The purpose is to investigate how the coronavirus disease 2019 (COVID-19) pandemic changed relocation behavior in an advanced economy. We compare manufacturing relocations before and during the pandemic to identify differences and similarities over time and between offshoring and backshoring.

We use an exploratory longitudinal trend survey approach with data from two surveys, the first before the pandemic, 2010–2015, and the second during the pandemic, 2020–2022. Both rounds were targeted to the entire population of Swedish manufacturing plants with 50 or more employees. We captured the same set of data for offshoring and backshoring projects in both surveys.

The pandemic did not stop manufacturing relocations. The extent of offshoring decreased, but the extent of backshoring increased. Labor costs remained a key driver for offshoring, but a trade-off versus lead time, flexibility and risk were observed, suggesting a tension between labor cost and a strive for creating shorter supply chains for offshoring. Lead time, logistics costs, market proximity and risk formed a new backshoring construct, with an emphasis on short supply chains, and that increased significantly in importance. At the same time, the importance of quality decreased, creating a need to balance quality against the pursuit of short supply chains for backshoring. Thus, local supply chains seem to be a desired outcome for any manufacturing relocation, suggesting a move towards a multi-local supply chain setup for the global manufacturing footprint.

This is the first longitudinal survey study that captures offshoring as well as backshoring before and during the pandemic. The results offer unique insights into the COVID-19-induced impacts on manufacturing relocations as the same total population was sampled before and after the pandemic, and it provides empirical evidence that neither offshoring nor backshoring are “steady-state” concepts but changes over time.

1. Introduction

The disruptive effects of the coronavirus disease 2019 (COVID-19) pandemic have added to the debate about the international location of manufacturing activities (Verbeke, 2020; Sodhi and Tang, 2021), and they have increasingly highlighted the benefits and challenges of global versus local supply chains and the pros and cons of offshoring and reshoring (Barbieri et al., 2020; van Hoek and Dobrzykowski, 2021; Chen et al., 2022; Bettiol et al., 2023).

The purpose of this research was to investigate how the COVID-19 pandemic changed relocation behavior in an advanced economy. We compared manufacturing relocation before and during the pandemic to identify differences and similarities over time. This research was based on two survey studies on manufacturing relocations: the first study was conducted in 2015–2016 and concerned the period 2010–2015 (i.e. a relatively stable situation after the financial crisis in 2007–2009, according to the World Bank, 2024), and the second was conducted in late 2022 and was concerned with the period 2020–2022 (i.e. during the COVID-19 pandemic). COVID-19 was declared a public health emergency of international concern (PHEIC) on January 30, 2020, and characterized as a pandemic on March 11, 2020, by the World Health Organization (WHO). On May 5, 2023, WHO declared that the disease no longer fit the definition of a PHEIC (World Health Organization, 2023). Hence, the period of 2020–2022 was largely dominated by the COVID-19 pandemic. Both surveys were targeted to the entire population of Swedish manufacturing plants with 50 or more employees. The same survey instrument was used to allow for comparisons over time. Together, the two studies provided a longitudinal perspective. The unit of analysis was the relocation project, and we investigated manufacturing relocations from and to the focal plant. Hence, we use the term “backshoring” to specify that the return movement of manufacturing was to the original plant from which it was previously offshored. The concept of reshoring is more general and refers to relocation from one location to another and not necessarily back to the original location.

The remainder of this paper is organized as follows. First, it reviews the related literature. It then presents the research design and methodology. The main section of the paper presents the results from the two surveys and the corresponding longitudinal comparison. The discussion focuses on the comparison between off- and backshoring over time and on how off- and backshoring perspectives changed during the COVID-19 pandemic, which leads to five propositions. Finally, we discuss implications for researchers and managers as well as limitations, and we provide suggestions for further research. This paper contributes empirical evidence from a longitudinal survey that captures offshoring and backshoring practices before and during the pandemic.

2. Related literature

The research involved two types of comparisons. The longitudinal aspect was concerned with two time periods for data collection: before and during the pandemic. In addition, we contrasted offshoring and backshoring practices to better understand how companies approached manufacturing relocation in changing their manufacturing footprint. This section reviews relevant literature on offshoring versus backshoring as well as on relocations during the pandemic.

2.1 Offshoring versus backshoring

Manufacturing firms have moved business functions to foreign locations for the past 50 years, and offshoring has grown to become a mainstream business practice. Since the millennium shift, a countermovement to offshoring in which manufacturing is brought closer to or all the way back to the original location has been observed. While offshoring is concerned with relocating value-adding activities across national borders to a foreign location, backshoring refers to a relocation back to the domestic location of the firm.

Mihalache and Mihalache (2016) emphasized the geographic aspect of offshoring, as well as the strategic focus on optimizing the value chain, rather than merely access to foreign markets, while noticing that there is no consensus regarding the absolute extent of the activity. There are several studies on the drivers and motivations of offshoring (Lewin and Peeters, 2006; Kinkel et al., 2007; Lewin et al., 2009; da Silveira, 2014; Waehrens et al., 2015). Although researchers have often used a multidimensional perspective and looked at interrelated trends in developed versus emerging countries, empirical results consistently point to cost as the dominant driver in offshoring (Schmeisser, 2013; Lin et al., 2017; Henkel et al., 2022); for example, by relocating labor-intensive operations to a less developed country with lower wage rates, or by outsourcing operations to an offshore contract manufacturer who has the expertise and economies of scale to obtain lower costs. The performance effects of offshoring reported in previous studies are mixed, providing no clear answer (Bhalla et al., 2008; Lo and Hung, 2015). The reason could be that performance is contingent on certain aspects of offshoring, such as strategic motives (Hijzen et al., 2011), the fit between activities and location characteristics (Jensen and Pedersen, 2011), and language and cultural congruence (Gray and Massimino, 2014). Podrecca et al. (2021) performed a longitudinal study of offshoring research and identified three offshoring phases during 2002–2020: expansion (2002–2006), reconsideration (2007–2009) and rationalization (2010–2020). While the first phase included an increase in the level of offshoring, the latter two phases were associated with decreases in the number of offshoring cases.

Research on backshoring or reshoring, in general, has focused on the amount, drivers, contexts and effects, as well as on creating conceptual frameworks (Stentoft et al., 2016). Many survey studies have been conducted to provide quantitative evidence for possible trends (Kinkel, 2012; Canham and Hamilton, 2013; Ellram et al., 2013; Tate et al., 2014; Stentoft et al., 2015). The results differ slightly from study to study, but the common picture is that even if the offshoring of manufacturing has decreased to some degree, the extent of backshoring is unlikely to outpace offshoring. In contrast to offshoring, the drivers for backshoring are many and diverse and typically include quality, flexibility, lead time, market access, proximity to research and development, and access to skills and knowledge (Stentoft et al., 2016; Ancarani et al., 2019; Johansson et al., 2019).

Over time, a consensus view has been established on the main drivers for both offshoring and backshoring activities. Henkel et al. (2022) performed a case survey of 43 case studies from 16 research articles, discussing offshoring and backshoring activities for the respective cases as well as contingencies. They identified three offshoring clusters: resource-seeking, price-cost efficiency and bandwagon, and three backshoring clusters: quality-centric, efficiency-seeking and resource-seeking. Price-cost efficiency was the dominant offshoring reason (22 of 43 cases), and quality-centric dominated the backshoring cases (25 of 43 cases); 12 cases exhibited this combination of offshoring-backshoring focus. Thus, the backshoring decision does not have to mirror the offshoring decision, such that the original offshoring reason is just a result of poor performance related to the original reason. Consequently, companies need to be prepared to reassess manufacturing location decisions in all their aspects.

2.2 Manufacturing relocations during the pandemic

The COVID-19 pandemic added fuel to the discussion on where to locate manufacturing, the relative advantages of homeshoring, as well as the risks and challenges associated with offshoring (Strange, 2020; Xu et al., 2020; Pla-Barber et al., 2021). The research literature contains mixed results. Some researchers reported that very little relocation activity happened and was unlikely to, while others reported on reshoring cases during the pandemic. In all, research on reshoring activities during the pandemic is relatively sparse.

Strange (2020) concluded that widespread reshoring is unlikely and will not lead to resilience but advocated that resilience will come from more globalization to safeguard against individual governments which may close their borders to international movements. Kapoor et al. (2024) saw the regionalization of production and supply chains as a management intervention in response to challenges related to lockdowns and underperforming production nodes. However, they noted numerous problems with such relocations, such as the time required to set up new networks and the high costs of making suppliers compliant and proficient in the necessary skills. Similarly, Panwar et al. (2022) stated that reshoring manufacturing is not practical because a large-scale economic localization would require a radical overhaul, and Handfield et al. (2020) highlighted difficulties associated with setting up new suppliers in other regions and countries. Di Stefano et al. (2022) found that COVID-19 did not spur large waves of reshoring nor plant closures of Italian multinational firms in 2020 or 2021. They argued that with respect to the sunk costs of the global manufacturing footprint, large and permanent shocks to demand, trade and foreign production costs were required to induce behavioral changes and initiate reshoring. Based on interviews up to March 2021, Kamakura (2022) found that Japanese semiconductor firms were unlikely to reshore to Japan because of the pandemic; even though the Japanese government had sought to provide subsidies for supply chain stabilization, this only led to reshoring on a small scale. Van Hoek and Dobrzykowski (2021) interviewed three firms in 2020 that considered reshoring as a method to respond to supply chain disruptions, even though reshoring decision-making was found to be complex and required a long-term perspective. They found that while labor costs may work against the reshoring decision, the need to respond to demand may justify the focus on developing local and nearshore suppliers.

Barbieri et al. (2020) mentioned a few cases of European companies that decided to move production back to Europe, triggered by the new conditions generated by the COVID-19 pandemic and the need to reduce their exposure to risk. Xu et al. (2020) indicated that the post-COVID-19 supply chains will tend to be shorter through revamped strategies focusing more and more on relocations and backshoring. Pla-Barber et al. (2021) and Holgado and Niess (2023) regarded increasing local and regional sourcing as a resilience-oriented action from different perspectives: Pla-Barber et al. (2021) from a conceptual perspective, while Holgado and Niess (2023) interviewed supply chain managers at 10 multinational corporations in the summer of 2021. Belhadi et al. (2021) found that the localization of sourcing (and processing) within the same region to meet the local demand was a key response strategy for risk and resilience, particularly for the automotive industry, based on a survey and interviews with firms in the automotive and airline sectors up until May 2020. Gebhardt et al. (2022) asked the participants in a Delphi study in September–November 2020 to project supply chain adaptations for the year 2025 and found an increasing risk criteria importance for supplier selection, supply chain collaboration and supply chain mapping. Hence, there are a few sources that suggest that backshoring during the pandemic could address risk and resilience as well as create local and regional supply chains. These are related such that shorter and more local supply chains reduce exposure to, for example, risks related to transportation and logistics. If the disruption risk can be contained within the region, risk incidents will not spill over to other regions.

3. Research design and methodology

Based on the mixed results in the extant literature concerning manufacturing relocations during the COVID-19 pandemic with a few examples but also counterarguments, this research aimed to understand how offshoring and backshoring have changed over time. In addition, we captured data for the three-year period 2020–2022 that was largely dominated by the COVID-19 pandemic. This provided us with a longer data collection period on relocations during the pandemic than previous research, which was restricted to data up until mid-2021 (see section 2.2). The purpose of this study was therefore to present and compare empirical evidence of manufacturing relocations before and during the COVID-19 pandemic. We studied the extent and drivers of offshoring and backshoring during the two separate and independent periods. Offshoring and backshoring have been considered strategies for global manufacturing, and the drivers are essential in this context in that they are the factors that motivate a firm to strategically change a location decision (see, e.g. Stentoft et al., 2015; Ancarani et al., 2019; Podrecca et al., 2021; Chen et al., 2022). Figure 1 illustrates the research framework for the study. The research design allowed us to investigate differences between offshoring and backshoring in both periods, as well as the changes over time.

Empirical data were collected in two exploratory surveys designed in accordance with general guidelines and recommendations on survey research (see, e.g. Forza, 2002). Both surveys were pretested by practitioners and researchers familiar with survey research to ensure survey item quality and accuracy. The surveys were developed in both English and Swedish and checked for alignment. In the surveys, the terms “offshoring” and “backshoring” were defined as follows: Offshoring and backshoring refer to transferring manufacturing activities from one geographical location to another, either from the focal plant in Sweden to another country (offshoring) or bringing them back to the focal plant in Sweden (backshoring). The two surveys asked about relocation activities in 2010–2015 and 2020–2022, respectively. Most items were perceptual with a 5-point scale, and the same set of questions was used for both backshoring and offshoring to be able to detect any significant differences. The questions on extent were concerned with the total number of projects in each direction during the period, that is, offshoring from the plant and backshoring to the plant. The questions on drivers were concerned with the “latest, significant manufacturing relocation project” in each respective relocation direction (offshoring and backshoring). Hence, any plant that experienced both offshoring and backshoring projects during the period reported details for both projects. The unit of analysis in this research is the relocation project, and we distinguish between offshoring and backshoring projects.

Both surveys targeted the entire population of plants in all manufacturing industry categories (SIC code 10-33) in Sweden with 50 or more employees. Plants with fewer than 50 employees were assumed to report very low levels of manufacturing relocation based on previous survey results (see, e.g. Kinkel, 2012; Canham and Hamilton, 2013) and were thus excluded in the first survey. Plant information and contact data were provided by Statistics Sweden (the Swedish Central Bureau of Statistics) for both data collection efforts. The population for the first survey constituted 1,637 plants. Plants were contacted by telephone before receiving the survey link by email. Data were collected in late 2015, and after two reminders, 373 responses were received. This is equivalent to a response rate of 22.8%. The survey was repeated in November–December 2022, targeted to the same population definition. The respondents were asked to provide data on their relocations in the period 2020–2022, that is, during the pandemic. The population had grown to 1,791 plants, and 222 responses were received, which transfers to a response rate of 12.4%.

The combination of these two surveys makes up a longitudinal trend survey, in that the surveys concern the same factors, and that the same population definition is targeted, but separated by some time (Giunipero et al., 2005; Cohen et al., 2017). Longitudinal trend studies are different from cohort studies and panel studies since trend studies focus on factors rather than people and do not have to include the same respondents over time, while cohort and panel studies follow individuals over time (Cohen et al., 2017). Lynn (2009) stipulated that the same variables should be used in precisely the same format in repeated studies. Therefore, we used the same set of questions in the new survey. Furthermore, both surveys targeted the same population definition (in line with Giunipero et al., 2005; Cohen et al., 2017), defined as “all plants in all manufacturing industry categories (SIC code 10–33) in Sweden with 50 or more employees.” Hence, we could not sample smaller plants in the second survey even though recent research indicates that even small firms can offshore as well as backshore (Ancarani et al., 2019). In both surveys, we used total population sampling, which is a purposive sampling technique, where the entire population is targeted. Since manufacturing relocations may have been limited to a smaller number of manufacturing plants, total population sampling reduces the risk of missing potential insights from members who would not have been included in a partial sample and allows the researcher to paint a more complete picture. While we could not guarantee that the exact same set of plants responded to the second survey, the population definition remained the same. We checked for the extent of “overlapping surveys,” that is, common respondents from one occasion to the other (Binder, 1998). Of the 222 respondents in the second survey, 56 participated in the first survey, while 166 respondents did not. The characteristics in terms of offshoring and backshoring activities were very similar between these two respondent types: 10.7% and 19.6% of the common respondents had offshored and backshored, respectively, versus 10.8% and 16.3%, respectively, of the new respondents to the second survey.

Table 1 presents the distribution of respondents with respect to plant size and the positions of respondents. The proportion of larger plants with more than 250 employees was stable, while there were smaller and fewer medium-sized plants in the second round. Most of the survey respondents were production managers, plant managers, or global operations directors with presumably good knowledge of manufacturing relocation, based on their experience in production and operations management: 13.8 and 17.3 years for the respondents in the two surveys, respectively. Since the survey items in this research concern offshoring and backshoring projects from and to the focal plant and thus focus on a single perspective, this study can be categorized as a monadic study (Flynn et al., 2018). In such studies, a single informant is useful if the variables are within their own area of expertise (Krause et al., 2018). A monadic study with a single respondent can possibly suffer from common methods bias, but not from respondent bias (Flynn et al., 2018). Hence, these individuals are most likely the best people at each plant to answer these questions. We used Harman’s single-factor test to check for common method variance (Podsakoff and Organ, 1986; Podsakoff et al., 2003). This test checks if a single factor emerges from the factor analysis, which would point to the presence of common method bias (Podsakoff et al., 2003). Our analyses resulted in two to four components for offshoring and backshoring drivers, of which the first component explained between 26.0% and 35.7%. Thus, our data set did not seem to suffer from common method variance. We also tested for non-response bias by comparing differences between the first wave of respondents and the later returns, based on the assumption that late respondents or respondents requiring reminders, respond in a similar way as non-respondents (Armstrong and Overton, 1977; Lambert and Harrington, 1990). However, this test did not indicate any problem with non-response bias in either survey round.

4. Results and discussion

Here, we present and discuss the changes over time: first, concerning the extent of relocation, and second, concerning the drivers for relocation.

4.1 Extent of manufacturing relocations over time

In both surveys, the respondents fell into one of four categories: some plants had only relocated in one direction (either only offshoring or only backshoring during the specific period), some reported details on both offshoring and backshoring projects, and some reported no movement of manufacturing during the specific period. Of the 373 respondents for the 2010–2015 period, 51 plants could be categorized as bi-directional movers (i.e. reporting both offshoring and backshoring projects during the period), 82 offshorers, 48 backshorers and 192 that had “stayed at home.” The corresponding numbers for the 222 respondents for the 2020–2022 period were: 6 bi-directional movers, 18 offshorers, 32 backshorers and 166 non-movers. Thus, the proportion of plants that did not move any production grew considerably, from 51.5% to 74.8%. This suggests a lower activity level overall concerning manufacturing relocations during the pandemic.

Table 2 shows indicators of the extent of relocations. We capture this in terms of the number of projects; the respondents reported the total number of projects in each direction during the period. Table 2 consists of two sections: the upper concerned with the 2010–2015 period and the lower concerned with the pandemic period. The rows in each section concern the number of relocation projects in each direction, which are then divided by the number of years in each period and further by the number of respondents. Finally, the last row in each section shows the average number of relocations per active plant and year. For example, the last number for offshoring in the period 2010–2015, 0.638, is calculated as 509 projects divided by 6 years and 133 plants (51 bi-directional movers and 82 offshorers), which is interpreted as the average number of offshoring projects per active plant and year before the pandemic. The number of active plants for the other situations is 99 backshoring plants before the pandemic (51 bi-directional movers and 48 backshorers), 24 offshoring plants during the pandemic (6 bi-directional movers and 18 offshorers) and 38 backshoring plants during the pandemic (6 bi-directional movers and 32 backshorers).

The change in the number of projects for offshoring and backshoring were tested using a chi-square test. The chi-square value was 12.277, which is significant at the 0.01 level. Thus, the decline in the number of offshoring projects (from 0.227 to 0.165 per year and with respect to the sample size, 373 respondents in 2015 and 222 in 2022) and the increase in the number of backshoring projects (from 0.128 to 0.159 per year and with respect to the sample size) are significant. The proportions of backshoring to offshoring were tested using a binomial proportions test. The ratio with respect to projects (from 47.7/84.3, i.e. 56.6%, to 35.3/36.7, i.e. 96.2%) was significant at the 0.05 level. The ratio indicates almost full balance between offshoring and backshoring during the pandemic.

In summary, the changes over time concerning the number of projects were highly significant. The extent of offshoring projects decreased significantly while the extent of backshoring projects increased significantly from before to during the pandemic. In addition, a noticeable change is that plants active during the pandemic relocated approximately twice as often as before the pandemic, that is, from 0.638 to 1.528 offshoring projects per year (+140%) for plants engaged in offshoring, and from 0.482 to 0.930 backshoring projects per year (+93%) for plants engaged in backshoring.

4.2 Drivers of manufacturing relocations over time

The list of potential drivers of manufacturing relocation in the survey included 20 factors. Country-specific conditions included subsidies, taxes, and duties, while trade barriers included customs, quotas and local content requirements. The respondents were asked to indicate the importance of each factor in the recent relocation decision along a 5-point scale from “very low” (1) to “very high” (5). Table 3 displays the results of a two-tailed t-test for equality of means. The sub-sample sizes for offshoring projects (24) and backshoring projects (38) during the pandemic may seem small, but as noted by Norman (2010, p. 627): “Nowhere in the assumptions of parametric statistics is there any restriction on sample size.” Small samples require larger effects to achieve statistical significance, so a small sample size makes the hurdle to reach statistical significance higher (Norman, 2010). The t-tests as well as the factor analyses—used to identify patterns in each period and comparing this over time, which is discussed in the following sections—are parametric statistical methods, and the sub-sample sizes were sufficiently large to lead to many significant results in the t-tests and to provide strong factor loadings and Cronbach alphas in the factor analyses. The communalities of the factor analyses for the 2020–2022 period ranged from 0.51 to 0.93 and the variables-to-constructs ratios were 11:4 and 11:3 for the offshoring and backshoring analyses, respectively. This indicates that the 2020–2022 factor analyses are sound despite the relatively small sample sizes (MacCallum et al., 1999; de Winter et al., 2009).

A key message from Table 3 is that there were many significant differences between the drivers for offshoring and backshoring. Before the pandemic, seven drivers were rated significantly higher for backshoring and three for offshoring, of which labor cost strongly dominated. The corresponding numbers during the pandemic were five drivers for backshoring and only one for offshoring – labor cost. Labor cost remained the dominant driver for offshoring and was the only factor that was rated significantly higher for offshoring than for backshoring during the pandemic. Quality was no longer the dominant driver for backshoring but was surpassed in importance by four factors: lead time, flexibility, market proximity, and logistics cost. Of these, market proximity and logistics cost newly exhibited significantly higher levels of importance for backshoring than for offshoring. In addition, proximity to R&D was rated significantly higher for backshoring than for offshoring. Below we discuss the results over time for offshoring, followed by backshoring over time.

4.3 Analyzing offshoring drivers over time

Table 3 shows that three factors received a significant increase in the level of perceived importance as drivers for offshoring: lack of qualified personnel at the 0.01 level, and lead time and exchange rates at the 0.05 level. This implies that the average plant investigated these perspectives considerably more during the pandemic than before it. However, only the lead-time factor was rated above 3.0 (the average on the 5-point scale), though awareness of the other two factors increased. In addition, a significant change was noted for the factor concerned with a focus on core areas (at the 0.05 level), but here the change was a significant reduction in perceived importance.

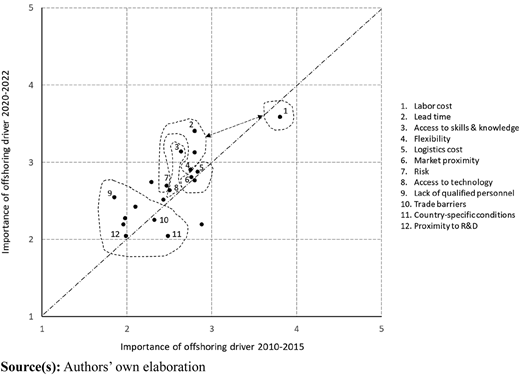

Besides the single-factor analysis in Table 3, we performed an exploratory factor analysis (EFA) on manufacturing relocation project data to investigate how the factors bundled into components (constructs). The result for offshoring is shown in Table 4. The total percentage of variance explained was 75% and 77% for the periods 2010–2015 and 2020–2022, respectively. Hence, these factors provide a considerable amount of explanation for the decision to offshore.

Of the 20 factors, 10 load into three constructs (with Eigenvalues above 1.0) in 2010–2015, and 12 factors load into four constructs in 2020–2022. This suggests that more factors were systematically considered during the pandemic. Each construct can be interpreted as a homogeneous perspective on the offshoring decision, suggesting that the perspective on offshoring broadened with respect to the increase from three to four constructs from before to during the pandemic.

Even though labor cost had a dominant role for offshoring in both periods (cf. Table 3), it displayed an interesting relationship to lead time, flexibility, and risk. During the pandemic, these four factors load together on one construct, albeit that labor cost has a negative sign, indicating an opposite relationship to lead time, flexibility, and risk. The same relationship held in the stable period (2010–2015), but labor cost received a factor loading slightly below 0.6 and was therefore excluded from the construct in that period. However, the factor loading was negative and almost at the level for inclusion in the construct (−0.548). Hence, in both periods, there was a negative relationship between labor cost on the one hand and lead time, flexibility, and risk on the other, indicating a tension or trade-off between labor cost and the other three factors. This interesting observation deserves further research attention.

Figure 2 illustrates the relationship for drivers of offshoring between the two periods. The x-axis indicates the importance of drivers for offshoring in the 2020–2015 period, and the y-axis indicates the importance of drivers for offshoring in the 2020–2022 period. The dashed line along the diagonal shows the position if the ratings were the same before and during the pandemic. A position above the dashed line indicates an increase in importance, and correspondingly a position below indicates a reduction in importance. All factors from Table 3 are included in Figure 2, and the factor groupings into constructs for the pandemic period are encircled.

Labor cost maintained its role as the leading driver for offshoring. Before the pandemic, no other drivers scored above medium importance, that is, above 3 (the middle of the scale; see the x-axis). During the pandemic, lead time, quality, and access to skills and knowledge increased in importance and scored above 3 (see the y-axis). Of these, lead time exhibited a significant increase and narrowed the gap to labor cost.

4.4 Analyzing backshoring drivers over time

Table 3 shows that no fewer than six factors were rated significantly higher as drivers for backshoring in the pandemic period compared to the stable period (and no factor was rated significantly lower). These were market proximity and exchange rates at the 0.001 level, lead time and logistics cost at the 0.01 level, and risk and country-specific conditions at the 0.05 level. All six factors that received higher ratings point toward more local or regional manufacturing footprints. These aspects are analyzed below.

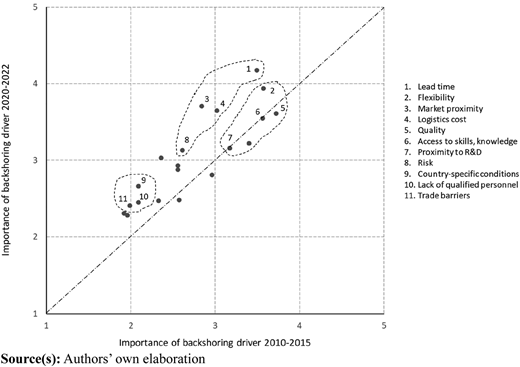

The EFA results for backshoring drivers are shown in Table 5, indicating how the factors bundle into constructs for backshoring. The total percentage of variance explained was 66% and 73% for the periods 2010–2015 and 2020–2022, respectively.

Of the 20 factors, 11 load into two constructs (with Eigenvalues above 1.0) in 2010–2015, and a slightly different set of 11 factors load into three constructs in 2020–2022. The increase from two to three constructs suggests that the perspective on offshoring may have broadened. There was a huge difference between the two constructs in 2010–2015 in terms of driver importance. All five factors in the “development” construct were rated above 3 (3.17–3.57), while all six factors in the “trade and cost” construct were rated well below 3 (1.99–2.56). A similar difference can be noted for the pandemic period: the factors in the “trade” constructs scored well below 3, while all factors in the other two constructs scored above 3. Hence, the major constructs for backshoring changed from “development” to “development” and “short supply chains.” Interestingly, the “development” construct for the pandemic period is largely the same as the corresponding construct for the preceding period, since they share three factors: flexibility, access to skills and knowledge, and proximity to R&D. Thus, the change over time is largely attributable to the addition of the “short supply chains” construct, where only one factor, lead time, was included in a construct in the preceding stable period, while logistics costs, risk, and production close to or in the market were new. This change is illustrated in Figure 3, which shows the changes in importance ratings for backshoring drivers over time: the 2010–2015 period on the x-axis and the pandemic period on the y-axis. The three constructs for the pandemic period are highlighted in the graph.

The key change over time for backshoring is the addition of the construct for “short supply chains.” It consists of lead time, logistics costs, risk, and production close to or in the market, where all four factors experienced a significant increase in the importance assessment for backshoring. This new construct dominated the backshoring drivers during the pandemic. The factors in the other construct with high average scores—“development”—are all positioned approximately in the same position as before the pandemic (cf. Figure 3), that is, very close to the dashed line along the diagonal in Figure 3. Thus, the perspective of local or regional manufacturing footprint had a significant influence on decisions to backshore and resonates well with the empirical findings in Belhadi et al. (2021) and Holgado and Niess (2023).

4.5 Comparing the relocation constructs over time

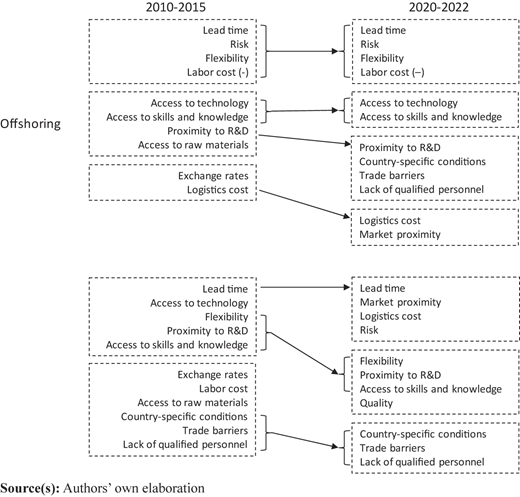

An overview of the changes over time in the EFA construct compositions for offshoring and backshoring is displayed in Figure 4. Most of the factors in the constructs remained over time, which indicates that the drivers for offshoring and backshoring exhibited some stability. However, many of these factors “changed partners.” Figures 2 and 3 show the construct compositions for the pandemic period and how individual factors changed over time. Figure 4 complements these figures by pinpointing the developments over time for the constructs.

An important observation is that the number of constructs had grown over time for both offshoring and backshoring, which indicated an increasing level of complexity of relocation projects. Since we sampled the same population definition twice, the change over time can be considered to have high validity. Only one construct remained unchanged over time. This was the top construct for offshoring, consisting of “lead time”, “risk”, “flexibility”, and “labor cost”, but it should be noted that labor cost did not fully load in the construct in the pre-pandemic period. This construct indicates a tension or trade-off between “labor cost” and the other three items, which suggests that there are competing drivers, and that the organization must find a balance among them.

The aspect of local supply chains seems to be prevalent for both offshoring and backshoring, based on two observations: (1) “logistics cost” and “market proximity” are included in the same construct for both relocation directions, and the same holds for (2) “lead time” and “risk”. Both groups of two items suggest a move towards shorter and more local supply chains. The two groups load in different constructs for offshoring; “logistics cost” and “market proximity” make up a separate construct, while “lead time” and “risk” are balanced against “labor cost” (together with “flexibility”). However, all four items are included in the same construct for backshoring, suggesting a uniform focus on local supply chains.

Quality was the number one driver for backshoring in the pre-pandemic period but did not load together with any other factor then. During the pandemic, quality complemented flexibility, proximity to R&D, and access to skills and knowledge in a construct that can be characterized as a group of factors that are important and remained so over time. However, three of the four factors in the “short supply chain” construct outscored quality in driver importance during the pandemic, implying that the concept of short supply chains was more important than quality for manufacturing relocations from before to during the pandemic.

5. Concluding remarks

In this section, we present the key conclusions and propositions, their implications for managers and researchers, the limitations of this study, and suggestions for future research. This longitudinal trend study offers unique insights regarding the COVID-induced impacts on manufacturing relocation as the same population definition was sampled before and during the pandemic. This research focused on manufacturing relocations from and to Sweden, an advanced economy in Europe. We used the same set of survey questions for offshoring and backshoring in the two survey studies. This allowed us to compare manufacturing offshoring with backshoring in each study and longitudinally to identify changes over time, that is, before and during the pandemic. The key findings are the following.

First, the pandemic did not stop manufacturing relocation, but there were fewer relocation projects overall per year during the pandemic than during the 2010–2015 period. Both offshoring and backshoring projects were carried out, and a shift was noted such that there were relatively more backshoring projects and relatively fewer offshoring projects per year during the pandemic than before it, leading to a balance between relocations from and to Swedish plants. There were fewer plants active in relocating manufacturing during the pandemic than before it, but plants active in this regard exhibited a relatively higher number of relocation projects per year during the pandemic. Thus, some plants reduced, while others increased their engagement in relocation activities during the pandemic. Based on the changes in the extent of offshoring and backshoring, we propose the following:

The extent of manufacturing backshoring is more likely to increase and the extent of manufacturing offshoring is more likely to decrease when the manufacturing operations are affected by major global disturbances, such as pandemic-induced effects.

Second, the key driver for offshoring remained labor cost, even though a few other aspects experienced significant increases in levels of importance – in particular lead time, which was the factor rated second highest for offshoring during the pandemic. An interesting observation is that there seemed to be a trade-off between labor cost on one hand and lead time, risk, and flexibility on the other. This suggests that lead time, risk, and flexibility replaced labor cost as the key driver for offshoring in some cases, potentially based on a desire to establish short supply chains in the vicinity of the host plant. When prioritizing short supply chains in times of disruption, there may not be enough time to find suppliers or contract manufacturers in the target region that can offer the desired labor cost levels. Instead, the importance of labor cost may have had to be downplayed in the offshoring decision-making process. Hence, a tension can be noted between short supply chains and labor costs when offshoring, leading to the following proposition:

A trade-off between labor cost and short supply chains (characterized by lead time, risk, and flexibility) is likely for offshoring decision-making when the manufacturing operations are affected by major global disturbances such as pandemic-induced effects.

Third, the main drivers for backshoring changed. Before the pandemic, quality, flexibility, access to skills and knowledge, lead time, access to technology, and proximity to R&D were rated very important for backshoring. During the pandemic, these factors changed in order of importance, and market proximity and logistics cost were added to the list of factors that were significantly more important for backshoring than for offshoring. Nevertheless, the main difference over time for backshoring was significant increases in importance for lead time, market proximity, logistics cost, and risk, which also formed a construct in the EFA. At the same time, quality dropped from first to fifth place in terms of importance as a driver. This change suggests that backshorers were seeking to create shorter and more local supply chains at the home plant, but with less attention to the quality dimension in this process. A possible explanation is that there was not enough time to find high-quality suppliers in the home region, wherefore the quality aspect had to be downplayed. Hence, a tension can be noted between short supply chains and quality when backshoring. We propose the following:

A trade-off between quality and short supply chains (characterized by lead time, risk, logistics cost, and market proximity) is likely for backshoring decision making when the manufacturing operations are affected by major global disturbances such as pandemic-induced effects.

Fourth, based on propositions 2 and 3, we can conclude that shorter and more local supply chains seemed to be a goal for both offshoring and backshoring of manufacturing. If the global manufacturing footprint aims for shorter supply chains, it means that local or regional supply chains must be set up in various parts of the world to satisfy the market demand in the corresponding region. However, tensions were observed with labor cost for offshoring and with quality for backshoring, implying that plants may have sacrificed some labor cost aspects when offshoring as well as sacrificed some quality aspects when backshoring during the pandemic. This suggests that decision-makers may not have had time enough to consider all aspects to the fullest but have focused on the creation of short supply chains during the pandemic. We propose the following:

The striving for short supply chains in remote locations as well as for the home market is likely when the manufacturing operations are affected by major global disturbances such as pandemic-induced effects.

Fifth, we observed a significant shift in the role of risk for manufacturing relocation from before to during the pandemic. The importance of risk as a driver for manufacturing relocations increased for both offshoring and backshoring (statistically significant increase for backshoring) and risk was included in the major constructs for both offshoring and backshoring, reflecting the strive for shorter supply chains. Risk was joined by lead time and flexibility for offshoring, and by lead time, logistics cost and market proximity for backshoring. This suggests that risk and short supply chains are strongly related for both offshoring and backshoring. A relationship between risk and local supply chains for backshoring has been noted in some recent research (Belhadi et al., 2021; Pla-Barber et al., 2021; Holgado and Niess, 2023), but our study suggests that the relationship is strong for manufacturing relocations in general, that is, irrespective of relocation direction. Hence, we propose the following:

Risk is likely to be a key factor for manufacturing relocations—for both offshoring and backshoring—when the firm is seeking to change the balance between global and local supply chains, potentially affected by major global disturbances such as pandemic-induced effects.

This longitudinal study provides empirical evidence that neither offshoring nor backshoring are “steady state” concepts but change in character over time. Most factors have increased in importance for the relocation decisions; only “focus on core areas” experienced a significant reduction in perceived importance as a driver for offshoring, while three other offshoring factors and six backshoring factors increased significantly in importance for the relocation decision.

The COVID-19 pandemic affected companies and plants differently, such that some firms saw opportunities to increase their global presence, while others moved manufacturing back to the home plant. This indicates that we will likely continue to see different responses to the dynamism in the global environment and pendulum movements in the future between free trade and protectionism as well as between global and local supply chains – not only in normal times but also in times of disruption (Norrman and Olhager, 2024). The risk dimension concerning global manufacturing is likely to grow in importance for decisions on the location and number of facilities and for those on inventory investments in the supply, manufacturing, and distribution networks, reflecting that firms think differently about creating a resilient operations network supporting global product demand.

5.1 Implications for managers

Most importantly, the results from this longitudinal study show that both offshoring and backshoring practices change over time and are becoming increasingly complex. Many factors have increased in perceived importance as drivers for offshoring and backshoring, which suggests that the decision to offshore or backshore is concerned with a broader perspective and more caution than before.

The key drivers for offshoring and backshoring still differ. While labor cost is the key driver for offshoring, the key drivers for backshoring are still many, most notably related to creating short supply chains and proximity to R&D, skills, and knowledge. Hence, there are different key rationales for offshoring and backshoring, suggesting that backshoring is more complex than just a reversal of offshoring.

Shorter and local supply chains have been emphasized during the pandemic for both offshoring and backshoring. There seems to be a tension between this strive and labor cost when offshoring and between short supply chains and quality when backshoring, suggesting that plants have prioritized the creation of short supply chain over other factors to adapt to the changing operating environment induced by the pandemic. Given this tension it is vital to consider these aspects together, raising questions like: Are we willing to downplay labor cost when creating short supply chains abroad, and are we willing to downplay quality aspects when creating short supply chains at home?

Finally, plants have reacted very differently in terms of relocation activity during the pandemic; some have avoided relocations altogether, while others have been quite active in moving manufacturing both from and to the focal plant. There are no simple recommendations that can be made. Each situation is unique, and the plant or firm must do a thorough investigation and build a business case before deciding on a manufacturing relocation. Nevertheless, this study provides a recent update on the factors that have been important for relocations during the pandemic, and that can serve as factors to be considered when investigating potential future changes to the manufacturing footprint.

5.2 Implications for researchers

This type of study—a longitudinal trend survey—is very rare in the OSCM area. We feel that this type of research is very rewarding in that a population can be followed over time to track trends and changes. We advocate more use of longitudinal trend survey in the OSCM area. One advantage of trend studies compared to cohort or panel studies is that the problem of attrition is avoided, that is, that participants leave the survey or die, that would have reduced the number of respondents to draw from in future studies. This is because trend studies focus on factors (a specific phenomenon and related items) rather than people over time, and new samples are drawn for each wave of data collection. We used total population sampling (already in the first survey), which has an advantage over random partial sampling in that it eliminates the risk of biased sample selection. The only drawback of total population sampling is that it is more costly since the entire defined population is targeted. In this research we used the relocation project as the unit of analysis. This allowed specificity and precision about the phenomenon and allowed each respondent to provide details on both offshoring and backshoring activities, thus potentially doubling the number of data collected (compared to individual respondents).

Some of the key factors for offshoring and backshoring reflect a change in the balance between global and local supply chains. Even though labor cost is still the most important driver for offshoring (significantly higher than for backshoring), lead time, risk, and flexibility are increasingly more important as drivers for offshoring, suggesting that shorter supply chains may be desired when moving manufacturing to an offshore location. An interesting construct consists of these factors, but with a trade-off between lead-time, risk, and flexibility versus labor cost (due to its negative sign; see Table 4). A similar type of result is noted for backshoring, where quality has dropped in importance (from first to fifth place) while lead-time, risk, logistics costs, and market proximity all exhibited significant increases in importance and combined to a construct, reflecting short supply chains. This suggests a tension between quality and creating short supply chains for backshoring.

Such tensions have not been observed in previous research, wherefore this is a novel and interesting finding. This observation extends the findings in Henkel et al. (2022). They surveyed 43 case studies from 16 research articles published in 2014–2021 and found that price-cost efficiency was the dominant offshoring reason (22 of 43 cases), while quality-centric drivers dominated the backshoring cases (25 of 43 cases). It should be noted that all reshoring activities in these 43 case studies were carried out before the pandemic. Price-cost efficiency and quality-centric drivers coincide well with the major drivers from our first survey before the pandemic (concerned with 2010–2015), that is, labor cost for offshoring and quality for backshoring. Our second study (concerned with 2020–2022) adds a new perspective to the drivers for offshoring and backshoring, in that the concept of creating short supply chains seems to be at least as important as labor cost or quality.

Additionally, a trade-off or tension was noted that suggests a more complex decision-making process during the pandemic. Handfield et al. (2020), Kapoor et al. (2024) and van Hoek and Dobrzykowski (2021) all brought up problems associated with finding suitable suppliers when relocating manufacturing and concluded that this had hindered manufacturing relocations. Our second study shows that some plants have indeed moved manufacturing during the pandemic, seemingly to shorten their supply chains, but may have downplayed some cost aspects for offshoring and some quality aspects for backshoring. These types of tensions may reflect a departure from a long-term and strategic perspective on global manufacturing footprints to quicker response adaptations to protect the flow of goods to the markets.

The aim to create shorter supply chains for both offshoring and backshoring suggests that firms are moving towards a multi-local supply chain setup, such as having one supply chain for the Americas, one for Europe, the Middle East, and Africa (EMEA), one for China, and one for the rest of Asia (cf. e.g. Norrman and Olhager, 2024). Such a multi-local supply chain setup is required if a firm wants to create shorter and more local supply chains and still supply global demand without excessive long-distance transportation of products. The consequence for manufacturing relocations is then that some manufacturing activities or products are reshored while others are offshored to create local supply chains in multiple regions. Hence, offshoring and backshoring decisions cannot be taken in isolation, but the consequences for the global manufacturing footprint must be considered. We therefore recommend that future research on reshoring (and offshoring) takes the entire manufacturing network into account.

5.3 Limitations

A limitation of the research is the use of a single high-cost country. However, Sweden has been exposed to a high level of both off- and backshoring and is therefore a suitable context for analyzing differences over time. We acknowledge that other factors may be of importance in manufacturing relocations that we did not include. For example, neither environmental and social sustainability nor resiliency were included in the 2016 survey, making it impossible to study any changes in these aspects during the pandemic. In hindsight, it would have been interesting to track how perceptions of sustainability and resiliency may have changed and impacted manufacturing relocations. We acknowledge that the sub-sample sizes for offshoring projects (24) and backshoring projects (38) during the pandemic are somewhat small, but as noted by Norman (2010), the use of parametric statistical methods (such as t-tests and factor analysis) does not impose a restriction on sample size. Our sub-sample sizes were sufficiently large to lead to many significant t-test results as well as provide strong factor loadings and Cronbach alphas in the factor analyses. Metrics suggested by MacCallum et al. (1999) and de Winter et al. (2009) also indicate that the factor analyses should provide adequate representations of the underlying constructs. The limited number of offshoring and backshoring projects during the pandemic indicates that pandemic-induced effects have had a strong inhibitive influence on manufacturing relocations. Still, the main contribution of this research is the longitudinal approach taken to capture and analyze offshoring and backshoring in a structured way. In this research, we did not consider nearshoring, which is an option where manufacturing is brought closer to the original manufacturing site—but not all the way. Since nearshored manufacturing does not end up at the original plant, such relocations were not captured in this study. While a plant can initiate offshoring and backshoring projects, decision-makers on nearshoring options tend to reside at company headquarters and, thus, such decisions are made at the company level.

5.4 Further research

We welcome longitudinal studies in other high-cost regions to allow for triangulation of these results. In-depth case studies can add nuance to decision-making in disturbing times, such as during a pandemic. In particular, the trade-offs between labor cost on the one hand and lead time, risk, and flexibility on the other for offshoring decisions, as well as between quality and lead-time, risk, logistics cost, and market proximity for backshoring deserves further attention, for example through case research. While we offered plausible explanations such as time constraints for finding new suppliers or contract manufacturers that could offer low labor costs for offshoring or quality products for backshoring, we acknowledge that there may be other reasons for these trade-offs or tensions, which can be researched in the future. The challenges associated with critical trade-offs and tensions span multiple levels—from the individual and functional/business levels to the broader supply chain network affecting multiple units. Future research should investigate how companies balance these factors across different units of analysis in an evolving risk environment. How learnings from research on offshoring and backshoring to date can inform future decision-makers in industry can be captured through Delphi studies (cf. e.g. Gebhardt et al., 2022). Such endeavors can extend our understanding of manufacturing relocations from the past and present into the future. Another avenue of research is to investigate how firms respond to global—local tensions and to tensions between free trade and protectionism. We also acknowledge that reshoring can be perceived as one possibility for making supply chains and manufacturing networks more resilient. We welcome research that can combine manufacturing relocations and other approaches to becoming more resilient in an integrated study. Such studies should also include sustainability considerations, for example on how firms can align environmental objectives with managing the trade-offs between global and local supply chains and maintain resilience. Exploring these aspects further could open valuable avenues for deeper investigations.