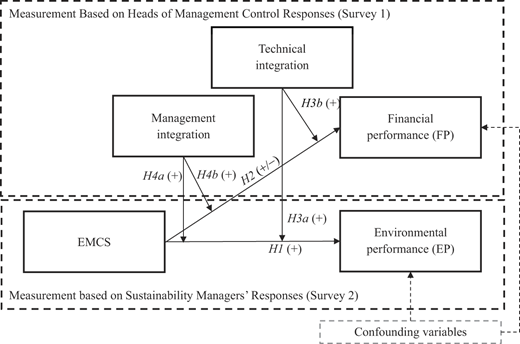

This study investigates the integration of environmental management control systems (EMCSs) into core business activities and its implication for environmental performance (EP) and financial performance (FP). Prior research highlights the potential benefits of EMCSs but often overlooks integration dimensions and their role in organizational change. This study aims to address these gaps by differentiating the technical and management dimensions of integration in a cross-sectional context.

This study employs a dyadic survey of 112 large German firms to empirically assess the influence of different dimensions on the relationship between EMCSs and performance. Using partial least squares structural equation modeling, we test whether management and technical integration moderate the effectiveness of EMCSs in improving EP and FP.

The results indicate that integrated EMCSs are associated with improvements in both EP and FP, though the impact varies based on the type of integration. Management integration strengthens the positive link between EMCSs and EP, whereas the positive relationship between EMCSs and FP is contingent upon high levels of technical integration. These findings indicate the conditions under which a win–win scenario for EP and FP may emerge.

This study distinguishes technical and management integration as contingencies in the EMCS–performance relationship and interprets them as deliberate change activities that enable organizational change. The findings suggest that integration can support both performance improvement and organizational transformation tendencies, refining contingency theory and offering managers guidance on embedding sustainability while balancing environmental and financial goals.

1. Introduction

Companies often consider environmental issues as strictly the environment department’s job and not as an inherent part of every employee’s job (Albertini, 2013, p. 447).

Rising demands from sustainability reporting (KPMG, 2024), stakeholder expectations (Schaltegger et al., 2019), and strategic renewal initiatives (Crutzen and Herzig, 2013) are requiring firms to embed environmental concerns into their core activities. Management control systems (MCSs) have emerged as crucial facilitators of this transformative process (Beusch et al., 2022; Lisi, 2015; Riccaboni and Leone, 2010), particularly through the integration of environmental management control systems (EMCSs) into broader management control structures. Recent research has suggested that the transformative potential of MCSs is not context-neutral but rather depends on its alignment with sustainability priorities, as traditional financially oriented MCSs may even marginalize sustainability by constraining rather than promoting organizational change (see Narayanan and Boyce, 2019). This underscores the need to examine how integration of EMCSs and MCSs shapes both performance outcomes and transformation processes.

Prior studies have examined and confirmed the benefits of integrating EMCSs into core business activities to improve different types of performance, but they often remain conceptual (Gond et al., 2012), focus on single cases (Beusch et al., 2022; Sundin and Brown, 2017), or treat integration as a uniform construct (Rötzel et al., 2019; Wagner, 2007). For instance, Wagner (2007) examined the influence of integration (such as corporate strategy integration or health and safety integration) on firm-level economic outcomes, while Rötzel et al. (2019) focused on managerial-level environmental performance without clearly disentangling the integration mechanisms. Our study builds on and advances this research by empirically distinguishing between two dimensions: technical integration, the linkage of environmental and financial data through common calculability infrastructures; and management integration, the organizational and cognitive embedding of environmental concerns into everyday business practices and decision-making. This distinction is inspired by Gond et al. (2012) and reflects whether firms integrate data or people.

Tipu (2022) synthesized prior research to show that integration can enable organizational change, align processes, foster cross-functional learning, engage stakeholders, and embed sustainability into the organization. In line with Stouten et al.’s (2018) notion that planned organizational change comprises deliberate efforts to move a firm from its present state toward a desired future, we consider technical and management integration to be purposeful activities highlighting different transformational pathways. Technical integration changes how organizations collect, process, and use data by linking EMCSs with MCSs for economic and environmental decision-making, bridging environmental and financial dimensions. In contrast, management integration involves shifting roles, promoting cross-functional collaboration, and fostering shared accountability across different departments (Gond et al., 2012). Both types of integration represent a move from environmental silos toward inclusive, firm-wide engagement with sustainability.

Furthermore, while the relationship between EMCSs and environmental performance (EP) has been well established in previous research (Buhr and Gray, 2012; Heggen and Sridharan, 2021; Henri and Journeault, 2010), the association between EMCSs and financial performance (FP) remains unclear. Business activities tied to EP can impact FP through revenue increases, cost reductions (Stefan and Paul, 2008), and commercial opportunities (Narayanan and Boyce, 2019), or they influence the attitudes and behavior of stakeholders (Buhr and Gray, 2012). However, neither Henri and Journeault (2010) nor Lisi (2015), in a cross-sectional setting, reported any direct associations between eco-control/environmental performance measurement system use and FP. Albertini’s (2013) meta-analysis suggested an overall positive association between environmental management and FP and emphasized the influence of moderators. However, integration has rarely been considered as such a moderator, despite its potential to explain these mixed findings (Narayanan and Boyce, 2019).

We build on this body of research by positing that the impact of EMCSs on performance is contingent on the degree and type of integration. Nonintegrated systems often lead to inconsistencies in planning (Wagner, 2007), conflicting priorities, and missed opportunities for synergies (Durden, 2008; Gond et al., 2012). The dominance of financially oriented control systems can marginalize environmental goals (Arjaliès and Mundy, 2013; Guenther and Hoppe, 2014), while lack of communication between departments and fragmented data can lead to information gaps, inhibiting effective decision-making (Bartolomeo et al., 2000; Buhr and Gray, 2012). Our study addresses these problems by showing how management integration is associated with stronger positive relationships between EMCSs and EP through cross-functional learning and how the positive association between EMCSs and FP appears contingent on high levels of technical integration, which can reduce inefficiencies and uncover cost-related environmental data. The lack of technical integration can therefore result in underperformance.

Our research contributes to the literature in three ways. First, we contribute to management control and organizational change research by conceptualizing integration as a deliberate change activity that may intentionally reconfigure technical infrastructures and managerial routines to bring sustainability and core business processes into alignment, thereby functioning as a potential mechanism of organizational transformation (e.g., Stouten et al., 2018; Tipu, 2022). Building on prior studies on integration (Gond et al., 2012; Rötzel et al., 2019; Wagner, 2007), we distinguish between technical integration and management integration and examine their moderating roles in the relationship between EMCSs and performance using a dyadic sample of 112 large German firms. Second, we contribute to the management control literature by showing how these two integration types relate to distinct mechanisms that may contribute to a win–win scenario for both EP and FP (Bartolomeo et al., 2000; Hart, 1995; Porter and van der Linde, 1995). Our results highlight the role of integrated systems in uncovering hidden efficiencies and strategic opportunities, building on prior theoretical arguments (Bartolomeo et al., 2000; Buhr and Gray, 2012). Technical integration enhances the calculability and visibility of environmental costs and benefits, whereas management integration embeds sustainability into managerial routines and responsibilities. In contrast to Henri and Journeault (2010), who examined eco-control systems in isolation, we show that specific integration types moderate the EMCS–performance relationship, thereby offering a more precise explanation of prior mixed findings. Third, we refine contingency theory by showing that the EMCS–performance link depends on integration type, introducing technical and management integration as distinct contextual variables. This more granular view of fit reveals how different types of integration align with specific performance goals, extending the theory’s relevance for both financial and environmental outcomes. Together, these contributions advance the literature on management control and organizational change by interpreting the integration of EMCSs into organizations’ MCSs as an enabling process that support both performance and transformation. In addition, this study offers practitioners actionable guidance on tailoring integration efforts to strategic priorities.

This paper proceeds as follows: Section 2 outlines the theoretical framework and hypotheses. Section 3 describes the research design and data. Section 4 presents the empirical results, followed by a discussion in Section 5. Section 6 concludes.

2. Theory and hypothesis development

2.1 Theoretical foundation and underlying concepts

2.1.1 Environmental management control systems.

Contingency-based research views MCSs as tools to help managers and employees achieve organizational goals by aligning systems with contextual factors such as strategy, structure, and environmental uncertainty (Chenhall, 2003; Otley, 2016; Rötzel et al., 2019). Simons (1995, p. 5) defines MCSs as “formal, information-based routines and procedures managers use to maintain or alter patterns in organizational activities.” Traditionally, MCSs have pursued primarily financial goals (Gond et al., 2012). EMCSs apply this concept specifically to environmental goals by integrating environmental and financial information into management processes (Buhr and Gray, 2012; Henri and Journeault, 2010; Sundin and Brown, 2017). EMCSs transform organizations and help integrate environmental matters into day-to-day business so that EP can be considered a priority alongside FP (Albertini, 2013).

Following Simons’ (1995) levers-of-control framework, EMCSs consist of the following:

belief systems, which embed (environmental) sustainability into core values and motivate innovation (Narayanan and Boyce, 2019; Simons, 1995);

boundary systems, which define acceptable environmental behavior and mitigate risk (Arjaliès and Mundy, 2013; Henri and Journeault, 2018);

diagnostic control systems, which monitor environmental KPIs and identify deviations from targets (Narayanan and Boyce, 2019); and

interactive control systems, which engage managers in strategic dialogue about environmental uncertainties and adaptation (Narayanan and Boyce, 2019; Simons, 1995).

A balanced use of these levers is critical for strategy implementation (Arjaliès and Mundy, 2013; Simons, 1995; Widener, 2007).

2.1.2 Environmental performance.

EP can be defined in various ways, mostly considering environmental impacts through the operational processes of organizations (Henri and Journeault, 2010; Lisi, 2015). Following Trumpp et al. (2015), we conceptualize EP as environmental operational performance – focusing on the direct results of organizational activities aimed at minimizing environmental harm (resulting, e.g. from the use of EMCSs), such as reductions in energy and water consumption, emissions of CO2, and (hazardous) waste produced.

2.1.3 Financial performance.

FP is broadly understood as a firm’s profitability (Albertini, 2013). In our study, we follow Hamann et al. (2013) and define FP by using accounting measures, [1] specifically returns on sales and assets, as well as cash flow returns on both. These accounting measures are chosen because they reflect management’s allocation of funds and its decision-making intentions rather than external capital market reactions to the entire organization (Albertini, 2013).

2.1.4 Integration.

In prior research, integration has been conceptualized and examined in various ways. Henri and Journeault (2010) described the use of eco-control as integrating environmental issues into strategic planning, while Wagner (2015) emphasized aligning environmental and other objectives to minimize conflict between them. We extend this thinking by defining integration between EMCSs and the overarching MCS as not only coordinating control systems across different dimensions but also facilitating broader changes in systems, roles, and routines. Building on Gond et al.’s (2012) conceptualization, which addresses technical, organizational, and cognitive integration, we propose a methodological refinement that translates these abstract dimensions into analytically distinct yet practically applicable integration constructs: technical and management integration.

Technical integration refers to the integration of a general MCS with activities and systems related to an EMCS. This integration involves creating methodological links, for example, through a common calculability infrastructure between the two systems to ensure the comprehensive collection of economic and environmental data (Gond et al., 2012), enabling informed decision-making and accountability (Sundin and Brown, 2017). Firms can foster technical integration when they migrate toward an IT/ERP system that supports the sharing of data from different systems as opposed to one that cannot process sustainability data (Gond et al., 2012). One possible approach could incorporate both financial and environmental metrics in performance measurement and strategic planning, resulting in systemic changes in how firms collect, process, and use data (Beusch et al., 2022).

In Gond et al.’s (2012) framework, organizational and cognitive integration are treated as separate dimensions. However, we argue that in practice, these two types of integration are deeply intertwined. Cognitive integration, defined as the development of shared understandings and frames of reference (Gond et al., 2012), is rarely achieved independently of the formal organizational structures and routines that foster collaboration. Moreover, individuals are unlikely to adopt sustainable practices that contradict their cognitive frames; conversely, organizational routines are unlikely to be adopted unless they resonate with or actively shape cognitive frames. In short, cognitive and organizational integration are co-constitutive. Therefore, from a methodological and operational perspective, we treat them as a single construct: management integration. This dimension captures the organizational mechanisms, routines, and structures that not only coordinate environmental sustainability-related activities but also enable cognitive alignment among actors, e.g. through similar practices between controllers and sustainability managers regarding reporting and management control and/or through communication to gain a similar mindset regarding environmental issues (Gond et al., 2012) or by providing a cognitive framework whereby environmental concerns are present for management (Sundin and Brown, 2017). Thus, management integration provokes role shifts, as all managers in the company (rather than a group of environmental specialists) share the responsibility for sustainability, expanding traditional boundaries (Beusch et al., 2022).

Planned organizational change refers to the deliberate efforts of managers to move their organization from its status quo to a more desirable future state (Stouten et al., 2018). From this perspective, technical and management integration can be considered as such deliberate change activities as both reflect transformational processes occurring in roles, routines, and systems. Technical integration reconfigures data infrastructures and decision-making logics, embedding environmental concerns into calculative practices. Management integration, in turn, shifts professional boundaries, fosters dialogical learning between accountants and sustainability experts, and enables shared routines and cognitive alignment. Together, these mechanisms facilitate organizational change by embedding environmental sustainability into operations and distributing responsibility from environmental specialists toward firm-wide accountability.

Tension can arise between the integration of data (i.e. technical integration) and the integration of people (i.e. management integration), as each dimension operates on distinct principles. While previous studies have often treated integration as a single, aggregated concept (e.g., Gond et al., 2012; Rötzel et al., 2019; Wagner, 2015), we argue that technical and management integration follow different operational logics and should therefore be examined separately. This conceptual distinction enables a more targeted analysis of how different integration mechanisms influence EP and FP.

2.1.5 Contingency theory.

We employ contingency theory to describe how the integration of EMCSs into core activities helps not only address environmental concerns for better EP but also align these issues with broader (financial) organizational goals. Therefore, we follow the reasoning of Gerdin and Greve (2004) and consider that firms are not at their optimum in terms of fit with context and that there is room for improvement in their performance. Thus, we explore technical and management integration as potential moderators (following Gerdin and Greve, 2004) to examine variations in the EMCS–performance relationships and thus explain that there are high- and low-performing firms resulting from a “more or less successful combination of context and structure” (p. 307). We also examine a dual-goal setting, which is likely to occur in companies.

2.2 Relationship between EMCSs and EP

EMCSs employ bonding and monitoring mechanisms to translate environmental concerns into actual organizational behavior (Sundin and Brown, 2017). They support decision-making, facilitate internal communication, and foster dialogue by providing financial and environmental data (Buhr and Gray, 2012; Henri and Journeault, 2018, 2010). When formally embedded, EMCSs actively utilize resources, direct the organization’s focus (Buhr and Gray, 2012), and motivate continuous improvement for effective resource management (Henri and Journeault, 2010).

Each EMCS lever supports EP differently. Belief and boundary systems communicate core values and set behavioral limits, aligning employee actions with environmental goals (Henri and Journeault, 2018; Simons, 1995). Diagnostic control instruments quantify the environmental actions to be managed and monitored against set targets (Arjaliès and Mundy, 2013) and adjust actions when deviations occur (Simons, 1995). This adjustment encourages feedback and organizational learning (Henri and Journeault, 2010). Interactive control systems promote dialogue and help adapt strategies in response to uncertainties (Simons, 1995), encouraging both single- and double-loop learning, which strengthens decision-making and environmental responsiveness (Henri and Journeault, 2010). EMCSs also stimulate prevention at the source through material substitution and the minimization of resource use and waste by optimizing (manufacturing) processes and recycling (Henri and Journeault, 2018). These mechanisms reduce negative environmental impacts and increase EP. From a natural resource-based view, EMCSs contribute to developing capabilities that improve EP (Hart, 1995; Journeault, 2016).

Empirical studies reinforce this relationship. Henri and Journeault (2018) reported that eco-control leads to improved EP, while earlier work (Henri and Journeault, 2010; Journeault, 2016) linked eco-control to EP through enhanced environmental capabilities. Lisi (2015) emphasized the role of environmental performance measurement systems, and Heggen and Sridharan (2021) showed that interactive eco-control and diagnostic eco-control positively affect EP, in the case of the latter, particularly under enabling conditions. Even partial implementation, such as eco-efficiency-focused EMCSs, can yield EP improvements (Buhr and Gray, 2012).

In conclusion, by motivating and uniting employees around a shared environmental vision, focusing their attention on environmental concerns, and setting clear measurable targets to be met and limits to avoid hazardous behavior, EMCSs can help a firm achieve better EP:

The use of EMCSs is positively associated with the level of EP.

2.3 Relationship between EMCSs and FP

Theoretical insights and empirical research suggest that EMCSs may contribute not only to improved EP but also to enhanced FP, creating a potential win–win scenario. EMCSs can improve resource management and detect cost savings potential, thereby positively affecting FP (Ferreira et al., 2010; Henri and Journeault, 2010). When pollution is treated as resource inefficiency (Porter and van der Linde, 1995), addressing environmental issues at the source can yield financial benefits (Henri and Journeault, 2008). EMCSs may also support pricing and enhance revenue, improve reputation, and develop capabilities to generate competitive advantages, thereby increasing FP (Ferreira et al., 2010; Hart, 1995; Henri, 2006; Henri and Journeault, 2018).

However, regarding the negative association between EMCSs and FP, trade-offs are brought to the forefront (e.g. Guenther and Hoppe, 2014), implying that managers perceive the high costs of environmental activities (Henri and Journeault, 2008), formal EMCSs consume resources that are missing for other investments (Buhr and Gray, 2012), incentives are dominated by financial goals instead of environmental goals (Arjaliès and Mundy, 2013; Sundin and Brown, 2017), elevated production costs are incurred when they are transferred to more sustainable processes (Klassen and Whybark, 1999), and more expenses are incurred for pollution control with increased regulation (Bartolomeo et al., 2000). In addition, unintegrated EMCSs might add complexity to existing systems and make them difficult to understand because of the large amount of information, incongruent goals, and increased administrative costs, resulting in a negative association with FP (Henri and Journeault, 2010; Ittner et al., 2003).

The empirical results are mixed. Henri and Journeault (2010), Henri et al. (2014) and Lisi (2015) reported no direct relationship between control systems and FP. The results of Albertini’s (2013) meta-analysis indicated that the relationship between EMCSs and FP is positive but contingent on several moderators, such as regional differences and the research design. Given the mixed theoretical and empirical evidence, we propose the following undirected hypothesis:

The use of EMCSs is associated with the level of FP.

2.4 Integration of EMCSs into the general MCS of a firm

Integrating environmental concerns into core business activities is essential, as sustainability cannot be separated from overall corporate strategy (Arjaliès and Mundy, 2013; Gond et al., 2012). Therefore, researchers have delved into the conceptual (Gond et al., 2012) and empirical (Henri and Journeault, 2010; Judge and Douglas, 1998; Rötzel et al., 2019; Wagner, 2015, 2007) aspects of integrating environmental concerns into the core activities of a firm, guided by general MCSs. While many firms continue to prioritize financial control (Narayanan and Boyce, 2019), studies have shown that integration can help balance environmental and financial goals. For instance, Judge and Douglas (1998) and Henri and Journeault (2010) reported that incorporating environmental issues into strategic planning enhances both EP and FP. Other research has demonstrated that integration – whether through linking environmental and “regular” control systems (Rötzel et al., 2019) or by aligning environmental management with broader functions such as quality or safety (Wagner, 2007) – strengthens firm performance. However, integration is often treated as a uniform or abstract concept, or granularity in terms of how this integration unfolds within organizations is lacking.

Recent work by Narayanan and Boyce (2019) posits that MCSs in themselves may not be transformational, as they often marginalize sustainability in favor of traditional financial priorities. This underscores the importance of understanding integration as change activity. In line with organizational change perspectives (Stouten et al., 2018; Tipu, 2022), we argue that integration should be viewed as a deliberate change activity for reconfiguring systems, roles, and routines. Technical integration reflects changes in data infrastructures and decision-making logics, whereas management integration reflects shifts in professional boundaries and shared cognition. Both represent distinct pathways for organizational transformation that determine how EMCS contribute to performance outcomes.

EMCSs are designed primarily to support EP, yet their effects on FP are less clear and may even conflict with short-term financial goals (Durden, 2008; Sundin and Brown, 2017). This potential trade-off highlights the need for integration mechanisms that reconcile environmental and financial logics (Arjaliès and Mundy, 2013; Henri and Journeault, 2018; Sundin and Brown, 2017). Firms require more nuanced integration mechanisms that align data, practices, and people. Therefore, integration must go beyond structural alignment to include both technical systems and managerial processes, with each offering distinct pathways to organizational transformation and performance gains.

Technical integration enhances EP by embedding environmental data into core decision-making systems through the incorporation of performance indicators (Buhr and Gray, 2012; Henri et al., 2017). It facilitates the tracking and monitoring of pollution, energy, and material flows, allowing firms to identify and address environmental inefficiencies (Bartolomeo et al., 2000; Henri et al., 2017). Through a shared calculability infrastructure (Gond et al., 2012), firms can explicitly incorporate environmental indicators into their MCSs, ensuring that these concerns are visible and consistently considered. In contrast, when technical integration is missing and systems are not linked, the better environmental option may lose to a more favorable financial option (Buhr and Gray, 2012), as economic trade-offs are made in favor of EP if environmental activities are found to pay off (Sundin and Brown, 2017). By making environmental impacts quantifiable and manageable (Henri and Journeault, 2018), technical integration helps translate environmental goals into measurable outcomes, exploiting new opportunities (Buhr and Gray, 2012) and thus improving EP. Accordingly, we expect technical integration not only to improve environmental data use but also to act as a change mechanism that reshapes decision-making logics, thereby strengthening the EMCS–EP relationship:

Technical integration positively moderates the relationship between EMCSs and EP.

Technical integration enhances decision-making by improving the compatibility of environmental and financial data (Bartolomeo et al., 2000), enabling a more accurate identification of environment-related costs such as material costs or energy use and waste disposal that are often hidden in overheads (Buhr and Gray, 2012). This transparency supports cost-effective decisions by highlighting savings opportunities (Henri et al., 2014) and aligning environmental actions with financial logic. More concretely, pollution prevention allows companies to reduce their expenditures on pollution control, minimize input and energy consumption, and promote material reuse by recycling (Albertini, 2013; Hart, 1997). Therefore, an integrated EMCS can enhance FP directly by controlling inputs at the source (Bartolomeo et al., 2000; Henri and Journeault, 2008). Furthermore, technical integration enables more complete information and thereby links environmental action to competitive advantages or profit opportunities in new markets by integrating stakeholder perspectives through a differentiation strategy (Arjaliès and Mundy, 2013; Hart, 1995; Wagner, 2007). Thus, interdependencies or complementarities between EP and FP can be made apparent, thereby revealing where there is potential for reducing inefficiencies and enhancing competitive advantage. Both approaches lead to increased FP (Albertini, 2013; Guenther et al., 2016; Hart, 1995; Porter and van der Linde, 1995). By embedding environmental data into accounting systems, firms can exploit efficiency gains, reduce redundancy in data collection, and reuse information across departments (Bartolomeo et al., 2000), thereby saving resources and improving FP. Similarly, we expect technical integration to not only improve transparency in environmental costs but also to function as a change mechanism that embeds sustainability into financial decision-making, thereby strengthening the EMCS–FP relationship:

Technical integration positively moderates the relationship between EMCSs and FP.

Management integration fosters shared responsibility for sustainability across departments and hierarchical levels, avoiding the isolation of environmental concerns within a specialized unit (Beusch et al., 2022) and signaling goal prioritization by top management (Rötzel et al., 2019). Through ongoing dialogues and inclusive practices, managers gradually adopt new sustainability-related roles, aligning environmental objectives with daily operations (Beusch et al., 2022). This collaborative approach builds mutual understanding and good relationships, and it encourages environmental awareness among accounting staff and financial literacy among environmental managers, avoiding siloed goals and perspectives (Bartolomeo et al., 2000; Buhr and Gray, 2012). Such mutual learning fosters tacit knowledge and empowers employees to find innovative ways to reduce pollution and improve processes (Albertini, 2013; Hart, 1995). Standardized practices such as shared reporting and communication routines (Gond et al., 2012) reduce unacceptable behavior, strengthen commitment to environmental goals (Arjaliès and Mundy, 2013), and develop environmental capabilities that improve EP (Henri and Journeault, 2018). These mechanisms support an organizational culture in which EP becomes part of everyday thinking and acting (Albertini, 2013; Beusch et al., 2022). Accordingly, because it functions as a mechanism of organizational change that enhances the EMCS–EP relationship, we expect management integration to foster roles shifts and shared responsibilities:

Management integration positively moderates the relationship between EMCSs and EP.

Management integration also improves the relationship between EMCSs and FP. There are cases in which win–win opportunities are not directly apparent because the costs of environmental activities appear to exceed the savings gained from them (Buhr and Gray, 2012) or because lucrative opportunities are missed owing to poor communication (Bartolomeo et al., 2000). When environmental management does not provide links to other management systems regarding organizational structures or processes, redundancies emerge, which are not economically efficient (Sharma and Henriques, 2005; Wagner, 2015) and require greater coordination efforts, leading to conflicting goals regarding environmental and financial objectives (Wagner, 2007). Therefore, the management integration of EMCSs and the consequent reduction in processual inefficiencies and effective resource management (Henri and Journeault, 2018) should be economically profitable, leading to improved FP. Similarly, we expect management integration to reconfigure routines and collaboration patterns across functions, operating as a mechanism of organizational change that aligns sustainability with financial priorities, thereby enhancing the EMCS–FP relationship:

Management integration positively moderates the relationship between EMCSs and FP.

Our conceptual model is shown in Figure 1.

3. Research design and method

3.1 Data collection and sample

We applied the tailored design method of Dillman et al. (2014) to administer two questionnaires: one on MCSs and FP (Survey 1) sent to heads of management control and another on EMCSs and EP (Survey 2) distributed to environmental or sustainability managers. Recipients were identified through phone calls, and both surveys were pretested with 12 academics and practitioners to ensure clarity and face validity.

Survey 1 measured technical integration, management integration, and FP, whereas Survey 2 addressed EMCSs and EP. Data were collected from the 3,000 largest German firms (based on net sales) listed in the Amadeus database between February 2015 and February 2016. The sample includes private firms (both listed and not listed, according to the structure of the population of German firms) in production, trade, and services but excludes financial institutions, nonprofits, and subsidiaries. Large firms were targeted due to their more developed MCSs (Janka and Guenther, 2018; Widener, 2004) and heightened environmental awareness (Chang and Chen, 2013).

We received 260 useable responses for survey 1 (response rate 11.9%) and 301 for survey 2 (13.8%), with 112 overlapping responses used as our final dyadic sample (5.1%). [2] Despite declining response rates in recent management accounting research (Hiebl and Richter, 2018), our rates compare favorably with those of similar studies (Pondeville et al., 2013; Rötzel et al., 2019). The characteristics of the respondents are presented in Table 1. Panel A shows a balanced industry distribution with no significant differences between the target sample and our study sample (in unreported results). Panel B highlights that over 85% (Survey 1) and 80% (Survey 2) of the respondents were senior executives (e.g. heads of controlling or sustainability). The respondents had an average tenure of 9.3 years (survey 1) and 10.7 years (survey 2) in their current roles and over 13 years (survey 1) and 15 years (survey 2) with the firm, indicating strong familiarity with internal systems. We tested for sample selection bias (Armstrong and Overton, 1977). Panel C shows no significant differences in return on assets or sales growth between respondents and nonrespondents, although respondents worked in slightly larger firms, which aligns with our sampling criteria. The percentage of item-level missing data did not exceed 4.5%, which is well below the 10% threshold. Panel D indicates no significant differences between early and late respondents, supporting generalizability [3].

To mitigate common method bias (CMB), we used a dyadic design, collected data from different roles, guaranteed anonymity, and employed neutral wording. The questionnaire formatting included encoded section headers and mixed question blocks to reduce priming. Harman’s single-factor test (Podsakoff et al., 2003) suggested that CMB is not a major concern, with the first factor explaining only 27.65% of the variance.

3.2 Measurement of constructs

We used established survey instruments drawn from prior research to measure the study constructs. All data were collected by asking respondents to answer each question with respect to the preceding three years (i.e. 2012–2014). EP and FP were perceptually assessed, and respondents were asked to rate their firm’s performance relative to industry averages. EP was measured via five indicators: energy consumption, water withdrawal, CO2 emissions, total waste, and hazardous waste (Trumpp et al., 2015). FP was assessed using return and liquidity dimensions, including return on sales, cash flow return on sales, return on assets, and cash flow return on assets (Hamann et al., 2013).

EMCSs were modeled as a formative second-order construct using the repeated-indicators approach (Sarstedt et al., 2019), with four reflectively measured first-order constructs aligned with Simons’ (1995) levers of control. Diagnostic control systems were measured by four items [4] adapted from Goebel and Weißenberger (2017), capturing environmental goal setting, monitoring, accountability, and feedback. Interactive control systems were measured via three items (Widener, 2007) assessing top management team members’ attention to and interpretation of environmental performance data and operating managers’ involvement in the environmental performance measurement process. Belief systems were measured using four items (Widener, 2007) concerning the communication and motivational role of environmental core values. Boundary systems captured the use of codes of conduct, environmental policies, and risk-avoidance standards, with four items from Widener (2007). All constructs were adapted to the environmental setting.

Technical and management integration were newly developed based on Gond et al. (2012). Technical integration (three items) referred to using shared ERP and control systems for environmental and financial data, whereas management integration (six items) involved collaboration and shared understanding between environmental specialists and management accountants. The wording of the items is displayed in Table A in the Online Appendix of this paper. Descriptive statistics (Table A, Supplementary material) revealed a wide range of integration levels across firms, supporting the application of contingency theory (Gerdin and Greve, 2004).

The indicator reliability of the measurements was evaluated (Table A, Supplementary material) via factor loadings exceeding 0.7. Cronbach’s alpha and composite reliability surpassed the threshold of 0.7, indicating robust internal consistency. The average variance extracted (AVE) exceeded 0.5, indicating strong convergent validity (Hair et al., 2022). Discriminant validity was supported via HTMT ratios below 0.85 (Henseler et al., 2015) and low interconstruct correlations (Table 2).

For the formative EMCS construct, the variance inflation factors (VIFs) were less than 3, suggesting that there was no multicollinearity. The significance and relevance of individual levers were confirmed (Hair et al., 2022; see Table 3).

To address potential endogeneity, we included several confounding variables known to influence EP and FP (Chenhall, 2003; Heggen and Sridharan, 2021; Henri and Journeault, 2010; Lisi, 2015; Wagner, 2015). These included organizational size (measured via log-transformed three-year averages of total employees, sales, and assets), organizational maturity (since incorporation), industry (dummy for manufacturing and other), the existence of a certified environmental management system (i.e. ISO 14001), and environmental reports. These factors were derived from either Amadeus data or the survey responses.

3.3 Data analysis

To assess the conceptual model, we used partial least squares structural equation modeling via SmartPLS version 4 (Ringle et al., 2022). This variance-based method was chosen because it is suitable for handling complex models with multiple dependent variables and moderators, small sample sizes, and nonnormal data, which are common with Likert-scale responses (Hair et al., 2014). We applied bootstrapping with 5,000 subsamples to assess significance (Henseler et al., 2012). One-tailed tests were used for the directional hypotheses, whereas two-tailed tests were used to assess the undirected hypothesis and confounding variables.

4. Results

The results are presented in Table 4, Panel A. In Model 1, H1 is supported, as EMCSs have a positive association with EP (β = 0.175, p < 0.05). Conversely, there is no significant relationship between EMCSs and FP, and H2 is not supported (β = 0.070, p > 0.1). Model 2 examines the moderating effects. H4a is supported, as management integration positively moderates the EMCS−EP relationship (β = 0.200, p < 0.05), whereas H3a lacks support (β = −0.154, p > 0.1). We conclude that higher levels of management integration appear to strengthen the positive association between the use of EMCSs and EP, which is consistent with contingency theory, where fit is indicated when the moderating effect is statistically significant (Gerdin and Greve, 2004).

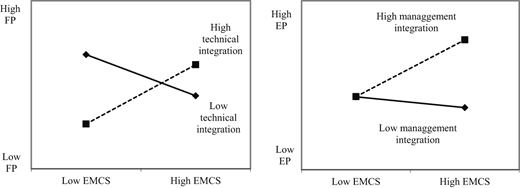

H4b is not supported (β = −0.132, p > 0.1), whereas technical integration shows a positive interaction effect with EMCSs (β = 0.299, p < 0.05) on FP, supporting H3b.

To evaluate H3b, we examine the conditional effects outlined in Panel B (Table 4) across seven values of technical integration (from −3 to +3 standard deviations (SDs)). This assessment is necessary to show the significant positive moderating effect on the EMCS−FP relationship in light of the rejection of H2. The conditional effects show that at higher levels of technical integration (+1 SD or more), EMCSs are positively and significantly associated with FP. At average or low levels (0 or −1/−2 SDs), the relationship remains nonsignificant. At −3 SDs, the relationship becomes significantly negative. Thus, the significance of EMCSs for FP appears contingent upon the level of technical integration. Both significant moderating effects (H3b, H4a) are visualized via simple slope analysis in Figure 2.

Confounding variables play a minor role. Firm maturity is positively linked to FP, suggesting that older firms tend to benefit from more developed control systems and resource availability (Guenther and Hoppe, 2014). The existence of an environmental report is positively associated with EP, likely by enhancing sustainability practices (Arnold and Hockerts, 2011).

Effect sizes demonstrate the individual contribution of each moderating effect by indicating changes in the coefficient of determination (R2) when the moderation terms are excluded from the model (Hair et al., 2022). Panel C (Table 4) shows effect sizes for EP (f2 = 0.028) and FP (f2 = 0.063) for the inclusion of both technical and management integration. In particular, the contribution of management integration as a moderator of the EMCS–EP relationship represents a medium effect size (>0.01), whereas the contribution of technical integration to the relationship between EMCSs and FP constitutes a large effect size (>0.025) (see Aguinis et al., 2005; Hair et al., 2022; Kenny, 2018). These findings highlight not only the statistical significance but also the practical relevance of the moderators in explaining performance outcomes.

Robustness checks, including an alternative EMCS specification as a reflective-reflective second-order construct and analyses at the disaggregated first-order level (beliefs, boundaries, diagnostic, and interactive control systems), confirm that our main moderation results are stable (see supplementary material for full results).

5. Discussion

5.1 Theoretical implications

Our findings show that EMCS use is positively associated with EP, regardless of integration (supporting H1), thereby aligning with the findings of previous studies (Henri and Journeault, 2010; Lisi, 2015). In addition, higher levels of management integration between environmental specialists and management accountants strengthen this relationship (supporting H4a). This integration fosters knowledge sharing and an environmental mindset across functions, overcoming cognitive barriers tied to financial perspectives (Gond et al., 2012) and ensuring recognition of environmental issues (Sundin and Brown, 2017). It facilitates iterative adjustments in routines and responsibilities and builds commitment around environmental matters through dialogue, embedding them into everyday managerial practice (Beusch et al., 2022). Therefore, management integration appears to support roles shifts, distributing environmental responsibilities across managerial functions and aligning different perspectives toward common environmental goals, which may signal early organizational adaptation. From an organizational change perspective, these findings suggest that management integration functions as an inferred initiated cultural transformation that embeds environmental sustainability into collective cognition and managerial routines.

Our results suggest that management integration may be ethically driven, aiming for pollution reduction and environmental leadership beyond financial returns (Bansal and Roth, 2000; Henri et al., 2014). These findings extend the results obtained by Rötzel et al. (2019) by demonstrating that management integration enhances EP at the firm level. We also expand the insights of Sundin and Brown (2017) and Arjaliès and Mundy (2013) in case studies for a cross-sectional sample, reinforcing the role of (E)MCSs and corporate-level integration in environmental decision-making.

In contrast, the EMCS−FP relationship was not significant (rejecting H2), indicating that this association might be conditional on contextual factors (Albertini, 2013; Gerdin and Greve, 2004). Our results identify technical integration as a contingency (supporting H3b). Higher levels of technical integration yield a significant positive association between EMCSs and FP. Conversely, very low or nonexistent technical integration demonstrates a negative association. Although control practices for resource efficiency may intuitively increase FP, their costs and benefits often remain unclear without technical integration. Technical integration makes inefficiencies visible by assigning costs to specific objects via shared ERP or IT systems (Bartolomeo et al., 2000). It embeds sustainability metrics into widely used control systems, distributing responsibilities and provoking role shifts as managers beyond the environmental department engage with sustainability issues (Beusch et al., 2022). These findings indicate how technical integration reflects a deliberately initiated structural transformation for organizational change, reconfiguring calculability infrastructures and decision-making processes to bring environmental and financial objectives into alignment. By embedding environmental data into shared systems, firms can potentially transform their control systems from financially dominant tools into systems for enabling cost visibility, efficiency gains, and strategic alignment.

This lack of a uniform EMCS–FP relationship does not imply the complete absence of a link; rather, it suggests that this relationship is conditional on the level of technical integration. Consistent with contingency theory, our findings indicate that the relationship between EMCS and FP becomes positive only under high technical integration, whereas a low level or complete lack of integration can even reverse this association. This helps reconcile prior mixed results (e.g. Albertini, 2013; Henri and Journeault, 2010) and highlights that H2 should be interpreted together with H3b as part of a broader framework rather than in isolation.

Our results imply that technical integration might be economically driven, as firms aim for production cost reductions to increase revenues and profits (Bansal and Roth, 2000; Henri et al., 2014), emphasizing the cost–benefits of environmental actions, i.e. eco-efficiency (Gond et al., 2012; Virtanen et al., 2013). Moreover, the results align with those of Wilmshurst and Frost (2001) and Henri et al. (2014), who stated that the integration of environmental issues into MCSs supports cost–benefit analyses and cost tracing. We complement and extend the research by Henri and Journeault (2010) by demonstrating that the absence of a direct EMCS–FP link can be explained by the moderating role of technical integration on the basis of contingency research.

Full integration across both dimensions (technical and management) improves data quality, reduces redundancy, and enhances interdepartmental collaboration, supporting value alignment and informed decision-making based on a complete picture of firm performance. This finding reveals that the performance implications of EMCSs vary by the level and type of integration, demonstrating that a one-size-fits-all approach fails to capture the complexity of real-world organizational challenges. Therefore, it is necessary for environmental concerns to be seen not merely as the responsibility of the environment department but as an integral part of every employee’s role within the organization (Albertini, 2013). By showing how technical and management integration correlate with organizational patterns typically associated with transformation, our findings complement Narayanan and Boyce (2019), who found that MCSs may not lead to organizational change per se. When embedded organization-wide, environmental concerns become integral to decision-making across functions, supporting dual performance goals. Table 5 summarizes how our distinction between technical and management integration provides a refined theoretical lens, clarifying their distinct mechanisms and differing effects on performance.

Our study contributes to the literature in three ways. First, we contribute to the management control and organizational change research by conceptualizing integration as a deliberate change activity that can reconfigure technical infrastructures and managerial routines to align sustainability with core business processes, and thus may function as a mechanism supporting organizational transformation (Stouten et al., 2018; Tipu, 2022). Prior evidence has suggested that traditional control systems may not be transformational when misaligned with sustainability priorities (Narayanan and Boyce, 2019). By distinguishing between technical and management integrating, we propose that integrated EMCSs can help overcome this limitation: technical integration appears to reshape data infrastructures and decision-making logics, while management integration is associated with shifts in roles, routines, and shared cognition. This dual perspective – the integration of data (technical) versus the integration of people (management) – clarifies how integration not only affects performance but also can facilitate organizational change processes.

Second, we contribute to management control research, extending prior research on integration of EMCS with MCS (e.g. Gond et al., 2012; Rötzel et al., 2019; Wagner, 2007). The findings suggest that the two integration types yield distinct effects that together support a win–win scenario for both EP and FP (Bartolomeo et al., 2000; Hart, 1995; Porter and van der Linde, 1995). Technical integration enhances the calculability and visibility of environmental costs and benefits, making eco-efficiency opportunities explicit, whereas management integration embeds sustainability into managerial routines and responsibilities, fostering collaboration and learning. In contrast to studies that examine eco-control in isolation (e.g. Henri and Journeault, 2010), we show that integration type moderates the EMCS–performance relationship, thereby explaining prior mixed findings and empirically supporting the coexistence of multiple integration pathways within firms, as suggested by Gond et al. (2012). This tailored perspective underscores that integration along both dimensions is likely necessary to simultaneously improve EP and FP without incurring trade-offs.

Third, our study contributes to the literature on contingency theory within the (E)MCS domain (e.g. Chenhall, 2003; Otley, 2016; Rötzel et al., 2019) by refining how contextual fit is understood. Traditional applications of contingency theory emphasize that there is no universally effective control system; rather, effectiveness depends on the alignment (or “fit”) between the control system and contextual variables (Gerdin and Greve, 2004). We extend this framework by introducing the integration type, specifically, technical and management integration, as an analytically distinct and practically relevant contingency. Our results show that while management integration strengthens the association between EMCSs and EP, technical integration is necessary for yielding FP. This differentiation adds precision to the theory by demonstrating that not only the presence but also the type of integration may matter for achieving specific performance outcomes. Moreover, by incorporating EP alongside FP, our study broadens the scope of contingency theory, aligning it with the dual performance goals that organizations increasingly face. These findings emphasize that achieving a high degree of integration is not uniformly beneficial; rather, integration must be tailored to the organizational priorities and outcomes sought. Thus, we show that nuanced, configurational interventions, matching EMCSs with the right integration mechanism, may enable more effective fit and lead to superior outcomes. In summary, we both support and extend contingency theory by positioning the integration type as a novel, process-oriented contingency that enhances the explanatory power of the theory in complex, sustainability-driven organizational settings.

5.2 Practical implications

To enhance EP, firms should integrate EMCSs into general MCSs at the management level by involving controllers and environmental specialists to share best practices and promote awareness of environmental issues. To improve FP, integration should focus on the technical dimension, establishing a shared ERP or IT system that enables consistent environmental and financial data, thereby supporting informed decision-making. Both integration types can facilitate shifts in roles and routines by embedding sustainability across functions with aligned goals, data systems, and shared responsibilities.

Importantly, our findings show that both integration types can be pursued simultaneously without compromising either EP or FP. If firms must prioritize due to limited resources, technical integration should come first, as it is essential for realizing FP improvements. In contrast, EMCSs are positively linked to EP regardless of integration level, although management integration further strengthens this effect. Thus, combining both forms of integration can boost overall performance and support a more competitive market position.

5.3 Future research and limitations

Our study opens avenues for future research on digitalization and management control. Future studies could examine how digitalization supports technical integration and explore the effectiveness of personnel training in fostering management integration, which promotes best practices, shared perceptions, and knowledge exchange around environmental issues. Longitudinal research could also shed light on the long-term effects of integration and the resulting role shifts among accountants and sustainability professionals.

As with any empirical research, our study has limitations. The sample consists of German firms, which are known for a stakeholder-oriented approach. Thus, future studies should test whether the findings hold in more shareholder-oriented contexts, such as the USA or the UK. The data that we collected for our study were self-reported by the firms in our sample. Although we ensured the reliability and validity of our data by approaching the most suitable individuals regarding management control and environmental management, ensuring the collection of data for endogenous and exogeneous variables from different respondents and trying to minimize CMB, we cannot be certain that these measures can be generalized to the entire organization. Although the observed path coefficients are modest, this likely reflects our dyadic design, which, despite reducing sample size, minimizes CMB and avoids artificially inflated relationships. Furthermore, the cross-sectional design (collecting data at a single point in time) limits causal inference and means that the organizational change processes discussed are inferred from patterns in the data rather than directly observed over time.

6. Conclusion

As sustainability continues to shape the future of economic development, our study suggests the importance of integrating EMCSs into (general) MCSs to enhance both EP and FP. By examining the technical and management dimensions of integration in a cross-sectional context (112 dyads), we show that management integration is associated with a stronger positive relationship between EMCSs and EP, whereas high levels of technical integration appear to be a condition for a positive association between EMCSs and FP. Our findings indicate the need for firms to allocate resources to the appropriate type of integration on the basis of their performance goals, thereby potentially supporting transformation and role shifts within these firms. Overall, our study proposes that integration can serve as a component of organizational change through which EMCSs may more effectively contribute to EP and FP.

Acknowledgements

This paper is part of a larger research program. The authors are grateful to Stefanie Einhorn, Jan Endrikat, Bernhard Fietz, Xaver Heinicke, Marc Janka, Takehisa Kajiwara, Hirotsugu Kitada, Katsuhiko Kokubu, Kimitaka Nishitani, Matthias Walz, and Qi Wu for their contributions to the survey design and collection of raw data for the entire research program, from which we used some variables for our study. The authors are grateful for the contributions of participants at the empirical research in management accounting and control (ERMAC) 2023 conference in Vienna, Austria, and workshop participants at Dresden University of Technology, Germany; Kobe University, Japan; and Nanyang Business School, Singapore. The authors appreciate the fruitful comments and recommendations of the editor, Zahirul Hoque, and of two anonymous reviewers.

Ethics statement

In the two surveys of this study we collected data about firms and not individuals. The data is anonymous and neither the firm nor the respondents are disclosed. Our data and study comply with all relevant guidelines and regulations for studies involving humans, whether that be data, individuals, or samples. The Institutional review board of TUD Dresden University of Technology confirmed that our study does not fall under the regulations according to § 1 para of the Statutes of the Ethics Committee of TUD Dresden University of Technology (see attached IRB statement).

Notes

Market measures such as earning per share are not applicable, as not every firm in our sample is publicly listed.

The total number of mailed questionnaires was 2,186.

Cases were classified as early responses when both surveys were sent back within the first 6 months after mailing; cases were classified as late responses when at least one questionnaire was sent back after 6 months, i.e., after follow-up.

The fifth item was removed due to a low factor loading.

References

Supplementary material

The supplementary material for this article can be found online.