To better understand the role power distance plays when embedding corporate sustainability in a large finance organisation, which impacts hundreds of thousands of customers.

Interpretive, qualitative, exploratory study where 24 participants from all hierarchical levels within one large Australian finance organisation (directors, managers, frontline staff) were interviewed (semi-structured). These interview transcripts were triangulated with the organisation's corporate reports and field notes.

While directors espoused corporate sustainability values where anyone could speak up in their ‘nice’ organisation, subordinates reported a high power distance; this behaviour stopped subordinates asking corporate sustainability questions. Subsequently, the organisation was media-shamed for engaging in greenwashing.

This study's limitations highlight opportunities for further theoretical and practical contributions. As a single-case design, findings cannot be generalised; however, their depth offers fertile ground for comparative multi-case research across finance and other purported low power-distance contexts. Future studies could examine how normative niceness interacts with structural power in organisations that espouse egalitarian cultures. Conceptually, the study contributes by theorising niceness as a moralised form of normative control that sustains silence and protects dominant financial logic, offering a transferable lens for understanding institutional barriers that inhibit the embedding of corporate sustainability.

Practically, this study illuminates the organisational levers directors and senior leaders can adjust to dismantle high power-distance norms that undermine corporate sustainability. By showing how normative niceness suppresses speaking up, the findings emphasise the need for governance mechanisms that surface undiscussables, including independent sustainability oversight and structured contrarian briefings. The study also contributes practical guidance for redesigning incentive systems to reward authentic upward challenge rather than compliance. Additionally, it highlights the value of establishing cross-level forums that normalise voice, enabling psychologically safe dialogue. Collectively, these insights provide actionable pathways for embedding sustainability as a lived organisational practice.

This study highlights significant social implications arising from high power distance and normative niceness within large finance organisations. When staff self-censor and uncomfortable issues remain undiscussable, risks tied to customers' financial wellbeing go unaddressed, contributing to erosion of public trust in the financial sector. Silencing subordinate voices also perpetuates inequity, as those closest to customers – often frontline staff – are least empowered to influence decisions that affect community outcomes. The persistent dominance of financial logic over corporate sustainability logic ultimately undermines societal efforts to address climate risk, ethical governance and long-term economic resilience, affecting millions who depend on responsible finance.

Australia prides itself as being egalitarian; however, this research found high power distance behaviours. Normative niceness played a role in masking high power distance, which enabled financial logic. As a consequence, corporate sustainability was stymied and subordinates were silenced from raising legitimate corporate sustainability suggestions and concerns.

Introduction

Large finance organisations in Australia consistently espouse corporate sustainability virtues in their corporate reports and websites. However, the industry has come under significant scrutiny in parliamentary inquiries, media investigations and a Royal commission into misconduct in the banking, superannuation and financial services industry (Commission) (ASIC, 2025a, 2025b; Campbell, 1981; Ferguson, 2017; Hayne et al., 2019). Politically, corporate sustainability has been strongly contested in Australia, where an emission trading scheme was intensely debated and eventually passed through parliament, only to be later repealed (Wright and Nyberg, 2017). Australia is perceived as a corporate sustainability laggard compared to the rest of the developed world (CDP, 2019). Commentators state: “Australia is behind many of its international peers. It is imperative that we catch up, building on international best practices and experience” (Australian Sustainable Finance Institute and KPMG, 2022, p. 5). It has been advised that the first action Australia needs to take is addressing leadership (directors) and organisational structures because “Australia's progress with embedding sustainability into leadership practice is slow” (Australian Sustainable Finance Institute and KPMG, 2022, p. 5).

In this study, corporate sustainability refers to the integrated pursuit of economic, social and environmental value over the long term, whereas environmental social governance (ESG) is treated as a narrower reporting and product-based instantiation of sustainability that is susceptible to symbolic compliance (Pazienza et al., 2022; Sisaye, 2011). The term financial logic is used to denote the dominant profit-maximising rationale shaping decision-making and power relations within the organisation (Yan et al., 2019).

Positioned within leadership and organisational development scholarship, this study examines how leadership practices, cultural assumptions and power relations interact to enable or obstruct purposeful organisational change (Fenwick, 2007). Drawing on Argyris' theory of organisational learning and defensive routines, the findings reveal a pattern of arrested development: double-loop learning is largely absent, as taken-for-granted assumptions aligned with financial logic remain unexamined, while silence, self-censorship and avoidance protect directors from disconfirming feedback (Argyris, 2010; Yan et al., 2019). Normative niceness functions as a leadership-reinforced defensive routine, stabilises the status quo and attempts to maintain the appearance of relational harmony at the expense of inquiry, experimentation and adaptive change. From a Scheinian perspective, the study highlights a misalignment across organisational subcultures, where directors' espoused values of egalitarianism and sustainability are decoupled from the basic underlying assumptions shaping everyday leadership behaviour and decision making (Schein and Schein, 2017). These assumptions are reinforced through leadership-endorsed power structures, embedded in governance processes, remuneration arrangements and human resources (HR)-mediated norms of niceness, which collectively constrain voice and organisational learning. In organisational development terms, the findings identify concrete intervention points beyond individual managerial action, including leadership-level diagnosis of defensive routines, redesign of participation and voice infrastructures, and deliberate disruption of culturally embedded power dynamics. Collectively, the study demonstrates why leadership-led culture change initiatives that fail to surface power distance and defensive norms are likely to reproduce symbolic compliance, rather than enable sustained organisational development.

Building on this leadership and organisational development framing, the study approaches problematic corporate sustainability practices through an institutional cultural lens, alongside power distance, in recognition that leadership, particularly at board and director level, has been identified as a persistent constraint in embedding sustainability within the Australian finance sector (Australian Sustainable Finance Institute and KPMG, 2022). This research adopts an interpretive, exploratory single-organisation case study design, examining the lived experiences of staff across hierarchical levels within one large Australian finance organisation. By focusing on a single case, the study offers close examination of power distance, institutional logics and subcultural dynamics as they are enacted in everyday organisational life.

While prior research has examined the effects of power distance in finance primarily through quantitative studies of equity-based financing, corporate debt, and innovation in contexts such as China, Indonesia, Iran and Pakistan, there remains limited empirical insight into how power distance is enacted and sustained through leadership practices in Australian finance organisations seeking to embed corporate sustainability (Silvia et al., 2024; Wang et al., 2021). Addressing this gap, the study asks: What role does power distance play when embedding corporate sustainability in a large Australian finance organisation? The objective is to examine how leadership behaviour, institutional logics, and power relations shape organisational learning and development outcomes, while responding to calls for a more critical examination of ethical blind spots, resistance to change and symbolic compliance in corporate sustainability practice (Guan and Frenkel, 2025; Peng and Zhang, 2022). In doing so, the study contributes leadership-relevant insights for finance directors and organisational development practitioners seeking to move beyond espoused commitment towards the substantive development of sustainable organisational practices.

Theoretical framework

Given the research question alludes to identifying institutional logics, which involves delineating between espoused corporate sustainability values and taken-for-granted norms where there is ceremonial conformity or symbolic compliance, this study is situated in institutional theory (Joseph et al., 2019; Powell and DiMaggio, 2012; Zhang et al., 2023). Alongside this, power distance will be explored as well as corporate sustainability logic (Hofstede, 2001; Schreiber et al., 2025). There have been problematic corporate sustainability issues within the Australian finance culture since 1893 (Hickson and Turner, 2002). In the Commission, “dishonesty and greed” were words used to describe the industry's culture, which impacts millions of finance customers and 541,200 staff (Australian Bureau of Statistics, 2024a; Hayne, 2018, p. 73). Fines of $1.3 billion and $700 million have been issued to Australian finance organisations for breaches of anti-money laundering practices; other fines for greenwashing, the environmental element of corporate sustainability, have also been issued (Austrac, 2019b; Australian Securities and Investment Commission, 2023, 2025). While greenwashing has featured in journals for over three decades across many countries, recent research has called for greater scrutiny regarding information asymmetry in corporate reporting and online communication (Athanasiou, 1996; He et al., 2025; Oppong-Tawiah and Webster, 2023). There has also been a call for the voice of staff to be heard when embedding corporate sustainability (de Souza Barbosa et al., 2023). Therefore, this research heard directly from staff, and their voice was triangulated with espoused words in corporate reports.

Decarbonising economies is critical to addressing climate change, one of the grandest challenges facing humanity (Lazarus, 2008; Wright and Nyberg, 2017). Addressing corporate sustainability challenges is complex – business and government cannot respond to this issue without finance. Yet, how Australian finance directors embed corporate sustainability, so their organisation can rise to the grand challenge, remains a black box. It is not known if directors couple or decouple their espoused values from their lived reality, but there are some indicators there may be a disconnect. When asked about corporate sustainability considerations in the process of making a decision finance directors have said, “We're not mining” (Burns et al., 2019, p. 1171; Jastram and Foersterling, 2024).

Power distance

The broad Australian community and finance directors alike pride themselves on upholding a low power distance, egalitarian culture (Backhouse and Wickham, 2020; Commonwealth Bank, 2024). Hofstede's cultural dimensions were originally developed to explain national culture, not different organisational cultures in a nation (Hofstede, 2001). However, subsequent research has extended these dimensions to organisational contexts, arguing that national cultural values often influence organisational norms and managerial practices (Ashkanasy, 2007; Schein and Schein, 2017). In the Australian context, Hofstede's work positions the country as a low power distance society, reflecting egalitarian ideals. Yet, empirical studies suggest that hierarchical norms persist within certain industries, including finance, where governance structures and finance logic can foster high power distance behaviours (Ashkanasy, 2007; Backhouse and Wickham, 2020). Like Australia, New Zealand and Nordic states position themselves as low power distance, egalitarian countries (Malmi et al., 2022; Zheng and Shen, 2025). And like Australia, these countries business leaders have been reported to be talking the corporate sustainability talk, rather than walking the walk (Compact, 2023; Sustainable Business Council and Kantar, 2025). This indicates national culture does not uniformly translate into organisational practice; rather, organisational subcultures may diverge from societal norms, creating environments where unequal power distribution is accepted. Exploring this divergence is critical because low power distance can shape communication, decision making and psychological safety – factors that influence the embedding of corporate sustainability (Tata and Prasad, 2015; Yan et al., 2021). Therefore, this study uses Hofstede's power distance dimension as a conceptual lens – acknowledging its national origins and situating its application within institutional theory.

High power distance is the element of culture that tolerates or accepts the unequal distribution of power. Individuals within an organisation accept unequal distribution of power between a leader and subordinates in high power distance cultures (Tata and Prasad, 2015). In low power distance cultures, egalitarianism is promoted to minimise inequality; here, the broader stakeholder voice is listened to as well as shareholders (Freeman et al., 2021). Other attributes of low power distance cultures include a focus on the long term, increased diversity, trust and the ability for existing assumptions to be questioned (Bao et al., 2021; Tata and Prasad, 2015). Leaders in high power distance cultures offer minimal scope for subordinates to question them (Yan et al., 2021). These leaders prioritise self-interest and resource control, which includes the desire for profit maximisation. Within the acceptance of unequal distribution of power is the belief that everyone needs to adhere to their rightful place in the hierarchy, which means obeying their superiors as a moral obligation (Rai and Fiske, 2011).

There has been minimal research into how power distance manifests in large finance organisations. Morgan (1988) posited that the finance industry tends to have more power because financial allocation control can shape society. The role of finance in society is for the allocation of resources and maximisation of efficiency, to bring about the common good (MacIntyre, 2007). In complex and globalised market environments, decision-making grounded narrowly in financial metrics often results in outcomes misaligned with consumer expectations.

Wright and Nyberg (2017) and Ashkanasy's (2007) study of Australian finance culture highlighted a dominant profit-oriented, capitalistic ideology. While these assumptions resonate with features commonly associated with high power distance cultures, there remains a notable paucity of research examining how power distance operates within Australian financial organisations (Dempere et al., 2024).

In large organisations, there are three generic subcultures: directors, middle managers (managers) and frontline staff (Schein and Schein, 2017). Directors are the guardians of the culture, entrusted with upholding the fiduciary duty of the organisation for its beneficiaries (Australian Institute of Company Directors, 2020). They are also responsible for managing the organisation's subcultures, which includes navigating conflict and misalignment between subcultures (Lok et al., 2005). Traditionally, directors have focused on managing financial success and survival, viewing people as resources that operationalise the organisation (Schein and Schein, 2017). In this purview, subordinates will often tell directors what they want to hear, rather than risk presenting a challenge (De Clercq et al., 2021). Managers, as a subculture, need to develop elegant processes to solve problems through the development of products and services. This work is often closely aligned to the area of expertise they studied (e.g. accountancy, law, communications) and is part of their identity (Schein and Schein, 2017). Frontline staff do the work set for them by managers and directors – they get the job done. In their role as the human face of the organisation, frontline staff need to negotiate the practical drift between formal policy processes and achieving efficiency (Snook, 2000).

Within the literature, power distance relating to corporate sustainability adoption has been explored from a marketing-communication and religious perspective, but there is minimal literature on how power distance (low or high) impacts embedding corporate sustainability within a finance organisation (Vizcaíno et al., 2021; Yan et al., 2021). There are now calls from investors, media and regulators for greater transparency with reporting, given the increase in greenwashing where finance organisations fail to walk the corporate sustainability talk (Austrac, 2019a; Australian Securities and Investment Commission, 2023; Ross, 2023). In effect, these calls for increased transparency are a call for a deeper review of the lived reality, compared to what is merely espoused (Argyris, 2010). Taken-for-granted, often unconscious, assumptions enacted in everyday organisational life offer a more authentic representation of organisational culture (Hong et al., 2021); however, examining these deeper assumptions requires significantly greater time and effort than analysing symbolic portrayals in corporate reports (Ahrens and Chapman, 2006; Su and Hahn, 2025).

Corporate sustainability

There is now more uniformity in reporting corporate sustainability from a quantitative perspective with the introduction of new international sustainability standards for accounting; the investment market also expects more meaningful corporate sustainability disclosure (International Sustainability Standards Board, 2023). Corporate sustainability differs from traditional one-dimensional financial logic, which focuses on short-term profit maximisation and externalising costs (Friedman, 1970). There are increasing calls for reporting to better integrate the environmental with the social and economic disclosures because stand-alone environmental or economic reports may not be decision-useful for stakeholders (Duan et al., 2025). Attributes of financial logic include materialism, self-interest and utilitarianism (Yan et al., 2019). Corporate sustainability is grounded in the long-term common good, which is also known to enhance corporate resilience; therefore, morally corrosive financial products are oppositional to corporate sustainability due to their short-term self-interest (Florez-Jimenez et al., 2025; Schinckus, 2015).

A number of financial products featured in the Commission did not meet the community's corporate sustainability or fiduciary standards expected in Australia (Hayne et al., 2019). These products included insurance policies where legitimate claims could not be made, issuing of loans to people who could not afford them, and “junk” funeral insurance, which does not align with the social element of corporate sustainability (Hayne et al., 2019). The Commission detailed subordinate voices being ignored and silenced, which is fertile ground for misconduct. This misconduct led to untrustworthy corporate reporting that harmed customers' financial security (Herold et al., 2020). Understanding institutional culture in this study is important because corporate sustainability is culturally constructed within the organisational learning environment (Fenwick, 2007; Kenter et al., 2019). One Australian study found finance directors who held corporate sustainability logics set the tone for their organisation engaging in more responsible action and were better positioned for changes in the market (Burns et al., 2019).

A number of frameworks have been developed to assist organisations and stakeholders in identifying where they are positioned on the corporate sustainability spectrum from weak to strong (Linnenluecke, 2022; Meuer et al., 2020). One recognised corporate sustainability framework is the Dyllick and Muff (2016) Business Sustainable Typology (BST). Within the BST framework, organisations at the lowest level of the spectrum do not have corporate sustainability training or robust policies, nor do they see social and environmental considerations as valid. Rather, there is an assumption of profit maximisation, where costs are externalised. These technocratic organisations are classified as Business-as-Usual (BAU) 0 and align with finance logic. At the other end of the spectrum are organisations that integrate corporate sustainability logic into their decision-making because there is an assumption that corporate sustainability creates value for the common good, is integral to their success strategy, and potentially a source of competitive advantage (Joseph et al., 2019). In these Business Sustainability 3.0 level (highest end of the spectrum) organisations customers, staff and stakeholders prioritise corporate sustainability, and are committed to addressing financial insecurity, sovereign debt overload, and corruption (Dyllick and Muff, 2016). It is not known where large Australian finance organisations sit on this spectrum.

In sum, there is a gap in the literature on how low or high power distance impacts, or does not impact, corporate sustainability being embedded into a large Australian finance organisation. This research is different in that it aims to contribute knowledge by exploring the lived reality of a large finance organisation attempting to embed corporate sustainability through an institutional cultural lens, where the voices of all levels of hierarchy are heard.

Methodology

An interpretive single case study methodology was the best fit for the complexity of the phenomenological research (Yin, 2017). A purposive sampling approach was used to select one large Australian finance organisation as the single case for this study. All 24 participants were employees of this organisation, drawn from three generic organisational subcultures: directors, managers and frontline staff. Hearing the voice of participants from each of these hierarchical levels enabled examination of power distance and organisational learning dynamics within the same institutional and cultural context (see Appendix 1 for a list of participant characteristics) (Campbell et al., 2020). When identifying potential organisations there were several selection criteria that needed to be met. First, the organisation needed to be Australian and classified as “large” according to the Australian Bureau of Statistics, reflecting the study's aim to explore corporate sustainability logic that can potentially impact hundreds of thousands of finance customers and more than 1,000 staff (Australian Bureau of Statistics, 2024b). Second, the organisation was required to be well established and to possess a strong external reputation within the broader community, such that it was subject to wide-ranging stakeholder expectations. Third, the organisation needed to have publicly available corporate reporting commitments to facilitate archival data collection. Finally, access was required to interview participants across all hierarchical levels, including directors, to ensure leadership voices could be directly captured, and contrasted with those of managers and frontline staff (Yin, 2017). Data collection was gathered from semi-structured interviews, field notes and archival documents (Kvale, 2007; Phillippi and Lauderdale, 2018). The interview questions were conducted between August 2019 to May 2020 by the researcher. Questions included basic demographic questions such as subculture, gender and length of time in the organisation (see Appendix 2). Participants were then asked general dialogue open-ended questions on their day-to-day lived experience to avoid defaulting to a cultural script (Smith, 1987). Twelve women and 12 men participated, each interview lasting approximately 64 minutes. Transcripts from these interviews produced 243,646 words.

In terms of field notes, participants “overall appearance and demeanour”, including nonverbal cues, were noted during interviews, such as facial gestures, voice intonation and body language (Phillippi and Lauderdale, 2018, p. 385). These notes were designed to “add back” to transcriptions (Gupta, 2024; Sandelowski, 1994). Understanding field notes are best developed immediately after interviewing, time was allocated to write additional notes post-interview. These notes captured building appearance (e.g. size, symbols, technology, entrance-welcoming, accessibility), dress of the participants (e.g. conservative corporate, modern, uniform, branding) and meeting rooms (e.g. images on walls, colours, size, and location) (Phillippi and Lauderdale, 2018). The author also completed a prompt sheet to facilitate discerning espoused values from assumptions, to ascertain where the organisation was positioned on the corporate sustainability spectrum (see Appendix 3) (Argyris, 2010; Schein and Schein, 2017). There were 216 pages of field notes, which supported reflexive analysis during the data triangulation process (Cunliffe, 2003). For instance, formal meeting room imagery predominantly depicted male customers, despite the organisation's customer base being primarily female.

The researcher also utilised the organisation's public web archives to find corporate reports and videos where directors communicated with stakeholders as part of the archival documents data collection (Prelinger, 2009). These documents were used to confirm the espoused values of the organisation. This data provided artefact information such as the formal organisational structure, stakeholders, product descriptions (e.g. ESG product), figures including funds under management, as well as customer and staff size. These documents were important for the triangulation of the data, providing corroborating or contradictory evidence with the transcripts and field notes (Yin, 2017).

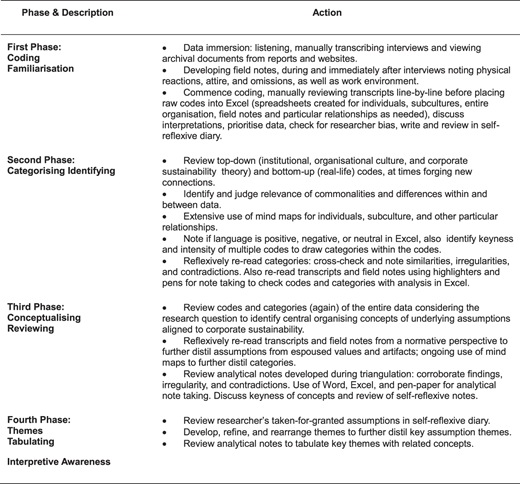

Four phases of coding were used in the thematic content analysis: initial coding, categorising, conceptualising and finally, themes, see Figure 1 (Braun and Clarke, 2006; Cunliffe, 2003; Saldaña, 2015). In the manual coding process, there were approximately 100 codes from each interview. The rationale for the manual coding was to ensure latent themes were not missed, and the delineation between espoused values and the lived reality was identified (Argyris, 2010; Sandberg, 2005). Throughout the thematic process, Excel spreadsheets were used extensively, as well as mind mapping and pen and paper note-taking (Braun et al., 2014; Buzan and Griffiths, 2013; Saldaña, 2015). There was ongoing reflexivity during the four phases, which resulted in recursive action; therefore, some initial concepts and themes were later revised.

Regarding researcher positionality, a key motivation for this qualitative study stemmed from the author's professional experience in a large finance organisation, where the day-to-day lived reality appeared incongruent with the narratives presented in formal corporate reports.

Findings

The requisite variety of data analysed offered insight into the research question of what impact power distance plays when embedding corporate sustainability. As will be discussed, there was strong evidence from the transcripts and field notes, to support that there was high power distance within the organisation, where the corporate sustainability positioning was BAU 0 (lowest level). The three key themes were: hierarchy, processes and niceness and customer centricity. The lived reality of corporate sustainability was decoupled from the organisation's overarching espoused value: “customers are at the centre of all we do” and the four organisational values of: “daring, brave, collaborative and skilled”.

Business-as-usual

The BAU 0 norm manifested in profit maximisation being the overarching assumption of the organisation. There was no evidence of policies aligned with science-based corporate sustainability targets, nor robust strategies to decarbonise (other than recycling paper), or the provision of fit-for-purpose ESG products. One field note following an interview with an investment manager (MGR9) observed: “The prevailing assumption is that if investment-finance is generating revenue, it should be shielded from corporate sustainability initiatives. Profit, it seems, can be used to justify almost anything”. Furthermore, there was no specific budget allocated for corporate sustainability development. While ESG was referenced as part of the organisation's approach to being a good corporate citizenship, this stewardship only extended to the economic element of ESG; social and environmental elements were not disclosed. At the time of interviews, there were no corporate sustainability or ESG experts in-house; the organisation outsourced their “green-sustainable” ESG product. While this product was widely adopted – attracting investments from hundreds of thousands of customers based on its purported ESG alignment – subsequent assessment identified substantial holdings in fossil-fuel-dependent energy producers and carbon-intensive construction firms. This archival analysis corroborated with field notes that continually referred to environmental considerations not being a day-to-day reality. Post interviewing the organisation, the media reported that the product performed poorly relative to peer ESG investments, to the extent that the regulator called for the organisation to formally disclose the suboptimal performance to the market.

Three key themes

Three key themes were present across all subcultures; however, the day-to-day sensemaking of these concepts differed.

Hierarchy shaped participants' experiences of high power distance within the organisation. Field notes indicated that participants frequently described their environment as one filled with “nice people in a nice place”. At the same time, directors consistently espoused egalitarian values, emphasising that anyone could “speak up” within what they characterised as a flat organisational structure (DIR2, DIR3, DIR4, DIR6). The CEO stated in the interview, “I don't think in levels that's ridiculous” (DIR6); yet, later referred to “junior female staff” and “senior execs” (DIR6). Similarly, the chair described their role as that of “the conductor” (DIR1), while a female director (DIR3) spoke openly about experiencing “imposter syndrome” in relation to her position on the board; therefore, she would not ask the chief investment officer (CIO) questions. For DIR3, an acute awareness of hierarchy was ever-present; she emphasised that “staff at all levels need to abide by the rules”, that is, know their place in the hierarchy. In contrast to directors' assertions that anyone could speak up within a supposedly low power distance environment, subordinates did not share this perception. They viewed hierarchy as firmly embedded in the organisation and did not believe that having a voice was genuinely available to all. Managers spoke of a “command and control” (MGR4, MGR7, MGR9) climate, and frontline staff were aware of their low hierarchical positioning, FRT6 saying, “You are the tiniest cog in the machine. Communication is one-way downhill”.

The impact of high power distance had a significant effect on frontline staff. There was high turnover in this subculture, with participants saying they “hated” (FRT4) the “toxic” (FRT4) environment. One frontline staff member (FRT1) who had been with the organisation for 11 years shared they had observed a colleague attempting to speak up about the workplace climate at a higher level: however, “It wasn't very good. The person speaking up left” (FRT1). This reality was quite different to a director (DIR4) who said:

I’ve certainly asked people if they can speak up and if there are any aspects of the organisation they don’t like regarding their work, but it’s all very positive around culture. People indicate [in staff surveys] they are comfortable to raise issues with management. They don’t feel that there will be adverse repercussions for them.

Across the business areas, investment held the most power. This power manifested in easy access to the board and remuneration flexibility, MGR9 saying: “We have highly qualified people [in investment] at the smarter end of the intellectual scale. We work closely with the CEO and board”. Senior investment managers did not believe they should be questioned by others (MGR3, MGR9) because they were the “engine room” of the organisation. While investment managers assumed a higher rank and order, they appeared to be oblivious to their assumptions perpetuating high power distance. Field notes referred to the overconfidence of investment managers expecting others to “get out of their way” because what they do holds the primary voice that needs to be listened to. These notes align with an investment manager (MGR3) expressing surprise that staff withhold their insights, saying: “Junior people will not speak out … No one had ever said it”.

Investment managers stated they could speak up, other managers did not believe they held that power, particularly if they were in human-centred areas such as marketing, customer development and customer experience. Reprisal was a concern; therefore, most chose to self-censor even when they had extensive knowledge and experience that could assist the organisation in fulfilling its espoused corporate sustainability values. Field notes suggested that this need for self-censorship had tangible physical and psychological effects on frontline staff. In one entry, I noted concern for employees at the lowest organisational level who appeared overcommitted and fatigued, driven by a persistent fear of making mistakes or speaking up at the wrong moment. As one frontline staff member expressed, “I'm just dead scared I'm going to do it wrong”. Similarly, a manager (B11) with a doctorate and substantial expertise in their human-centred field reported that they would not raise issues with those in power: “I would say hello, but I wouldn't speak up on an issue—I don't think I have the credibility to”. Field notes also highlighted a pattern of participants being “nice to everyone where everyone agreed; ” however, this collective niceness carried hidden organisational costs, including delays in decision-making and slowed processes.

Processes emerged as another central theme. Directors expressed a strong pride in what they described as their “robust processes” (DIR4), in particular their “robust governance processes” (DIR1, DIR3). As DIR1 emphasised, “My key priority is governance of the organisation”. Directors attributed their perceived efficiency and effectiveness to the “simplicity” (DIR1, DIR4, DIR6) of the organisational structure, noting that “all groups and divisions get along” (DIR3). They believed this process proficiency underpinned their identity as a “terribly successful” organisation (DIR1) that consistently delivered profit for customers, with DIR4 affirming, “We've got really good governance processes”.

Managers, however, perceived organisational processes as a form of “command and control” (MGR7). And unlike directors, subordinates did not perceive the organisation as simple, rather “complex” (MGR7, MGR4, MGR5, MGR7, MGR8, FRT1, FRT4, FRT5, MGR10), where there are constant misunderstandings and conflict between business areas and other stakeholders, MGR6 saying, “There's tension between some areas. For example, our member experience division, and our advice division, there's tensions because they have a different view about execution”. Similarly, MGR3 said, “Deeper work needs to be done to address silos. There's also a poor capability aspect in there, but it's not a poor reflection on them, it reflects the system”. Indeed, subordinates did not view the processes are robust, MGR8 saying, “It happens so often—my team complaining about a process that is inefficient”. Aligned to this were many field notes where subordinates referred to people being change resistant (MGR1, MGR2, MGR7, MGR9, C20, C23), all the while the CEO (DIR6) spoke of their “progressive” organisation. Field notes also highlighted concerns about outdated organisational processes and the heavy emphasis placed on compliance. Subordinates expressed scepticism that meaningful or lasting change would occur without formal legislative requirements – their assumptions stood in stark contrast to the CEO's espoused progressive sustainable change agenda.

“Frustration” (MGR7, MGR2, MGR3, MGR6, MGR7, MGR8, MGR10) was a perpetual manager emotion because people did not take “accountability” (MGR7, MGR2, MGR7, MGR10) for their actions and inactions in the nice culture. One frontline staff (FTR5) expressed the normalisation-rationalisation of this accountability lack as “No fault of anybody's that we get overloaded and can't meet target”. A number of managers (MGR7, MGR3, MGR5, MGR7, MGR9, MGR10, MGR10) spoke of attempting to put corporate sustainability processes in place that aligned with community expectations, such as new corporate sustainability product offerings, improved technology and upskilling staff. However, when the subordinates attempted to embed these corporate sustainability initiatives, they were informed that this work did not align with their one-up manager's key performance indicators (KPIs). Therefore, no budget or resources were allocated because there were no specific targets or monitoring of corporate sustainability.

Managers, other than those in investment, avoided making decisions, MGR8 saying, “When we need to make decisions, we send the delegation up, a lot of papers go up to make a decision”. This decision-avoidance norm was driven by fear and absent of cultural dynamism and progressiveness. MGR7 shared the system was, “hierarchical, slow, and stymie[d] creativity”. Another manager (MGR3) alluded to the high power distance norm contributed to, “Deep thinking not being done”. Frontline staff stated under-resourcing was an issue. This resource lack was a factor in the 1- to 2-hour phone customer wait times, FRT4 saying, “We had a gentleman come in the other day and say, “You are longer than waiting for Centrelink [government welfare program] now”. We don't want to hear that. Please help the call centre to get more staff”. Directors justified their distribution of resources as the customer being unwilling to pay for operational costs – this assumption is aligned with financial logic where profit is maximised, and costs are externalised. Most frontline staff accepted this lack as a norm and did not see it as being at odds with their nice customer-centric assumptions. However, some frontline staff were aware the remuneration (REM) process was not aligned to their organisation's values, FRT3 saying, “With REM some parts aren't metricated in the best way, it encourages the wrong behavior”. There was also evidence of an authority-centric climate in that subordinates expressed their role was to be compliant, FRT2 stating, “Dotting my i's, crossing my t's and not going outside the lines” was important. This implies an inability to question; therefore, it was unsurprising FRT3 said they, “Never get on anyone's offside; I avoid it” so that they can appear to be agreeable with everyone.

Niceness and customer-centricity emerged as the final theme. Without prompting, one manager (MGR2) remarked, “Everyone's very pleasant and very nice and very accommodating … It is a really nice culture”. The organisation's emphasis on being both “nice” and customer-centric was closely tied to claims of delivering strong customer returns, effectively integrating financial logic into its espoused values, the chair (DIR1) stating, “Customer returns are the easiest way to measure success”. Across all subcultures, participants reiterated that customers were positioned at the centre of organisational activity, a message they attributed directly to leadership – for example, DIR4 affirmed, “Customers are at the centre of all we do; that's genuine”. Many participants also spoke of wanting to leave a “nice legacy” (DIR5), reinforcing how deeply niceness was woven into the organisation's identity. Early field notes from director interviews suggested that this emphasis on niceness functioned as a euphemism – a facade. Later interviews with subordinates made clear that niceness often concealed multiple undiscussable issues. Nonetheless, participants continued to view their nice culture as central to delivering high-quality customer service, which they perceived as morally superior to the practices of Australia's “big four” banks, with several stating proudly, “We're not like the banks” (DIR5).

Despite the organisation's stated commitment to delivering customer value, several observed practices suggested a disconnect between its espoused statements and staff's lived experience. As previously noted, customers routinely waited one- to two-hours for service, signalling operational inconsistencies that undermined the organisation's value proposition in practice. Field notes also captured staff concerns regarding the CEO (DIR6), whom many described as personable, charismatic and outwardly values driven, yet frequently evasive when responding to questions during staff town halls. As a researcher, I likewise observed occasions in which the CEO did not substantively engage with sustainability-related inquiries, further reinforcing perceptions of misalignment between values-based rhetoric and day-to-day leadership behaviour.

When frontline participants were asked to describe what fiduciary duty (aligns with the social and economic dimensions of corporate sustainability) meant in the context of their roles, most expressed uncertainty. Responses included, “What?” (MGR3, FRT1, FRT5, FRT8) and “That sounds as though it's above my pay grade” (FRT1). This lack of clarity was notable given that many of these employees had extensive professional experience, including prior roles such as bank managers with 10–20 years of tenure. The findings suggest that key governance concepts – and, by extension, understanding of sustainability-related responsibilities – were not consistently embedded across hierarchical levels.

The organisation's emphasis on niceness also created an accountability deficit. Several managers referred to a “dark side to nice” (MGR6, MGR10). As MGR10 explained, the dark side manifested when “people don't face into challenging conversations because they're too worried about others … People publicly agree and privately disagree. It is actually toxic”. Frontline participants echoed these concerns. FRT9 noted that staff continued to “learn from others on the old [nice] way of doing things”, which they believed hindered sustainable change. As a result, FRT9 argued, “We need to let go of a certain percentage of people and hire very different people”.

Normative niceness meant that challenging conversations about corporate sustainability or behaviour change did not feel safe, a concern reflected by FRT8: “I don't know if everyone would speak up”. In practice, staff remained silent on matters such as the organisation's high reliance on fossil-fuel investments and the poor performance of ESG products. As FRT7 explained, “If you keep speaking up and nothing happens, you stop speaking up—initiative wasn't rewarded”. Field notes similarly documented that the absence of challenging dialogue contributed to growing unmanageability across teams.

Raising uncomfortable, undiscussable issues – whether about fiduciary duty, staff underperformance, product value or potential greenwashing – was not perceived as nice. Directors and HR referred to vetting candidates to ensure cultural fit, with DIR3 stating, “A lot of work is put into recruitment to ensure [a nice] culture. It's really important we vet attitudes”. Directors also asserted their ability to “fire” (DIR6) individuals who did not align with the culture. In addition to silencing or removing staff, “coaching” (MGR1, MGR9) was also used to shut down uncomfortable conversations; that is, managers who expressed themselves too directly or in ways deemed “not nice” were sent to coaching. In sum, the interplay of hierarchy, process rigidity and normative niceness created conditions in which financial logic flourished, while discussions of corporate sustainability were kept out of sight.

Discussion

Findings from this study posit that there is a relationship between high power distance and its impact on corporate sustainability. In this Australian finance organisation, high power distance stymied corporate sustainability from being embedded, so it remained business-as-usual, where assumptions aligned with financial logic (Dyllick and Muff, 2016; Yan et al., 2019). This logic reduced, and at times opposed, corporate sustainability being enacted throughout the organisation. As detailed in the findings, directors lead the decoupling of espoused egalitarian corporate sustainability values from the lived reality. There was evidence of ceremonial conformity as niceness (role modelled by directors) acting as a social lubricant to mask decoupling words from actions (Arroyo et al., 2025; Snell, 1993). This manifested in symbolic compliance only with their ESG product (Li et al., 2024). In short, normative niceness was a buffer that shielded financial logic from critique while maintaining an appearance of ethical, egalitarian and relational harmony.

What is new about this Australian finance study, where the voices of all generic subcultures were heard, is the role high power distance played in circumventing corporate sustainability being a lived reality. These subcultural insights are important because they may be representative of 541,200 Australian finance staff who serve millions of customers daily (Australian Bureau of Statistics, 2024a). Beyond identifying high power distance as a barrier to corporate sustainability, this study makes a distinct conceptual contribution by theorising normative niceness as a mechanism through which silence is maintained. Unlike overt authoritarian control, niceness operated through moralised norms of agreeableness and relational harmony, rendering dissent inappropriate rather than explicitly forbidden. In doing so, it sustained a façade of corporate sustainability commitments while protecting financial logic from scrutiny. The voice of risk regarding corporate sustainability was silenced; subordinates had been trained to self-censor (with the exception of technocratic investment managers) (Power et al., 2013). Systematically, the subcultures served to reinforce a voice-silence (defensive) loop, which was enabled by normative niceness (Argyris, 1990). That is, directors set financially weighted incentives (not aligned to corporate sustainability), managers aligned their team structures to these incentives and frontline staff learned to self-censor from their managers, having grasped that speaking up results in informal excommunication. HR further reinforced this loop through normative control mechanisms, where speaking up was moralised as incivility, using tools such “coaching”. These systematised defensive behaviours served to concretise financial logic assumptions. In doing so, the study extends leadership and organisational development research by demonstrating how defensive routines and power distance constrain learning and development, despite espoused commitments to corporate sustainability (Fenwick, 2007; Su and Hahn, 2025).

There was no strong evidence of corporate sustainability organisational learning. High power distance did not create space for this learning or creativity (Argyris, 2002). Particular questions were known to be undiscussable; it was not safe to query the organisation's heavy investment in fossil-fuel-producing assets and other carbon-intensive businesses. Additionally, poor performance, be it about their ESG product or staff, was not safe to discuss; nor were there consequences from HR for poor productivity. Subordinates' description of top-down communication and command and control norms further confirmed the presence of high power distance (Tata and Prasad, 2015). Yet, directors appeared oblivious to the profit-oriented, technocratic ideology, high power distance norms they continued to perpetuate (Ashkanasy et al., 2017; Yan et al., 2019).

All participants defined organisational success as financial profit, not the realisation of the organisation's “progressive” espoused values of daring, brave, collaborative and skilled. The CIO could not be questioned, even by some members of the board. Within the organisation, the CIO appeared to have equal power, with the CEO, in terms of board access and influencing the board's decision-making (Ashkanasy, 2007). The extent of this positional power was also reflected in the remuneration arrangements of the CIO relative to the CEO, with corporate reports indicating financial parity between the two roles. The majority of the CIO's salary was additional to base pay and paid at the end of a 12-month cycle. A CIO having all elements of their salary paid in full at the end of 12 months is not indicative of an organisation aligned to long-term corporate sustainability logic. Further evidence of the board-endorsed CIO power was their ability to set remuneration packages for staff in their business area, which did not align with the rest of the organisation. The sensemaking investment managers took from the CIO's power was that they, too, should not be questioned.

The failures to enact corporate sustainability in this discussion respond to the call for increased critical analysis of corporate sustainability to identify ethical pitfalls (Guan and Frenkel, 2025). In sum, these findings highlighted that high power distance masked as niceness within this organisation acted as a structural barrier to embedding corporate sustainability, reinforcing financial logic and silencing critical voices.

Theoretical and managerial implications

This study advances theory by demonstrating, in this case, that high power distance in finance is not merely a national cultural artifact but a structural force within institutions that shaped corporate sustainability outcomes. Three theoretical contributions are offered, extending institutional theory into the domain of corporate sustainability and challenging assumptions of egalitarianism in Australian organisations. It is theorised niceness, as a moralised form of normative control, framed speaking up as incivility and command and control as virtue, thereby silencing subordinates and upholding the dominant financial logic. Niceness helped normalise the gap between espoused values and actual practice, allowing employees to view ceremonial and symbolic compliance as acceptable rather than prompting corrective moral action Arroyo et al. (2025), Li et al. (2024), Powell and DiMaggio (2012). In hiring for “fit”, enforcing corrective “coaching” and policing “not nice” interactions, the organisation constructed a culture of niceness that rendered contestable sustainability issues undiscussable and preserved BAU 0 (Dyllick and Muff, 2016; Yan et al., 2019). This contribution may be transferable to other contexts where there is evidence of high power distance, strong normative niceness that is associated with voice suppression and moralised decoupling between corporate sustainability talk and walk.

The second contribution is subcultural coupling of niceness and power distance enables a voice–silence loop. This is based on the mapping of how directors, managers, frontline staff and HR acted as differentiated carriers of niceness-enabled silence (Sulphey and Jasim, 2022). Directors' as sensegivers valorised “robust processes” that incorporated routing decisions upward. Managers' KPIs and risk avoidance also resulted in upward delegation. Similarly frontline staff's adoption of compliance and avoidance of “getting on anyone's offside” also meant decisions were not questioned. And HR's institutionalised niceness via selection and coaching sealed the niceness-enabled silence. Together with high power distance, these practices created a voice–silence loop that privileged deference to finance logic, which crowded out corporate sustainability logic (Power et al., 2013; Powell and DiMaggio, 2012).

The third contribution is the co-production of logic dominance: linking normative control to material anchors. In the case, “moral order”, controlled by normative niceness, was connected to structural-material anchors such as remuneration, decision-making rights, access to the board and KPI design. This behaviour signalled financial logic as legitimate, while corporate sustainability was not. Here, the CIO–CEO access and remuneration parity and investment's discretion to set local pay acted as material signals reinforcing the financial logic despite corporate sustainability espousals (Yan et al., 2019; Powell and DiMaggio, 2012). In sum, when niceness is reinforced through material structures, financial logic becomes the overriding force shaping resource allocation and organisational attention, despite organisational espousals suggesting otherwise.

For practitioners, addressing the nice mask of high power distance is not optional – it is a strategic imperative to address reputational and regulatory risk, and enhance corporate resilience (Florez-Jimenez et al., 2025). Three implications-interventions are proposed based on the case: (1) governance and oversight mechanisms, (2) incentive and performance systems and (3) voice and participation infrastructures.

Firstly, directors' governance reforms need to bring to the surface what niceness suppresses. More specifically, it means addressing how information is filtered to ensure they consistently receive decision-useful information. This action will challenge niceness norms all throughout the hierarchy, starting at the top. Practically, board-level logics will need to be challenged through an ethical corporate sustainability ombud that is independent of management, investment and has direct reporting access. Another governance reform is the establishment of contrarian briefings being developed for all major investment decisions. Authentic voice can also be strengthened by appointing frontline staff and managers as fixed-term, non-voting observers on board sub-committees, with participation rights (Song and Gu, 2024).

Secondly, redesign incentive systems to reward behaviour where subordinates speak up, that is, go beyond compliant behaviour. Explicit evaluative criterion aligned to this incentive could include raising material risks, identifying operational failures and opportunities, as well as cross-functional challenges. To reinforce this behaviour, a portion of senior management remuneration could be contingent on validating and addressing the upward challenges presented, developing material cross-functional collaboration on sustainability initiatives, as well as learnings from informal feedback.

The third implication is creating a psychologically safe space through participatory forums; therefore, normalising subordinates speaking up as a day-to-day low risk exercise for surfacing undiscussables. Practically, this could involve an external facilitator who is familiar with corporate sustainability and institutional issues establishing cross-subcultural learning forums that do not recognise hierarchy, where issues are logged, and there is no reprisal for raising undiscussables. Additionally, directors could implement mechanisms that foster psychological safety, such as cross-level decision forums and transparent corporate sustainability metrics, to dismantle hierarchical barriers and enable genuine sustainability integration of espoused values.

Limitations and future research

While this single-case study limits generalisability, its depth of subcultural findings to garner particularisations offers institutional insights (Weick, 1987). These findings may create opportunities for comparative research across multiple organisations and sectors. As such, normative niceness may be particularly prevalent in organisations and national contexts that emphasise egalitarianism and civility, suggesting its relevance beyond finance and beyond Australia. Nordic countries and New Zealand, like Australia, espouse egalitarian, participative ideals and sustainability leadership; yet execution barriers due to governance blind spots, and paradoxes remain – supporting the theorisation of niceness as a normative control that enables silence despite low power distance self-images (Sustainable Business Council and Kantar, 2025; UN Global Compact Denmark Finland Norway Sweden, 2023). Another indicator that this study's findings may have some transferability is based on Commission, regulator and media findings that subordinate voices are often not listened to by directors on corporate sustainability issues (ASIC, 2025a; Boyd, 2025; Hayne, 2018).

Directors' obliviousness to their high power distance, financial logic rendered their espoused corporate sustainability words void. Masked in niceness, this incongruent culture silenced subordinate voices, stopped meaningful collaboration and circumvented corporate sustainability action. Still, there is hope that directors will use their legitimate power to shift the culture to a low power distance culture, opening the door to psychological safety and increasing corporate sustainability as a lived reality to serve the community.

Appendix 1

Interview participants

| Subculture | Reference | Interview type | Gender | Years in the organisation |

|---|---|---|---|---|

| Director | DIR1 | Phone | Male | 7 |

| Director | DIR2 | Face-to-face | Female | 7 |

| Director | DIR3 | Phone | Female | 6 |

| Director | DIR4 | Phone | Male | 10 |

| Director | DIR5 | Face-to-face | Female | 1 |

| Director | DIR6 | Face-to-face | Male | 9 |

| Middle manager | MGR1 | Face-to-face | Female | 6 |

| Middle manager | MGR2 | Face-to-face | Female | 4 |

| Middle manager | MGR3 | Face-to-face | Male | 11 |

| Middle manager | MGR4 | Face-to-face | Male | 21 |

| Middle manager | MGR5 | Face-to-face | Female | 1 |

| Middle manager | MGR6 | Face-to-face | Female | 13 |

| Middle manager | MGR7 | Face-to-face | Male | 13 |

| Middle manager | MGR 8 | Face-to-face | Male | 4 |

| Middle manager | MGR 9 | Face-to-face | Male | 11 |

| Middle manager | MGR10 | Face-to-face | Female | 6 |

| Middle manager | MGR11 | Face-to-face | Male | 3 |

| Frontline staff | FRT1 | Face-to-face | Female | 11 |

| Frontline staff | FRT2 | Phone | Female | 1 |

| Frontline staff | FRT3 | Phone | Male | 3 |

| Frontline staff | FRT4 | Face-to-face | Female | 4 |

| Frontline staff | FRT5 | Phone | Female | 4 |

| Frontline staff | FRT6 | Face-to-face | Male | 9 |

| Frontline staff | FRT7 | Face-to-face | Male | 5 |

Appendix 2 Interview questions

The following questions are designed for members of the director subculture. Manager and frontline staff interview questions are similar but adjusted to ensure relevance.

Director interview questions

| Director subculture | Hello (introduction) |

| Thank you for your cooperation and assistance … | |

| Make sure the participant understands the nature of research and the interview process – any questions? | |

| Start recording | |

| Collect basic demographic data | |

| Name: | |

| Gender: | |

| Best contact: | |

| Organisation name: | |

| Length of time in organisation (current role): | |

| What is your current role? | |

| Other roles within this organisation: | |

| Qualifications: | |

| Who are the people you work most closely (their roles)? | |

| Description of the people you work with as whole? | |

| Diversity of the board (board mix): | |

| Location: | |

| Date | |

| Consent | Written consent from a signed document OR |

| Verbal consent provided over the phone/MS Teams recorded: | |

| On _________[date] at ________ [time], _______________________ [participant] read/had read to him/her the participant information/verbal consent script, confirming they understood the nature of the research and their participation, and agreed to proceed with the interview. | |

| Time | 30–120 minutes |

| General dialogue open-ended questions (Smith, 1987; Yin, 2017) | Response |

| Introduction | |

| |

| Research | |

| |

| Policy | |

| |

| Evaluation | |

| |

| Directors | |

| |

| Evaluation questions | |

| |

| THANK YOU | |

Appendix 3

Post-interview embedding mechanism prompt sheet

| Mechanisms | Field notes |

|---|---|

| Primary embedding mechanisms (assumptions) | |

| What are directors paying attention to, measuring and controlling on a regular basis? | |

| How do directors allocate resources? | |

| What deliberate role modelling, teaching or coaching is taking place? | |

| How are directors allocating rewards and status? | |

| How are directors recruiting, selecting, promoting and excommunicating? | |

| Secondary reinforcement and stabilising mechanisms (espoused values and artifacts) | |

| Type of organisation design and structure: | |

| Type of organisation systems and procedures: | |

| Rites of the organisation: | |

| Design of physical space (e.g. buildings): | |

| Stories about important events and people: | |

| Formal statements of organisational philosophy, creeds and charters: | |

| Defensive mechanisms | |

| Circle and describe evidence of: | |

|