The purpose of this paper is to investigate into the conditions under which founders’ human capital (HC) benefits new venture growth (NVG). One such condition is investigated in this study – initial assets at founding. Specifically, founding assets are hypothesized to moderate the relationship between founders’ HC and NVG.

The longitudinal panel database from the Kauffman Firm Survey for the period 2004–2011 was used to test the hypotheses. The final sample consisted of 4,923 firms, with 34,461 observations made over seven years.

The regression analysis found the effect of founders’ HC on NVG and the moderating role of founding assets in the HC–NVG relationship.

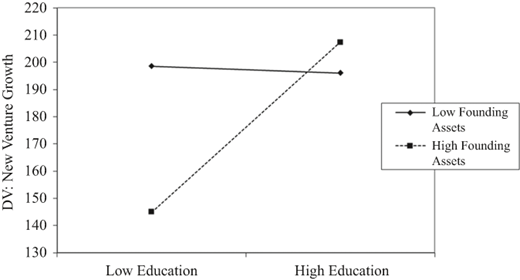

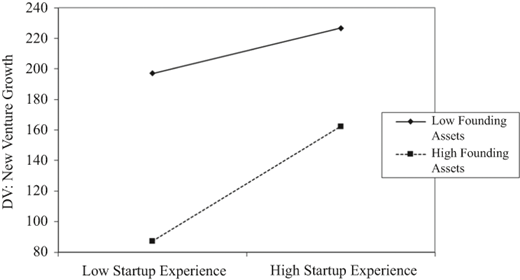

New ventures benefit even more from founders’ education level, industry and startup experiences when the startups have larger assets at founding. The effect of founders’ education and experiences on startup growth is contingent upon the initial assets at founding.

The results of this study can help practitioners and policy makers to understand the drivers of NVG and the interactions among these drivers. Growth-oriented startups may require a large investment in founding assets such as production facilities. Startups with fewer founding assets may find it particularly difficult to negotiate with external stakeholders and may face unusually intense competitive responses from competitors. Policy makers should tailor the support to the founding conditions of new firms.

The prior literature has shown mostly the independent positive effects of various resources on firm growth. This study argues and empirically shows that startups grow faster when founders with high HC have more assets to utilize. The resource-based view literature was expanded by adding important new causal mechanisms, enriching our understanding of how founders’ HC interact with founding assets, jointly affecting NVG. Like a big fish in a small pond, even highly educated and experienced entrepreneurs have limited opportunities to utilize their talents in a startup with a lower initial resource position.

Introduction

Growth is an indicator of new firm success (Feeser and Willard, 1990; Fischer and Reuber, 2003; Barringer et al., 2005), and founders’ human capital (HC) endowments, such as their knowledge and skills, are critical elements in new venture growth (NVG) (Colombo and Grilli, 2010). More experienced founders are particularly likely to lead their ventures to early success (Delmar and Shane, 2006). HC theory argues that HC, both generic and firm-specific, is the major driver of productivity (Dess and Shaw, 2001) and has a positive effect on organizational performance (Crook et al., 2011). HC is often valuable and rare for a firm, because individuals bring unique knowledge, skills and abilities, particularly in the area of highly specialized expertise (Barney, 1991; Hatch and Dyer, 2004; Coff and Kryscynski, 2011). A firm with superior HC can therefore achieve greater economic value by accessing and utilizing employees’ knowledge, skills and abilities (Coff and Kryscynski, 2011).

In the context of new firms, entrepreneurs with higher HC endowments are more capable of mobilizing and recombining various resources to exploit opportunities (Clough et al., 2019). However, the results of these empirical studies into the role of founders’ HC on NVG are inconclusive (Stuart and Abetti, 1990; Westhead and Cowling, 1995; Almus and Nerlinger, 1999; Colombo and Grilli, 2005; Cassar, 2014), possibly because of a lack of investigation into the conditions under which founders’ HC benefits NVG. One such condition is investigated in this study – initial assets at founding. As a critical component of the initial stock of resources of a new organization, founding assets are mobilized or recombined by entrepreneurs to grow their businesses (Clough et al., 2019). Specifically, founding assets are hypothesized to moderate the relationship between founders’ HC and NVG. This study contributes to a better understanding of the process through which entrepreneurs scale up their ventures. The interaction between founders’ HC and the initial assets at founding is examined to open up the black box of entrepreneurial resource mobilization process.

In the next section, the representative works in relevant research streams were reviewed. In the subsequent sections, the hypotheses were empirically tested with a sample of 4,923 firms in the longitudinal panel data set from the Kauffman Firm Survey (KFS) for the period from 2004 to 2011, followed by a discussion of the theoretical and practical implications of the findings.

Literature review

The resource-based view argues that valuable, rare, inimitable and non-substitutable resources play an important role in the creation of competitive advantage of a firm (Barney, 1991; Peteraf, 1993; Crook et al., 2008) and that firms’ sustainable competitive advantages originate from their unique and difficult-to-imitate resources and capabilities (Barney, 1991; Grant, 1996). Founders’ HC endowment, including elements such as their knowledge and skills, is a critical aspect of the capability of new firms (Cooper et al., 1994; Feeser and Willard, 1990; Colombo and Grilli, 2005). Specific types of HC, such as venturing and industry experience, expedite venture creation and development (Davidsson and Honig, 2003), whereas general types of HC, such as educational level, facilitate successful initial public offerings (Dimov and Shepherd, 2005).

The Penrosean theory of the growth of the firm also emphasizes the role of managerial capabilities in firm growth and has inspired much current research on resource complementarities and knowledge-based competencies (Nason and Wiklund, 2018; Penrose, 1959; Kor and Mahoney, 2004). In Penrose’s theory, some important endogenous factors in the rate of firm growth are imperfectly mobile tacit knowledge and managerial capabilities to utilize this knowledge. The focus of Penrose’s theory, the combination of versatile resources, was found to be associated with more rapid growth in a meta-analysis of 113 recent studies that included 612 bivariate effect sizes and represented data on 38,815 firms (Nason and Wiklund, 2018). Decision makers need to recombine resources in creative ways to create growth; in the context of new ventures, founders’ skills, education and experiences all influence their views of opportunities and ways of utilizing various resources to grow new ventures.

However, the results of empirical studies on the role of founders’ HC on NVG are inconclusive. For example, mixed results have been reported on the role of the founder’s education in firm growth (Stuart and Abetti, 1990; Westhead and Cowling, 1995; Almus and Nerlinger, 1999; Colombo and Grilli, 2005). Results of studies on the impact of experience on firm performance are also inconclusive. Experience is of two main kinds: industry experience and startup experience. Some have argued that industry experience helps entrepreneurs comprehend current trends in production processes or service delivery (Delmar and Shane, 2006), enhances their understanding of the impact of economic environment on industry growth (Mikhail et al., 1997), enables them to evaluate business opportunities within the industry (Delmar and Shane, 2006; Ronstadt, 1988) and improves their ability to forecast business performance (Cassar, 2014). Likewise, entrepreneurs can gain valuable skills from previous or serial venturing experiences (Baron and Ensley, 2006; Corbett, 2005; MacMillan and McGrath, 2006; Parker, 2006; Ronstadt, 1988; Shane, 2000; Wiklund and Shepherd, 2003). However, researchers have also presented some counterarguments; for example, entrepreneurs may gain incomplete benefits from experience, because the knowledge it generates cannot necessarily be applied to other businesses (Reuber and Fischer, 1994). Only a portion of the knowledge gained from experience can be applied to a novel and non-recurring task (Clement et al., 2007). Because each business opportunity is unique, entrepreneurs can transfer only part of the knowledge gained from experience (Bonner and Lewis, 1990; Jacob et al., 1999). In addition, entrepreneurs’ emotional responses and cognitive biases may inhibit learning from experience. Individuals must evaluate prior events and alter their opinions accordingly if they are to learn from experience (Haleblian et al., 2006; Madsen and Desai, 2010), but entrepreneurs may be unable to evaluate their startup experience accurately because of emotional responses and cognitive biases (Shepherd, 2003). For example, performance feedback, as recalled by entrepreneurs, may be systemically biased (Cassar and Craig, 2009).

In addition to such counterarguments, a possible explanation of the aforementioned inconclusive results is the lack of investigation of the conditions under which founders’ HC is beneficial to NVG. One such condition is initial assets at founding of a new firm, a critical component of the initial resource endowments of a new firm (Clough et al., 2019). At the scale-up stage, entrepreneurs endowed with higher levels of skills, knowledge and experiences are more capable of mobilizing and recombining these assets to expand their businesses. A higher initial resource position helps entrepreneurs with higher levels of education or venturing experiences to establish better social networks, raise financial capital and exploit market opportunities. A series of hypotheses were therefore developed to explore the interrelationships among founders’ educational level, industry and startup experiences, founding assets and NVG.

Hypotheses development

Founders’ HC is first hypothesized to have a positive impact on NVG because firms that possess valuable resources should perform better in the market selection process (Wernerfelt, 1984; Barney, 1991). For example, the initial stocks of financial and HC exert an enduring effect on firm performance (Cooper et al., 1994; Eisenhardt and Schoonhoven, 1990). HC, in particular, influences firm performance more than physical capital does, because knowledge assets are more difficult to trade or imitate (Youndt et al., 1996; Barney, 1991; Teece, 1998). High-quality HC possesses more complex and tacit knowledge, which is particularly difficult to transfer (Simonin, 2004; McEvily and Chakravarthy, 2002). HC has been found to be a good predictor of firm survival (Mata and Portugal, 2002; Cooper et al., 1994; Gimeno et al., 1997). In the context of new firms, the ability to develop and exploit firm-specific assets is critical to performance (Burgelman, 1994; Bogner et al., 1996; Chang, 1996). Founders with high-quality HC are likely to have better entrepreneurial judgment and consequently be better at identifying new business opportunities and integrating others’ knowledge to expand their business. They are also highly likely to recruit and retain exceptionally skilled employees.

A generic form of founders’ HC, educational level, may have a positive impact on startup growth in that the formal educational experience helps entrepreneurs develop their cognitive ability, an ability that can help new firms recognize and exploit opportunities (Alvarez and Busenitz, 2001). However, mixed results have been reported on the relationship of education to firm growth (Stuart and Abetti, 1990; Westhead and Cowling, 1995; Almus and Nerlinger, 1999; Colombo and Grilli, 2005). Some studies have identified the entrepreneur’s education as being positively associated with firm growth (McPherson, 1996; Mead and Liedholm, 1998), whereas others have reported that formal education does not directly relate to venture tasks, although other types of HC, such as industry and start-up experiences, do directly relate to the current tasks of the venture (Cooper et al., 1994; Marvel et al., 2014). Despite these mixed findings, education is generally assumed to equip entrepreneurs with greater knowledge and skills and consequently to help them improve their judgment in opportunity identification and business expansion, which ultimately benefit startup growth. Therefore, founders’ educational level is hypothesized to be positively related to NVG:

The founders’ level of education is positively related to NVG.

Next, founders’ industry experience is predicted to drive startup growth. Individuals’ judgment can improve when tasks are clearly defined and repetitive and when feedback is provided regularly (Hayward et al., 2006; Wright, 2001). Founders can gain knowledge and skills by learning about the industry, and thus can become better at identifying business opportunities and integrating specialists’ domain-specific knowledge. They can also gain relevant knowledge and skills by learning by doing (Cassar, 2014). Because entrepreneurship involves discovering facts in which entrepreneurs create and operate new businesses (Kirzner, 1997), those individuals with industry-specific experience tend to possess relevant information about such matters as cost structure, pricing and the value chain of differentiated markets in the same industry (Bruderl et al., 1992; Landier and Thesmar, 2009; Dimov, 2010). Founders with extensive industry-specific work experience therefore tends to have superior entrepreneurial judgment, and idiosyncratic entrepreneurial judgment helps to determine how an individual identifies new business opportunities (Foss, 1993; Hodgson, 1998; Alvarez and Barney, 2002). Because experience helps individuals improve in areas such as forecasting ability (Clement, 1999; Mikhail et al., 1997), entrepreneurs gain entrepreneurial judgment by learning from work and startup experiences (Baron and Ensley, 2006; Corbett, 2005; MacMillan and McGrath, 2006; Parker, 2006; Ronstadt, 1988; Shane, 2000; Wiklund and Shepherd, 2003). Furthermore, founders need to integrate and coordinate the complementary domain-specific knowledge possessed by specialists if they are to create and expand their businesses (Colombo and Grilli, 2010), and the insight gained from work experience can improve their ability to integrate the specialists’ domain-specific knowledge. Therefore, founders’ industry experience is hypothesized to exert a positive effect on startup growth:

The founders’ industry experience at founding is positively related to NVG.

In addition, entrepreneurs’ previous venturing experience is beneficial in multiple ways to NVG. First, entrepreneurs gain knowledge about business creation and development by learning through experimentation (Ardichvili et al., 2003; Baron and Ensley, 2006; Delmar and Shane, 2006; Shane and Khurana, 2003; Jovanovic, 1982). In the process of learning by doing, individuals repeatedly perform the task at hand, thus increasing their expertise specific to this task (Choo and Trotman, 1991; Dew et al., 2009). Second, startup experience improves entrepreneurs’ evaluation and judgment of business opportunities (Colombo and Grilli, 2005; Corbett, 2005), because they develop strong cognitive structures by reflecting on previous entrepreneurial activities (Baron and Ensley, 2006; Gruber et al., 2008). They learn from their own misperceptions of market places and improve their beliefs with regard to their ability to precisely assess business opportunities (Parker, 2006; Shane, 2000). Studies have found that cognitive capability was positively associated with sales growth and profit growth (Simons et al., 1999) as well as with task performance (Hunter and Hunter, 1984). Third, startup experience helps entrepreneurs become aware of the cognitive biases in their judgment, so that past misperceptions and errors in judgment do not produce biases in their beliefs (Forbes, 2005), allowing them to better understand the entrepreneurial risks and the base rates of new business success and failure (Hayward et al., 2006). Entrepreneurial experiences also reduce the tendency to excess optimism with regard to business forecasting (Hmieleski and Baron, 2009). For all these reasons, founders’ startup experience is hypothesized to have a positive effect on startup growth:

The founders’ startup experience at founding is positively related to NVG.

In addition, the interplay of founders’ capabilities and organizational resources affects the speed at which new ventures expand their businesses. Firm assets are critical resources for the growth of a firm; firms with larger assets may operate more efficiently than those with smaller assets because their operation is closer to the minimum efficient scale (Audretsch and Mahmood, 1994), and smaller firms operate at a smaller scale because of greater cash constraints (Zingales, 1998). Even if a firm adjusts to its desirable size later, it must do so gradually because of insufficient resources (Penrose, 1959) or the uncertainty involved (Cabral, 1995). A startup with larger founding assets can endure periods of poor performance and suffer losses for a longer time because of its larger assets as well as better access to funds.

Capable founders can configure resource endowments in unique combinations that create economic value, because many resources included in a startup’s founding assets can offer a variety of potential services. The availability of larger assets provides founders with the opportunity to capitalize fully on their skills and abilities. In addition, the existence of underutilized and excess resources motivate founders to look for ways to use them, and entrepreneurs with better cognitive capability and more experience are able to generate more creative and productive applications from these resources. Furthermore, founders with higher HC can discover more ways of redeploying existing resources into novel and more valuable resource combinations so as to generate the specialized services of those resources as fully as possible. In contrast, resource constraints have a particularly strong negative impact on founders with higher HC during the development of their startups. In the early years, firms endure the strongest impact of cash constraints because of lack of reputation and information asymmetries (Diamond, 1989). Even founders with better education and experiences can have great difficulty expanding their business when their startups have fewer assets.

However, the counterargument might also be true. Managers with access to abundant resources may have little incentive to experiment (Sinclair et al., 2000) and may thus become less entrepreneurial (Bradley et al., 2011; Stevenson and Jarillo, 1990). Resource scarcity triggers entrepreneurial management practices that make the most efficient use of the current resources (Stevenson and Jarillo, 1990). Despite these counterarguments, in the context of new ventures, limited resources and smaller founding assets constrain the ability of even experienced entrepreneurs to recombine existing resources in novel ways so as to expand their businesses. Hence, larger founding assets are hypothesized to reinforce the effect of founders’ HC endowment on NVG:

The founders’ level of education is more highly and positively associated with NVG when the new venture has larger assets at founding.

The founders’ industry experience is more highly and positively associated with NVG when the new venture has larger assets at founding.

The founders’ startup experience is more highly and positively associated with NVG when the new venture has larger assets at founding.

Methods

Data and sample

Because a cross-sectional time series (panel) data design with fixed-effect controls can eliminate many alternative explanations for observed changes in NVG and minimize the risk of omitted-variable bias (Hsiao, 1986), the longitudinal panel database from the KFS for the period 2004–2011 was used to test the hypotheses. The KFS is a panel study of 4,928 new firms in the USA that began operations in 2004. The same firms were followed every year until 2011. This data set includes detailed information on the firm and up to ten owners. The respondents’ answers to the survey questions were cross-checked every year to confirm their validity; therefore, the biases associated with using single-source data were significantly reduced. Five firms were excluded due to duplications or being founded prior to 2004. The final sample consisted of 4,923 firms, with 34,461 observations made over seven years.

Measures

All the variables were from the restricted-access KFS data set provided by the National Opinion Research Center through a secure, remote access data enclave. This confidential data set includes the details on founders’ characteristics, new venture performance and the external business environment. To capture causal relationships between the independent and dependent variables, all left-hand-side variables were lagged by one year.

Dependent variables

New venture growth

NVG is measured by the Birch index (Birch, 1987) to reduce the bias caused by firm size:

where Eit is the employment of firm i at time t.

Employment is used as a growth indicator because measuring firm size in terms of employment neither reflects input prices of a company nor requires deflation, as use of sales data does (Coad, 2009). Using employment as the measure also avoids the bias caused by the manipulation of reported sales and profits common in many small businesses (Cressy, 2006).

Independent variables

Three indicators of founders’ HC were used in the regression analyses: education, industry experience and startup experience. In the management literature, these indicators are typically used to measure HC (Unger et al., 2011). Education is the proxy measure of generic HC, whereas industry experience and startup experience are proxy measures of specific HC.

Education

The founder(s)’ education level was measured as their average level of education on the following five-point scale: 0 – less than high school (93 responses); 1 – high school (439 responses); 2 – some college, technical or associate’s degree (1,918 responses); 3 – bachelor’s degree (1,131 responses); and 4 – post-bachelor’s degree (1,332 responses). The use of a continuous variable is consistent with previous studies (Cassar, 2014).

Industry experience

The founder(s)’ industry experience was measured as the natural log transformation of the average number of years they had worked in the industry in which the startup operates plus one.

Startup experience

The founder(s)’ startup experience was measured as the natural log transformed average number of businesses they had previously started plus one.

Moderator

Founding assets

The founding assets were measured as the total assets owned by the firm in the founding year, consisting of inventories, equipment, land, buildings, cash and any other assets. The total value of all the assets was represented on the following nine-point scale: (1) $500 or less; (2) $501–$1,000; (3) $1,001–$3,000; (4) $3,001–$5,000; (5) $5,001–$10,000; (6) $10,001–$25,000; (7) $25,001–$100,000; (8) $100,001–$1,000,000; and (9) $1,000,001 or more.

Control variables

State fixed effects

To control for systematic differences across 50 states, a dummy variable was created for each state.

Industry fixed effects

To control for systematic differences across industries, one dummy variable was created for each industry. There are 84 industries in the sample with all the firms being classified using the three-digit North American Industry Classification System (NAICS) code.

Year fixed effects

To control for systematic differences across years, one dummy variable was created for each year.

Gender

This dummy variable equals 1 if any founder of the startup is female and 0 otherwise.

Age

The average age of the founder(s) was measured as the natural log transformation of the average age plus one.

Intellectual properties

The intellectual properties of the new firm possessed in the founding year were measured as the natural log transformation of the total number of patents, copyrights and trademarks plus one. Firms that own intangible resources tend to exhibit proactive and risk-taking behaviors in the pursuit of growth opportunities (Wiklund et al., 2010; Anderson and Eshima, 2013). One source of firm growth is the accumulated stock of intellectual properties in the form of patents, copyrights and trademarks. Startups with IP rights have certain early-mover advantages (Pereira et al., 2015). For example, patents play an important role in high-growth firms (Parker et al., 2010), and in those software startups backed by venture capitals in the USA, patents positively influenced firm performance (Mann and Sager, 2007).

Market competition

Without controlling for market competition, misleading conclusions can be drawn about the role of founders’ HC in NVG. Industry concentration was used as a proxy for market competition, because the sample includes multiple industries with a wide variety of structures (Geroski et al., 2010). Current firm concentration in a certain area matters; competition from other firms may limit the business expansion of new firms, because ,first, new firms cannot secure the funds required, as they lack legitimacy in financial markets (Diamond, 1989) and consequently are more likely to suffer from cash constraints (Cabral and Mata, 2003) and ,second, strong local competition can lead founders to change their growth expectations for their new businesses, although the impact of local competition may be low because firm heterogeneity limits the threat posed by industry competitors (Bertin et al., 1996). To compile data on the industry-level characteristics of the local area, the KFS data were merged with the County Business Patterns data on the basis of the county in which each firm is located and the three-digit NAICS code. Industry concentration was measured by two indicators: total mid-March employees of all the local firms in the same industry; and total number of local firms in the same industry. Both indicators were included and mean centered in the regression analyses.

Initial external equity

This dummy variable was created to indicate whether external capital was received by the startup before founding.

In addition to the above-mentioned control variables, sampling weights were also included in the analyses (Farhat and Robb, 2014).

Results

Table I presents the descriptive statistics and correlation matrix of all variables. The data show that NVG was positively and significantly correlated with founders’ education level, industry experience, startup experience, founding assets, intellectual properties, initial external equity and interaction terms. It also shows that NVG was negatively and significantly correlated with founders’ gender, age and the total number of local firms in the same industry.

Descriptive statistics and correlation matrix

| Variable | n | Mean | SD | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Firm growth | 19,537 | 330.79 | 653.69 | |||||||||||||

| 2. Education | 34,391 | 2.65 | 1.03 | 0.026*** | ||||||||||||

| 3. Industry experience | 34,461 | 2.21 | 0.99 | 0.015* | 0.031*** | |||||||||||

| 4. Startup experience | 34,461 | 0.44 | 0.57 | 0.049*** | 0.102*** | 0.055*** | ||||||||||

| 5. Founding assets | 34,370 | 5.24 | 2.69 | 0.034*** | 0.025*** | 0.055*** | 0.082*** | |||||||||

| 6. Gender | 34,461 | 0.20 | 0.40 | −0.020** | 0.007 | −0.143*** | −0.114*** | −0.142*** | ||||||||

| 7. Age | 34,461 | 3.78 | 0.34 | −0.020** | 0.091*** | 0.193*** | 0.144*** | 0.074*** | −0.017** | |||||||

| 8. Intellectual properties | 34,461 | 0.27 | 0.68 | 0.028*** | 0.145*** | 0.013* | 0.100*** | 0.043*** | −0.043*** | −0.018** | ||||||

| 9. Market competition1 | 24,647 | 0.00 | 256363.72 | −0.008 | 0.117*** | 0.064*** | 0.002 | −0.041*** | −0.015* | −0.023*** | 0.028*** | |||||

| 10. Market competition2 | 24,647 | 0.00 | 22220.76 | −0.015* | 0.130*** | 0.088*** | −0.005 | −0.039*** | −0.017** | −0.029*** | 0.018** | 0.901*** | ||||

| 11. Initial external equity | 22,904 | 0.08 | 0.27 | 0.039*** | 0.053*** | 0.005 | 0.099*** | 0.104*** | −0.052*** | 0.011 | 0.123*** | −0.004 | −0.028*** | |||

| 12. Founding assets × Industry experience | 34,412 | 11.71 | 8.45 | 0.037*** | 0.032*** | 0.636*** | 0.084*** | 0.733*** | −0.178*** | 0.158*** | 0.036*** | 0.009 | 0.024*** | 0.087*** | ||

| 13. Founding assets × Startup experience | 34,440 | 2.45 | 3.83 | 0.064*** | 0.090*** | 0.050*** | 0.841*** | 0.404*** | −0.133*** | 0.132*** | 0.105*** | −0.014* | −0.022*** | 0.137*** | 0.319*** | |

| 14. Founding assets × Education | 34,335 | 13.93 | 9.47 | 0.047*** | 0.589*** | 0.055*** | 0.122*** | 0.766*** | −0.100*** | 0.108*** | 0.124*** | 0.040*** | 0.047*** | 0.116*** | 0.569*** | 0.373*** |

Notes: *p<0.05; **p< 0.01; ***p<0.001 (two-tailed)

Table II presents the determinants of NVG. The independent variables and moderator were introduced in the subsequent models, following a hierarchical approach. The sample size was reduced to 12,180 observations in the regression analyses due to missing data. Model 1 includes the fixed effects and other control variables. A positive association was found between NVG and initial external equity and a marginally significant positive association between NVG and the first indicator of market competition (total current employees of the local firms in the same industry). It is noteworthy that the association between NVG and the second indicator of market competition (total number of local firms in the same industry) is significantly negative. The main effects of the independent variables were estimated in Model 2. A significant positive association was found between NVG and founders’ education as well as between NVG and founders’ startup experience, whereas the positive association between NVG and founders’ industry experience was marginally significant. Among the control variables, founders’ age and the second indicator of market competition have significantly negative associations with NVG. The first indicator of market competition and initial external equity are marginally significantly positive. Echoing the results of previous research, these results support H1a, H1b (marginally significant) and H1c. Model 3 reports the significant positive main effect of founding assets on NVG. Among the control variables, the first indicator of market competition and initial external equity has significant positive associations with NVG. The second indicator of market competition is significantly negative. Model 4 also reports positive and significant effects of all three independent variables and moderator.

Regression analysis: determinants of new venture growth

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Coeff. | SE | Coeff. | SE | Coeff. | SE | Coeff. | SE | Coeff. | SE | |

| Control variables | ||||||||||

| Constant | 127.289**** | 75.587 | 123.570 | 76.758 | 106.777 | 75.848 | 103.922 | 77.022 | 249.949** | 88.291 |

| State fixed effects | Yes | Yes | Yes | Yes | Yes | |||||

| Industry fixed effects | Yes | Yes | Yes | Yes | Yes | |||||

| Year fixed effects | Yes | Yes | Yes | Yes | Yes | |||||

| Gender | −20.048 | 15.242 | −10.521 | 15.347 | −16.402 | 15.281 | −7.207 | 15.383 | −7.901 | 15.385 |

| Age | −10.327 | 18.362 | −38.757* | 18.965 | −14.236 | 18.399 | −42.108* | 18.992 | −43.679* | 19.008 |

| Intellectual properties | −0.084 | 7.282 | −6.232 | 7.348 | −0.525 | 7.281 | −6.601 | 7.346 | −7.966 | 7.350 |

| Market competition | ||||||||||

| 1. Total current employees in the local industry | 0.000**** | 0.000 | 0.000**** | 0.000 | 0.000* | 0.000 | 0.000**** | 0.000 | 0.000**** | 0.000 |

| 2. Total current establishments in the local industry | −0.002** | 0.001 | −0.002** | 0.001 | −0.002** | 0.001 | −0.002** | 0.001 | −0.002** | 0.001 |

| Initial external equity | 46.315* | 19.953 | 38.414**** | 19.956 | 40.134* | 20.045 | 32.635 | 20.046 | 29.669 | 20.052 |

| Independent variables | ||||||||||

| Education | 16.839** | 5.645 | 16.770** | 5.643 | −16.068 | 12.826 | ||||

| Industry experience | 10.756**** | 5.740 | 10.502**** | 5.739 | −0.171 | 12.687 | ||||

| Startup experience | 50.264*** | 9.224 | 49.698*** | 9.223 | 7.132 | 21.240 | ||||

| Founding assets | 6.331** | 2.040 | 6.009** | 2.038 | −19.422* | 7.527 | ||||

| Interactions | ||||||||||

| Founding assets × Education | 5.842** | 2.023 | ||||||||

| Founding assets × Industry experience | 2.070 | 2.014 | ||||||||

| Founding assets × Startup experience | 7.383* | 3.284 | ||||||||

| R2 | 0.042 | 0.045 | 0.043 | 0.046 | 0.047 | |||||

| F | 3.782*** | 4.022*** | 3.826*** | 4.057*** | 4.092*** | |||||

Notes: n=12,180 The analysis takes into account sampling weights. *p<0.05; **p<0.01; ***p<0.001; ****p<0.1

To examine H2a–2c, Model 5 adds the interactions of independent variables and moderator. The results, together with the graphic analyses plotted in Figures 1 and 2, provide support for these three hypotheses. As predicted, the positive effect of the founders’ education or startup experience on NVG is stronger when the startup has larger founding assets. To test robustness, the panel data set was split into two subsamples, and the regression analysis was performed on each subsample. The unreported results are robust, and coefficients quantitatively similar.

Discussion

Analysis of the results suggests a complex relationship among founders’ HC, founding assets and NVG. Founders’ education level, industry and startup experiences benefit NVG, and founding assets moderates this relationship. New ventures benefit even more from founders’ education level, industry and startup experiences when the startups have a higher initial resource position. Previous studies have investigated the effect of founders’ HC on firm performance, but few known studies have examined the conditions under which founders’ HC is particularly important to NVG. Previous studies generally focused on the direct effects of various resources and capabilities on firm performance, often ignoring the interactions among those resources in the process of new firm growth. The results inform previous inconclusive findings on the role of HC in firm growth. The effect of founders’ education and experiences on startup growth is contingent upon the initial assets at founding. A startup’s initial resource position amplifies the positive effect of founders’ HC on NVG.

Conceptually, this study advances theoretical development on firm growth. HC theory argues that people’s varying knowledge and skills have economic value (Becker, 1964; Schultz, 1961). HC has been found to be vital to entrepreneurial success (Unger et al., 2011) because it helps new firms accumulate new knowledge and create advantages (Bradley et al., 2012; Corbett, 2007). However, this study has revealed the different effects of various types of HC on NVG. The positive impact of founders’ industry experience is not as strong as that of their educational level and startup experience on startup growth. One possible explanation is that only limited knowledge gained from industry experience can be applied to novel business opportunities, whereas capabilities and skills gained from education and venturing experiences enable founders to better mobilize initial resources to exploit growth opportunities. The empirical findings also extend the theory on NVG by showing that one type of resource amplifies the role of another resource in NVG. The prior literature has shown mostly the independent positive effects of various resources on firm growth. This study argues and empirically shows that startups grow faster when founders with high HC have more assets to utilize. The resource-based view literature was expanded by adding important new causal mechanisms, enriching our understanding of how founders’ HC interact with founding assets, jointly affecting NVG. Like a big fish in a small pond, even highly educated and experienced entrepreneurs have limited opportunities to utilize their talents in a startup with a lower initial resource position. Even though much former research examined correlations between attributes of entrepreneurs and the firm performance, the entrepreneurial resource mobilization process remains a black box (Clough et al., 2019). By examining the amplifying role of the initial resource position of a new venture, this study helps us open up this black box.

The results of this study can help practitioners and policy makers to understand the drivers of NVG and the interactions among these drivers. Consistent with the hypotheses, the empirical examination revealed that founders’ educational level and startup experience drive startup growth and that larger founding assets intensify these positive effects. Capable entrepreneurs creatively utilize and combine existing resources to expand their new businesses. Their HC endowment, together with the initial resource position of their startup, jointly affects NVG. Entrepreneurs need to prepare carefully for the founding of a firm, because the strategic choices made at inception can have long-lasting effects. Growth-oriented startups may require a large investment in founding assets such as production facilities. Startups with fewer founding assets may find it particularly difficult to negotiate with external stakeholders and may face unusually intense competitive responses from competitors. Policy makers should tailor the support to the founding conditions of new firms.

This study has several limitations. First, many new businesses in the KFS had closed by the time each follow-up survey was conducted, resulting in self-selection of businesses in the follow-up surveys. This self-selection bias might influence the statistical effects of various variables on NVG. Second, finer-grained approaches to the operationalization of aspects of HC could be possible. For example, the education measures could consider the discipline, such as business, engineering, liberal arts or other degrees, and the work experience construct could consider various types, such as experience in R&D, operations, marketing, etc. Future research could integrate theories of motivation with HC theory, because motivation provides the entrepreneur with the impetus and energy to acquire the necessary HC and to implement actions. Founders’ expectations affect their behaviors with regard to expanding their businesses. Aggregate measures could be designed to represent firm-level HC. Other elements of HC could also be examined, including judgment, decision making and insight. Future studies could also explore how access to venture capital drives NVG; venture capital investors may provide resources and capabilities as coaches in addition to providing capital (Colombo and Grilli, 2010).

Conclusion

This study proposed and empirically tested the moderating role of founding assets in the relationship between founders’ HC and NVG. The research findings enrich our understanding of how founders’ HC interact with founding assets, jointly affecting NVG. Like a good horse with a good saddle, highly educated and experienced entrepreneurs are better able to utilize their talents in a startup with a higher initial resource position in the process of NVG.