This paper aims to systematically reviews and synthesises post-COVID-19 research on consumer payment behaviour, examining how the accelerated diffusion of digital and contactless payment solutions intersects with sustainable marketing concerns, including responsible consumption, trust, transparency and digital choice architectures. The review does not treat digital payment adoption as inherently sustainable; rather, it shows that sustainability-related implications depend on how payment systems are embedded within consumption journeys, governed through transparent practices and interpreted by consumers across contexts.

A systematic literature review was conducted on peer-reviewed journal articles published between 2022 and 2025. Studies were retrieved from Scopus and Google Scholar using a predefined search strategy and eligibility criteria, and analysed through descriptive mapping and thematic synthesis across marketing, information systems and sustainability-related streams.

Based on 57 journal articles, the review highlights a rapidly expanding multidisciplinary body of research on post-COVID-19 consumer payment behaviour. Adoption, continuance and switching are shaped by mechanisms such as perceived convenience and value, trust and security/privacy, perceived risk, habit formation and contextual factors including channel setting and platform integration. Importantly, payment practices are not value-neutral: their sustainability implications depend on how systems are embedded in consumption processes, communicated through marketing and aligned with consumer responsibility. The paper proposes an integrative framework linking payment infrastructures, consumer psychology, marketing and corporate social responsibility (CSR) processes and sustainability-related behavioural outcomes.

This study provides one of the first systematic syntheses focused on post-COVID-19 consumer payment behaviour from a sustainable marketing perspective, offering a framework that contributes to theory and informs practitioners and policymakers designing responsible digital payment ecosystems.

1. Introduction

Over the past decade, smartphones and digital infrastructures have reshaped how consumers search, purchase and pay (Verhoef et al., 2017). Beyond convenience, these technologies are increasingly discussed as having the potential to support more transparent, responsible and resource-efficient consumption (Świecka et al., 2021; Prabhu and Kumar, 2024). The COVID-19 pandemic further accelerated these dynamics, reinforcing e-commerce, omnichannel journeys and contactless payment solutions (Graziano et al., 2025;Petroccione et al., 2025; Baidoun and Salem, 2024). Many of these changes have persisted post-pandemic, with consumers maintaining familiarity with and reliance on digital and contactless options (Graziano et al., 2023). Post-pandemic payment behaviour therefore reflects a broader reconfiguration of routines and transaction architectures, rather than temporary crisis-driven adaptations.

From a sustainable marketing perspective, the rise of digital payments raises critical questions. Although frequently associated with sustainability goals, their actual effects depend on adoption patterns, their embedding within consumption journeys and consumers’ perceptions of usefulness, trust, risk and control (Doan et al., 2025; Ansari et al., 2025; Albastaki et al., 2024). These factors ultimately determine whether digital payment pathways support responsible decision-making or reinforce convenience-driven and potentially unsustainable routines (Golchha and Nagariya, 2025).

Technology adoption research provides a well-established foundation for analysing these dynamics, highlighting drivers such as perceived usefulness, ease of use, satisfaction and expectation confirmation (Venkatesh et al., 2003). Recent post-COVID-19 studies further emphasise the role of trust, privacy and perceived control, which are increasingly central to stabilising consumption practices and underpinning credible sustainability and responsibility claims (Trianto et al., 2025; Vrontis et al., 2020; Zaidan et al., 2025; Alam and Al Mubarak, 2025).

Against this background, two questions are particularly salient. First, which behavioural changes reflect temporary crisis responses, and which indicate persistent habit formation capable of shaping sustainable – or unsustainable – consumption routines? Second, how do payment determinants vary across instruments and contexts, and how does this variation affect consumers’ capacity for responsible choice? Post-pandemic trajectories are heterogeneous, influenced by digital literacy, age, income, prior experience and institutional environments, with important implications for inclusion and sustainability-oriented marketing strategies (Wauk et al., 2025).

Motivated by these considerations, this paper presents a systematic review of research published between 2022 and 2025 on post-COVID-19 consumer behaviour and digital payments, interpreted through a sustainable marketing lens. Specifically, the review aims to (a) map recent research on post-pandemic payment behaviour, (b) develop an integrative framework linking digital payment infrastructures, consumer psychology, marketing and communication processes and sustainability-related outcomes and (c) identify theoretical gaps and future research avenues related to sustainable marketing, authenticity, transparency and generational differences. This review does not assume that digital payment adoption is inherently sustainable or that post-COVID-19 shifts were primarily driven by environmental concerns. Rather, it examines the conditions under which evolving payment practices may align with, complicate or undermine sustainable and responsible consumption.

2. Methodology and research question

This study adopts a systematic literature review to map and synthesise post-COVID-19 research on consumer payment behaviour through a sustainable marketing lens. Beyond documenting changes in payment adoption, the review examines how post-pandemic payment practices intersect with sustainability concerns such as responsible consumption, trust, transparency, inclusion and digital choice architectures. The review follows a transparent four-stage process:

formulation of research questions;

development of a review protocol defining databases, search strategy and eligibility criteria;

descriptive mapping of selected studies; and

thematic synthesis focused on sustainability-relevant mechanisms and outcomes.

The review is guided by one overarching question:

How has consumer payment behaviour evolved post-COVID-19, and what are the implications for sustainable and responsible consumption?

Two subordinate questions structure the synthesis:

Which technological, psychological and contextual mechanisms shape adoption, continuance and switching of payment instruments, and how do they enable or constrain responsible consumer choice?

How do marketing, communication and institutional factors, such as trust, transparency and perceived control, mediate the link between digital payment ecosystems and sustainability outcomes?

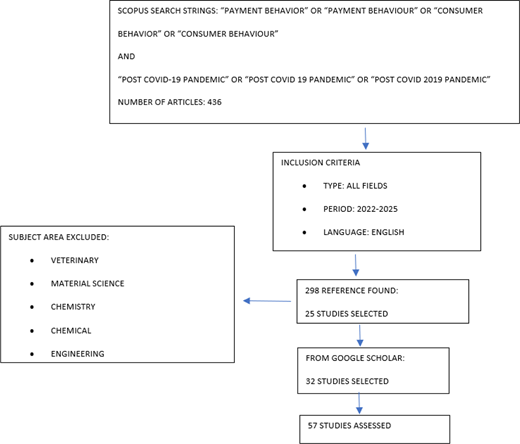

Following established SLR guidelines (Christofi et al., 2017; Vrontis and Christofi, 2019), Scopus was the primary database, complemented by Google Scholar. Searches were conducted in titles, abstracts and keywords using Boolean operators. Scopus was selected as the primary database because of its broad multidisciplinary coverage, strong indexing of peer-reviewed journals and frequent use in systematic review studies within business and management research. Google Scholar was used as a complementary search source to widen retrieval and reduce the risk of omitting relevant articles that may not have been captured through a single indexed database. This combination was intended to balance comprehensiveness, transparency and feasibility within a focused review design. While other databases, such as Web of Science or discipline-specific sources, may also have yielded additional records, the present review prioritised a manageable and replicable search strategy aligned with its conceptual objectives.

A representative search string was:

(“payment behavior” OR “payment behaviour” OR “consumer behavior” OR “consumer behaviour”)AND(“post COVID-19 pandemic” OR “post COVID 19 pandemic” OR “post COVID 2019 pandemic”).

The scope was limited to peer-reviewed articles in English published between 2022 and 2025. The initial search yielded 436 records. After removing duplicates, non-English publications, non-eligible document types and papers without full text, 298 records remained.

Screening involved two stages: first, titles and abstracts were assessed for relevance; second, full texts were reviewed. Only studies explicitly examining post-COVID-19 consumer behaviour regarding digital, mobile, contactless payments, e-wallets, or payment apps were retained; supply-side or indirect studies were excluded. The final sample consists of 57 peer-reviewed articles, listed in the reference section (Figure 1).

A manual content analysis was conducted using a structured extraction form. Each study was coded for bibliographic information, country/context, payment instrument, theoretical framing, methodology, focal constructs and principal findings. In addition, sustainability-related dimensions, including trust, transparency, perceived control, inclusion, responsibility and consumer autonomy, were coded to support the thematic synthesis. The coding process combined deductive categories derived from the research questions with inductive refinement during repeated reading of the articles. To enhance consistency, the coding framework was iteratively reviewed and category definitions were refined throughout the analysis. Based on this data set, the following sections present (i) a descriptive overview, (ii) a thematic synthesis through a sustainable marketing lens and (iii) an integrative framework linking antecedents, mechanisms and sustainability-related outcomes of post-COVID-19 consumer payment behaviour. A subset of articles was independently reviewed by both authors, and discrepancies were discussed until agreement was reached.

3. Descriptive analysis

Reviewing the post-COVID-19 literature reveals several distinctive patterns in research on consumer behaviour and digital payments when interpreted through a sustainable marketing perspective. This section provides a descriptive map of the selected publications to outline the evolution of the field, highlight the main publication outlets and offer an initial understanding of how research has addressed post-pandemic changes in payment behaviour in relation to broader consumption systems. In line with the objectives of this study, the descriptive analysis focuses on:

the temporal evolution of publications and journal outlets;

methodological approaches and paper types; and

the main payment instruments and consumption contexts investigated, with particular attention to how these dimensions intersect with issues of trust, transparency, inclusion and responsible consumption. This descriptive overview provides the foundation for the thematic synthesis developed in the subsequent section.

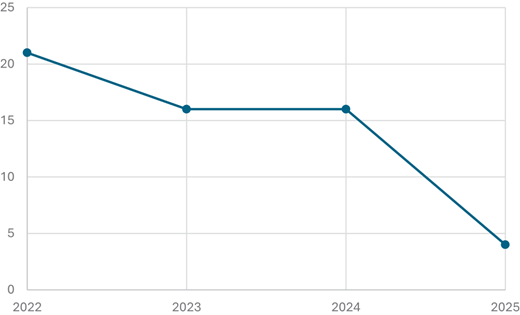

Focusing on the post-COVID-19 period (2022–2025), the volume of studies on consumer behaviour and digital payments reflects sustained scholarly attention, with publication activity increasing over the review window and concentrating in the most recent years. This pattern suggests that research interest has moved beyond the phase of “emergency adoption” triggered by pandemic-related constraints and increasingly addresses post-pandemic stabilisation processes. As shown in Figure 2, the annual distribution of publications on digital payments and consumer behaviour in the post-COVID context indicates that research output remained relatively high between 2022 and 2024, with 21 articles published in 2022, followed by a slight decrease to 16 in 2023 and a modest increase to 16 in 2024. A sharp decline is observed in 2025, with only 4 publications, which likely reflects incomplete indexing and the ongoing publication cycle rather than a genuine reduction in scholarly interest.

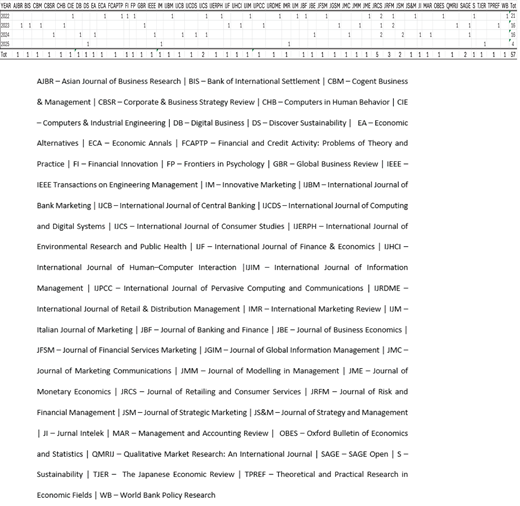

With respect to publication outlets, the corpus is widely dispersed across a large number of journals rather than concentrated within a single disciplinary domain, reinforcing the inherently multidisciplinary nature of post-COVID-19 research on consumer payment behaviour. The reviewed studies span retailing and consumer research, marketing, information systems, finance and ethics/CSR-oriented outlets, reflecting the fact that payment practices sit at the intersection of technological infrastructures, market processes and societal concerns. As shown in Figure 3, the Journal of Retailing and Consumer Services emerges as the most recurrent outlet (n = 5).

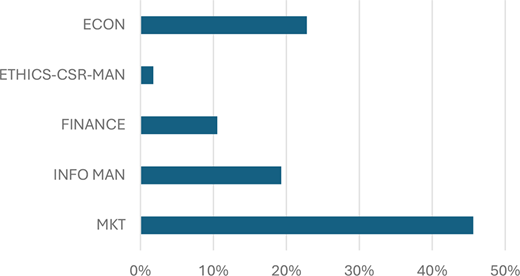

To further clarify the intellectual positioning of the literature, journals were classified by primary field of focus. As reported in Figure 4, research on consumer behaviour in the payments market is predominantly published in Marketing journals (46%, n = 26), followed by Economics (23%, n = 13), Information Management (19%, n = 11) and Finance (11%, n = 6), with only a marginal presence in Ethics–CSR–Management journals (2%, n = 1). From a sustainable marketing perspective, this distribution is particularly revealing. While a substantial share of the literature is published in marketing and ethics/CSR outlets, contributions remain scattered and rarely integrated within a coherent sustainability-oriented framework. This pattern underscores both the growing relevance of sustainability-related concerns, such as trust, responsibility and social impact, in payment research and the absence of cumulative theorisation that explicitly links digital payment ecosystems to sustainable marketing strategies and consumer behaviour.

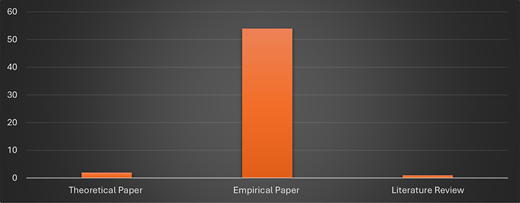

Building on common literature review classifications, the selected studies were categorised by paper type and methodology. Post-COVID-19 research on consumer payment behaviour is predominantly empirical, reflecting a focus on adoption, continuance, trust, security and digitally mediated consumption systems. From a sustainable marketing perspective, this dominance highlights attention to observable behaviours while revealing a scarcity of theory-driven work addressing sustainability implications. A smaller set of conceptual and review papers complements the empirical core but remains limited.

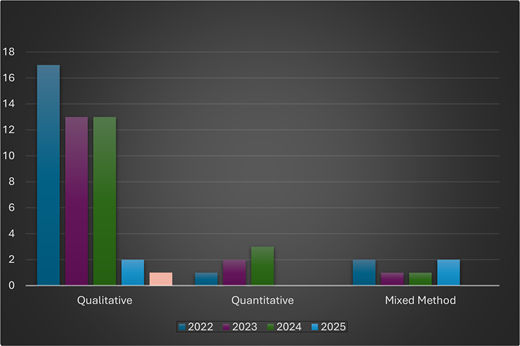

Research designs span quantitative, qualitative and mixed methods. Quantitative studies, mostly survey-based, examine links between consumer perceptions (e.g. perceived usefulness, ease of use, trust, security, perceived risk) and behaviours such as adoption, loyalty or engagement. Sustainability-related constructs are often operationalised indirectly rather than explicitly. Qualitative studies provide rich contextual insights into motives, barriers and situational drivers, showing how consumers interpret digital payment choices in everyday routines. Mixed-method designs, combining perceptual measures with behavioural indicators (e.g. app engagement, channel use), are particularly suited to capturing complex digital consumption ecosystems but remain scarce.

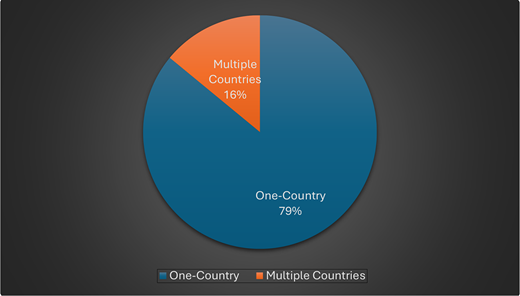

This methodological diversity enriches the field but increases heterogeneity in constructs, measures and levels of analysis, complicating cumulative theory building. As shown in Figure 5, 95% of studies (54 of 57) are empirical, 4% theoretical and 2% reviews, highlighting the need for more theory-driven and interpretive research linking digital payment behaviour to sustainable marketing and responsible consumption. Figure 6 shows qualitative studies dominate (45 articles), while quantitative and mixed-method studies are limited (6 each). Figure 7 indicates a strong prevalence of single-country studies (79%), with cross-country research representing only 16%, revealing limited comparative or international perspectives.

4. Thematic analysis

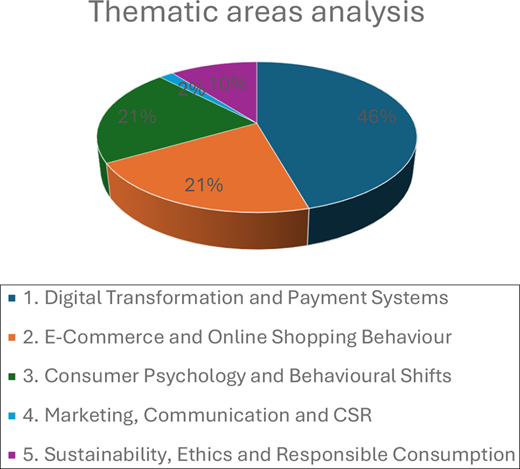

This review adopts a multidisciplinary perspective to explain how consumers reconfigured payment and shopping practices post-COVID-19. As illustrated in Figure 8, the thematic analysis organises the evidence into five macro-areas:

digital transformation and payment systems;

e-commerce and online shopping behaviour;

consumer psychology and behavioural shift;

marketing, communication and CSR; and

sustainability, ethics and responsible consumption.

These themes were identified to capture the technological, behavioural, strategic and normative dimensions through which post-pandemic changes have emerged, as well as their interconnections. Together, they reflect the recomposition of payment and consumption practices within digital ecosystems rather than isolated or purely instrumental changes. Each thematic area is discussed in detail in the following subsections.

4.1 Digital transformation and payment systems

Post-COVID-19 research on digital payment adoption (mobile payments, e-wallets, fintech) identifies perceived usefulness, ease of use, trust and security as core predictors (Upadhyay et al., 2022; Kapoor et al., 2022). However, pandemic-induced adoption only persists if service performance and satisfaction remain stable (Jena, 2022;Petroccione et al., 2025). This suggests that while the health crisis acted as a catalyst for initial trial, the long-term integration of these tools into daily routines depends on their ability to outperform traditional methods in terms of functional reliability and user experience. Consequently, the “forced” nature of adoption during lockdowns is gradually being replaced by a value-driven evaluation of digital service quality.

Significant segmentation exists: younger consumers rapidly normalise digital payments, while older cohorts face barriers related to habit and technology readiness (Ardiansah et al., 2024; Jena, 2023). Macro-level analyses show that this acceleration depends on pre-existing financial inclusion and digital infrastructure (Demirgüç-Kunt et al., 2022). These findings highlight a persistent “digital divide” where socio-demographic factors and regional technological maturity dictate the pace of the cashless transition. From a sustainable marketing perspective, such disparities necessitate inclusive design strategies that address the specific cognitive and structural constraints of vulnerable or less tech-savvy populations.

Overall, post-pandemic behaviour reflects an ecosystem process shaped by individual perceptions and structural conditions, leading to hybridisation or partial reversion rather than a linear replacement of cash (Wisniewski et al., 2024). This complexity implies that cash remains a resilient psychological and functional anchor for many consumers, particularly in informal or local economies. Rather than a total shift, the current landscape is characterised by “payment multi-homing”, where users select instruments based on the specific context, transaction size and perceived situational risk.

4.2 E-Commerce and online shopping behaviour

This area examines how pandemic-era online habits evolve post-crisis. Key determinants of continuance include perceived behavioural control and consumer commitment (Al Hamli and Sobaih, 2023). Within the digital customer journey, payment choice is a critical touchpoint that can either reduce friction or amplify perceived risk, directly influencing conversion (Bhatti et al., 2022). The seamlessness of the checkout process has therefore become a primary competitive advantage in the digital retail space, as any perceived technical hurdle can trigger cart abandonment. Modern consumers increasingly expect a “one-click” experience that balances high-speed processing with transparent security protocols.

Channel choice remains dynamic: while some shifts persist, others revert based on convenience and situational constraints (Kao, 2024; Tran et al., 2023). In sectors like food services, persistence relies on service experience rather than lingering crisis effects (Singh et al., 2024). This transition from “necessity-based” to “convenience-based” shopping indicates that the post-pandemic market has entered a mature phase where digital channels must compete directly with the sensory and social benefits of physical stores. Success in this environment is increasingly tied to omnichannel strategies that allow for a fluid movement between online discovery and offline fulfilment.

Ultimately, post-pandemic online shopping is highly segmented, with the acceptance of contactless alternatives (e.g. facial recognition vs QR codes) hinging on the balance between convenience and safety (Zhong and Moon, 2022). Emerging evidence suggests that consumer typologies are no longer defined solely by demographics, but by their specific “technological temperament” and privacy concerns. Retailers must therefore navigate a fragmented landscape where some segments embrace high-tech biometric solutions while others retreat toward more traditional, privacy-preserving digital interfaces.

4.3 Consumer psychology and behavioural shifts

The third macro-area integrates evidence on post-COVID-19 psychological and behavioural changes, such as fear, anxiety and shifts in spending habits, linking these mechanisms to the stabilisation of consumption routines (Das et al., 2022; Georgarakos and Kenny, 2022). This psychological reconfiguration suggests that the pandemic acted as a “habit-breaking” event, forcing consumers to renegotiate the balance between emotional impulses and rational planning. Consequently, post-pandemic behaviour is increasingly viewed through the lens of cognitive resilience, where the ability to adapt to digital environments is mediated by the individual’s psychological capacity to manage persistent uncertainty.

A first line of research examines crisis-reactive behaviours, such as panic or compulsive buying, showing how anxiety and perceived scarcity trigger reduced self-control (Huang and Guo, 2023; Yuen et al., 2022). In the context of payments, these dysfunctional patterns often lead to a preference for frictionless “one-touch” transactions that minimise the “pain of paying” during stressful periods. This highlights a critical tension between the convenience of digital payment ecosystems and the need for consumer self-regulation to prevent financial over-extension in volatile economic climates.

A second line focuses on the reconfiguration of offline routines, where safety, comfort and trust have become embedded in the retail experience (Mortimer et al., 2024; Gupta and Mukherjee, 2024). The return to physical stores is thus not a simple reversion to 2019 patterns, but a hybridised experience where hygiene-related expectations and digital integration coexist. This shift implies that brick-and-mortar retailers must now offer “psychological safety” alongside traditional value propositions to maintain footfall and customer loyalty.

Finally, macro-level evidence shows that COVID-19 reshaped household saving and spending, influenced by fiscal policy and unequal digital capabilities (Georgarakos and Kenny, 2022; Šostar and Hak, 2025). These findings underscore that post-pandemic recovery is deeply uneven, with “technological temperament” and health-related constraints creating fragmented consumption trajectories. From a sustainability perspective, this heterogeneity requires more nuanced marketing interventions that account for the differing levels of consumer vulnerability and financial literacy across socio-economic segments.

4.4 Marketing, communication and CSR

The fourth macro-area examines how marketing and CSR narratives shape post-pandemic environments, framing communication as “soft infrastructure” that facilitates trust and stabilises new practices. Beyond mere product promotion, post-pandemic communication serves a pedagogical function, guiding consumers through the complexities of new digital interfaces and contactless protocols. In this context, the perceived transparency of institutional messaging becomes a fundamental driver of systemic trust, reducing the cognitive friction associated with adopting unfamiliar financial technologies.

A key contribution frames recovery as a process of consumption reorientation guided by social marketing and CSR (Rrustemi et al., 2024). By aligning corporate goals with collective well-being and long-term societal resilience, brands can legitimise the transition to digital-first consumption as a responsible choice rather than a forced necessity. This strategic alignment suggests that CSR is no longer a peripheral activity but a central behavioural steering mechanism that reinforces the perceived appropriateness of evolving market routines.

This area also incorporates a macro-perspective on economic instability, where heightened uncertainty affects consumer sentiment and risk sensitivity (Belaid et al., 2023). The effectiveness of marketing initiatives in this volatile landscape depends heavily on the coherence between corporate rhetoric and actual practice. Consequently, organisations that demonstrate genuine institutional reliability and ethical consistency are better positioned to foster the long-term commitment required to sustain digital consumption patterns amidst ongoing global shocks.

4.5 Sustainability, ethics and responsible consumption

The fifth macro-area interprets post-COVID-19 consumer change through a sustainability and ethics lens. Importantly, the reviewed literature does not demonstrate that the pandemic-driven shift toward digital payments was itself motivated by environmental concerns or that digital payment adoption directly produces sustainable consumption outcomes. Rather, the evidence suggests that post-pandemic payment practices may have sustainability-related implications when they affect transparency, perceived control, inclusion, traceability and the design of consumer choice environments. Beyond accelerating digital routines, the pandemic intensified value-based evaluations of what constitutes “responsible” consumption and how consumers reconcile convenience with ethical concerns (Rrustemi et al., 2024; Wong et al., 2023). This shift indicates that the post-pandemic consumer is no longer merely a passive adopter of technology, but an active agent seeking alignment between their digital footprint and personal moral compass. Consequently, the long-term viability of payment infrastructures is increasingly tied to their perceived contribution to social equity and environmental transparency.

A key theoretical contribution is the transition from viewing behavioural change as simple technology adoption toward a broader reorientation of consumption systems. Rrustemi et al. (2024) argued that post-COVID reorientation is not linear, requiring ecosystem-level interventions to stabilise responsible routines under persistent uncertainty. This highlights the necessity for a “purpose-driven” digital economy where social marketing and corporate transparency work in tandem to mitigate the psychological stresses of the crisis. Without such coordinated efforts, the adoption of digital consumption practices remains vulnerable to sudden reversals if consumers perceive a conflict between corporate efficiency and societal well-being.

Complementing this, Wong et al. (2023) linked environmental concern to sustainable consumption through cognitive and affective pathways, identifying COVID-related fear as a contextual amplifier. By distinguishing egoistic, altruistic and biospheric motivations, they explain why sustainable behaviour remains unstable for segments where trade-offs between convenience and responsibility persist. These findings suggest that “green” digital transitions are heavily dependent on the consumer’s emotional state and their ability to rationalise the higher costs often associated with ethical choices. Therefore, for sustainable practices to become permanent, digital ecosystems must lower the “ethical entry barrier” by making responsible options the default and most convenient choice.

Finally, additional studies interpret post-pandemic responsibility through well-being, restraint and control, showing how mental-health vulnerabilities can constrain responsible consumption (Huang and Guo, 2023). Institutional dimensions, such as the transparency and traceability of spending, further highlight the ethical implications of the transition to a cashless society (Šostar and Hak, 2025). This suggests that “financial mindfulness” is a critical component of post-pandemic responsibility, where the traceability of digital payments serves as a double-edged sword for consumer autonomy. Ultimately, the ethical consolidation of these practices requires a regulatory framework that protects vulnerable users while leveraging data to promote more conscious and restrained consumption patterns.

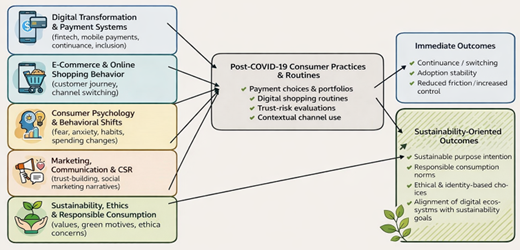

5. Integrative framework

The proposed framework (Figure 9) conceptualises post-pandemic consumption and payment practices as a socio-technical adjustment process rather than a mere choice between instruments. It aligns systematic review findings with sustainable marketing pillars: value creation, authenticity, technology-enabled marketing and generational heterogeneity. This perspective shifts the focus from individual transactions to the broader ecosystem, where the durability of new habits is contingent upon the alignment of digital tools with social values. By framing the transition as a multi-layered process, the framework allows for a more granular analysis of how external shocks are internalised into permanent market structures.

The framework operates through five overlapping layers. At the infrastructural level, digital payment systems (e-wallets, fintech) act as enabling architectures that condition financial inclusion and consumer control. These systems are inherently normative, as their design can either empower users through transparent information or create new forms of digital exclusion. The reliability of these infrastructures is thus the primary determinant of whether pandemic-induced digital adoption evolves into a stable, long-term consumption routine.

Payment practices are further embedded within omnichannel routines, where the design of the digital customer journey can promote responsible decision-making or reinforce convenience-led overconsumption. This suggests that the “architecture of choice” in e-commerce is a critical lever for sustainability, where friction-reduced checkouts must be balanced with ethical prompts. Consequently, marketers must navigate the tension between maximising conversion rates and fostering a deliberative shopping environment that discourages impulsive, unsustainable purchasing.

At the psychological and communicative levels, crisis-shaped drivers like risk perception and anxiety interact with CSR narratives to determine the legitimacy of new practices. The transition to sustainable routines is often hindered by the “intention-behaviour gap,” where emotional stress leads consumers to prioritise immediate convenience over long-term ethical goals. Authentic and transparent communication serves as the “soft infrastructure” necessary to bridge this gap, transforming digital consumption from a necessity into a socially accepted and responsible habit.

Ultimately, the framework identifies three patterns: the partial stabilisation of digital routines, the rise of context-dependent switching and the emergence of value-based trajectories. These patterns indicate that post-COVID-19 behaviour is not a linear progression but a complex portfolio of practices that vary by situational risk and generational maturity. For sustainability to prevail, market ecosystems must ensure that digital transparency and perceived control are the defaults, rather than optional features, thereby aligning technological efficiency with the normative core of responsible consumption.

6. Conclusions

6.1 Theoretical and practical implications

This analysis consolidates the 2022–2025 literature into a coherent multidisciplinary framework encompassing digital infrastructures, e-commerce, consumer psychology, CSR and ethics. By integrating fragmented insights from marketing, information systems and finance, the study supports cumulative theory building in a highly heterogeneous field. The synthesis shows that the pandemic did not merely accelerate pre-existing trends but redefined the theoretical boundaries of consumer agency in digital market environments. As a result, future research should move beyond isolated constructs and adopt a systemic perspective on how payment technologies interact with evolving social norms, market design and sustainability-oriented expectations.

Addressing RQ1, post-COVID-19 payment behaviour emerges as hybrid and portfolio-based rather than a linear transition from cash to digital instruments. Consumers increasingly engage in situational switching, with implications for sustainable consumption that depend on how payment options are embedded within consumption journeys. In response to RQ2, the review identifies a recurring set of technological, psychological and contextual mechanisms jointly shaping adoption, continuance and switching behaviours. These mechanisms influence not only usage, but also consumers’ capacity for deliberation and responsible choice by amplifying or mitigating the “pain of paying”. Regarding RQ3, marketing, communication and institutional arrangements function as mediating “soft infrastructures” that shape the legitimacy of digital payments through trust, transparency and perceived control.

From a sustainable marketing perspective, responsible outcomes depend less on the payment instrument itself and more on how payment options are framed, governed and embedded in digital journeys. Future research should therefore focus on post-adoption dynamics, such as habit persistence and switching, while accounting for regulatory and cross-country institutional differences.

From a managerial standpoint, banks, fintech firms and retailers should prioritise trust management and journey design over the promotion of a single dominant payment method. Supporting payment multi-homing through reliable, transparent and user-centric ecosystems can enhance engagement and legitimacy beyond the pandemic context. Communication and CSR emerge as critical soft infrastructures when embedded in data governance, interface design and choice architecture. Transparency and perceived control thus become central to credible value propositions in digital markets, where consumers increasingly assess offerings in terms of both efficiency and ethical compatibility.

6.2 Limitations and future lines of research

Despite the robustness of this analysis, certain limitations suggest avenues for further investigation. The synthesis focuses on peer-reviewed literature from 2022 to 2025, which captures the immediate post-pandemic shift but may not yet reflect long-term structural changes in global financial regulation. Future studies should therefore adopt longitudinal designs to track how the “new normal” evolves over time, distinguishing temporary crisis-driven adaptations from permanent shifts in consumer psychology. Expanding the scope to include grey literature and industry reports could also provide more granular insights into emerging technological deployments.

A further limitation concerns database selection. The review relied on Scopus as the primary database and Google Scholar as a complementary source, which ensured broad coverage but may still have excluded relevant studies indexed elsewhere, including Web of Science or more specialised journal databases. Accordingly, the findings should be interpreted as a focused synthesis of the immediate post-pandemic literature rather than an exhaustive census of all publications on digital payments and consumer behaviour.

Theoretical development should move beyond technology adoption models to address post-adoption dynamics such as switching behaviour and habit persistence. Evidence suggests that payment decisions are increasingly context-dependent, highlighting the need to examine how regulatory environments and ecosystem maturity act as boundary conditions. Multidisciplinary frameworks combining behavioural economics and socio-technical systems theory may help explain why certain digital habits fail to stabilise across cultural contexts. Investigating the interaction between institutional trust and individual risk tolerance will also be critical for understanding the resilience of cashless infrastructures during future economic shocks.

From a practical perspective, the findings indicate that banks and retailers should move away from promoting single payment methods toward supporting interoperable and trustworthy ecosystems. Future research should examine how embedding payments within data-intensive platforms affects consumer autonomy and perceived control, as well as how different digital “choice architectures” balance frictionless experiences with ethical transparency. Finally, sustainability remains an emerging frontier: future work should explore how responsible consumption motives and ethical self-concepts are mediated by payment transparency and journey design. Features such as carbon footprint tracking or ethical micro-donations warrant further investigation to assess their impact on long-term loyalty and alignment with broader environmental and social responsibility goals.

Building on the present review, future research should develop a more explicit agenda around the conditions under which digital payment systems shape post-pandemic consumption practices. First, scholars should move beyond initial adoption models and examine post-adoption dynamics such as habit persistence, switching behaviour and payment multi-homing across different retail and service contexts. Second, greater attention should be paid to digital choice architectures, particularly how checkout design, interface friction, default options and transparency tools influence impulse buying, spending awareness, and perceived consumer control. Third, cross-country and institutional comparisons are needed to clarify how regulatory protections, digital infrastructure, financial inclusion and trust in institutions condition the legitimacy and durability of cashless ecosystems. Finally, the relationship between digital payments and sustainability should be investigated more directly. Rather than assuming that digital payment adoption is inherently aligned with responsible consumption, future studies should test whether specific features, such as transaction traceability, budgeting prompts, carbon footprint feedback, or ethical micro-donation options, affect responsible consumption outcomes through mechanisms such as trust, transparency and perceived control.