Kalro, 2024), with the dual aim of identifying trends and uncovering research gaps in SMFs across diverse enterprise contexts. The assessment was structured around the TCCM framework, which enables multidimensional evaluation of the existing knowledge base.

3. General overview

3.1 Publication trend

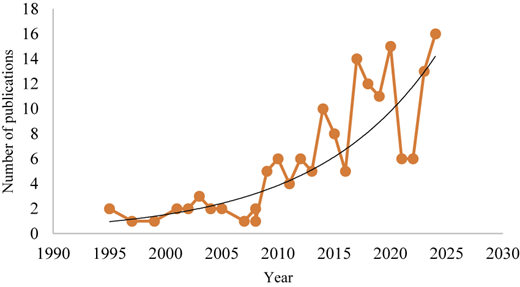

This SQLR study analysed papers published in peer-reviewed journals until 2024 (see Figure 2). The UN's SDGs Agenda 2030, building upon the introduction of the SDGs in 2016, produced a significant increase in sustainability measurement-related literature, as demonstrated in Figure 2. The UN SDGs require all enterprises to incorporate sustainability objectives into their policies coherently and holistically, and the sustainability measurement field experienced remarkable growth since half the papers in this study's sample were published between 2016 and 2024.

3.2 Top journals' contribution

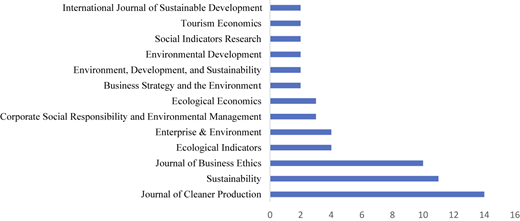

The bar chart below presents the distribution of journal outlets that contribute to the literature on SMFs and demonstrates that research on SMFs is concentrated in a few leading journals, with the Journal of Cleaner Production contributing the highest number of publications (15), followed by Sustainability and the Journal of Business Ethics, with 11 and 10, respectively, as illustrated in Figure 3, which suggests an interdisciplinary interest in environmental management, ethics and sustainability-focused journals. However, many high-impact journals feature fewer contributions, indicating that, while SMFs are gaining traction, the research is still relatively fragmented across diverse academic outlets.

3.3 Top cited studies

Table 4 presents a comprehensive overview of the most highly cited articles in sustainability measurement research, highlighting the scholarly influence, thematic breadth, theoretical orientations and regional origins of foundational works. Leading this compilation is the seminal article by Gladwin et al. (1995), cited over 3,300 times, which laid a critical theoretical foundation by challenging existing paradigms and advocating for a shift toward sustainable development within the context of management theory. Similarly, in the USA, contributions by York et al. (2003) and Veleva et al. (2001) reveal the focus on environmental and production sustainability and illustrate American scholarship's early dominance in shaping the field's direction.

4. TCCM framework application

4.1 Theories (T)

RQ1: What are the theoretical foundations that guide the development of SMFs in enterprise contexts?

This section offers a synthesis of the theoretical foundations that guide the development, structure and application of sustainability indicators. Guided by the TCCM framework, this SQLR identifies a range of dominant and emerging theories, categorised by their frequency of use, conceptual orientation and application across various enterprise contexts, based on the analysis of 161 peer-reviewed journal articles (see Table 5).

CSR theory is the most frequently utilised, with 19 mentions (Asiaei et al., 2021; Nigri and Del Baldo, 2018; Sardana et al., 2020) and provides a foundation for ethical governance and stakeholder accountability, particularly relevant to corporates, SMEs and supply chain-oriented organisations. Stakeholder Theory, cited in 12 studies, emphasises inclusive engagement of multiple actors in sustainability-related decision-making processes and is widely adopted across corporate governance and non-profit sectors (Johansen and Nielsen, 2011a, b; Schaltegger et al., 2019). Moreover, the GRI, which appears in nine studies, offers an institutional reporting model widely used in ESG disclosures and benchmarking practices (Delai and Takahashi, 2011; Fonseca et al., 2014). The RBV (Almada and Ferreira, 2022), mentioned in seven studies, links sustainability innovation to firm-level capabilities, often applied within contexts of competitive advantage and environmental innovation.

Both the Sustainability Disclosure Theory and the Ecological Modernisation Theory are referenced in four studies. The former supports transparency in sustainability practices through standardised reporting, while the latter aligns economic development with environmental sustainability, typically reflected in environmental policy and cleaner production systems (Ramos and Caeiro, 2010; Rodrigues Pinto et al., 2020). In addition, the Life Cycle Assessment (LCA), the Institutional Theory and the Neo-classical Economic Theory are all cited in three studies and emphasise environmental auditing, the influence of regulatory institutions and the economic valuation of sustainability trade-offs. In addition, the Stewardship Theory, the Legitimacy Theory and the Contingency Theory appear in two studies, which highlight long-term accountability, alignment with societal norms and contextual adaptation in SMF design (Crossley et al., 2021; Daddi et al., 2017; Yusuf et al., 2023).

Despite this theoretical variety, the literature remains heavily skewed toward CEs (Dang and Serajuddin, 2020) and a critical gap exists in integrating theories tailored to non-commercial, hybrid and SEs. Notably, no dominant theory in the research to date explicitly addresses the distinct needs of non-profit organisations, such as the Inclusive Growth Theory, the Social Justice Theory, Social Impact and Regenerative Sustainability (Goel and Misra, 2017; Laurett et al., 2021; Li et al., 2012; Panizzolo, 2021). While these provide structure, they are predominantly rooted in corporate logic and lack relevance for non-profit, hybrid and mission-oriented enterprises. This finding contributes to theory by revealing a gap in inclusive theoretical modelling and calls for new frameworks integrating social impact, equity and community-driven value creation, underserved areas in SMF scholarship.

4.2 Contexts (C)

RQ2: To what extent are existing SMFs contextually relevant and adaptable to different enterprise types?

4.2.1 Regional contributions to SMFs

The reviewed literature spans a wide array of contexts but reveals significant imbalances in representation. Geographically, most studies originate from high-income regions, particularly North America and Europe, while scholarly contributions from Asia, Africa and Latin America remain limited. This skewed distribution raises concerns about the global applicability and contextual relevance of existing SMFs, especially for underrepresented and developing regions. Studies from developed economies primarily address formalised frameworks (e.g. GRI, ISO standards), with strong attention to environmental performance, corporate reporting and investor accountability, but these models often presuppose reliable data systems, regulatory oversight and institutional capacity. In contrast, research from developing countries emphasises contextual adaptability and local stakeholder inclusion, pointing to persistent challenges in data access, policy enforcement and resource availability. This contrast highlights the need to contextualise SMFs rather than apply models developed elsewhere without adaptation.

The data in Table 6 illustrate the regional distribution and temporal evolution of research contributions on SMFs from 1994 to 2024. Europe is the most prominent contributor, accounting for 45 of 161 studies, which mirrors the region's integrated commitment to sustainability in policy, research funding and higher education. Statutorily, the EU-embedded non-financial disclosure a decade ago as the 2014 Non-Financial Reporting Directive mandated large undertakings to publish environmental and social data, and its 2023 replacement, the CSRD, will extend compulsory reporting to nearly 50,000 firms to generate demand for sustainability measurement tools and the scholarship that underpins them (Krasodomska et al., 2020). Financially, Europe has channelled exceptional public investment into sustainability research, such as Horizon 2020, allocating almost €80bn to research and innovation (2014–20), including “Green Deal” calls that funded 73 climate- and biodiversity-focused projects, with Horizon Europe (2021–27) continuing this trajectory (Soete et al., 2021). European universities and business schools embed sustainability more deeply than most regions, with dedicated SDG offices, institution-wide strategies and compulsory ESG coursework now common across higher-education institutions. The Americas (n = 32) and Asia (n = 21) also demonstrate significant contributions, particularly in the period from 2015 to 2024. This upward trend signals a growing international recognition of sustainability as a research priority and suggests diversifying scholarly engagement across varying socio-economic and institutional contexts. Although historically underrepresented, developing countries and the BRICS nations showed a noticeable rise in contributions during 2020–24, highlighting an increasing focus on contextually appropriate and locally grounded sustainability measurement tools.

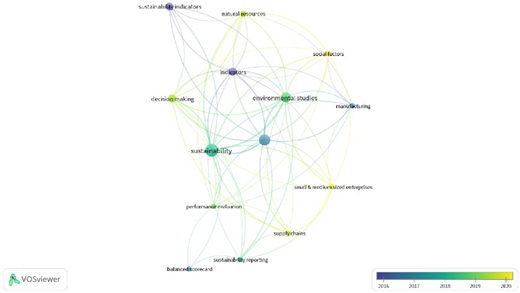

Additionally, in the contextual analysis of SMF-related literature, this study identifies key research themes through keyword co-occurrence analysis (Klarin, 2024) (see Figure 4) and its method enables mapping core concepts by examining the frequency and relational structures among keywords extracted from 161 peer-reviewed studies. This technique distinguished 12 major thematic clusters and items within the SMF literature, as presented in Table 7.

Keyword co-occurrences analysis was undertaken (Amini et al., 2018; Arici and Uysal, 2022) to identify various SMF global themes in the literature and consisted of a frequency count of concepts and mapping of these concepts within the sample of research articles. The map locates concept images in proximity to others, denoting they are similar in meaning or share relationships within the dataset, as concepts were grouped according to their mutual relevance. The concept image was “dot”-sized, demonstrating the frequency of its appearance in Figure 4 as a visual presentation of the analysed SMF concepts. The dots highlight the predominant clusters that emerged, such as sustainability, corporate sustainability, environmental sustainability, use of sustainability-related themes and sustainability-related analysis.

The keyword co-occurrence analysis further focused on economic, social and environmental domains. In the enterprise context, economic sustainability optimises production processes, job creation, contribution to economic activity and revenue maximisation (Johansen and Nielsen, 2011a, b; San-Jose et al., 2011) and, though they are more subtle, income-generating sustainability activities can also be strategically established to create economic value. The social sustainability of an enterprise is often linked with CSR, despite this concept being often broader in that it generates collective social welfare, including for employees and members of society (Austin, 2006). Enterprise environmental sustainability primarily relates to the integrity of the ecosystem, such as goals to lower the capacity for global resource utilisation rates as opposed to furthering resource regeneration (Figge et al., 2014; Passetti and Tenucci, 2016).

Furthermore, early SMFs focused on economic and environmental metrics grounded in conventional paradigms such as ecological modernisation, resource efficiency and neo-classical economic theory. In contrast, more recent studies demonstrate a growing incorporation of social and governance dimensions that reflect a transition toward holistic, multidimensional constructs. Additionally, the analysis reveals an uneven distribution of these constructs across contexts, with a concentration of studies in high-income regions. This geographic skewness signals a gap in the applicability of SMFs to low- and middle-income countries and marginalised organisational types, as presented in Table 6, which highlights the limited generalisability of dominant frameworks and the urgent need for more adaptable, context-sensitive models that can support sustainability goals in varied institutional and cultural settings.

This section responds to RQ2, which demonstrates how SMF's core constructs and sustainability dimensions mirror theoretical advancements and the expansion of paradigms in sustainability research. However, it also exposes a substantial gap: current SMF clusters do not sufficiently address the sustainability needs of non-profit and mission-driven enterprises. The lack of theoretical integration that embraces equity-driven, non-market-oriented frameworks limits the capacity of SMFs to function effectively across diverse organisational types. This SQLR contributes new insight by demonstrating dominant SMFs' contextual rigidity, revealing their limited adaptability to SEs and developing-country settings and underscores the urgent need for more flexible, context-sensitive models responding to varying institutional and cultural realities.

4.3 Characteristics/constructs (C)

RQ3: How are the core constructs and sustainability dimensions embedded in SMFs?

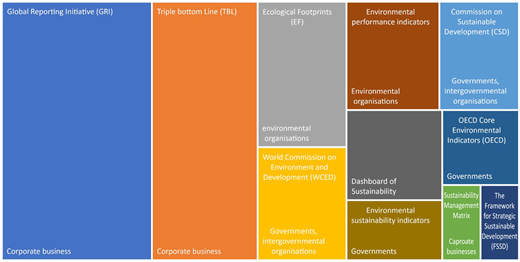

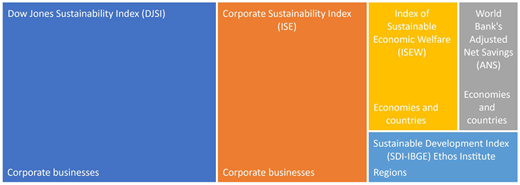

The SMFs exhibited various constructs, tools and indicators to assess sustainability performance across different enterprise settings, reflecting distinct levels of integration – from high-level strategic frameworks to operational project-level applications – and varied in their specificity, measurability and alignment with international standards. However, a critical evaluation reveals considerable inconsistencies in domain coverage, standardisation and contextual adaptability, as presented in Figures 5 and 6.

Most tools and frameworks in the reviewed literature emphasise economic and environmental dimensions. Tools such as the GRI, ISO 14001 and the Ecological Footprint dominate environmental performance measurement (Clarkson et al., 2019; Staniškis and Arbačiauskas, 2009) while, at the same time, economic constructs are embedded in indices including the Dow Jones Sustainability Index and Corporate Sustainability Index. Although present in frameworks, including the Ethos indicators and ISO 26000, social dimensions are often less operationalised, more descriptive and sometimes developed using CSR. Governance constructs are the most underrepresented, appearing occasionally in strategic management tools such as the Balanced Scorecard and isolated regulatory instruments (Dağıdır and Özkan, 2024; de Castro Sobrosa Neto et al., 2020; Mio et al., 2022) and indicates a significant imbalance in domain coverage, with limited capacity to capture inclusive governance practices, ethical accountability and stakeholder empowerment, which are particularly critical in non-profit and social enterprise contexts.

SMFs range from strategic frameworks, including the Framework for Strategic Sustainable Development and Balanced Scorecard, to more project-specific tools, such as the Environmental Impact Assessment and Eco-indicator 99 (Broman and Robèrt, 2017; Searcy, 2016; Trisyulianti et al., 2023). Strategic frameworks are typically used for long-term planning and internal alignment, often within corporate structures. Conversely, project-level tools are more focused, outcome-driven and frequently used in regulatory or sector-specific settings (e.g. construction and manufacturing) (Chang et al., 2018; Ferreira et al., 2023).

The analysis suggests that SMFs have primarily been applied to CEs. Consequently, the distinct measurement needs of SEs, non-profits and hybrid organisations are frequently overlooked. These entities prioritise social impact and environmental stewardship alongside or in place of financial goals – priorities not adequately addressed in most conventional frameworks. This narrow application reduces the relevance of mainstream SMFs for organisations operating with alternative value propositions.

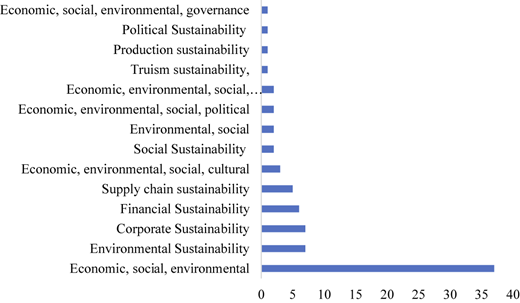

4.3.1 Sustainability dimensions

The literature has highlighted sustainability measurement across various dimensions utilising various SMFs, as illustrated in Figure 7. There are correlations between social and environmental practices in enterprises and economic sustainability, as well as social and economic practices in environmentally sustainable enterprises (Adams et al., 2014; Sardana et al., 2020). These SMFs address multiple dimensions of sustainability (i.e. economic, social and environmental) (Adams et al., 2014; Ameer and Othman, 2012; Junior et al., 2018) and aim to balance sustainability dimensions (Mundra and Mishra, 2021). Despite this progress, a significant portion of the literature continues to adopt a unidimensional focus, measuring sustainability within a single domain. There are studies (Ameer and Othman, 2012; Chow and Chen, 2012; Escrig-Olmedo et al., 2017; Qiu et al., 2020) providing detailed insights into isolated dimensions but fall short of capturing the complex interdependencies that characterise sustainable development, which underscores the need for future research to embrace multidimensional, context-aware and inclusive sustainability measurement frameworks adaptable to the unique characteristics of diverse organisational types and global contexts.

4.3.1.1 Economic dimension

Most SMFs still favour traditional economic value, profitability, cost efficiency and risk mitigation. TBL studies operationalise the “profit” pillar with familiar accounting ratios and cost–benefit metrics, devoting far less granularity to non-financial capitals (Ali et al., 2023; Pranugrahaning et al., 2021), likewise, GRI-based research focus on economic disclosures (GRI 201–203) because they are auditable and investor-driven (Gunawan et al., 2021). Manufacturing and extractive-sector data show that strong economic scores often coincide with robust environmental and social practices (Adams et al., 2014; Ameer and Othman, 2012; Junior et al., 2018), however, meta-analyses of Asian SMEs find no significant link between eco-efficiency and profitability, highlighting moderating factors such as regulatory pressure and market maturity (Pham and Kim, 2019). These contradictions point to the need for SMFs that blend conventional financial indicators with mission-centric metrics – e.g. community wealth creation – when applied to social enterprises and other hybrids.

4.3.1.2 Environmental dimension

The environmental pillar is the most developed, reflecting decades of ISO 14001 diffusion and the carbon-accounting mandates embedded in the EU CSRD. Typical indicators track resource intensity, emissions, waste and life-cycle impacts (Manfredi and Goralczyk, 2013), but many studies still treat these variables as “add-ons” rather than integrating them into core strategy (Ragas et al., 1995; Rennings and Wiggering, 1997). TBL has been criticised for reinforcing this bolt-on logic by placing ecology alongside two competing pillars (Kocmanova et al., 2017; Kudratova et al., 2020; Pranugrahaning et al., 2020) and, as a result, emerging approaches such as emergy analysis (Zhang et al., 2023; Zhao et al., 2024) and science-based target setting aim to correct the imbalance but remain confined to high-impact industrial contexts. Moreover, few frameworks translate environmental performance into outcomes that matter to mission-driven firms, limiting their utility for resource-constrained SEs.

4.3.1.3 Social dimension

Social constructs – equity, inclusion, labour well-being and community empowerment – are least consistently operationalised. Although GRI's Social Standards offer extensive guidance, empirical work often defaults to qualitative narrative or proxy measures (head-count diversity and philanthropy spend) that obscure substantive impact (Passetti and Tenucci, 2016). Interest in socio-economic indicators such as accessibility and participation is rising, particularly in post-2015 studies aligned with the SDGs (Mundra and Mishra, 2021). Nevertheless, social metrics remain thin and poorly standardised, hampering cross-study comparability.

4.3.1.4 Cross-dimensional integration and gaps

Only a minority of the 161 studies employ truly integrative SMFs: 37% analyse a single pillar, 44% two pillars and just 19% all three (Adams et al., 2014; Ameer and Othman, 2012), and this fragmentation confirms that “multidimensional” frameworks often default to economic and ecological biases, relegating social value to narrative disclosure. For SEs and other hybrids – whose theories of change require simultaneous optimisation across economic, environmental and social goals – such partial integration is particularly limiting. Future work must develop SMFs that capture interdependencies among the three dimensions and translate them into actionable metrics for mission-driven organisations.

A key insight from this review is the need for inclusive, multidimensional indicators that are measurable and responsive to the distinct value orientations of social and hybrid enterprises. This gap in construct integration presents a valuable direction for future research aiming to design sustainability frameworks that truly reflect the principles of inclusive, equitable and impact-driven enterprise models.

4.4 Methodology (M)

RQ4: What methodological approaches have been utilised in designing, validating and applying SMFs?

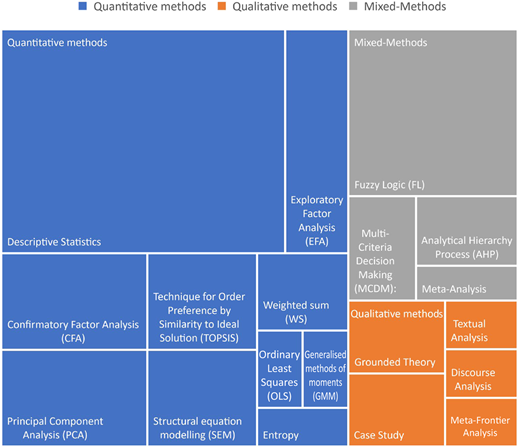

The methodologies employed across the reviewed studies are overwhelmingly quantitative, with a smaller yet growing presence of qualitative (Passetti et al., 2014; Searcy and Buslovich, 2014) and mixed-methods research (Lisi, 2015; Pondeville et al., 2013). The summary statistics are presented in Figure 8.

Literature has indicated that quantitative techniques and applied structural equation modelling (SEM) are used to measure sustainability (Bodhanwala and Bodhanwala, 2018; Hall and Wagner, 2012; Mundra and Mishra, 2021) and Singh et al. (2009) developed the Composite Sustainability Performance Index (CSPI), Composite Sustainable Development Index and CSPI. Moreover, Jiang et al. (2018) proposed a model of corporate sustainability using the Sustainability Performance Index, while Engida et al. (2018) similarly established the Composite Sustainability Index. In addition, the generalised method of moments was applied (Asongu and Odhiambo, 2021; Ibrahim and Vo, 2020), panel data regressions (Kleemann and Abdulai, 2013; Lin et al., 2021), ARDL bounds testing (Kalai and Zghidi, 2019) and vector error correction modelling (Liu, 2009) were utilised. Furthermore, Hierarchy Process, Multi-Criteria Decision-Making and fuzzy logic analysis were reported in the literature as guiding methods to measure sustainability (Nuong et al., 2011; Qu et al., 2020). Labuschagne et al. (2005) illustrated an integrated multidimensional SMF for businesses. In contrast, qualitative methods, including grounded theory, case studies and textual/discourse analysis, remain underrepresented. While these approaches offer valuable insights into sustainability, they often contain socially embedded aspects and their limited use restricts a deeper understanding of context-specific and institutional dynamics.

This section addresses RQ4, which examines the methodological approaches used in designing, validating and applying SMFs. The findings indicate a firm reliance on quantitative methodologies, notably SEM, composite index construction and econometric analysis. Although these methods contribute to empirical rigour and promote standardisation, the limited use of qualitative and participatory approaches constrains the field's capacity to reflect lived experiences, contextual nuances and institutional dynamics that influence sustainability practices. This imbalance reveals a critical gap as many of the frameworks overlook sustainability's value-driven and socially embedded aspects, especially within hybrid and mission-oriented enterprises. To bridge this gap and improve sustainability measurement, future research must embrace methodological pluralism by adopting mixed methods, grounded theory and stakeholder-led strategies that better represent sustainability's complexity and multidimensional nature across varied enterprise contexts.

5. Discussion and conclusion

This review offers an innovative and critical contribution to the evolving field of enterprise sustainability measurement by drawing on the integrative insights of the TCCM framework (Bhardwaj and Kalro, 2024; Klarin, 2024; Paul and Menzies, 2023; Paul et al., 2021b; Pomerlyan and Belitski, 2023). One of the key arguments advanced is the persistent dominance of corporate-centric theoretical paradigms – such as stakeholder theory, legitimacy theory and the TBL.

As illustrated in Figure 9, although these theories offer valuable insights, their focus on financial outcomes and commercial objectives marginalises alternative frameworks crucial to social enterprises, non-profits and hybrid organisations. These entities inherently prioritise social equity, community empowerment and environmental well-being (Crossley et al., 2021; Dato-on and Kalakay, 2016; Salavou and Manolopoulos, 2021), yet the narrow orientation of existing SMFs sustains an epistemological bias that restricts theoretical inclusivity within sustainability research. Another significant yet underexplored insight highlighted is the contextual rigour within current SMFs. Empirical research is disproportionately concentrated in high-income, Western contexts, resulting in frameworks that inadequately address the Global South's cultural, institutional and resource-specific conditions, which limit the transferability and relevance of existing frameworks and neglect grassroots and community-based innovations. Therefore, there is an urgent need for contextually adaptable and participatory frameworks that better reflect diverse socio-economic realities and incorporate local knowledge and practices.

At a conceptual level, this research identifies notable fragmentation within current SMFs, with many studies overly focusing on isolated sustainability dimensions. Such unidimensional approaches fail to capture the complex interplay among economic, social and environmental objectives, particularly within mission-driven organisations where balancing these dimensions is integral to achieving their goals, and future research should emphasise developing multidimensional, integrative frameworks capable of comprehensively capturing sustainability synergies and trade-offs. Moreover, the existing literature methodologically utilises the descriptive quantitative approaches; however, prioritising statistical validation over rigorous qualitative understanding is lacking, which limits studying non-commercial organisations, where sustainability performance is often deeply embedded in values, narratives and stakeholder relationships. An emphasis on interpretive, participatory and systems-based methodologies is necessary to capture these nuanced aspects adequately and methodological triangulation, combining quantitative rigour with qualitative depth, will substantially enhance the robustness and applicability of sustainability research.

This SQLR concludes that there is a substantial disconnect between existing SMFs and the practical realities of diverse organisational forms, particularly in hybrid enterprises. As a result, this gap requires contextual, theoretical grounding and re-embedding theoretical foundations that expand contextual applicability, enhance conceptual multidimensionality and adopt methodological pluralism. Future research must prioritise inclusivity, flexibility and interdisciplinary integration to ensure SMFs are methodologically rigorous, contextually relevant and practically effective in guiding sustainable transformations across commercial and mission-driven enterprises.

6. Practical implications

In response to the growing demand for accountability, transparency and long-term value creation (Abhayawansa et al., 2021), this study outlines several practical implications for businesses that seek to adopt SMFs. Firstly, the dominance of economically and environmentally focused frameworks reveals a gap that enterprises, mainly social, hybrid and non-profit organisations, must address by adapting SMFs to better reflect social impact and governance indicators. Such adaptations can improve legitimacy, attract stakeholder support and open pathways to ethical investment. Secondly, businesses in resource-constrained or low-income contexts (Hossain et al., 2023) can adopt context-specific, integrated frameworks that match sustainability goals with local conditions. Thirdly, the use of participatory and stakeholder-led assessment methods can support internal decision-making (González-Romero et al., 2024), promote employee ownership and foster community trust. Finally, adopting multidimensional, inclusive and adaptive measurement practices can improve sustainability outcomes, increase competitiveness and strengthen brand reputation in a global market that places greater value on ethics and impact.

7. Limitations and future research directions

While this SQLR offers valuable insights, it is not without its limitations. Primarily, the scope of the review was restricted to studies published in English, possibly excluding critical findings from literature in other languages. Furthermore, this SQLR is anchored in the TCCM framework, and, despite TCCM offering a transparent map of prior work, its four-cell structure can obscure the interdisciplinary, multi-scalar character of SMF research. Future reviews should experiment with hybrid mapping tools, bibliographic coupling, co-citation analysis and topic modelling to expose cross-domain linkages that TCCM alone may miss. A second, common constraint is the reliance on keyword-based search strings, as even carefully crafted queries can overlook studies that use different terminology. We mitigated this risk by iteratively expanding our keywords and snowballing reference lists, yet relevant non-English work may still have escaped detection. Combining free-text queries with controlled-vocabulary searches in the future could also further widen coverage in subsequent studies.

Note

KW3 did not expand the number of retrieved articles.