Systematic reviews on sustainability and climate assurance-related constructs have focused on the macro and meso levels, overlooking the role of individuals in carbon assurance as well as the underlying mechanisms supporting its activities. This paper reviews the literature on carbon assurance, employing a microfoundations research framework to examine interactions among the macro, meso (organizational) and micro (individual) levels of analysis.

The literature review covered a sample of 67 peer-reviewed articles (qualitative, quantitative and conceptual) on carbon assurance, published between 2007 and 2025.

First, the macro and meso drivers of carbon assurance have been researched, but little attention has been given to how they interact with individual-level factors. Second, the collective contributions (behaviors and actions) of individuals to carbon assurance outcomes at the organizational and macro levels are poorly understood. Third, the role of formal institutions has been thoroughly researched, but that of informal institutions has largely been overlooked. The latter is a significant gap as informal institutions shape individuals’ behaviors and actions, especially when formal institutions are weak. Lastly, the microfoundations perspective provides insights into how the multiple levels of analysis are interrelated.

The review expands the literature on carbon accounting and climate-related assurance by focusing on the underexplored topic of carbon assurance. Furthermore, it adopts a microfoundations perspective to provide practitioners with a more balanced appreciation of the emerging field of carbon assurance. The microfoundations research approach can be applied to other types of assurance, thus promoting multilevel theorizing. The review findings were consolidated into a holistic future research framework that extends the scope of research on carbon assurance.

1. Introduction

Growing awareness of climate change challenges has prompted stakeholders to exert pressure on companies to adopt strategies to reduce and disclose their carbon emissions or carbon footprint (Hoffmann and Busch, 2008). Proactive companies are responding by adopting strategies such as carbon assurance. Carbon assurance is the third-party verification of carbon emissions data, a process that enhances the accuracy and credibility of carbon emissions disclosures (Ioannou et al., 2016; Luo et al., 2023; Simnett, 2007; Simnett et al., 2009; Zhang et al., 2020) while also improving carbon emissions performance (Rohani et al., 2023).

Several recent review papers have focused on carbon assurance within the broader contexts of carbon accounting (Borghei, 2021; He et al., 2022), sustainability assurance (Hazaea et al., 2022; Zhou, 2022) and external reporting assurance (Venter and Van Eck, 2021). While these papers have advanced carbon assurance by acknowledging its drivers, they still have limitations. For example, Borghei (2021) examined the timelines for international regulatory developments that contributed to the emergence of carbon assurance. He et al. (2022) identified determinants of carbon assurance, including the choice of assurance providers, incentives and companies' institutional backgrounds. Hazaea et al. (2022) and Zhou (2022) provide the broad determinants of sustainability and climate-related assurances, detailing firm-, industry- and country-level characteristics. Venter and Van Eck (2021) offer a more advanced review of external reporting on general sustainability issues, identifying firm-, industry- and country-level determinants and consequences.

However, these papers do not provide a comprehensive review of carbon assurance as an emerging research area, nor do they evaluate it across multiple levels (micro, meso and macro) of analysis. While the macro- and meso-level determinants of carbon assurance are fairly well known (He et al., 2022), the individual-level (micro) focus is largely lacking (Rohani et al., 2023). Where individual efforts do receive attention, the research is limited to the aggregated contributions of individual actors to their organizations. Moreover, the influence of informal institutions on carbon assurance activities has largely been overlooked. Furthermore, these reviews do not explain the interrelationships among the macro-, meso and micro-level factors in the carbon assurance literature.

It is important to address these gaps as climate change practices, including carbon assurance, are multidimensional and shaped by macro, organizational and individual factors (Ascui and Lovell, 2012). Individual factors are particularly salient because they drive the implementation of carbon assurance. A thorough review of the literature on carbon assurance is therefore needed. The fact that the construct has not been the subject of a focused review is linked to the slow development of the construct in academia, which, in turn, is attributable to the difficulty that organizations face in implementing carbon assurance (Datt et al., 2020). The slow uptake in business practice stems primarily from organizational heterogeneity and boundary conditions, which have resulted in different interpretations across jurisdictions (Datt et al., 2018; Rohani et al., 2023; Tang, 2019). Given the dual challenges of limited integration in academic research and slow adoption in practice, a systematic literature review will serve as a bridge to document factors relating to adoption at multiple levels, from the individual level to the macro level. Furthermore, a review will help to advance carbon assurance as a standalone thematic area of study within carbon accounting research, as opposed to a narrow application within climate- and sustainability-related assurance.

This paper presents our approach to conducting a systematic review and the findings arising therefrom. The review focuses on the question: What, and how, do micro-, meso- and macro-level factors shape carbon assurance and its outcomes? We argue that microfoundations research could help organize the carbon assurance literature by mapping carbon assurance factors and outcomes and by demonstrating the mechanisms that drive these relationships. The microfoundational lens is important for a study of this nature because it examines how macro-level factors, such as institutions and social structures, shape organizational processes and individual actions (Coleman, 1994; Cowen et al., 2022; Hedström and Ylikoski, 2010). Furthermore, the microfoundations focus reveals individuals’ actions and how they can be aggregated to contribute to organizational and macro outcomes (Barney and Felin, 2013) – for example, how team carbon assurance practices contribute to organizational carbon performance. Using this approach reveals the linkages across multiple levels of analysis, which is scarce in assurance-related reviews.

This paper's findings contribute to carbon assurance and broader carbon accounting literature through a multi-level framework from the microfoundations perspective. First, microfoundations research shows that interactions among the micro, meso and macro levels can advance research on carbon assurance. The complex nature of adopting carbon assurance requires multiple rather than a single viewpoint. Second, the review shows that research has focused primarily on meso- and macro-level factors and outcomes that drive carbon assurance adoption. Significant literature examined how climate initiatives have led organizations to adopt carbon assurance.

Third, the review demonstrated that micro-level factors have received inadequate attention, leaving a black box around how individual actions and behaviors result in organizational and macro outcomes. Furthermore, the research is also limited in showing the aggregated efforts of the individual actors in contributing to their organizations. This review developed a matrix that shows the roles of the individual actors, driven by the state of development of meso- and macro-institutions in carbon assurance. Fourth, another contribution is the neglect of informal institutions and their influence on carbon assurance activities at the micro, meso and macro levels. Informal institutions matter as they are ignited by individuals in cases where formal institutions are underdeveloped. Research in this area could identify and elaborate on the role of informal institutions in driving carbon assurance activities, especially when the formal institutions are weak and underdeveloped. Lastly, we propose a framework outlining possible research pathways for developing and implementing carbon assurance. Incorporating micro-level factors in this framework provides future research pathways and an opportunity for multilevel theorizing as a desirable approach to advancing carbon assurance research.

The rest of this paper is structured as follows: Section 2 covers the conceptual background to the study and related work on carbon assurance; Section 3 outlines the methodology used to conduct the review; Section 4 presents the findings from the review from a microfoundations perspective; Section 5 presents a framework that summarizes additional research opportunities and outlines the academic and practical implications of the study; and Section 6 concludes the paper.

2. Conceptual background and related work on carbon assurance

Existing literature makes a distinction between carbon assurance and traditional assurance, in the form of financial assurance (audits) and sustainability assurance. Carbon assurance focuses on sources of carbon emissions or derivatives thereof in the manufacturing, energy, construction and transportation industries (Trotman and Trotman, 2015; Zhang et al., 2020). Financial assurance focuses on (through the audit mechanism) revenues and expenses, legal compliance and internal management reporting across all sectors of the economy (Safiullah et al., 2025). Sustainability assurance addresses the broader aspects of environmental and social reporting (Safiullah et al., 2025). Furthermore, carbon assurance differs from corporate social responsibility (CSR) assurance, which typically encompasses social and environmental activities but may exclude carbon emissions, an area that often necessitates specialized expertise (Datt et al., 2020). Although carbon assurance remains nascent, its definition and positioning relative to other types of assurance are becoming clearer.

The systematic review of carbon assurance presented in this paper exceeds the scope of other studies, which focus on the broader aspects of carbon accounting and sustainability. Previous literature reviews explored clusters in carbon accounting research, including carbon management accounting, carbon financial accounting, carbon disclosure and reporting and carbon accounting education (Ascui, 2014). More recent studies have developed descriptive themes in carbon accounting, including strategic climate response, determinants of carbon disclosure, assurance of carbon disclosure, quality of carbon disclosure and consequences of carbon disclosure (Borghei, 2021). Sustainability reviews have focused on broader assurance practices, including carbon assurance as a subtheme (Hazaea et al., 2022). These studies have demonstrated that the primary focus of carbon accounting is on establishing broad themes of interest, without demonstrating how these themes are connected across macro, meso and micro levels.

More closely related to our research, the literature review by Venter and Van Eck (2021) examined the assurance of non-financial information in external assurance reporting, revealing firm-, industry- and country-level characteristics that influence external assurance. Although the research addressed broader sustainability issues, the insights remain applicable to carbon assurance research. Venter and Van Eck (2021) raised some interesting debates, but gave limited attention to how macro elements interact with micro elements in external reporting. Other literature reviews have attempted to bring the individual into the debates. For example, Mahran and Elamer (2024) reviewed the literature on the role of chief executive officers (CEOs) in corporate environmental sustainability but did not consider multi-level interactions. Wehrhahn and Velte (2024), in turn, focused on the interaction between the review committee and external assurers. Despite their attempts to integrate the literature, current reviews still omit interactions among individuals, their organizations and the environment.

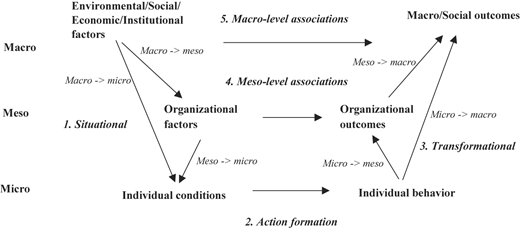

We contend that a microfoundations perspective, using Coleman's (1994) framework, will help to consolidate the literature by showing how the multiple levels are connected. The foundational premise of Coleman (1994) is that individuals play a significant role in explaining the meso and macro mechanisms. In other words, microfoundations do not merely focus on individuals, but also on how individuals interact within their organizations and system-level institutions (Barney and Felin, 2013). Macro elements influence individual behaviors, which, in turn, become transformative actions that affect the macro elements (Cowen et al., 2022).

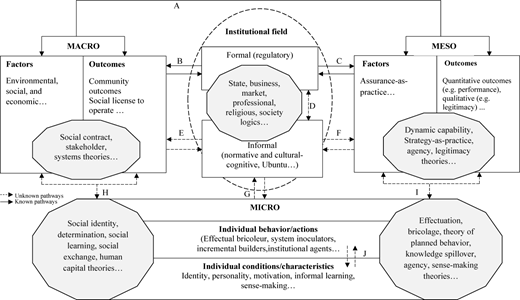

Figure 1 shows the multiple levels used to map carbon assurance research. Since carbon assurance involves the interaction of macro factors, organizations and individuals, the adapted Coleman framework depicted in the figure has three levels (Coleman, 1994; Cowen et al., 2022; Hedström and Ylikoski, 2010). First, the macro level covers environmental, institutional and socio-economic factors. Second, the meso level encompasses organizational factors, including management practices, resources and capabilities, which translate into outcomes. Third, the micro level covers individual factors, such as personalities, skills and beliefs, which translate into actions.

We argue that carbon assurance is a phenomenon that is influenced by the macro factors (e.g. Datt et al., 2020), which translate into meso conditions represented by organizational actions (e.g. Sheldon and Jenkins, 2020) and micro conditions, representing individuals’ characteristics (e.g. Zhang et al., 2020). While existing literature reviews detail the macro and meso elements (e.g. Venter and Van Eck, 2021), it is unclear how all factors within carbon assurance interact. Furthermore, the limited focus on micro elements in the literature reviews limits understanding of how individual agency shapes meso- and macro-level outcomes. Therefore, the microfoundations perspective is a suitable framework for demonstrating the role of individuals in carbon and the interlinkages across multiple levels of focus.

The diagram in Figure 1 also depicts the mechanisms of interaction (Coleman, 1994; Cowen et al., 2022; Hedström and Ylikoski, 2010). Arrow 1 represents situational mechanisms, where elements at the macro and meso levels influence individual conditions. Moreover, meso-level factors influence micro-level conditions and actions. Arrow 2 demonstrates how individual conditions translate into actions or behavior. Arrow 3 depicts the collective actions of individuals that contribute to intended or unintended meso- and macro-level outcomes. Similarly, the arrow indicates that meso outcomes contribute to macro outcomes. Arrow 4 focuses on meso-level associations, which are outcomes derived from organizational factors. Arrow 5 shows outcomes from institutional and social factors.

Adopting the microfoundations perspective contributes to carbon accounting research by emphasizing the need for a systematic approach to understanding assurance practices. First, the focus on multiple levels of analysis in the review extends the accounting literature by adopting various theoretical frameworks at the micro, meso and macro levels. For example, the micro level focuses on individual behavior and actions, which calls for theories from general management and psychology. Second, the review demonstrates that multiple levels of analysis enhance understanding of the context, especially institutional interaction and meaning-making for carbon assurance adoption. Third, the mechanisms of interaction, such as situational and transformative interaction, reveal how the factors lead to specific outcomes. Lastly, the microfoundations perspective yields a framework that demonstrates how the three levels are integrated and underpinned by multidisciplinary theories.

3. Methodology

3.1 Structured literature review design

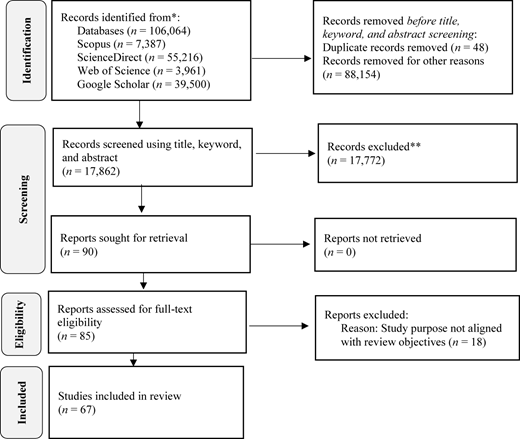

For this study, we employed a structured literature review – defined as “an empirical study that analyzes literature development within a field to answer specific research questions” (Massaro et al., 2016, p. 782). We used a structured literature review framework (Massaro et al., 2016) and Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) (Liberati et al., 2009) to examine a body of scholarly literature and develop insights, critical reflections and future research directions. The PRISMA approach (a four-phase guideline in the form of a flow diagram that improves the reporting and transparency of different types of systematic reviews) provided a detailed protocol for our literature search strategy, which included literature identification, screening, eligibility assessment and final sample size determination. Following Massaro et al. (2016), we organized the search by article impact, country of focus, year of publication, analysis of the authors included in the review, methodology used and level of analysis in each article. Combining these two robust frameworks enabled us to map the carbon assurance literature across the macro, meso and individual levels.

3.2 Literature search

Figure 2 illustrates how we conducted the literature search.

3.2.1 Identification

In the identification phase, we drafted a search plan using keywords (“carbon*” AND “assur”*) to include relevant synonyms for carbon, such as “CO2,” “global warming,” “climate change,” and “GHG,” as well as “assurance” and “assuring” for comprehensive coverage of the topic. We conducted the search using the Boolean features “AND” to include all items and “OR” to identify at least one item (Tranfield et al., 2003). We attached an asterisk/truncation/wildcard search (*) to the root of “carbon” in databases that supported it – except for ScienceDirect – to retrieve results containing any variation of that root. We used four databases – Google Scholar, ScienceDirect, Scopus and Web of Science – because they are peer-reviewed and have typically been used in prior reviews (Ascui, 2014; Bazhair et al., 2022; Borghei, 2021; He et al., 2022). We selected the results (articles) on the basis of the following inclusion and exclusion criteria (see Table 1).

Inclusion criteria

We screened the research results based on journal quality, review period, content and citations. First, we assessed the quality of the articles using the Australian Business Deans Council (ABDC) 2022 and the Academic Journal Guide (AJG) 2024 journal quality rankings to ensure the robustness of the review. We included journals listed and ranked as 4*, 4, 3, 2, 1 (AJG, 2024) and A*, A, B, C (ABDC, 2022) – such as Business Strategy and the Environment; International Journal of Disclosure and Governance; and Sustainability Accounting, Management and Policy Journal. Using both lists assisted in providing an expansive sample of journals. Second, we included articles published between January 1, 2007, and March 6, 2025, to align with the introduction of the greenhouse gas (GHG) assurance standard (International Auditing and Assurance Standards Board, 2012). Third, we ensured that the sample included accounting, business, economics, finance and management disciplines to minimize the exclusion of important studies, as carbon assurance spans multiple subject areas and is performed by both accountants and non-accountants (Datt et al., 2020). We included (English-language) articles discussing GHG assurance, carbon assurance, carbon audits and climate change risk assurance in the sample. Lastly, we assessed the impact of carbon assurance articles by analyzing citations on Google Scholar, as this metric is widely used and highly significant (Massaro et al., 2016).

Exclusion criteria

We excluded articles published in Chinese, Portuguese, French and Russian, as well as grey literature (conference proceedings, letters, book chapters, dissertations, theses and meeting abstracts) because it is difficult to assess the quality of these works, as they are not peer-reviewed. We also excluded articles published in disciplines outside the relevant fields, such as leadership, governance and hospitality. Abstracts that contained the keywords associated with carbon assurance but differed in content were excluded from the analysis. Lastly, we excluded topics that gave broad attention to climate change and sustainability but did not focus on carbon assurance.

The identification phase generated 106,064 articles. We then applied an inclusion criterion to reduce the initial results to a manageable size. This resulted in the exclusion of 88,202 articles (including 48 duplicates), leaving an initial sample of 17,862 that formed the basis for the next phase (screening).

3.2.2 Screening and final sample

We then screened the titles, keywords and abstracts to determine the alignment of the articles with the systematic review's search terms, concepts and purpose. We archived articles on GHG assurance, carbon assurance, carbon audits and climate change risk assurance in an Excel spreadsheet for later retrieval. We also excluded articles with a focus on sustainability, CSR and financial assurance (audits). The final sample for the review comprised 67 articles.

3.3 Analytical framework

3.3.1 Testing the literature review's validity

We read the abstracts and full texts of the articles and eliminated those articles whose content was not specifically geared to carbon assurance (Rousseau et al., 2008). Topics, such as those that focused broadly on environmental or climate audits or whose discussion was not explicitly aligned with carbon assurance research, were excluded.

3.3.2 Achieving reliability

We used Krippendorff's alpha to measure the reliability of the coding scheme (Krippendorff, 2013). Our first attempt yielded a k-alpha of 0.91, which aligned with the recommended score of 0.80 (Krippendorff, 2013). The primary coding differences pertained to research method, location and organizational focus.

3.3.3 Analyzing the content

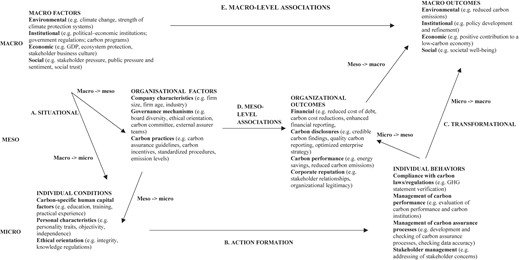

We adopted a three-step content analysis process (Hsieh and Shannon, 2005). In step one, we read the hard copies of the text emerging from the data and descriptively labeled them to develop initial codes on Atlas.ti., a qualitative data analysis software package. In step two, we transferred the Atlas.ti codes to a spreadsheet to facilitate code categorization and theme identification aimed at producing credible, replicable review findings. We grouped similar codes into categories to aid the analysis further. We then regrouped the 191 generated codes into 25 broad categories (see Figure 4), omitting any redundant codes from the categories. In step three, we grouped the 25 categories into seven subthemes and then organized them into three main themes, which are discussed in the next section.

4. Findings and discussion

4.1 Descriptive overview of carbon assurance publications

4.1.1 Journals

Most journals that publish carbon assurance research are from the accounting discipline. Australian Accounting Review publishes the most carbon assurance research, followed by Sustainability Accounting; Management and Policy Journal; Journal of Applied Accounting Research; The International Journal of Auditing; Auditing: A Journal of Practice and Theory; Accounting and Finance; Accounting, Auditing and Accountability Journal; The British Accounting Review; and Business Strategy and the Environment (see Appendix).

4.1.2 Year

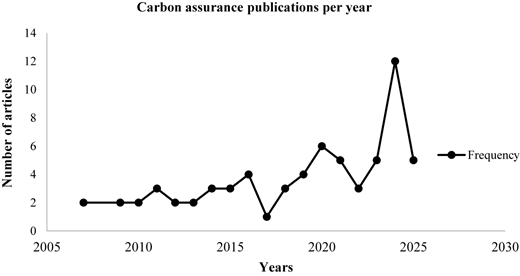

The findings showed that, in recent years, 2024 saw the highest number of carbon assurance articles being published, which may point to the growing popularity of carbon assurance in academic and business circles (He et al., 2022). Figure 3 shows the progression in carbon assurance publications over time.

4.1.3 Country of research

The articles that we coded were drawn from various regions (Africa, Asia, Europe, North America and Oceania). The bulk of the studies (42%) (e.g. Alkebsee et al., 2025; Bugshan et al., 2024; Bui et al., 2021) were conducted across multiple locations (such as Europe, the USA, Australia, India and China). This was followed by studies conducted in Oceania (30%) (e.g. Ekasingh et al., 2019; Green and Li, 2012; Green and Taylor, 2013) and North America (13%) (e.g. Datt et al., 2019; Safiullah et al., 2025). A few sole studies (6%) were conducted in Europe (e.g. Dutta and Dutta, 2021; Simic et al., 2024; Velte, 2024) and Asia (4%) (e.g. Lee et al., 2017; Tang, 2019; Zhang et al., 2020), while Africa (4%) (Pitrakkos and Maroun, 2020; Saa et al., 2025) had the least representation.

4.1.4 Article impact

Table 2 presents the top 10 articles according to citation counts, as determined by Google Scholar. To validate the data, we retrieved the top citations per year from Scopus to address the issue of older articles receiving more citations than newer ones, also known as the Google Scholar effect (Serenko and Dumay, 2015). The use of Scopus was appropriate because it has the largest citation database (Massaro et al., 2016).

4.1.5 Research methods

We categorized the articles as theoretical or empirical and then further grouped the empirical articles into qualitative (e.g. case studies, content analysis, structured and semi-structured interviews, observations) and quantitative (e.g. survey design, partial least squares structural equation modeling, Tobit model regression, linear, logit and probit, Mann–Whitney U test, experimental survey design) and mixed methods (e.g. covering both qualitative and quantitative methods).

Quantitative research was the most frequently employed methodology in carbon assurance research, followed by qualitative research and mixed methods. The majority of the quantitative studies (e.g. Bugshan et al., 2024; Bui et al., 2021; Datt et al., 2018, 2019, 2024; Fan et al., 2021; Green et al., 2017; Safiullah and Nguyen, 2024; Tang and Luo, 2014) used the Carbon Disclosure Project (CDP) database, because it is arguably the world's largest database for listed companies that voluntarily disclose their carbon assurance activities. The selected carbon assurance studies are profiled in Table 3.

4.2 Thematic analysis

We used Coleman's (1994) microfoundations framework to map the research themes that emerged from the carbon assurance literature. The framework (see Figure 4) helped to organize the literature into microfoundations factors and drivers, interaction mechanisms and outcomes of actions and factors.

4.2.1 Theme 1: informal interactions that augment the formal drivers of carbon assurance at the micro, meso and macro levels

4.2.1.1 Subtheme 1: formal regulatory factors are well theorized as antecedents of carbon assurance at the macro level, but the influence of informal institutions remains unknown

The institutional perspective on carbon assurance has centered mainly on formal institutions. The literature demonstrates that carbon institutions (such as energy and emissions-related national laws and emission trading schemes), a country's institutional environment, stakeholder orientation and government spending on green funding are external drivers of the demand for carbon assurance (Datt et al., 2018, 2019; Green and Zhou, 2013; Zhou et al., 2016). For example, the level of economic openness, as reflected in ecosystem-friendly policies, is an important factor determining whether or not companies will adopt carbon assurance (Datt et al., 2018). In addition, growing pressure from stakeholders and public awareness about climate change (evidenced in extreme weather events) have prompted companies to respond by incorporating carbon assurance into their internal business processes (He et al., 2022), shifting from traditional accounting practices, such as financial audits, to new carbon accounting practices (Chithambo and Tauringana, 2014; Tang and Demeritt, 2018). However, the fact that carbon assurance practice remains voluntary in some jurisdictions and industries creates additional challenges, such as a lack of both uniform GHG assurance standards (Datt et al., 2018; Rohani et al., 2023; Tang, 2019) and an internationally recognized regulatory framework governing the assurance of carbon emissions disclosures (Green and Zhou, 2013).

In such cases of a lack of uniform standards, informal institutions, such as normative and cultural–cognitive pillars, which are essentially the unspoken “rules of society” (Scott, 2013), could drive the adoption of carbon assurance, but they remain poorly documented. However, the underdeveloped nature of hard laws (formal regulations) pertaining to carbon assurance creates opportunities for the application of soft laws, which are a mixture of available resources, including informal practices and institutions (Lemma et al., 2024). The normative approach explains the informal norms, standards and values that guide behaviors, while the cultural–cognitive approach focuses on shared beliefs about how individuals engage in meaning-making (Scott, 2013). Studying individuals' and communities' norms and beliefs helps us to better understand how these translate into the adoption of carbon assurance beyond formal institutions.

The literature showed that companies in societies with high levels of social trust engage in more environmentally responsible behavior, such as information transparency (Sun et al., 2023). In addition, informal norms embedded in Ubuntu (humaneness), which is a moral principle found in Sub-Saharan Africa, can inform business and executive decisions relating to climate preservation (Lutz, 2009). Through Ubuntu principles, carbon assurance issues become a matter of collective action and justice in support of climate preservation. Since carbon assurance is not yet universal, numerous informal practices and institutions may serve as substitutes when formal regulations are weak. In other words, the values and beliefs that individuals share as a collective become instrumental in their interactions. Therefore, it is necessary to understand how these shared values and beliefs shape carbon assurance practices beyond formal institutions.

4.2.1.2 Subtheme 2: it is important to move beyond formal organizational characteristics to informal carbon assurance-as-practice

Research on meso-level factors has predominantly focused on quantifiable, formal firm characteristics that influence the adoption of carbon assurance rather than on strategic intent. Firm size influences carbon assurance activities (Datt et al., 2019), with larger and older companies more likely to have assurance and disclosure processes to minimize the risk of criticism (Chithambo and Tauringana, 2014; Datt et al., 2019). Furthermore, large firms with higher emissions levels and more complex energy structures are more likely to secure independent assurance to manage stakeholder pressures, minimize information gaps and build legitimacy (Datt et al., 2018, 2019; Fan et al., 2021). In addition, corporate governance factors, especially gender-diverse boards, executive compensation and incentives and environmental committees, drive firms' adoption of environmental strategies, including carbon assurance (Datt et al., 2018; Velte, 2024; Simic et al., 2024; Zhou et al., 2016).

While these descriptive characteristics provide insights into generic drivers, they do not shed sufficient light on the strategic practices that underpin the adoption of carbon assurance. Drawing on strategy-as-practice (Jarzabkowski et al., 2025), the meso-level drivers discussed in the literature do not adequately explain how and why executives develop strategies for carbon assurance, including the detailed strategic change processes involved. The strategy-as-practice theoretical framing centeres on the human side of management, exploring who does what, what they do, how they do it, what they have and what implications there are for the development and implementation of carbon assurance strategy (Jarzabkowski and Paul Spee, 2009). This conceptualization of assurance-as-practice not only matters to carbon accounting practices; it could also be extended to other climate- and sustainability-related assurances. Future research could develop constructs such as sustainability-as-practice to understand the role of organizations in driving climate initiatives.

4.2.1.3 Subtheme 3: the human capital characteristics of actors can be enhanced by considering how their informal and social learning context can drive carbon assurance adoption

The literature adequately covers individual conditions or characteristics in carbon assurance that are the result of human capital investments – namely, skills, knowledge and abilities that have economic value (Becker, 1964). Olson (2010) suggests that carbon assurance requires cross-functional skills, including operational and process knowledge, as well as accounting expertise, with investors preferring accountants as auditors because they follow stringent processes (Dal Nial et al., 2025). The literature also shows that the ethics and integrity of assurers influence perceptions about carbon assurance quality (Green and Taylor, 2013), as do team leaders' personal characteristics, such as knowledge, reputation and personality (Green et al., 2017). From the above, it is clear that the literature has focused mainly on technical requirements rather than on the social learning context and personal belief systems that may encourage carbon assurance adoption.

Existing research can be extended beyond a focus on technical skills by incorporating intra- and inter-agent elements that highlight individuals' social environment (Marshall et al., 2024). From the intra-agenetic perspective, an individual's personality traits, degree of extraversion or openness, conscientiousness and/or neuroticism can influence carbon-related investment decisions (Dal Nial et al., 2025). For example, identity theory (Stets and Burke, 2000) can explain how some individuals occupying managerial positions identify or self-categorize as environmental conservationists and are likely to support climate-related activities, such as carbon assurance. Meanwhile, self-determination theory can explain some individuals' motivation to support carbon assurance in their organizations (Deci, 1971).

Inter-agent interactions can also promote the development of knowledge, skills and abilities in relation to carbon assurance. While identity theory explains individuals' self-categorization, social identity explains how identity is formed through in-group and out-group interactions (Stets and Burke, 2000). For example, in-groups who are passionate about climate issues can drive the adoption of carbon assurance within their organizations. However, tensions will remain with out-groups who do not identify with climate activities. In such contexts, social learning theory can explain how individuals acquire skills by observing others (Bandura, 1971), where these skills may be converted into carbon assurance behaviors and practices. Social cognitive theory, in turn, explains how individuals learn behaviors and attitudes pertaining to carbon assurance by observing others (Bandura, 1991) while also learning from their lived experiences (Kolb, 1984). More research on inter-agent theories is required to explain individual actions.

4.2.2 Theme 2: individual actions that strengthen and explain the mechanisms of interactions

4.2.2.1 Subtheme 1: while meso and macro interactions are in evidence, micro linkages are often excluded

Macro-level factors affect meso-level factors and micro-level conditions (Cowen et al., 2022; Hedström and Ylikoski, 2010). Macro–meso linkages (which explain how macro-level facts influence organizational factors and actions) are well covered in the existing literature (Datt et al., 2018; Luo and Zhang, 2024; Zhou et al., 2016), highlighting how companies in countries with strong political–economic institutions and stakeholder orientation are likely to adhere to the prescribed carbon assurance disclosures, using third parties (Chatterjee, 2012). However, macro–micro linkages are underexplored in carbon assurance research. The only aspect emphasized at the individual level is that political–economic settings influence the choice of assurers (Datt et al., 2020). In cases where legitimacy is prioritized and stakeholder pressure is applied, companies tend to engage accounting firms as auditors (Datt et al., 2020).

Meso–micro linkages, showing the impact of organizational factors on individual conditions, are also underexplored in the literature. Existing research outlines the roles that managers and employees play in carbon assurance (Datt et al., 2020) but provides limited insights into how companies' strategies influence employees' choices regarding carbon assurance. These knowledge gaps demonstrate the need for multilevel theorizing to provide an integrated view of the interrelationships among the various levels of interaction.

An example of multilevel theorizing is when institutional theories (Scott, 2013) are combined with dynamic capabilities (Teece, 2007) to demonstrate how carbon assurance pressures emanating from the context lead organizations to deploy their internal capabilities, including sensing, seizing and transforming their carbon assurance strategies, for better organizational performance (Teece et al., 1997). These dynamic and strategic activities, implemented by managers, can be explained by agency theory (Jensen and Meckling, 1976). The relationship between the principals and the agents determines the success of implementation, which, in turn, shapes the organization's performance and ultimately enhances its legitimacy. However, the integration of the underpinning theoretical assumptions must be done with great care to ensure that there are no conflicting interpretations and applications across these levels. Therefore, more research is required on multilevel theorizing.

4.2.2.2 Subtheme 2: the actions of individual actors should be defined according to their institutional status

Two actions are important for explaining the interactions among macro-, meso- and micro-level activities. The first action is translating individuals' behaviors into actions. The review's findings indicated that management actions include training technical personnel in low-carbon practices, ensuring compliance with laws and regulations and promoting low-carbon initiatives (Zhang et al., 2020). Carbon management actions involve GHG statement verification, assessment of low-carbon investment, evaluation of carbon performance, compliance attestation and evaluation of the effectiveness of carbon institutions (Tang, 2019). There is, however, a scarcity of research on management actions pertaining to carbon assurance. In this case, individual-level theories can be used to explain how behaviors give rise to actions. For example, the theory of planned behavior (Ajzen, 1991) examines the factors that influence individuals' decisions regarding carbon assurance, from initial intention to actual adoption. In this case, subjective norms (societal pressures), perceived behavioral control (ease of implementation) and attitude toward the behavior (attitude toward third-party verification) will determine the actual carbon assurance adoption process.

The second action is using transformational mechanisms to explain the aggregated actions of individuals and their influence at the macro and meso levels (Cowen et al., 2022; Hedström and Ylikoski, 2010). These outcomes reflect the behaviors, preferences and actions not of a single person, but of a collective (Cowen et al., 2022; Hedström and Ylikoski, 2010). Regarding micro–meso linkages, the carbon assurance literature has scarcely examined the role of collectives in enhancing organizational outcomes. Existing research highlights the role of internal teams in strengthening carbon assurance regulations and managing risks (Trotman and Trotman, 2015). However, little attention has been given to how collectives of individuals, such as audit committee members, senior accountants, internal auditors and partners, view the role of internal teams in the assurance of GHG and energy reporting (Trotman and Trotman, 2015), and how this contributes to organizational outcomes. For example, auditors may help the government to develop climate-related policies by assessing the strengths and weaknesses of institutional arrangements (Tang, 2019). They may also identify irregularities in the allocation of funds to climate-change-related initiatives (Tang, 2019).

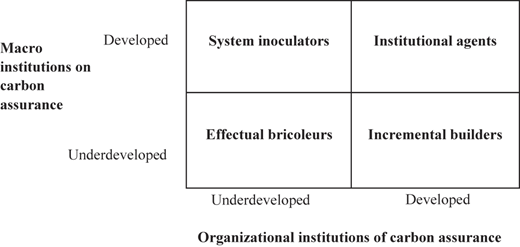

From the review, we identified four roles that individuals can play in advancing carbon assurance adoption, which can be explored more fully in future research. These roles can be assessed at the individual level or aggregated to the team level to demonstrate their impact on other aspects of the company's carbon assurance activities. Figure 5 presents a 2 × 2 matrix of individual roles, which are dependent on the development of carbon assurance institutions at the macro and meso levels.

Actors are “effectual bricoleurs” when they operate in an environment in which both macro- and meso-institutions for carbon assurance are underdeveloped, and there is uncertainty about how things should unfold. A bricoleur's actions flow from making decisions in uncertain environments and “making do” with whatever resources are available, given limited institutional support (Baker and Nelson, 2005; Sarasvathy, 2001). In such an environment, actors may either be spurred into action or remain passive.

Some climate-conscious organizations implement carbon assurance in the interests of their stakeholders, even though national institutions remain underdeveloped. In these kinds of organizations, actors serve as “incremental builders,” reinforcing carbon assurance practices within their institutions and ultimately contributing to the national sustainability agenda. Here, knowledge spillover enables a better understanding of the mechanisms that actors use to transfer carbon assurance practices from their organization to the macro level as system changers. However, it is difficult at times for the actors to penetrate the macro institutions and make an impact. As a result, some may keep the carbon assurance practices within their organizations.

Many climate institutions (e.g. laws, rules and procedures) have been established by the government for implementation in organizations, irrespective of whether the organizations are sufficiently prepared for such a move. In such cases, actors serve as “system innoculators,” taking, for example, enacted legislation or guidance and implementing it in their organizations. Their role is to straddle multiple boundaries and select and interpret information from the environment and transmit it to the organization (Aldrich and Herker, 1977). Ideally, there would be carbon assurance institutions at the macro and meso levels and the actors would be institutional agents with a mandate to implement what is already in place. In this role, they would impact both their organizations and macro institutions.

4.2.3 Theme 3: moving toward multidimensional measures of outcomes at the meso and micro levels

4.2.3.1 Subtheme 1: it is desirable to augment quantitative with qualitative outcomes

The literature demonstrates a range of outcomes of carbon assurance initiatives at the organizational level. Carbon assurance affects multiple forms of disclosure, the integrity of reporting and companies' value (Datt et al., 2024; Khalid et al., 2024; Koutoupis et al., 2024). Companies that are assured are perceived to be legitimate, which enhances their reputation (Khalid et al., 2024). Furthermore, a company's value can be enhanced by attracting investment (Koutoupis et al., 2024), securing higher levels of trade credit (Safiullah et al., 2025) and reducing its cost of debt (Koutoupis et al., 2024). Beyond a company's reputation, identified outcomes are quantitative. In delivering a comprehensive analysis of outcomes, the literature could also focus on the qualitative aspects of carbon assurance and how these contribute to organizational success. In this regard, further insights are required into how carbon assurance adoption has enhanced organizational processes, stakeholder trust, business innovations and strategic initiatives and has reduced greenwashing.

4.2.3.2 Subtheme 2: the community's voice is an important part of meso and macro outcomes

Macro-level associations explain how environmental, social, institutional and economic factors contribute to macro outcomes (Cowen et al., 2022; Hedström and Ylikoski, 2010). However, existing research does not clearly explain the macro-level associations with carbon assurance. For example, the macro-level associations between stakeholders and shareholders and between carbon-emission performance and carbon assurance, remain underexplored.

A frequently neglected stakeholder is the community. Adopting normative approaches, such as social justice and collective action, could give the community a stronger voice in assurance matters. The literature tends to focus broadly on the issue of public pressure (He et al., 2022) without delving into the community's voice. Since a majority of companies with high carbon emissions, such as mining companies, operate in communities, it is essential to include their voices in carbon assurance efforts. Frameworks such as the social license to operate from a community perspective become instrumental in enhancing the community's voice (Breakey et al., 2025). Therefore, future research should consider the community's voice and perspective in carbon disclosure and assurance matters.

5. Framework for future research on carbon assurance

This review demonstrated that carbon assurance has progressed over the years. However, the main finding was the lack of integration across the macro, meso and micro levels of analysis. Furthermore, individual-level factors and the role of informal institutions have been neglected. Figure 6 demonstrates the thematic integration across multiple levels, highlighting well-known research pathways and offering suggestions for future exploration.

5.1 Known pathways

Pathway A demonstrates the relationship between macro and meso factors. The findings from the review showed that macro-level factors influencing meso-level factors have been studied (Datt et al., 2018; Luo and Zhang, 2024; Zhou et al., 2016). However, there is an opportunity to explore the reverse causal relationship, where the meso institutions bring about macro-level changes. In this case, organizations act as agents that bring about institutional changes.

Pathway B, which shows formal regulations as antecedents of carbon assurance, has been well studied in carbon accounting research (Datt et al., 2018; Fan et al., 2021; Rohani et al., 2023). The literature demonstrates that carbon institutions, a country's institutional environment, stakeholder orientation and government spending on green funding drive the external demand for carbon assurance (Datt et al., 2018; Zhou et al., 2016). Carbon institutions, such as energy and emissions-related national laws and emission trading schemes, drive carbon assurance (Datt et al., 2019; Green and Zhou, 2013).

Pathway C focuses on research into how formal institutions have driven the adoption of carbon assurance within organizations. The review findings showed that external regulatory and stakeholder pressures also influence disclosure and assurance of carbon information in businesses (Comyns, 2018). Green and Zhou (2013) and Tang (2019) empirically found that companies operating in countries with mandatory emissions trading institutions adopt carbon assurance. Some countries, such as China, have introduced carbon audit indices that help companies track their activities (Zhang et al., 2020). Using multi-country data, studies have established a positive relationship between formal institutional requirements and carbon assurance.

5.2 Unknown pathways and suggestions for future research

Pathway D represents an opportunity to further explore the interlinkages between formal and informal institutions. Existing research has identified how formal institutions support the adoption of carbon assurance (Datt et al., 2018; Zhou et al., 2016). However, there are cases where carbon assurance institutions are not fully developed. In that context, weak institutions create opportunities for informal institutions to play a significant role. Therefore, further research is required to elucidate how (and what types of) informal institutions address institutional voids and weaknesses in carbon assurance. Furthermore, there is an opportunity to explore the interaction between formal and informal institutions through the lens of institutional logics, such as corporate, state, market and society. In their study, Mahmood and Uddin (2021) found that the co-existence of these logics was instrumental in driving sustainability reporting practices.

Future research in this area can expand on the role of institutional logics, focusing on issues such as: how and under what conditions formal and informal institutions interact to drive sustainable carbon outcomes; and what and how institutional logics drive the adoption and/or enhancement of carbon assurance.

Pathway F concerns the role of informal institutions in addressing macro issues related to carbon assurance. The limited research in this area has focused on culture as one of the informal institutions that can advance carbon assurance (Chatterjee, 2012; Luo et al., 2023). However, it does not reveal how different cultural orientations, including social norms and shared beliefs, influence the uptake of carbon assurance. Future research in this area can focus on issues such as: local indigenous practices that influence carbon assurance; the role of cultural–cognitive and normative institutions in driving carbon assurance; and ethical practices that boost the authenticity and trustworthiness of carbon assurance practices.

Pathway G examines how informal institutions shape individuals' behaviors and actions related to carbon assurance. Informal institutions can guide behavior when formal institutions are compromised. Since the carbon assurance field is still nascent, many actors are prone to greenwashing. The presence of informal institutions that promote integrity would help the actors to respond appropriately in the face of remediable dysfunction (correctable deficiencies, such as producing irregular carbon assurance reports) and non-remediable dysfunction (systematic or fundamental failures owing to, for example, weak state capacity). Future research in this area can focus on issues such as: what and how informal institutions shape the behaviors of actors when the formal institutions are weak; and how actors can navigate and/or overcome remediable dysfunction in carbon assurance practices in an organizational context.

Pathway H explores the relationship between the micro and macro factors influencing carbon assurance, which has received little research attention. As suggested earlier, actors play a limited role as system innoculators. In other words, it is not clear how they interpret macro institutions (such as regulations) and implement them within their organizations. Furthermore, they are effectual bricoleurs in a context where institutional support for carbon assurance is underdeveloped. Future research in this area can focus on issues such as: how managers leverage limited resources to support carbon assurance initiatives; how culture and social factors (such as stakeholder orientation) inform managers' or employees' carbon assurance orientation; and how managers gather emissions data and undertake carbon reporting.

Pathway I explores the relationship between the micro and the meso factors influencing carbon assurance, which has received little research attention. Research has primarily focused on employee incentives (Datt et al., 2018) and the decision as to whether assurers should be professional accountants or consultants (Zhang et al., 2020). Future research in this area can focus on issues such as: how organizations ensure that assurance managers have the necessary education levels, knowledge, personal attributes, ethical value system and sustainability orientation; and how organizations ensure that assurance managers and employees are both technically competent and motivated to engage in carbon assurance activities.

Pathway J focuses on micro-level behaviors and how they are translated into actions. Internal carbon assurance managers play a significant role in introducing and checking carbon management practices (Rohani et al., 2023). However, research on the conditions or qualities of individuals engaged in carbon assurance practices is limited. In addition, extant research on carbon assurance does not explain the processes and mechanisms underlying carbon assurance from the perspectives of employees or managers (Rohani et al., 2023).

Future research in this area can focus on issues such as: how managers can develop internal strategies to counter climate change risks; how managers prepare for carbon assurance audits by third parties and engage with relevant stakeholders; how managers respond to and integrate recommendations on carbon assurance processes; how managers' measurement, reporting and assurance of carbon emissions can be improved through technology; what role employees play in carbon assurance practices in their organizations; and what individual-level theories explain managers' and employees' behaviors and actions in respect of carbon assurance.

The aggregated actions of individuals contribute to meso- and macro-level outcomes, although the review showed that limited research has been conducted on how collectives contribute to organizational and macro outcomes. For example, it is not clear how employees' collective ethical orientation shapes accurate disclosures of companies' carbon emissions. It is therefore important to investigate the effects of multidisciplinary teams on the quality of carbon assurance, comparing the quality of GHG statements assured by a multidisciplinary team and those assured independently by an audit or specialist team. Future research in this area can focus on issues such as: how the collective culture of teams contributes to organizational carbon performance; how the collective identity of teams influences organizations' carbon assurance activities; and how the aggregation of capabilities contributes to improved carbon performance or a reduction in emissions.

6. Conclusion

The focus of the structured literature review was to analyze existing research on carbon assurance from a microfoundations perspective. A key finding was that the drivers of carbon assurance have been comprehensively studied at the macro and meso levels, but not at the individual (micro) level. As a result, it is not clear how individuals' actions translate into carbon management practices. Also unclear is how the collective behaviors and actions of employees and managers, drawing on their respective attributes, influence organizations’ carbon performance and carbon assurance practices.

Another area that has received little research attention is the informal institutions that influence individuals' actions with respect to carbon assurance. Consequently, we developed a framework to show the interactions between informal and formal institutions and how such interactions influence the micro, meso and macro factors and outcomes. The framework also reveals future research pathways.

6.1 Academic implications of the review

The academic implications of the review are three-fold. First, the literature on carbon accounting, sustainability and climate-related assurances could benefit from the adoption of a microfoundations perspective, as climate action requires the participation of individuals, organizations and society at large. A microfoundations perspective would extend existing theories by drawing on insights from other disciplines. Second, the integration of multiple theories, as evident from the study, would allow for multi-level (individual, organizational and macro-level) theorizing and would encourage a better, more holistic understanding of carbon assurance practices. Third, the application of these theories would be context-specific and therefore dependent on organizational dynamics, evolving regulatory processes, prevailing reporting standards in companies and implementation complexities and challenges across different industries.

6.2 Practical implications of the review

The practical implications of the review are evident at the macro, meso and micro levels.

6.2.1 Macro level

The review findings showed that the lack of standardization of carbon assurance guidelines has led to conflicting research results in the literature. To address this problem, policymakers should work with other stakeholders to develop carbon assurance guidelines. In addition, macro-level carbon assurance outcomes are not well articulated. It would therefore be prudent for public institutions to collaborate with private institutions to clearly define macro-level outcomes, including the influence of informal practices in carbon assurance adoption. Lastly, there is limited interaction between social actors and individuals. Policymakers would benefit from engaging with managers at the organizational level in the development of carbon assurance interventions.

6.2.2 Meso level

The findings also showed that companies need creative platforms that support managers’ and employees’ participation in carbon assurance activities and that such platforms should map the carbon assurance skills required by managers and employees. Companies can also run training and educational programs to enhance internal verification processes. However, incentive structures for carbon assurance activities still pose challenges. As a result, companies should develop policy guidelines to incentivize carbon assurance adoption. To this end, companies could also work with industry bodies to optimize conditions for carbon assurance while developing tailored, company- and industry-specific programs.

6.2.3 Micro level

The findings showed limited knowledge about how managers and employees collectively contribute to organizational carbon assurance outcomes. Managers, therefore, need to clarify their internal assurance guidelines and processes, how these processes connect with the overall organizational strategy and goals, and how different teams contribute to better carbon performance and assurance. Managers could also participate in discussions on carbon assurance at the policy level by sharing their lived experiences with carbon management practices.

6.3 Limitations of the review and suggestions for future research

One of the limitations of the review was that it did not consider the different carbon management practices that companies adopt. This is an aspect that could be included in future systematic reviews as it would contribute to the development of standardized approaches. In addition, the review did not explore how the microfoundations perspective can be applied in other climate-related assurances, thereby presenting another future research opportunity.

Another potential research pathway is to conduct meta-analytic tests of the relationship between carbon assurance and macro-, meso- and individual-level outcomes. Such quantitative studies would help to illuminate and defuse contentious issues, such as the relationship between incentives and carbon assurance. There is also considerable scope for future review papers to focus on the role of individuals in carbon assurance, with specific reference to assurance managers who have a pivotal, interfacing role to play at all three levels – macro, meso, and micro.

Appendix

Journals in which sampled articles appeared

| Journal | No. of articles |

|---|---|

| Australian Accounting Review | 7 |

| Sustainability Accounting, Management and Policy Journal | 5 |

| Auditing: A Journal of Practice and Theory | 4 |

| International Journal of Auditing | 4 |

| Journal of Applied Accounting Research | 4 |

| Accounting and Finance | 3 |

| Accounting, Auditing and Accountability Journal | 3 |

| Business Strategy and the Environment | 3 |

| The British Accounting Review | 3 |

| Accounting Horizons | 2 |

| Corporate Social Responsibility and Environmental Management | 2 |

| Current Issues in Auditing | 2 |

| Meditari Accountancy Research | 2 |

| The International Journal of Accounting | 2 |

| The Accounting Review | 2 |

| ABACUS: A Journal of Accounting, Finance and Business Studies | 1 |

| Accounting Forum | 1 |

| Accounting Research Journal | 1 |

| The Accounting Review | 1 |

| Australian Journal of Management | 1 |

| Behavioral Research in Accounting | 1 |

| Critical Perspectives on Accounting | 1 |

| Economics Letters | 1 |

| EuroMed Journal of Business | 1 |

| Finance Research Letters | 1 |

| Journal of Accounting and Organizational Change | 1 |

| Journal of Accounting Literature | 1 |

| Journal of Business Ethics | 1 |

| Journal of Cleaner Production | 1 |

| Journal of Global Responsibility | 1 |

| Journal of International Accounting Research | 1 |

| Journal of International Accounting, Auditing and Taxation | 1 |

| Managerial Auditing Journal | 1 |

| Review of Environmental Economics and Policy | 1 |

| Total | 67 |