The impact of political stability and economic growth on foreign direct investment (FDI) is analysed using a quantitative regression approach in countries of the Gulf Cooperation Council (GCC).

The study used panel data covering the period 1995–2020, involving six GCC countries, and applied quantile panel estimates to determine the relationships between the variables employed in this study.

The findings indicate that trade openness is more dominant and has a positive influence on FDI inflows. Economic growth, financial stability and political stability have a detrimental effect on FDI flows for GCC countries. Furthermore, this research demonstrates that political stability has played a more significant role in FDI flows for GCC countries over the past thirty years.

The empirical findings of quantile estimates offer valuable insights for macroeconomic policymakers in aligning future FDI inflows to GCC countries with uncertainty of global economic conditions, trade barriers and political barriers. Inflows of inward FDI allow GCC countries to establish bilateral trade with expanding economic blocks and regions that engage in free trade and FDI inflows.

1. Introduction

The economies of the Gulf Cooperation Council (GCC) consist of six countries, including Saudi Arabia, Bahrain, Qatar, the United Arab Emirates, Kuwait, and Oman. Although all six countries differ in size and demographics, they share many of the social, political, and economic characteristics. The GCC countries have the largest oil reserves in the world, and their economies depend on their ability to export oil to other countries (Vohra, 2017). Moreover, few countries in the region also purely depend on oil has led to economic prosperity in the long-term period (Amir et al., 2017). The World Bank (2024a) with the Gulf Economic Update (GEU) projects a 6.9% growth for GCC economies in 2022, driven by the eased pandemic restrictions and a strong market, before slowing to 3.7% in 2023 and 2.4% in 2024. According to the report, investing in green growth has the potential to increase GCC GDP to over USD13 trillion by 2050, as opposed to USD6 trillion without any measures (World Bank, 2024b). It is also evident that many indicators of economic growth, for instance, stock market returns, GDP, current account deficit, inflation, etc., are affected by volatility in energy prices (Beckmann et al., 2020). Although the GCC countries differ in size and demographics, they share many of the social, political, and economic characteristics (Vohra, 2017). The spike in oil prices has drawn attention from around the world to the region. According to Elheddad (2016), the natural resources of those countries can have both positive and negative impacts on economic progress in the long run.

In terms of production, exports, and abundance of capacity, the GCC countries are considered key players in global energy markets. As GCC economies dominate in massive oil and gas reserves, their role is likely to become more important in the future. Meyer and Habanabakize (2018) demonstrated that economic growth has a positive effect on FDI flows in both long and short-term periods. Asif and Majid (2018) and Njangang et al. (2018) also reported a positive relationship between GDP and FDI flows, leading to consistently encouraging and stimulating FDI flows. According to a study by Tahir and Alam (2020), GDP is categorized as an important indicator of a sustainable economy, influencing FDI flows in a significant and positive manner. Elheddad (2016) discovered that relying too heavily on natural resources would make GCC countries vulnerable to any changes in the oil market and increase the effect of crowding out. This condition ultimately diminishes the interest of foreign investors in the area.

The discovery raises questions about whether the area is considered a favourable business climate based on structural characteristics of governance quality and the financial landscape. The distinctive qualities of a nation or area have a substantial impact on the successful adoption and implementation of governance and accounting systems, according to Black (2010). Around 72% of global commerce in the Middle-East and North Africa (MENA) region is done in the GCC region (Saidi and Prasad, 2018). More than 55% of FDI inflows into the MENA area come from GCC countries. In addition, the economy of the GCC nations is heavily dependent on oil and gas resources. Abidi et al. (2018) undertook a study to identify specific criteria of companies that attract GCC investors, despite current institutional and economic constraints in MENA markets.

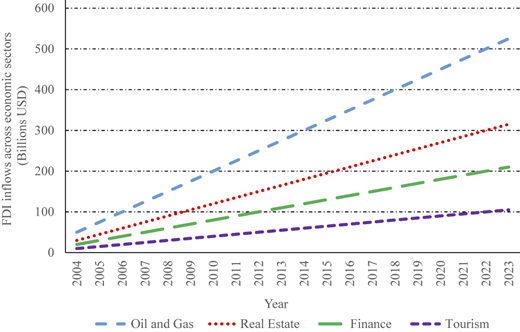

According to Sekkat (2014), there are two theories that can be used to address this. The first point pertains to the ownership structure of investors since FDI typically comes from government agencies that are aligned with national interests and goals. The second reason focuses on the significance of informal networks, which are widespread in Arab countries that assist Arab investors in overcoming the obstacles of information asymmetry more efficiently in local markets. Government support and international influence can lead to exclusive deals and favourable investment terms, particularly in uncertain business environments like those found in MENA countries. Interest rates are increasingly important in influencing international capital flows according to a recent study by Ning and Zhang (2018) and Wang et al. (2019). In addition, Hatmanu et al. (2020) found that interest rates have a negative impact on economic growth, and that exchange rates have a positive impact on growth. The trends in cumulative FDI inflows across GCC countries by economic sectors are indicated in Figure 1.

Trends in cumulative FDI inflows across GCC countries by economic sectors, 2004–2023. Source: World Bank (2024b)

Trends in cumulative FDI inflows across GCC countries by economic sectors, 2004–2023. Source: World Bank (2024b)

The GCC is a major economic group in the Middle East with a combined GDP of around USD1.64 trillion. Saudi Arabia, which is the largest economy in the GCC, accounts for more than half of this total, followed by the UAE and Qatar. Qatar and the UAE are among the wealthiest nations worldwide because of their extensive hydrocarbon resources, leading to high per capita incomes. Despite their reliance on oil and gas, GCC countries are actively working towards diversifying their economies. The tourism, aviation, and finance sectors in the UAE have been expanded, while Saudi Arabia’s Vision 2030 aims to enhance the entertainment, tourism, and technology sectors to reduce oil dependency. The region’s trade significance is enhanced by its strategic location, which connects Europe, Asia, and Africa, with key logistics hubs like Dubai’s Jebel Ali port facilitating extensive trade routes.

The GCC’s economies are susceptible to oil price volatility due to their dependence on oil revenues, as demonstrated by the oil price crash in 2020 during the COVID-19 pandemic. The urgency for accelerated economic diversification is underscored by this vulnerability. The need for workforce nationalization and youth unemployment are further obstacles, leading to initiatives like “Saudization” and “Emiratization” to boost national employment. Economic stability and investor confidence can be affected by geopolitical tensions, such as the Qatar diplomatic crisis, but recent reconciliation efforts are encouraging. The GCC is committing to sustainability and a greener economy by investing in renewable energy projects like Saudi Arabia’s NEOM project and the UAE’s solar initiatives. The GCC region is a resilient economic bloc that has a significant global impact due to its combination of efforts, significant investments through sovereign wealth funds, and strategic trade agreements.

The structure of the paper is as follows. Section 2 deals with the review of literature. Section 3 describes the data and estimation methods, which are then followed by conclusions in Section 4. In the final section of the study, the discussion is concluded, and policy implications and recommendations are presented.

2. Literature review

The GCC nations are distinguished by their distinct traits, extensive natural resources, and geographic location. Furthermore, governance variables such as legal frameworks, regulations, and corruption have a significant impact on FDI inflows. Osmanovic and Avi (2022) analysed the accumulation of FDI from abroad as the primary driver of the development of GCC nations. Simionescu (2016) and Chantasasawat et al. (2010) observed a disparity in GDP performance and FDI flows, indicating a negative connection affected by a global economic slowdown in the GCC region. Kisto (2017) found no significant correlation between GDP and FDI flows, and resource-rich countries receive less FDI because of uneven development in host countries. The role of home country financial development in encouraging outbound FDI from India is highlighted by Nayyar and Mukherjee (2020). ARDL estimates used by Faras and Ghali (2009) revealed significant variations in the significance and contribution of FDI inflows to economic growth in the 6 GCC countries labour productivity growth can be greatly influenced by the efficiency chances and political stability of GCC countries (Elmawazini, 2014).

Suliman and Elian (2014) demonstrate a significant and positive impact and show that local banks are confident in investing in local projects and market segments as their main focus. Increased local competition could also cause harm to FDI due to financial stability. Tahir and Alam (2020) stated that the presence of more private credit experience from SAARC economies discourages FDI in an economy. Zhu et al. (2020) exhibit that the negative impact of financial development on innovation-driven growth may result in a decrease in FDI. Nutassey and Frimpong (2020) claimed that there is no significant connection between financial stability and FDI flows. If oil prices fluctuate in GCC economies, which are abundant in oil, it will negatively affect FDI, which is a result of the natural resource curse (Elheddad, 2016).

Elheddad et al. (2020) investigated the hypothesis of FDI-natural resources curse in oil-dependent countries and found that natural resources and FDI inflows had a negative relationship. Yusuf et al. (2020) empirically found that FDI inflows have a positive long-run effect on West Africa’s economic growth. While the democracy variable does not affect FDI inflows, political instability is found to significantly and negatively affect the growth of the region. According to Rutledge and Polyzos (2022), the GCC region has increased its economic and political stability by relying on Eastern countries instead of North American alliances.

Numerous studies have shown that trade openness has a positive impact on FDI flows. FDI flows in Vietnam can be positively impacted by trade openness, as found by Ta et al. (2020) and Le and Kim (2020). Lien (2021) findings suggested that the Vietnamese government improve the quality of trade openness and maintain economic relations with other countries to increase trade openness in the future. Political stability was identified by Rashid et al. (2017) as the most influential factor among the Asia Pacific countries along with other indicators. Likewise, Asif and Majid (2018) indicate that institutional quality has a positive relationship with FDI flows for both short- and long-run periods. According to the findings, a boost in the quality of institutions will result in favourable changes in FDI inflows. Bannour and Abdelkawy (2024) reveal that trade openness amplifies the positive impact of Sovereign Environmental, Social, and Governance (SESG) on FDI for liberal trade policies in GCC countries. Kishore (2024) discovered that FDI for GCC countries is driven by trade openness, inflation levels, and political stability.

Al-Samman and Mouselli (2018) confirm that FDI and political stability are strongly connected in MENA countries. Few previous studies have indicated that political stability has not been a major factor in attracting FDI inflows (see Tahir and Alam, 2020; Kurul and Yalta, 2017; Kisto, 2017). However, a negative association has been found between political stability and FDI (see Yang et al., 2018; Lucke and Eichler, 2016). FDI inflows can be decreased by the absence of a stable institutional environment due to an increase in perceived risk, which is related to the cost of doing business and investing (Blonigen, 2008). Saudi Arabia, among other GCC countries, has changed their fiscal policies to ensure sustainable macroeconomic performance and attract FDI inflows in the future (Mohaddes et al., 2021). A recent study by Cieślik and Hamza (2023) has shown that FDI inward for GCC countries has a significant impact due to government efficiency, control of corruption, political stability, and rule of law.

Economic freedom was found by Seyoum and Ramirez (2019) to have a positive correlation with inbound FDI, which affects trade flows and government stability. According to Sabir et al. (2019), institutional quality positively influences FDI inflows in all types of nations. Significant coefficients for government effectiveness, political stability, regulatory quality, rule of law, and voice and accountability are higher in rich countries than developing countries. The Japanese and Chinese markets in East Asian countries had a cause-and-effect relationship between political and economic stability (Yorucu and Kirikkaleli, 2021). Political and economic stability in both nations is linked in a bidirectional manner, as demonstrated by a causality test in the temporal domain. Political unrest and high inflation had an impact on FDI inflows in Pakistan. Saleem et al. (2020) found a lasting connection between GDP, trade openness, and institutional strength in relation to FDI inflows.

The unique heterogeneity impact on FDI flows by region-specifically using a quantile regression approach has not been identified in any of the fast studies. This study is unique in that it addresses the research gap by addressing the issues of FDI in terms of economic growth, financial stability, trade openness, and political stability in GCC countries.

3. Data source and methodology

The prominent macroeconomic determinants were utilized in this study to capture the FDI flows of GCC economies. The data is comprised of annual panel observations from 1995 to 2020, with data availability limited to GCC countries such as Saudi Arabia, Bahrain, Qatar, the United Arab Emirates, Kuwait, and Oman. The World Bank (2024b) through World Development Indicators and Center for Systemic Peace (2024)databases were used as sources of data for this study. In addition, the growth rate of real GDP has been employed to determine economic growth, and several comprehensive studies have utilized GDP per capita to evaluate economic growth performance (see Tahir and Alam, 2020; Meyer and Habanabakize, 2018; Asif and Majid, 2018). The study uses the percentage of domestic credit to the private sector as a percentage of GDP to indicate financial development, not financial stability. The trade openness data is determined by comparing the sum of exports and imports to GDP, taking into account the significant size differences between the countries. The Polity IV formulation of Marshall et al. (2002) is used to calculate political stability, and all variables used in this study are described in Table 1.

Data description and sources

| Variable name/Symbols | Description | Data source |

|---|---|---|

| Foreign Direct Investment (FDI) | The total inflow of foreign direct investment into GCC countries. | World Bank (2024b) |

| Economic Growth (GDP) | The real gross domestic product (US Dollar) measured using the deflator value to ensure the inflation condition considered based on the following formulation | World Bank (2024b) |

| Financial Stability (FS) | The domestic credit to the private sector is measured as a percentage of the country’s GDP. | World Bank (2024b) |

| Trade Openness (TOP) | The ratio of exports and imports measured by GDP is the total volume of exports and imports | World Bank (2024b) |

| Political stability (PS) | Political index indicates the measurement of political stability of the country. | Center for Systemic Peace (2024) Polity IV |

To investigate the long-term impact of economic determinants, the use of POLS, DOLS, and FMOLS techniques was utilized in this study. The equation below is the basis for the general panel regression model:

Foreign direct investment is referred to as FDI, economic growth is indicated by GDP, financial stability is indicated by FS, political stability is indicated by PS, and trade openness is indicated by TOP, i denotes GCC countries involve, t shows time, β′s indicates the coefficients, and shows the error term. All estimated variables have been transformed into logarithmic form to avoid biased estimator results due to endogeneity and serial correlation problems. The Dynamic Ordinary Least Square (DOLS) and Fully Modified Ordinary Least Square (FMOLS) methods are utilized to expand the usual least squares estimation by solving serial correlation and endogeneity problems for small sample bias problems. This study uses the null hypothesis formulation to test the following hypotheses:

Economic growth in GCC countries does not have a positive impact on FDI

Financial stability in GCC countries does not have a positive impact on FDI

Trade openness in GCC countries does not have a positive impact on FDI

Political stability in GCC countries does not have a positive impact on FDI

The next phase of this study involves analysing panel cointegration tests like Johansen Fisher and Maddala and Wu (1999) to examine the long-term association between the variables involved. To examine the variation of FDI flows between the economies of the GCC, the panel quantile regression method is utilized. The unique and cross-border characteristics of the GCC’s economic progress and political alliances necessitate a collective response. Therefore, there has been little attention paid to examining the diverse impact of financial and political uncertainties and economic growth determinants on FDI flows through quantile panel regression. Equation (2) provides an illustration of the panel data conditional quantile function, as follows:

where, denotes the dependent variable which is the FDI, are the independent variable vector, is the individual effect and represent the th quantile of regression parameter. The conditional quantile function for quantile regression analysis of the study is expressed in the following equation (3):

4. Empirical findings

The summary descriptive statistics for all variables involved can be found in Table 2. The deviation from the standard deviation of FDI and political stability indicates a high spread out and volatility, which is followed by GDP in GCC economies. The higher variations are a sign of political turmoil in resource-rich GCC economies because of an unstable environment, which caused an outflow of FDI. Additionally, the normal distribution hypothesis is disproven by the skewness and kurtosis values of all series. The Shapiro-Wilk (1965) and Shapiro-Francia (1972) normality tests reject the null hypothesis of a normally distributed series, as shown in Table 3. The existence of heterogeneous conditions among variables is confirmed by this result. It is suggested that panel quantile regression is a more suitable and reliable approach to investigate the diverse conditions of the factors contributing to FDI in GCC economies.

Summary of descriptive statistics

| FDI | GDP | FS | TOP | PS | |

|---|---|---|---|---|---|

| Mean | 0.653 | 10.03 | 3.640 | 4.122 | 3.369 |

| Median | 0.543 | 9.947 | 3.685 | 4.123 | 3.511 |

| Maximum | 3.542 | 11.641 | 4.590 | 4.453 | 4.521 |

| Minimum | −2.681 | 8.453 | 1.917 | 3.853 | 0.000 |

| Std. Dev. | 0.897 | 0.716 | 0.488 | 0.136 | 0.831 |

| Skewness | 0.020 | 0.043 | −0.579 | 0.281 | −1.795 |

| Kurtosis | 3.673 | 2.689 | 3.432 | 2.514 | 7.607 |

Note(s): *, **, *** denotes the rejection of null hypothesis at 1, 5 and 10% significance level, respectively

Normal distribution estimations

| Variables | Shapiro-Wilk test | Shapiro-Francia test | ||

|---|---|---|---|---|

| Statistics | p-value | Statistics | p-value | |

| FDI | 0.980* | 0.002 | 0.978* | 0.002 |

| GDP | 0.962* | 0.000 | 0.964* | 0.000 |

| FS | 0.979* | 0.000 | 0.966* | 0.000 |

| PS | 0.861* | 0.000 | 0.851* | 0.000 |

| TOP | 0.980* | 0.002 | 0.982* | 0.007 |

Note(s): * Statistical significance at the 1% level

The variance inflation factor (VIF) tests to identify multicollinearity across the variables. Table 4 indicates that the variables involved in this study do not experience any multicollinearity effect, given that all series VIF values fall below 4. Pesaran (2021) cross-sectional dependency test rejects the null hypothesis, which implies that there is sufficient cross-sectional dependency condition for all GCC countries. The Pesaran and Yamagata (2008) homogeneity test did not reject the null hypothesis, which indicates that there were not enough conditions for estimating heterogeneous panels in this study, as shown in Table 5.

VIF test for heteroscedastic

| Variables | VIF | Collinearity statistic |

|---|---|---|

| GDP | 1.830 | 0.547 |

| FS | 2.500 | 0.400 |

| PS | 1.140 | 0.879 |

| TOP | 3.680 | 0.271 |

Note(s): The mean VIF for the estimated model equal to 2.290

Cross dependency and homogeneity test

| Variables | Pesaran (2021) CD test results | |

|---|---|---|

| Statistics | p-value | |

| FDI | 6.139* | 0.000 |

| GDP | 4.466* | 0.000 |

| FS | 15.161* | 0.000 |

| PS | 11.876* | 0.000 |

| TOP | 22.877* | 0.000 |

| Pesaran and Yamagata (2008) test results | ||

|---|---|---|

| −0.940 | 0.347 | |

| -adjusted | −1.024 | 0.306 |

Note(s): *, **, *** denotes the rejection of null hypothesis at 1, 5 and 10% significance level, respectively

The panel unit root tests in Table 6 suggest that all series are integrated at first difference, as they do not reject the null hypothesis of unit root existence at any level. To examine the long-term relationship between variables, the study used the Johansen Fisher cointegration approach. The results of Johansen Fisher cointegration for panel and single country results are presented in Table 7 to examine the long-run relationship between the variables. Based on the findings, it can be inferred that there is cointegration between FDI flows and the explanatory variables in the GCC economies, rejecting the null hypothesis of no cointegration (see Table 8).

Panel unit root test results

| GDP | FS | FDI | PS | TOP | |

|---|---|---|---|---|---|

| Panel A: At level | |||||

| LLC | −0.678 | 1.827 | −1.523 | −0.406 | −0.874 |

| Breitung | −0.124 | −1.019 | −0.309 | −0.573 | −1.257 |

| IPS | −0.366 | −0.637 | −0.439 | 0.174 | 1.749 |

| Fisher-ADF | 23.381 | 13.321 | 14.002 | 11.392 | 5.146 |

| Fisher-PP | −0.678 | 0.932 | 8.952 | 15.144 | 15.623 |

| CSD-ADF | 4.466 | 15.217 | 5.2421 | 11.876 | 22.877 |

| Panel B: At first difference | |||||

| LLC | −6.809* | −16.618* | −15.456* | −4.314* | −6.802* |

| Breitung | −4.755* | −11.984* | −14.005* | −9.706* | −12.212* |

| IPS | −7.075* | −12.406 * | −7.610* | −5.466* | −13.423* |

| Fisher-ADF | 71.911* | 123.373* | 165.174* | 106.233* | 147.432* |

| Fisher-PP | 105.522* | 301.893* | 152.039* | 108.673* | 128.837* |

| CSD-ADF | 6.958* | 9.456* | 0.735* | 10.266* | 3.2451* |

Note(s): * Statistical significance at the 1% level

Johansen fisher cointegration test results

| Country | Null hypothesis | Cointegration decision |

|---|---|---|

| Bahrain | Rejected | Yes |

| Kuwait | Rejected | Yes |

| Oman | Rejected | Yes |

| Qatar | Rejected | Yes |

| Saudi Arabia | Rejected | Yes |

| UAE | Rejected | Yes |

| Overall panel | Rejected | Yes |

Results of the panel cointegration estimates

| Variable | POLS | FMOLS | DOLS |

|---|---|---|---|

| GDP | −0.267* (0.015) | −0.122 (0.453) | 0.323 (0.287) |

| FS | −0.482* (0.005) | −0.634* (0.004) | −0.408 (0.287) |

| TOP | 3.806* (0.000) | 4.472* (0.000) | 3.436* (0.047) |

| PS | −0.049 (0.529) | 0.126 (0.290) | −0.083 (0.640) |

Note(s): *, **, and *** represents 1, 5 and 10% significance level, respectively. The p-value shows in parentheses

Simionescu’s (2016) study that demonstrates the relationship between the global economic slowdown and FDI flows shows that economic growth is detrimental to FDI flows, as demonstrated by the POLS and DOLS estimates. Most GCC countries have limited growth rates and are heavily reliant on oil exports, which account for almost 80% of their government revenues. In addition, GCC countries must diversify their economies to survive in the uncertain globalized economy and not be solely dependent on hydrocarbon production. The Implementation of a Value Added Tax in 2018 has expanded Saudi Arabia and the UEA’s fiscal strategies, which aim to increase their national income through non-fossil production.

Furthermore, Elheddad (2016) has proven that economic progress can inhibit FDI flows in the oil-rich regions of the GCC, which is in contrast to Meyer and Habanabakize (2018) and Tahir and Alam (2020). Excessive economic growth in the GCC nations could present issues while economic development is often considered a desirable element for FDI. Due to volatile oil prices, the economies of the GCC, which are mainly dependent on oil and gas exports, frequently experience severe economic changes. Foreign investors seeking more stable and predictable conditions may be deterred from investing by inflationary pressures, infrastructural bottlenecks, and other issues caused by rapid economic development. In terms of FDI, the dependence of the GCC country on oil and gas exports could be a double-edged sword, as another interpretation suggests. Investors interested in the energy industry may be tempted by the region’s abundant natural resources on the one hand. On the flip side, it could result in these economies being subject to commodity price changes, leading to uncertainty and risk for investors.

The Global Financial Crises (GFC) has had a negative impact on financial stability and FDI, leading to uncertainty between FDI inwards and bank stability. In 2019, the region also experienced the COVID-19 pandemic. Although Islamic banks are less impacted by global economic uncertainty, the majority of trading and investor partners in GCC countries depend on conventional banks and financial institutions from the global banking sector. Low oil prices in the financial sector had an impact on the profitability of production and logistic sectors in GCC countries, which also face unstable financial activities in the region. Most of the GCC banks are branches of major international banks. Currently, these banks are required to transfer ownership to local residents and allow minority ownership of domestic banks.

Furthermore, GCC countries have imposed restrictions on the establishment of new banks and branches in the region. The bank credit ratio shows the capability of banks in raising deposits that are deployed as loans. For GCC countries, the proportion of banks offering private credit offered by financial institutions in GCC countries has expand at the compound annual growth rate which consistent with Zhu et al. (2020) and Tahir and Alam (2020) earlier studies. In general, private credit is an alternative method of providing financing, and most of the banking sectors in GCC countries have recently shown an appetite to expand their financial presence in major global financial markets. In addition, a significant amount of capital has been invested in private credit in the GCC countries, which has increased the total size of the private credit market in the region.

Foreign firms have a greater confidence in generating profits without risking their capital and human resources because political stability is not significantly impacted by FDI flows. The results provided by Tahir and Alam (2020) on SAARC economies and Pradhan (2017) findings on China and India coincide with this conclusion. Moreover, the evidence indicated that trade openness is a positive influence on FDI flows based on POLS, DOLS, and FMOLS estimates. The creation of a favourable investment climate is believed to be influenced by the increase in trade openness between countries, which could result in a positive impact on FDI flows into GCC economies. Furthermore, a boost in trade openness could provide exporting firms with more chances to acquire knowledge of local markets and establish operations in regions. The positive influence of trade openness on FDI flows was supported by Tahir and Alam (2020), Ta et al. (2020), and Le and Kim (2020).

Table 9 presents the results of panel quantile estimation, which was used to investigate the influence of determinants of FDI at all quantiles. The findings suggest that economic growth has a negative impact on FDI at the 0.50 quantile at the 1% level of significance. The empirical findings from Elheddad (2016) indicate that economic growth prevents FDI in oil-rich GCC countries, as shown by the study. Foreign investors may overlook the market’s size, and more foreign companies might select GCC countries as their sole production facility. Simionescu (2016) findings indicate that the negative relationship between GDP and FDI is likely to be a result of the global economic slowdown. In addition, financial stability negatively impacts FDI in the GCC economies in the 0.25, 0.50, and 0.75 quantiles.

The Quantile regression estimation results

| Variable | ||||

|---|---|---|---|---|

| GDP | −0.193 (0.112) | −0.343* (0.004) | −0.078 (0.757) | −0.056 (0.892) |

| FS | −0.366*** (0.088) | −0.685* (0.000) | −0.793* (0.010) | 0.101 (0.832) |

| TOP | 2.905* (0.019) | 4.257* (0.000) | 4.008* (0.027) | 1.495 (0.562) |

| PS | −0.046 (0.598) | 0.042 (0.703) | −0.189*** (0.099) | −0.068 (0.633) |

Note(s): *, **, and *** represents 1, 5 and 10% significance level, respectively. The p-value shows in parentheses

The results infer that, without increasing the amount of private credit into the greenfield projects, the banks are progressively facilitating the dominant and existing business entities by financing their operations and enriching the rivalry for the FDI projects in the domestic markets. Zhu et al. (2020) also mention that financial stability would have a negative impact on innovation-led growth conditions, resulting in a decrease in FDI flows. Furthermore, trade openness and FDI have a positive correlation at quantities of 0.25, 0.50, and 0.75. In previous studies, Burakov et al. (2018), He and Choi (2020), Ta et al. (2020), and Lien (2021) also reported similar empirical findings. The long-term growth of FDI in the GCC economies would be a result of the trade openness performance, which would contribute to overall economic progress. The positive impact of trade openness on FDI suggests that open economies can attract FDI to the GCC economies. Furthermore, the study demonstrates that political stability has a negative impact on FDI at 0.75 quantiles. Yang et al. (2018) and Lucke and Eichler (2016) show that political stability has the effect of increasing local investment and decreasing FDI flows in GCC economies. In general, the governance had a significant impact on attracting foreign investors. Moskalev (2007) asserts that the definition of governance quality that benefits foreign investors is not straightforward, and poor governance is not always weak when it comes to protecting investment inflows.

Table 10 displays the Wald test results for the equality of coefficients for 0.25 compared to 0.50 and 0.95 quantiles. Except for the case of financial stability for 0.25 versus 0.50 and 0.95, the hypothesis of parameter homogeneity is rejected, as shown by the results. To examine the relationship between economic growth, financial and political uncertainty, and economic growth in GCC economies, it is important to consider the heterogeneous distribution. Additionally, the financial stability is experiencing the most significant changes in the 0.25 against 0.50 and 0.95 quantiles, respectively. Countries that have a large supply of oil resources are investigating the potential for FDI inflow and resource-driven financial development in GCC economies, according to the conclusion.

Wald tests for the quantile equality of slopes

| Variable | 0.25 vs. 0.50 | 0.25 vs. 0.95 |

|---|---|---|

| ΔGDP | 0.149 (0.187) | −0.287 (0.187) |

| ΔFS | 0.319*** (0.098) | −0.786*** (0.098) |

| ΔTOP | −1.352 (0.218) | 2.762 (0.218) |

| ΔPS | −0.089 (0.341) | 0.110 (0.341) |

Note(s): *, **, and *** represents significance level at 1, 5 and 10%, respectively. While the p-value in the parentheses

GCC countries have a positive relationship between trade openness and FDI flows. Eissa and Elgammal (2020) claim that this occurs because countries with large oil reserves, like those in the GCC, have enough financial resources to finance their economic development. In GCC countries, there was a minimally negative correlation between interest rates and FDI flows. Hye and Wizarat (2013) asserted that the financial liberalization element is having a negative impact. Mushtaq and Siddiqui (2016) pointed out that investing uncertainties rise because of macroeconomics’ diffusion model and demand after liberalization. Contradictory results exist with the work of Osmanovic and Avi (2022), who demonstrated a positive relationship between economic growth and FDI.

In GCC economies, the negative association between the abundance of natural resources is viewed as a curse. Elheddad (2016) conducted a study that found that some countries view natural resources in abundant countries as a blessing, while others see them as curses. Oil price volatility has resulted in a decrease in FDI inflows in oil-rich GCC economies, which shows a negative association between political stability, financial stability, and economic growth with FDI. The volatility of oil prices is clearly preventing FDI in GCC countries, and the focus of FDI inflows in GCC countries has been on resource sectors like oil, gas, and gold. Investing in resource sectors may cause an unbalanced expansion in the countries, which is likely to attract positive spillovers of FDI. The GCC countries that are more dependent on oil have less trade diversification, which increases their vulnerability to external shocks. Our conclusion of the negative relationship matches with the results of Alshubiri (2022), where exchange rates are crucial for economic growth and attracting investment, as they may contribute to economic instability and erratic exchange rate policies.

Moreover, GCC countries have a positive correlation between trade openness and FDI. Trade openness policies implemented since 1980, as part of structural adjustment programs by the International Monetary Fund (IMF) and World Bank, have contributed to the FDI flows in the GCC countries. In fact, Bilateral Investment Treaties (BIT) with Organization for Economic Cooperation and Development (OECD) and upper middle-income countries have a favourable impact on domestic institutions of foreign direct investment for GCC countries, as demonstrated by a study conducted by Mina (2009). By providing both long-term economic incentives and a business infrastructure that is favourable for foreign investors, GCC countries have experienced improvements in their foreign investment flows in recent years, according to Alharthi et al. (2024). Liberal policies are essential for attracting FDI, but the GCC economies have found that they can be supplemented by strategies that safeguard local investors and ensure long-term economic stability. According to this study, trade openness is a factor that attracts multinational companies and increases FDI inflows for the region.

5. Conclusions

This study has a threefold impact on the understanding of FDI flows, particularly within the Gulf region. Global financial crises and the COVID-19 pandemic have caused a negative impact on economic growth and FDI flows in the GCC countries, resulting in slower progress of economic growth in the past few days. The negative impact on financial and political stability in the GCC countries can be attributed to the majority of the financial system being based on bank-based financial activities. To guarantee long-term sustainability and attract foreign investment flows in the future, the GCC should reform their domestic financial system with an threshold effect. Even though GCC economies are rich in oil, their economic growth will not persist unless they invest more in productive assets as a long-term investment. The crowding-out effect can be increased by any changes in oil-rich countries due to their resource-rich nature. Therefore, the empirical findings pointed out the significance of all the observed variables in describing FDI at different quantile levels in GCC economies. The study’s findings revealed that trade openness has been more significant in boosting FDI in GCC countries. GCC countries aim to diversify their revenue sources by prioritizing non-oil sectors and increasing their contribution to economic prosperity in the long run. Previous studies have shown that certain resource-rich countries have a lower FDI flow rate than others. Due to the fact that FDI is considered a vehicle, economic growth is slowed down, which leads to the natural resource curse. It is known that resource-rich countries attract more FDI, but this cannot be applied to all countries.

Furthermore, the diversification of these economies could be achieved through the inward FDI from GCC countries. The impact of GDP on boosting trade levels will be linked to the amount of inward FDI (Abdulsahib, 2024). Policymakers must strengthen the quality of governance when devising investment policies to increase FDI. Eliminating trade barriers, promoting economic integration in the region, and strengthening free trade engagement are essential for policymakers. Despite everything, Gulf nations must keep their trade and investment reforms organized within a multilateral framework like the World Trade Organization (WTO) to gain more credibility and maintain open access to global markets. The cost of natural resources, specifically oil prices, has been impacted by financial crises and political turmoil in the Gulf countries. Alternative policies should be implemented by the Arab economy to reduce dependence on the oil sector and decrease vulnerability to external shocks and dependence on natural resources.

This research was funded by the Universiti Teknologi Malaysia Fundamental Research (UTMFR) fund (Vote No. Q.J130000.3855.21H93).